financial incentives under section 1603 of the american recovery and reinvestment act of 2009 ©...

TRANSCRIPT

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

Tuesday, May 25, 2010

Presented by

Alexander M. Wixted, Esq.

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

What are the benefits for developers?

Qualifying projects are eligible for a payment in lieu of a tax credit of up to 30% of the project costs

Applicant can also pledge payment to contractor for down payment or to a bank as collateral for a loan.

In either instance, the payment is an immediate infusion of equity into the project – in the case of solar = 30%

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Background

On February 17, 2009, President Obama signed the American Recovery and Reinvestment Act of 2009 (the “Act”).

Among the purposes of the Act was to

preserve and create jobs, promote economic recovery in the near term, and to invest in infrastructure that will provide long-term benefits.

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Section 1603 Program – Payments for Specified Energy Property In Lieu of Tax Credits

Under Section 1603, the Act appropriates funds for payments relative to specified energy property that is placed in service:

- During 2009 or 2010; or

- After 2010 and before the Credit Termination Date with respect to such property, but only if the construction of such property began in 2009 or 2010.

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Summary of Key Dates

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Who is eligible? Owner or lessee of specified energy property that is the original

user of the property (i.e. originally placed it into service)

Eligible Applicants include Sole Proprietors, Joint Venturers, Partnerships, C corporations, S corporations, and REITs.

Lessees must have written consent/authorization of lessor and include same as part of application.

- Other requirements include waiver of lessor’s right to receive payment or to claim other tax credits which conflict with the Section 1603 credit.

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

“Qualified Property”?

Covered by Sections 45 and 48 of the Internal Revenue Code (“IRC”)

Only property used in a trade or business or held for the production of income is eligible for Section 1603 payments.

Personalty excluded (residential solar improvements qualify separately)

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

When is the payment made?

If the qualifying property has been placed in service at the time of the application, then the Treasury Department will make payments to the applicant within 60 days from the date the completed application is received.

If the property is not yet in service, the Treasury Department will review the application and notify the applicant of any outstanding requirements that must be met before the property is placed in service.

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

“Placed In Service” Means that the qualified property is ready and available

for its specific use.

The property need not be placed in service in order to apply, but it must be in order to be paid.

To evidence the property has been placed in service, a Commissioning Report must be provided by the project engineer, or the equipment vendor, or an independent third party that certifies that the equipment has been installed, tested, and is ready and capable of being used for its intended purpose.

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

What does all of this mean to deveolpers and lenders alike?

Equity Reliability of payment from the

Treasury Department versus borrower’s creditworthiness.

Federal Administrative oversight

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Conditions on Assignment to Lender

1. The Section 1603 payment must be $1,000 or more;

2. The assignee must be a bank, trust company or other financing institution, including any Federal lending agency;

3. The assignment covers all amounts payable and is not subject to further assignment

Exception – any assignment may be made to one party acting as agent or trustee for two or more parties who are participating in the financing

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

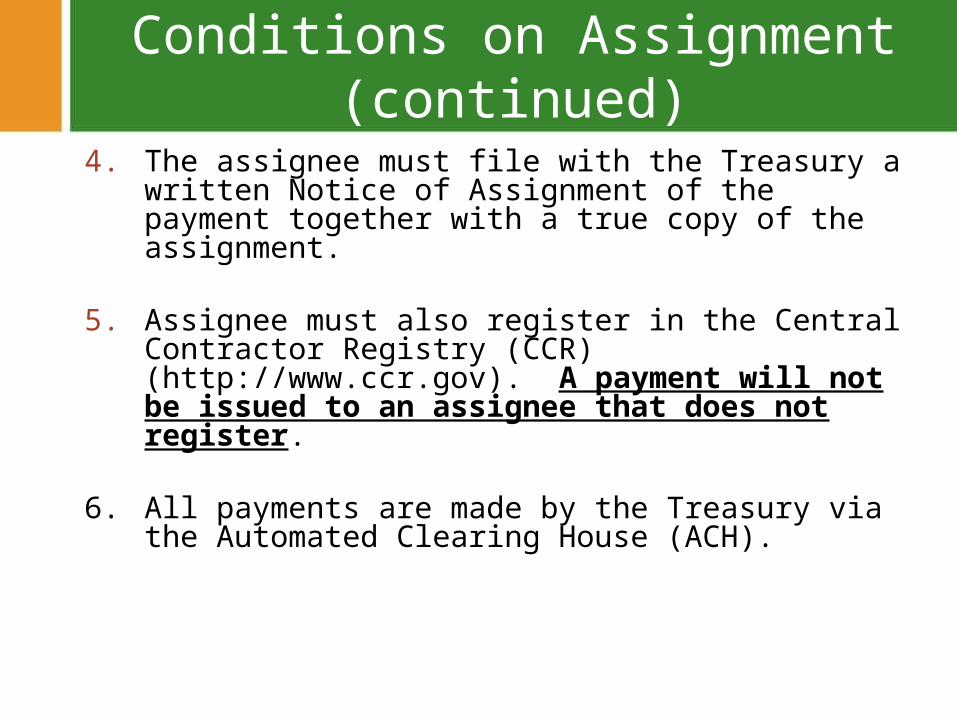

Conditions on Assignment (continued)

4. The assignee must file with the Treasury a written Notice of Assignment of the payment together with a true copy of the assignment.

5. Assignee must also register in the Central Contractor

Registry (CCR) (http://www.ccr.gov). A payment will not be issued to an assignee that does not register.

6. All payments are made by the Treasury via the Automated Clearing House (ACH).

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Sample Notice of Assignment

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Key Considerations

1. Recapture2. Basis3. Reporting Requirements4. Representations and Warranties in

Loan Documentation will likely require compliance with lender’s and Federal government’s reporting requirements.

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Recapture The IRC recapture provisions apply to Section 1603 payments.

Recapture rules are invoked if the applicant disposes of the property to a disqualified person or the property ceases to qualify as a specified energy property within five (5) years from the date the property is placed into service.

Penalties range from return of 100% of the payment down to 20% depending on the timing of the recapturing event.

Generally, property is considered disposed of to a disqualified person if it is sold to a governmental entity, a 501(c) nonprofit organization, or a cooperative electric company or clean renewable energy bond lender (as described in Section 54(j) of the IRC).

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Recapture (continued) Temporary cessation of energy production will not result in

recapture provided the owner of the property intends to resume production at the time production ceases; however, permanent cessation will result in recapture.

- This will hinge on factual issues and representations and warranties aimed at using commercially reasonable efforts to maintain production might be appropriate.

Sale/Leaseback transactions are permitted such that the lessee who is not the owner can claim the payment provided the lessee placed the property into service and the sale/leaseback occurs within three months of the date placed into service

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Basis

2. Basis: The basis of the property will be reduced by the amount of the Section 1603 payment.

- The applicant must submit with the application documentation to support the basis claimed for their property.

- For properties that have a cost basis in excess of $500,000.00, the applicant must submit an independent accountant’s certification attesting to the accuracy of all costs claimed as part of the basis of the property

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Basis (continued)

Costs that will be deducted for federal income tax purposes in the year in which they are paid or incurred are not includable in the basis on which the payment is determined.

Example: if the applicant is electing to claim a Section 179D deduction for qualifying energy efficient commercial building expenditures, then the Section 1603 payment does not include the portion for which the 179D deduction is taken.

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

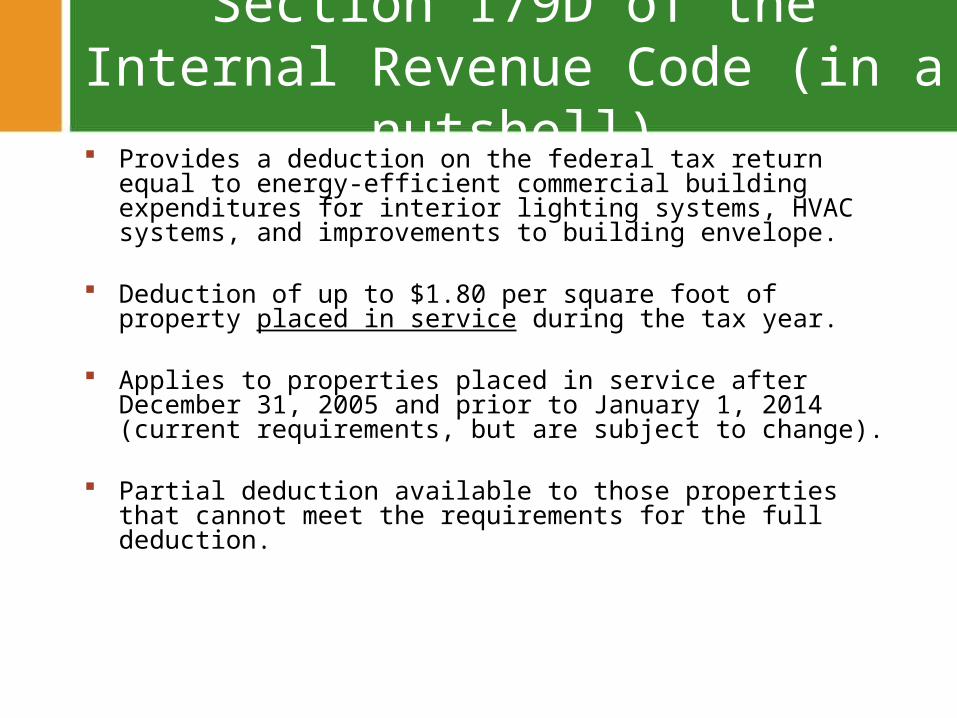

Section 179D of the Internal Revenue Code (in a nutshell)

Provides a deduction on the federal tax return equal to energy-efficient commercial building expenditures for interior lighting systems, HVAC systems, and improvements to building envelope.

Deduction of up to $1.80 per square foot of property placed in service during the tax year.

Applies to properties placed in service after December 31, 2005 and prior to January 1, 2014 (current requirements, but are subject to change).

Partial deduction available to those properties that cannot meet the requirements for the full deduction.

Financial Incentives Under Section 1603 of the American Recovery and Reinvestment Act of 2009

© 2010 Fox Rothschild

Stringent Reporting Requirements

The Section 1603 applicant must maintain project, financial and accounting records sufficient to demonstrate that the funds were properly obtained.

For projects under development at the time the application is made, periodic updates and reporting must be furnished to the Treasury Department as required.