finance - pages - bvsd content hubcontenthub.bvsd.org/curriculum/course catalog/finance.docx · web...

TRANSCRIPT

Finance

Curriculum EssentialsDocument

Boulder Valley School DistrictDepartment of CTEC

October 2011

Introduction

The number one college major for both men and women is Business. As a result, the Boulder Valley School District offers a number of comprehensive college-oriented business classes which allow students the opportunity to begin evaluating a potential career in business and the selection of business as a major or minor in college. For those students who complete two or more business courses, during their high school career, the Boulder Valley School District provides a Business Pathways Completion Certificate.

Because over 70% of college students indicate that they wish they had had more financial literacy education in high school, the Finance course is designed to provide students with the most comprehensive personal financial literacy (PFL) education in the Boulder Valley School District. This hands-on, eighteen week course offers the following units of study: Goal Setting, Budgeting and Financial Record Keeping, Saving and Investing, Financial Services and Banking, Credit and Debt Management, Risk Management and Insurance, Careers and Consumer Protection. The material covered is reinforced and enhanced through the use of technology, guest speakers, videos and hands-on, project-based activities, such as the Stock Market Experience/Game, whenever possible. In addition, because experiential learning is an important aspect of this course, a field trip to the Junior Achievement Finance Park and/or the Federal Reserve Bank of Denver or other finance related field trip may be offered.

Students may also have the opportunity to take the National Financial Capability Challenge test which is a standardized online test offered by the U.S. Department of the Treasury in cooperation with the U.S. Department of Education and the President’s Advisory Council on Financial Literacy. Historically, the BVSD Finance students who have taken this standardized test have scored the highest in the state and averaged approximately 15% above the National average for this test.

5/7/2023 BVSD Curriculum Essentials 2

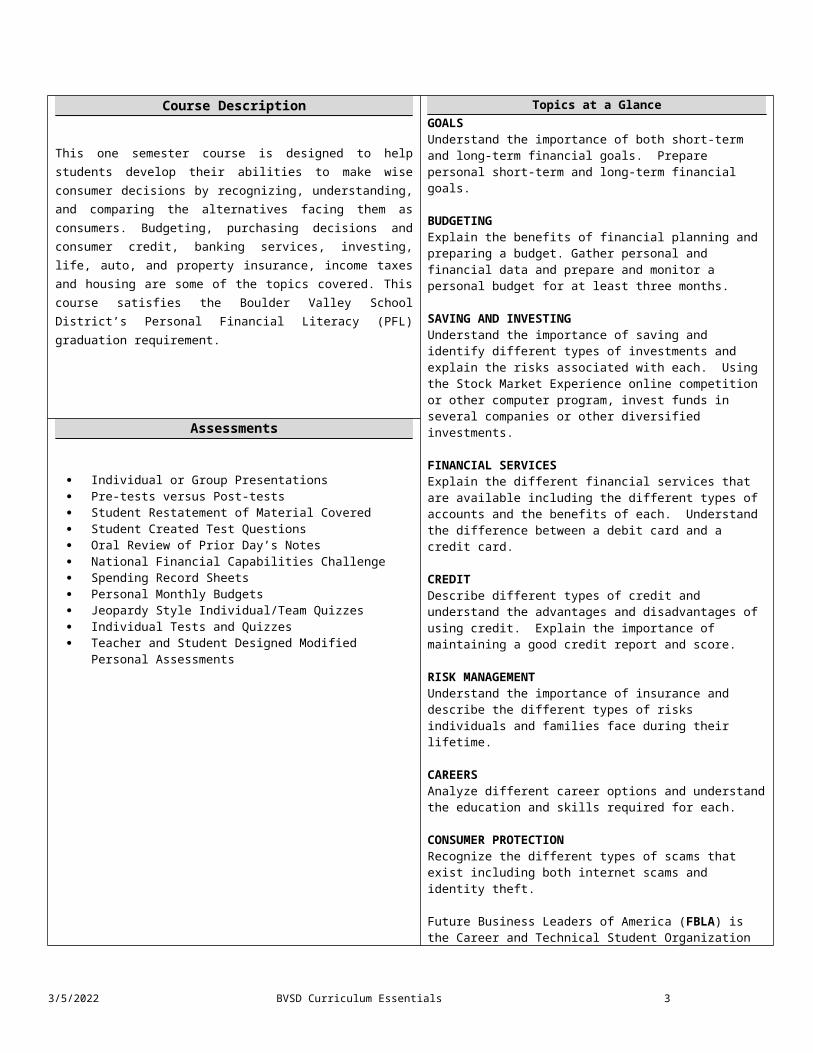

Course Description

This course is designed to help students develop their abilities to make wise consumer decisions by recognizing, understanding, and comparing the alternatives facing them as consumers. Budgeting, purchasing decisions and consumer credit, banking services, investing, life, auto, and property insurance, income taxes and housing are some of the topics covered. This course satisfies the Boulder Valley School District’s Personal Financial Literacy (PFL) graduation requirement.

Topics at a GlanceGOALSUnderstand the importance of both short-term and long-term financial goals. Prepare personal short-term and long-term financial goals.

BUDGETINGExplain the benefits of financial planning and preparing a budget. Gather personal and financial data and prepare and monitor a personal budget for at least three months.

SAVING AND INVESTINGUnderstand the importance of saving and identify different types of investments and explain the risks associated with each. Using the Stock Market Experience online competition or other computer program, invest funds in several companies or other diversified investments.

FINANCIAL SERVICESExplain the different financial services that are available including the different types of accounts and the benefits of each. Understand the difference between a debit card and a credit card.

CREDITDescribe different types of credit and understand the advantages and disadvantages of using credit. Explain the importance of maintaining a good credit report and score.

RISK MANAGEMENTUnderstand the importance of insurance and describe the different types of risks individuals and families face during their lifetime.

CAREERSAnalyze different career options and understand the education and skills required for each.

CONSUMER PROTECTIONRecognize the different types of scams that exist including both internet scams and identity theft.

Future Business Leaders of America (FBLA) is the Career and Technical Student Organization (CTSO) that Finance students are encouraged to join.

Assessments

Individual or Group Presentations Pre-tests versus Post-tests Student Restatement of Material Covered Student Created Test Questions Oral Review of Prior Day’s Notes National Financial Capabilities Challenge Spending Record Sheets Personal Monthly Budgets Jeopardy Style Individual/Team Quizzes Individual Tests and Quizzes Teacher and Student Designed Modified Personal

Assessments

Finance Overview

Prepared Graduates

5/7/2023 BVSD Curriculum Essentials 3

All students are expected to master the following concepts and skills to ensure their success in both the postsecondary and workforce settings.

1. CTE Essential Skills: Academic Foundations

ESSK.01: Achieve additional academic knowledge and skills required to pursue the full range of career and postsecondary education opportunities within a career cluster.

Prepared Graduate Competencies in the CTE Essential Skills standard:

Complete required training, education, and certification to prepare for employment in a particular career field

Demonstrate language arts, mathematics, and scientific knowledge and skills required to pursue the full range of post-secondary and career opportunities

2. CTE Essential Skills: Communications Standards

ESSK.02: Use oral and written communication skills in creating, expressing, and interrupting information and ideas, including technical terminology and information

Prepared Graduate Competencies in the CTE Essential Skills standard:

Select and employ appropriate reading and communication strategies to learn and use technical concepts and vocabulary in practice

Demonstrate use of concepts, strategies, and systems for obtaining and conveying ideas and information to enhance communication in the workplace

3. CTE Essential Skills: Problem Solving and Critical Thinking

ESSK.03: Solve problems using critical thinking skills (analyze, synthesize, and evaluate) independently and in teams using creativity and innovation.

Prepared Graduate Competencies in the CTE Essential Skills standard:

Employ critical thinking skills independently and in teams to solve problems and make decisions

Employ critical thinking and interpersonal skills to resolve conflicts with staff and/or

5/7/2023 BVSD Curriculum Essentials 4

customers

Conduct technical research to gather information necessary for decision-making

4. CTE Essential Skills: Safety, Health, and Environmental

ESSK.06: Understand the importance of health, safety, and environmental management systems in organizations and their importance to organizational performance and regulatory compliance

Prepared Graduate Competencies in the CTE Essential Skills standard:

Implement personal and jobsite safety rules and regulations to maintain safe and helpful working conditions and environment

Complete work tasks in accordance with employee rights and responsibilities and employers obligations to maintain workplace safety and health

5. CTE Essential Skills: Leadership and Teamwork

ESSK.07: Use leadership and teamwork skills in collaborating with others to accomplish organizational goals and objectives

Prepared Graduate Competencies in the CTE Essential Skills standard:

Employ leadership skills to accomplish organizational skills and objectives

6. CTE Essential Skills: Employability and Career Development

ESSK.09: Know and understand the importance of employability skills; explore, plan, and effectively manage careers; know and understand the importance of entrepreneurship skills

5/7/2023 BVSD Curriculum Essentials 5

Prepared Graduate Competencies in the CTE Essential Skills standard:

Indentify and demonstrate positive work behaviors and personal qualities needed to be employable

Develop skills related to seeking and applying for employment to find and obtain a desired job

5/7/2023 BVSD Curriculum Essentials 6

COLORADO COMMUNITY COLLEGE SYSTEM CAREER & TECHNICAL EDUCATION TECHNICAL STANDARDS REVISION & ACADEMIC ALIGNMENT PROCESS

Colorado’s 21st Century Career & Technical Education Programs have evolved beyond the historic perception of vocational education. They are Colorado’s best kept secret for:

• Relevant & rigorous learning

• Raising achievement among all students

• Strengthening Colorado’s workforce & economy

Colorado Career & Technical Education serves more than 116,000 Colorado secondary students annually through 1,200 programs in 160 school districts, 270 High Schools, 8 Technical Centers, 16 Community Colleges & 3 Technical Colleges. One of every three Colorado high school students gains valuable experiences by their enrollment in these programs.

ALIGNMENT REQUIRED BY SB 08-212

22-7-1005. Preschool through elementary and secondary education - aligned standards - adoption - revisions.

2(b): In developing the preschool through elementary and secondary education standards, the State Board shall also take into account any Career & Technical Education standards adopted by the State Board for Community Colleges and Occupational Education, created in Section 23-60-104, C.R.S., and, to the extent practicable, shall align the appropriate portions of the preschool through elementary and secondary education standards with the Career and Technical standards.

STANDARDS REVIEW AND ALIGNMENT PROCESS

Beginning in the fall of 2008, the Colorado Community College System conducted an intensive standards review and alignment process that involved:

NATIONAL BENCHMARK REVIEW

Colorado Career & Technical Education recently adopted the Career Cluster and Pathway Model endorsed by the United State Department of Education, Division of Adult and Technical Education. This model provided access to a national set of business and industry validated knowledge and skill statements for 16 of the 17 cluster areas. California and Ohio provided the comparative standards for the Energy cluster

• Based on this review Colorado CTE has moved from program-specific to Cluster & Pathway based standards and outcomes

• In addition, we arrived at fewer, higher, clearer and more transferrable standards, expectations and outcomes.

COLORADO CONTENT TEAMS REVIEW

The review, benchmarking and adjusting of the Colorado Cluster and Pathway standards, expectations and outcomes was through the dedicated work of Content Teams comprised of secondary and postsecondary faculty from across the state. Participation by instructors from each level ensured competency alignment between secondary and postsecondary programs. These individuals also proposed the draft academic alignments for math, science reading, writing and communication, social studies (including Personal Financial Literacy) and post secondary and workforce readiness (PWR.)

5/7/2023 BVSD Curriculum Essentials 7

ACADEMIC ALIGNMENT REVIEW

In order to validate the alignment of the academic standards to the Career & Technical Education standards, subject matter experts in math, science, reading, writing and communication, and social studies were partnered with career & technical educators to determine if and when a true alignment existed.

CURRENT STATUS

• One set of aligned Essential skills to drive Postsecondary and Workforce Readiness inclusion in all Career & Technical Education programs.

• 52 pathways with validated academic alignments

• 12 pathways with revised standards ready for alignment (currently there are no approved programs in these pathways)

• 21 pathways where no secondary programming currently exists. Standards and alignments will be developed as programs emerge.

• Available for review at: www.coloradostateplan.com/content_standards.htm

5/7/2023 BVSD Curriculum Essentials 8

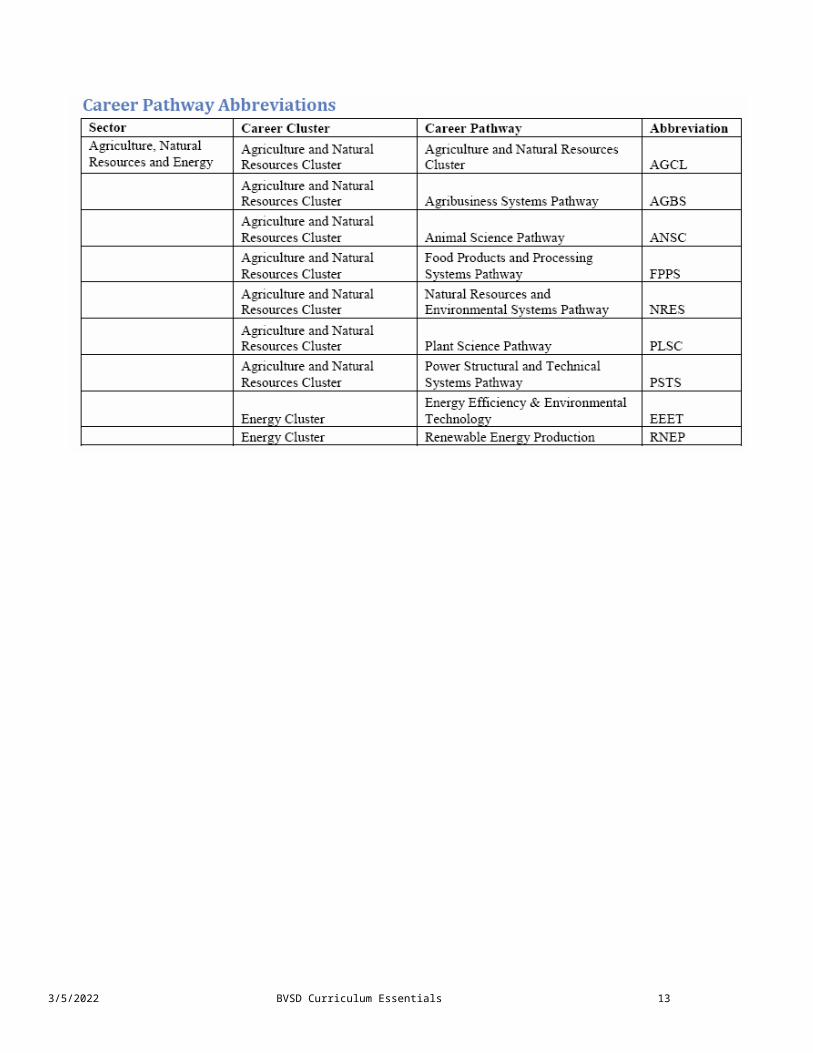

Colorado Career & Technical Education Standards Academic Alignment Reference System

The Career & Technical Education standards have been organized by Career Cluster (17) and Pathway (81). In addition, a set of “Essential Skills” was developed to ensure the Postsecondary and Workforce Readiness within any cluster or pathway. These workforce readiness skills are applicable to all career clusters and should form the basis of each CTE program.

Organization

Essential Skills There exists a common set of knowledge and skills that are applicable to all students regardless of which cluster or pathway they choose. This set of standards, is meant for inclusion in each program to enhance the development of postsecondary and workforce readiness skills.

Career Cluster A Career Cluster is a grouping of occupations and broad industries based on commonalities. The 17 Career Clusters organize academic and occupational knowledge and skills into a coherent course sequence and identify pathways from secondary schools to two- and four-year colleges, graduate schools, and the workplace. Students learn in school about what they can do in the future. This connection to future goals motivates students to work harder and enroll in more rigorous courses.

Career Pathway Pathways are sub-groupings of occupations/career specialties used as an organizing tool for curriculum design and instruction. Occupations/career specialties are grouped into Pathways based on the fact that they require a set of common knowledge and skills for career success.

Prepared Completer Competency This level targets the “big ideas” in each pathway. These are the competencies that all students who complete a CTE pathway must master to ensure their success in a postsecondary and workforce setting. Prepared Completer Competencies will not usually be “course” specific but grow with the student’s progression through the sequence of courses.

Concept/Skill The articulation of the concepts and skills that indicates a student is making progress toward being a prepared completer. They answer the question: What do students need to know and be able to do?

Evidence Outcome The indication that a student is meeting an expectation at the mastery level. How do we know that a student can do it? Pathway Abbreviation (4 Letter)

5/7/2023 BVSD Curriculum Essentials 9

Academic Alignments

Academic alignments, where appropriate in Math, Reading, Writing and Communication, Science and Social Studies (including Personal Financial Literacy) were defined by CTE and academic subject matter experts using the following criteria:

• It was a point where technical and academic content naturally collided;

• The student must demonstrate adequate proficiency with the academic standard to perform the technical skill; and

• It could be assessed for both academic and technical understanding.

Colorado’s CTE programs have had academic alignments dating back to the early 1990’s. While these alignments resulted in an increase in academic focus in CTE programs, the reality is that a true transformation in intentional teaching toward the academic standard was limited.

With these alignments comes a new expectation: If a CTE instructor is teaching a CTE concept that has an identified alignment, they must also be intentional about their instruction of the academic standard. CCCS will be providing professional development and instructional resources to assist with the successful implementation of this new expectation. In addition, this expanded expectation will require increased collaboration between CTE and academic instructors to transform teaching and learning throughout each school.

For each set of Cluster and Pathway standards, the academic alignments have been included and are separated by academic area. CCCS chose to align at the “Evidence Outcome” level. The aligned academic evidence outcome follows the CTE evidence outcome to which it has been aligned. For a sample, see Illustration A.

5/7/2023 BVSD Curriculum Essentials 10

The academic standard number used in the alignments matches the Colorado Department of Education standards numbering convention.

5/7/2023 BVSD Curriculum Essentials 11

5/7/2023 BVSD Curriculum Essentials 12

5/7/2023 BVSD Curriculum Essentials 13

5/7/2023 BVSD Curriculum Essentials 14

5/7/2023 BVSD Curriculum Essentials 15

Finance

FINC.01 Academic Foundations: Solve mathematical problems to obtain information for decision making in finance.

FINC.01.01 Employ numbers and operations in finance.FINC.01.01.a Recognize relationships among numbers.MA10-GR.HS-S.1-GLE.1-EO.b Use properties of rational and irrational numbers. (CCSS: N-RN)MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

FINC.01.01.b Employ mathematical operations.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

FINC.01.01.c Perform computations successfully.MA10-GR.HS-S.2-GLE.2-EO.c

Model periodic phenomena with trigonometric functions. (CCSS: F-TF)

MA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)FINC.01.01.d Predict reasonable estimations.MA10-GR.HS-S.1-GLE.2-EO.a Reason quantitatively and use units to solve problems (CCSS: N-

Q)MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.01.04 Perform data analysis to make business decisions.FINC.01.04.a Formulate questions effectively.FINC.01.04.b Collect relevant data.MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.3-GLE.1-EO.a.iii

Interpret differences in shape, center, and spread in the context of the data sets, accounting for possible effects of extreme data points (outliers). (CCSS: S-ID.3)

FINC.01.04.c Organize useful data.

5/7/2023 BVSD Curriculum Essentials 16

MA10-GR.HS-S.3-GLE.1-EO.a.iii

Interpret differences in shape, center, and spread in the context of the data sets, accounting for possible effects of extreme data points (outliers). (CCSS: S-ID.3)

FINC.01.04.d Answer questions appropriately.MA10-GR.HS-S.3-GLE.2-EO.b

Make inferences and justify conclusions from sample surveys, experiments, and observational studies. (CCSS: S-IC)

FINC.01.04.e Employ appropriate statistical methods in data analysis.MA10-GR.HS-S.3-GLE.1-EO.b.ii

Represent data on two quantitative variables on a scatter plot, and describe how the variables are related. (CCSS: S-ID.6) 1. Fit a function to the data; use functions fitted to data to solve problems in the context of the data. Use given functions or ch

MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.01.04.f Develop and evaluate inferences and predictions.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

MA10-GR.HS-S.3-GLE.2-EO.b

Make inferences and justify conclusions from sample surveys, experiments, and observational studies. (CCSS: S-IC)

MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.01.04.g Apply basic concepts of probability.MA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.01.05 Use problem-solving techniques to evaluate the accuracy of mathematical responses in finance.

FINC.01.05.a Identify problem-solving techniques.MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.01.05.b Apply a variety of problem-solving strategies.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

FINC.01.05.c Adjust problem-solving strategies, when needed.MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)FINC.07 Systems: Describe tools, strategies, and systems used to maintain, monitor, control, and plan the

use of financial resources.

5/7/2023 BVSD Curriculum Essentials 17

FINC.07.01 Describe the nature and scope of finance.FINC.07.01.a Explain the role of finance in business.FINC.07.01.b Discuss the role of ethics in finance.

FINC.14 Technical Skills: Maintain, control, and plan the use of financial resources to protect solvency.FINC.14.01 Discuss the fundamental principles of money.

FINC.14.01.a Explain forms of financial exchange (cash, credit, debit, electronic funds transfer, etc.).

MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

FINC.14.01.b Identify types of currency (paper money, coins, banknotes, government bonds, treasury notes, etc.).

MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

FINC.14.01.c Describe functions of money (medium of exchange, unit of measure, store of value).

MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

FINC.14.01.d Describe sources of income (wages/salaries, interest, rent, dividends, transfer payments, etc.).

MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

FINC.14.01.e Explain the time value of money.MA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.14.01.f Explain the purposes and importance of credit.MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

FINC.14.01.g Explain legal responsibilities associated with financial exchanges.

FINC.14.02 Analyze personal financial needs and goals.FINC.14.02.a Explain the nature of financial needs (e.g., college, retirement, wills,

insurance, etc.).MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

FINC.14.02.b Set financial goals.MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.1-GLE.2-

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate

5/7/2023 BVSD Curriculum Essentials 18

EO.a.v how living within your means is essential for a secure financial future (PFL)

FINC.14.02.c Develop personal budget.MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

FINC.14.02.d Explain the need to save and invest.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

FINC.14.03 Manage personal finances to achieve financial goals.FINC.14.03.a Explain the nature of tax liabilities.FINC.14.03.b Interpret a pay stub.MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

FINC.14.03.c Read and reconcile bank statements.MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

FINC.14.03.d Maintain financial records.FINC.14.03.e Demonstrate the wise use of credit.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

FINC.14.03.f Validate credit history.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

FINC.14.03.g Protect against identity theft.FINC.14.03.h Prepare personal income tax forms (i.e., 1040 EZ).

FINC.14.04 Describe the use of financial-services providers.FINC.14.04.a Describe types of financial-services providers.FINC.14.04.b Discuss considerations in selecting a financial-services

provider.MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

5/7/2023 BVSD Curriculum Essentials 19

MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.14.05 Use investment strategies.FINC.14.05.a Explain types of investments.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

FINC.14.05.c Establish investment goals and objectives.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.14.06 Identify potential business threats and opportunities to protect a business’s financial well-being.

FINC.14.06.a Describe the concept of insurance.FINC.14.06.e Explain the nature of risk management.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

MA10-GR.HS-S.3-GLE.3-EO.a.v

Recognize and explain the concepts of conditional probability and independence in everyday language and everyday situations. (CCSS: S-CP.5)

MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.14.08 Manage financial resources to ensure solvency.FINC.14.08.a Describe the nature of budgets.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

FINC.14.09 Explain the importance of financial markets in business.FINC.14.09.a Describe the role of financial institutions.MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

5/7/2023 BVSD Curriculum Essentials 20

FINC.14.09.b Explain types of financial markets (i.e., money markets,. securities markets, property market, market for risk transfer).

FINC.14.10 Explain the nature of assets’ values.FINC.14.10.a Discuss factors that affect the value of an asset (e.g., cash flows, growth rate,

timing, inflation, interest rate, opportunity cost, and risk and required return).MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

FINC.14.11 Utilize sources of securities information to make informed financial decisions.FINC.14.11.a Describe sources of securities information.FINC.14.11.b Read/Interpret securities table.

FINC.20 Financial Skills: Employ financial risk-management strategies and techniques used to minimize business loss.

FINC.20.01 Describe the nature and scope of risk management in finance.FINC.20.01.a Explain the role of ethics in risk management.FINC.20.01.c Discuss legal considerations affecting risk management.

FINC.20.03 Describe risk control methods in finance.FINC.20.03.a Discuss the nature of risk control (i.e., internal and

external).MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

FINC.20.03.b Explain ways to assess risk.MA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

ESSK.11 Independent Living: Know and understand the skills, rights, resources, and responsibilities required to live independently in society.

ESSK.11.01 Demonstrate the financial knowledge and skills necessary for independent living.ESSK.11.01.a Develop a personal budget based on a given income level.MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d Model personal financial situationsESSK.11.01.b Demonstrate the ability to open and maintain checking and savings

accounts.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d Model personal financial situationsMA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

ESSK.11.01.c Demonstrate an understanding of investments (types, purposes, rates of return, and compound interest).

MA10-GR.HS-S.2-GLE.1-EO.c.i

Graph functions expressed symbolically and show key features of the graph, by hand in simple cases and using technology for more complicated cases.? (CCSS: F-IF.7)

MA10-GR.HS-S.2-GLE.2-EO.d Model personal financial situationsMA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

5/7/2023 BVSD Curriculum Essentials 21

ESSK.11.01.d Demonstrate an understanding of credit (types, usage, and costs).

MA10-GR.HS-S.2-GLE.2-EO.d Model personal financial situationsMA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

ESSK.11.01.e Demonstrate the ability to calculate wages, overtime, and commission.

MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d Model personal financial situationsESSK.11.01.f Understand different types of insurance (auto, health, life, disability,

renters) and how to compare costs.MA10-GR.HS-S.2-GLE.2-EO.d Model personal financial situationsMA10-GR.HS-S.3-GLE.3-EO.c

Analyze* the cost of insurance as a method to offset the risk of a situation (PFL)

ESSK.11.01.g Demonstrate an understanding of taxes by calculating tax rates and completing personal income tax returns.

MA10-GR.HS-S.1-GLE.2-EO.a.iv

Describe factors affecting take-home pay and calculate the impact (PFL)

MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d Model personal financial situationsESSK.11.01.h Demonstrate an understanding of Social Security benefits and how to

access them.ESSK.11.01.i Compare and calculate the costs of purchasing a car.MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d Model personal financial situationsMA10-GR.HS-S.2-GLE.2-EO.d.i

Analyze* the impact of interest rates on a personal financial plan (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d.ii Evaluate* the costs and benefits of credit (PFL)MA10-GR.HS-S.2-GLE.2-EO.d.iii

Analyze various lending sources, services, and financial institutions (PFL)

ESSK.11.01.j Demonstrate an understanding of how to rent an apartment (compare features and costs, understand lease agreements).

MA10-GR.HS-S.1-GLE.2-EO.a.v

Design and use a budget, including income (net take-home pay) and expenses (mortgage, car loans, and living expenses) to demonstrate how living within your means is essential for a secure financial future (PFL)

MA10-GR.HS-S.2-GLE.2-EO.d Model personal financial situations

5/7/2023 BVSD Curriculum Essentials 22

5/7/2023 BVSD Curriculum Essentials 23

Glossary

Adjustable Rate Mortgage - a mortgage loan subject to changes in interest rates; when rates change, monthly payments increase or decrease at intervals determined by the lender and a prescribed index and set margin; the monthly payment increases usually have a per adjustment and a lifetime cap.

Advertising - an announcement—usually paid—of a product’s or service’s benefits that is intended to encourage its purchase.

Amortization - the process by which loan payments are applied to the principal, or amount borrowed, as well as the interest on a loan according to a set schedule.

Annual Percentage Rate (APR) - the percentage cost of credit on an annual basis, which must be disclosed by law. Example 1: A $100 loan repaid in its entirety after one year with a $10 finance charge ($9 interest plus a $1 service fee) has an APR of 10%. Example 2: A $100 one-year loan with a $10 finance charge repaid in twelve equal installments (meaning the borrower has the use of less and less of the loan principal each month) has an APR of 18%.

Annual Percentage Yield (APY) - the annual rate of return on an investment, which must be disclosed by law and which varies by the frequency of compounding. Example 1: A $1,000 investment that earns 6% per year pays $60 at year-end and has an APY of 6%. Example 2: A $1,000 investment that earns 0.5% per month (6%/12) pays $61.68 in one year and has an APY of 6.17%. Example 3: A $1,000 investment that earns 0.0164% per day (6%/365) pays $61.83 in one year and has an APY of 6.18%.

Annuity - a contract between an individual and an insurance company where the individual makes a series of payments that are invested by the company and repaid to the individual at a later date–generally during retirement. Annuities may be fixed or variable. Appreciation - a rise in value or price.

Asset - something of monetary value owned by an individual or an organization.

Automated Teller Machine (ATM) - a computer terminal used to conduct business with a financial institution or purchase items such as postage stamps or transportation tickets; also known as a cash machine.

Back-end load - a sales charge paid when investments are sold.

Bait and Switch - an illegal sales technique in which sellers advertise a product with the intention of persuading customers to buy a more expensive product or; loan terms are switched and become less favorable to the consumer.

Balloon Mortgage - a short-term mortgage in which small periodic payments are made until the completion of the term, at which time the balance is due as a single lump-sum payment.

Bankruptcy - a state of being legally released from the obligation to repay some or all debt in exchange for the forced loss of certain assets. A court’s determination of personal bankruptcy remains in a consumer’s credit record for 10 years.

Bank - a state or federally chartered for-profit financial institution that offers commercial and consumer loans and other financial services.

Banking services – services such as checking accounts, savings accounts, automated teller machines and online banking provided by individual banks.

Beneficiary - a person or organization named to receive assets after an individual’s death.

5/7/2023 BVSD Curriculum Essentials 24

Bond - a certificate representing the purchaser’s agreement to lend a business or government money on the promise that the debt will be paid—with interest—at a specific time.

Borrowing – the act of receiving and using something belonging to somebody else, with the intention of returning or repaying it-often with interest in the case of borrowed money.

Brokerage Firms - Financial services businesses that buy and sell securities such as stocks and bonds to investors.

Budget - a plan for managing money, dividing up expected income and expenses among spending and saving options based on personal goals during a given time period.

Capacity - the ability to repay a loan from present income; used in loan underwriting.

Capital - money or other assets owned by individuals or used in operating a business.

Career - a profession or field of employment for which one study or trains, such as financial services or medicine. A pattern of activities and positions involved in an individual’s lifetime of work to which the person has made a long-term commitment. See Job.

Cash Flow - a measure of the money a person receives and spends.

Cash flow statement - a summary of receipts and payments for a given period, helpful when preparing a budget; also known as an income and expense statement.

Character - refers to trustworthiness; one of three factors in credit scoring (e.g., paying bills on time shows financial responsibility). Creditworthiness indicates a responsible attitude toward living up to agreements. Used in underwriting a loan.

Charitable giving - the act of giving to charitable organizations or to those in need.

Check – a written order directing a bank or credit union to pay a person or business a specific sum of money.

Closed-end credit - a specific-purpose loan requiring repayment with interest and any other finance charges by a specific date. Examples include most mortgages or auto loans.

Collateral - property that a borrower promises to give up to a lender in case of default.

Collectibles - physical objects—such as fine art, stamps, and antiques—that an investor buys in the hope that they will grow in value.

Collection agency - a business that specializes in obtaining payments from debtors who have defaulted on their loans.

Comparison shopping - the process of seeking information about products and services to find the best quality or utility at the best price.

Compensation - payment and benefits for work performed; also payment to injured or unemployed workers or their dependents.

Complaint - an expression of dissatisfaction with a product or service, often in the form of a letter to the seller or manufacturer documenting the problem and stating the desired solution.

5/7/2023 BVSD Curriculum Essentials 25

Compound Interest - interest earned not only on the principal but also on the interest already earned.

Compounding - paying interest on the principal and on interest already earned; the longer the money is left in the account, the more dramatic the compounding effect.

Consumer - a buyer or user of goods and services for personal use.

Consumer Fraud - wrongful or criminal deception intended to manipulate consumer for financial or other personal gain.

Contract - a legally binding agreement between two or more parties. Cost/benefit analysis, risk/reward relationship - a tool used to choose among alternatives involves weighing the cost of a product or service against the benefit it will provide.

Credit - an agreement to provide goods, services, or money in exchange for future payments with interest by a specific date or according to a specific schedule. The use of someone else’s money for a fee. See Open-end credit, Closed-end credit, and Easy-access credit.

Credit bureau - an establishment that collects and distributes credit-history information of individuals and businesses. The three major credit bureaus are Experian, Equifax, and Trans Union.

Credit card - a plastic card that authorizes the delivery of goods and services in exchange for future payment with interest, according to a specific schedule.

Credit report - an official record of a borrower’s credit history, including such information as the amount and type of credit used, outstanding balances, and any delinquencies, bankruptcies, or tax liens.

Credit score/rating - a measure of creditworthiness based on an analysis of the consumer’s financial history, often computed as a numerical score, using the FICO or other scoring systems to analyze the consumer’s credit. A creditor’s evaluation of a person’s willingness and ability to pay debts as judged by character, capacity, and capital; a mathematical model used by lenders to predict the likelihood that bills will be paid as promised.

Credit union - a state or federally chartered not-for-profit financial cooperative that provides financial services to its member-owners, who have met specific employment, residence, or other eligibility requirements.

Creditworthy - the presumption that a specific borrower has sufficient assets, income, and/or inclination to repay a loan.

Debit card - a plastic card that provides access to electronic funds transfer (EFT) from an automated teller machine (ATM) or a point-of-sale (POS) terminal.

Debt - something owed, usually measured in dollars. Entire amount of money owed to lenders.

Debt to Income Ratio - the percentage of a consumer's monthly gross income that goes toward paying debts.

Decision making - a method of selecting a course of action after gathering and evaluating information and considering the costs and benefits of various alternatives and consequences.

Deductible - the dollar amount or percentage of a loss that is not insured, as specified in an insurance policy.

5/7/2023 BVSD Curriculum Essentials 26

Default - failure of a borrower to repay a student loan according to the terms agreed upon when the promissory note was signed. When a borrower defaults, the school, loan holder, state government, and federal government can take action to recover the money. Defaults are reported to national credit bureaus and might affect a borrower’s ability to get credit in the future.

Deferred Interest - a deferred interest loan is when a loan payment stays the same while the interest rate increases. A deferred interest loan will let you choose to pay only the minimum payment-a payment less than the entire interest owed for that month. The unpaid interest is then added to your loan amount to be paid at a later date.

Delinquency - failure of a borrower to make a loan payment on the scheduled payment due date.

Demand – the quantity of a good or service that buyers are willing and able to buy at all possible prices during a period of time. Depreciation - decline in a product’s value that starts the moment a product is purchased (e.g., car).

Discount Point - an amount or fee a borrower pays to a lender, which will help decrease the interest rate on a mortgage loan. One point is equal to one percent.

Disposable income - gross pay minus deductions for taxes.

Diversification - a strategy for reducing some types of risk by selecting a wide variety of investments.

Dividends - earnings from corporate stock or credit union share accounts.

Down payment - (1) an initial, partial payment made at the time of purchase to permit the buyer to take delivery of the purchase. (2) a partial payment made to evidence good faith that the buyer will complete the purchase transaction at the time the contract is signed.

Earned income - earnings from employment, including commissions and tips.

Easy-access credit - short-term loans granted regardless of credit history, often for very short periods and at high interest rates. See Pawnshops, Payday loans, Rent-to-own, and Title loans.

Economy – global or world - worldwide system that results from choices of consumers, workers, business owners, manufacturers and government officials in multiple societies and with increasing trade and cultural exchange.

Electronic Funds Transfer (EFT) - the shifting of money from one financial institution account to another without the physical movement of cash.

Emergency fund - money set aside for unexpected expenses or for living costs in case of job loss.

Employee benefits - compensation that an employee receives in addition to a wage or salary. Examples include health insurance, life insurance, childcare, retirement pension, and subsidized meals.

Employer-sponsored retirement savings plan - tax-deferred investment programs, such as 401(k) plans for corporate employees and Section 457 plans for state and local government employees, which provide, in some cases, employer-matching funds.

Entrepreneur - an individual, who conceives of, establishes, operates, and assumes the risks of a business. A person who owns and operates her or his own business. A person who creates a business from scratch, based on a need or personal expertise, and puts creativity and ingenuity into action to provide a service or product. A person who organizes, manages, and takes the risks involved in creating a new product/service or developing a better way to operate a business.

5/7/2023 BVSD Curriculum Essentials 27

Entrepreneurship - a process that involves (a) seeing an opportunity to provide a product/service, (b) taking initiative to find out about competitors and what customers want from the product/service, and (c) developing plans to market the business. Imagination, innovative thinking, and management skills are needed to start and operate a business.

Equal Credit Opportunity Act - a federal law that forbids lenders from discriminating against loan applicants based on gender, race, marital status, religion, national origin, age, or receipt of public assistance.

Equity - stock ownership in a corporation.

Escrow Account - funds held by a third party for future use by the borrower; funds are for special purposes and may be paid out or returned to the borrower only under certain conditions. With mortgages, monthly house payments may include payments for insurance and taxes that are placed in a special account to meet those obligations.

Estate - the assets and debts that a person leaves at death.

Ethics - a set of moral principles or beliefs that govern an individual’s actions.

Expenses - the costs of goods and services, including those that are fixed such as rent and auto loan payments and those that are variable such as food, clothing, and entertainment.

Fair and Accurate Credit Transactions Act (FACT Act) - a federal law that gives consumers more ways to recover their credit reputations after they have been victims of identity theft, and allows consumers to request one free copy of their credit reports from the major credit reporting agencies each year.

Fair Credit and Charge Card Disclosure Act - a part of the Truth in Lending Act that mandates a description of key features and costs— such as APR, grace period, balance calculation, annual fees, and penalty fees—on credit card applications.

Fair Credit Billing Act - a federal law that addresses billing problems with open-end credit accounts by requiring, for example, that consumers send a written error notice within 60 days of receiving the first bill containing the error, and preventing creditors from damaging a consumer’s credit rating during a pending dispute.

Fair Credit Reporting Act - a federal law that covers the reporting of debt repayment information, requiring, for example, the removal of certain information after seven or ten years, and giving consumers the right to know what is in their credit reports, to dispute inaccurate information, and to add a brief statement explaining accurate negative information.

Fair Debt Collection Practices Act - a federal law that prohibits debt collectors from engaging in unfair, deceptive, or abusive practices, such as calling consumers at work after being told not to.

FICA - Federal Insurance Contributions Act. See Social Security.

FICO - the most commonly used credit score. The name comes from the Fair Isaac Corporation, which developed the scoring model. They are used to predict the likelihood that a person will pay his or her debts. The scores use only information from credit reports.

Finance charge - the total cost of credit, including interest and transaction fees.

5/7/2023 BVSD Curriculum Essentials 28

Finance company - a type of financial institution that makes consumer loans; generally, such loans are made to individuals with less than perfect credit ratings at higher interest rates.

Financial adviser - a person who provides financial information and advice. Examples include employee benefits staff, bank and credit union employees, credit counselors, brokers, financial planners, accountants, insurance agents, and attorneys.

Financial aid - money provided to the student and/or parents to help pay for the student’s education. Major forms of financial aid include gift aid (grants and scholarships) and self-help aid (loans and work-study).

Financial goals - desired results from one’s efforts to achieve personal economic satisfaction.

Financial institutions - businesses that deal primarily with money, such as deposits, investments, and loans, rather than goods or services.

Financial literacy - the ability to use knowledge and skills to manage one’s financial resources effectively for lifetime financial security. Financial plan - a report that identifies a person’s financial goals, needs, and expected future earning, saving, investing, insurance, and debt management activities; it typically includes a statement of net worth. Ongoing thinking process to develop an orderly program or blueprint for handling all aspects of one’s money, including spending, credit, saving, and investing.

Financial products - products sold or provided by financial institutions, such as savings accounts, loans, etc.

Fixed rate mortgage - a mortgage in which the interest rate and the amount of each payment remain constant throughout the life of the loan.

Foreclosure - it is a repossession of property by a legal process due to default on terms of mortgage by the borrower. This property is sold at a public auction, the proceeds of which are used to settle mortgage debt.

Fraud - intentional and illegal deception, misrepresentation, or concealment of information for monetary gain.

Free Application for Federal Student Aid (FAFSA) - a federal form required to apply for federal student aid. Forms can be completed online at <www.fafsa.ed.gov>, or paper copies can be found at high schools, colleges and local libraries. The information provided on this form is used to determine the student’s expected family contribution (EFC), which allows financial aid offices to identify the types of aid the student might be eligible to receive.

Front-end load - a sales charge paid when investments are purchased and sometimes when dividends are reinvested.

Garnishment - a court-sanctioned procedure that sets aside a portion of an employee’s wages to pay a financial obligation.

Gifts in-kind - a non-cash contribution to a charitable organization which can be given a cash value.

Goal - a statement about what a person wants to be, do, or have, accomplished by taking certain steps; provides direction to a plan of action.

Goal setting - the process used to determine what an individual wants to be, do, or have, i.e., what a person wants to accomplish.

5/7/2023 BVSD Curriculum Essentials 29

Grace period - a transition period (generally six months following the date a borrower leaves school or drops below half-time status) during which the borrower is not required to make loan payments. This period is designed to help the borrower prepare for repayment.

Grants - money for college that does not have to be repaid, which is based on a student’s financial need. Eligibility for federal grants is determined when a student applies for federal student aid through the FAFSA (Free Application for Federal Student Aid).

Gross pay - wages or salary before deductions for taxes and other purposes.

Guarantee - a written guarantee from the manufacturer or distributor that specifies the conditions under which the product can be returned, replaced, or repaired.

Identity theft - the crime of using another person’s name, credit or debit card number, Social Security number, or another piece of personal information to commit fraud.

Implied Warranty - an unwritten guarantee that a product is of sufficient quality to fulfill the purpose for which it was designed.

Impulse buying/purchase - purchasing goods or services without considering needs, goals, or consequences.

Income - money earned from investments and employment.

Individual Retirement Account (IRA) - an investment with specific tax advantages. A traditional IRA defers taxes on earnings until withdrawal and, under certain circumstances, allows the deduction of some contributions from current taxable income. A Roth IRA requires after-tax contributions only, but allows tax-free withdrawals under certain rules.

Inflation - an overall rise in the prices of goods and services; the opposite of the less common deflation.

IRA - see Individual Retirement Account. Insurance - a risk management tool that protects an individual from specific financial losses under specific terms and premium payments, as described in a written policy document. Major types include: Auto - provides liability and property damage coverage under specific circumstances. Disability - replaces a portion of income lost when a person cannot work because of illness or injury. Health - covers specific medical costs associated with illness, injury, and disability. Homeowners - provides property damage and liability coverage under specific circumstances. Liability - protects the insured party from others’ claims of loss due to the insured’s alleged or actual negligence or improper actions. Life - protects dependents from loss of income, debt-repayment, and other expenses after the death of the insured party. Long-term care - covers specific costs of custodial care in a nursing facility or at home. Renters - protects from losses due to damage to the contents of a dwelling rather than the dwelling itself.

Insurance deductible - a set amount an insured person must pay per loss before the insurance company will pay a claim.

Insurance premium - the payment a person makes to an insurance company in exchange for its promise of protection and help.

Interest - payment for the use of someone else’s money; usually expressed as an annual rate in terms of a percent of the principal (the amount owed).

Interest income - money that financial institutions, governments, or corporations pay for the use of investors’ money.

5/7/2023 BVSD Curriculum Essentials 30

Interest rate - the percentage rate of interest charged to the borrower or paid to a lender, saver, or investor.

Investing - purchasing securities such as stocks, bonds, and mutual funds with the goal of increasing wealth over time, but with the risk of loss. Setting aside money for future income, benefit, or profit to meet long-term goals; using savings to earn a financial return.

Investments - the amount of money invested in stocks, bonds, mutual funds, and other investment instruments.

Job - a position of employment with specific duties and compensation. See Career. Lease/leasing - a written contract specifying the terms for the use of an asset and the legal responsibilities of both parties to the agreement, such as a property owner and tenant. Liability - an actual or potential financial obligation. Life expectancy - a statistical measure of the average length of life from birth to death. Liquidity - the quality of an asset that permits it to be converted quickly into cash without loss of value. For example, a mutual fund is more liquid than real estate. Living will - a document that contains the signer’s desires for specific medical treatment in case the person is unable to make medical decisions; also known as a health care directive.

Loan – a contractual promise between a borrower and a lender; the borrower agrees to repay a sum of money (generally with interest) in exchange for the lender giving another sum of money.

Loan shark - an unlicensed person who lends money at an exorbitant rate of interest.

Medicaid - a program financed by state and federal government tax revenues, to pay specified health care costs care for those who cannot afford them.

Medicare - a federal government program, financed by deductions from wages, that pays for certain health care expenses for older citizens. The Social Security Administration manages the program.

Money - anything that is generally accepted as payment for goods and services; a medium of exchange; legal tender.

Mortgage - a long-term loan to buy real estate; that is, land and the structures on it.

Mortgage company - a firm or individual who brings the borrower and lender together, receiving a commission if a sale results.

Mutual fund - an investment tool that pools the money of many shareholders and invests it in a diversified portfolio of securities, such as stocks, bonds, and money market assets.

Needs - essentials or basics necessary for maintaining physical life including food, clothing, water, and shelter, sometimes called material well-being.

Net worth - a measure of a person’s financial condition at a given time, equal to what that person owns (assets) minus what that person owes (liabilities).

NSF (Non-Sufficient Funds) - an NSF is issued by a bank when there is not enough money in the account to cover the amount of the check or transaction.

Online commerce - buying and selling goods and services electronically, primarily utilizing Web-based companies or sites.

5/7/2023 BVSD Curriculum Essentials 31

Open-end credit - an agreement with a financial institution that gives a borrower the use of money up to a specified limit for an indefinite time as long as repayment of the outstanding balance and finance charge proceeds on schedule; also known as revolving credit or a revolving line of credit. A credit card is an example. Opportunity cost - the value of the second-best alternative that a person gives up when making one choice instead of another. Pawnshop - an easy-access credit business that makes high-interest loans secured by personal property collateral, such as jewelry. Payday loan - an easy-access credit business that makes high interest loans for the period of the borrower’s pay cycle. This practice is illegal in some states. Payment method - the means of settling a financial obligation, such as by cash, check, credit card, debit card, smart card, or stored value card. Payroll deductions - an amount an employer withholds from a paycheck. Mandatory deductions include various taxes. Voluntary deductions include loan payments, charitable contributions, and direct deposits into financial institution accounts. Pay Yourself First (PYF) - disciplined saving or setting aside money as a regular part of the budget for later spending or investing. Peer pressure - the influence that a social group has on an individual, based on the individual’s desire for the group’s approval. Pension Protection Act - a federal law that attempts to strengthen employees’ retirement security by, among other things, allowing employers to automatically enroll employees in retirement savings plans. Personal finance - the principles and methods that individuals use to acquire and manage income and assets. Personal income - an individual's total annual income received from all sources, including wages, salaries, investments, etc.; also called "before-tax income". Personal income tax - taxes paid on personal income to the state and federal governments. Philanthropy - the act of voluntarily contributing to others’ welfare. Phishing - an attempt to criminally and fraudulently acquire sensitive information, such as usernames, passwords, and credit card details, by posing as a trustworthy entity in an electronic communication such as an email.

Portfolio - a collection of securities—such as stocks, bonds, mutual funds, and real estate—that an individual investor owns.

Points—mortgage - a one-time service charge by mortgage lenders at closing to increase the return on the loan; each point is one percent of the amount of the principal.

Predatory Lending Practices - any of a number of fraudulent, deceptive, discriminatory, or unfavorable lending practices. Many of these practices are illegal, while others are legal but not in the best interest of the borrowers. Lending practices which promise loans that are ―too good to be true‖ and pressure borrowers to take loans on the spot. Lending practices include a variety of financial abuses such as excessive fees, penalties for early pay-off of the loan, balloon payments, loan flipping, high interest rates, monthly payments the borrower can not afford, and unauthorized refinancing of loans. Examples of the practice include predatory mortgages, payday loans, overdraft loans, excessive credit card debt, and instant tax refund loans.

Principle - 1. an amount of money originally invested, excluding any interest or dividends. 2. an amount borrowed, or an outstanding loan balance.

Privacy - freedom from unauthorized release of personal information.

Probate court - the government institution with jurisdiction over a deceased person’s will and estate.

Profit - the positive difference between total revenue and total expenses of a business or investment.

5/7/2023 BVSD Curriculum Essentials 32

Property tax - a tax on land and structures built on it; payments go to state and/or local governments to pay for police protection, public schools, libraries, etc.

Prospectus - a legal document that provides detailed information about mutual funds, stocks, bonds, and other investments offered for sale, as required by the Securities and Exchange Commission (SEC).

Purchasing Power - the value of money measured in the amount of goods and services that can be bought with it.

Pyramid Scheme - an illegal scheme of selling goods. Participants are recruited by advertisements offering big profits to those who pay a fee for agency rights, that is, rights to sell goods as a representative of the pyramid company. Each recruited agent then recruits others to join, with each new participant paying a fee to join. The key is that each person is promised commissions not only on his or her sales but also on the sales of other people they recruit as distributors.

Rate of return - how fast money in savings account or investment grows. Annual earnings on an investment expressed as a percentage of the amount invested; also known as yield. Example: A $3 annual dividend divided by $34 share cost = 0.088, an 8.8% rate of return. Reconcile - the process of comparing personal bank account records to the bank's records of that account balance in order to uncover any possible discrepancies.

Recordkeeping - the process of keeping an orderly account of a person’s financial affairs, including income earned, taxes paid, household expenditures, loans, insurance policies, and legal documents.

Renting - paying a periodic fee for the use of property. Rent-to-own - a plan to buy a product with little or no down payment by renting it until the final payment is made, at which point the total paid far exceeds the product’s purchase price.

Repossession - confiscation of collateral, often without notice, if a borrower defaults on a loan.

Resources - human resources are those resources people have within themselves, such as working knowledge, skill, mental effort, motivation, energy. Non-human or external resources include money, time, and equipment.

Retirement - the point where a person stops employment completely, usually when reaching a specific age or when physical conditions prevent the person from working any longer. Retirement may also be a personal choice with an adequate amount of financial planning.

Retirement accounts - accounts such as IRAs (Individual Retirement Accounts), annuities and 401Ks that allow individuals to save money toward retirement on a tax-deferred basis.

Return on investment - the measure of profitability of an investment.

Reverse Mortgage - an arrangement in which a homeowner borrows against the equity in his/her home and receives regular monthly tax-free payments from the lender. This is also called reverse-annuity mortgage or home equity conversion mortgage.

Risk - a measure of the likelihood of loss or profit; the uncertainty of an investment’s rate of return. Possible losses involving income or standard of living. The possibility of a loss from perils to people or property covered by insurance.

Risk management - the process of calculating risk and devising methods to minimize or manage loss, for example, by buying insurance or diversifying investments.

5/7/2023 BVSD Curriculum Essentials 33

Risk tolerance - the amount of uncertainty or possibility of loss the individual can bear.

Rule of 72 - how long it takes money to double in value. A rough calculation of the time or interest rate needed to double the value of an investment. Divide 72 by the interest rate to determine the number of years it will take money to double. Calculating interest on both principal and previously earned interest. For example: to figure how many years it will take to double a lump sum invested at an annual rate of 8%, divide 72 by 8, for a result of 9 years.

Salary - compensation for work expressed as an annual sum and paid in prorated portions regularly-usually weekly, bi-weekly, or monthly. See Wage.

Sales Tax - tax paid as percent of the cost of a good or service; paid to local and state governments when goods and services are purchased.

Saving - the process of setting income aside for future spending. Saving provides ready cash for emergencies and short-term goals, and funds for investing.

Savings - money set aside for a future use that is held in easily accessed accounts, such as savings accounts and certificates of deposit (CDs).

Savings account - a financial institution deposit account that pays interest and allows withdrawals.

Savings bond - a document representing a loan of more than one year to the U.S. government, to be repaid, with interest on a specified date.

Scam, rip-off - a fraudulent or deceptive act. Swindle or fraud, especially to cheat or swindle by a con artist in a confidence game (e.g., home repairs, cell phones, gasoline and oil stocks, Internet, telemarketing, credit card, securities, pyramid schemes). See Fraud.

Scarcity - an economic condition created by an excess of human wants over the resources necessary to satisfy them; an inability to satisfy all of everyone’s wants.

Scholarships - money for college that do not have to be repaid, which is awarded for merit or achievement. Eligibility for scholarships can be based on many criteria, including academics, athletics, ethnicity, religious affiliation, and special interests.

Security - 1. a legal agreement that records a debt or equity obligation from a corporation, government, or other organization. (e.g., stocks and bonds). 2. collateral for a loan.

Shared Risk – Insurance Principle - using premiums from many policyholders to reimburse the losses of a few, so that no one suffers a financially devastating loss.

Simple interest - interest calculated periodically on loan principal or investment principal only, not on previously earned interest.

Social Security - a federal government program that provides retirement, survivor’s, and disability benefits, funded by a tax on income, which appears on workers’ pay stubs as a deduction labeled FICA (for Federal Insurance Contributions Act, the enabling legislation).

Spending plan - another name for budget.

Standard of living - the overall degree of comfort of an individual, household, or population, as measured by the amount of goods and services its members consume.

Stock - an investment that represents shares of ownership of the assets and earnings of a corporation.

5/7/2023 BVSD Curriculum Essentials 34

Stored-value card - a prepaid plastic card that allows purchases up to a set limit, at which point the card is discarded or; if ―rechargeable, replenished from an account.

Supply - the quantities of an item that producers are willing and able to make available for sale at various prices over a given time period.

Supply and Demand - the relationship between the quantity consumers are willing and able to buy and the quantity producers are willing and able to produce; the point of agreement (quantity supplied equals quantity demanded) is where prices are set in a market-based economy.

Take-home pay - gross wage or salary, plus bonuses, minus deductions such as taxes, health care premiums, and retirement savings.

Taxes - government fees on business and individual income, activities, or products to support government programs.

Tax credit - an amount that a taxpayer who meets certain criteria can subtract from tax owed. Examples include a credit for earned income below a certain limit and for qualified postsecondary school expenses. See Tax deduction and Tax exemption.

Tax deduction - an expense that a taxpayer can subtract from taxable income. Examples include deductions for home mortgage interest and for charitable gifts. See Tax credit and Tax exemption.

Tax deferral - the feature of an investment in which taxes due on principal and/or earnings are postponed until funds are withdrawn, often at retirement.

Tax exemption - earnings, such as interest from municipal bonds that are free of certain taxes. See Tax credit and Tax deduction.

Time value of money - the relationship between time, money, and rate of return (interest), and their effect on earnings growth. The more time, money, and rate of interest, the more money yielded at the end of a period of time.

Title loan - a high-cost, short-term loan that uses the borrower’s automobile as collateral.

Transfer payment - money that a government provides to citizens for reasons other than current employment or the delivery of goods or services in exchange. Examples include Social Security, veteran’s benefits, and welfare.

Trust - a legal arrangement through which a trust or manages a trustee’s assets for the good of one or more beneficiaries. Truth in Lending Act - a federal law that requires financial institutions to disclose specific information about the terms and cost of credit, including the finance charge and the annual percentage rate (APR).

Truth in Savings Act - a federal law that requires financial institutions to disclose specific information about the terms and costs of interest-earning accounts—such as annual percentage yield (APY)—and certain other financial services.

Unearned income - earnings from sources other than employment, including investment returns and royalties.

Utilities - services such as telephone, water, garbage collection, gas, and electric.

5/7/2023 BVSD Curriculum Essentials 35

Value judgment - the process of reasoning to a conclusion using facts and values for purposes of determining worth, quality, importance, fairness, and credibility.

Value system - a set of criteria, standards, or principles that guide an individual or group’s behavior and provides a sense of direction to life.

Value (individual) - an individual’s beliefs about what is important, desirable, and worthwhile, which often influence decisions.

Vision-financial - a description of (a) how an individual defines future financial success, and (b) what he/she wants to accomplish; provides direction for decision and actions that invent the preferred future: What will the future look like if financial strategies are successfully implemented and one’s full potential is achieved?

Volunteer Service - working to help others or one’s community without being paid.

Wage - compensation for work usually calculated on an hourly, daily, or piecework basis and paid on schedule—usually weekly, biweekly, or monthly. See Salary.

Wants - items that a person would like to have but are not essential for life. Items, activities, or services that may increase the quality of life, but one can live without them.

Wealth - accumulated assets; positive net worth.

Wealth building - increasing the total value of what one owns; one’s tangible assets using strategies to increase savings and personal asset accumulation, thereby promoting individual/family economic well-being and financial security.

Welfare - aid in the form of money or necessities for those in need; often from a government program.

Will - a legal declaration of a person’s wishes for the disposition of his or her estate after death.

Withholding - employer deductions from employees’ earnings to pay employees’ taxes.

Work/Job - employment; occupation; effort exerted to make or do something. On a relative basis, short-term work or tasks completed for pay.

5/7/2023 BVSD Curriculum Essentials 36

Properties of the CED

Finance

Finance

B42

This course is designed to help students develop their abilities to make wise consumer decisions by recognizing, understanding, and comparing the alternatives facing them as consumers. Budgeting, purchasing decisions and consumer credit, banking services, investing, life, auto, and property insurance, income taxes and housing are some of the topics covered. This course satisfies the Boulder Valley School District’s Personal Financial Literacy (PFL) graduation requirement.

1 Semester

[Course Fees]

5

[Elective Required]

Active

Businesse50629da-8d86-4b17-ade7-4be88fe11c71

1/1/1980[Expiration Date]

[NCAA]

[Hear]

Practical Experiences; Electives

[NonAcademic]

0300 - Business

Business

5/7/2023 BVSD Curriculum Essentials 37