finances of housing chapter 7. lifestyle and choice of living how you spend your time and money will...

TRANSCRIPT

Finances of HousingChapter 7

Lifestyle and Choice of Living How you spend your time and money will

affect where you live Ask yourself

How close do you want to live to work? How long you plan to stay in one place? How much privacy would you like to have?

Opportunity Costs of Housing Choices

Housing decisions require trade-offs or opportunity costs

Consider what you might be giving up Buying a “handyman’s special” Building a new house Renting an apartment or house

Renting vs. Buying Based on your lifestyle – young, single, couple

with children, retired Housing for Different Life Situations

Based on financial factors Renting

Young adults, mobility, little maintenance, cheaper Buying

Stability, privacy, freedom, tax advantages, long-term investment

Advantages/Disadvantages of Renting/Owning

On-Campus Housing Dormitories

have roommate, or to self for extra charge lounges for TV and laundry convenient location, eating facilities small rooms

Sororities and Fraternities may require certain GPA or community service must be invited

Housing Cooperatives available on large campuses share in cleaning, cooking, maintenance rent less than regular dormitories

Central Michigan University

One Semester

Year

Tuition $5,370 $10,740

Room and Board

$4,106 $8,212

Total $9,476 $18,952

Based on 30 credit hrs, unlimited meal plan, $100 flex money

Does not include books, supplies, personal items $1,500+

Carey, Cobb, Troutman, Wheeler

•Coed by room •7 floors; elevators •1-bedroom suite shared by 4 people

•Private bathroom •Single beds

Campbell, Kesseler, and Kulhavi

Coed by room 5 floors; elevators 4 person, 4 bedroom, 2

bathroom suite Tobacco-Free Accessible accommodations

available

Movable bedroom furniture that may be lofted

No university furniture in shared living room

Air conditioned 30% additional room charge First-year students are not eligible for

this hall

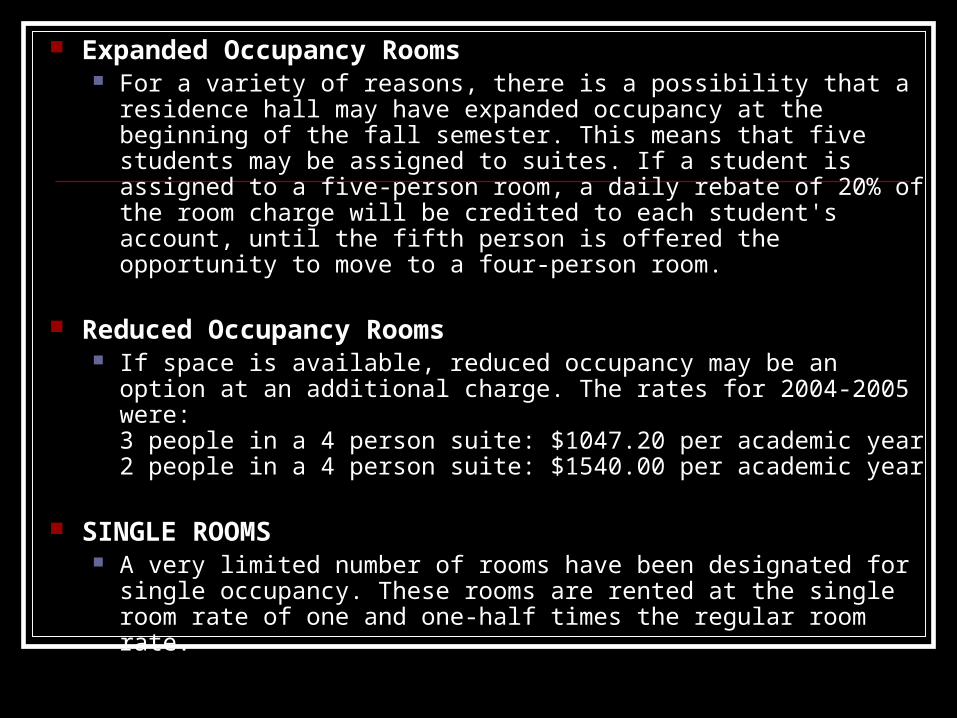

Expanded Occupancy Rooms For a variety of reasons, there is a possibility that a residence hall

may have expanded occupancy at the beginning of the fall semester. This means that five students may be assigned to suites. If a student is assigned to a five-person room, a daily rebate of 20% of the room charge will be credited to each student's account, until the fifth person is offered the opportunity to move to a four-person room.

Reduced Occupancy Rooms If space is available, reduced occupancy may be an option at an

additional charge. The rates for 2004-2005 were:3 people in a 4 person suite: $1047.20 per academic year2 people in a 4 person suite: $1540.00 per academic year

SINGLE ROOMS A very limited number of rooms have been designated for single

occupancy. These rooms are rented at the single room rate of one and one-half times the regular room rate.

SVSU

Year (28 credits)

Tuition $7,312

Room and Board$8,000

Books $1,200

Total $16,512

http://www.svsu.edu/housing/cost-payment-schedule.html

Michigan State University

In State Out of State

Tuition (15 credits/semester) $12,822 $31,692

FM Radio Tax $6 $6

Undergrad Tax $36.00 $36.00

State News Tax $10 $10

Housing $8,204 $8,204

$21,078 $39,948

Housing Information Sources Libraries Newspapers Internet Friends and family Real Estate agent Government agencies

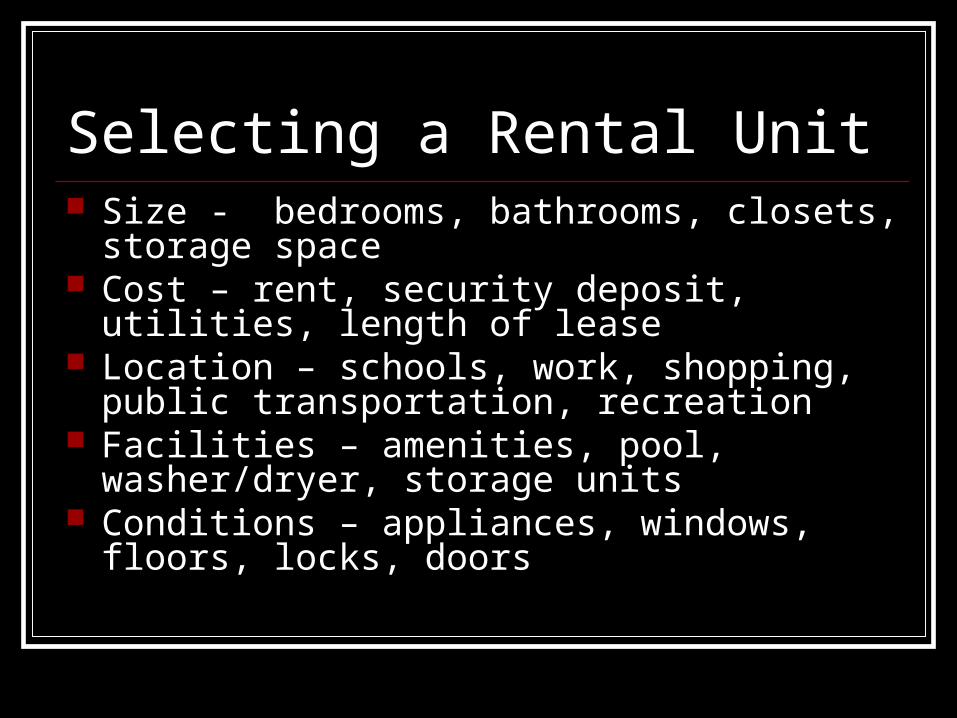

Selecting a Rental Unit Size - bedrooms, bathrooms, closets, storage

space Cost – rent, security deposit, utilities, length of

lease Location – schools, work, shopping, public

transportation, recreation Facilities – amenities, pool, washer/dryer, storage

units Conditions – appliances, windows, floors, locks,

doors

Advantages of Renting Greater mobility – don’t have to sell house

which could take months Fewer responsibilities – maintenance,

property taxes and insurance Low initial costs – no large down payment,

only deposit and first and last months rent

Disadvantages of Renting Financial restrictions – no tax deductions,

nothing to show for over time, rent could go up

Lifestyle restrictions - limited on what can be done in house; parties, noise, redecorating

Legal issues – sign a lease, legally binding contract; need to understand and agree with

Landlord/Tenant Responsibilities Landlord

Exterior is water and weather proof

Floors, walls, ceilings, stairs, railings are in good repair

Fire, safety, plumbing, electrical, heating, etc. regulations are met

Adequate door and window locks

Adequate water supply Buildings and grounds are

clean and sanitary

Tenant Read, understand, and

follow lease Pay the rent on time Give 30-60 days notice Keep premises in good

and clean condition Use premises for only what

is intended Allow landlord access to

make repairs or improvements

Obey the rules of the complex or living area

Rental Inventory Done to assure that you are not accused of

breaking, damaging, or taking inventory Inventory should list and describe the

conditions of the property Take inventory with landlord when you

move in and when you move out – each get a copy

Rental Inventory

Cost of Renting Location – the closer you are to conveniences the

more expensive Living space – larger means more $$, may have

to get a roommate Utilities – some included in rent Security deposits – pay when move in, get back if

there are no damages or unpaid rent Renters insurance – cheap, covers the cost of

property damages by fire, flood, etc – not covered by the landlord’s insurance

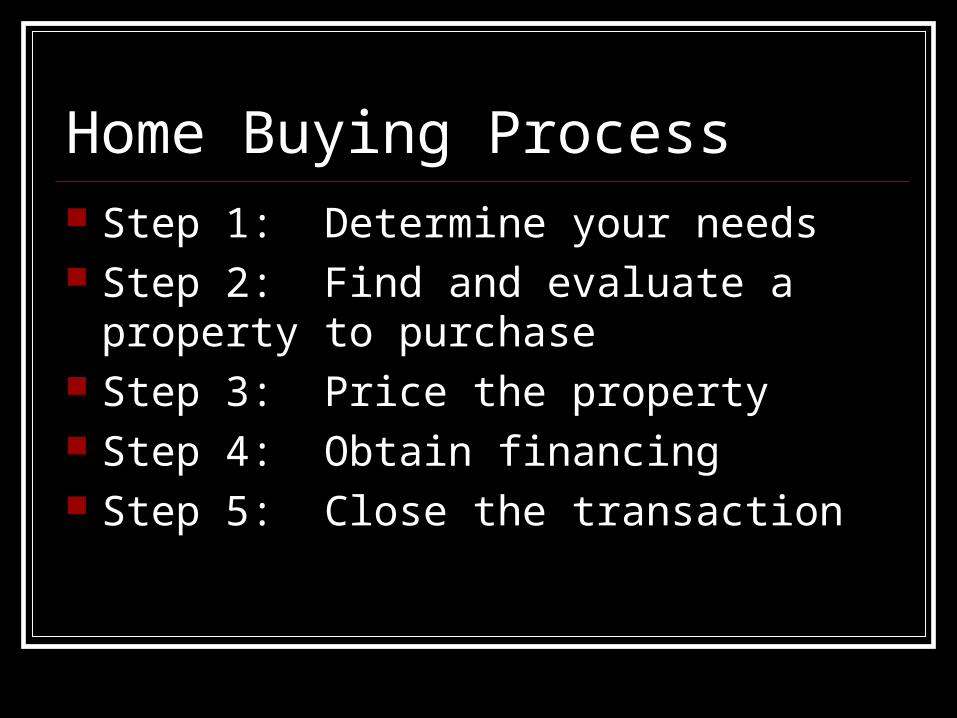

Home Buying Process Step 1: Determine your needs Step 2: Find and evaluate a property to

purchase Step 3: Price the property Step 4: Obtain financing Step 5: Close the transaction

Advantages of Owning Stability – no landlord to raise rent, sell, or

make you leave Sense of pride Freedom – can decorate, entertain how you

want Financial benefits – tax deductibles for

interest charges and property tax Investment – build equity, can always sell

Disadvantages of Owning Financial – have to save for down payment

and property value can go down Limited mobility – may take a long time to

sell High expenses – house payment,

insurance, taxes, maintenance and repairs

Types of Housing Single-family homes – most popular in US, most private,

most expensive Multiunit dwellings – duplexes and townhouses Condominiums – apts. or townhouses that are owned, pay a

monthly fee for maintenance, improvements, and insurance Cooperative housing – apt style building owned by nonprofit

group, monthly fee covers rent and operating expenses Prefabricated homes – manufactured and partially assembled Mobile homes – fully preassembled, very cheap, maybe

unsafe, and do not increase in value

Affordability and Your Needs Price and Down Payment

Down payment 10-20% of cost of house Amount depends on interest rates and economic

conditions Taxes and insurance

Size and Quality May have to start small and lower quality

Trading Up Experts say buy what you can afford, not necessarily what

you want, later after building equity “trade up”

Find and Evaluate Purchase Select location – country, city, neighborhood,

recreation, school system Hire a real estate agent – help you find home,

negotiate price, arrange financing, usually represent seller on a 3-6% commission

Conduct a home inspection – required in some states, check for problems, may also get an appraisal that does a value estimation of house Repair/Replacement Costs

Top 10 Defects Roof leaks due to flashing and valley problems Water penetration in the basement or crawlspace Electrical

safety issues due to age of home Deterioration of the wall material or substrate behind ceramic

tile in shower and tub areas Roof material failure due to age and deterioration Heating unit and distribution system inequities due to age and

workmanship or system compromises Structural issues due to improper construction and/or

alterations, or excessive unbalanced load (ie. Failing concrete block foundation wall)

Fire safety issues related to fireplace chimneys Termite and other wood destroying organisms On-site waste (septic) system failures usually due to lack of

maintenance

Determine Price of Home How long house has been on market? What have similar homes in area sold for? Is it a “seller’s market” or “buyer’s market”? Do the current owners have to sell in a

hurry? How well does the home fit your needs? How easily can you get good financing?

Negotiate Price Offer a price, owner may counteroffer –

always make first offer lower than what the most you would pay is

Sign a purchase agreement May have to pay “earnest money” to show

that offer is serious

Determine Amount of Down Payment

10-20%, may come from savings accts, sales of investments or assets, or gifts

Pay less than 20% down payment – will pay PMI insurance to protect lender if buyer cannot make payments

PMI is dropped once 20 – 25% of purchase price is paid

Qualifying for a Mortgage House loan paid back in 15, 20, or 30 years Lenders take your debt, income, and

savings and put it in a formula to see if and for how much you qualify for

Mortgage size can depend on interest rates which will affect the amount of your monthly payment

Mortgage Payments Payment was $739.02 Payment 1 - $646.88 went to interest, $53.14 to

principal, and mortgage insurance is $39.00 Payment 180 - $700.02 - $508.50 in interest,

$191.52 to principal , and mortgage insurance is none

Payment 359 - $700.02, $9.84 to interest and $690.18 to principal, no mortgage insurance

Mortgages Payments Greatest financial obligation most people

make in lifetime Amount of payment first applied to interest

owed, then to principal Can pay off early – paying an extra $25 per

month on a 30 year, 10 percent mortgage of $75,000 will save more than $34,000 in interest and will repay the loan in 25 years

Fixed-Rate Mortgages Also called a conventional mortgage Interest rates charges never vary over time Offer the peace of mind that monthly

payments will always stay the same

Adjustable-Rate Mortgages These interest rates will vary according to

economic factors so loan payments will change also

Rate caps available to prevent rates from rising or falling to far

May get convertible ARMs which could allow you to convert to a fixed rate for an added fee

Government Financing Programs

FHA Federal Housing Administration and VA Veterans Administration help buyers obtain low-interest, low down payment loan

They do not lend money but help qualified buyers get loans and guarantee repayments

Home Equity Loans Based on the difference of the amount

owed on mortgage and the current market value of home

Can provide money for improvements, education, doctor bills

Taking out too many can put people in debt for much more in the long run

Refinancing Obtain a new mortgage to replace the old

one Only an advantage when interest rates fall

more than 2% and owner is going to stay in for at least two years longer

Must pay extra fees to do this – could be several thousand dollars

Closing Closing costs:

Title insurance to insure no problems with ownership and estate taxes

Survey Deed which transfers ownership to you Appraisal Credit report Lender’s fee Real estate commission

My Closing Costs in 2000

Loan Origination Fee $400 Appraisal Fee $250 Credit Report $42 Flood Zone Determination $21 Hazard Insurance Premium $450 Hazard Insurance Reserves $37.50 County Tax Reserves $375.00 Title Insurance $200.00 Recording Fee to Register of Deeds $33.00 Total $1808.50

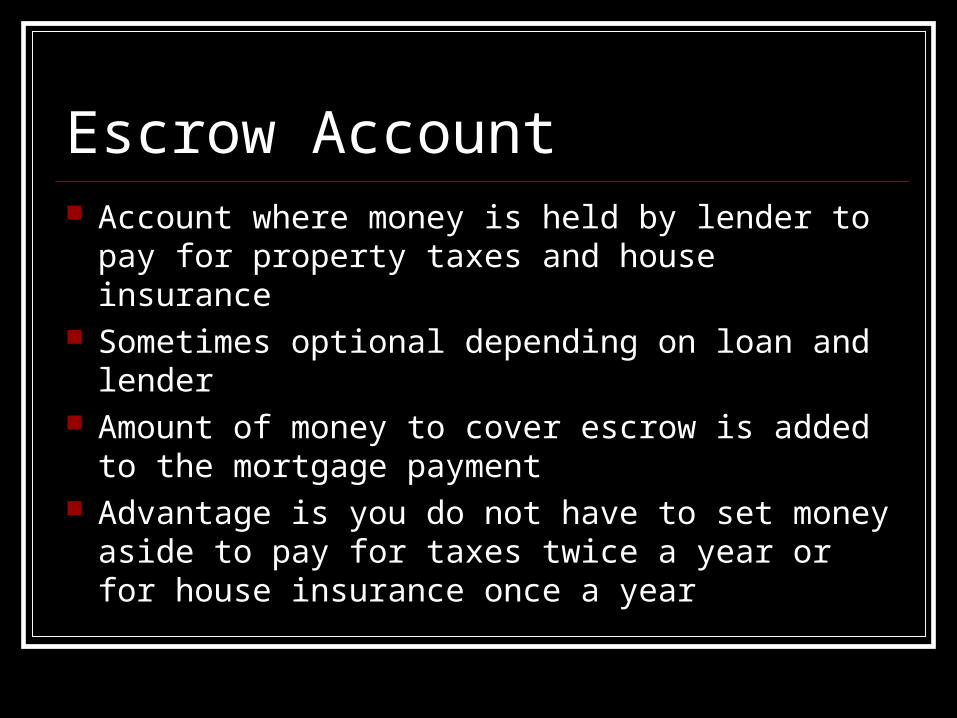

Escrow Account Account where money is held by lender to pay for

property taxes and house insurance Sometimes optional depending on loan and

lender Amount of money to cover escrow is added to the

mortgage payment Advantage is you do not have to set money aside

to pay for taxes twice a year or for house insurance once a year

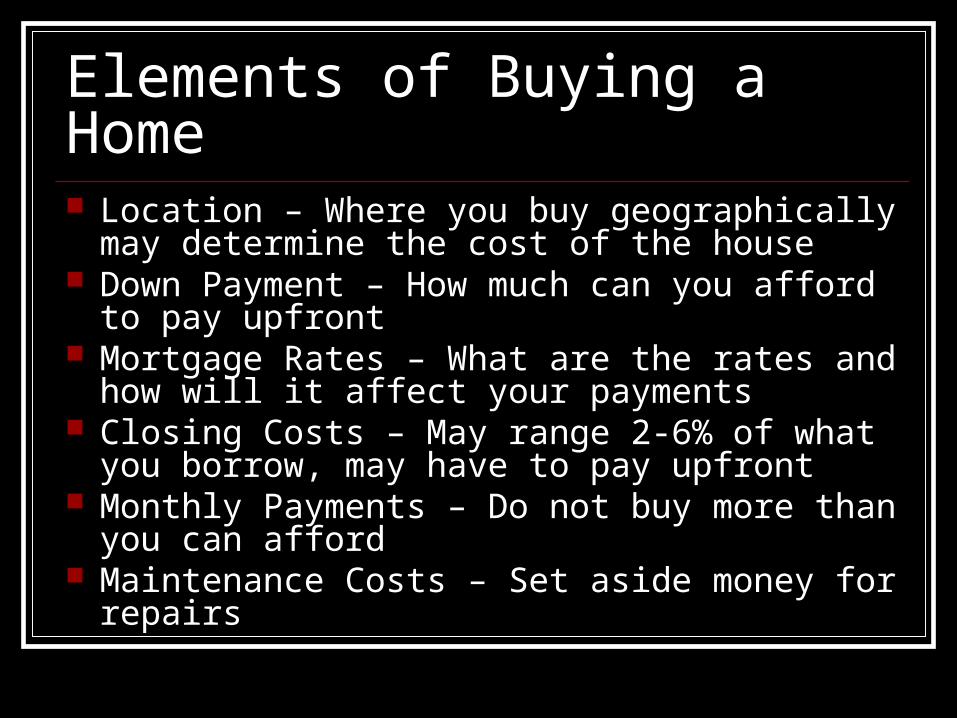

Elements of Buying a Home Location – Where you buy geographically may

determine the cost of the house Down Payment – How much can you afford to

pay upfront Mortgage Rates – What are the rates and how will

it affect your payments Closing Costs – May range 2-6% of what you

borrow, may have to pay upfront Monthly Payments – Do not buy more than you

can afford Maintenance Costs – Set aside money for repairs

Prepare a Home for Selling Nicer it looks, better it will sell – may add on extra

features (bathroom or deck) Determine a price, set higher than what you want Choose a real estate agent or sell yourself (10%

of homes sold this way) to save money but yourself it may be more work to determine selling price, attract buyers, show your home, and handle financial aspects

What Home Owners Say About…… Their Neighborhood

80% of Americans believe their own community is “a great place to raise a family”

Nearly 50% worry about overdevelopment with chain stores and restaurants

Home Improvement In last year, 11% spent between $1000 and $1500 in

repairs and upgrades Nearly 1/3 invested more than $5000 in painting, buying

furniture and landscaping.

What Home Owners Say About……

The Internet Nearly 66% access info. thru the Internet as

opposed to a broker Nearly 58% feel the Internet is diminishing their

reliance on a broker 27% cannot imagine buying or selling a home

without one

What Home Owners Say About……

Commuting 63% of homeowners would trade in square

footage or less time on the road

Their Dream House Top of list is beachfront mansion on the OC and

the Walton’s farmhouse No. 1 factor in next home purchase is a

“spacious, modern kitchen”

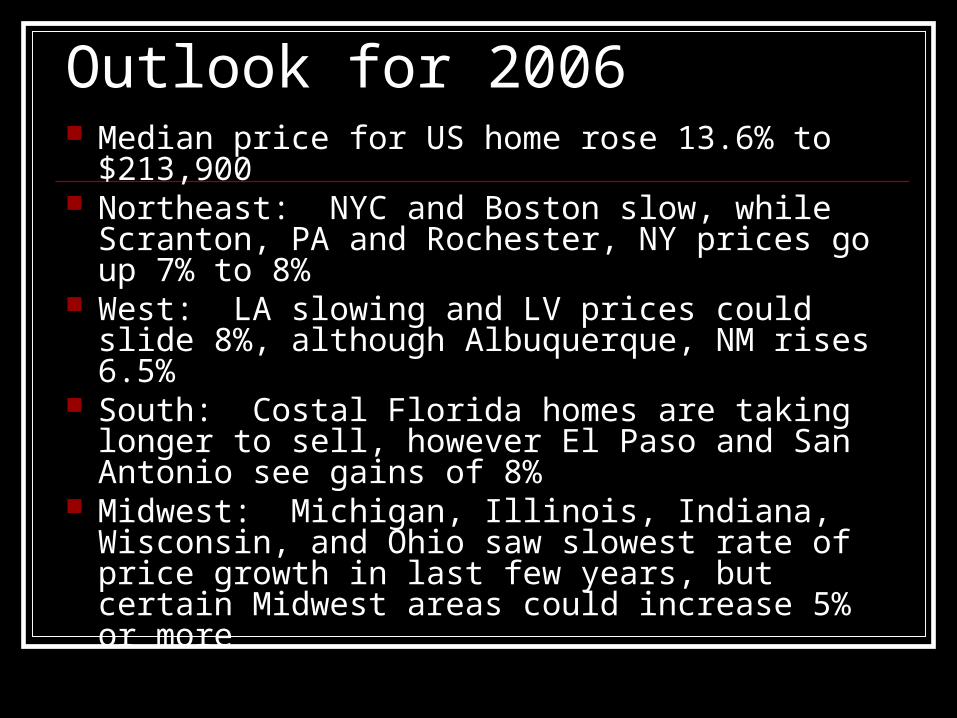

Outlook for 2006 Median price for US home rose 13.6% to

$213,900 Northeast: NYC and Boston slow, while

Scranton, PA and Rochester, NY prices go up 7% to 8%

West: LA slowing and LV prices could slide 8%, although Albuquerque, NM rises 6.5%

South: Costal Florida homes are taking longer to sell, however El Paso and San Antonio see gains of 8%

Midwest: Michigan, Illinois, Indiana, Wisconsin, and Ohio saw slowest rate of price growth in last few years, but certain Midwest areas could increase 5% or more

Four Reasons to Downsize Less Financial Stress – Family of three sold five-bedroom,

three story Victorian for $765,000, twice what they paid for it Less Maintenance – Older couple sold 2,800 sq. foot home in

country for an 1,800 sq foot home in town – no more large driveway to shovel, yard to rake

More Freedom – Cookie cutter home in development that dictated what color blinds could be hung and gave tickets when parked on street, traded for smaller home with a bigger lot

More Comfort – Family went from formal ballroom and five porches to a home with a comfortable family room

What You Get For $100,000 in

What You Get For $100,000 in

What You Get For $100,000 in

What You Get For $100,000 in

What You Get For $100,000 in

What You Get For $100,000 in

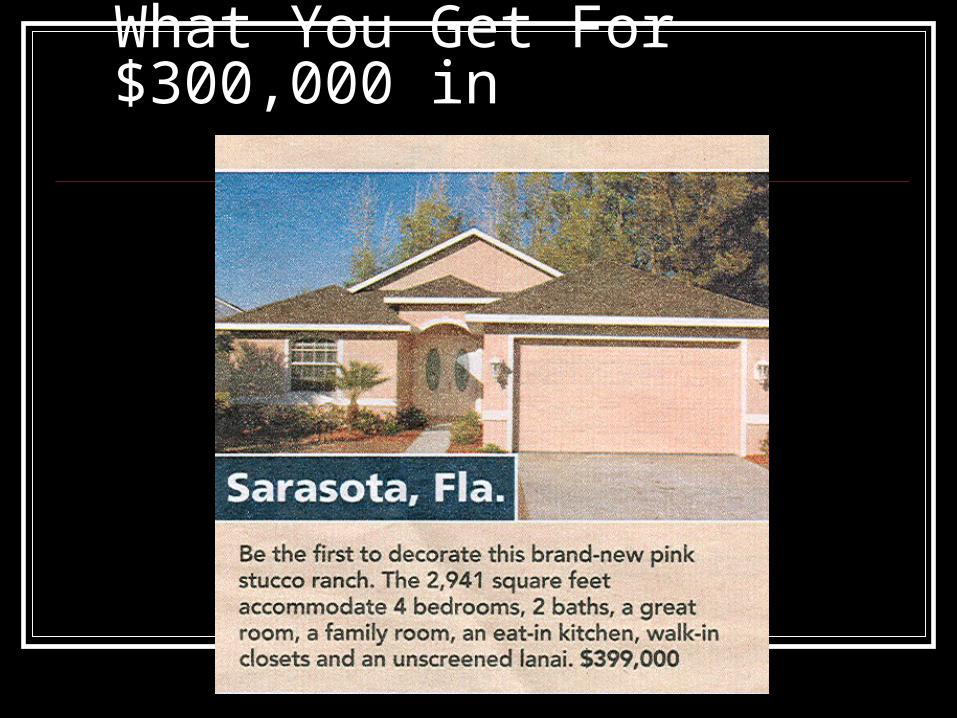

What You Get For $300,000 in

What You Get For $300,000 in

What You Get For $300,000 in

What You Get For $300,000 in

What You Get For $300,000 in

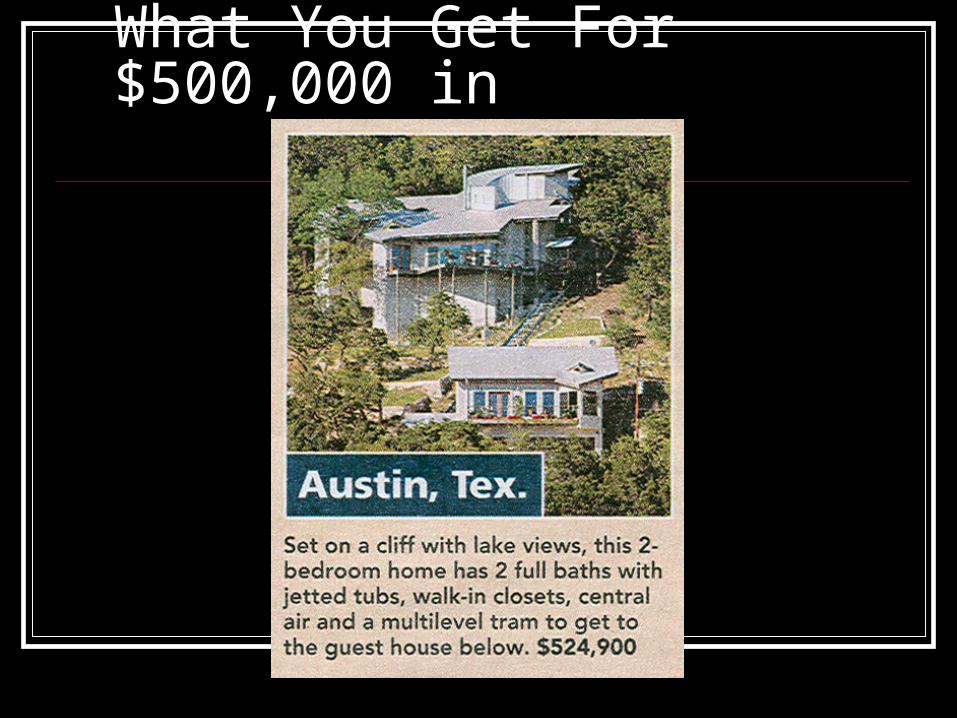

What You Get For $500,000 in

What You Get For $500,000 in

What You Get For $500,000 in