financial handbook for schools table of · pdf file1.14 secure and effective systems 48 ......

TRANSCRIPT

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page i April 2003

FINANCIAL HANDBOOK FOR SCHOOLSTABLE OF CONTENTS

INTRODUCTION iACKNOWLEDGEMENTS iGLOSSARY OF TERMS AND ABBREVIATIONS v

PART I SCHOOLS AND THE LEA’S FINANCIAL FRAMEWORK 1

PART II SCHEME FOR FINANCING SCHOOLS 6Section 1 Introduction 7Section 2 Financial Requirements: Audit 11Section 3 Instalments of Budget Share: Banking 19

arrangements 19Section 4 The treatment of surpluses and deficit balances 22

arising in relation to budget sharesSection 5 Income 24Section 6 The charging of school budget shares 26Section 7 Taxation 29Section 8 The provision of facilities and services by the 30

Authority 30Section 9 Private and Public Partnership projects 32Section 10 Insurance 33Section 11 Miscellaneous 34Section 12 Former grant maintained schools’ balances 38Section 13 Responsibility for repairs and maintenance 39Section 14 Power to provide community facilities 40

Annex A Schools to which the Scheme will apply 48Annex B Responsibility for repairs and maintenance 56Annex C Approved banks and building societies 68Annex D National Westminster Bank: pooling 70

arrangements for schools 70Annex E Health and Safety 72Annex F DfES Statement on Best Value and schools 5Annex G Fees to be deducted from teachers’ salaries and

remitted to the General Teaching Council forEngland

Glossary To The Scheme For Financing Schools 9

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page ii April 2003

PART III FINANCIAL REGULATIONSSection 1 Financial management and internal control 3Section 2 Financial planning and budget monitoring 4Section 3 Financial reporting to the authority and parents 6Section 4 Audit, inspection and financial records 7Section 5 Control of assets and security 9Section 6 Banking arrangements and cash holdings 12Section 7 Private and voluntary funds 15Section 8 Capital 16Section 9 Purchasing strategies, leasing and Best Value 17Section 10 Ordering of goods and services and payment of accounts 18Section 11 Income 21Section 12 Value Added Tax 23Section 13 Personnel and payroll 23Section 14 Construction Industry Scheme 25

PART IV GUIDANCE

SECTION 1 FINANCIAL MANAGEMENT AND INTERNALCONTROL

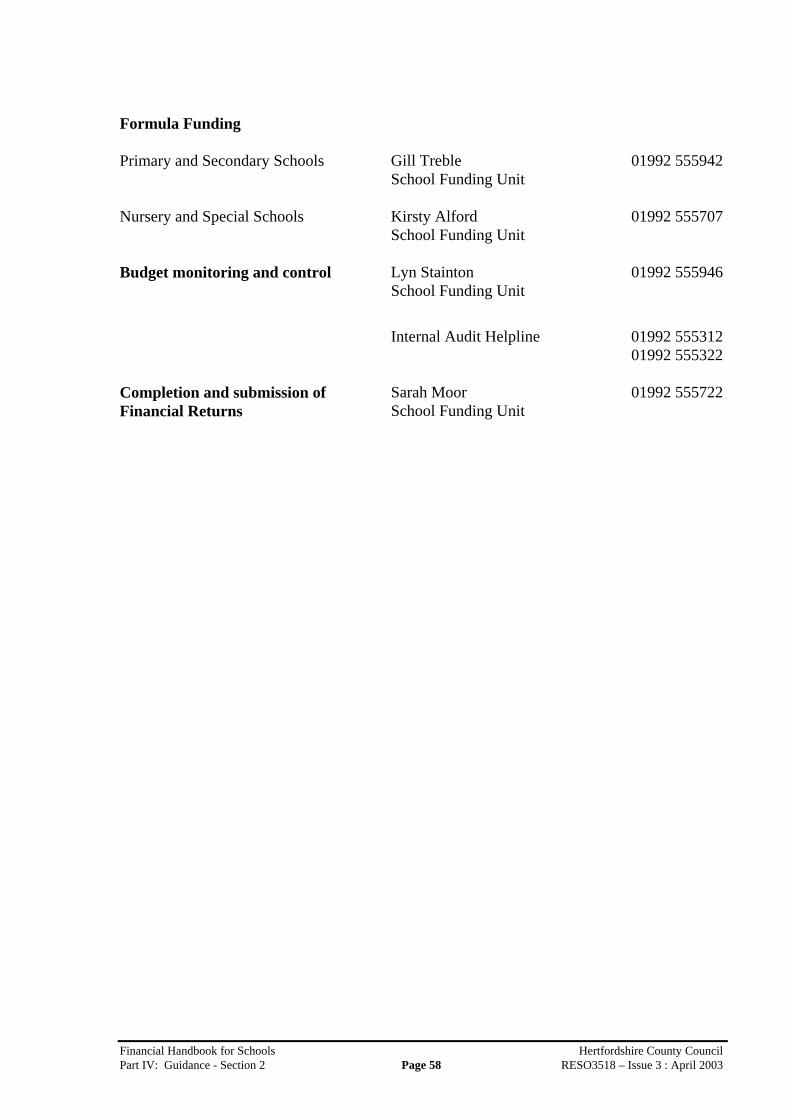

Contacts 33

Financial management1.1 Introduction 351.2 Governing Body responsibilities 351.3 Register of Business Interests 361.4 Whistleblowing 361.5 Delegation of Governing Body responsibilities 371.6 Template for a Schedule of Financial Delegation 38

Internal control1.7 Introduction 441.8 Financial control features 451.9 Formal allocation of responsibilities 451.10 Organisation 461.11 Segregation of duties 461.12 Personnel 471.13 Authorisation and supervision 481.14 Secure and effective systems 481.15 Documentation 481.16 Arithmetical and accounting accuracy 49

Appendix A Guidance notes on Register of Business Interests 51

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page iii April 2003

SECTION 2 FINANCIAL PLANNING AND BUDGETMONITORING

Contacts 57

Financial planning2.1 Introduction 592.2 Financial planning in the medium term 592.3 Benchmarking and Management Information 602.4 Annual budget preparation 61

2.4.1 Budget approval 612.4.2 Registration of budget holders 612.4.3 Budget preparation timetable 61

Budget Monitoring2.5 Introduction 632.6 Timetable

632.7 Monitoring Process 64

2.7.1 Profiling the budget 642.7.2 Recording income, expenditure and commitments 642.7.3 Format of budget monitoring reports 652.7.4 Reviewing budget monitoring reports 652.7.5 Variances 662.7.6 Correcting variances 672.7.7 Recording budget monitoring activity 69

SECTION 3 FINANCIAL REPORTING TO THE AUTHORITY ANDPARENTS

Contacts 72

Financial Reporting to the Authority3.1 Introduction 743.2 Financial returns and formula funding data 743.3 Timetable for submission of financial returns 75

Financial Reporting to Parents3.4 Introduction 753.5 Governing Body eport 753.6 Statutory content 763.7 Discretionary content 763.8 Statutory requirements 77

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page iv April 2003

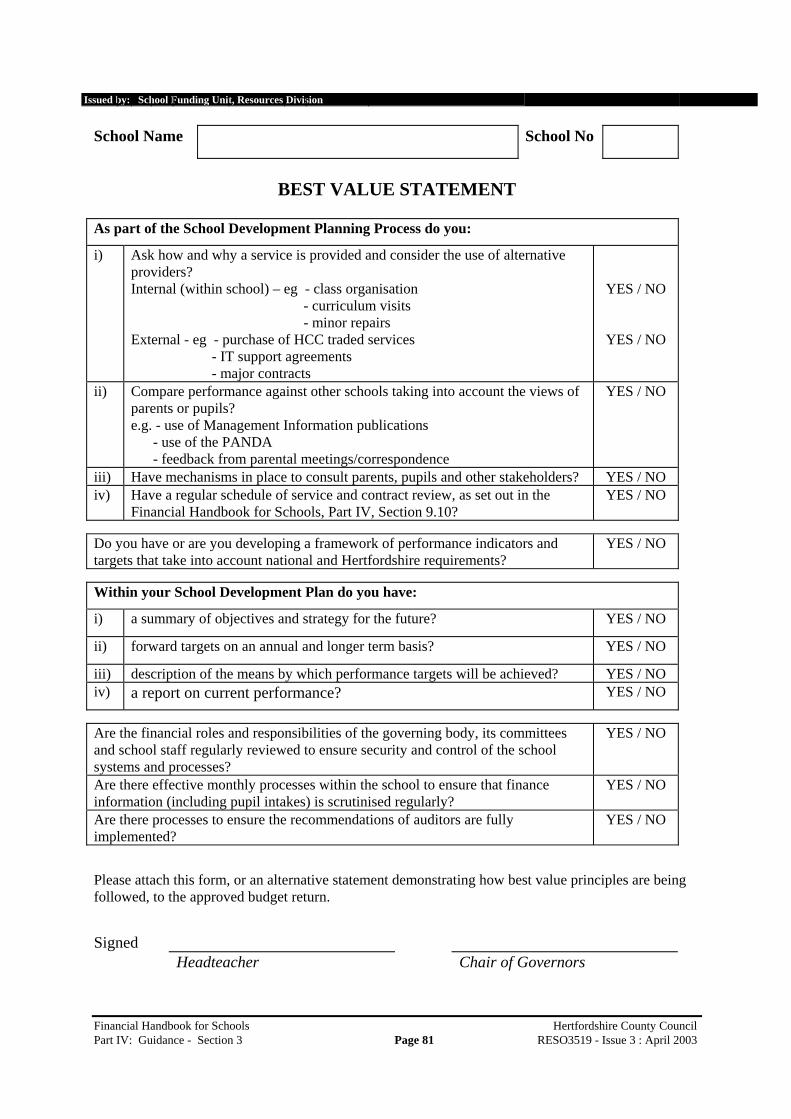

Appendix A Approved Annual Budget Return andBest Value Statement 78

Appendix B Quarterly Returns and Revised ForecastStatement 84

Appendix C End of Year Statement of Accounts 98

SECTION 4 AUDIT AND INSPECTION REQUIREMENTSAND FINANCIAL RECORDS

Contacts 115

Audit and Inspection4.1 Audit and Inspection requirements 1174.2 Internal Audit standards 1174.3 Financial records 1184.4 Controlled financial stationery 118

4.4.1 Controls over cheque stationery 1194.5 Funding the Internal and External Audits 1204.6 Internal Audit – intervals and scope 1204.7 Internal Audit Report and Recommendations 1204.8 External Audit 1214.9 Office for Standards in Education (Ofsted) inspections 121

Retention and Disposal of Financial Records4.10 Legal requirements 1224.11 What financial records must be retained 1224.12 How long to keep records 122

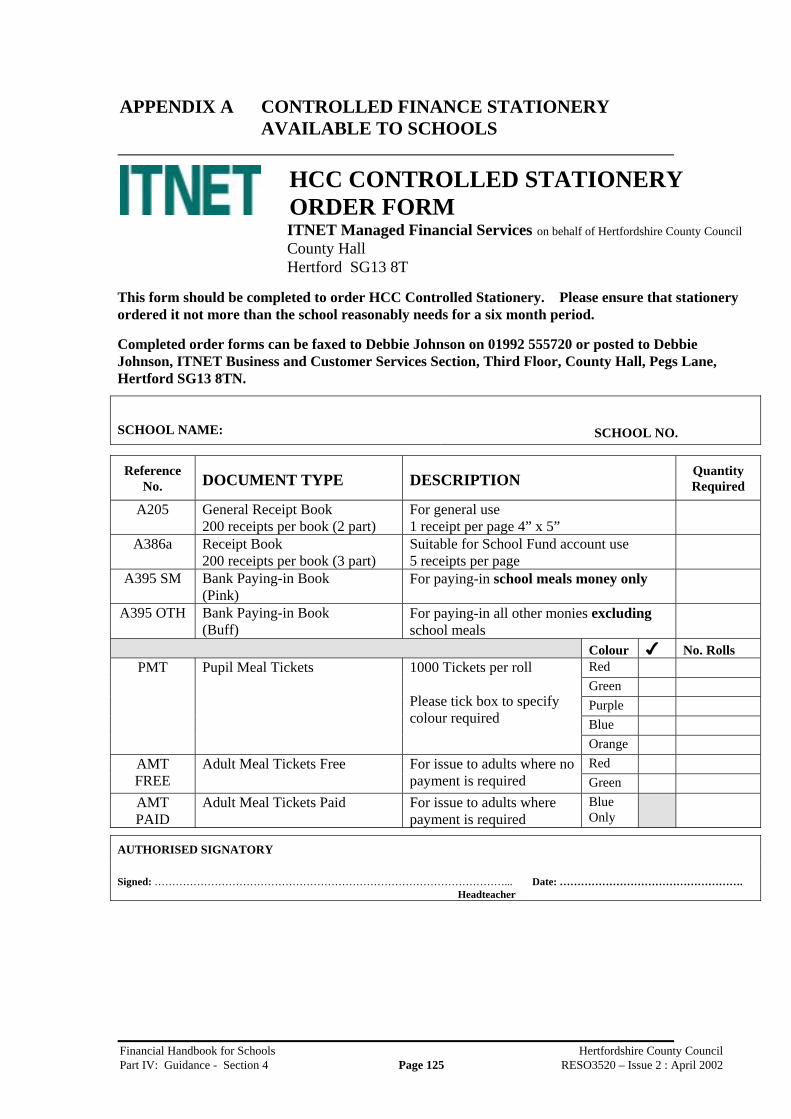

Appendix A Controlled finance stationery 125available to schools 125

Appendix B Scope of thes school internal audit 127

SECTION 5 CONTROL OF ASSETS AND SECURITY

Contacts 134

Control of Assets 1365.1 Introduction 1365.2 Responsibilities 1365.3 Inventories 136

5.3.1 Content of the Inventory 1375.3.2 Completing the Inventory 137

5.4 Stock control record 1385.5 Keys 1385.6 Disposals 139

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page v April 2003

Insurance5.7 Introduction 1395.8 Cover provided by the Authority 1395.9 Optional extensions of cover 1425.10 Governors’ liabilities and insurance of governors 144

The Data Protection Act 1998 1445.11 Introduction 1445.12 The Data Protection Act 1998 1455.13 Obligations under the Data Protection Act 1998 1455.14 Use of Personal Data 1475.15 Notification 148

5.15.1 Notifying for the first time 1485.15.2 Renewing your school’s notification 1485.15.3 Penalties for non-notification 148

5.16 Definition of Terms 1485.17 Code of Practice for CCTV Systems 1495.18 Fair Processing Notices 1505.19 Further advice and guidance 150

Computer Systems And Security of Data5.20 Security and control of data 151

5.20.1 Networks 1515.20.2 Backups 1515.20.3 Viruses 1525.20.4 Passwords 1525.20.5 Preventing snooping 1535.20.6 Preventing theft at work 1545.20.7 Keeping laptops safe 1545.20.8 Disposal of unwanted IT equipment 155

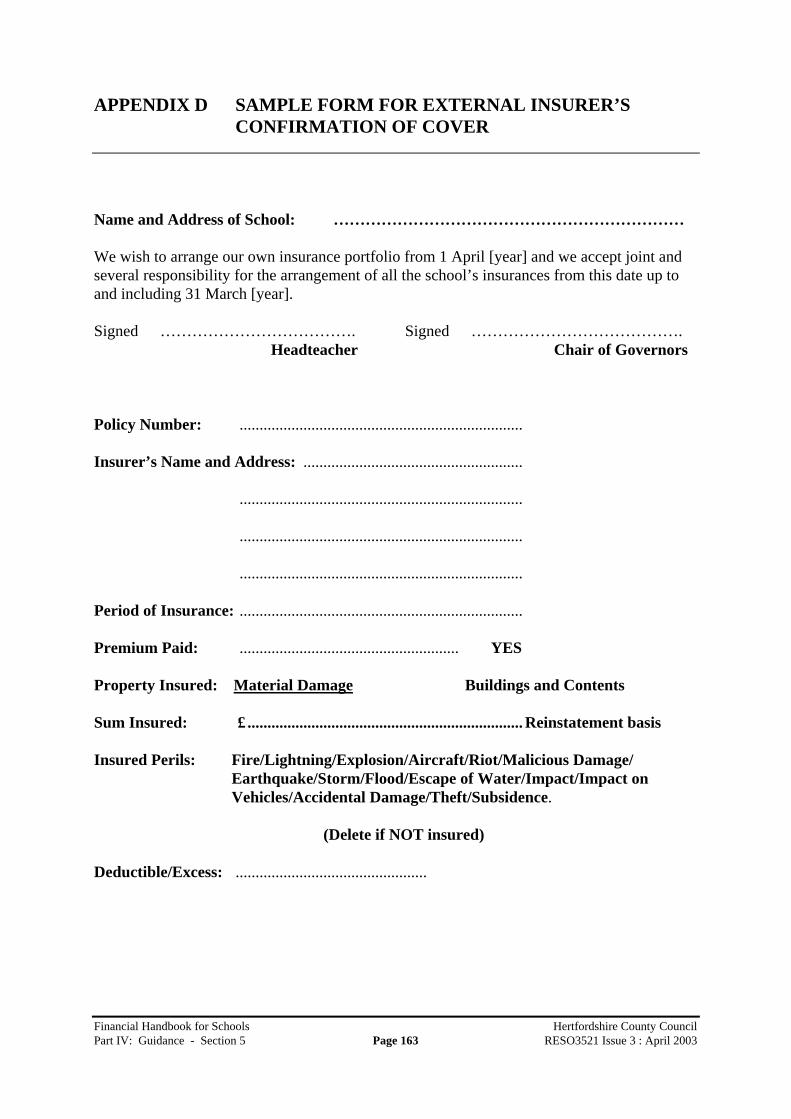

Appendix A Inventory 156Appendix B Stock Record Card 158Appendix C Sample Disposals Policy 159Appendix D Sample Form for external insurer’s confirmation of cover 163

SECTION 6 BANKING ARRANGEMENTS AND CASH HOLDINGS

Contacts 167

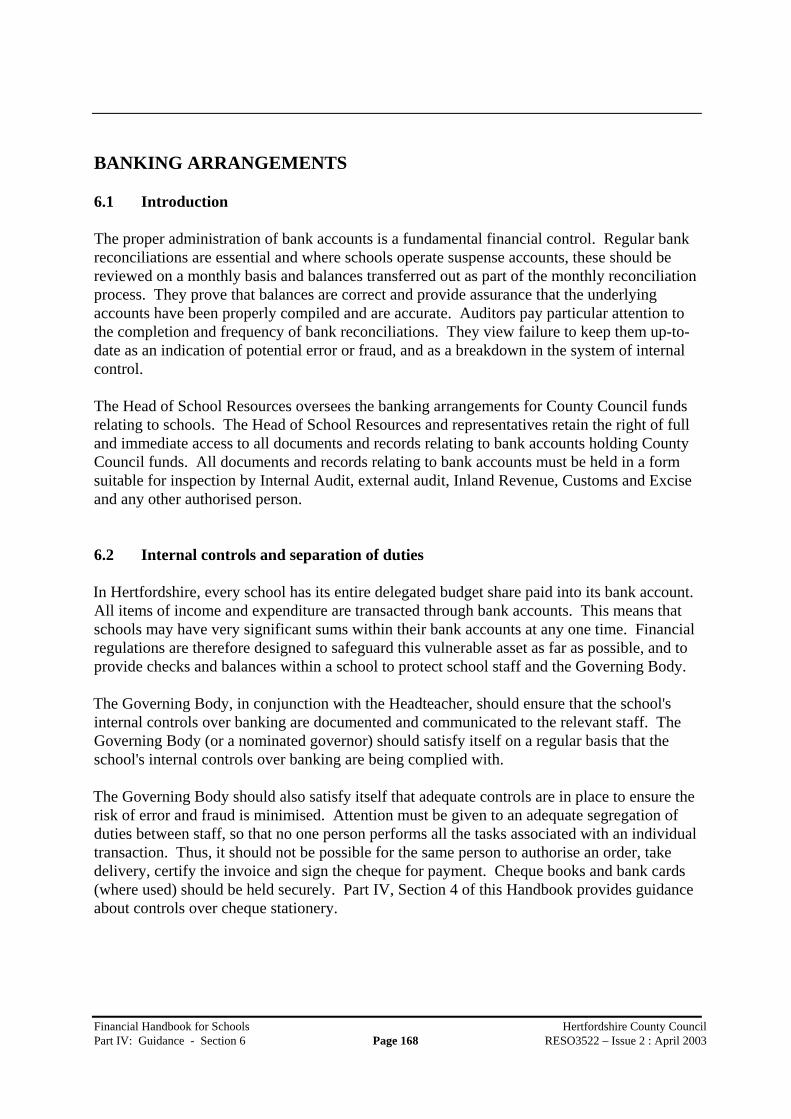

Banking Arrangements6.1 Introduction 1686.2 Internal controls and separation of duties 1686.3 Banking arrangements for County Council funds 1696.4 Pooled banking arrangements 1696.5 Transfer of School Budget Share 1706.6 Interest deduction 170

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page vi April 2003

6.7 Eligible expenditure from the school’s bank accountholding public funds 172

6.8 Governors as authorised signatories 1726.9 Overdrafts and borrowings 1736.10 Banking services for schools 173

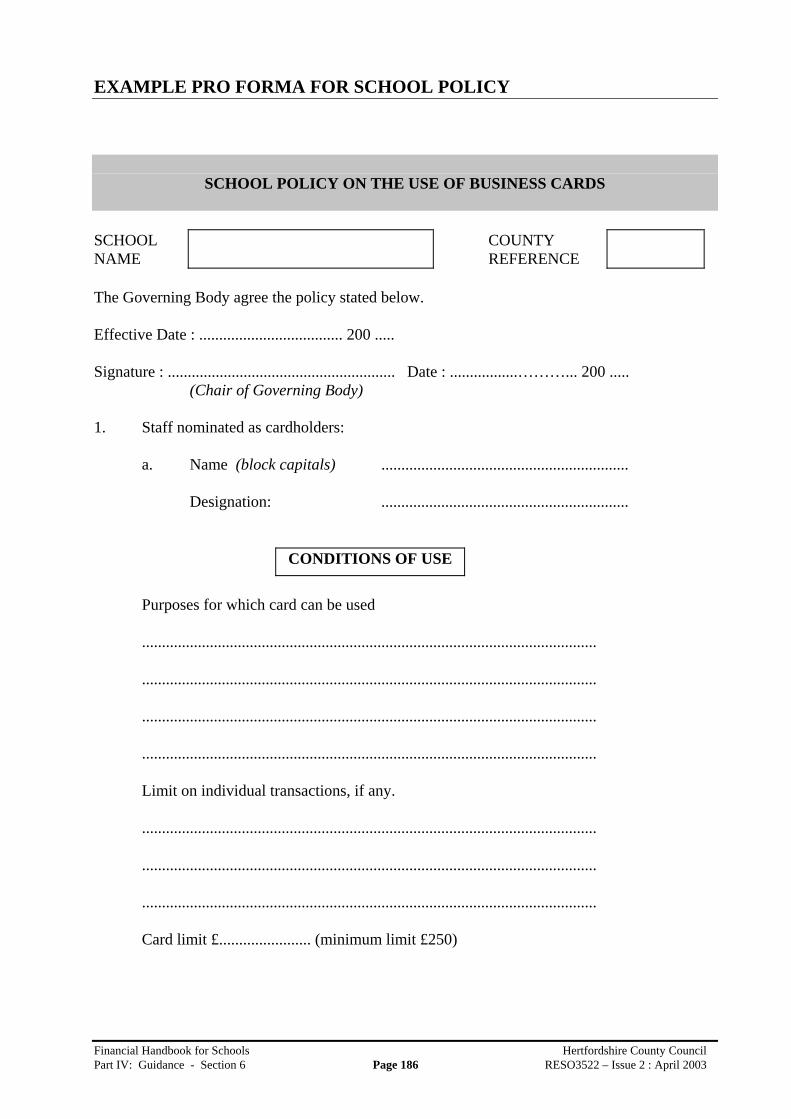

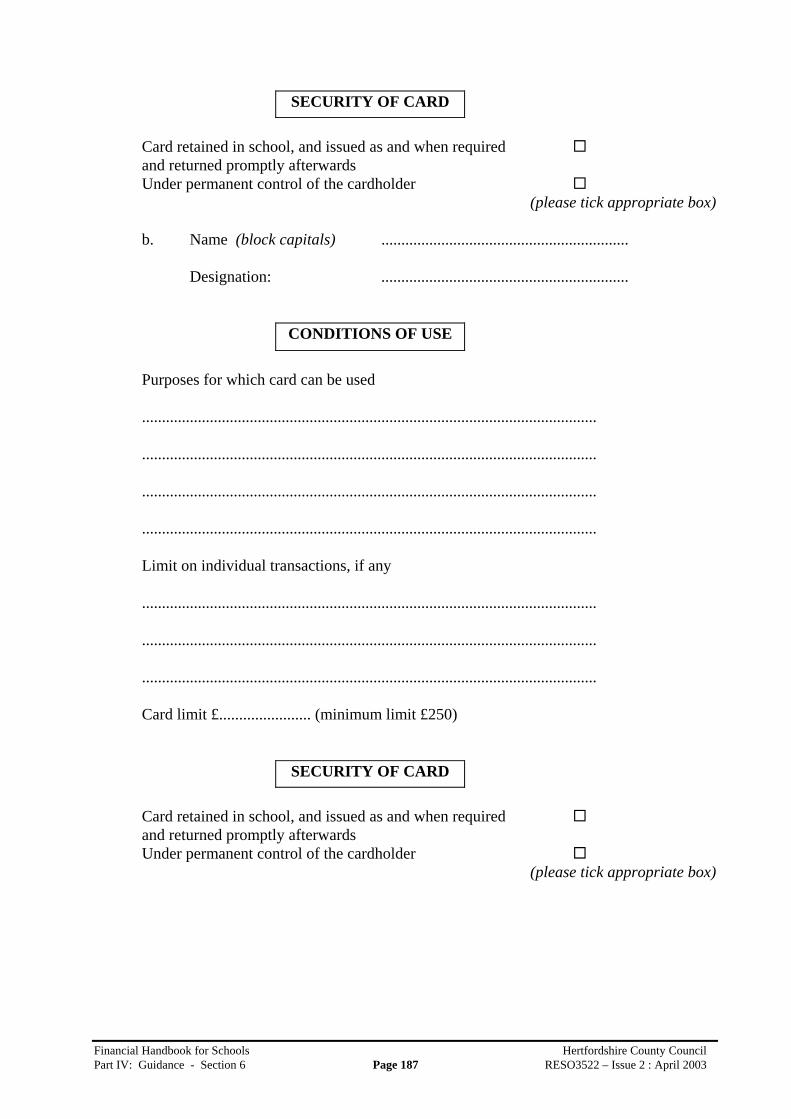

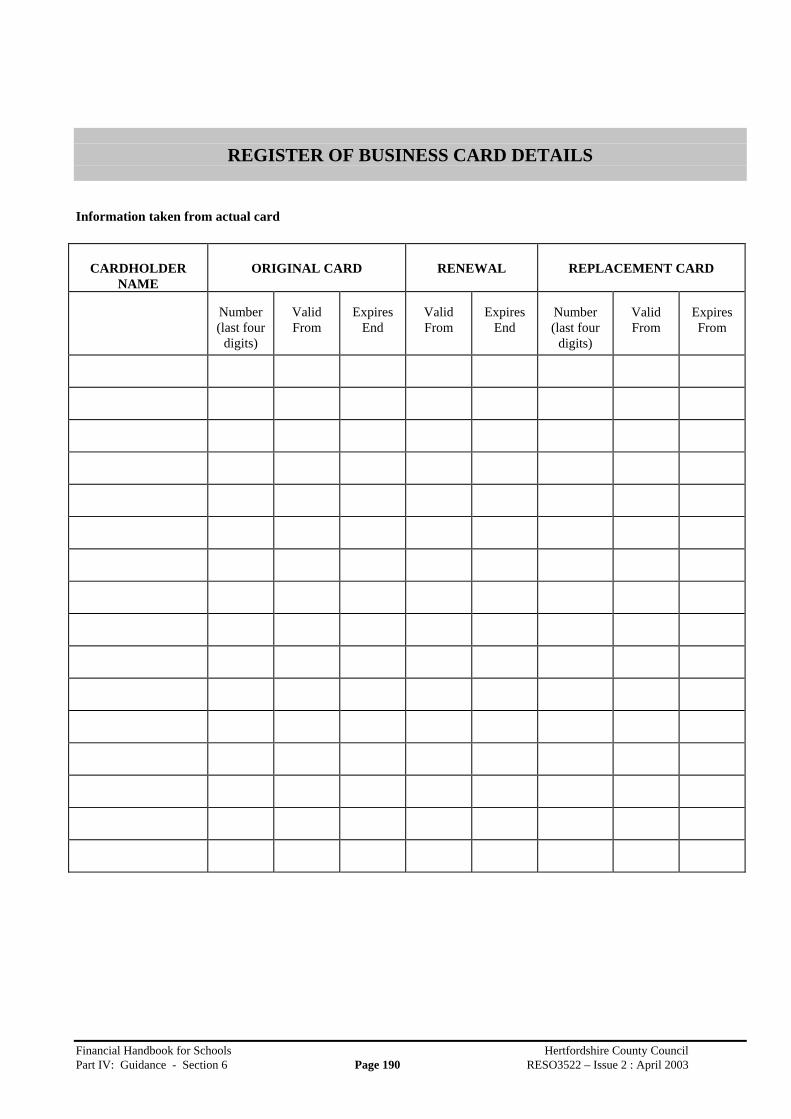

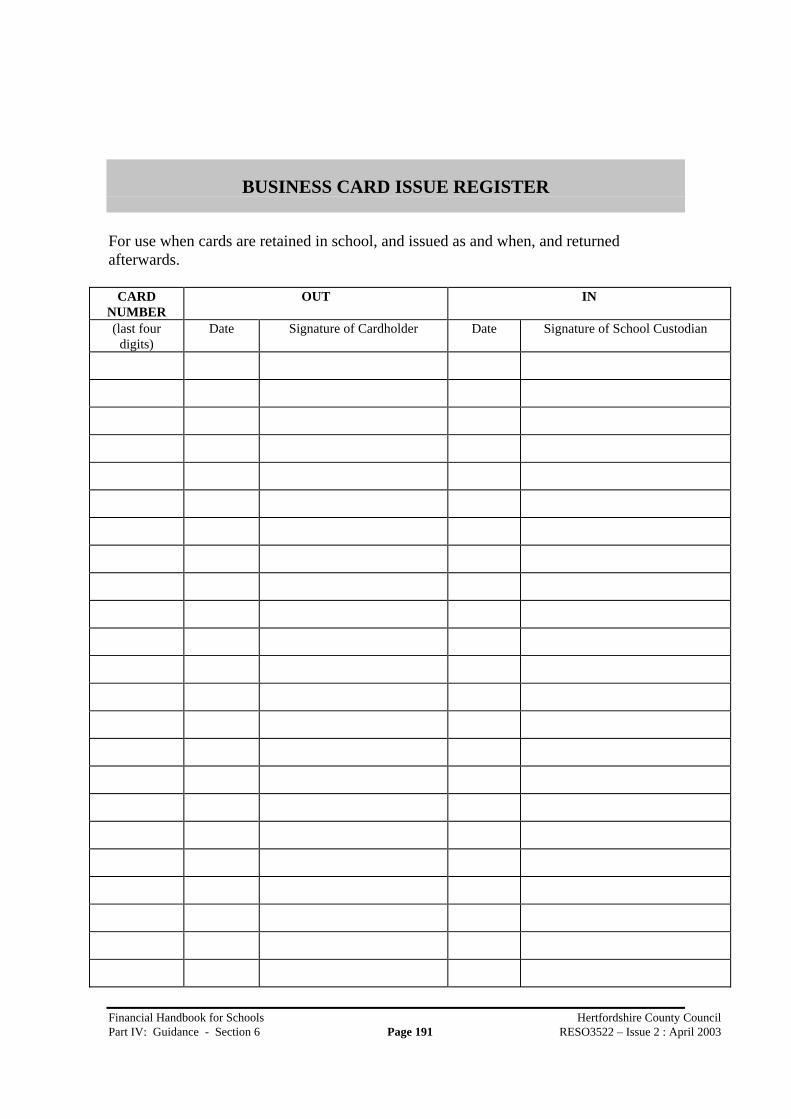

6.10.1 Business cards 1736.10.2 Banking courier service 1736.10.3 Cheque stationery 173

6.11 Insurance cover 173

Cash Holdings6.12 Management of petty cash 175

Appendix A Bank charges for schools within thepooled banking arrangements 176

Appendix B Change of authorised signatory forms for schoolswithin the pooled banking arrangements 178

Appendix C Business Card 183Appendix D Banking Courier Service 193

SECTION 7 PRIVATE AND VOLUNTARY FUNDS

Contacts 197

7.1 Introduction 1997.2 Public and private funds 1997.3 Internal Audit coverage 2007.4 Other accounts 200

Appendix A Tests to determine eligible expenditure 203

SECTION 8 CAPITAL EXPENDITURE

Contacts 207

8.1 Introduction 2098.2 Sources of funding for capital projects 2098.3 Definition of capital expenditure 2108.4 Notification of capital works 2118.5 Commissioning and undertaking capital works 2118.6 Construction Industry Scheme (CIS) 2118.7 Value Added Tax and Voluntary Aided schools 2128.8 Financial administration 213

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page vii April 2003

Appendix A Guidance notes for financial administrationof capital projects 215

Appendix B Schools Loan Scheme 219

SECTION 9 PURCHASING STRATEGIES, LEASING ANDBEST VALUE

Contacts 225

Purchasing Strategies9.1 Introduction 2279.2 Purchasing goods and services 2279.3 Responsibility for purchasing 2289.4 Process for purchasing 2289.5 Organisation 2299.6 Purchasing strategy 2299.7 Specifications 2309.8 Choosing the provider 2309.9 Delivery and monitoring 2329.10 Review 232

Leasing of Equipment9.11 Introduction 2339.12 Definition of a 'Lease' 2339.13 Types of lease 2339.14 Controls on leases 2349.15 Operating leases 2349.16 Lease costs 2359.17 Lease arrangements through County Supplies 2359.18 Schools Loan Scheme 2359.19 Photocopier Contracts 236

Best Value9.20 Best Value 2369.21 Applicability by schools 2369.22 Management implications 2369.23 Best Value guides 237

Appendix A Purchasing conditions and guidelines 239Appendix B Code Of Purchasing Practice 243Appendix C Photocopier contracts 247Appendix D Purchasing of electricity and gas 251

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page viii April 2003

SECTION 10 ORDERING OF GOODS AND SERVICES ANDPAYMENT OF ACCOUNTS

Contacts 256

10.1 Introduction 25810.2 Orders for goods and services 25810.3 Ordering via the Internet 26010.4 Payment of accounts 26010.5 Payment of accounts via ITNET Accounts Payable 26110.6 Payment of Headteachers’ expenses 26110.7 Recording the transactions in the accounts 26210.8 Separation of duties 262

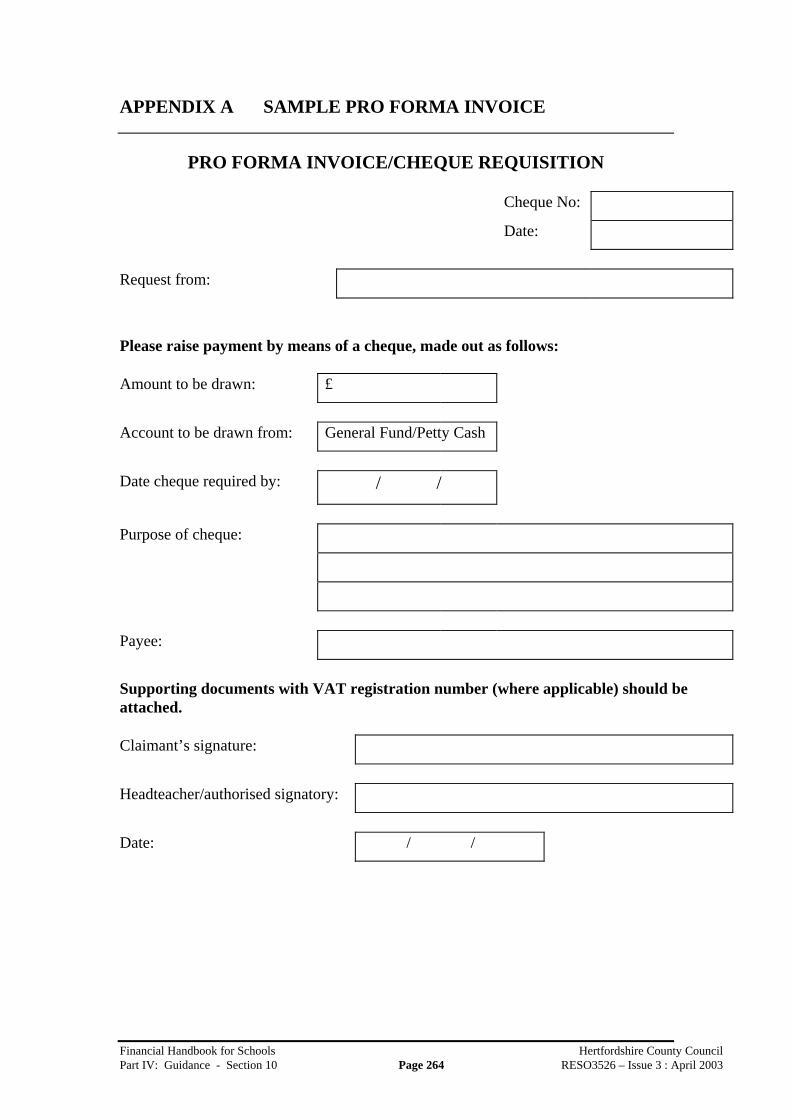

Appendix A Sample pro forma invoice 264Appendix B Guidance notes on completion of

A529 And A14 Forms 266

SECTION 11 INCOME

Contacts 273

11.1 Introduction 27511.2 Security of cash holdings 27511.3 Collection and banking of school income 27511.4 Income records 27611.5 Collection and banking of income on behalf of County Council 27611.6 Hirings income 27711.7 School meals and milk 27711.8 Banking intact 27711.9 VAT on taxable goods and services 27811.10 Debt recovery 27811.11 Writing off debts 27911.12 Charging and Remissions 280

11.12.1Voluntary contributions 28011.12.2Residential trips 28011.12.3Instrumental music lessons 28111.12.4Public examinations 28111.12.5Transportation costs 281

Appendix A Income Record Sheets 283Appendix B Guidance for educational visits and journeys 285Appendix C The County Council's Charging and Remissions Policy 289

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page ix April 2003

SECTION 12 VALUE ADDED TAX

Contacts 293

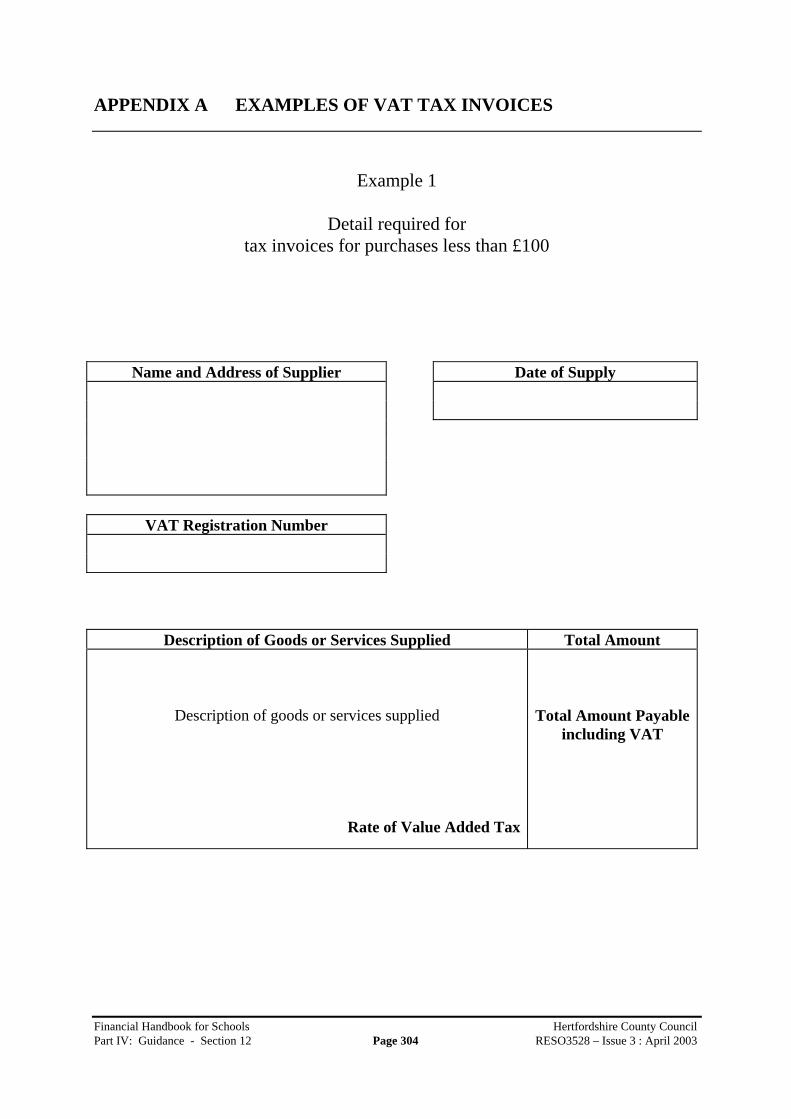

12.1 Introduction 29512.2 General notes 29512.3 Categories of VAT 29512.4 Special treatment of local authorities 29612.5 Input and Output Tax 29712.6 Penalties and interest 29712.7 Recovery of VAT on purchases 29712.8 Documentation required to recover VAT 29812.9 Purchases made from donated funds 29812.10 Income 30012.11 Calculation of VAT in gross amounts 30112.12 Liaison with Customs and Excise 30112.13 VAT on School Fund (Private) Accounts 301

Appendix A Examples of VAT tax invoices 304Appendix B VAT - Specific Issues 308

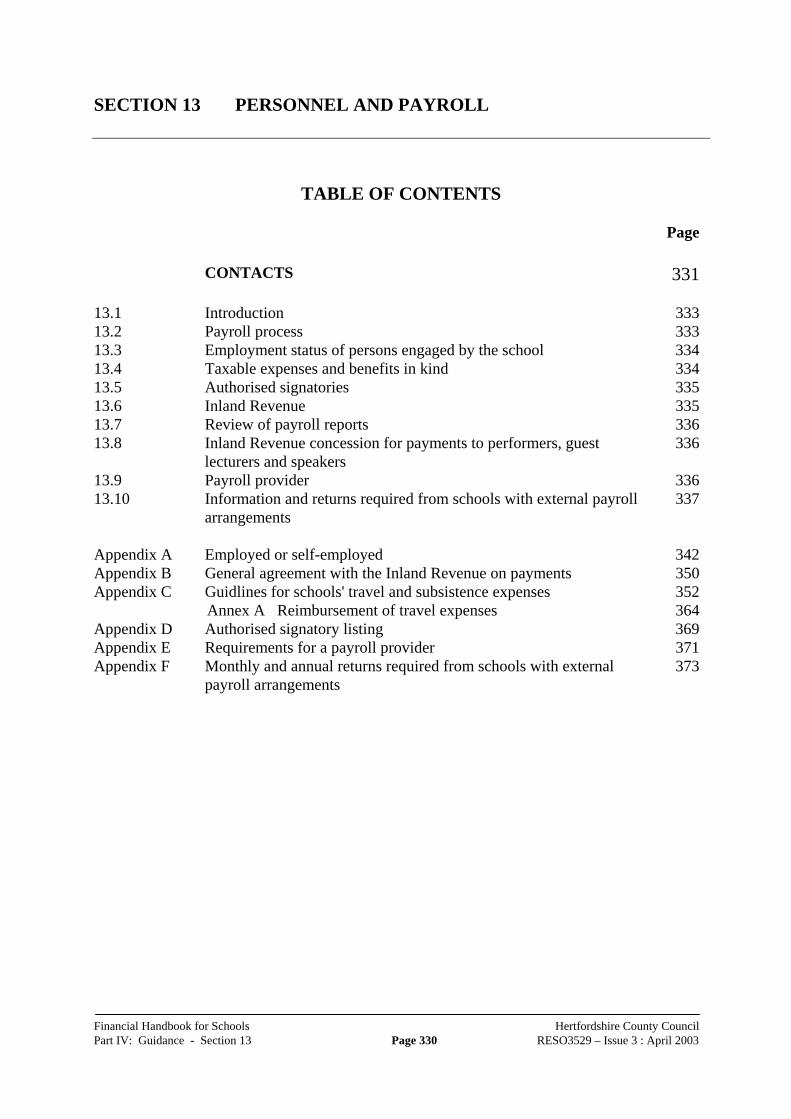

SECTION 13 PERSONNEL AND PAYROLL

Contacts 331

13.1 Introduction 33313.2 Payroll process 33313.3 Employment status of persons engaged by the school 33413.4 Taxable expenses and benefits in kind 33413.5 Authorised signatories 33513.6 Inland Revenue 33513.7 Review of payroll reports 33613.8 Inland Revenue concession for payments to performers,

guest lecturers and speakers 33613.9 Payroll provider 33613.10 Information and returns required from schools with

external payroll arrangements 337

Appendix A Employed or self-employed? 342Appendix B General agreement with the Inland Revenue on

payment to performers, guest lecturers andspeakers, Etc. 350

Appendix C Guidelines for schools’ travel and subsistence expenses 352Appendix D Authorised signatory Listing 369Appendix E Requirements for a payroll provider 371Appendix F Monthly and annual returns required from schools

with external payroll arrangements 373

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page x April 2003

SECTION 14 CONSTRUCTION INDUSTRY SCHEME (CIS)

Contacts 380

14.1 Introduction 38214.2 How does the scheme work? 38214.3 What is a subcontractor? 38314.4 What is a contract? 38314.5 What are construction operations? 38314.6 When can payment be made? 38314.7 When should the deduction be made? 38414.8 Should the deduction be made from the whole payment? 38414.9 County Council arrangements 38414.10 CIS certificates 38514.11 Executive summary 38614.12 CIS and Voluntary Aided schools 386

Appendix A Definitions of Construction 389

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page i April 2003

INTRODUCTION

The Financial Handbook for Schools (“the Handbook”) contains key documents setting outthe financial relationship and financial management requirements between the Authority andits schools. This Handbook applies to all community, voluntary, foundation and specialschools maintained by the Authority.

The Handbook is divided into four parts:

PART I: Schools and the LEA’sFinancial Framework

Sets out the delegation of powers fromthe Finance Director to the AssistantDirector (Resources) of ChildrenSchools & Families of HertfordshireCounty Council to the GoverningBodies of schools.

PART II: Scheme for Financing Schools Sets out the financial relationshipbetween the Authority and maintainedschools. It contains requirementsrelating to financial management andassociated issues, binding on both theAuthority and on schools.

PART III: Financial Regulations Provides the regulatory frameworkwithin which the financial affairs ofschools operate.

PART IV: Guidance Provides information and practicalguidance to enable schools to fulfil theirfinancial responsibilities.

The Handbook is written in plain English, however, the use of some technical terms isunavoidable and a glossary of terms and abbreviations has been provided.

Material within the Handbook will be reviewed annually and revised text will be circulated asnecessary.

Further copies of the Handbook are available from School Funding Unit on 01992 555722.

Comments and suggestions for improving the Handbook are welcomed. Please providedetails on the form overleaf or, alternatively, e:mail Lyn Stainton [email protected].

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page ii April 2003

Financial Handbook for Schools Hertfordshire County CouncilTable of Contents Page iii April 2003

FINANCIAL HANDBOOK FOR SCHOOLS

Please use this form to make suggestions for improving the Handbook.

Please return to: Lyn StaintonSchool Funding UnitResources DivisionCounty HallHertford SG13 8DF

e-mail: [email protected]

Contact: Telephone No:

School Name\Department: School No:

Financial Handbook for Schools Hertfordshire County CouncilAcknowledgements Page iv July 2001

ACKNOWLEDGEMENTS

This Handbook has been compiled using and reproducing materials from:

• The County Council’s Financial Regulations, Standing Orders, Purchasing Conditions andGuidelines, Code of Purchasing Practice and A Finance Guide for Managers

• Ofsted and The Audit Commission’s publications Keeping your Balance and Getting theBest from Your Budget

• Department for Education and Skills Rainbow Pack

and additional material relevant to the financial administration of schools.

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page v Issue 3 : April 2003

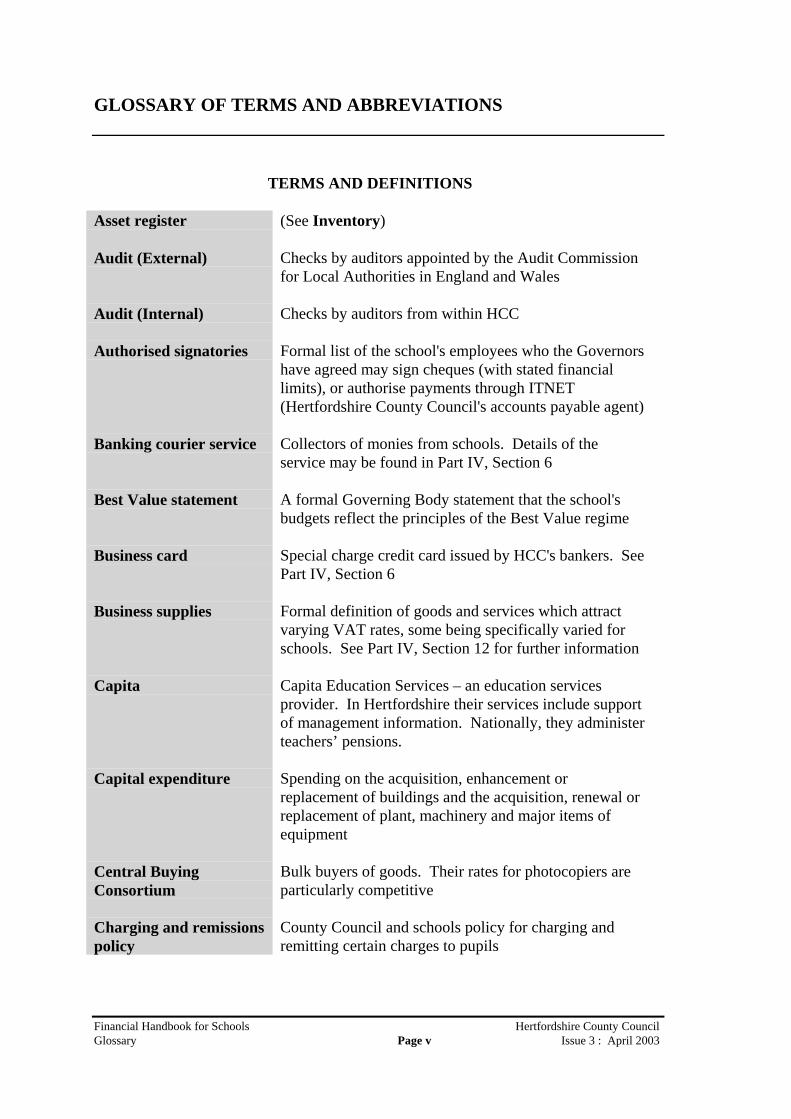

GLOSSARY OF TERMS AND ABBREVIATIONS

TERMS AND DEFINITIONS

Asset register (See Inventory)

Audit (External) Checks by auditors appointed by the Audit Commissionfor Local Authorities in England and Wales

Audit (Internal) Checks by auditors from within HCC

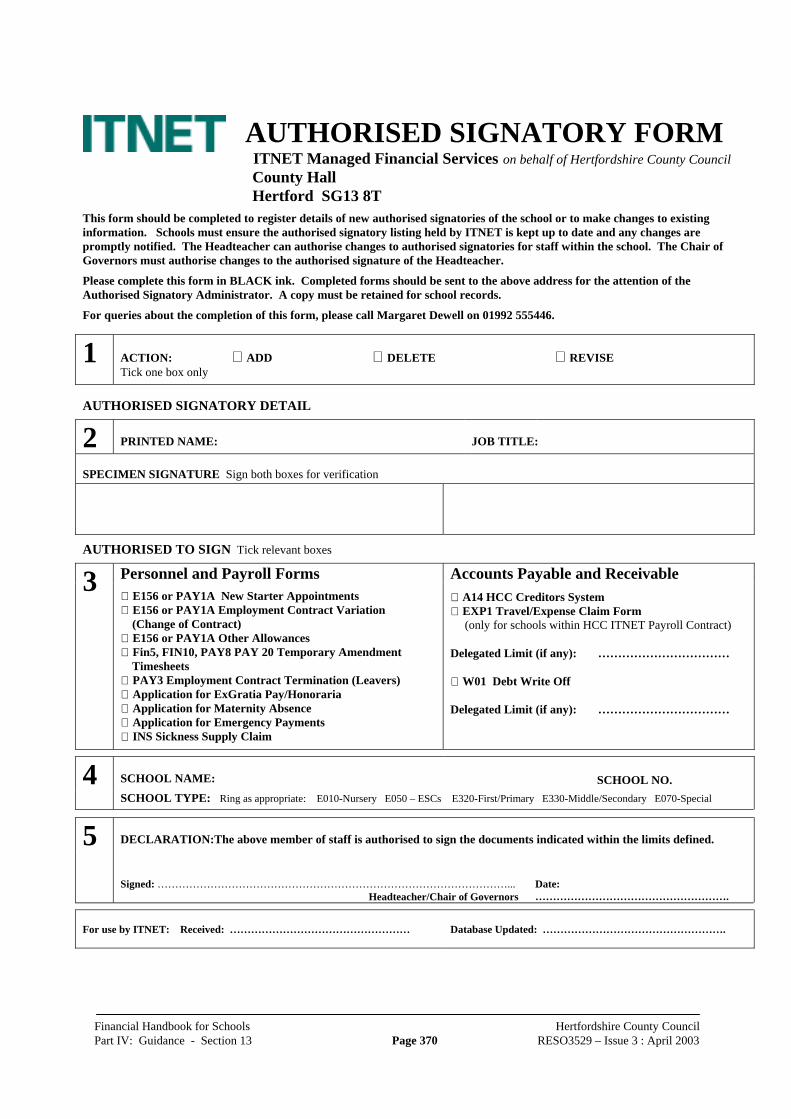

Authorised signatories Formal list of the school's employees who the Governorshave agreed may sign cheques (with stated financiallimits), or authorise payments through ITNET(Hertfordshire County Council's accounts payable agent)

Banking courier service Collectors of monies from schools. Details of theservice may be found in Part IV, Section 6

Best Value statement A formal Governing Body statement that the school'sbudgets reflect the principles of the Best Value regime

Business card Special charge credit card issued by HCC's bankers. SeePart IV, Section 6

Business supplies Formal definition of goods and services which attractvarying VAT rates, some being specifically varied forschools. See Part IV, Section 12 for further information

Capita Capita Education Services – an education servicesprovider. In Hertfordshire their services include supportof management information. Nationally, they administerteachers’ pensions.

Capital expenditure Spending on the acquisition, enhancement orreplacement of buildings and the acquisition, renewal orreplacement of plant, machinery and major items ofequipment

Central BuyingConsortium

Bulk buyers of goods. Their rates for photocopiers areparticularly competitive

Charging and remissionspolicy

County Council and schools policy for charging andremitting certain charges to pupils

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page vi Issue 3 : April 2003

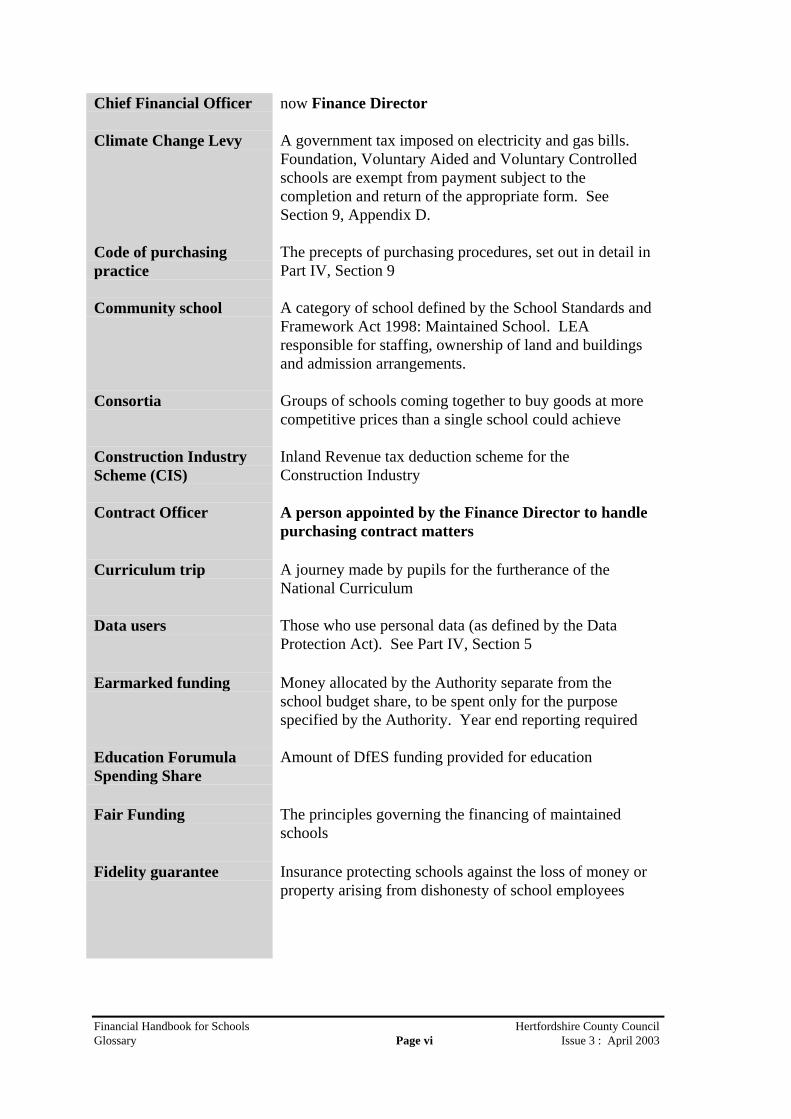

Chief Financial Officer now Finance Director

Climate Change Levy A government tax imposed on electricity and gas bills.Foundation, Voluntary Aided and Voluntary Controlledschools are exempt from payment subject to thecompletion and return of the appropriate form. SeeSection 9, Appendix D.

Code of purchasingpractice

The precepts of purchasing procedures, set out in detail inPart IV, Section 9

Community school A category of school defined by the School Standards andFramework Act 1998: Maintained School. LEAresponsible for staffing, ownership of land and buildingsand admission arrangements.

Consortia Groups of schools coming together to buy goods at morecompetitive prices than a single school could achieve

Construction IndustryScheme (CIS)

Inland Revenue tax deduction scheme for theConstruction Industry

Contract Officer A person appointed by the Finance Director to handlepurchasing contract matters

Curriculum trip A journey made by pupils for the furtherance of theNational Curriculum

Data users Those who use personal data (as defined by the DataProtection Act). See Part IV, Section 5

Earmarked funding Money allocated by the Authority separate from theschool budget share, to be spent only for the purposespecified by the Authority. Year end reporting required

Education ForumulaSpending Share

Amount of DfES funding provided for education

Fair Funding The principles governing the financing of maintainedschools

Fidelity guarantee Insurance protecting schools against the loss of money orproperty arising from dishonesty of school employees

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page vii Issue 3 : April 2003

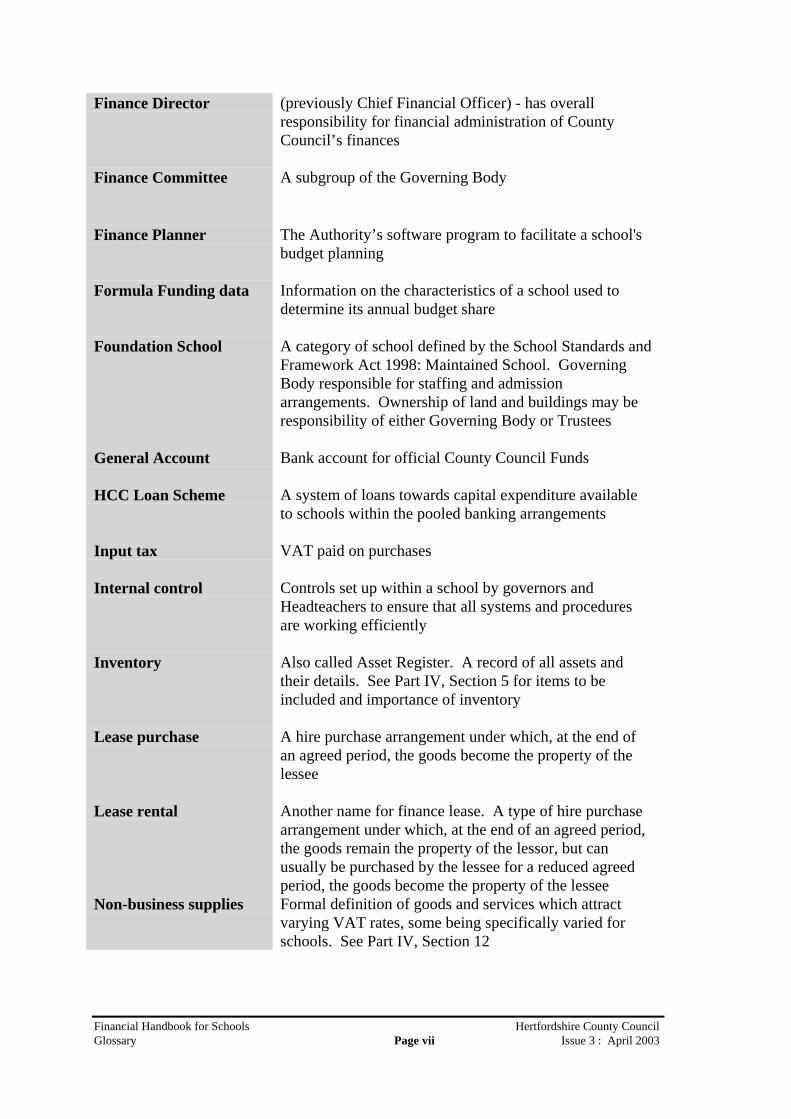

Finance Director (previously Chief Financial Officer) - has overallresponsibility for financial administration of CountyCouncil’s finances

Finance Committee A subgroup of the Governing Body

Finance Planner The Authority’s software program to facilitate a school'sbudget planning

Formula Funding data Information on the characteristics of a school used todetermine its annual budget share

Foundation School A category of school defined by the School Standards andFramework Act 1998: Maintained School. GoverningBody responsible for staffing and admissionarrangements. Ownership of land and buildings may beresponsibility of either Governing Body or Trustees

General Account Bank account for official County Council Funds

HCC Loan Scheme A system of loans towards capital expenditure availableto schools within the pooled banking arrangements

Input tax VAT paid on purchases

Internal control Controls set up within a school by governors andHeadteachers to ensure that all systems and proceduresare working efficiently

Inventory Also called Asset Register. A record of all assets andtheir details. See Part IV, Section 5 for items to beincluded and importance of inventory

Lease purchase A hire purchase arrangement under which, at the end ofan agreed period, the goods become the property of thelessee

Lease rental Another name for finance lease. A type of hire purchasearrangement under which, at the end of an agreed period,the goods remain the property of the lessor, but canusually be purchased by the lessee for a reduced agreedperiod, the goods become the property of the lessee

Non-business supplies Formal definition of goods and services which attractvarying VAT rates, some being specifically varied forschools. See Part IV, Section 12

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page viii Issue 3 : April 2003

Operating lease The same as a lease rental, but at the end of the agreedperiod the goods can only be bought by the lessee onpayment of the full market value

Output tax VAT added to invoices for sales (of goods or services).See Part IV, Section 12

Pooled BankingArrangements

An arrangement between the Authority and NationalWestminster Bank to treat the bank balances of allschools within the pooled arrangements as part of theCounty Council’s overall bank balance.

Register of businessinterests

A record of the Governors' and staff's financial interestsoutside the school which might possibly conflict with theschool's interests

Section 52 – BudgetStatement

Document providing details of LEA budget for educationdetailing amounts delegated to schools. This documentis available for both schools and the public

Section 52-OutturnStatement

Document providing details of LEA and schools spendingfor education. This document is available for bothschools and the public

Schedule of charge fortaxation

Part of tax law under which a particular type of income ischargeable. For example, the self-employed are liableunder Schedule D; employees under Schedule E. Thereare further Schedules applicable to income outside thescope of this guidance.

Schedule of delegation A record of the tasks and responsibilities within a schoolwhich are passed from the Governing Body to theHeadteacher, and from the Headteacher to the staff.

School DevelopmentPlan

The overall statement of the school's aims and objectives.All activities, purchases, sales and other procedures mustfit within the financial and other aims of this plan

Tax exemptioncertificate

Documentary proof that a subcontractor is properlyentitled to be paid under the CIS

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page ix Issue 3 : April 2003

VAT rates The varying rates of VAT are defined in Part IV,Section 12

Virement Moving funding from one budget to another

Voluntary Aided School A category of school defined by the School Standardsand Framework Act 1998: Maintained School.Governing Body responsible for staffing and admissionarrangements. Ownership of land and buildings may beresponsibility of Governing Body or Trustees

Voluntary ControlledSchool

A category of school defined by the School Standardsand Framework Act: Maintained School. LEAresponsible for staffing and admission arrangements.Ownership of land and buildings may be theresponsibility of Governing Body or Trustees

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page x Issue 3 : April 2003

ABBREVIATIONS AND ACRONYMS

A Level Advanced level qualificationABR Approved budget return – school’s summary of intended budget

spendingAFM (see APS)AMG Annual maintenance grantAMP Asset management plan – describes the condition, suitability and

sufficiency of school premisesAPS Amey Property Services (formerly AFM)– outsourced company doing

work previously done by HCC Property DepartmentAS Level Advanced supplementary level qualificationAST Advanced skills teacherATL Association of Teachers and Lecturers – a trades unionAVCs Additional voluntary (pensions) contributionsAWPU Age weighted pupil unit – factor in pupil-led formula funding

BACS Bankers’ automated clearance systemBISCUIT Business information system for central units to support internal

trading – the system that supports trading units with schoolsBS British standardBV Best value

C & E Customs & ExciseCCT Compulsory competitive tendering – re contractsCCTV Closed circuit televisionCD Compact discCFR Consistent Financial ReportingCEO Chief Education Officer – statutory role which is the Director of

Children, Schools and Families within HertfordshireCFO Chief Financial Officer (now Finance Director)CFR Consistent Financial ReportingCFU Central Finance Unit – within Resources division of CSFChRIS Child related information systemCIPFA Chartered Institute of Public Finance Accountancy – professional

accountancy bodyCIS Construction Industry Scheme – for taxation purposesCoSHH Control of substances hazardous to healthCP Child protectionCSF Children, Schools & Families Department – incorporates former

Education Department and parts of former Social Services DepartmentCSCS County Supplies & Contract Services – a department within HCC

DfEE Department for Education & Employment (now DfES)DfES Department for Education & Skills (formerly DfEE)

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page xi Issue 3 : April 2003

EBD Emotional & behavioural difficulties – type of SENEDI Electronic Data InterchangeEDP Education development planEEC European Economic CommunityELP Early learning plan – scheme of 2 admission dates for nursery pupilsESC Education Support CentreEPF Earmarked Pupil FundingEWT Equivalent whole time

FAQ Frequently Asked QuestionsFAS Funding Agency for Schools – re GM schools; no longer in operationFD Finance Director (formerly Chief Financial Officer)FE Forms of entryFLA Foreign Language AssistantFMS6 Financial Management Systems, version 6FSM Free school mealsFSS Financial Services for Schools – part of the School Funding UnitFTE Full time equivalent – staffingFUG Finance User Group – refer to the School Funding UnitFUN Finance User Network – refer to the School Funding Unit

GCSE General Certificate of Secondary Education – qualificationGM Grant Maintained schools – now either Foundation, VA or CommunityGNVQ General National Vocational Qualification

H&S Health & Safety – refer to Property Unit of Resources DivisionHASSH Hertfordshire Association of Secondary HeadteachersHCC Hertfordshire County CouncilHEADLAMP Headteachers Leadership and Management ProgrammeHGfL Hertfordshire Grid for LearningHI Hearing impaired – type of SENHMI Her Majesty’s InspectorHSE Health & Safety Executive

IB International Baccalaureate – a qualificationICT Information & Communications TechnologyINSET In-service education and trainingISAS In-school accounting service – provided by FSSISB Individual schools budgetISR Individual School RangeISO International Standards OrganisationIT Information TechnologyITNET ITNET Managed Services – outsourced payroll and IT functions

JCC Joint Consultative CommitteeJM Junior mixed school

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page xii Issue 3 : April 2003

JMI Junior mixed and infants school

KPI Key Performance IndicatorsKS Key stage

LEA Local education authorityLFM Local financial managementLLSC Local Learning Skills CouncilLMNS Local management of nursery schoolsLMS Local management of schoolsLMSS Local management of special schoolsLRM4/5 Local Resources Management version 4/5 – schools accounting systemLSA Learning Support AssistantLSB Local schools budgetLSC Learning and Skills Council – a body which has replaced the TEC, and

funds Post-16 education in schoolsLWA London Weighting Allowance

MECSS Minority Ethnic Curriculum Support Service – part of SchoolStandards & Curriculum division

MFL Modern foreign languageMIU Management Information Unit – part of Resources divisionMLD Moderate learning difficulties – type of SENMPLS Multi-professional local service – within CSF structureMSA Midday supervisory assistant – a “dinner lady”

NAGM National Association of Governors and ManagersNAHT National Association of HeadteachersNAS/UWT National Association of Schoolmasters/Union of Women TeachersNC National CurriculumNDS New Deal for SchoolsNGfL National Grid for LearningNIC National Insurance contributionsNJC National Joint CouncilNNEB National Nursery Examination BoardNOF New Opportunities FundNOR Numbers on roll, i.e. pupil numbersNPQH National Professional Qualification for HeadshipNQT Newly qualified teacherNSSEN Non-statemented special educational needsNVQ National Vocational QualificationNTL National Telecommunications Ltd – schools service provider for NGfLNUT National Union of Teachers

OfSTED Office for Standards in Education

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page xiii Issue 3 : April 2003

PANDA Performance and Assessment dataPAT Professional Association of TeachersPAYE Pay as you earn – taxationPDRS Primary Dinner Register SystemPE Physical education – see also PTPFI Private Finance InitiativePGCE Post-graduate Certificate in EducationPH Physically handicappedPHF Primary Heads ForumPI Physically impaired – type of SENPICSI Pre-inspection context and school indicatorPLASC Pupil Level Annual School CensusPNI Physical and neurological impairment – type of SENPNSU Permanent non-school usePPA Pre-school Playgroups AssociationPPP Public & Private PartnershipPRC Premature retirement compensationPRU Pupil Referral Unit – now referred to as Education Support CentrePSE Personal & social educationPT Physical trainingPTA Parent Teacher AssociationPTR Pupil : teacher ratio

QCA Qualifications & Curriculum Authority

R&M Repairs and maintenanceRE Religious educationRoA Record of AchievementRSA Royal Society of ArtsRSG Rates Support GrantRTG Real Terms Guarantee

S122 Section 122 – Statement of Education Budget and ExpenditureS&L Speech and language difficultiesS&S Supplies and servicesSACRE Standing Advisory Council on Religious EducationSATs Standard Assessment TasksSCAA School Curriculum & Assessment AuthoritySCC Schools Causing ConcernSCP Scale point for staffingSDA School development adviserSDP School development planSFU School Funding UnitSEN Special educational needsSENCO SEN co-ordinatorSHA Secondary Heads Association

Financial Handbook for Schools Hertfordshire County CouncilGlossary Page xiv Issue 3 : April 2003

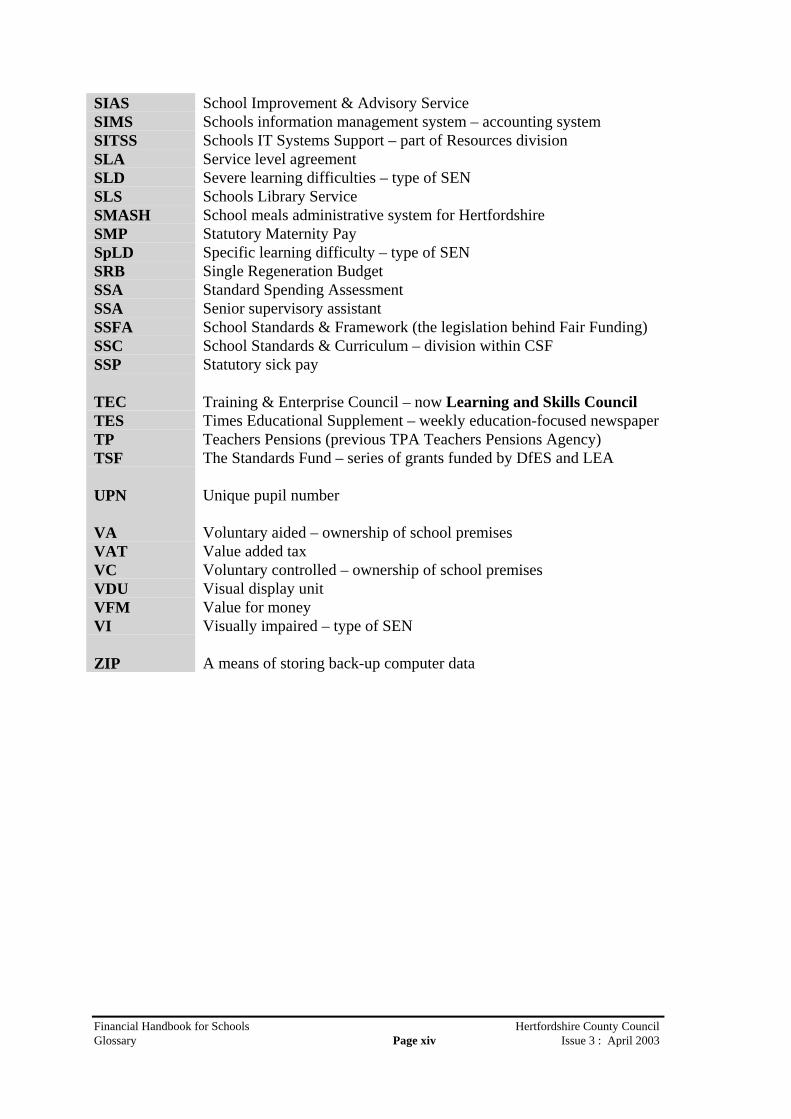

SIAS School Improvement & Advisory ServiceSIMS Schools information management system – accounting systemSITSS Schools IT Systems Support – part of Resources divisionSLA Service level agreementSLD Severe learning difficulties – type of SENSLS Schools Library ServiceSMASH School meals administrative system for HertfordshireSMP Statutory Maternity PaySpLD Specific learning difficulty – type of SENSRB Single Regeneration BudgetSSA Standard Spending AssessmentSSA Senior supervisory assistantSSFA School Standards & Framework (the legislation behind Fair Funding)SSC School Standards & Curriculum – division within CSFSSP Statutory sick pay

TEC Training & Enterprise Council – now Learning and Skills CouncilTES Times Educational Supplement – weekly education-focused newspaperTP Teachers Pensions (previous TPA Teachers Pensions Agency)TSF The Standards Fund – series of grants funded by DfES and LEA

UPN Unique pupil number

VA Voluntary aided – ownership of school premisesVAT Value added taxVC Voluntary controlled – ownership of school premisesVDU Visual display unitVFM Value for moneyVI Visually impaired – type of SEN

ZIP A means of storing back-up computer data

Financial Handbook for Schools Hertfordshire County CouncilPart I: Schools and the LEA's Financial Framework Page 1 RESO3514: April 2003

PART I SCHOOLS AND THE LEA’S FINANCIALFRAMEWORK

Schools are funded from public funds and are, therefore, bound by the same obligations as theCounty Council and any other public body for the proper stewardship of and accountabilityfor public funds.

Local management has significant implications for the way in which school budgets aremanaged, and hence how the Finance Director of the County Council discharges his statutoryand general duties. It does not in any way reduce the duties of the Finance Director nor is itinconsistent with those duties. Therefore, the Finance Director still retains ultimateresponsibility for ensuring compliance with statutory and other financial requirements.

To meet his responsibilities, the Finance Director will:

• determine and maintain a regulatory framework, consistent with his statutory dutiesfor the stewardship of public money

• determine and maintain a system of financial reporting to the Authority, to ensure thatpublic funds are properly accounted for

• monitor schools' financial performance and, in the case of schools at risk, activate acorrective or recovery programme.

Further, LEAs are required to adopt a monitoring role towards schools. LEAs exercise littledirect, detailed control over the bulk of spending in schools but have a vital overallresponsibility to implement effective arrangements for the control and proper use of publicfunds.

There are a number of key areas where the LEA has a lead function. It will:

• determine the total resources available to schools• establish and manage the Scheme for Financing Schools and funding formulae• in conjunction with the Finance Director set out the financial control environment

within which Governing Bodies must operate• operate sanctions, including withdrawal of delegation, where appropriate• support Governing Bodies with professional advice and guidance

This Handbook sets out the framework of responsibility and accountability for GoverningBodies and school staff and the general conditions applying to delegation of public funds. Italso provides guidance to support schools in implementing and maintaining robust financialprocedures and systems to ensure compliance with the County Council's FinancialRegulations.

Financial Handbook for Schools Hertfordshire County CouncilPart I: Schools and the LEA's Financial Framework Page 1 RESO3514: April 2003

Roles and Responsibilities and Delegation of Powers

The County Council's Financial Regulations are intended to clarify responsibilities forparticular functions and provide a framework within which decisions are made. Where thereare specific statutory powers and duties, the Financial Regulations seek to ensure compliancewith, as well as reflecting best professional practices and the decisions of the County Council.

The Financial Regulations complement various County Council general regulations and applyto the Governing Body of all maintained schools covered by the Scheme for FinancingSchools. They also apply to Headteachers and all others to whom functions may be delegated.The Financial Regulations include sensible measures of internal control and as such representa minimum standard. Governing Bodies are required to act in accordance with all of theCounty Council's regulations but can tailor specific provisions as long as the minimumstandards are met.

The Finance Director

The Finance Director (“FD”) is the financial adviser to the County Council.

The FD is required by Section 151 of the Local Government Act 1972 to secure properfinancial management of the Authority’s affairs. The FD is therefore responsible for decidingthe Authority’s accounting procedures, systems, and the form of its accounts and supportingrecords.

Under the Accounts and Audit Regulations 2003 the FD must produce an Annual Reportdetailing the Authority’s income and expenditure and its assets and liabilities. This is thensubject to examination by the Authority’s external auditors. This duty encompasses allmaintained schools and creates the need for schools to make returns and supply otherinformation for this purpose. Under the Accounts and Audit Regulations, the FD needs toensure that the accounting systems are observed and that the accounts and supporting recordsare kept up to date.

Under Section 114 of the Local Government Finance Act 1988 the FD is required to stop andreport to the Authority:

• any items of unlawful expenditure• any item which would cause a loss to the Authority• any situation where the Authority’s total expenditure seems likely to exceed the

resources available to meet it.

When such a report is made, the FD will send a copy to the County Council’s externalauditors and to each member of the County Council.

In order to comply with these duties, the FD and any staff to whom he has delegated powersshall be provided with any information required and shall have access todocuments and records for this purpose.

Financial Handbook for Schools Hertfordshire County CouncilPart I: Schools and the LEA's Financial Framework Page 1 RESO3514: April 2003

The Assistant Director (Resources) and Board of Governors

The FD has delegated power in relation to schools to the Assistant Director (Resources) andreference elsewhere in this Handbook reflects this delegation, and further delegations togetherwith any reporting requirements on exercising such.

The Assistant Director (Resources) in turn, delegates power to Governing Bodies. They, inexercising their delegated financial responsibilities, must confirm and document these in aschedule of delegation. This schedule sets out the responsibilities of each party, and furtherdelegations.

Subject to any statutory limitation, the Board of Governors can delegate their powers andduties to committees or the Headteacher. Where this is done, ultimate responsibility remainswith the Governing Body as a whole.

External Audit and the Audit Commission

Schools are subject to external audit by auditors appointed by the Audit Commission forLocal Authorities in England and Wales. The current external auditors to HertfordshireCounty Council are the District Audit Service.

The District Audit Service has direct responsibilities to the County Council, to the localtaxpayers and to the public at large. It operates to a strict Code of Practice that outlines itsresponsibilities in matters of legality, regularity and best value.

The external auditor’s powers to obtain documents and information are conferred by Section16 of the Local Government Finance Act 1982 as amended by the Local Government Act1988. This provides that the external auditor:

• shall have a right of access at all reasonable times to all such documents relating to thebody whose accounts are under audit as appear necessary for the purpose of theauditor’s functions under the 1982 Act

• is entitled to require from any person holding or accountable for any such documentsuch information and explanation as the auditor thinks necessary for the purpose of theauditor’s functions under the 1982 Act

• may require any such person to attend in person to give information or explanation orto produce any such document

• is entitled to require any officer or member of the body whose accounts are under auditto provide such information and explanations as appear necessary for the purposes ofthe auditor’s functions under the Act

• may require any such officer or member to attend in person to give the information orexplanation.

Financial Handbook for Schools Hertfordshire County CouncilPart I: Schools and the LEA's Financial Framework Page 5 RESO3514: April 2003

Her Majesty’s Chief Inspector of Schools

The School Inspection Act 1996 requires the “efficiency with which the financial resourcesmade available to schools are managed” are to be inspected under the arrangements set out byHer Majesty’s Chief Inspector of Schools in the Framework for Inspection of Schools.

The inspection of financial administration, as opposed to the wider aspects of efficientresource management, will be reported within the section on school management andadministration.

Judgements about the efficiency of financial control will be based on a self-reportingquestionnaire. In this, the Headteacher of a school can summarise the school’s currentpractice in financial administration and how it applies best value principles in its managementand use of resources. The judgements will also consider a copy of the most recent auditor’sreport. The information from the Headteacher will be validated by the inspectors' first-handevidence gained when reviewing the school’s procedures during the course of theirinspection.

The Governing Body and the Headteacher should consider and respond promptly to anyrecommendations made by inspectors. The Headteacher should also notify the registeredinspector of any suspected irregularity.

The Internal Audit Service

The Accounts and Audit Regulations 2003 require all local authorities to maintain anadequate and effective system of internal audit. Any officer of member of the authority mustprovide such documents, information and explanation, as the authority considers necessary forthat purpose.

The main role of Internal Audit is:

• to inspect regularly accounts of schools with delegated budgets as set out in the SchoolStandards 7 Framework Act 1998; the inspection is made in terms of the accuracy ofthe financial records kept and the adequacy of systems and controls in relation to thefinancial procedures at a school

• to review the arrangements for delegation and the management of a school's delegatedbudget

• to ensure that management arrangements exist to minimise the opportunity for fraudand to detect the results of any significant fraud

• to report findings to the Headteachers and Chair of Governors, makingrecommendations for improvement where appropriate.

Financial Handbook for Schools Hertfordshire County CouncilPart II: Scheme for Financing Schools Page 6 RESO3515 – Issue 3 : April 2003Contents

PART II SCHEME FOR FINANCING SCHOOLS

CONTENTSPage

Section 1 Introduction 7Section 2 Financial requirements: Audit 11Section 3 Instalments of budget share: Banking arrangements 19Section 4 The treatment of surpluses and deficit balances arising in 22

relation to budget sharesSection 5 Income 24Section 6 The charging of school budget shares 26Section 7 Taxation 29Section 8 The provision of services and facilities by the Authority 30Section 9 Private and Public Partnership projects 32Section 10 Insurance 33Section 11 Miscellaneous 34Section 12 Former grant maintained schools’ balances 38Section 13 Responsibility for repairs and maintenance 39Section 14 Power to provide community facilities 40

ANNEX

A Schools to which the Scheme will apply 48

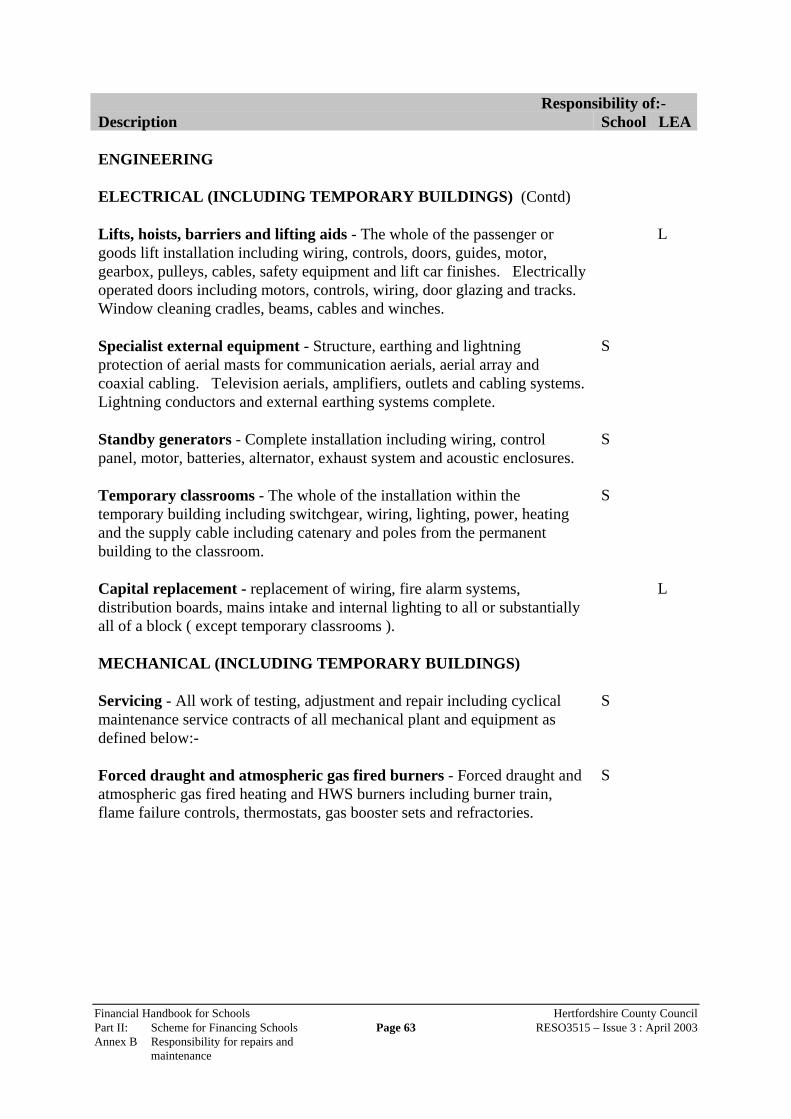

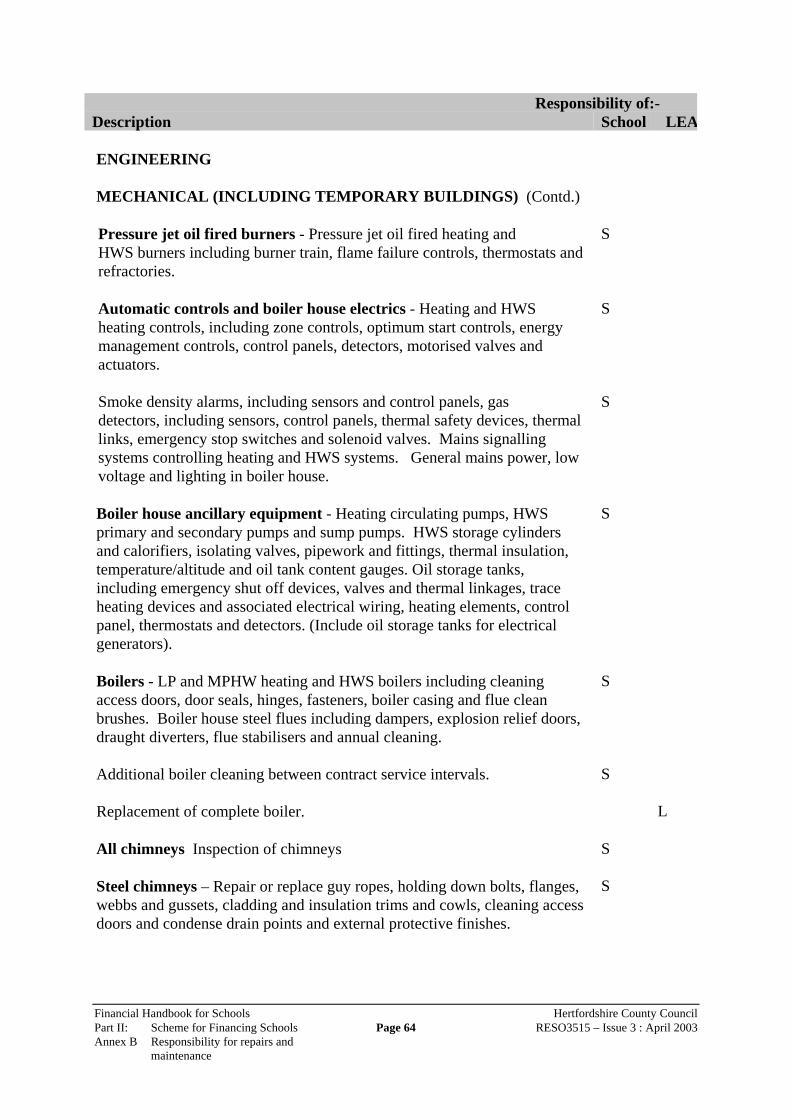

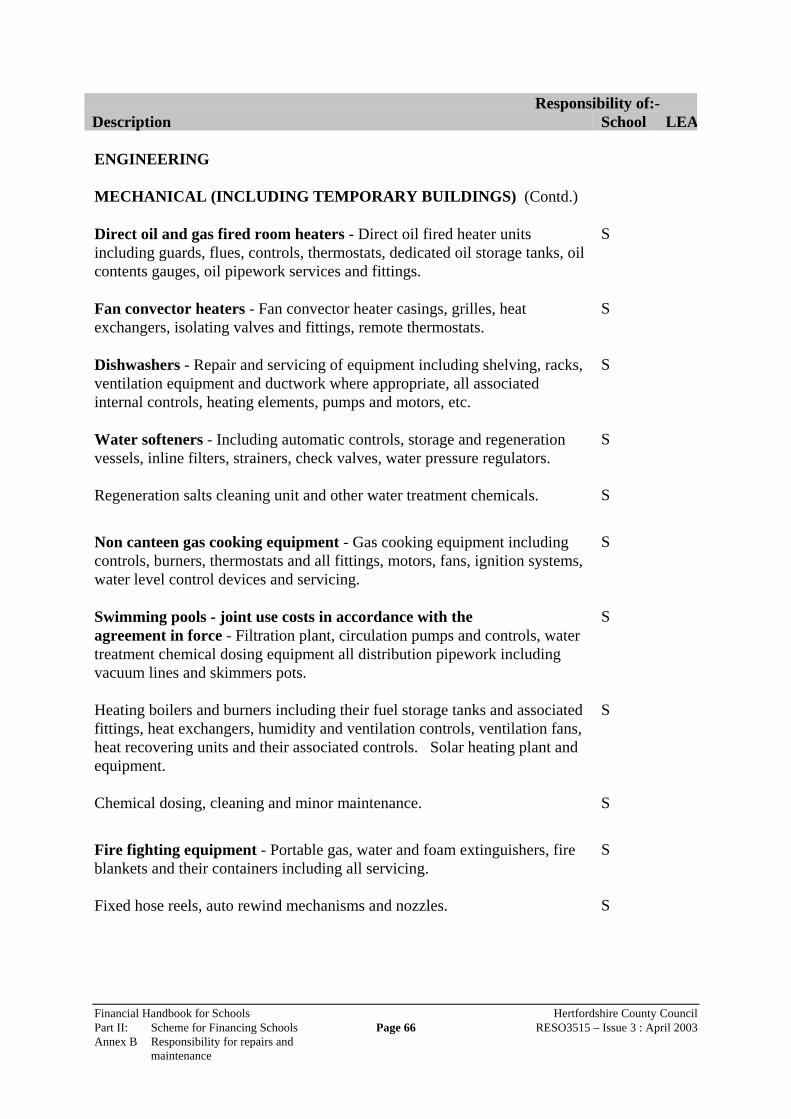

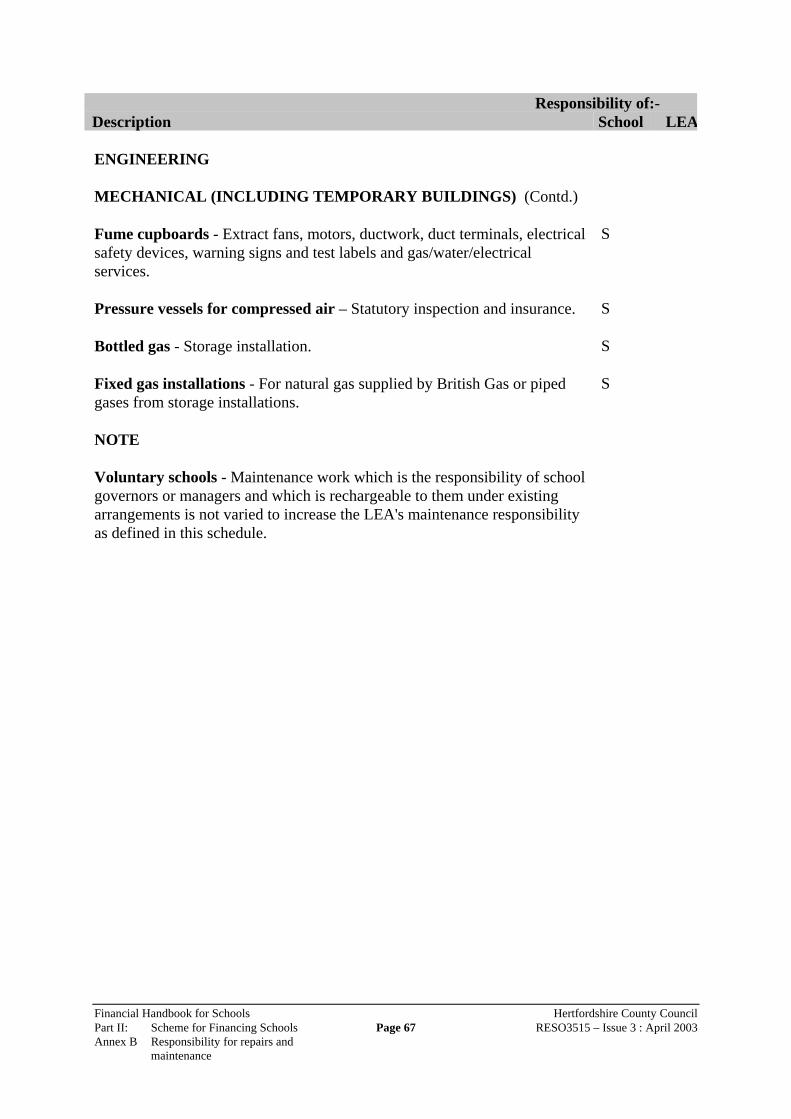

B Division of responsibility for building and grounds 56maintenance between the Authority and schools

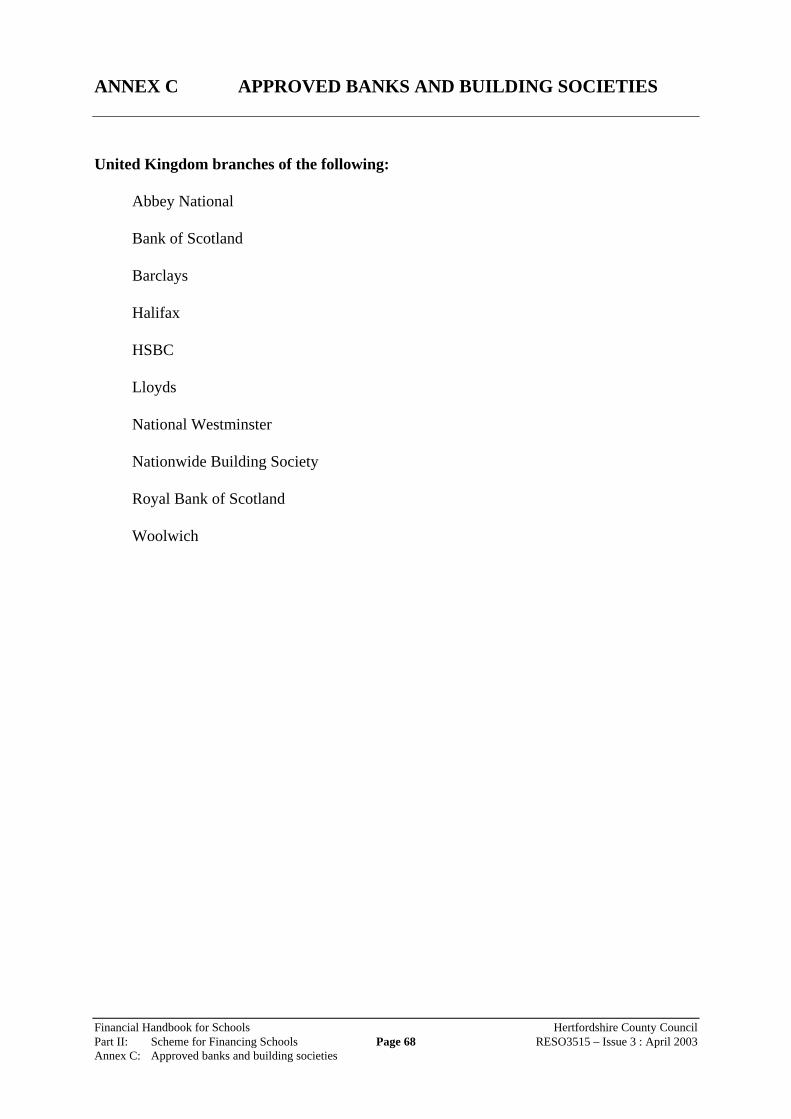

C Approved banks and building societies 68

D National Westminster Bank 70pooling arrangements for schools

E Health and Safety 72

F DfES Statement on Best Value and schools 5

G Fees to be deducted from teachers’ salaries andremitted to the General Teaching Council for England 7

Glossary to the Scheme for Financing Schools 9

7Financial Handbook for Schools Hertfordshire County CouncilPart II: Scheme for Financing Schools Page 7 RESO3515 – Issue 3 : April 2003Annex G: Fees to be deducted from teachers’

salaries and remitted to the GeneralTeaching Council for England

SECTION 1 INTRODUCTION

1.1 The Funding Framework

The funding framework that replaces Local Management of Schools is based on thelegislative provisions in sections 45-53 of the School Standards and Framework Act 1998.

Under this legislation, local education authorities determine for themselves the size of theirSchools Budget and LEA Budget – although the Secretary of State has power to require anLEA to increase its Schools Budget to a prescribed level. The categories of expenditurewhich fall within the two budgets are prescribed under regulations made by the Secretary ofState, but included within the two, taken together, is all expenditure, direct and indirect, on anAuthority’s maintained schools.

Local authorities may retain funding for purposes defined in regulations made by theSecretary of State under section 45a of the Act. The amounts to be retained centrally aredecided by the Authority concerned, subject to any limits or conditions prescribed by theSecretary of State. The balance of the Schools Budget left after deduction of centrallyretained funds is termed the Individual Schools Budget (ISB). Expenditure items in the LEAbudget must be retained centrally (although earmarked allocations may be made to schools).Local education authorities may retain an unallocated reserve within the ISB, but mustotherwise distribute the ISB amongst their maintained schools using a formula which accordswith regulations made by the Secretary of State, and enables the calculation of a budget sharefor each maintained school. This budget share is then delegated to the governing body of theschool concerned, unless the school is a new school which has not yet received a delegatedbudget, or the right to a delegated budget has been suspended in accordance with section 51of the Act. The financial controls within which delegation works are set out in a schememade by the Authority in accordance with section 48 of the Act and approved by theSecretary of State. All revisions to the scheme must also be approved by the Secretary ofState, who has power to modify schemes or impose one.

Subject to provisions of the scheme, governing bodies of schools may spend budget shares forthe purposes of their school. They may also spend budget shares on any additional purposesprescribed by the Secretary of State in regulations made under Section 50.

The Authority may suspend a school's right to a delegated budget if the provisions of theschool financing scheme (or rules applied by the scheme) have been substantially orpersistently breached, or if the budget share has not been managed satisfactorily. There is aright of appeal to the Secretary of State. A school's right to a delegated budget share may alsobe suspended for other reasons (section 17 of the School Standards and Framework Act1998), but in that case there is no right of appeal.

Each Authority is obliged to publish each year a statement setting out details of its plannedSchools Budget and LEA Budget, showing the amounts to be centrally retained, the budget

8Financial Handbook for Schools Hertfordshire County CouncilPart II: Scheme for Financing Schools Page 8 RESO3515 – Issue 3 : April 2003Annex G: Fees to be deducted from teachers’

salaries and remitted to the GeneralTeaching Council for England

share for each school, the formula used to calculate those budget shares, and the detailedcalculation for each school. After each financial year the Authority must publish a statementshowing out-turn expenditure at both central level and for each school, and the balances heldin respect of each school.

The detailed publication requirements for financial statements and for schemes are set out inregulations, but each school must receive a copy of the scheme and any amendment, and eachyear's budget and out-turn statements so far as they relate to that school or centralexpenditure.

Full details of the formula and centrally retained expenditure will be published in the Section52 Budget Statement, annually by 31 March.

1.2 The role of the scheme

The scheme is founded on seven principles:

• Raising standards in schools• Self-management for schools• Clear accountability of both LEA and school• Transparency of school finances• Opportunity for schools to take greater responsibility for management decisions• Equity between the new categories of community, voluntary and foundation schools• Value for money for schools and the LEA The scheme sets out the financial relationship between the Authority and the maintainedschools that it funds. It contains requirements relating to financial management andassociated issues, binding on both the Authority and on schools. 1.2.1 Application of the scheme to the Authority and maintained schools The scheme applies to all community, voluntary, foundation, community special and

foundation special schools maintained by the Authority. A list of all schools coveredby the scheme is shown at Annex A.

New maintained schools will be covered by the scheme by virtue of section 48 of the

Act. 1.2.2 Responsibility of the governing body

All governing bodies have full responsibility for the management of the school'sbudget and for the appointment and dismissal of teaching and non-teaching staff,taking into account the professional advice of the Director of Children, Schools &Families and the headteacher.

9Financial Handbook for Schools Hertfordshire County CouncilPart II: Scheme for Financing Schools Page 9 RESO3515 – Issue 3 : April 2003Annex G: Fees to be deducted from teachers’

salaries and remitted to the GeneralTeaching Council for England

Governing bodies are required:

• to spend their budgets in a manner which is consistent with the implementationof the National Curriculum; with the statutory requirements relating to thecurriculum as a whole, including religious education and worship;

• to operate an effective and efficient education service within the strategicframework set by the Authority for the benefit of their pupils;

• to operate within their budget share;• to meet the actual cost of all expenditure from their delegated budget.

The Authority will issue documents of instruction, advice and guidance, and will

otherwise provide support to governing bodies and headteachers to assist them in theexercise of their responsibilities, including advice on personnel and employmentissues. In particular, schools are referred to the documents listed in paragraph 11.10.

1.3 Publication of the scheme A copy of the scheme will be supplied to the headteacher and to the governing body of eachschool covered by the scheme, and any approved revisions will be notified to each suchschool. 1.4 Revision of the scheme Any proposed revisions to the scheme will be the subject of consultation with schools andwill require approval by the Secretary of State. 1.5 Delegation of powers to the headteacher The governing body is required to consider the extent to which it wishes to delegate itsfinancial powers to the headteacher, and to record its decision (and any revisions) in theminutes of the governing body. There are some powers that should not be delegated, inparticular approval of the annual budget. Further information on this is set out in Part IVSection 1 of Financial Handbook for Schools. Such decisions by the governing body will besubject to any requirements of regulations to be made under section 38 of the Act, andSchedule 11 thereto. 1.6 Maintenance of Schools The Local Education Authority is responsible for maintaining the schools covered by thescheme, and this includes the duty of defraying all the expenses of maintaining them (exceptin the case of a voluntary aided school where some of the expenses are, by statute, payable by

10Financial Handbook for Schools Hertfordshire County CouncilPart II: Scheme for Financing Schools Page 10 RESO3515 – Issue 3 : April 2003Annex G: Fees to be deducted from teachers’

salaries and remitted to the GeneralTeaching Council for England

the governing body). Part of the way an Authority maintains schools is through the fundingsystem put in place under sections 45 to 53 of the School Standards and Framework Act 1998.

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 11 RESO3515 - Issue 3: April 2003 Section 2: Financial requirements: audit

SECTION 2 FINANCIAL REQUIREMENTS: AUDIT 2.1.1 Application of financial controls to schools

Schools are required to abide in the management of their delegated budgets by theAuthority's requirements on financial controls and monitoring, not only those in theScheme but also those contained in the publications set out in section 11.10. In theevent of serious or persistent non-compliance, the Authority would exercise its right towithdraw delegation.

2.1.2 Provision of financial information and reports

Schools are required to provide the Authority each quarter with details of anticipatedand actual expenditure and income, at times determined by the Authority.

Current arrangements for the format of reports and the timetable for returns are set outin Part IV, Section 3 of the Financial Handbook for Schools. The Authority provides and supports software that allows forms to be processedautomatically in a required format.

2.1.3 Payment of salaries; payment of bills

All salaries, wages, fees and other remuneration due to staff and other individuals,whether under formal contract of employment or not, must be paid through a payrollsystem approved by the Finance Director.

The criteria defining a system acceptable to the Finance Director are set out in Part IV,Section 13 of the Financial Handbook for Schools.

Where the school seeks a payroll provider other than the County Council’s payrollagent, any costs, calculated on the basis of a published schedule, arising from theconsolidation of returns, including TPA, would be payable by the school.

Procedures for payment of salaries, wages and fees and other remuneration due to staffand other individuals are laid out in the Financial Handbook for Schools, Part IV,Section 13 and its Appendices. Regulations place a duty on the employer of teachers at maintained schools registeredwith the General Teaching Council (GTC) to deduct and remit the GTC fee in respectof a teacher who has not already paid the fee to the GTC, where the GTC has notifiedthe employer to deduct and remit the fee of that teacher. In order to ensure the performance of the duties to deduct and remit the fee imposedon employers by the Regulations, conditions are imposed on the Authority and

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 12 RESO3515 - Issue 3: April 2003 Section 2: Financial requirements: audit

governing bodies of all maintained schools covered by this Scheme in relation to theirbudget shares. Full details of these conditions are set out in Annex G on page 77.

The governing body should ensure procedures and best practice are exercised toobtain goods and services in the most cost effective way, from the cheapest sourcescommensurate with the required quality, performance and delivery. Purchasing by schools is subject to the Authority’s contract tendering procedures andto the Authority’s general regulations regarding purchasing which are covered by thePurchasing Conditions and Guidelines, Code of Purchasing Practice and ContractRegulations. These are set out in the Financial Handbook for Schools, Part IV,Section 9 Appendices A, B and C. Schools must adhere to the Authority’s proceduresfor placing orders for goods and services and the payment of accounts; these can befound in Part IV, Section 10 of the Financial Handbook for Schools.

The procedures will vary according to the position on delegation of funds and anybuyback of services which is in place.

2.1.4 Control of assets

Each school is required to maintain an inventory of its moveable non-capital assets, ina form to be determined by the Authority.

The governing body should authorise all write-offs and disposals of surplus stocks andequipment with a value above £500. All items for disposal above a predeterminedsum should be subject to competitive quotations.

Items of property, other than land or buildings, funded through the budget share maybe sold, where they are considered surplus to educational needs and where disposaldoes not interfere with the efficient running of the school. Any such disposal shall bemade at the best obtainable price and the funds should be re-deposited in the School’sGeneral Account. Other items may not be disposed of without the prior approval ofthe Director of Children, Schools & Families.

All disposals should be recorded. There may be a VAT liability in the sale proceeds.Further information is set out in Part IV, Section 12 of the Financial Handbook forSchools.

Thefts should be reported to departmental management and Internal Audit and, whereappropriate, the Insurance Officer and Police.

The governing body shall ensure that assets such as land, buildings, plant etc. aremanaged properly and are safeguarded against misuse, theft and undue deterioration. Governors cannot dispose of land and buildings; however the Incentive Scheme mayallow a governing body to take a share of the proceeds of such a sale.

Further regulations and standards on the control of assets and the content of aninventory record are provided in Part IV, Section 5 of the Financial Handbook for

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 13 RESO3515 - Issue 3: April 2003 Section 2: Financial requirements: audit

Schools. The inventory record should be kept up to date in terms of acquisitions,disposals, etc. and should be checked at least annually and certified correct.

2.1.5 Accounting Policies (including year-end procedures)

Schools are required to abide by procedures issued by the Authority relating toaccounting policies; these can be found in the Part IV, Section 3 of the FinancialHandbook for Schools and as issued by the Authority from time to time.

2.1.6 Writing off of debts

Schools are required to draw up a policy or procedure for dealing with any debtsleading, if necessary, to their write-off. Such a policy should ensure that staff areclear about how to deal with debts and that debtors receive consistent treatment. PartIV, Section 11 of the Financial Handbook for Schools provides guidance on this.

A debt may only be written off with the prior approval of the relevant officer or body,which depends on the amount of the debt as shown below:

• Up to £500 – the governing body may authorise a write off, where incomeaccrues to the school. Otherwise the approval of the Director of Children,Schools & Families is required, who will consult with the Finance Director.

• Over £500 – the governing body, with agreement of the Finance Director.

Where the governing body write off debts, these shall be formally recorded and therecord retained for seven years.

The County Secretary, who will advise on the correct course of action, may onlyinitiate legal action in respect of outstanding debts.

2.2 Basis of accounting Annual reports and accounts, including forecasts, furnished to the Authority must be on anaccruals basis. Quarterly reports may be on either an accruals or a cash basis. Further information is set out in Part IV, Section 3 of the Financial Handbook for Schools. 2.3 Submission of budget plans Each school must submit a plan to the Authority by 1 May showing its intentions forexpenditure in the current financial year and the assumptions underpinning the budget plan.This budget plan should take account of the estimated deficit/surplus at the previous 31March. Schools will be required to complete a revised budget forecast on each quarterlyreturn submitted to the Authority. This should take account of any virements made and thelatest financial information available to the school.

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 14 RESO3515 - Issue 3: April 2003 Section 2: Financial requirements: audit

The Authority will specify the format of the plan, and the current format can be found in thePart IV, Section 3 of the Financial Handbook for Schools. The Authority will publish, alongside the Budget Share information, guidance to schools onassumptions likely to be the same for all schools e.g. on inflation. These assumptions willalso be embedded in the software available. Part IV, Section 2 of the Financial Handbook forSchools, gives details of what schools can expect to receive at the same time as their budgetshares are issued. The Authority will supply schools with school income and expenditure data that it holds,which is necessary to the efficient planning by schools. This will be in the form ofmanagement information and Section 52 Budget and Out-turn Statements. 2.4 Best value The governing body of each school will be required to submit a statement, with its annualbudget return, setting out what steps it will be taking in the course of the year to ensure thatexpenditure, particularly in respect of large service contracts, will reflect the principles of thebest value regime. The DfES’s statement ‘ Best Value and Schools’ is attached as Annex F. 2.5 Virement Schools are allowed to vire freely between budget heads in the expenditure of their budgetshares. This does not apply to earmarked funds. 2.6 Audit: General The accounts of all schools with delegated budgets are subject to regular internal audit, andshould also be available for inspection as necessary by Hertfordshire’s external auditors(currently District Audit). In this respect schools will be audited within the regime set out inPart IV, Section 4 of the Financial Handbook for Schools. The auditors’ roles include: • the assessment of the adequacy of schools’ stewardship of public funds by recording

compliance with standards of financial management contained in this scheme, the , theCounty Council’s financial regulations and standing orders and the school’s owninternal control arrangements;

• assessing the achievement of value for money; and• investigation of fraud and irregularity. Whilst schools may be subject to direct external audit, generally speaking the District AuditService will assess the reliance it can place on the County Council’s Internal Audit Service to

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 15 RESO3515 - Issue 3: April 2003 Section 2: Financial requirements: audit

avoid duplication of effort, and will therefore not engage significantly in the inspection ofindividual schools’ accounts. Schools that contract with external payroll providers are expected to make provision withintheir contracts to allow access on the part of the LEA’s auditors to relevant records held bythe bureau, should such access prove necessary, and for reasonable co-operation to enable theLEA’s auditors to complete their enquiries effectively. The governing body and school staff are required to provide auditors and inspectors with anyexplanations the latter consider necessary in the performance of their duties. The headteacher should consider and respond promptly to the recommendations in audit andinspection reports and report directly to the governing body on the results of audit or anyaction to be taken by the school. The headteacher or governing body should immediately notify the Director of Children,Schools & Families of any suspected irregularity, who in turn should immediately inform theChief Internal Auditor. 2.7 Separate external audits A governing body may spend funds from its budget share to obtain external audit certificationof its accounts, separate from any Hertfordshire internal or external audit process. This auditwould need to take into account the status of the school as a spender of LEA funds, ratherthan a grant maintained institution. 2.8 Audit of voluntary and private funds Schools are required to provide to the Chief Internal Auditor an annual certified statement ofthe balances held by them in all private or voluntary funds, and of the accounts of any tradingorganisations, under the control of the governing body. The Chief Internal Auditor willspecify the format of this return. This requirement does not apply to Charitable Trusts or funds of separate organisations or management committees, such as parent teacher associations. Failure by a school to comply with this requirement by a date specified by the Chief Internal Auditor will constitute a breach of the scheme, and the Authority may takeaction on that basis. In addition, within the routine programme of audit visits, schools may elect for Internal Auditto review the effectiveness of the internal control procedures operating in relation to one oftheir private accounts without charge. Schools may purchase additional audit resources tocover any other accounts within their control. For accounts which schools have not elected to be audited by Internal Audit, the ChiefInternal Auditor may require that the annual certificate is certified by an appropriate qualifiedindependent person. This does not imply that the LEA requires access to such funds. 2.9 Register of business interests

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 16 RESO3515 - Issue 3: April 2003 Section 2: Financial requirements: audit

The governing body of each school is required to maintain a register which lists, for eachmember of the governing body and the headteacher, any business interests they or anymember of their immediate family have; the register must be kept up to date with notificationof changes and through annual review of entries, and must be made available for inspectionby governors, staff and parents, Authority auditors and Ofsted inspectors. A suggested formatfor the register and further guidance can be found in Part IV, Section 1, of the FinancialHandbook for Schools. 2.10 Purchasing, tendering and contracting requirements Schools are required to abide by the Authority's financial regulations and standing orders inpurchasing, tendering and contracting matters except where these would require schools:

• To do anything incompatible with any of the provisions of the scheme, or any statutoryprovision, or any EU Procurement Directive.

• To seek LEA officer countersignature for any contracts for goods or services for a valuebelow £60,000 in any one year.

• To select suppliers only from an approved list.• To seek fewer than three tenders or quotations in respect of contracts with a value

exceeding £10,000 in any one year. Schools should assess in advance, where relevant, the health and safety competence ofcontractors, taking account of the LEA's policies and procedures. Schools are required to achieve best value for money from all of their purchases. Thegoverning body must ensure that proper procedures and best practice are exercised to obtaingoods and services in the most cost-effective way. They must be purchased from the cheapestsources commensurate with the required quality, performance and delivery. There are variousways of establishing whether the prices being obtained are competitive. Consulting CountySupplies and Contract Services (CSCS), checking trade journals and catalogues and seekingquotations or formal tenders are all examples of good practice, depending upon the nature andvalue of the purchase concerned. Part IV, Section 9 and Appendices of the FinancialHandbook for Schools, highlights the procedure schools should adopt in testing the market. All payments to contractors should take into account the Authority’s procedures in connectionwith the Construction Industry Scheme (see 7.2). 2.11 Application of contracts to schools All Corporate contracts rely upon the commitment of participants throughout their term. Inthe case of contracts such as energy, or equipment maintenance and servicing arrangements,schools will have been given the opportunity to withdraw prior to any commitment beingentered into by the County Council. In these cases, schools will remain committed for the term of the contract. There will be no extension of the contract or any new commitmententered into by the Authority, on behalf of any school, without the agreement of the school.

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 17 RESO3515 - Issue 3: April 2003 Section 2: Financial requirements: audit

In the case of the payroll provider contract where the Authority has an existing commitmenton behalf of schools, a school may only withdraw from the contract if it meets the conditionsset out in Part IV, Section 13 of the Financial Handbook for Schools (see 2.1.3) and givesfour months notice of its intention to withdraw. In all other cases the school may opt out of the relevant contract in accordance with thetermination notice required. 2.12 Central funds and earmarking The Authority is authorised to make sums available to schools from central funds, in the formof allocations that are additional to and separate from the schools’ budget shares (e.g. throughthe Standards Fund regulations). Such allocations will be subject to conditions showing thepurpose or purposes for which the funds may be used, as set out in the and/or regulations thatmay be published from time to time. Earmarked funding from centrally retained funds can only be spent on the purposes for whichit is given, or on other budget heads for which earmarked funding is given, and cannot bevired into the budget share. The Authority will recover funds that are not spent for thepurposes prescribed or not spent in the specified time period. All earmarked funds must bereported in the form laid down by the Authority. 2.13 Spending for the purposes of the school Governing bodies can spend their budget shares for the purposes of providing education for children on the school roll, as provided for in the School Standards & Framework Act 1998and other relevant legislation, and in the Articles of Government of the school. This willinclude expenditure on:

• the employment of staff• the upkeep and improvement of premises, including the cost of equipment and routine

repairs and maintenance• the provision of the curriculum• the general duties and responsibilities relating to the management and government of

the school Under section 50(3)(b) of the SSAF Act 1998 the Secretary of State may prescribe additionalpurposes for which expenditure of the budget share may occur. 2.14 Capital spending from budget shares The governing bodies can use their budget shares to meet the cost of capital expenditure onthe school premises. This includes expenditure by the governing body of a voluntary aidedschool on work that is its responsibility under paragraph 3 of Schedule 3 of the SSAF Act1998. The definitions of capital for this purpose are set out in Annex B. The governing bodymust notify the County’s Capital Programme Co-ordinator of all capital expenditure. Schoolsmust take into account any advice from the Director of Children, Schools & Families as to the

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 18 RESO3515 - Issue 3: April 2003 Section 2: Financial requirements: audit

merits of proposed expenditure which exceeds £12,000. If the County Council owns thepremises, the governing body should seek its consent to the proposed works. Schools are required to separately identify these works in any financial returns made to theAuthority.

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 19 RESO3515 – Issue 3 : April 2003 Section 3: Instalments of budget share: banking arrangements

SECTION 3 INSTALMENTS OF BUDGET SHARE: BANKINGARRANGEMENTS

3.1 Frequency of instalments The budget share will be made available to governing bodies on the following basis:

• For schools within the County Council pooled banking arrangements the budget share,less the interest deduction set out in paragraph 3.3, will be in one instalment on 1 Aprileach year (or the nearest bank day in April);

• For schools with other banking arrangements, instalments will be made on a monthlybasis preceded by an instalment paid on 1 April equivalent to 1/3 of the monthlyinstalment. Payment of equal monthly instalments will be made from April toFebruary with an instalment equal to 2/3 being made in March. These will be made onthe banking day closest to the 15th day of each month.

3.2 Proportion of budget share payable at each instalment

The whole of each school’s budget share, less any deduction for interest deduction if relevant,is paid into the school’s bank account in equal instalments in line with the frequencies set outin the preceding paragraph. The budget share includes all pay costs that are delegated toschools. All inflation and pay factors included in the budget share are set out in the budgetinformation sent out to schools as discussed in paragraph 2.3.

3.3 Interest deduction

For schools within the County Council’s pooled banking arrangement the Authority willdeduct from budget share instalments an amount equal to the estimated interest lost by theAuthority in making available the budget share in advance. The basis of the calculation of thisdeduction is as follows.

D = A x i ( 1 - i + i2)2 2 4

where D = the deductionA = the school’s budget sharei = the assumed rate of interest

No deduction will be made for schools outside the pooled arrangements.

The LEA will make no deduction, in respect of interest costs to the LEA, from payments toschools of devolved specific or special grant.

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 20 RESO3515 – Issue 3 : April 2003 Section 3: Instalments of budget share: banking arrangements

3.4 Bank and building society accounts

All Hertfordshire maintained schools have external bank accounts into which their budgetshare instalments are paid. Schools retain all interest payable on the account. Hertfordshireprovides a pooled arrangement for all bank accounts, in which all schools may participate.This arrangement is particularly beneficial for schools, and the details of it are set out inAnnex D.

New bank account arrangements may only be made with effect from the beginning of eachfinancial year.

3.4.1 Restrictions on accounts

The banks or building societies authorised to be used by schools for the purpose ofreceiving budget share payments are listed in Annex C. These are the ten top-ratedUnited Kingdom banks and building societies. This list will be reviewed on an annualbasis. However, former GM schools may nominate, as the account for budget sharepayments, the account used in 1998/99 for payments of annual maintenance grant bythe Funding Agency for Schools, even if it is not on the list contained in the scheme.

Any school closing an account used to receive its budget share and opening anothermust select the new bank or building society from the approved list, even if the closedaccount was not with an institution on that list.

All schools must notify the Head of School Resources of all banking arrangements.Schools should not set up bank accounts for official County Council funds and shouldnot invest County funds in any way other than in bank accounts set up through theHead of School Resources.

Schools may have accounts for budget share purposes, which are in the name of theschool rather than the Authority; however, the bank accounts within the pooledarrangement will be in the name of Hertfordshire County Council but specific to eachschool.

Money paid by the Authority and held in such accounts remains LEA property untilspent.

3.5 Overdrafts and borrowing by schools

Schools should not go into overdraft except in exceptional circumstances. If a schoolanticipates that this is likely to occur it should immediately inform the Head of SchoolResources. Any costs arising from this situation will be borne by the school.

Governing bodies may borrow money only with the written permission of the Secretary ofState. This requirement does not, however, apply to the Schools Loan Scheme (see paragraph4.9).

Financial Handbook for Schools Hertfordshire County Council Part II: Scheme for Financing Schools Page 21 RESO3515 – Issue 3 : April 2003 Section 3: Instalments of budget share: banking arrangements

3.6 Other provisions

A school must have a minimum of two and a maximum of four cheque signatories, one ofwhich must be the headteacher. A second signatory must be a senior member of staff e.g.deputy headteacher or a governor. This does not normally extend to the secretary or bursar,as this is unlikely to result in an adequate segregation of duties. However, in certaincircumstances where the secretary or bursar is not involved in payment processing andaccounting and provided that an adequate level of internal control is maintained they may be asignatory. No member of the governing body who is not an employee of the Authority or ofthe governing body may be authorised to sign cheques unless the school can demonstrate thatit has arranged insurance to indemnify the Authority against loss.

All cheques of £2,000 and above must be signed by the headteacher and another authorisedsignatory. Cheques below the value of £2,000 may be signed by the headteacher only or,where three or four cheque signatories are appointed, by any two of the other signatories.

All direct debit and standing order mandates must be signed by the headteacher and anotherauthorised cheque signatory. The bank will confirm the details with one of the authorisedsignatories before it is actioned.

A governing body may set a lower (but not a higher) limit than the £2,000 above whichcheques must be countersigned.

The Head of School Resources and her representatives will have full and immediate access toall documents and records relating to bank accounts. All documents and records, relating tobank accounts must be held in a form suitable for inspection by Internal Audit, external audit,the Inland Revenue, Customs and Excise and any other authorised persons.

Any discrepancy in the bank account, or any breach of the banking terms, must be reportedimmediately by the headteacher to the Head of School Resources.