financial analysis prime bank

TRANSCRIPT

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 1/21

“Financial Analysis”Prime Bank

Prepared For:

Anju-man-ara begum.Course Instructor

Money and Banking.

Course Code:

Prepared By:

Kazi Mohammad Maruf -ID.2002210000067Istiak Syeed Jenny-ID.2002210000081

A.B.M Khairul Alam Titash -ID.2002210000077

A.T.M Rashadul Karim Rana –ID.2002210000056

----------------------------

2nd Batch

Section-B

Date of submission -

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 2/21

25th August 2005

Anju-man ara

Course Instructor School of Business Studies

Southeast University

Dhaka.

Madam,

I am a student of school of Business Studies. I am about to complete the “ Banking ”

Course. Under this course I have done this financial analysis on Prime Bank. I haveworked hard to complete this term paper successfully. Today I am going to submit this

paper.

Yours truly

…………………

On Behalf of the Group

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 3/21

ACKNOWLEDGEMENT

We with due respect and honors, appreciate the help of our course

instructor of Banking Anju Man Ara. We must honestly say that it was

absolutely impossible for Us to complete this financial analysis without

your proper guidance and also very much thankful to you as he

provided with the information about the different banking functions,

services and others for the term paper financial analysis of Prime Bank.

We also like to thank our fellow classmate who gave us all the support

and once again thanks our madam for expending your valuable time for

us.

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 4/21

Origin

In this semester,fall 2006, we enrolled ourselves in the course Banking. This course has

a requirement for a Term paper. To fulfill this requirement of this course, we have

prepared this Term paper on financial analysis on Prime Bank as our Term paper’s topic.

Rationale of the Study

As a part of course Banking, we had the opportunity to prepare this term paper. The

reason for choosing this topic is we would like to expose the different features of our Course outline and by this we hope that we will be able to introduce ourselves about the

different banking system, functions and services. To full fill this purpose we have made

an effort to study thoroughly about the whole financial operations and transactions on

Prime Bank.

Objective of the study

As a student of Bachelor of business studies, we need in depth knowledge about the

different financial transaction of banks and other financial institutions. This study will

help us to learn about the different banking system, functions and operations. It will also

give us a clear idea about the different money and capital market instruments and will

increase our knowledge about the different aspects of financial transactions of banks and

other financial institutions.

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 5/21

Methodology

All the information has been collected from the Secondary source of information. We

have visited the SEU Library, collected annual report on Prime Bank,

Discussion paper, and web sites.

Limitations

Although we have tried to collect detailed information about Prime Bank and tried to give

proper information about the financial position and risk of the bank, but still we believe

that there might be some lacking in the secondary information/annual report of banks

financial reporting. So we could not collect all the factual material in a row.

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 6/21

Risk Analysis of Prime Bank

Year 2001 2002 2003 2004

Total Assets1573694250

32004770351

22424913064

23236161678

8

Cash asset 938096330 1366744576 1133517980 2247699221

Government securities 1601432100 1931233000 2633114400 2972210900

Total Shareholders Equity 1258263495 1526408120 1781863568 2239801912

Total Loans and advances 9074941476

1268684533

0

1649222440

5

2321967330

5

Total Deposits

1310987340

2

1617228788

0

2048322552

1

2806924265

0

Market Value of share 409.5 307.51 374.25 879.5

Number of shares outstanding 5000000 6000000 10000000 10000000

Net income After Tax 482985103 418144625 375455477 611938344

Earnings per Share 96.5970206 69.69077083 37.5455477 61.1938344

Dividend Paid 120000000 150000000 120000000 154000000

Annual Dividend Per Share 24 25 12 15.4

Credit Risk

Ratio of total loans to Total deposits 69.22% 78.45% 80.52% 82.72%

Liquidity Risk

Loans and advances to Total asset 57.67% 63.28% 68.01% 71.75%

Cash and Govt.Securiries to total assets 16.14% 16.45% 15.53% 16.13%

Market Risk

Price Earning Ratio 4.239261185 4.412492448 9.967892944 14.37236298

Dividend ratio 0.058608059 0.081298169 0.032064128 0.017509949

Earning Risk

Return on Asset(ROA) 3.07% 2.09% 1.55% 1.89%

Return on Equity(ROE) 38.39% 27.39% 21.07% 27.32%

Solvency Risk

Ratio of Equity capital to Total

Assets 8.00% 7.61% 7.35% 6.92%

CURRENT

MARKET

POSITION

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 7/21

TABLE OF CONTENT

1. INTRODUCTION

a. Brief history of Primes Bank 1-2

b. Current market position 3c. Function of banks 4

2. RESEARCH METHODOLOGY

a. Rationale of study 5

b. Objective of study 6c. Data collection Method 7

d. Limitation of study 8

3. ANALYSIS AND FINDINGS

A. Performance Evaluation

Return on asset 9

Return on equity 10

Net interest margin 11 Net non-interest margin 12

Employee productive ratio 13

Asset utilization 14

B. Risk Analysisa. Credit risk 15 b. Liquidity risk 16

c. Market risk 17

d. Earnings risk 18e. Solvency risk 19

4.CONCLUSION 20

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 8/21

APPENDIX

BACKGROUND OF PRIME BANK

Accordingly, Prime Bank Ltd. was created and commencement of business started on17th April 1995. The sponsors are reputed personalities in the field of trade and

commerce and their stake ranges from shipping to textile and finance to energy etc.

As a fully licensed commercial bank, Prime Bank Ltd. is being managed by a highly

professional and dedicated team with long experience in banking. They constantly focus

on understanding and anticipating customer needs. As the banking scenario undergoes

changes so is the bank and it repositions itself in the changed market condition.

Prime Bank Ltd. has already made significant progress within a very short period of its

existence. The bank has been graded as a top class bank in the country through

internationally accepted CAMEL rating. The bank has already occupied an enviable

position among its competitors after achieving success in all areas of business operation.

Prime Bank Ltd. offers all kinds of Commercial Corporate and Personal Banking

services covering all segments of society within the framework of Banking Company Act

and rules and regulations laid down by our central bank. Diversification of products and

services include Corporate Banking, Retail Banking and Consumer Banking right from

industry to agriculture, and real state to software.

The bank has consistently turned over good returns on Assets and Capital. During the

year 2004, the bank has posted an operating profit of Tk. 1146.14 million and its capital

funds stood at Tk 2476.06 million. Out of this, Tk. 1000 million consists of paid up

capital by shareholders and Tk. 1476.06 million represents reserves and retained

earnings. The bank’s current capital adequacy ratio of 10.74% is in the market and much

above the stipulated line of 9%. In spite of complex business environment and default

culture, quantum of classified loan in the bank is very insignificant and stood at less than

1.52%.

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 9/21

In order to retain competitive edge, investment in technology is always a top agenda and

under constant focus. Keeping the network within a reasonable limit, our strategy is to

serve the customers through capacity building across multi delivery channels.

PERFORMANCE ANALYSIS

RETURN ON ASSET (ROA)

The Return on asset of Prime bank for the year 2004 is,

Return on asset = Net income after tax / Total asset

= 611938344/32361616788

= 1.89%

The return on asset of prime bank 1.89% means if the Bank Tk.100 asset then it can

generate 1.89taka net income or the prime banks Tk.100 asset can generate Tk.1.89 netincome. In the same way we can calculate the other years ROA of Prime Bank . After

calculating all of the Prime banks ROA for the year of 2001,2002 &2003 we get 3.75%,

2.09% &1.55%. If we plot all the ROA

values according to the Y-axis and years

according to the X-axis then we will get the

Graphical figure of ROA for Prime bank.

But higher ROA indicates higher net income

in comparison to the total asset of a bank or

Proper asset utilization and lower ROA

indicates lower Net income in comparison to

the total asset or poor asset utilization. From

the Graph it is clearly understandable that the ROA of prime bank in 2001 was very high

3.07%

2.09%

1.55%

1.89%

0.00%

0.50%

1.00%1.50%

2.00%

2.50%

3.00%

3.50%

2001 2002 2003 2004

RETURN ON ASSET 2001 2002

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 10/21

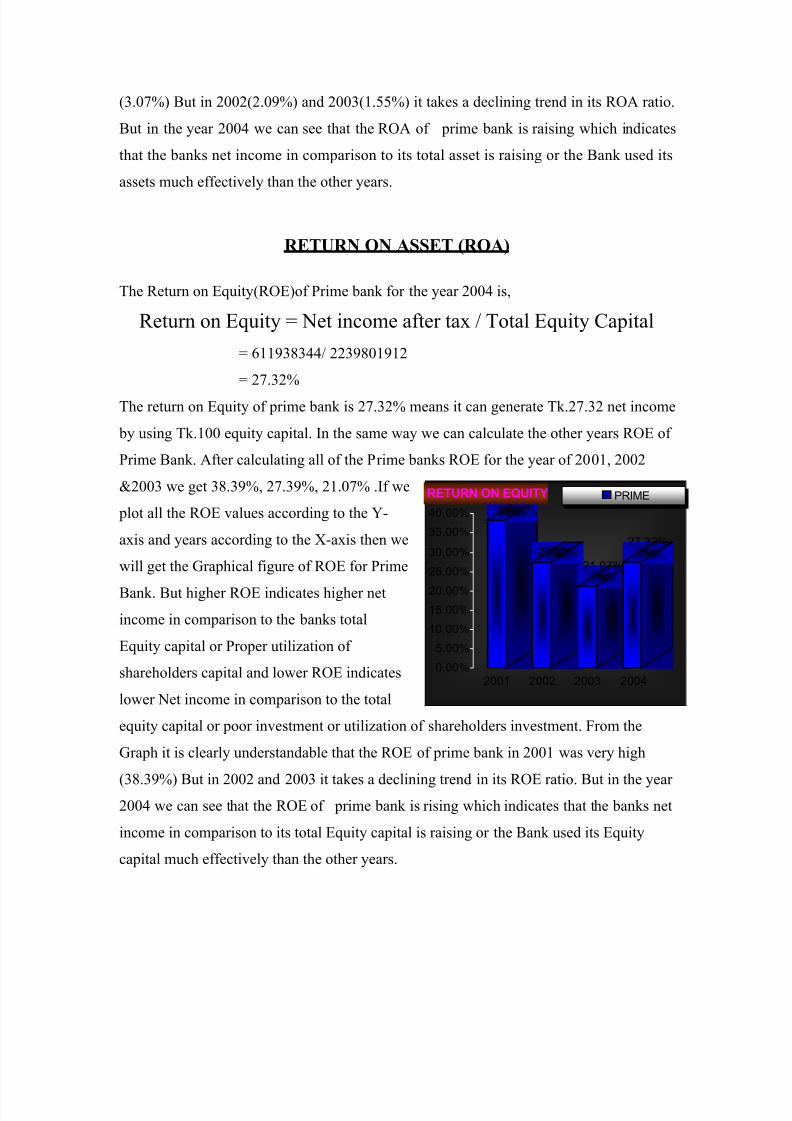

(3.07%) But in 2002(2.09%) and 2003(1.55%) it takes a declining trend in its ROA ratio.

But in the year 2004 we can see that the ROA of prime bank is raising which indicates

that the banks net income in comparison to its total asset is raising or the Bank used its

assets much effectively than the other years.

RETURN ON ASSET (ROA)

The Return on Equity(ROE)of Prime bank for the year 2004 is,

Return on Equity = Net income after tax / Total Equity Capital

= 611938344/ 2239801912

= 27.32%

The return on Equity of prime bank is 27.32% means it can generate Tk.27.32 net income

by using Tk.100 equity capital. In the same way we can calculate the other years ROE of

Prime Bank. After calculating all of the Prime banks ROE for the year of 2001, 2002

&2003 we get 38.39%, 27.39%, 21.07% .If we

plot all the ROE values according to the Y-

axis and years according to the X-axis then we

will get the Graphical figure of ROE for Prime

Bank. But higher ROE indicates higher net

income in comparison to the banks total

Equity capital or Proper utilization of

shareholders capital and lower ROE indicates

lower Net income in comparison to the total

equity capital or poor investment or utilization of shareholders investment. From the

Graph it is clearly understandable that the ROE of prime bank in 2001 was very high

(38.39%) But in 2002 and 2003 it takes a declining trend in its ROE ratio. But in the year 2004 we can see that the ROE of prime bank is rising which indicates that the banks net

income in comparison to its total Equity capital is raising or the Bank used its Equity

capital much effectively than the other years.

38.39%

27.39%

21.07%

27.32%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

2001 2002 2003 2004

RETURN ON EQUITY PRIME

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 11/21

NET INTEREST MARGIN The net interest margin of Prime bank for the year 2004 is,

(Interest income from loans and Securities

Net Interest Margin (NIM) = – Interest Expenses on Deposits and other Debts)

Total asset

2640910158 +196150200 - 1616184117

= ------------------------------------------------------32361616788

= 0.037726058

The Prime banks net interest Margin

0.033726058 means that the bank can

generate Tk.0.033726058 net interest

income by utilizing Tk.1 Asset.

In this way by calculating the NIM of

prime bank for the year 2001,2002 &

2003 we can get 0.04021,0.034 &

0.039 . Now,If we plot all the NIM values according to the Y-axis and years according to

the X-axis then we will get the Graphical figure of NIM for Prime Bank.

0.04021

0.03471

0.0391

0.03773

0.03

0.032

0.034

0.036

0.038

0.04

0.042

2000 2001 2002 2004

NET INTEREST MARGIN 2000 20012002 2004

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 12/21

NET NON-INTEREST INCOME

The Net-Non Interest Margin of Prime bank for the year 2004 is,

Net Noninterest Margin (NNIM) = (Noninterest Revenues – Noninterest Expenses)

Total Assets

= (749489244 – 824227141) / 32361616788

=0.002309461

The Prime banks net Non-interest

Margin -0.002309461 means that the

banks Non-interest expense is higher

than its Non-interest income.

In this way by calculating the NIM of

prime bank for the year 2001, 2002 &

2003 we can get 0.00784, 0.002596 &

0.002195. Now, if we plot all the

NNIM values according to the Y-axis and years according to the X-axis then we will get

the Graphical figure of NNIM for Prime Bank.

NET NON INTEREST MARGIN

0.00784 0.002596 0.002195

-0.00231

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

2001 2002 2003 2004

2001 2002 2003 2004

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 13/21

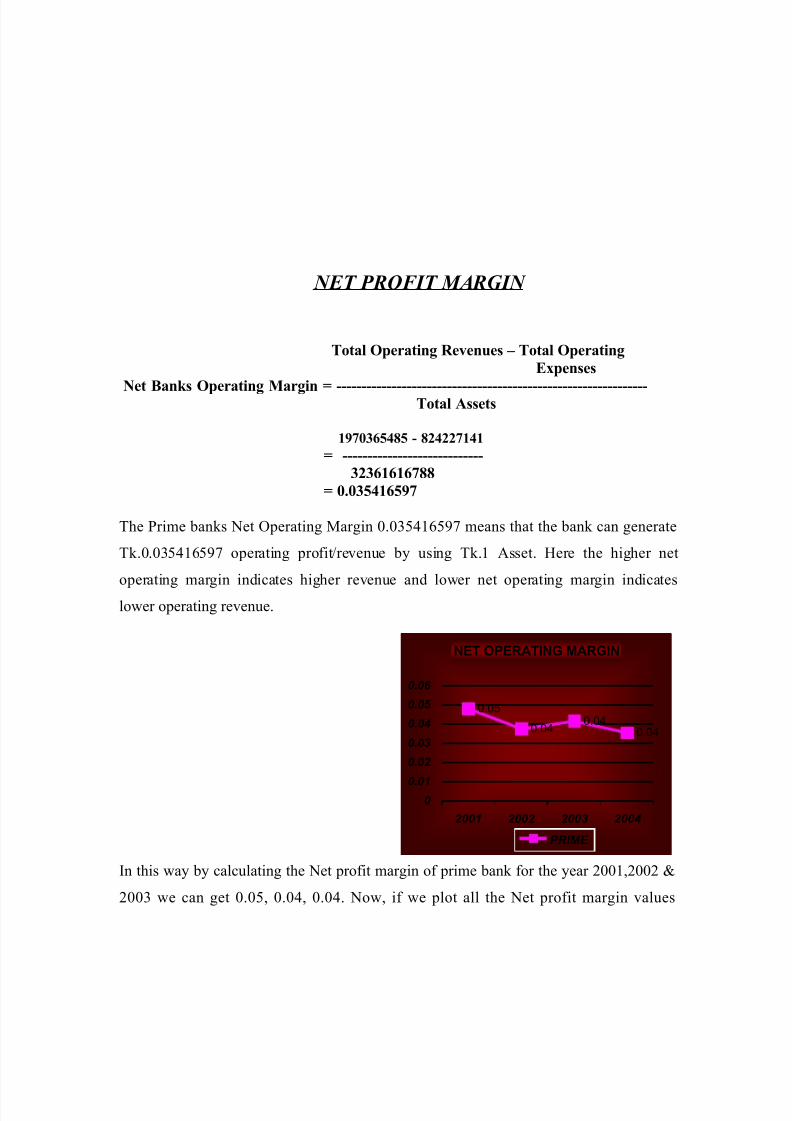

NET PROFIT MARGIN

Total Operating Revenues – Total Operating

Expenses

Net Banks Operating Margin = --------------------------------------------------------------Total Assets

1970365485 - 824227141

= ----------------------------

32361616788

= 0.035416597

The Prime banks Net Operating Margin 0.035416597 means that the bank can generate

Tk.0.035416597 operating profit/revenue by using Tk.1 Asset. Here the higher net

operating margin indicates higher revenue and lower net operating margin indicates

lower operating revenue.

In this way by calculating the Net profit margin of prime bank for the year 2001,2002 &

2003 we can get 0.05, 0.04, 0.04. Now, if we plot all the Net profit margin values

NET OPERATING MARGIN

0.05

0.040.04

0.04

0

0.01

0.02

0.03

0.04

0.05

0.06

2001 2002 2003 2004

PRIME

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 14/21

according to the Y-axis and years according to the X-axis then we will get the Graphical

figure of Net operating margin for Prim Bank.

ASSET UTILIZATION RATIO

The degree of asset utilization of Prime bank for the year 2004 is,

Asset Utilization = Total Operating Revenue / Total asset

= 1970365485 / 32361616788

= 0.060885879

The Prime banks degree of asset utilization or asset utilization ratio 0.06088 means that

the bank can generate Tk.0.060885879 operating profit/revenue by using Tk.1 Asset.

Here the higher ratio of asset utilization

indicates higher revenue and lower rate of

asset utilization indicates lower revenue.

In this way by calculating the degree of asset of prime bank for the year 2001,2002 &

2003 we can get 0.07, 0.06, 0.06 . Now, if we plot all the asset utilization values

according to the Y-axis and years according to the X-axis then we will get the Graphical

figure of degree of asset utilization for Prime Bank

ASSET UTILIZATION RATIO

0.07

0.06

0.07

0.06

5%

6%

6%

7%

7%

8%

2001 2002 2003 2004

PRIME

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 15/21

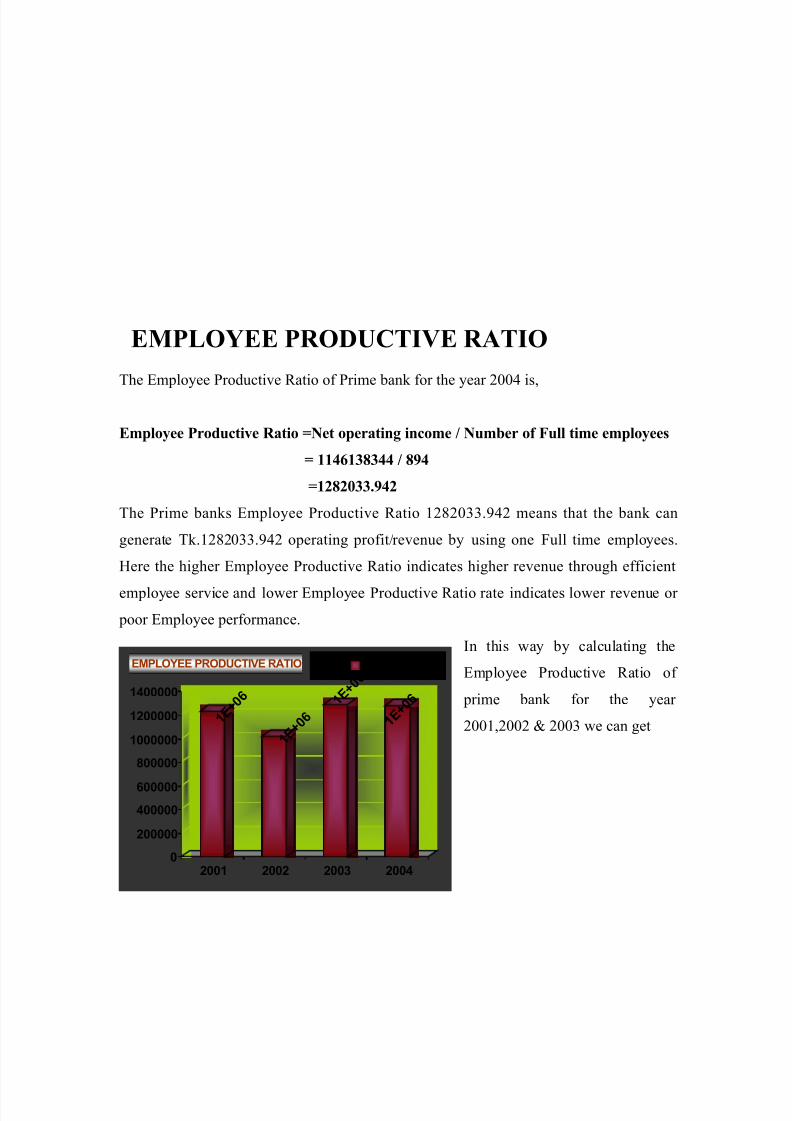

EMPLOYEE PRODUCTIVE RATIO

The Employee Productive Ratio of Prime bank for the year 2004 is,

Employee Productive Ratio =Net operating income / Number of Full time employees

= 1146138344 / 894

=1282033.942

The Prime banks Employee Productive Ratio 1282033.942 means that the bank can

generate Tk.1282033.942 operating profit/revenue by using one Full time employees.

Here the higher Employee Productive Ratio indicates higher revenue through efficient

employee service and lower Employee Productive Ratio rate indicates lower revenue or

poor Employee performance.

In this way by calculating the

Employee Productive Ratio of

prime bank for the year

2001,2002 & 2003 we can get 1 E + 0 6

1 E + 0 6

1 E + 0 6

1 E + 0 6

0

200000

400000

600000

800000

1000000

1200000

1400000

2001 2002 2003 2004

EMPLOYEE PRODUCTIVE RATIO ÿ /

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 16/21

1233422.1,1024444.7&1288816.5 . Now, if we plot all the

Employee Productive Ratio according to the Y-axis and years

according to the X-axis then we will get the Graphical figure of

degree of asset utilization for Prime Bank.

CREDIT RISK

RATIO OF TOTAL LOAN TO TOTAL DEPOSIT

The ratio of total loans to deposits of prime bank for the year 2004 is,

Total loans

Ratio of Total Loans to Total Deposits = --------------------

Total deposits

= 23219673305/28069242650

=82.72%

The ratio of total loans to total deposits of Prime bank 82.72% means that prime bank is

issuing Tk.82.72 loans against Tk.100 deposits or if the prime banks have TK.100 deposit

then it gives Tk.82.72 in loan. In this

way we can Calculate and explain

explain the other years Ratio of total

loans to total deposits of prime bank.

69.22%

78.45%

80.52%82.72%

60.00%

65.00%

70.00%

75.00%

80.00%

85.00%

2001 2002 2003 2004

RATIO OF TOTAL LOANS TO TOTAL DEPOSITSPRIME

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 17/21

After calculating all of the Prime banks ratio of total loans to deposits for the year of

2001, 2002 &2003 we get 69.22%, 78.45%, 80.52%. If we plot all the ratios of total loans

to deposits according to the Y-axis and years according to the X-axis then we will get the

Graphical figure of total loans to deposits for Prime Bank. But ratio of total loans to

deposits indicates higher net income and risk of default and lower total loans to deposits

ratio indicates lower Net income or lower risk gives more loans or invest most of its

deposits as loans than DBBL.

LIQUIDITY RISK

LOANS AND ADVANCES TO TOTAL ASSET The ratio of loans and advances to total asset of prime bank for the year 2004 is,

Loans and Advances to Total Assets = Loans and advances/ Total assets

= 23219673305 / 32361616788

= 71.75%

The ratio of loans and advances to total deposits of Prime bank 71.75% means that prime

bank is issuing Tk.71.75 loans against Tk.100 total asset or if the prime banks have

TK.100 asset then it gives Tk.82.72 in loan. In this way we can Calculate and explain the

other years Ratio of loans and advances to total asset of Prime bank.

57.67%

63.28%68.01%

71.75%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

2001 2002 2003 2004

LOANS AND ADVANCES TO TOTAL

ASSET PRIME

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 18/21

After calculating all of the Prime banks ratio of loans and advances to total asset for the

year of 2001, 2002 &2003 we get 57.67%, 63.28%, 68.01%... If we plot all the ratios of

loans and advances to total asset according to the Y-axis and years according to the X-

axis then we will get the Graphical figure of total loans to deposits for Prime Bank. Here,

the higher ratio of loans and advances to total asset indicates higher interest income from

loans and advances and higher risk of loan default and lower ratio of loans and advances

to total asset indicates lower interest income from loans and d advances or lower risk of

loan default.

EARNINGS RISK

ROA &ROE

After analyzing the ROA of Prime bank and DBBl we can clearly say that the position of

prime bank in term of return on asset is higher than DBBl which means that the prime

banks net income is higher than the than the net income of DBBL in comparison to its

total asset or the prime bank is more capable of generating higher revenue than DBBL.

But if we look at the Graph of ROE of DBBl then we will see that from 2001 to 2004 the

banks ROE is declining which indicates that the banks net income is decreasing or poor

utilization of shareholders equity.

So, after analyzing the ROA & ROE of Prime bank and DBBl we can clearly say that the

position of prime bank in term of return on Equity or Asset is higher than DBBl which

means that the prime banks net income is higher than the than the net income of DBBL incomparison to its total Equity capital/Asset or the prime bank is more capable of

generating higher revenue than DBBL. But as we know when there is higher return there

is higher risk. So, prime banks earning risk is higher than DBBL

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 19/21

SOLVENCY RISK

RATIO OF EQUITY CAPITAL TO TOTAL ASSET

The ratio of equity capital to total asset of Prime bank for the year 2004 is,

Ratio of equity capital to risk assets = Equity Capital/ Total Assets

= 2239801912 / 32361616788

= 6.92%

The ratio of equity capital to total asset of Prime bank 6.92% means that prime bank is

issuing Tk.82.72 loans against Tk.100 asset or if the prime banks have TK.100 depositthen it gives Tk.82.72 in loan. In this way

we can Calculate and explain the other

years Ratio of equity capital to total asset

of prime bank.

After calculating all of the Prime banks

ratio of equity capital to total asset for the

year of 2001, 2002 &2003 we get 8.00%,

7.61%, 7.35%. If we plot all the ratios of

equity capital to total asset according to

the Y-axis and years according to the X-axis then we will get the Graphical figure of

equity capital to total asset for Prime Bank. But higher ratio of equity capital to total asset

8.00%

7.61%

7.35%

6.92%

6.20%

6.40%

6.60%

6.80%

7.00%

7.20%

7.40%

7.60%

7.80%

8.00%

2001 2002 2003 2004

RATIO OF EQUITY TO TOTAL ASSET PRIME

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 20/21

indicates higher safe investment and profitability lower equity capital to total asset ratio

indicates lower risk

CONCLUSION

After analyzing the ROA & ROE of Prime bank and DBBl we can clearly say that the net

prime bank is higher which means the prime bank is more capable of generating higher

revenue than DBBL. But as we know when there is higher return there is higher risk. So,

prime banks earning risk is higher than DBBL Also the prime banks average Net interest

& Non-interest income is higher than the Dutch bangla bank. That why although the

prime bank is earning more interest from their loans but it is also in a higher risk of loan

default then the DBBL. So, the prime bank is in a higher credit risk and liquidity risk than

DBBl. But the liquidity risk of DBBl is lower than prime bank because they have enough

liquid assets in hand to meet short-term obligations than prime bank. Investing in prime

bank is more profitable and also risky for shareholders because of higher market value of

shares.

So, at last we have to say that in this case we need to do an portfolio investment means

investing in both the banks which will minimize the investment risk and will ensure more

safe return.

7/28/2019 Financial Analysis PRIME BANK

http://slidepdf.com/reader/full/financial-analysis-prime-bank 21/21