financial condition reporting aashto audit conference, july 2015 oregon secretary of state audits...

TRANSCRIPT

Financial Condition Reporting

AASHTO Audit Conference, July 2015

OregonSecretary of State Audits Division

Gary BlackmerAudits Director

Overview

Why assess financial condition?

What does a report look like?–For Oregon–For its counties

Why assess financial condition?

• Identify emerging problems• Communicate complex ideas in a clear,

concise way• Extend the financial timeline beyond a

year or biennium• Recommend strategies to improve

financial condition

• Recognize improvements resulting from actions and decisions

• Identify potential audit areas• Show your audit agency’s commitment to

on-going monitoring, to assure the public• Get greater value out of the CAFRs

Introduction to the 2011 report by Secretary of State Kate Brown…

“It is my hope that the analysis provided by the Audits Division will give Oregonians and public officials the tools they need to understand the unfavorable trends the state experienced and identify potential solutions to forge a better future for our state and for our people.”

The most favorable trends are: – Oregon’s unemployment fund helped cover the needs of

many Oregonians during this deep recession, unlike many other states that are borrowing from the federal government to support the unemployed;

– Payments to state PERS retirees appear to be leveling out in recent years; and

– Oregon continues to see a declining rate of violent property crimes.

Unfortunately, less favorable trends are prevalent in this report: – Basic conditions for Oregonians have worsened with

increased unemployment, increasing poverty rates, and greater dependence on Medicaid and other public assistance;

– K-12 education costs have grown substantially in the past 9 years;

– Oregon’s Rainy Day Fund, created 3 years ago, has already been reduced by two-thirds; and

– Oregon has doubled its long-term debt over the last 9 years, limiting its future options.

• big problems can creep up on you• big problems take time to solve• setting goals and policies can prevent,

lessen problems

What does a report look like?

• Revenues• Expenditures• Long-Term Debt• Fiscal Health• Demographics

• Operational indicators are an additional report…

Or some variation on

these sections…

Approach• Apply the skills and insights of our financial

auditors to the task• International City and County Managers

Association published “Evaluating Financial Condition” in 1985 in response to the municipal bankruptcies in the 1980s.

• 36 indicators, which is more than necessary- GASB has more recent guidance

• Instead, identify 10-20 key indicators and put the extra effort into deeper analyses of any emerging trends.

Regular reporting

• State financial condition reports– 2011, 2013, 2015

• County financial condition reports– 2012, 2014

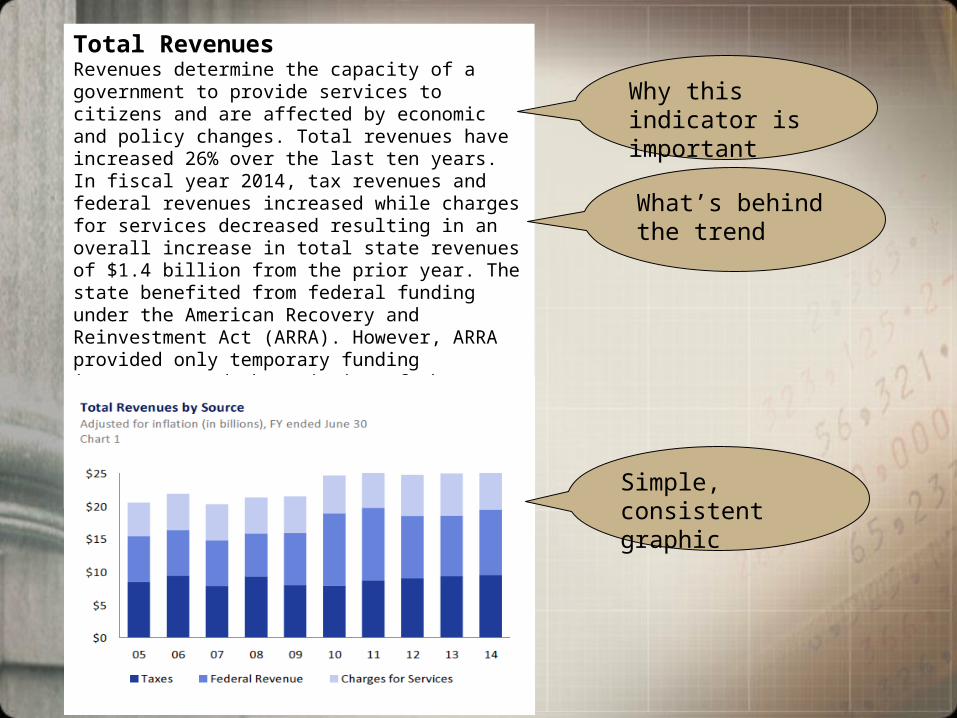

Total RevenuesRevenues determine the capacity of a government to provide services to citizens and are affected by economic and policy changes. Total revenues have increased 26% over the last ten years. In fiscal year 2014, tax revenues and federal revenues increased while charges for services decreased resulting in an overall increase in total state revenues of $1.4 billion from the prior year. The state benefited from federal funding under the American Recovery and Reinvestment Act (ARRA). However, ARRA provided only temporary funding increases, and the majority of those funds were spent in fiscal years 2010 and 2011. In 2014 declines in federal revenues included approximately $327 million in Unemployment Compensation and $73 million to Economic Development.

Why this indicator is important

What’s behind the trend

Simple, consistent graphic

What’s behind the numbers?Federal Revenues by Program AreaThe state received about $9.9 billion in federal assistance in FY14, an increase of $950 million from the previous year. Traditionally, the largest federal revenue source is for Medicaid in the human services program area, for which Oregon receives between $2.0 and $4.8 billion annually. Other large human services programs include Supplemental Nutrition Assistance Program (formerly known as food stamps) and Temporary Assistance to Needy Families.

Human Services

Education

University System

Transportation

Public Safety

Unemployment Compensation

Natural Resources

Lottery Operations

Administration

Other

Economic Development

Liquor Control

Interest on Long Term Debt

Judicial

Consumer and Business Services

State Hospitals

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

$9,880$4,421

$2,505

$1,556

$1,300

$832

$724

$494

$404

$400

$385

$384

$347

$340

$283

$279

Education

Human Services

Public Safety

Judicial

Administration

Natural Resources

Debt Service Principal

Interest

Legislative

Economic and Community Development

Transportation

Consumer and Business Services

Other Debt Service

0 1,000 2,000 3,000 4,000

$3,764 $1,723

$1,013

$308

$238

$128

$90

$58

$35

$29

$10

$5

$1

Total Expenditures by program

General Fund Expenditures by program

Long-term perspective on financial issues

Patterns emerge

Oregon’s Counties

• We had concerns about the finances of our partners

• After our state assessment, we began looking at counties

• Timber payments changed the game– How many counties, how much?– What actions have other states taken with financially-

troubled municipalities

Adapting to the loss of federal funds

• “Although Federal officials had repeatedly warned that the program would end…many municipal officials expected that the program would be reduced.

• ‘It's forcing a whole rethinking of municipal finances. Many municipalities are stuck. They have no choice but to cut back.’”

New York Times, January 31, 1987

Challenges

• How to conduct high-level financial reviews of local governments?– No agreement on the right indicators– No agreement on standards of financial condition– Without consistent accounting

10 indicators• Self-Support • Timber Payment Dependence• Debt Burden• Liquidity• Fund Balance• Retirement Benefit Obligation• Public Safety• Personal Income• Population Trends• Unemployment

ShermanGilliam

WheelerTillamook

MorrowHarney

MultnomahLincoln

GrantClatsop

ClackamasWallowa

DeschutesWashington

LakeCrook

WascoHood River

JeffersonKlamath

BakerUnion

ColumbiaYamhillBenton

LinnCoosCurry

JacksonUmatilla

MarionMalheurDouglas

PolkLane

Josephine

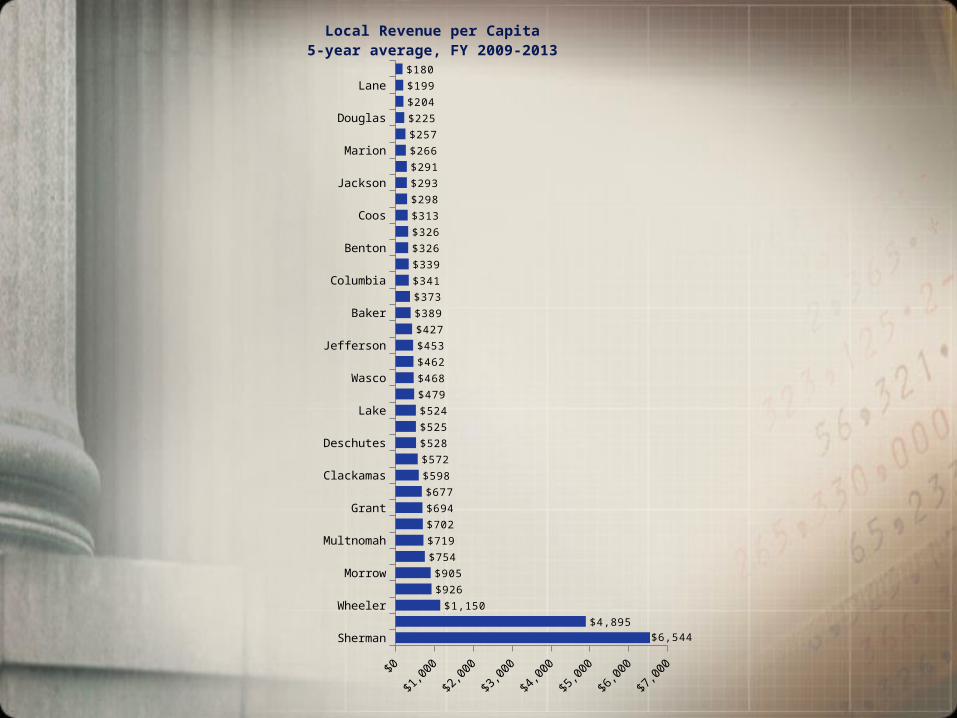

$6,544$4,895

$1,150

$926

$905

$754

$719

$702

$694

$677

$598

$572

$528

$525

$524

$479

$468

$462

$453

$427

$389

$373

$341

$339

$326

$326

$313

$298

$293

$291

$266

$257

$225

$204

$199

$180

Local Revenue per Capita5-year average, FY 2009-2013

Multnomah

Washington

Lincoln

Marion

Yamhill

Clackamas

Tillamook

Linn

Klamath

Benton

Columbia

Polk

Lane

Jackson

Coos

Curry

Douglas

Josephine

0% 5% 10% 15% 20% 25%

0.1%

0.1%

0.5%

0.6%

1.0%

1.0%

1.1%

2.4%

2.9%

4.0%

4.2%

4.5%

4.6%

7.9%

11.0%

13.8%

18.3%

19.7%

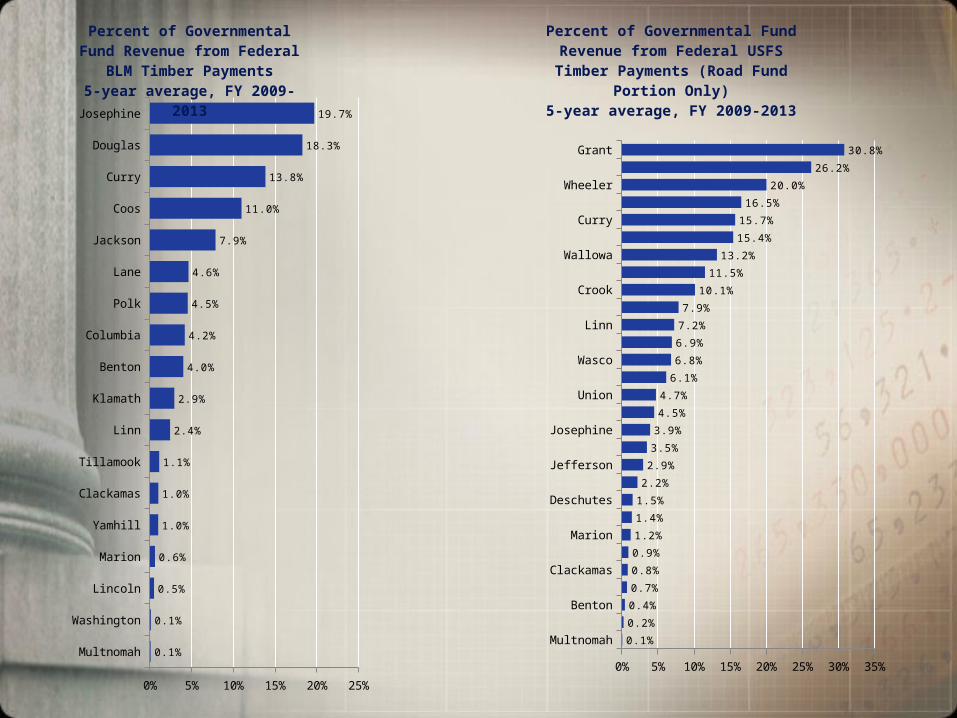

Percent of Governmental Fund Revenue from Federal BLM Timber

Payments5-year average, FY 2009-2013

Multnomah

Umatilla

Benton

Yamhill

Clackamas

Coos

Marion

Morrow

Deschutes

Jackson

Jefferson

Tillamook

Josephine

Lincoln

Union

Baker

Wasco

Lane

Linn

Hood River

Crook

Douglas

Wallowa

Klamath

Curry

Harney

Wheeler

Lake

Grant

0% 5% 10% 15% 20% 25% 30% 35%

0.1%

0.2%

0.4%

0.7%

0.8%

0.9%

1.2%

1.4%

1.5%

2.2%

2.9%

3.5%

3.9%

4.5%

4.7%

6.1%

6.8%

6.9%

7.2%

7.9%

10.1%

11.5%

13.2%

15.4%

15.7%

16.5%

20.0%

26.2%

30.8%

Percent of Governmental Fund Revenue from Federal USFS Timber Payments (Road

Fund Portion Only)5-year average, FY 2009-2013

Washington

Clackamas

Multnomah

Lane

Marion

Jackson

Deschutes

Yamhill

Linn

Josephine

Benton

Douglas

Polk

Umatilla

Columbia

Lincoln

Klamath

Coos

Jefferson

Curry

Crook

Hood River

Wasco

Union

Malheur

Tillamook

Morrow

Clatsop

Lake

Harney

Baker

Wallowa

Sherman

Gilliam

Grant

Wheeler

-50,000 150,000 350,000 550,000 750,000

489,721

299,364

284,993 230,349

221,479

147,800

140,713

67,916

64,348

56,273

56,155

54,301

50,748

36,192

26,883

25,252

24,660

20,595

16,504

16,252

11,699

10,555

10,258

8,363

8,217

6,769

6,642

6,494

1,291

1,147

105

(219)

(491)

(872)

(894)

(1,883)

Population Change, 1950 to 2013

1950 Population

Increase to 2013

CurryJosephine

DouglasCrookCoosBaker

KlamathHarney

GrantLincoln

LinnJackson

JeffersonLake

WheelerLane

BentonDeschutes

UnionTillamookColumbia

MalheurYamhillMorrowMarion

WallowaPolk

ClackamasMultnomah

GilliamClatsop

WashingtonUmatilla

ShermanWasco

Hood River

40% 50% 60% 70% 80% 90%

45%

48%

50%

52%

54%

55%

55%

55%

56%

56%

58%

58%

58%

59%

59%

59%

59%

59%

59%

60%

61%

61%

62%

63%

63%

63%

63%

64%

65%

65%

67%

69%

70%

70%

73%

82%

Labor Force Participation Rate2013 Estimate

Employed+Seeking employmentTotal Population over 16

Identifying counties to watch

• On the weak end of the range for several indicators

• Extra weighting for dependence on federal funds

ColumbiaCoosCurryDouglasJacksonJosephine

LaneLinnPolk

Douglas County

• Overview• County response• Indicators – 10 year trends

Douglas overview• Approximately 50% of Douglas County’s 5,071 square miles

is public land, with forest products and agriculture being key to its economy. The selected financial management indicators show that the county has sound debt management practices and one of the largest fund balances among counties. The indicators also show that Douglas County has strong liquidity and has experienced steady population growth over the past several decades.

• The county levies the fourth lowest property tax rate in Oregon, which limits its ability to generate local revenues. It is the most dependent among counties on federal timber payments, has high unemployment, and a high pension obligation per capita.

County Response• Douglas County has responded to the loss of a safety net

by reducing budgets, service levels and personnel services until a permanent revenue solution is found. The County continues to budget the use of reserves at levels that are not sustainable. Based on current spending patterns, in approximately two years, the County’s General Fund will need to reduce service levels and expenditures to balance the budget with current revenues. Minimum reserve levels needed for operating cash requirements will be reached near that time.

Local revenue per capitaadjusted for inflation

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

$0

$50

$100

$150

$200

$250

$300

$350

$400

$231

$256$273

$320

$280

$255

$230 $230$216

$236

Fund balanceadjusted for inflation

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

$0

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

$70,000,000

$80,000,000

$90,000,000

$100,000,000

Total General Fund Expenditures Unrestricted General Fund Balance

2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

20,000

40,000

60,000

80,000

100,000

120,000

10-Year Population Trend

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0%

5%

10%

15%

20%

9.2%

8.2%7.5% 7.7%

9.9%

15.3%14.6%

13.2%

12.2%

10.9%

County Unemployment RatesSeasonally adjusted average

Strategies of other states

• Monitoring– State offices review financial statements– Some track indicators

• Proactive– Engage, advise, assist troubled municipalities

• Intervention– Prevent, react to financial crises– Highly controversial

Portland

Metro

Multnomah County

Why auditors?

• Management may resist this transparency• Auditors have the credibility• Good insights into finances, operations• Organizations never sustain these efforts