financial and investor reporting for aifs - ey.com · (or included in a disposal group that is ......

TRANSCRIPT

Financial and investor reporting for AIFsFinancial year-end 2017 warm-up9 November 2017

Page 2

Agenda

1. IFRS update

2. INREV update

3. Reporting process - trends

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 3

IFRS updates – December 2017

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 4

IFRS Hot topics contents

► Update on relevant IFRS Amendments applicable for 2017

► Update on IFRS Amendments not yet effective

► Update on relevant IFRIC staff papers

► Preparing financial statements for entity entered into liquidation

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 5

Update on relevant IFRS Amendments applicable for 2017but still subject to EU endorsement

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 6

Amendment to IAS 7 Statement of Cash Flows

► Effective for periods beginning on or after 1 January 2017

► Part of the IASB’s Disclosure Initiative to help better understand changes in an entity’s debt

► Requires entities to provide disclosures about changes in their liabilities arising from financing activities, including both changes arising from cash flows and non-cash changes (such as foreign exchange gains or losses).

► On initial application, entities are not required to provide comparative information

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 7

Amendments to IAS 12: Recognition of Deferred Tax Assets for Unrealised Losses

► Effective for periods beginning on or after 1 January 2017

► Clarification on the accounting for deferred tax assets for unrealized losses on debt instruments measured at fair value

► Requires entities to consider whether tax law restricts the sources of taxable profits against which it may make deductions on the reversal of that deductible temporary difference

► Provide guidance on how an entity should determine future taxable profits and explain the circumstances in which taxable profit may include the recovery of some assets for more than their carrying amount

► Requires a retrospective application, however on initial application, the change in the opening equity of the earliest comparative period may be recognised in opening retained earnings (or in another component of equity, as appropriate), without allocating the change between opening retained earnings and other components of equity. Entities applying this relief must disclose that fact.

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 8

Amendment to IFRS 12 Disclosure of Interests in Other Entities

► Clarification of the scope of disclosure requirements in IFRS 12

► Effective for periods beginning on or after 1 January 2017► Part of the Annual Improvements to IFRS Standards 2014-2016 cycle

► Disclosure requirements in IFRS 12, other than those in paragraphs B10–B16 (summarised financial information), apply to an entity’s interest in a subsidiary, a joint venture or an associate that is classified (or included in a disposal group that is classified) as held for sale

► May be relevant for investments in seed capital funds accounted for under IFRS 5

► Additional disclosure requirements within IFRS 5

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 9

Update on IFRS Amendments not yet effective

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 10

Update on IFRS Amendments not yet effective

► The following are the recent new/amended standards not yet effective and most relevant for AIF:

► IFRS 9 Financial Instruments (effective date 01.01.18)► The following are not yet endorsed by the EU

► Amendments to IAS 28 Investments in Associates and Joint Ventures (effective date 01.01.18)► Annual Improvements to IFRS Standards 2014-2016 Cycle

► Amendments to IAS 40: Transfers of Investment Property (effective date 01.01.18)► IFRIC 23 Uncertainty over Income Tax Treatments (effective date 01.01.19)► IFRS 16 Leases (effective date 01.01.19)

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 11

Amendments to IAS 28 Investments in Associates and Joint Ventures

► Clarification that measuring investees at fair value through profit or loss is an investment-by-investment choice

► An entity that is a venture capital organisation, or other qualifying entity, may elect, at initial recognition on an investment-by-investment basis, to measure its investments in associates and joint ventures at fair value through profit or loss

► If an entity that is not itself an investment entity has an interest in an associate or joint venture that is an investment entity, ► the entity may, when applying the equity method, elect to retain the fair value measurement applied by that

investment entity associate or joint venture to the investment entity associate’s or joint venture’s interests in subsidiaries.

► This election is made separately for each investment entity associate or joint venture, at the later of the date on which ► (a) the investment entity associate or joint venture is initially recognised; ► (b) the associate or joint venture becomes an investment entity; ► and (c) the investment entity associate or joint venture first becomes a parent

► Retrospective application

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 12

Amendments to IAS 40: Transfers of Investment Property

► Clarification of when an entity should transfer property, including property under construction or development into, or out of investment property

► A change in use occurs when the property meets, or ceases to meet, the definition of investment property and there is evidence of the change in use. A mere change in management’s intentions for the use of a property does not provide evidence of a change in use

► Entities should apply the amendments prospectively to changes in use that occur on or after the beginning of the annual reporting period in which the entity first applies the amendments

► An entity should reassess the classification of property held at that date and, if applicable, reclassify property to reflect the conditions that exist at that date

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 13

Summary of accounting for properties

Land and Buildings

Fixed assets for use inproduction/supply of

goods/services oradministrative purposes

Current assetsheld for sale

in the ordinarycourse of business

CurrentNon-Current

IAS 16 Property Plant Equipment

IAS 40Investment Properties

IAS 2Inventory

Revalue tofair value Cost Fair value

Lower of cost orNet Realisable Value

Yes

No – held to earn rentalsor for capital appreciation

• Revaluation surplus• Depreciation• Impairment (IAS 36)

• Depreciation• Impairment (IAS 36)

• Changes of fair values are recorded directly to income statement

Choose either and apply to all IPsOR

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 14

IFRIC 23 Uncertainty over Income Tax Treatments

► Clarification on the application of the recognition and measurement requirements in IAS 12 Income Taxes when there is uncertainty over income tax treatments

► Does not apply to taxes or levies outside the scope of IAS 12, nor does it specifically include requirements relating to interest and penalties associated with uncertain tax treatments

► The Interpretation specifically addresses the following:► Whether an entity considers uncertain tax treatments

separately► The assumptions an entity makes about the examination

of tax treatments by taxation authorities► How an entity determines taxable profit (tax loss), tax

bases, unused tax losses, unused tax credits and tax rates

► How an entity considers changes in facts and circumstances

► Retrospective application with certain reliefs

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 15

IFRIC 23 Uncertainty over Income Tax Treatments

► Entity A’s income tax filing in a jurisdiction includes deductions related to transfer pricing. The taxation authority may challenge those tax treatments. In the context of applying IAS 12, the uncertain tax treatments affect only the determination of taxable profit for the current period.

► Entity A notes that the taxation authority’s decision on one transfer pricing matter would affect, or be affected by, the other transfer pricing matters. Applying paragraph 6 of IFRIC 23, Entity A concludes that considering the tax treatments of all transfer pricing matters in the jurisdiction together better predicts the resolution of the uncertainty.

► Entity A also concludes it is not probable that the taxation authority will accept the tax treatments.

► Consequently, Entity A reflects the effect of the uncertainty in determining its taxable profit applying paragraph 11 of IFRIC 23.

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 16

Update on relevant IFRIC staff papers

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 17

Update on relevant IFRIC staff papers – issue on IFRS 10 for investment entities

► The Committee received four questions on the application of IFRS 10 to an investment entity:

► Does an entity qualify as an investment entity if it possesses all three criteria, but does not have one or more of the typical characteristics?

► Does an entity provide investment management services to investors if it outsources the performance of these services to a third party?

► To what extent can an investment entity provide investment-related services to third parties?

► Does a subsidiary provide services that relate to its parent investment entity’s investment activities by holding an investment portfolio as beneficial owner?

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 18

Update on relevant IFRIC staff papers – issue on IFRS 10 for investment entities (cont’d)

► Does an entity qualify as an investment entity if it possesses all three criteria, but does not have one or more of the typical characteristics?► YES!► IFRS 10.27 states that all criteria must be met► IFRS 10.28 states that characteristics do not need to be met

► Does an entity provide investment management services to investors if it outsources the performance of these services to a third party? ► Yes – this is not forbidden by IFRS 10 so IFRIC concluded that some or all such activities may be

outsourced

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 19

Update on relevant IFRIC staff papers – issue on IFRS 10 for investment entities (cont’d)

► Can an investment entity provide investment-related services to third parties? To what extent?► Yes – can be substantial► B85C specifically allows this as long as such services are ancillary to its core investing activities

► Does a subsidiary provide services that relate to its parent investment entity’s investment activities by holding an investment portfolio as beneficial owner?► No – the same response given to the same request in 2014!

► Overall IFRIC decided (rightly) that nothing further was needed on any of these questions …

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 20

Update on relevant IFRIC staff papers – issue on IAS 12 Deferred tax initial recognition exemption

► How, in its consolidated financial statements, an entity accounts for a transaction in which it acquires all the shares of another entity that has an investment property as its only asset

► In the fact pattern submitted► the acquiree had recognised in its statement of financial position a deferred tax liability arising from

measuring the investment property at fair value. The amount paid for the shares is less than the fair value of the investment property because of the associated deferred tax liability

► The transaction described in the submission does not meet the definition of a business combination in IFRS 3 Business Combinations because the acquired entity is not a business

► The acquirer applies the fair value model in IAS 40

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 21

Update on relevant IFRIC staff papers – issue on IAS 12 Deferred tax initial recognition exemption (cont’d)

► The Committee noted that:► Because the transaction is not a business combination, paragraph 2(b) of IFRS 3 Business

Combinations requires the acquiring entity, in its consolidated financial statements, to allocate the purchase price to the assets acquired and liabilities assumed; and

► Paragraph 15(b) of IAS 12 says that an entity does not recognize a deferred tax liability for taxable temporary differences that arise from the initial recognition of an asset or liability in a transaction that is not a business combination and that, at the time of the transaction, affects neither accounting profit or loss nor taxable profit (tax loss)

► Accordingly, on acquisition, the acquiring entity recognises only the investment property and not a deferred tax liability in its consolidated financial statements. The acquiring entity therefore allocates the entire purchase price to the investment property.

► Refer to IAS 12 for additional guidance on subsequent measurement

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 22

Preparing financial statements for entity entered into liquidation

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 23

Preparing financial statements for entity entered into liquidation

► Chapter 4 Conceptual Framework► 4.1 The financial statements are normally prepared on the assumption that an entity is a going

concern and will continue in operation for the foreseeable future. Hence, it is assumed that the entity has neither the intention nor the need to liquidate or curtail materially the scale of its operations; if such an intention or need exists, the financial statements may have to be prepared on a different basis and, if so, the basis used is disclosed.

► Accounts are prepared on a liquidation basis

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 24

INREV updates

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 25

Flow and charging of services to the vehicle and its investors

► The picture below shows the different stakeholders and the flow of services charged to the vehicle and its investors.

*In case of REIT structures management fee mechanics will be covered by staff costs.

Properties

Services (incl. outsourcing)

services

Expenses

Costs

Investment vehicle

Investment Manager*

Service providerIndependent expertse.g. auditor, external valuer

Service provider Contracted by manager e.g. accounting, debt raising, tax

Investors

LocalTaxAuthorities

Taxes

Taxes

Taxes

Taxes

Taxes

Fee Rebates

Fees e.g. performance

Net Return

Investments Costs Services

Fees Services

Expenses

Services(incl. outsourcing)

Fees Services

Costs Services

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 26

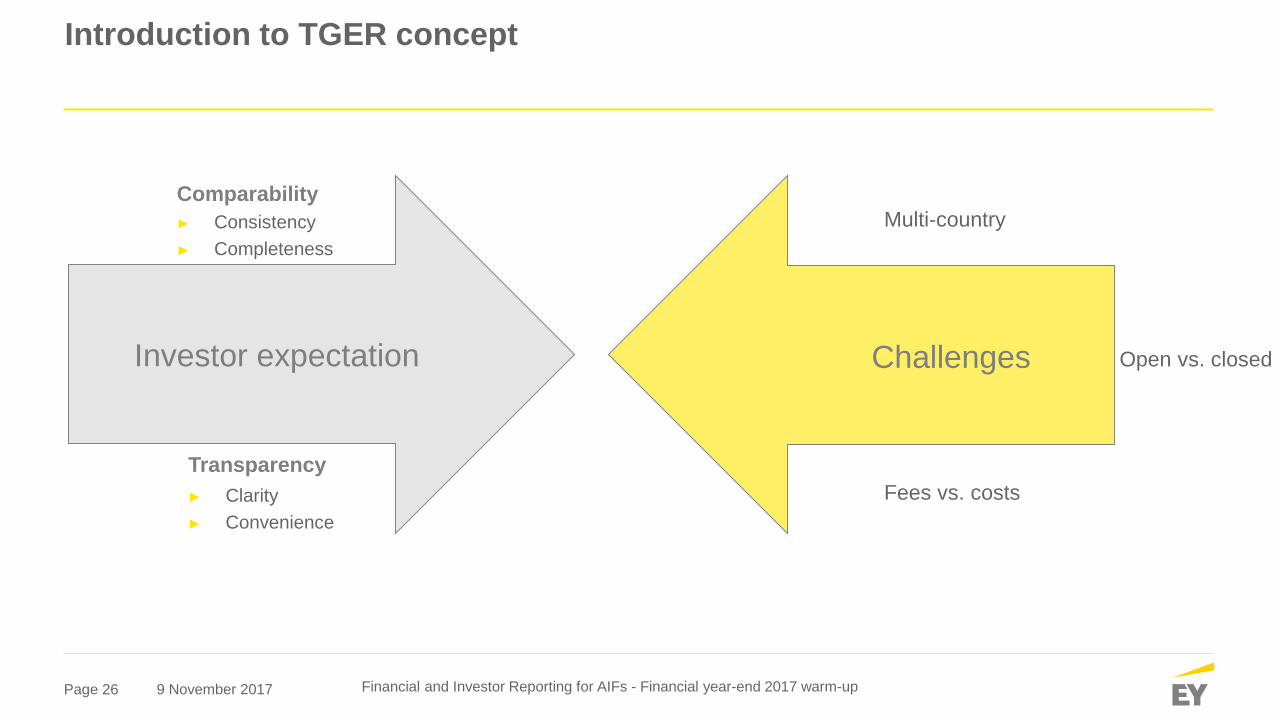

Introduction to TGER concept

Comparability ► Consistency► Completeness

Transparency ► Clarity► Convenience

Investor expectation

Multi-country

Fees vs. costs

Open vs. closedChallenges

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 27

Global Expense Ratio

GER =

Management fees (vehicle level) + Vehicle costs

Weighted average Gross Asset Value

Management fees (vehicle level) + Vehicle costs + Tax expenses

Weighted average Gross Asset Value

GERafter tax

=

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 28

Main Component of the Ratio

Global terminology established in project phase one: Costs describe 3rd party charges and fees describe manager charges.

•Fund and asset management fees charged by investment managers for their services regarding the management of the vehicle and its portfolio.

Ongoing Management Fees

•Fees charged by investment managers for their services regarding the entry/exit of investors and acquisition/disposition of real estate.

Transaction-based Management Fees

•Fees charged by investment managers after a predetermined investment performance has been attained. Performance Fees

•3rd party costs incurred predominantly at vehicle level to maintain and grow its operations.Vehicle Costs

•Expenses related to the tax structure and position of the vehicle.Tax Expenses

Total assets derived from Generally Accepted Accounting Principles (GAAP), adjusted for specific elements to arrive at a market-relevant gross asset value in accordance with INREV Guidelines / NCREIF PREA Reporting Standards.

Gross Asset Value

Fees charged by the Investment Manager

Costs charged by third parties

Ratio denominator

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 29

Consistent allocation- independent of investment hierarchy

Vehicle

Sub-Vehicle(tax blocker)

HoldCo(Investment)

HoldCo(Investment)

PropCo-SPV(Asset

Ownership)

Property

PropCo-SPV(Asset

Ownership)

Property

Audit costs

Audit costs

Audit costs

3X audit costs to include in

TGER

Investors

Investment

Assetownership

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 30

Consistent treatment of services

Who provides the services?

Investment Managere.g. accounting, debt arrangement 3rd party (Outsourced)

No double counting;already included in GER Include as separate expense to TGER

In lieu of 3rd party (Insourced) In addition to 3rd party

Charged via Fund Management fee?

Include as separate fee to TGER

Yes No

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 31

Indirect investments now fairly accounted for

Vehicle A expenses

Direct portfolio

Indirect investment / JV (40% ownership)

100%

40%

Proportional consolidation recommended

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 32

Transparency reaches new heights

Investment vehicle

Investment Manager

(Net) Performance Fee after clawbacks*

(Net) Fund Management Fee = Gross amount less -Fee Reduction

-Fee Waivers-Transaction Offsets

Rebate of Fund Management fee (e.g. due to significant investment)

Excluded from TGER (but potentially disclosed)

Investor C

2X Investment / Net return

Investor B

Investment / Net return

Investor A

Investment / Net return

Included in the ratioIncluded in GER Management Fee

Arrangements

*In some cases performance fee is earned by affiliate

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 33

Comparison with regional expense ratios

Total Expense Ratio (TER)

Real Estate Fee and Expense Ratio (REFER)

Global Expense Ratio(TGER)

Released in 2008 Released in 2013 Released (for consultation) in 2017

Vehicle level Fund level Vehicle level

NAV and GAV based NAV based GAV based

Management fees and 3rd party vehicle costs, before and after performance fees

Base and transaction management fees, performance fees, third party fees and expenses

Ongoing and transaction-based management fees (net of performance fees), 3rd party vehicle costs, tax expenses

Proportional consolidation recommended Proportional consolidation recommended Proportional consolidation recommended

All fees and costs within the structure are allocated based on the nature of the service rendered

Most fees and costs within the structure are allocated based on the nature of the service rendered

All fees and costs within the structure are allocated based on the nature of the service rendered

Excludes tax and financing expenses Excludes tax and financing expenses Excludes financing expenses, includes tax expenses

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 34

Disclosure

At Inception Annually Quarterly

Open end vehicles Required Optional

Closed endvehicles Optional Required Optional

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 35

Disclosure note 1

Global Expense Ratio %GAV

Before tax (note A)

After tax (note B)

The following notes clarify the components of the expense ratio and should also be read in conjunction with the classifications shown in the fees and costs matrix.

Constituent elements (Currency) Current period Prior period

Ongoing management fees

Transaction-based management fees

Performance fees

Vehicle costs

Corporate income taxes

Deferred tax liability

Weighted average GAV

A. Includes vehicle fees and costs, and any performance fees which have either been paid, accrued, or disclosed as a potential liability, in accordance with INREV Guidelines / NCREIF PREA Reporting Standards.B. Items included in A plus tax expenses.

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 36

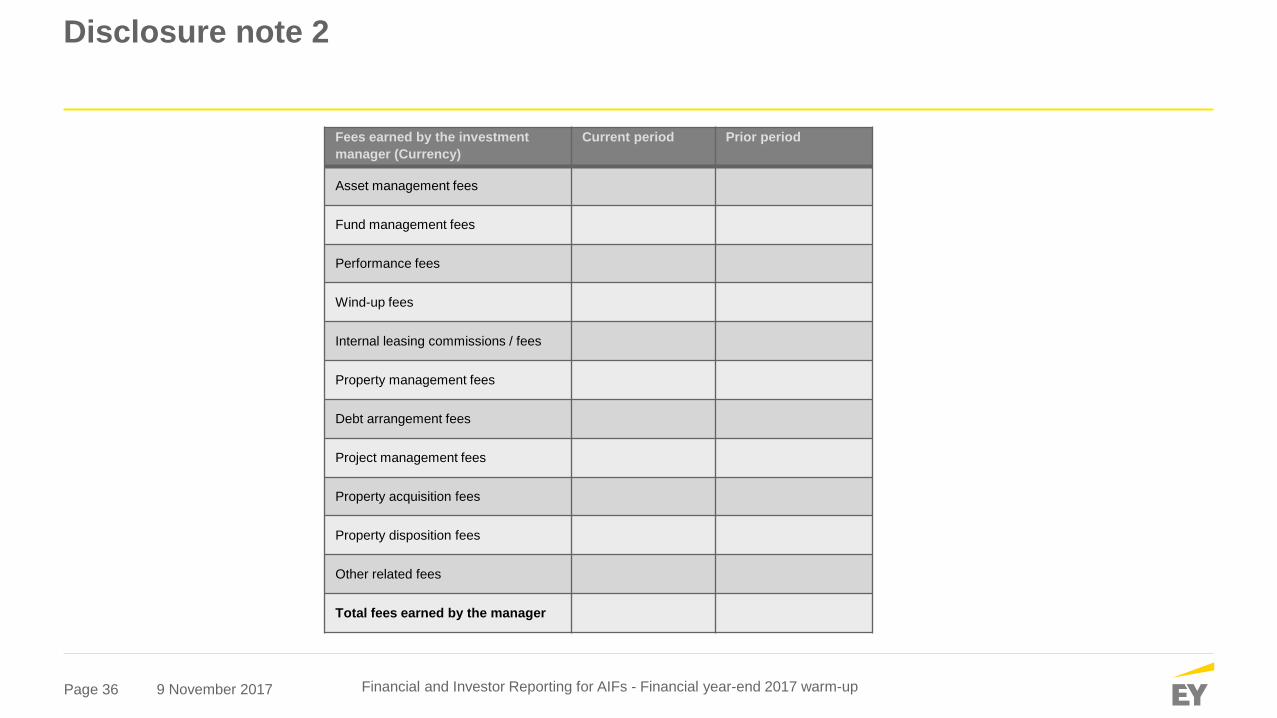

Disclosure note 2

Fees earned by the investment manager (Currency)

Current period Prior period

Asset management fees

Fund management fees

Performance fees

Wind-up fees

Internal leasing commissions / fees

Property management fees

Debt arrangement fees

Project management fees

Property acquisition fees

Property disposition fees

Other related fees

Total fees earned by the manager

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 37

Revamped Assessment Tool

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

► Shows level of alignment module by module

► Enables transparency and more appropriate disclosure

Page 38

SDDS version 3.1.

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 39

What’s next on INREV’s agenda

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

► Global standards in conjunction with NCREIF, PREA and ANREV► fee and expense metrics► global NAV► performance measurement

► Integrated digital platform (connecting the dots):► Global Definitions Database► Online SDDS & DDQ► Analytical tools

► Applied research: Open end fund pricing study

Page 40

INREV workplan

Other• Open ended focus group• Debt fund focus groud• Definitions (estimated Q4 2016)

Performance measuresPhase 2

• Net vs. gross performance• Property level performance (including Index)• Alignment with NCREIF/PREA

Reporting matters

• INREV balance sheet / income statement• SDDS upgrade• Alignment with NCREIF/PREA (focus on ratios)• Computation of weighting of NAV/GAV• Acquisition cost amortization

Fee and expense metrics

• Joint venture accounting• Still debat on the way to weight GAV• Additional KPIs:

• Total leakage• Tax• Financing

• Alignment with NCREIF/PREA

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 41

2017 Closing process feedback

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 42

Financial reporting process – blue print

Key inputs Key process outputs

Data collection Entity close & submission Consolidation Reporting & Filing

Analysis

Deals

► A

► B

► C

Close Checklist

► Detailed checklist for each department

► includes specific delivery dates and time

Production feedschedule

Synchronized production feed schedules to reduce data reporting errors

Chart of accounts

Data structure to capture transactional detail. Foundation for data analysis

► Property/asset management

► General accounting► FA and project

accounting► Treasury processes► Tax processes

Consolidation process

Budgeting and planning

Multi-Year planning

Statutory & management reporting

External reporting►Balance sheet► Income statement►Cash flow►Supporting

schedules

Internal reporting►Actual vs. Budget►Forecasting►Ad-hoc reporting

External entities►Group►Subsidiaries

Internal entities►Segments►BUs►Service lines

Financial statement preparation ► Subsidiaries submissions► Intercompany eliminations► Topside journal entries► Flash report creation

Consolidated financial

information

1a

1b2

5

7

6

4

3

Key areas to improve a closing process:• Start upstream to understand interdependencies• Tack progress • Route cause of issues to avoid downstream domino effect

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 43

Feedbacks from best in classes

Better support of management

Accelerated closing may help senior management make better business decisions by providing data more quickly and accurately.

Increased transparency and reliance

Accelerated closing increases the transparency of subsidiaries’ FSCP and reliance on financial results.

More efficient finance department

Accelerated closing gives finance departments the opportunity to work on additional tasks, partnering the business.

Improved employee motivation

Employees are able to be more motivated as unnecessary and time-consuming procedures are reduced by the acceleration.

Reduced investors’ perceived risk

Timely and accurate reporting meets external requirements and reduces investors’perceived risk.

OverallAccelerated closing satisfies internal and external needs, which brings transparency of FSCP and confidence in the financial statements, and creates a more efficient finance department.

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 44

EY’s approach when analysis financial reporting process

► We analyze issues and come up with possible resolutions of acceleration from three angles: process and accounting, technology, and people and organization.

► Our recommendation is to focus on process and accounting first, since it is likely to be more cost-effective than technology or people and organization.

TechnologyPeople andorganization

Process andaccounting

Area Improvement suggestion Cost

Process andaccounting

► Improve working procedures

► Reduce unnecessary procedures

► Spread workload across the month

► Introduce simplified accounting processes

► Coordinate the interests of internal departments and external stakeholders

Low

People andorganization

► Carry out adequate training programs

► Use SSC and outsourcing services

Moderate

Technology ► Optimize the process interface between different systems and review interface timing

► Integrate chart of accounts between parent company and subsidiaries

High

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Page 45

Q&A

9 November 2017 Financial and Investor Reporting for AIFs - Financial year-end 2017 warm-up

Thank you

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2017 Ernst & Young S.A.All Rights Reserved.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/luxembourg