finance-growth-and-inequality-bloomberg-london-17-june-2015

TRANSCRIPT

FINANCE, GROWTH AND INEQUALITYCatherine L. MannOECD Chief Economist and G20 Deputy

Bloomberg, London, 17 June 2015

www.oecd.org/eco/finance-growth-inequality.htm

1. Secular trends

2. Finance and growth

3. Finance and inequality

4. Policies for a healthy financial future

Structure of the presentation

2

SECULAR TRENDS

4

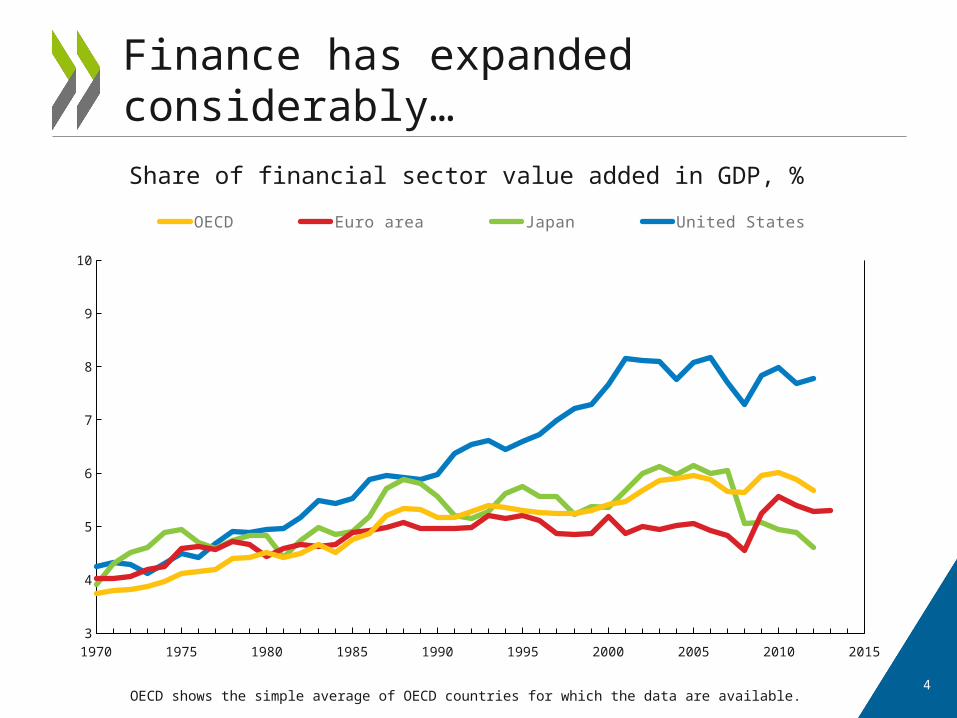

Finance has expanded considerably…

1970 1975 1980 1985 1990 1995 2000 2005 2010 20153

4

5

6

7

8

9

10

OECD Euro area Japan United States

Share of financial sector value added in GDP, %

OECD shows the simple average of OECD countries for which the data are available.

5

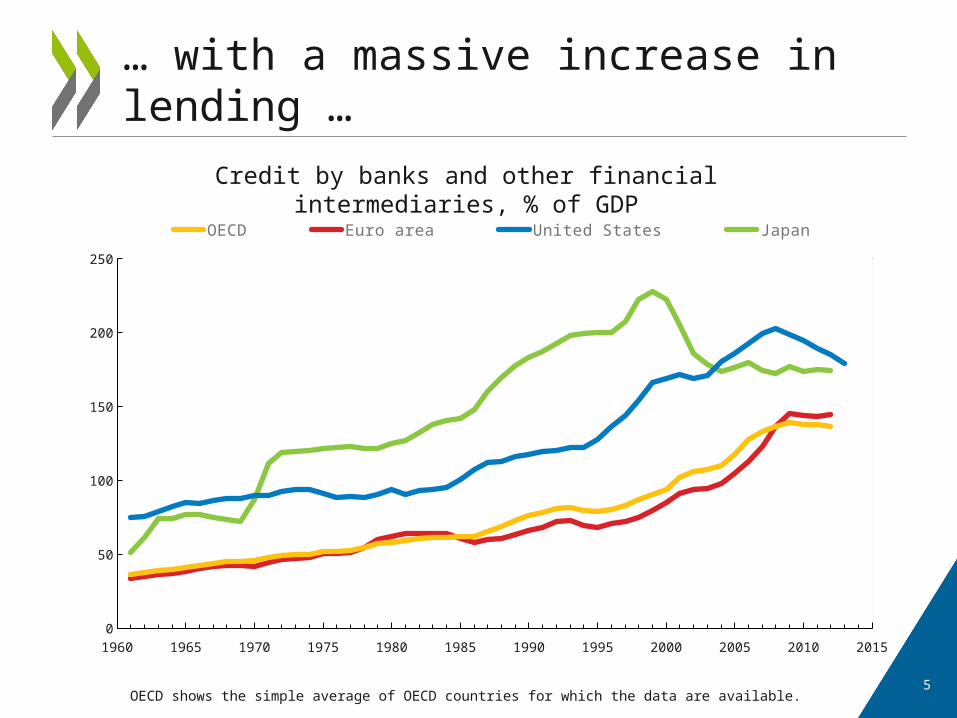

… with a massive increase in lending …

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

50

100

150

200

250

OECD Euro area United States Japan

Credit by banks and other financial intermediaries, % of GDP

OECD shows the simple average of OECD countries for which the data are available.

6

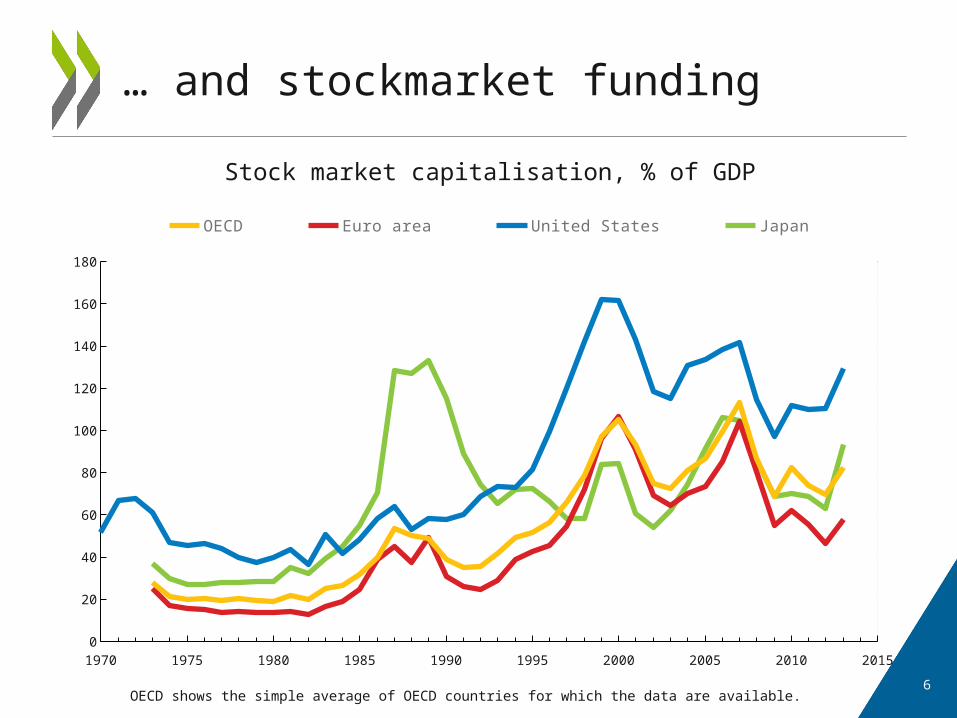

… and stockmarket funding

1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

20

40

60

80

100

120

140

160

180

OECD Euro area United States Japan

Stock market capitalisation, % of GDP

OECD shows the simple average of OECD countries for which the data are available.

FINANCE AND GROWTH

• Reducing the need for self-financing, hence

– allocating capital more efficiently

– monitoring investments more professionally

• Facilitating international trade

• Smoothing cash-flow shocks

• Facilitating monetary policy transmission

Finance boosts growth by:

8

• Misallocating capital

• Magnifying the cost of implicit guarantees

• Distorting allocation of talented labor

• Generating boom-bust cycles

• Heightening the risk of regulatory capture

Too much finance can harm growth by:

9

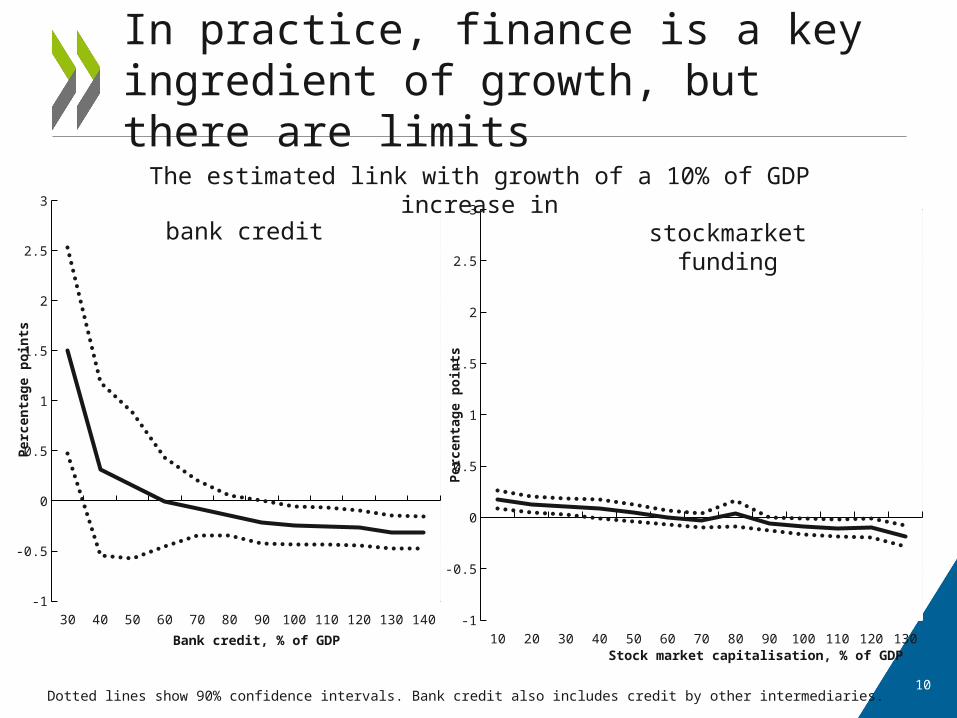

In practice, finance is a key ingredient of growth, but there are limits

30 40 50 60 70 80 90 100 110 120 130 140-1

-0.5

0

0.5

1

1.5

2

2.5

3

Bank credit, % of GDP

Per

cen

tag

e p

oin

ts

10 20 30 40 50 60 70 80 90 100 110 120 130-1

-0.5

0

0.5

1

1.5

2

2.5

3

Stock market capitalisation, % of GDP

Per

cen

tag

e p

oin

ts

The estimated link with growth of a 10% of GDP increase in

bank credit stockmarket funding

Dotted lines show 90% confidence intervals. Bank credit also includes credit by other intermediaries.10

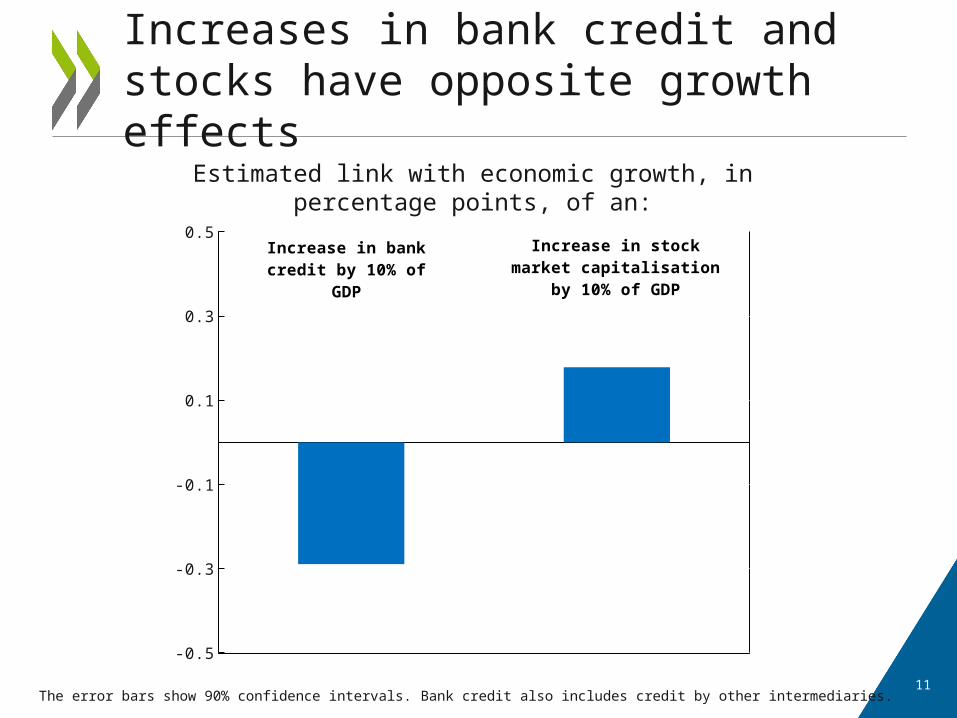

Increases in bank credit and stocks have opposite growth effects

-0.5

-0.3

-0.1

0.1

0.3

0.5

Increase in bank credit by 10% of GDP

Increase in stock market capi-talisation by 10% of GDP

Estimated link with economic growth, in percentage points, of an:

The error bars show 90% confidence intervals. Bank credit also includes credit by other intermediaries.11

12

1. Excessive financial deregulation

2. Too-big-to-fail guarantees

3. Bank lending outpacing bond financing

4. Household credit outpacing business credit

Channels behind the negative link between credit and growth

13

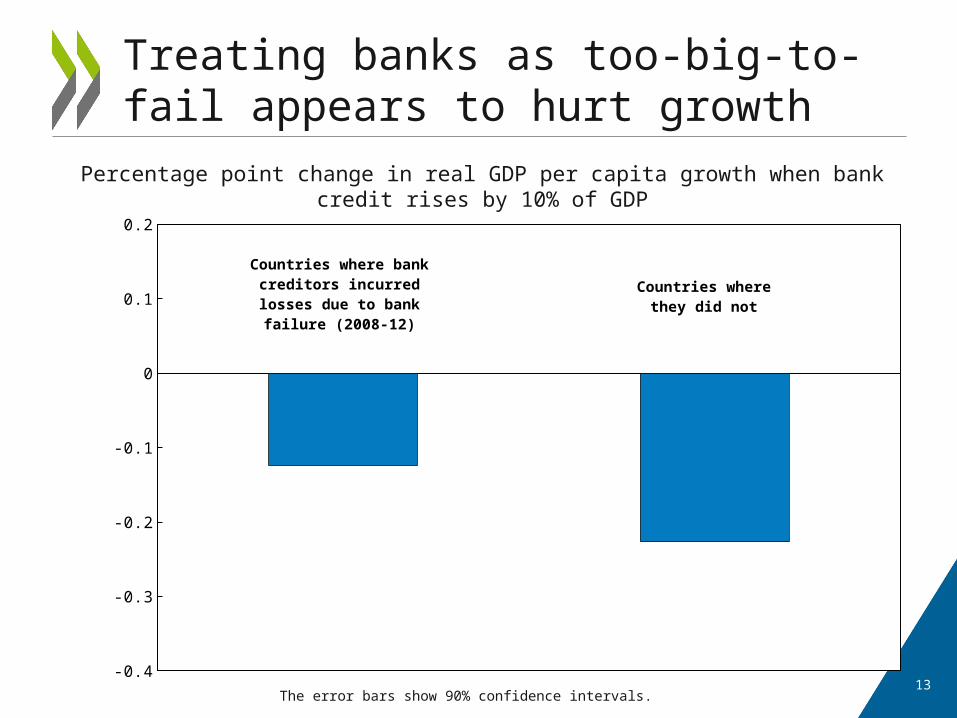

Treating banks as too-big-to-fail appears to hurt growth

Percentage point change in real GDP per capita growth when bank credit rises by 10% of GDP

The error bars show 90% confidence intervals.

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

Countries where bank credi-tors incurred losses due to

bank failure (2008-12)

Countries where they did not

14

Increases in bank lending have a more negative link with growth than other debt

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

Increase in bank lend-ing by 10% of GDP

Increase in other debt by 10% of GDP

Estimated link with economic growth, in percentage points, of an:

The error bars show 90% confidence intervals.

15

Business credit has a more favourable link with growth than household credit

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

Increase in credit to households by 10% of

GDP

Increase in credit to busi-nesses by 10% of GDP

Estimated link with economic growth, in percentage points, of an:

The error bars show 90% confidence intervals.

FINANCE AND INEQUALITY

More finance can promote income• equalisation if:

– It relaxes consumption constraints on poor– It encourages work in the formal sector

• inequality if:– It flows more freely to the better off– Finance pays particularly dispersed wages

Finance can shape inequality both ways

17

18

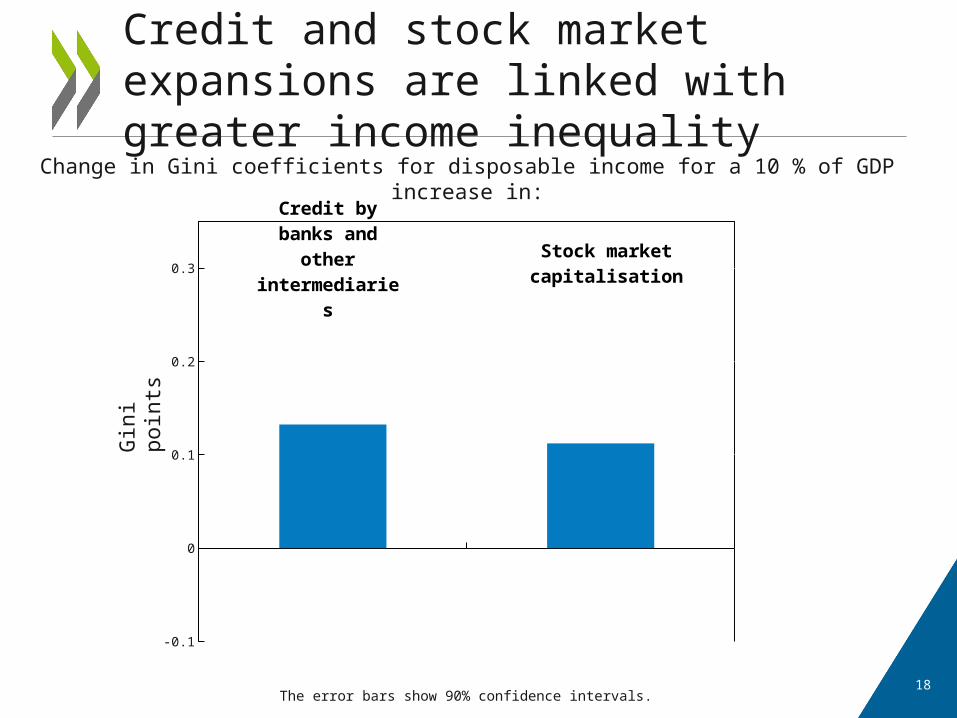

Credit and stock market expansions are linked with greater income inequality

Change in Gini coefficients for disposable income for a 10 % of GDP increase in:

The error bars show 90% confidence intervals.

-0.1

0

0.1

0.2

0.3

Credit by banks and other in-termediaries

Stock market capitalisa-tion

Gin

i poi

nts

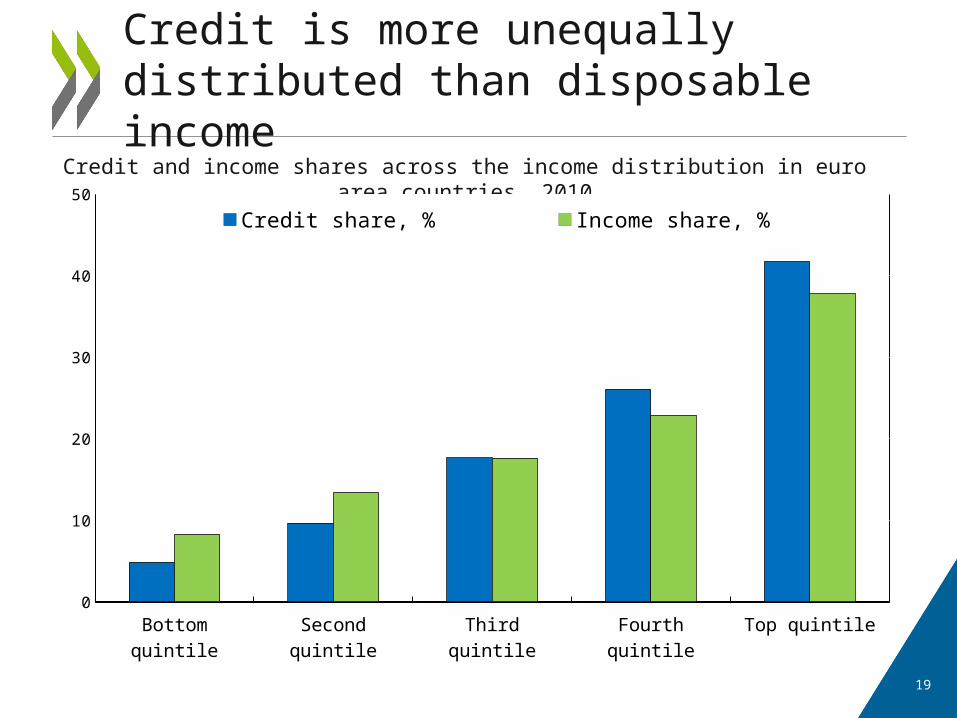

Credit is more unequally distributed than disposable income

Credit and income shares across the income distribution in euro area countries, 2010

Bottom quintile Second quintile Third quintile Fourth quintile Top quintile0

10

20

30

40

50Credit share, % Income share, %

19

20

Lower-income households find access to credit more difficult

Bottom quintile Second quintile Third quintile Fourth quintile Top quintile0

10

20

30

40

50

60

70

Percentage of households expressing difficulty in obtaining credit in euro area countries, 2010

The share of financial-sector employees rises with the income bracket

Percentage of financial-sector employees in each percentile of the income distributionEuropean countries, 2010

Percentile0 10 20 30 40 50 60 70 80 90 1000

2

4

6

8

10

12

14

16

18

20

21

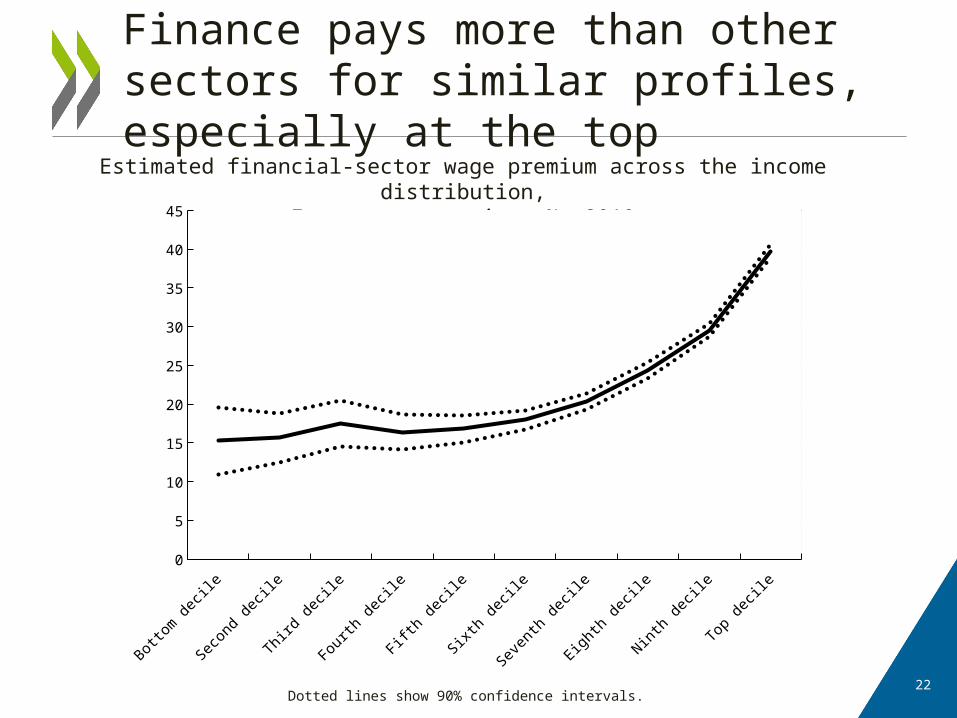

Finance pays more than other sectors for similar profiles, especially at the topEstimated financial-sector wage premium across the income distribution,

European countries, %, 2010

Bottom decile

Second decile

Third decile

Fourth decile

Fifth decile

Sixth decile

Seventh decile

Eighth decile

Ninth decile

Top decile

0

5

10

15

20

25

30

35

40

45

Dotted lines show 90% confidence intervals.22

POLICIES FOR A HEALTHY FINANCIAL FUTURE

• Withdraw implicit too-big-to-fail subsidies– break-ups, capital surcharges, structural

separation, resolution plans

• Implement macro-level financial supervision– debt-service-to-income caps

• Improve compensation practices – clawbacks

• Reduce tax biases against equity – corporate income tax, lending to businesses

(VAT)

A healthy future for finance

24

Financial reform is compatible with inclusive growth

Growth Equality

Win-win

Enforce strong macro-prudential controls + +Split TBTF banks or reduce TBTF support through other means + +Recuperate TBTF subsidies through taxation + +

Income-enhancing Reduce the debt bias in corporate taxation + Reduce the bias against business loans in VAT +

Trade-off Lower barriers to stock market financing + -

25

26

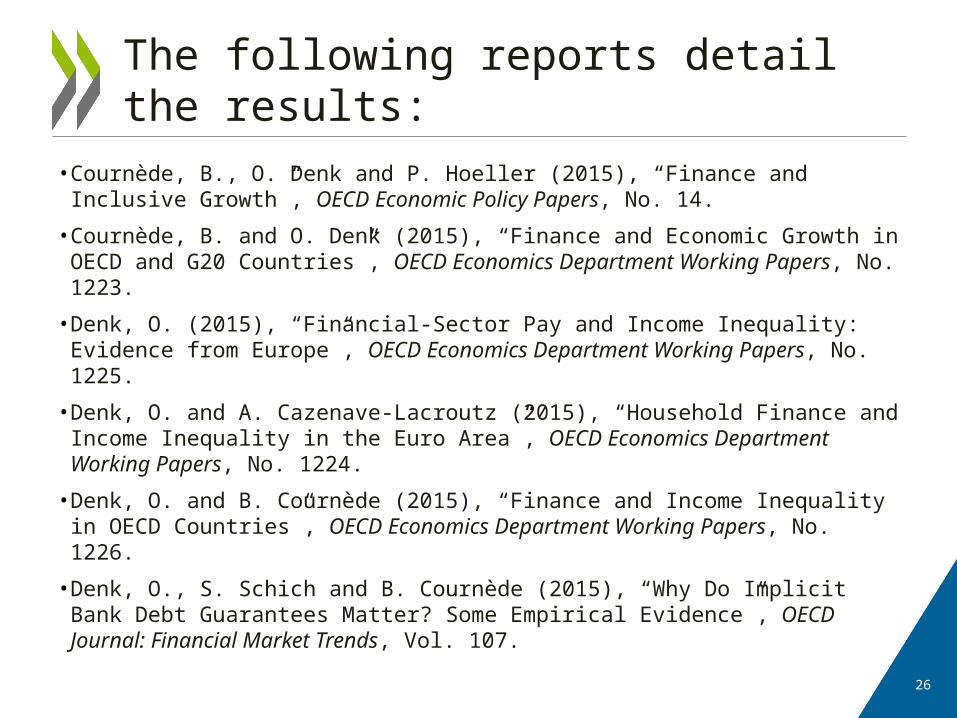

• Cournède, B., O. Denk and P. Hoeller (2015), “Finance and Inclusive Growth”, OECD Economic Policy Papers, No. 14.

• Cournède, B. and O. Denk (2015), “Finance and Economic Growth in OECD and G20 Countries”, OECD Economics Department Working Papers, No. 1223.

• Denk, O. (2015), “Financial-Sector Pay and Income Inequality: Evidence from Europe”, OECD Economics Department Working Papers, No. 1225.

• Denk, O. and A. Cazenave-Lacroutz (2015), “Household Finance and Income Inequality in the Euro Area”, OECD Economics Department Working Papers, No. 1224.

• Denk, O. and B. Cournède (2015), “Finance and Income Inequality in OECD Countries”, OECD Economics Department Working Papers, No. 1226.

• Denk, O., S. Schich and B. Cournède (2015), “Why Do Implicit Bank Debt Guarantees Matter? Some Empirical Evidence”, OECD Journal: Financial Market Trends, Vol. 107.

The following reports detail the results: