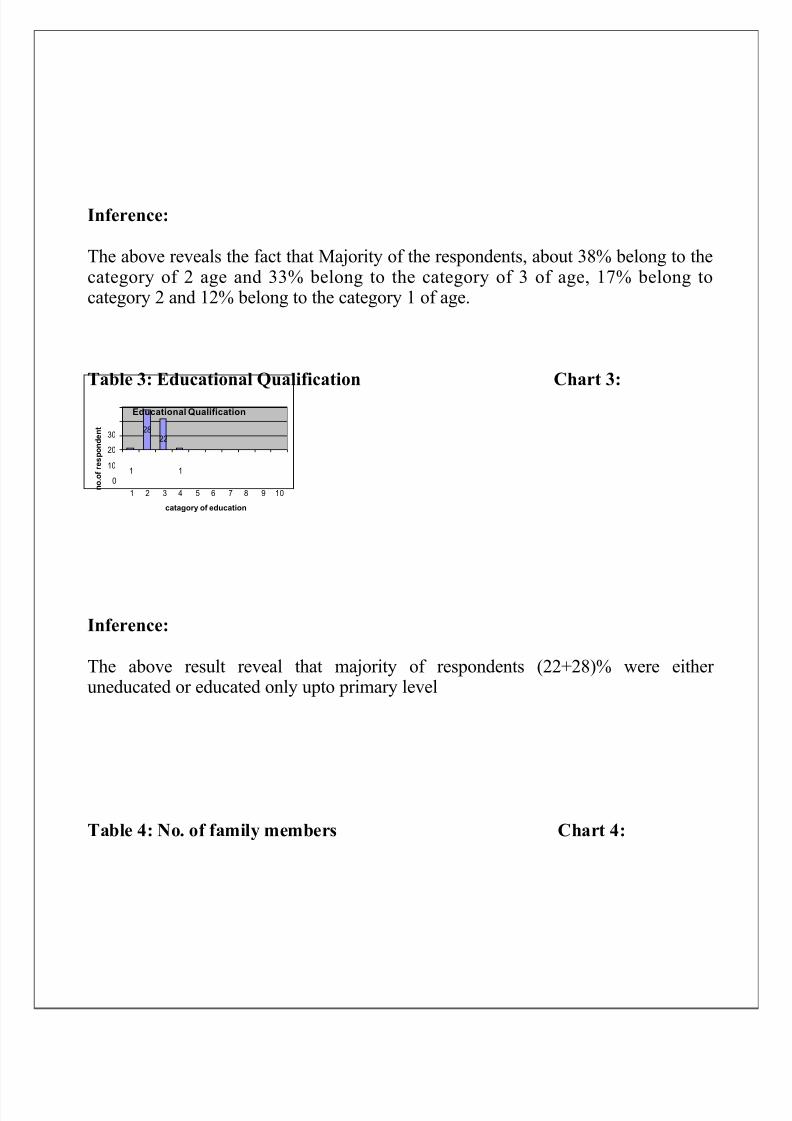

finance in micro insurance with referance to sharekhan

TRANSCRIPT

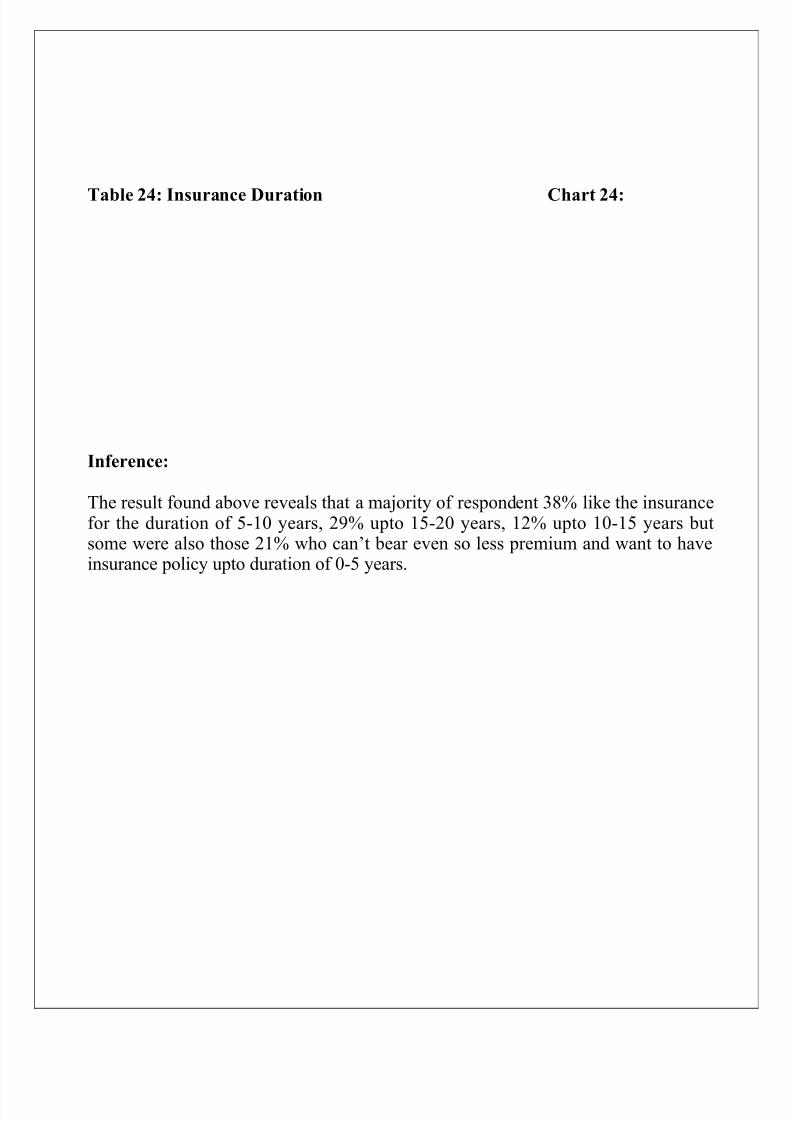

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 1/64

PROJECT ON

“FINANCE IN MICRO INSURANCE ”

PREPARED BY

HARDIK S. MODI

ROLL NO:-22

T.Y.B.B.I. (BANKING AND INSURANCE)

SEMISTER-VI, YEAR-2010-11

UNDER THE GUIDANCE OF

PROF. SHRADDHA SHUKLA

SUBMITTED TO

SHAILENDRA EDUCATION SOCIETY’S

ARTS, SCIENCE, COMMERCE COLLEGE

DAHISAR (E), MUMBAI-400068

(NAAC ACCREDITATED B+)

(AFFILIATED TO UNIVERSITY OF MUMBAI)

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 2/64

ACKNOWLEDGEMENT

I take this opportunity to express my sincere gratitude to the staff of

SHAILENDRA COLLEGE. I specially thank “SHRADDHA SHUKLA” for

creating out the study and for their guidance and encouragement that made the

project very effective and easy.

I sincerely express my gratitude to MRS. ANUJA JADHAV, – LIBRARIAN,

for his guidance and support throughout my project.

I would like to thank AMEY AND YASH, for guiding and directing me in the

process of making this project report and for all the support and encouragement.

I am grateful to our Internal PRINCIPAL Mr. INGAVALE for his support

and assistance in Completion of my project work.

INDUSTRY PROFILE

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 3/64

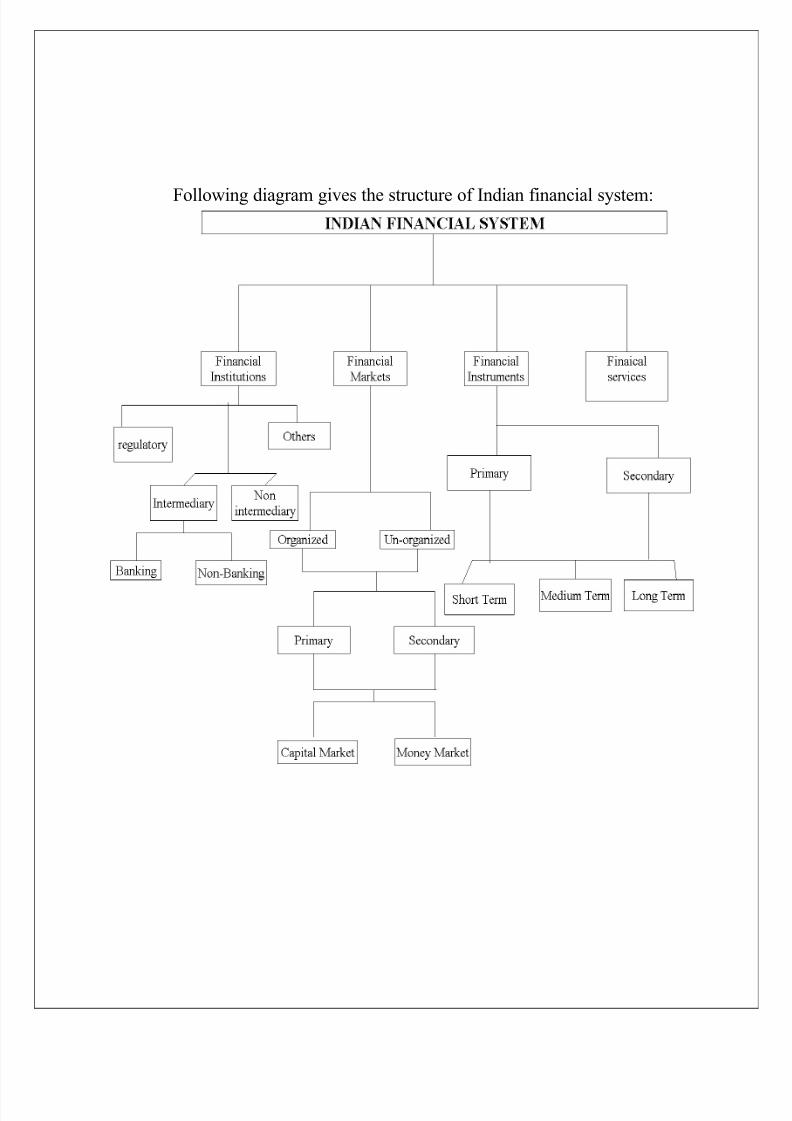

Following diagram gives the structure of Indian financial system:

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 4/64

Contents

Foreword....................................................................................................... i

Introduction...................................................................................................1

• Development of Micro-insurance in India........................................3

• Supply and Demand Side Developments ........................................5

3.1Supplyofmicroinsurance..................................................................5

3.2 Demand for micro-insurance...............................................................6

• On Extending Micro-insurance .......................................................10

4.1 Flexibility in Premium........ ................................................................11

4.2 Micro-insurance and micro-finance ...................................................16

• Conclusions.......................................................................................20

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 5/64

FINANCIAL MARKET:

Financial markets are helpful to provide liquidity in the system and for smooth

functioning of the system. These markets are the centers that provide facilities for

buying and selling of financial claims and services. The financial markets match

the demands of investment with the supply of capital from various sources.

According to functional basis financial markets are classified into two types.

They are:

➢ Money markets (short-term)

➢ Capital markets (long-term)

According to institutional basis again classified in to two types. They are

➢ Organized financial market

➢ Non-organized financial market.

The organized market comprises of official market represented by recognized

institutions, bank and government (SEBI) registered/controlled activities and

intermediaries. The unorganized market is composed of indigenous bankers,

moneylenders, individual professional and non-professionals.

MONEY MARKET:

Money market is a place where we can raise short-term capital.

Again the money market is classified in to

➢ Inter bank call money market

➢ Bill market and

➢ Bank loan market Etc.

➢ E.g.; treasury bills, commercial papers, CD's etc.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 6/64

CAPITAL MARKET:

Capital market is a place where we can raise long-term capital.

Again the capital market is classified in to two types and they are

➢ Primary market and

➢ Secondary market.

E.g.: Shares, Debentures, and Loans etc.

PRIMARY MARKET:

Primary market is generally referred to the market of new issues or market for

mobilization of resources by the companies and government undertakings, for

new projects as also for expansion, modernization, addition, diversification and

up gradation. Primary market is also referred to as New Issue Market. Primary

market operations include new issues of shares by new and existing companies,further and right issues to existing shareholders, public offers, and issue of debt

instruments such as debentures, bonds, etc.

The primary market is regulated by the Securities and Exchange Board of India

(SEBI a government regulated authority).

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 7/64

FUNCTION:

The main services of the primary market are origination, underwriting, and

distribution. Origination deals with the origin of the new issue. Underwriting

contract make the shares predictable and remove the element of uncertainty in the

subscription. Distribution refers to the sale of securities to the investors.

The following are the market intermediaries associated with the market:

1. Merchant banker/book building lead manager

2. Registrar and transfer agent

3. Underwriter/broker to the issue

4. Adviser to the issue

5. Banker to the issue

6. Depository

7. Depository participant

INVESTORS’ PROTECTION IN THE PRIMARY MARKET:

To ensure healthy growth of primary market, the investing public should be

protected. The term investor protection has a wider meaning in the primary

market. The principal ingredients of investors’ protection are:

➢ Provision of all the relevant information

➢ Provision of accurate information and

➢ Transparent allotment procedures without any bias.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 8/64

SECONDARY MARKET

The primary market deals with the new issues of securities. Outstanding

securities are traded in the secondary market, which is commonly known as stock

market or stock exchange. “The secondary market is a market where scrip’s are

traded”. It is a market place which provides liquidity to the scrip’s issued in theprimary market. Thus, the growth of secondary market depends on the primary

market. More the number of companies entering the primary market, the greater

are the volume of trade at the secondary market. Trading activities in the

secondary market are done through the recognized stock exchanges which are 23

in number including Over the Counter Exchange of India (OTCE), National

Stock Exchange of India and Interconnected Stock Exchange of India.

Secondary market operations involve buying and selling of securities on the stock

exchange through its members. The companies hitting the primary market are

mandatory to list their shares on one or more stock exchanges in India.

Listing of scrip’s provides liquidity and offers an opportunity to the investors to

buy or sell the scrip’s.

The following are the intermediaries in the secondary market:

1. Broker/member of stock exchange – buyers broker and sellers broker

2. Portfolio Manager

3. Investment advisor

4. Share transfer agent

5. Depository

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 9/64

6. Depository participants.

STOCK MARKETS IN INDIA:

Stock exchanges are the perfect type of market for securities whether of

government and semi-govt bodies or other public bodies as also for shares and

debentures issued by the joint-stock companies. In the stock market, purchases

and sales of shares are affected in conditions of free competition. Government

securities are traded outside the trading ring in the form of over the counter sales

or purchase. The bargains that are struck in the trading ring by the members of

the stock exchanges are at the fairest prices determined by the basic laws of

supply and demand.

Definition of a stock exchange:

“Stock exchange means any body or individuals whether incorporated or not,

constituted for the purpose of assisting, regulating or controlling the business of

buying, selling or dealing in securities.” The securities include:

➢ Shares of public company.

➢ Government securities.

➢ Bonds

HISTORY OF STOCK EXCHANGES:

The only stock exchanges operating in the 19th century were those of Mumbai

setup in 1875 and Ahmedabad set up in 1894. These were organized as voluntary

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 10/64

non-profit-marking associations of brokers to regulate and protect their interests.

Before the control on securities under the constitution in 1950, it was a state

subject and the Bombay securities contracts (control) act of 1925 used to regulate

trading in securities. Under this act, the Mumbai stock exchange was recognized

in 1927 and Ahmedabad in 1937. During the war boom, a number of stock

exchanges were organized. Soon after it became a central subject, central

legislation was proposed and a committee headed by A.D.Gorwala went into the

bill for securities regulation. On the basis of the committee’s recommendations

and public discussion, the securities contract (regulation) act became law in 1956.

FUNCTIONS OF STOCK EXCHANGES:

Stock exchanges provide liquidity to the listed companies. By giving quotations

to the listed companies, they help trading and raise funds from the market. Over

the hundred and twenty years during which the stock exchanges have existed inthis country and through their medium, the central and state government have

raised crores of rupees by floating public loans. Municipal corporations, trust and

local bodies have obtained from the public their financial requirements, and

industry, trade and commerce- the backbone of the country’s economy-have

secured capital of crores or rupees through the issue of stocks, shares and

debentures for financing their day-to-day activities, organizing new ventures and

completing projects of expansion, diversification and modernization. By

obtaining the listing and trading facilities, public investment is increased and

companies were able to raise more funds. The quoted companies with wide

public interest have enjoyed some benefits and assets valuation has become easier

for tax and other purposes.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 11/64

VARIOUS STOCK EXCHANGES IN INDIA:

At present there are 23 stock exchanges recognized under the securities contracts

(regulation), Act, 1956. Those are:

Ahmedabad Stock Exchange Association Ltd.

Bangalore Stock Exchange

Bhubaneshwar Stock Exchange Association

Calcutta Stock Exchange

Cochin Stock Exchange Ltd.

Coimbatore Stock Exchange

Delhi Stock Exchange Association

Guwahati Stock Exchange Ltd

Hyderabad Stock Exchange Ltd.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 12/64

Jaipur Stock Exchange Ltd

Kanara Stock Exchange Ltd

Ludhiana Stock Exchange Association Ltd

Madras Stock Exchange

Madhya Pradesh Stock Exchange Ltd.

Magadh Stock Exchange Limited

Meerut Stock Exchange Ltd.

Mumbai Stock Exchange

National Stock Exchange of India

OTC Exchange of India

Pune Stock Exchange Ltd.

Saurashtra Kutch Stock Exchange Ltd.

Uttar Pradesh Stock Exchange Association

Vadodara Stock Exchange Ltd.

Out of these major stock exchanges were:

1. NSE (National Stock Exchange)

2. BSE (Bombay Stock Exchange)

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 13/64

NSE (National Stock Exchange):

The National Stock Exchange of India Limited has genesis in the report of the

High Powered Study Group on Establishment of New Stock Exchanges, which

recommended promotion of a National Stock Exchange by financial institutions

(FI’s) to provide access to investors from all across the country on an equal

footing. Based on the recommendations, NSE was promoted by leading Financial

Institutions at the behest of the Government of India and was incorporated in

November 1992 as a tax-paying company unlike other stock exchanges in the

country. On its recognition as a stock exchange under the Securities Contracts

(Regulation) Act, 1956 in April 1993, NSE commenced operations in theWholesale Debt Market (WDM) segment in June 1994. The Capital Market

(Equities) segment commenced operations in November 1994 and operations in

Derivatives segment commenced in June 2000

NSE's mission is setting the agenda for change in the securities markets in India.

The NSE was set-up with the main objectives of:

•Establishing a nation-wide trading facility for equities and debt instruments.

• Ensuring equal access to investors all over the country through an appropriate

communication network.

• Providing a fair, efficient and transparent securities market to investors using

electronic trading systems.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 14/64

• Enabling shorter settlement cycles and book entry settlements systems, and

•

Meeting the current international standards of securities markets.

The standards set by NSE in terms of market practices and technology, have

become industry benchmarks and are being emulated by other market

participants. NSE is more than a mere market facilitator. It's that force which is

guiding the industry towards new horizons and greater opportunities.

BSE (Bombay Stock Exchange):

The Stock Exchange, Mumbai, popularly known as "BSE" was established in

1875 as "The Native Share and Stock Brokers Association". It is the oldest one in

Asia, even older than the Tokyo Stock Exchange, which was established in 1878.

It is a voluntary non-profit making Association of Persons (AOP) and is currently

engaged in the process of converting itself into demutualised and corporate entity.

It has evolved over the years into its present status as the premier Stock Exchange

in the country. It is the first Stock Exchange in the Country to have obtainedpermanent recognition in 1956 from the Govt. of India under the Securities

Contracts (Regulation) Act 1956.The Exchange, while providing an efficient and

transparent market for trading in securities, debt and derivatives upholds the

interests of the investors and ensures redresses of their grievances whether

against the companies or its own member-brokers. It also strives to educate and

enlighten the investors by conducting investor education programmers and

making available to them necessary informative inputs.

A Governing Board having 20 directors is the apex body, which decides the

policies and regulates the affairs of the Exchange. The Governing Board consists

of 9 elected directors, who are from the broking community (one third of them

retire ever year by rotation), three SEBI nominees, six public representatives and

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 15/64

an Executive Director & Chief Executive Officer and a Chief Operating Officer.

The Executive Director as the Chief Executive Officer is responsible for the day-

to-day administration of the Exchange and the Chief Operating Officer and other

Heads of Department assist him.

The Exchange has inserted new Rule No.126 A in its Rules, Byelaws pertaining

to constitution of the Executive Committee of the Exchange. Accordingly, an

Executive Committee, consisting of three elected directors, three SEBI nominees

or public representatives, Executive Director & CEO and Chief Operating Officer

has been constituted. The Committee considers judicial & quasi matters in which

the Governing Board has powers as an Appellate Authority, matters regarding

annulment of transactions, admission, continuance and suspension of member-

brokers, declaration of a member-broker as defaulter, norms, procedures and

other matters relating to arbitration, fees, deposits, margins and other monies

payable by the member-brokers to the Exchange, etc.

REGULATORY FRAME WORK OF STOCK EXCHANGE

A comprehensive legal framework was provided by the “Securities Contract

Regulation Act, 1956” and “Securities Exchange Board of India 1952”. Three tier

regulatory structure comprising

➢ Ministry of finance

➢ The Securities And Exchange Board of India

➢ Governing body

MEMBERS OF THE STOCK EXCHANGE:

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 16/64

The securities contract regulation act 1956 has provided uniform regulation for

the admission of members in the stock exchanges. The qualifications for

becoming a member of a recognized stock exchange are given below:

• The minimum age prescribed for the members is 21 years.

• He should be an Indian citizen.

• He should be neither a bankrupt nor compound with the creditors.

• He should not be convicted for fraud or dishonesty.

• He should not be engaged in any other business connected with a company.

• He should not be a defaulter of any other stock exchange.

• The minimum required education is a pass in 12 th standard examination.

SECURITIES AND EXCHANGE BOARD OF INDIA (SEBI)

The securities and exchange board of India was constituted in 1988 under a

resolution of government of India. It was later made statutory body by the SEBI

act 1992.according to this act, the SEBI shall constitute of a chairman and four

other members appointed by the central government.

With the coming into effect of the securities and exchange board of India act,

1992 some of the powers and functions exercised by the central government, in

respect of the regulation of stock exchange were transferred to the SEBI.

OBJECTIVES AND FUNCTIONS OF SEBI

• To protect the interest of investors in securities.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 17/64

• Regulating the business in stock exchanges and any other securities

market.

• Registering and regulating the working of intermediaries associated with

securities market as well as working of mutual funds.

• Promoting and regulating self-regulatory organizations.

• Prohibiting insider trading in securities.

• Regulating substantial acquisition of shares and take over of companies.

• Performing such functions and exercising such powers under the

provisions of capital issues (control) act, 1947and the securities to it by the

central government.

SEBI GUIDELINES TO SECONDARY MARKETS: STOCK EXCHANGES

•

Board of Directors of Stock Exchange has to be reconstituted so as to includenon-members, public representatives and government representatives to the

extent of 50% of total number of members.

• Capital adequacy norms have been laid down for the members of various

stock exchanges depending upon their turnover of trade and other factors.

• All recognized stock exchanges will have to inform about transactions within

24 hrs.

TYPES OF ORDERS:

Buy and sell orders placed with members of the stock exchange by the investors.

The orders are of different types.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 18/64

LIMIT ORDERS:

Orders are limited by a fixed price. E.g. ‘buy Reliance Petroleum at

Rs.50.’Here, the order has clearly indicated the price at which it has to be bought

and the investor is not willing to give more than Rs.50.

Best rate order: Here, the buyer or seller gives the freedom to the broker to

execute the order at the best possible rate quoted on the particular date for

buying. It may be lowest rate for buying and highest rate for selling.

Discretionary order: The investor gives the range of price for purchase and sale.

The broker can use his discretion to buy within the specified limit. Generally the

approximation price is fixed. The order stands as this “buy BRC 100 shares

around Rs.40”.

STOP LOSS ORDER :

The orders are given to limit the loss due to unfavorable price movement in

the market. A particular limit is given for waiting. If the price falls below the

limit, the broker is authorized to sell the shares to prevent further loss. E.g. Sell

BRC limited at Rs.24, stop loss at Rs.22.

Buying and selling shares: To buy and sell the shares the investor has to locate

register broker or sub broker who render prompt and efficient service to him. The

order to buy or sell specifying the number of shares of the company of investors’

choice is placed with the broker. The order may be of any type. After receiving

the order the broker tries to execute the order in his computer terminal. Once

matching order is found, the order is executed. The broker then delivers the

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 19/64

contract note to the investor. It gives the details regarding the name of the

company, number of shares bought, price, brokerage, and the date of delivery of

share. In this physical trading form, once the broker gets the share certificate

through the clearing houses he delivers the share certificate along with transfer

deed to the investor. The investor has to fill the transfer deed and stamp it. The

stamp duty is one of the percentage considerations, the investor should lodge the

share certificate and transfer deed to the register or transfer agent of the company.

If it is bought in the DEMAT form, the broker has to give a matching instruction

to his depository participant to transfer shares bought to the investors account.

The investor should be account holder in any of the depository participant. In the

case of sale of shares on receiving payment from the purchasing broker, the

broker effects the payment to the investor.

Share groups: The scrips traded on the BSE have been classified into

‘A’,’B1’,’B2’,’C’,’F’ and ‘Z’ groups. The ‘A’ group represents those, which are inthe carry forward system. The ‘F’ group represents the debt market segment (fixed

income securities). The Z group scrips are of the blacklisted companies. The ‘C’

group covers the odd lot securities in ‘A’, ‘B1’&’B2’ groups.

ROLLING SETTLEMENT SYSTEM:

Under rolling settlement system, the settlement takes place in days (usually 1,

2, 3 or 5days) after the trading day. The shares bought and sold are paid in for n

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 20/64

days after the trading day of the particular transaction. Share settlement is likely

to be completed much sooner after the transaction than under the fixed settlement

system.

The rolling settlement system is noted by T+N i.e. the settlement period is n

days after the trading day. A rolling period which offers a large number of days

negates the advantages of the system. Generally longer settlement periods are

shortened gradually.

SEBI made RS compulsory for trading in 10 securities selected on the basis of

the criteria that they were in compulsory demat list and had daily turnover of

about Rs.1 crore or more. Then it was extended to “A” stocks in Modified Carry

Forward Scheme, Automated Lending and Borrowing Mechanism (ALBM) and

Borrowing and lending Securities Scheme (BELSS) with effect from Dec 31,

2001.

SEBI has introduced T+5 rolling settlement in equity market from July 2001

and subsequently shortened the cycle to T+3 from April 2002. After the T+3

rolling settlement experience it was further reduced to T+2 to reduce the risk in

the market and to protect the interest of the investors from 1 st April 2003.

Activities on T+1: conformation of the institutional trades by the custodian is

sent to the stock exchange by 11.00 am. A provision of an exception window

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 21/64

would be available for late confirmation. The time limit and the additional

changes for the exception window are dedicated by the exchange.

The exchanges/clearing house/ clearing corporation would process and download

the obligation files to the broker’s terminals late by 1.30 p.m on T+1. Depository

participants accept the instructions for pay in securities by investors in physical

form upto 4 p.m and in electronic form upto 6 p.m. the depositories accept from

other DPs till 8p.m for same day processing.

Activities on T+2: The depository permits the download of the paying in files

of securities and funds till 10.30 a.m on T+2 from the brokers’ pool accounts.

The depository processes the pay in requests and transfers the consolidated pay in

files to clearing House/clearing Corporation by 11.00am/on T+2. The

exchange/clearing house/clearing corporation executes the pay-out of securities

and funds latest by 1.30 p.m on T+2 to the depositories and clearing banks. In the

demat mode net basis settlement is allowed. The buy and sale positions in thesame scrip can be settled and net quantity has to be settled.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 22/64

COMPANY PROFILE

ABOUT SHAREKHAN LIMITED

Sharekhan Limited is one of the fastest growing financial services providers

with a focus on equities, derivatives and commodities brokerage execution on the

National Stock Exchange of India Ltd. (NSE), Bombay Stock Exchange Ltd. (BSE),

National Commodity and Derivatives Exchange India (NCDEX) and Multi

Commodity Exchange of India Ltd. (MCX). Sharekhan provides trade execution

services through multiple channels - an Internet platform, telephone and retail outlets

and is present in 280 cities through a network of 704 locations. The company was

awarded the 2005 Most Preferred Stock Broking Brand by Awwaz Consumer Vote.

ORIGIN

➢ Sharekhan traces its lineage to SSKI, an organization with more than decades

of trust and credibility in the stock market.

➢ Pioneers of online trading in India- Sharekhan.com was launched in 2000 and

is now the second most visited broking site in India.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 23/64

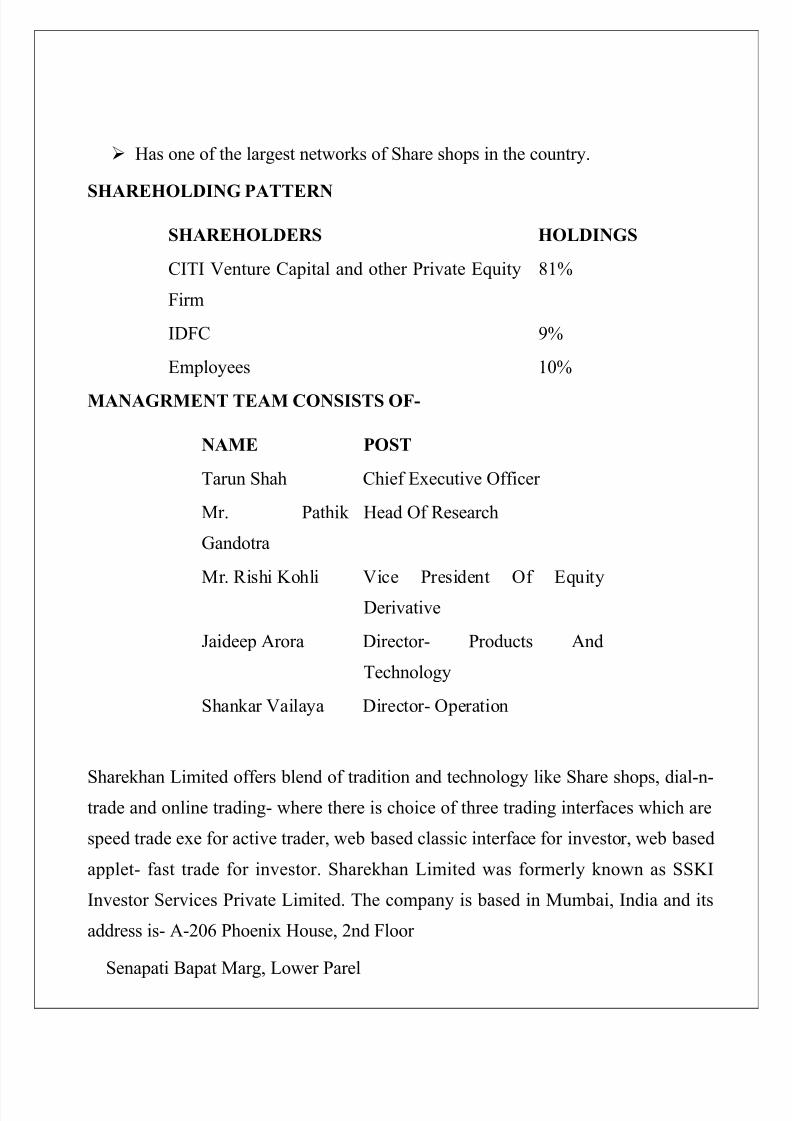

➢ Has one of the largest networks of Share shops in the country.

SHAREHOLDING PATTERN

SHAREHOLDERS HOLDINGS

CITI Venture Capital and other Private Equity

Firm

81%

IDFC 9%

Employees 10%

MANAGRMENT TEAM CONSISTS OF-

NAME POST

Tarun Shah Chief Executive Officer

Mr. Pathik

Gandotra

Head Of Research

Mr. Rishi Kohli Vice President Of Equity

Derivative

Jaideep Arora Director- Products And

Technology

Shankar Vailaya Director- Operation

Sharekhan Limited offers blend of tradition and technology like Share shops, dial-n-trade and online trading- where there is choice of three trading interfaces which are

speed trade exe for active trader, web based classic interface for investor, web based

applet- fast trade for investor. Sharekhan Limited was formerly known as SSKI

Investor Services Private Limited. The company is based in Mumbai, India and its

address is- A-206 Phoenix House, 2nd Floor

Senapati Bapat Marg, Lower Parel

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 24/64

Mumbai, 400 013. India

Phone: 91 22 24982000

Fax: 91 22 24982626

www.sharekhan.com

Advanced Technology Used By Sharekhan

Sharekhan selected Aspect® EnsemblePro™ from the Aspect Software Unified IP

Contact Center product line, a unified contact centre solution delivering advanced

multichannel contact capabilities, because it provided the best total value over other

solutions evaluated. It enabled Sharekhan to meet customer service needs for

inbound call handling, voice self service, predictive outbound dialing, call blending,

call monitoring and recording, and creating outbound marketing campaigns, among

other capabilities. This helps them to

➢ Increased agent efficiency and productivity.

➢ Enabled company to execute proactive customer service calls and expand

services offered to customers.

➢ Enhanced call monitoring for improved service quality

Financial services are a highly competitive and volume-driven industry which

demands high standards of customer service, effective consultation and quick

deliverables. This is something Sharekhan Limited, a financial services provider

based in India, understands. The company offers several user-friendly services for

customers to manage their stock portfolios, including online capabilities linked to an

information database to help customers confidently invest, and inbound customer

services using voice self-service technology and customer service agents handling

telephone orders from clients.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 25/64

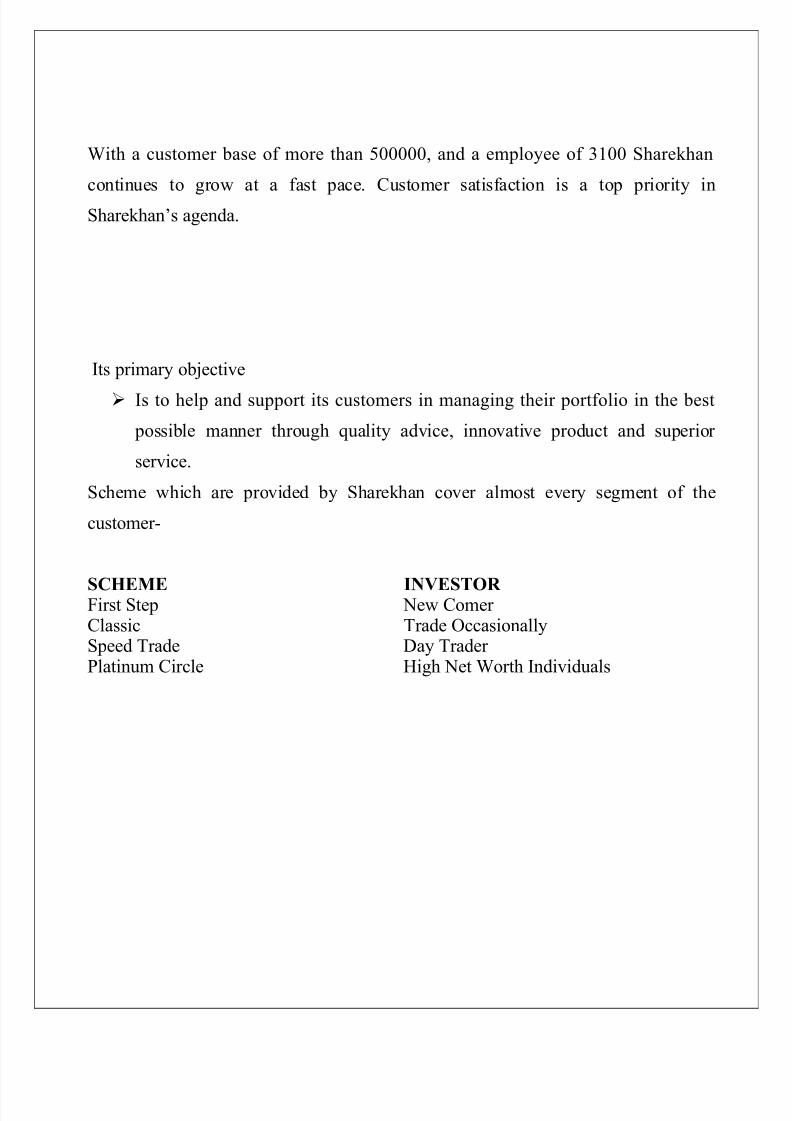

With a customer base of more than 500000, and a employee of 3100 Sharekhan

continues to grow at a fast pace. Customer satisfaction is a top priority in

Sharekhan’s agenda.

Its primary objective

➢ Is to help and support its customers in managing their portfolio in the best

possible manner through quality advice, innovative product and superior

service.

Scheme which are provided by Sharekhan cover almost every segment of the

customer-

SCHEME INVESTOR First Step New Comer Classic Trade OccasionallySpeed Trade Day Trader Platinum Circle High Net Worth Individuals

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 26/64

Contents

Foreword....................................................................................................... i

Introduction...................................................................................................1

• Development of Micro-insurance in India........................................3

• Supply and Demand Side Developments ........................................5

3.1Supplyofmicroinsurance..................................................................5

3.2 Demand for micro-insurance...............................................................6

• On Extending Micro-insurance .......................................................10

4.1 Flexibility in Premium........ ................................................................11

4.2 Micro-insurance and micro-finance ...................................................16

• Conclusions.......................................................................................20

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 27/64

Introduction

InsuranceInsurance is an essential part of running any business. If you are operating a smallbusiness you need more than just property insurance. Taking out the right insurancewill help protect your business and minimize its exposure to risk.

Your insurance requirements will vary according to the type of business you areoperating, but you should be aware that some forms of insurance are compulsory,such as workers’ compensation and third party car insurance.

When you’re in business you deal with a variety of potential risks each day. Risk isnot something you can avoid, but it is something you can manage. Risk management

will increase the probability of success and reduce the probability of failure of your business.

Types of insurance

• Assets & revenue insurance

• People insurance

• Liability insurance

Assets & revenue insurance

To protect your assets and revenue-generating capacity, here are some of the types of insurance available:

Building and contents

Covers the building, contents and stock of your business against fire and other perilssuch as earthquake, lightning, storms, impact, malicious damage and explosion.

Burglary

Insures your business assets against burglary, and is most important for retailers or a

business which maintains unattended premises.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 28/64

Business interruption or loss of profits

Covers you if your business is interrupted through damage to property by fire or other insured perils. Ensures your ongoing expenses are met and anticipated netprofit is maintained through a provision of cash flow.

Fidelity guarantees

Covers losses resulting from misappropriation by employees who embezzle or steal.

Machinery breakdown

Protects your business when mechanical and electrical plant and machinery at thework site break down.

Motor vehicle

It is compulsory to insure all company or business vehicles for third party injuryliability. Many different types of policies are available, so make sure youunderstand the options before making a decision. There are four basic options:

1. Compulsory third party (injury) – covers you for claims made against youfor personal injuries and legal costs arising from the use of your car. You must

obtain this insurance to register your car.2. Third party property damage - covers your liability for damage to another

person or to the property of others and your legal costs. It doesn’t includerepairs to your own car if you caused an accident.

3. Third party, fire and theft - covers you against the events covered above, aswell as fire and theft. It also insures against damage caused if your car wasstolen.

4. Comprehensive - covers you for all of the above plus damage caused to your own car by you in an accident. If you're buying a car on an installment basis,

financiers will usually insist on this cover.

People insurance

It includes:

• Superannuation

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 29/64

• Workers compensation requirements

Insurance cover for you and your employees:

Workers Compensation

You must provide accident and sickness insurance for your employees - workerscompensation - through an approved insurer. Workers compensation is covered byseparate state and territory legislation.

Personal accident and illness

If you are self employed you won’t be covered by workers compensation, so you

need to cover yourself for accident and sickness insurance through a private insurer.There are several types of life insurance. Some are investment-type funds where youcontribute over a certain time and get back your investment plus interest earnings atthe maturity date. Others are designed to cover risk - things that could happen toyou.

• Income protection or disability insurance - covers part of your normalincome if you are prevented from working through sickness or accident.

• Trauma insurance - provides a lump sum when you are diagnosed with oneof several specified life threatening illnesses.

• Term life insurance or whole of life cover - provides your dependents with alump sum if you die.

• Total and permanent disability insurance - provides a lump sum only if youare totally and permanently disabled before retirement.

SuperannuationIf you are running a business or employing people, you are likely to havesuperannuation obligations to your employees. If you are self-employed you alsoneed to provide for your retirement - superannuation is generally used to provide for a retirement plan.

Liability insurance

Types of liability insurance you need to consider:

Public Liability

Public liability insurance protects you and your business against the financial risk of being found liable to a third party for death or injury, loss or damage of property or ‘pure economic’ loss resulting from your negligence.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 30/64

Professional Indemnity

Professional indemnity insurance protects you from legal action taken for lossesincurred as a result of your advice. It provides indemnity cover if your client suffersa loss - either material, financial or physical - directly attributed to negligent acts.

Product Liability

If you sell, supply or deliver goods, even in the form of repair or service, you mayneed cover against claims of goods causing injury or damage. Product liabilityinsurance covers damage or injury caused to another business or person by thefailure of your product or the product you are selling.

What is Micro Insurance?

On a daily basis, the poor around the world face a multitude of risks that threaten toderail any progress they have made to work their way out of poverty. The death of afamily member, loss of property and livestock, illness, and natural disasters eachpose unique dangers. Protecting people against these losses is an important step toalleviating global poverty.Micro insurance - the protection of low-income people against specific perils inexchange for regular monetary payments (premiums) proportionate to the likelihoodand cost of the risk involved – seeks to provide a suitable solution for managingthese risks.

The Global Landscape

It is estimated that only eighty million out of the world's 2.5 billion poor are nowcovered by some form of micro insurance. Most remain without access to thiscritical financial service. In India and China, where organizations are estimated to

serve nearly 30 million micro insurance clients each, the percentage of poor livesinsured hovers below 3%. In Africa this figure is much lower – just 0.3% of thecontinent’s poor are insured. According to recent data, in 23 of the poorest 100countries in the world, there is currently no identified micro insurance activity,representing an unserved population of 370 million.

History and Vision

The Micro Insurance Agency has its roots within Opportunity International, a largemicrofinance network motivated by Jesus Christ’s call to serve the poor. With a

network of 47 microfinance institutions, Opportunity International has been serving

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 31/64

the entrepreneurial poor since 1971. In partnership with Opportunity’s microfinanceinstitutions, we began working in 2002 on the development of a range of life,

property, livestock, crop derivative, disability, unemployment and health insuranceproducts to cover the risks faced by Opportunity’s loan clients.Micro Insurance Agency staff observed that the risks the poor face can often setthem back months and years behind where their loans and savings products offeredby Opportunity had taken them. For instance, a death of a family member fromHIV/AIDS – a “pre-condition” most insurance companies would not cover – wouldoften mean expensive funeral costs and the loss of a breadwinner, resulting inincreased economic hardship for the family. In response, Micro Insurance Agencystaff developed an affordable funeral benefit product that did not exclude any pre-conditions, including HIV/AIDS. This transformed the mindset of retail insuranceproviders in the country, who later developed similar non-exclusive products in lightof the competing environment.Through the experience of serving Opportunity’s microfinance institutions and their clients, Micro Insurance Agency staff observed that the products most demanded bythe poor are not always the ones available. Health insurance, for example, is acritical need of the poor but the most limited in terms of supply. In addition, policiesthat are available are often based on first world practices and are too complex for thesimple coverage demanded. Further, when offered on an individual, one-off basis,high premium requirements and a need to pay in a single lump sum preclude a huge

sector of the market from access. New distribution models and channels were neededto increase access and reduce the effective price charged to clients.In 2005, the Micro Insurance Agency was founded by Opportunity International as afully-owned subsidiary capable of offering insurance products and services to a widerange of customers.Our mission is to empower the materially poor to transform their lives by insuringthem against financial risk and its consequences. Specifically, we seek to serve theeconomically active poor who live on $4 per day or less in developing countries andprovide a safety net to reduce economic setbacks.

Definitions of micro-insurance

Micro-insurance, the term used to refer to insurance to the low-income people, isdifferent from insurance in general as it is a low value product (involving modestpremium and benefit package) which requires different design and distributionstrategies such as premium based on community risk rating (as opposed to individualrisk rating), active involvement of an intermediate agency representing the targetcommunity and so forth. Insurance is fast emerging as an important strategy even for the low-income people engaged in wide variety of income generation activities, and

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 32/64

who remain exposed to variety of risks mainly because of absence of cost-effectiverisk hedging instruments.

Although the type of risks faced by the poor such as that of death, illness, injury andaccident, are no different from those faced by others, they are more vulnerable tosuch risks because of their economic circumstance. In the context of healthcontingency, for example, a World Bank study (Peters et al. 2002), reports that aboutone-fourth of hospitalized Indians fall below the poverty line as a result of their stayin hospitals. The same study reports that more than 40 percent of hospitalizedpatients take loans or sell assets to pay for hospitalization. Indeed, enhancing theability of the poor to deal with various risks is increasingly being considered integralto any poverty reduction strategy (Holzmann and Jorgensen 2000, Siegel et al.2001).

Of the different risk management strategies2, insurance that spreads the loss of the(few) affected members among all the members who join insurance scheme and alsoseparates time of payment of premium from time of claims, is particularly beneficialto the poor who have limited ability to mitigate risk on account of imperfect labour and credit markets.

In the past insurance as a prepaid risk managing instrument was never considered as

an option for the poor. The poor were considered too poor to be able to affordinsurance premiums. Often they were considered uninsurable, given the wide varietyof risks they face. However, recent developments in India, as elsewhere, have shownthat not only can the poor make small periodic contributions that can go towardsinsuring them against risks but also that the risks they face (such as those of illness,accident and injury, life, loss of property etc.) are eminently insurable as these risksare mostly independent ,idiosyncratic. Moreover, there are cost-effective ways of extending insurance to them. Thus, insurance is fast emerging as a prepaid financingoption for the risks facing the poor.

In this paper, we analyze the early evidence on micro-insurance already available inthis regard, highlight the current initiatives being contemplated to strengthen micro-insurance activity in the India, and suggest specific ways that can help promoteinsurance to the target segment.

Development of Micro-insurance in India

Historically in India, a few micro-insurance schemes were initiated, either by non-

governmental organizations (NGO) due to the felt need in the communities in which

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 33/64

these organizations were involved or by the trust hospitals. These schemes have nowgathered momentum partly due to the development of micro-finance activity, and

partly due to the regulation that makes it mandatory for all formal insurancecompanies to extend their activities to rural and well-identified social sector in thecountry (IRDA 2000). As a result, increasingly, micro-finance institutions (MFIs)and NGOs are negotiating with the for-profit insurers for the purchase of customizedgroup or standardized individual insurance schemes for the low-income people.Although the reach of such schemes is still very limited anywhere between 5 and 10million individuals---their potential is viewed to be considerable. The overall marketis estimated to reach Rs. 250 billion by 2008 (ILO 2004).

The insurance regulatory and development authority (IRDA) defines rural sector asconsisting of:

•

• a population of less than five thousand,• a density of population of less than four hundred per square kilometer • More than twenty five per cent of the male working population is engaged in

agricultural pursuits. The categories of workers falling under agriculturalpursuits are: cultivators, agricultural labourers, and workers in livestock,forestry, fishing, hunting and plantations, orchards and allied activities.

The social sector as defined by the insurance regulator consists of:• Unorganized sector • informal sector • economically vulnerable or backward classes, and• Other categories of persons, both in rural and urban areas.

The social obligations are in terms of number of individuals to be covered by bothlife and non-life insurers in certain identified sections of the society. The ruralobligations are in terms of certain minimum percentage of total polices written by

life insurance companies and for general insurance companies, these obligations arein terms of percentage of total gross premium collected. Some aspects of theseobligations are particularly noteworthy. First, the social and rural obligations do notnecessarily require (cross) subsidizing insurance. Second, these obligations are to befulfilled right from the first year of commencement of operations by the newinsurers. Third, there is no exit option available to insurers who are not keen onservicing the rural and low-income segment. Finally, non-fulfillment of theseobligations can invite penalties from the regulator.In order to fulfill these requirements all insurance companies have designed products

for the poorer sections and low-income individuals. Both public and private

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 34/64

insurance companies are adopting similar strategies of developing collaborationswith the various civil societies associations. The presence of these associations as a

mediating agency, or what we call a nodal agency, that represents, and acts on behalf of the target community is essential in extending insurance cover to the poor. Thenodal agency helps the formal insurance providers overcome both informationaldisadvantage and high transaction costs in providing insurance to the low-incomepeople. This way micro insurance combines positive features of formal insurance(pre paid, scientifically organized scheme) as well as those of informal insurance (byusing local

information and resources that helps in designing appropriate schemes delivered in acost effective way). In the absence of a nodal agency, the low resource base of thepoor, coupled with high transaction costs (relative to the magnitude of transactions)gives rise to the affordability issue. Lack of affordability prevents their latentdemand from expressing itself in the market. Hence the nodal agencies that organizethe poor, impart training, and work for the welfare of the low-income people play animportant role both in generating both the demand for insurance as well as thesupply of cost-effective insurance.

AN OVERVIEW OF THE MARKET

B Wealthy A

Middle Income

D

Poor

E

Severely Poor

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 35/64

The market for micro insurance is represented by this pyramid diagram. Formalsector insurance companies generally focus on the area identified as “A”. In this

realm the customers are corporations and wealthy individuals, and the products arevoluntary products such as life insurance, and obligatory products required either bylaw (such as motor third party liability) or by banks (such as property loss and creditlife). Also offered are products covering employees and civil liability. Most of thenon-auto related commercial products are being sold within the area marked “B”.The aggregate market for microfinance providers is generally in the area identifiedas “C”. Some MFPs require borrowers to obtain insurance for property, or credit-lifeinsurance as a means of protecting the institution’s interests. Area “D” indicates thebroad range of products offered by the social security and public health insurancesystems of developing country governments. They include coverage for pensions,disability benefits, primary health care, and medications. The weakness of this sector is indicated by the dashed line that suggests incomplete coverage. The potentialmarket for microinsurance is indicated as “E”. This extends above the MFP range inproviding access to individuals and others that cannot obtain appropriate productsfrom the commercial sector. The microinsurance range also extends below the MFPrange because it addresses agricultural coverage in some cases, and is now beingsold through many delivery channels other than MFPs. Just a few of these deliverychannels include:

• Low-income focused retailers in South Africa• Post offices in Indonesia• On bags of agricultural inputs or through computer kiosks in India.

Micro-insurance delivery models

One of the greatest challenges for micro-insurance is the actual delivery to clients.Methods and models for doing so vary depending on the organization, institution,

and provider involved. In general, there are four main methods for offering micro-insurance the partner-agent model, the provider-driven model, the full-servicemodel, and the community-based model. Each of these models has their ownadvantages and disadvantages.

• Partner agent model: A partnership is formed between the micro-insurancescheme and an agent (insurance company, microfinance institution, donor,etc.), and in some cases a third-party healthcare provider. The micro-insurancescheme is responsible for the delivery and marketing of products to the clients,while the agent retains all responsibility for design and development. In this

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 36/64

model, micro-insurance schemes benefit from limited risk, but are alsodisadvantaged in their limited control.

• Full service model: The micro-insurance scheme is in charge of everything;both the design and delivery of products to the clients, working with externalhealthcare providers to provide the services. This model has the advantage of offering micro-insurance schemes full control, yet the disadvantage of higher risks.

• Provider-driven model: The healthcare provider is the micro-insurancescheme, and similar to the full-service model, is responsible for all operations,delivery, design, and service. There is an advantage once more in the amountof control retained, yet disadvantage in the limitations on products and

services.• Community-based/mutual model: The policyholders or clients are in charge,

managing and owning the operations, and working with external healthcareproviders to offer services. This model is advantageous for its ability to designand market products more easily and effectively, yet is disadvantaged by itssmall size and scope of operations.

NEW MODELS FOR POOR COMMUNITIES

Much interest over the last few decades has focused on helping communities toestablish mutual or community-based insurance schemes. Professionals typicallymanage mutual insurance companies. Community-based schemes, promoted by ILOSTEP and CIDR among others, tend to be run by well meaning local people whogive freely of their time, but are not insurance professionals. Often people who weresimply in need of insurance end up being insurance managers with these schemes.One member of the management committee of a community- based scheme inTanzania noted that he “wants insurance, but doesn’t want to be an insurer.” Incommunity-based schemes, the limited management capacity frequently leads to arange of difficulties. The key issues of concern for community-based schemesinclude:

• Pricing – Often the process of pricing is focused on what people say they canpay rather than being linked to the cost structure of benefits that the groupwants to receive.

• Insurance is subject to cash flow fluctuations and thus requires significantreserves. These schemes frequently have insufficient reserves or no reserves at

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 37/64

all. Also, commercial reinsurance is rarely available to unregulated insuranceschemes thus leaving them with no ability to manage cash flow deficits.

• Controls on management are weak and temptation is strong. Fraud bymanagement is frequently a problem.

• These schemes are limited in size to those people within the defined localarea. This reduces their ability to diversify a rather small risk pool, andenhances the potential for adverse selection, both of which make sustainabilitya serious challenge for local management.

• Finally, in many countries there is no legal framework for these schemes.Indeed regulators are often unwilling to allow such schemes for fear that theywill not be able to adequately supervise many small schemes run by non-professionals. This is the case in India. Service providers, most typicallyhospitals and other healthcare providers have offered pre-financingmechanisms that act somewhat like insurance. These products, it is argued,will attract more people to the facility and the people who come will be able topay for the services. Often this becomes a problem because providers havelimited ability to manage the insurance administration issues. One overseer of a particular group of hospitals noted that attempting to offer microinsurance

could present a dual threat to the hospital network for which he works. Henoted that the hospital administrators “do not even know how to price their own healthcare services”. Therefore, they mis-price their premiums based onthose prices, which are typically too low. The resulting increase in patientsusing the insurance leads to even higher losses, due to higher administrativecosts and incorrect fees that do not cover the actual costs of services.Governments also provide a form of microinsurance through the programsthey provide for low-income Citizens. Unfortunately, in many countries theseprograms are simply insufficient to address the financial risks of the low-income and destitute populations. Certainly there is a population that will not

be covered by commercial or other non-government microinsurance.However, if a proper balance could be found, it is possible that thecombination of government programs, commercial microinsurance, mutualinsurance, and traditional commercial insurance could make each of thesemore efficient, and make the government interventions more effective inaddressing those that truly require such services.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 38/64

Need for Developing Micro-Insurance in India – IRDA perspective

Background

• Micro-insurance refers to protection of assets and lives against insurable risks

of target populations such as micro-entrepreneurs, small farmers and thelandless, women and low-income people through formal, semiformal andinformal institutions. Such products are often bundled with micro-savings andmicro-credit, thereby allocating scarce resources to micro-investments withthe highest marginal rates of return. Microinsurance is the mostunderdeveloped part of microfinance. Yet various schemes exist that areviable, benefiting both the institutions and their clients. Such schemes havegenerally served two major purposes: (i) they have contributed to loansecurity; and (ii) they have served as instruments of resource mobilization.The greatest challenge for microinsurance lies in the combination of viability

and sustainability with outreach.• Although introduction of sound practices such as appropriate policy sizes and

timely payment of installments of premium or positive incentives to renew ontime in order to avoid policy getting lapsed can be feasible, the ultimateeffectiveness of interventions focusing on institutional transformation andsound insurance practices will vary considerably, depending on theappropriateness of the regulatory environment.

Development Goal

To enable microinsurance to be an integral part of a country's wider insurancesystem, it is important for every insurer to adjust its costs of serving marginal clientsin remote areas, collecting premiums and installments, and offering doorstepservices. It is also important to recognize a wide network of intermediaries in therural and social sectors and notify regulations in order to guide and supervise themicro-insurance service providers and their customers.

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 39/64

Today we have a variety of microfinance institutions with national and localoutreach. Many of them have already become corporate agents or have entered into

referral

arrangements with insurers. However, semiformal institutions including savings andcredit cooperatives, NGOs and self-help groups which have immense potential incarrying the message of insurance as also solicit insurance business are yet to beutilized in a manner where their true potential can be harnessed to increase theinsurance penetration levels. This is due to restrictions in the existing agencyregulations in terms of minimum eligibility norms in order to become an agent.Depending on the existence and vigour of such institutions, the followingalternatives have emerged, for offering strategic entry points for microinsurancedevelopment:

• Adapting formal insurance arrangements to the needs of the micro-economy.

• Upgrading non-formal (comprising semiformal and informal) insurancearrangements with insurance companies.

• Linking formal and non formal insurance institutions with banks and self-helpgroups.

• Establishing new local institutions providing microinsurance services.

The first three strategies may be inter-connected:

• adapting insurance companies to the requirements of the micro-economy is afirst step; then

• Linking them as wholesale institutions to self-help groups as retailers; andfinally,

• Upgrading self-help groups e.g. to the level of financial cooperatives or

village banks.

If insurers are to serve customers who differ widely in terms of service costs andrisks, the only viable inducement for them is an adequate margin, lest they excludesmall farmers, - micro-entrepreneurs and people in remote areas. Only sound socialinsurance, which combines a social mandate with profit-making, has a chance of sustainability.

Institutional Adaptation

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 40/64

The experience so far has been that formal financial institutions serve but a fraction

of the population, which typically lies within the upper quartile of the socialhierarchy. Through adaptation to the microfinance market requirements, they maygradually expand into the second-highest quartile and into segments of the lower quartiles. Within the foreseeable future they will normally not be able to fully servethat market.Non formal finance mostly rests on local institutions which are directly accessible toall segments of the population. Self-Help Groups (SHGs) are member-owned andmember-controlled local institutions. They may either be financial groups, withfinancial intermediation as their primary purpose; or non financial groups, withfinancial intermediation as a secondary purpose, such as vendors' associations,family planning groups and numerous other types of voluntary associations.The functions that need to be focused must include: providing guidance to members,collecting premium installments from members, insurance services to members,communication and exchange of experience, providing linkages with banks, NGOsor donors, supporting the proposals of individual members to insurance companiesthrough recommendations.

Linkage to Insurers

On a modest scale, various forms of life and health insurance have been successfullypracticed by different institutions in different countries, particularly as part of loanprotection schemes. Micro-insurance procedures and services should be set byinsurers rather than the regulator. Appropriate procedures and services should beapplied to attain:

(1) Sound financial management,

(2) Convenient and safe savings premium collection and deposit facilities,

(3) Appropriate claim appraisal and processing procedures,

(4) Adequate risk management,

(5) Timely collection of premium installments,

(6) Monitoring and

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 41/64

(7) Effective information gathering, all of which may include cooperation betweendifferent formal and non-formal intermediaries in fields where each is most

effective.

Proposed Micro-insurance Regulations

In order to introduce the concept micro-insurance it is necessary to draft suitablebring in suitable regulations to enable insurers to design and distribute and servicemicro-insurance products and discharge their obligations to the rural and socialsectors as per provisions of the Insurance Act, 1938.

1. It is proposed that an insurer transacting life insurance business shall bepermitted to provide life micro-insurance products as well as general micro-insurance products provided it ties up with an insurer transacting generalinsurance business for the general micro-insurance products, and vice versa.

2. In addition to an insurance agent or corporate agent or insurance broker whoare authorized to solicit and procure insurance business, including micro-insurance business with an insurer in accordance with the provisions of theInsurance Act, 1938 and the regulations made there under it is also proposedto introduce the concepts of “micro-insurance product” and “micro-insurance

agent” .

Micro-insurance Product1. A “life micro-insurance product” means any term insurance contract

with or without return of premium, any endowment insurance contractor health insurance contract, with or without an accident benefit rider,either on individual or group basis, as per terms stated in the Table Abelow, filed with the Authority:

Table A:

Type of Cover MinimumAmountof Cover

MaximumAmount of Cover

Termof Cover Min.

Term of Cover Max.

MinimumAge atentry

Maximumage at entry

TermInsurance withor withoutreturn of

premium

Rs.10,000

Rs.50,000

5 year 7 years 18 60

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 42/64

EndowmentInsurance

Rs.10,000

Rs.50,000

5 year 7 years 18 60

HealthInsuranceContract

Rs.10,000

Rs.15,000

1 year 7 year 18 60

AccidentBenefit as rider

Rs.10,000

Rs.50,000

1 year 5 years 18 60

NOTE: The present average sum insured is around Rs. 5,000. This is highlyinadequate to provide any tangible relief even to an individual below thepoverty line. Therefore, it is suggested that the minimum amount of cover of Rs

10,000 appear more realistic.

2. A “general micro-insurance product” means any health insurancecontract, any contract covering the belongings such as hut, livestock,any personal accident contract, or tools or instruments, either onindividual or group basis, as per terms stated in the Table B below, filedwith the Authority:

Table B:

Type of Cover MinimumAmount of Cover

MaximumAmount of Cover

Term of Cover Min.

Term of Cover Max.

Minimum Ageat entry

Maximum ageat entry

Hut or livestock or Tools or implements or other assets— against all perils

Rs.10,000

Rs.20,000

1 year 1 year 18 70

Health InsuranceContract

Rs.10,000

Rs.15,000

1 year 1 year 18 60

PersonalAccident

Rs.10,000

Rs.50,000

1 year 1 year 18 60

Micro-insurance Agent

• A “micro-insurance agent” shall be a Non Government Organization (NGO)

or a Self Help Group (SHG).

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 43/64

• Explanation: For the purposes of this regulation:

• A Non Government Organization (NGO) shall be a registered non-profitorganization under the Society’s Act, 1968 with a proven track record of working with marginalized groups with clearly stated aims and objectives,transparency, and accountability outlined in its memorandum, rules andregulations and demonstrates involvement of committed people.

• Self Help Group (SHG) may be an informal group or registered under Societies Act, State Co-operative Act or as a partnership firm, consisting of 10to 20 with a proven track record of working with marginalized groups withclearly stated aims and objectives, transparency, and accountability outlined inits memorandum, rules and regulations and demonstrates involvement of committed people.

• The minimum number of members comprising a group should be atleast tenfor insurance of individuals, and atleast fifty for group insurance.

Scope and Functions

A micro-insurance agent shall be appointed by an insurer by a deed of agreement or memorandum of understanding which should clearly specify the terms andconditions, duties and responsibilities of both the micro-insurance agent and theinsurer, and he shall abide by the following:-

• He shall work either for one life insurer or for one general insurer or for onelife insurer and one general insurer;

• He shall be specifically authorized to perform one or more of the followingfunctions:--

a) Maintaining a register of all members and their dependants covered under theinsurance scheme alongwith details of name, age, address, nominees andthumb impression/ signature;

b) Collection of proposal forms;

c) Collection of self declaration from the member that he is in good health;

d) Collection of monies for issuance of contract or remittance of premium;

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 44/64

e) distribution of policy documents;

f) Assistance in the settlement of claims;

g) Nomination; and

h) Any policy administration service.

i) The micro-insurance agent or the insurance company shall have the option toterminate the agreement/ MOU after giving a notice of three months.

j) All such agreements/ MOU must have the prior approval of the Head office of the insurance company.

Initiative Taken By Private Sectors

Tata AIG Life - First insurance company to launch Micro Insurance

• First major Micro Insurance initiatives venture by an Indian insurancecompany

• Launches three new Micro Insurance products and five Micro Insurancebranches

• Adopts a tailor made rural communication strategy to reach out to the ruralcommunity

American International Group, Inc. (AIG)

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 45/64

American International Group, Inc. (AIG), world leaders in insurance and financialservices, is the leading international insurance organization with operations in more

than 130 countries and jurisdictions. AIG companies serve commercial, institutionaland individual customers through the most extensive worldwide property-casualtyand life insurance networks of any insurer. In addition, AIG companies are leadingproviders of retirement services, financial services and asset management around theworld. AIG's common stock is listed in the U.S. on the New York Stock Exchange,as well as the stock exchanges in London, Paris, Switzerland and Tokyo.

Micro Insurance is the process of delivering and servicing relevant and affordablelife insurance products to the low-income socio economic strata. The focus of TataAIG Life’s Micro insurance program is rural India, where traditionally the far-flung,lower and lower middle-income segments have had limited access to life insurance

services.

Cost of plans:

Tata AIG Life Micro insurance plans are available with or without survival benefitsand with death benefits ranging from Rs.5, 000 to Rs.50, 000. With premiums as lowas Rs.5** per month, there is now an affordable life insurance product for nearlyevery rural household in India.

Policies Available:

The following special Micro Insurance products from Tata AIG Life are nowavailable for the rural population at the bottom of the pyramid.

• Navkalyan Yojana

• Ayushman Yojana

• Sampoorn Bima Yojana

NAVKALYAN YOJANA

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 46/64

A regular premium payment, low cost term plan for the rural adults who seek lifeinsurance protection without any maturity benefit.

Key features include:

• Policy Term : 5 years• Coverage Limits : Minimum Death Benefit (Sum Assured): Rs.5,000/-

Maximum Death Benefit (Sum Assured): Rs.50,000/-• Premium payment frequency : Monthly, quarterly, half yearly & yearly• Death Benifit : Sum assured to the policyholder’s nominee• Maturity benefit : None• Rider : Option to attach Accident Death Benefit Rider for issue ages 18 to 55

years at a nominal extra charge.

Tax Benefits and Age Eligibility

• Premiums paid under this plan are eligible for tax benefits as per the Income

Tax Act, 1961 and are subject to any amendments made therein from time totime.*

Anyone between ages 18 and 60 can apply for this policy.

AYUSHMAN YOJANA

A single premium plan where the policyholder pays the premium at the beginning of the policy term. This is especially useful for those rural people who have a seasonalincome.

Key features include:

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 47/64

• Policy Term : 10 years• Coverage Limits : Minimum Death Benefit (Sum Assured): Rs.5,000/-

Maximum Death Benefit (Sum Assured): Rs.50,000/-• Death Benifit : Sum assured to the policyholder’s nominee• Maturity benefit : On survival, 125% of the single premium paid.

Tax Benefits and Age Eligibility

• Premiums paid under this plan are eligible for tax benefits to the extent of 20% of Sum Assured as per the Income Tax Act, 1961 and are subject toamendments made therein from time to time.*

Anyone between ages 18 and 60 can apply for this policy.

SAMPOORNA BIMA YOJANA

A low cost insurance plan where the policyholder receives all the premiums paid

during the policy term upon survival until the term of the policy. Premiums arepayable for only 10 years, while the coverage is up to 15 years.

How do we operate?

We operate in 11 states with a specific relationship management team for each state.A dedicated & trained sales and marketing team manages the front end of the Microinsurance program. Our micro insurance distribution model collaborates with NGO’s

(Non-governmental organizations) and Rural organizations with community levelSHG (Self Help Group) women advisors who provide insurance advisory services tothe rural customers at their doorstep. The grassroots level agents explain the productdetails in the local language of the customer, thereby enabling the customer to makea decision. The training programs, brochures, contract documents, and applicationforms are available in 8 different languages other than English and Hindi

Key features include:

• Policy Term : 15 years

8/7/2019 Finance In Micro Insurance With Referance To Sharekhan

http://slidepdf.com/reader/full/finance-in-micro-insurance-with-referance-to-sharekhan 48/64

• Coverage Limits : Minimum Death Benefit (Sum Assured): Rs.5,000/-Maximum Death Benefit (Sum Assured): Rs.50,000/-

• Premium payment frequency : Monthly, quarterly, half yearly & yearly• Death Benifit : Sum assured is paid to the policyholder’s nominee• Maturity benefit : At the end of the 15 years, all the premiums paid will be

returned to the policyholder.

Tax Benefits and Age Eligibility

Premiums paid under this plan are eligible for tax benefits as per the Income Tax

Act, 1961 and are subject to any amendments made therein from time to time.*Anyone between ages 18 and 60 can apply for this policy.

RESEARCH OBJECTIVE

To find out potential depth in society for providing opportunities for further

extention for micro insurance

Sub objective:

✔ Determine need and ability of people segment whose per day income is

less than 100 bugs. What really matters to him or her while think about

insurance.

✔ Determine awareness about insurance among them. if aware then source

of information

✔ To determine the govt. and private sector proceeding in this area andextent of their success

RESEARCH METHODOLGY

Data collection

For data collection, we developed a well defined questionnaire as a research

instrument, consisting questions aimed to measure the people perception about

insurance, their need and problems, bottleneck why hadn’t insured, and target to find