finance for club boards - e3learning€¦ · assessment and accreditation completing the...

TRANSCRIPT

Finance for Club Boards

2 | P a g e

Copyright

© 2013 ClubsNSW The workbook materials are copyright, and copyright is vested in ClubsNSW. Except as permitted by the Copyright Act 1968, no part of it may in any form or by any electronic, mechanical, photocopying, recording, or any other means be reproduced, stored in a retrieval system or be broadcast or transmitted without the prior permission of the publisher, ClubsNSW. Every effort has been made to trace copyright material. Should any infringement have occurred accidentally the authors and ClubsNSW tender their apologies.

FFGB – 121119 - Finance for Club Boards Workbook VI

Disclaimer

This workbook is only intended as a preliminary guide for boards and managers of clubs. It does not replace legal advice or accountant’s advice and it is not intended that clubs should rely on information in the guide in lieu of taking such advice. Clubs should take professional advice where appropriate.

This information has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information, you should consider its appropriateness having regard to your objectives, financial situation or needs. Any information about a third party's products or services is provided for convenience only.

Use of the workbook by workshop participants is permitted. No other use, citation or publication (in whole or part) is permitted without the prior written consent of ClubsNSW. Without limiting those general words, clubs must only use the workbook for their own internal purposes. Copies of the workbook are not to be used by, or provided to, anyone else.

Author

Debbie Organ: Learning and Development Executive, ClubsNSW

Example Club Limited Accounts: C. Roan (KPMG)

ClubsNSW Contact Details

For more information on the content covered in this workbook, ClubsNSW member clubs can contact the ClubsNSW Member Enquiries Centre:

Phone: 1300 730 001 Fax: (02) 9268 3066

Email: [email protected] Web: www.clubsnsw.com.au

Finance for Club Boards

3 | P a g e

CONTENTS

INTRODUCTION ............................................................................................................................... 7

ASSESSMENT AND ACCREDITATION ................................................................................................. 9

CERTIFICATE IV IN GOVERNANCE .................................................................................................... 9

GLOSSARY OF FINANCIAL TERMS ....................................................................................................... 11

UNIT 1: OPERATING IN THE NOT FOR PROFIT SECTOR ............................................................................ 19

NSW CLUBS IN THE NOT FOR PROFIT SECTOR ................................................................................ 21

TYPES OF CLUBS INCLUDE: .......................................................................................................... 21

WHAT DOES NOT FOR PROFIT MEAN? ......................................................................................... 22

TYPES OF ORGANISATION ........................................................................................................... 22

PROFIT MAKING ENTITIES ........................................................................................................... 22

NOT FOR PROFIT ENTITIES .......................................................................................................... 23

WHAT DOES “INCORPORATION” MEAN? ........................................................................................ 23

COMPANY LIMITED BY GUARANTEE .............................................................................................. 24

CO-OPERATIVES ........................................................................................................................ 26

CLUB CONSTITUTION ................................................................................................................. 26

UNIT 2: UNDERSTANDING FINANCIAL CONCEPTS AND REPORTS................................................................ 27

SETTING THE SCENE FOR GOOD FINANCIAL REPORTING .................................................................... 29

IMPORTANCE OF FINANCIAL REPORTS ........................................................................................... 29

STATUTORY FINANCIAL REPORTS .................................................................................................. 32

ANNUAL FINANCIAL REPORTS ...................................................................................................... 32

ANNUAL REPORTING ................................................................................................................. 32

QUARTERLY REPORTING ............................................................................................................. 33

ANNUAL FINANCIAL STATEMENTS ................................................................................................ 34

KEY COMPONENTS OF THE ANNUAL REPORT .................................................................................. 36

1. BALANCE SHEET (ALSO KNOWN AS THE STATEMENT OF FINANCIAL POSITION) ................................... 36

ELEMENTS OF BALANCE SHEET..................................................................................................... 37

CATEGORIES OF ASSETS AND LIABILITIES ........................................................................................ 39

CATEGORIES OF ASSETS .............................................................................................................. 39

CURRENT ASSETS ...................................................................................................................... 40

NON-CURRENT ASSETS .............................................................................................................. 41

REVIEW ACTIVITY 1 ........................................................................................................ 42

CATEGORIES OF LIABILITIES ......................................................................................................... 42

CURRENT LIABILITIES ................................................................................................................. 42

NON-CURRENT LIABILITIES .......................................................................................................... 44

MEMBERS EQUITY .................................................................................................................... 45

CLUB SOLVENCY AND LIQUIDITY ................................................................................................... 47

SHORT TERM SOLVENCY INDICATORS ............................................................................................ 48

Finance for Club Boards

4 | P a g e

LIQUIDITY RATIOS ..................................................................................................................... 48

REVIEW ACTIVITY 2: BALANCE SHEET................................................................................. 49

LONG TERM SOLVENCY RATIOS .................................................................................................... 50

UNDERSTANDING YOUR DEBT TO ASSETS ...................................................................................... 51

REVIEW ACTIVITY 3: BALANCE SHEET................................................................................. 52

LIMITATIONS OF A BALANCE SHEET ............................................................................................... 53

2. UNDERSTANDING THE STATEMENT OF COMPREHENSIVE INCOME ................................................... 59

TOTAL REVENUE ....................................................................................................................... 61

GROSS PROFIT .......................................................................................................................... 62

OPERATING EXPENSES ............................................................................................................... 62

EARNINGS BEFORE INTEREST, TAX, DEPRECIATION AND AMORTISATION (EBITDA) ............................... 63

EBITDA AS A PERCENTAGE OF REVENUE ....................................................................................... 64

DEPRECIATION AND AMORTISATION ............................................................................................. 64

EARNINGS BEFORE INTEREST AND TAX (EBIT) ................................................................................ 65

FINANCE COSTS/INCOME ........................................................................................................... 65

INTEREST COVERAGE RATIO ........................................................................................................ 67

EARNINGS BEFORE TAX .............................................................................................................. 68

IMPAIRMENT LOSSES OF LAND AND BUILDINGS ............................................................................... 68

INCOME TAX EXPENSE ............................................................................................................... 70

COMPREHENSIVE INCOME FOR THE YEAR ....................................................................................... 71

REVIEW ACTIVITY 4: STATEMENT OF COMPREHENSIVE INCOME .............................................. 72

REVIEW ACTIVITY 5: LOOKING AT YOUR CLUB’S INCOME STATEMENTS ...................................... 73

4. UNDERSTANDING THE STATEMENT OF CASH FLOW ...................................................................... 74

STATEMENT OF CASH FLOWS ...................................................................................................... 74

CATEGORIES OF CASH FLOWS ...................................................................................................... 76

REVIEW ACTIVITY 6: YOUR CLUB’S STATEMENT OF CASH FLOWS .............................................. 78

5. UNDERSTANDING THE NOTES TO THE FINANCIAL STATEMENT ........................................................ 79

6. UNDERSTANDING THE AUDITORS REPORT .................................................................................. 98

WHO CAN ACT AS THE CLUB’S AUDITOR? ..................................................................................... 101

TYPES OF AUDIT REPORTS ......................................................................................................... 103

YOUR BANKERS REQUIREMENTS ................................................................................................ 105

THE EXPECTATION GAP ............................................................................................................ 105

INDEPENDENCE OF THE AUDITOR IS CRITICAL TO THE CLUB .............................................................. 107

APPOINTMENT OF CLUB AUDITORS............................................................................................. 109

APPOINTMENT OF A NEW AUDITOR ............................................................................................ 110

7. DIRECTORS REPORT ............................................................................................................. 112

8. DIRECTORS DECLARATION ..................................................................................................... 116

UNDERSTANDING MANAGEMENT ACCOUNTS ............................................................................... 118

REVIEW ACTIVITY 7: MANAGEMENT ACCOUNTS ................................................................ 121

UNIT 3: MONITOR FINANCIAL PERFORMANCE .................................................................................... 123

BOARD.................................................................................................................................. 125

Finance for Club Boards

5 | P a g e

THE FINANCIAL ROLES AND RESPONSIBILITIES OF A BOARD .............................................................. 125

CEO ..................................................................................................................................... 126

MANAGEMENT TEAM .............................................................................................................. 127

STAFF ................................................................................................................................... 128

FINANCIAL PERFORMANCE MANAGEMENT ................................................................................... 128

RECORD KEEPING FOR IMPROVED FINANCIAL INFORMATION ........................................................... 129

PREPARATION OF FINANCIAL INFORMATION ................................................................................. 129

FINANCIAL CONTROLS .............................................................................................................. 130

BUDGETING AND FORECASTING ................................................................................................. 131

BUDGETS ............................................................................................................................... 131

WHAT ARE THE ADVANTAGES OF PREPARING A BUDGET? ................................................................ 133

TYPES OF BUDGETS ................................................................................................................. 133

THE BUDGET PERIOD ............................................................................................................... 135

A COMBINED APPROACH? ........................................................................................................ 138

REVIEW ACTIVITY 8: YOUR CLUB’S APPROACH TO BUDGETING .............................................. 139

FACTORS TO CONSIDER ............................................................................................................ 140

KEY PERFORMANCE INDICATORS ................................................................................................ 142

BENCHMARKING ..................................................................................................................... 154

UNIT 4: MANAGING BUSINESS CHANGES .......................................................................................... 155

CHANGE MANAGEMENT........................................................................................................... 157

REVIEW ACTIVITY 9: ANALYSING EXTERNAL CHANGES ......................................................... 158

COMMON TYPES OF CHANGES MADE BY CLUBS: ............................................................................. 158

REVIEW ACTIVITY 10: BUSINESS CHANGE ......................................................................... 166

UNIT 5: EXTERNAL FINANCING ........................................................................................................ 169

EXTERNAL FINANCING .............................................................................................................. 171

DEBT FINANCING .................................................................................................................... 171

UNDERSTANDING YOUR FINANCING ........................................................................................... 171

COMMERCIAL LENDING DOCUMENTATION ................................................................................... 178

TYPES OF DOCUMENTS ............................................................................................................. 178

APPLYING FOR GRANTS ............................................................................................................ 193

Finance for Club Boards

6 | P a g e

Finance for Club Boards

7 | P a g e

Introduction

Finance for Club Boards

8 | P a g e

INTRODUCTION Welcome to the ClubsNSW Finance for Club Boards course. Boards of Directors have a significant influence on the management and financial performance of registered clubs. As part of this course you will be asked to refer to the documents and websites listed below.

ClubsNSW Club Industry Guide: Governance and Compliance

Club Code of Practice

Best Practice Guidelines (contained in the Club Code of Practice)

Registered Clubs Act 1976 and Registered Clubs Regulation 1996

Corporations Act 2001 (Commonwealth)

Associations Incorporation Act 1984 and Associations Incorporation Regulation 1999

The Office of Liquor Gaming and Racing (forms and fact sheets)

This course addresses five key areas of finance on club boards:

Operating in the not for profit sector Understanding financial concepts and reports

Monitoring Financial performance

Managing business changes,

External Financing options

Finance for Club Boards

9 | P a g e

Assessment and Accreditation

Completing the assessments for the Finance for Club Boards course means that you are able to achieve 1 unit of competency in BSB040907 Certificate IV Governance – BSBGOV403A Analyse financial reports and budgets. Completing the assessments for the Finance for Club Boards course means that you are able to achieve the following nationally recognised units of competency:

Assessment questions are clearly marked. There are multiple choice questions at the end of each unit to check your progress that must be completed online. It is important to understand that completing the multiple choice questions only is not sufficient to have an effect on your understanding of financial concepts. You must also complete the practical exercises provided. It is important to note that accreditation is optional. The fee for accreditation is not included in the course fee. Please note that ClubsNSW is not involved in the marking of assessments. It is marked by an external registered training organisation. The award which your unit will go towards is the Certificate IV of Governance. This is a nationally recognised certificate.

Certificate IV in Governance

ATQF Code BSB040907 Certificate IV in Governance

CORE BSBGOV401A Implement board member procedures BSBGOV402A Working within an organisational structure BSBGOV403A Analyse financial reports and budgets ELECTIVES BSBATSIM507A Establish and maintain a strategic planning cycle BSBMKG401A Profile the market BSBMGT405A Provide personal leadership BSBRSK401A Identify Risk and Apply Risk Management Processes BSBPMG408A Apply Contract and Procurement Processes BSBREL401A Establish Networks BSBDIV301A Work Effectively with Diversity

AQTF code BSB40907 Certificate IV in Governance

BSBGOV403A Analyse financial reports and budgets

Finance for Club Boards

10 | P a g e

Finance for Club Boards

11 | P a g e

Glossary of Financial Terms

Finance for Club Boards

12 | P a g e

GLOSSARY OF FINANCIAL TERMS There is wealth of jargon and terminology associated with financial management. It is helpful for you to understand these terms when reading financial statements. Accruals Also called accrued expenses. This item is usually included in

creditor’s payables and is typically estimated for expenses incurred by the Balance Sheet date but not yet invoiced by suppliers. E.g. Electricity used between the date covered by the last invoice and the Balance Sheet date, or interest on borrowings not paid by the Balance Sheet date.

Accrual accounting Recognising income and expenses when they occur rather than

when income is received or expenses paid. Accounting entry The basic recording of business transactions as debits and

credits. Accounts payable The amount the Club owes to vendors or suppliers for the

purchase of goods or services that are supplied on credit. Generally these liabilities are non interest bearing (although interest or fees may apply where the invoice is not paid by the due date).

Accounts receivables Amounts that are owed to the club, also known as debtors. It is

the amount owed to the club for from sales of goods and services which are yet to be paid (e.g. a function at a club) for which the customer is yet to pay. Customers are not normally charged interest unless there is a fee for late payment.

Amortisation The process by which the value of an intangible asset is

gradually reduced (based on its expected life). It is the allocation of the cost of an intangible asset over its expected useful life to the club.

ASIC Australian Securities and Investment Commission. Asset Anything having a commercial value that is owned by the club. Balance Sheet Also known as a statement of financial position shows all the

clubs assets, liabilities and accumulated members funds at a specific point in time.

Finance for Club Boards

13 | P a g e

Bank overdraft A form of short term finance. Usually provided by a Bank, the Club is authorised to overdraw its account up to an agreed set limit. Costs include set up fees and interest. An overdraft has no fixed term and is repayable on demand by the Bank. For this reason an overdraft should only be used for come and go purposes.

Break even The annual sales volume or sales revenue at which total margin

equals total annual fixed expenses, that is the exact sales amount at which the club covers its fixed expenses and makes a nil profit ( and avoids a loss). Break even is a useful point of reference in analysing profit performance and the effects of making sales in excess of break even.

Budget A financial plan the club, typically done once a year. Capital expenditure Funds used by the club to acquire or upgrade physical assets

such as property, buildings or equipment. This type of outlay is made by clubs to maintain or increase the scope of their operations. These expenditures can include everything from repairing a roof to building extensions to buying new gaming machines.

Cash accounting Accounting for income and expenses as they are received or

paid. Cash Flow The flow of cash into and out of the club. ClubsNSW The Registered Clubs Association of NSW. Cost of goods sold The direct costs attributable to the production of the goods sold

by the club. This amount includes the cost of the materials used in creating the goods along with the direct labor costs used to produce the good. It excludes indirect expenses such electricity, office costs etc. COGS appears on the income statement and can be deducted from revenue to calculate a clubs gross margin. Also referred to as ‘cost of sales’.

Constitution A constitution is a basic set of rules for the daily running of the club. It details for the club’s members and others the name, objects, methods of management and other conditions under which the club operates, and generally the reasons for its existence.

Creditors Any company or person that the club owes money to (creditor

balance).

Finance for Club Boards

14 | P a g e

Current Refers to the time period of less than 12 months which assists in

allocation of assets and liabilities. Debtors Any company or person who owes money to the club (debtor

balance). Deferred tax The postponement of tax payable to a future period. Depreciation The write-off of a portion of a fixed assets value in a financial

period based on its estimated useful life. Each year of an assets life is charged with part of its total cost as the asset gradually wears out and loses its economic value to the club. Most commonly an accelerated or straight line method of depreciation is used. An accelerated method allocates more of the cost to the early years than the later years. The straight line method allocates an equal amount to every year of the assets expected useful life.

EBIT Earnings before interest and income tax. EBITDA Earnings before interest, income tax, depreciation and

amortisation. EBITDARD Earnings before interest, income tax, depreciation,

amortisation, rent and donations. Employee Benefits This represents money owed to employees in the form of

wages, bonuses, annual leave, sick leave and long service leave entitlements which are expected to be paid.

Equity Also known as Members Equity is the accumulated funds from

the operation of the Club. It is the difference between assets and liabilities.

Expenses Money spent or cost incurred in the clubs efforts to generate

revenue, representing the cost of doing business. Expenses may be in the form of actual cash payments (such as wages and salaries), a computed expired portion (depreciation) of an asset, or an amount taken out of earnings (such as bad debts). Expenses are summarised and charged in the income statement as deductions from the income before assessing income tax.

Finance for Club Boards

15 | P a g e

Factoring A form of short term finance. Finance is secured against the debtors of the club and finance is usually provided by a finance company specialising in factoring. The club is effectively selling its debtor book (at a discount) and receives money in advance. The finance company then collects the payments from the debtors.

Financial ratio The method by which an organisation can measure the financial

health and compare their organisational operations to those of similar organisations in the same industry.

Financial year Accounting period that can start on any day of a calendar year

and has twelve consecutive months (52 consecutive weeks) at the end of which account books are closed, profit or loss is computed, and financial reports are prepared. It may or may not match a calendar year, but is often the financial year being 30 June.

Forecasting The process of predicting the future financial performance of an

organisation. GST Goods and Services Tax. Impairment When the carrying values of an asset is higher than its

recoverable amount, the asset must be written down to its recoverable amount. It is the reduction in the value of an asset because the asset no longer generates the benefits expected earlier, as determined by the club through periodic assessments. This could happen because of changes in market value of the asset, business environment, government regulations, changes in technology etc.

Income Tax Expense The total amount the club paid in company income taxes. Incorporation Means the Club becomes a legal entity in its own right, separate

from the individual members. Inventory The raw materials, work-in-progress goods and completely

finished goods that are considered to be the portion of a business’s assets that are ready or will be ready for sale. Inventory represents one of the most important assets that most businesses possess, because the turnover of inventory represents one of the primary sources of revenue generation.

Intangibles Assets that don’t have a physical form, e.g. patents, gaming

machine entitlements.

Finance for Club Boards

16 | P a g e

IPART Independent Pricing and Regulatory Tribunal. Leases (Financial) Leases are for a fixed period of time and the costs are in the

form of interest charges. Security is the equipment being financed. A finance lease is where the underlying substance of the transaction is a financing arrangement. An operating lease is where the underlying substance of the transaction is a rental agreement.

Liability The amount the club owes to external stakeholders. Loans Generally provided for a fixed purpose and repayable in a fixed

period of time. They have set repayment dates, and costs include interest and set up fees. May be secured secured by club assets.

Management Accounts Management accounts are any financial report that a club

prepares in order to help make management decisions. As these accounts are prepared for internal use only, the structure and content can be tailored to suit the club, and therefore their content varies greatly from club to club.

Mark-up The percentage by which the sales price exceeds the cost. Mutuality principle An entity’s income consists only of monies derived from

external sources. Accordingly, subscriptions and contributions from members for particular services provided by a club or association are generally excluded from the assessable income of that club or association.

Non-Current Refers to the time period of greater than 12 months which

assists in allocation of assets and liabilities. Not for profit Profits are not distributed to the individual members of the

organisation while either the organisation is in operation or when it ends, rather any profits must be used to further the organisation. It is reinvested back into the organisation to continue to pay and provide for its activities and services.

Overheads Costs not directly associated with the products or services sold

by the organisation.

Finance for Club Boards

17 | P a g e

Prepayments Are payments made in advance for goods and/or services. For example, prepaying for stock which will be delivered in the future, or services such as general insurance paid for in advance in the period in which they will be used (i.e. they will be used in the year after the balance sheet date).

Profit (surplus) Revenue minus expenses. Purchase order A commercial document issued by a buyer to a seller, indicating

the type, quantities and agreed prices for products or services the seller will provide to the buyer.

Revenue The income the club earns from its activities, including grants,

donations, fundraising and any trading income. Retained earnings Profits that have remained in the organisation. Short Term Finance Finance for a period of less than one year. It should only be used

to finance short-term capital requirements, such as working capital requirements.

Statement of Cash Flow One of the three primary financial statements prepared by the

club which summarises its cash inflows and outflows during a period according to a threefold classification being: Cashflow from operating activities, investing activities and financing activities.

Statement of Comprehensive Income The primary purpose of the income statement (also more

commonly referred to as a profit and loss statement) is to report the clubs earnings, over a specific period of time (usually one year) to its members. The income statement sets out the clubs income and expenses incurred, as well as its profit or loss for the period. The profit or loss figure is calculated by offsetting income against expenses for the period.

Statutory Financial Reports Required by and prepared in accordance with Federal or State

legislation. As their content is prescribed by law, their structure tends to be similar from club to club, being the clubs annual and quarterly reports.

Stock Goods that the club purchases to sell.

Finance for Club Boards

18 | P a g e

Trade credit A form of short-term finance provided to a business by its suppliers. It has few costs in terms of interest, and security is not required. Clubs should however, be mindful that discounts (for the goods) may be forgone if the club does not pay within a set time frame.

Working capital The excess of current assets over current liabilities.

Finance for Club Boards

19 | P a g e

Unit 1: Operating in the Not For Profit Sector

Finance for Club Boards

20 | P a g e

OPERATING IN THE NOT FOR PROFIT SECTOR In this section, we outline the distinction of organisations in Australia that classify as profit making entities and those that are not for profit entities. Learning Outcomes:

Understand types of clubs which compromise the 1500 venues across the state of NSW.

Understand the difference between an organisation that is classified as a ‘profit making entity’ and one which is ‘not for profit’.

Understand the definition of incorporation and why it is important.

Finance for Club Boards

21 | P a g e

16%

NSW Clubs in the Not For Profit Sector

The NSW Registered Club industry comprises almost 1500 individual venues spread across every region of the state with total membership of approximately 5.7 million. Clubs are independently managed which leads to high levels of diversity within the sector. Whilst clubs share a common non-profit, members’ based model and operate under the same regulatory regime, they are highly varied in their purpose.

Types of Clubs include:

Bowling clubs (approximately 471 venues)

Sporting and recreation clubs (approximately 265 venues)

Returned services clubs (approximately 231 venues)

League and football clubs (approximately 76 venues)

These clubs are also diverse in their size. The largest clubs can have more than 100,000 members and generate annual revenues in excess of $60 million per annum. These clubs provide a diverse range of products and services to their membership and local communities ranging from traditional hospitality and gaming to aged care, child care, swim centre’s and gymnasiums. Large clubs are also increasingly being involved in other commercial activities such as property investment and development, retail leasing and hotel accommodation. At the other end of the spectrum there are several small clubs that generate revenue of less than $20,000 and operate to provide facilities such as bowling green’s or golf courses for their small membership base.

Finance for Club Boards

22 | P a g e

What Does Not For Profit Mean?

Clubs form an essential part of the social fabric of Australian life. As not for profit organisations, clubs have utilised their revenue to build sporting and community infrastructure, support charities and provide a comfortable and affordable place to meet, eat, drink and enjoy entertainment. Clubs today also provide facilities such as aged accommodation, child minding and other in-house sporting facilities such as swimming centre’s and gyms. But do you understand what is meant by not for profit?

Types of Organisation

Organisations in Australia can be classified as either:

Profit-making entities, or

Not for profit entities.

Profit Making Entities

Common types of profit-making entities structures are:

Sole Proprietorship: (commonly known as sole trader business) is fairly simple to establish and allows for control of a business by an individual, E.g. Trades people such as plumbers, bricklayers, etc, often operate as sole traders.

Partnerships: is where 2 or more individuals form a partnership to conduct business with a view to profit. Common partnerships include doctors, accountants and lawyers.

Companies: are the most common structure used in business as a separate legal entity from its owners, who are referred to as shareholders.

In these ‘for profit’ organisations, the aim of the business is to make a profit, and those profits can be distributed to the organizations’ owners, or to individual members or shareholders. In these organisations, people who are involved in the organisation are entitled to receive a personal benefit from the profits. This benefit can come from direct payments, dividends or money when they sell their shares.

Finance for Club Boards

23 | P a g e

Not For Profit Entities

So, is a ‘not-for-profit’ (NFP) organisation one that makes no profit?

The answer is The term is actually a little misleading. Whether your organisation is a ‘not for profit’ organisation is determined by what your organisation does with that profit, not by whether your organisation makes a profit. Hence a better term would be, “not for private gain” as opposed to “not for profit.” In an NFP organisation, the profits are not distributed to the individual members of the organisation while the organisation is in operation or when it ends. Rather, any profit made by the organisation must be used to further the purpose of the organisation, which is reinvested back into the organisation to continue to pay and provide for its activities and services. The distinction between ‘for profit’ and ‘not for profit’ is clearly an important one. Given that NFP organisations have not been established by people to make a personal profit, but rather the resources of the organisation will be put back into helping the community, NFP organisations often receive favorable treatment in relation to tax, legal structures, fundraising, etc., and in terms of funding options such as government grants. Since 1969 all registered clubs have been required to be incorporated. Initially clubs could be incorporated under the Company legislation of the day or under the Co-operatives Act. However, the Registered Clubs Act now provides that all clubs must be incorporated only under the Corporations Act

What does “incorporation” mean?

Incorporation of a club means that it becomes a legal entity in its own right, separate from the individual members. Put another way, the club is considered at law to have a distinct identity that continues regardless of changes to the membership.

Finance for Club Boards

24 | P a g e

Why incorporate? The major features of becoming incorporated are:

the club acquires the powers of a body corporate with perpetual succession and a common seal;

the club may enter into contracts and acquire, hold and dispose of property;

the club can apply for government grants;

Members or officers of the club are generally not liable to contribute towards the payment of debts or liabilities of the club;

The club may sue or be sued;

If members or office bearers of the club incurred liabilities or obligations on behalf of the club prior to incorporation, those liabilities and obligations can be exercised against the incorporated entity; and

The name of the club concludes with the word “Incorporated” or the abbreviation “Inc.” as part of its name;

There are three different and distinct organisational models within the non-profit sector in Australia and they can be legally structured as:

A company limited by shares (under the Commonwealth Corporations Law) Limited by guarantee

A cooperative (under the relevant state or territory’s Cooperatives Act)

An association (under the relevant states or territory’s Association Incorporation Act), more suitable to small community based groups with limited resources.

In the NSW club industry, most clubs are companies limited by guarantee, however, there are approximately 100 clubs which are cooperatives. As noted above, all new clubs are now required to be incorporated under the Corporations Act, which means they must be companies limited by guarantee.

Company Limited by Guarantee

Limited by guarantee means the liability of the club’s members is limited to the amount the members undertake to contribute in the event the club is wound up. This is typically a nominal amount and is prescribed in the club’s constitution. As noted above, the registration of the club creates a legal entity separate from its members. And the club can hold property and can sue or be sued. Clubs are registered under the Corporations Act 2001 (Corporations Act), which is Commonwealth legislation administered by the Australian Securities and Investment Commission (ASIC).

Finance for Club Boards

25 | P a g e

The Club’s registration is recognised Australia wide. At the very least the Club must:

Have at least three directors and one secretary

Have at least one member

Have a registered office address and principal place of business located in Australia

Have its registered office open and accessible to the public

Be internally managed by a constitution or replaceable rules

Maintain a register of its members

Keep a record of all directors’ and members; meeting minutes and resolutions

Appoint a registered company auditor within one month of its registration

Keep proper financial records

Prepare, have audited and lodge financial statements and reports after the end of every financial year

Send to its members a copy of its financial statements and reports, unless the member has a standing arrangement with the company not to receive them

Hold an annual general meeting once every calendar year within five months after the end of its financial year

Lodge notices whenever changes to its officeholders, office addresses, constitution and its name occur within specified timeframes as determined by the Corporations Act

It is important to note that as a public company limited by guarantee and registered under the Corporation Act, directors generally have the same legal duties, responsibilities and liabilities as directors of commercial entities that are public companies registered under the Act.

Finance for Club Boards

26 | P a g e

Co-operatives

Co-operatives are a form of mutual organisation which has existed in Australia since the mid 19th century. The nature and function of co-operatives in Australia vary widely and can be set up as a profit making organisation or as a not for profit organisation. A not for profit co-operative is known as a non-trading co-operative. While a non-trading co-operative can conduct commercial activities, it is prohibited under law to distribute surplus funds to members from profits or winding up. An incorporated non-trading co-operative has mostly the same features of a company limited by guarantee.

It is a legal person that is separate from the persons who are its members.

It has the power to hold property, enter into contracts, and sue and be sued in its Club name.

Like other incorporated bodies, a co-operative is responsible for its debts, not the members who own the co-operative.

The co-operative is governed by the Co-operatives Act in each individual state, however, the Co-operatives Act makes reference to or adopts or repeats many relevant provisions of the Corporations Act.

Club Constitution

Every club has a constitution which sets out its objectives and rules. clubs that were incorporated before the Co-operatives Act came into effect may still have a memorandum and articles of association. Co-operatives are required to have a constitution which is referred to as “rules of the co-operative”. Since the Corporations Act came into effect the term “constitution” has been applied to the document which sets out the objects and rules of clubs and covers the memorandum and articles of association. Given the laws relating to clubs change from time to time, the Board needs to review their constitutions from time to time to ensure they are up to date. (In changing the same, given they are technical documents, it is recommended you seek legal advice before making changes to the clubs constitution).

Finance for Club Boards

27 | P a g e

Unit 2: Understanding Financial Concepts and Reports

Finance for Club Boards

28 | P a g e

UNDERSTANDING FINANCIAL CONCEPTS AND REPORTS In this section we will outline the key financial reports that should be prepared by registered clubs. We will provide a summary of the purpose of each type of report and an overview of the key issues and items to watch for when reviewing such reports. We will also look at some of the key financial concepts that should be understood by directors in order to properly administer their duties. Learning outcomes:

Understand the difference between statutory reports and management accounts

Be able to list the different types of statutory financial reports that are required to be prepared by registered clubs

Understand the major components of a statutory financial report prepared in accordance with the Corporations Act 2001

Understand the purpose of the three principal statements generally included in a statutory financial report and be able to identify issues

Finance for Club Boards

29 | P a g e

Setting the Scene for Good Financial Reporting

For directors and management, understanding your club’s financial position is critical to the success of the club, and therefore, the ability of the club to continually provide services to its members. Good financial management starts with precise record keeping and good information systems. As a director, are you comfortable that your club is keeping accurate records or has the required information systems? Knowing what financial statements or reports need to be produced and how to read these reports is critical to your clubs continued financial success.

Importance of Financial Reports

One of the principal roles of directors is to monitor the financial aspects of their clubs on behalf of members. This role requires directors to regularly review financial reports prepared by management and to seek explanations on key issues or risks that come to their attention. In addition, directors of registered clubs must ensure that financial information is regularly provided to members for their review. This includes the preparation and distribution of an audited annual financial report and the provision of quarterly information to members. It is therefore critical that directors understand the different types of financial reports, the key things to look for in each and some of the terms that are relevant when reviewing financial information. Types of Financial Reports Broadly, there are two major categories of financial reports:

Statutory Financial Reports, and

Management accounts.

Finance for Club Boards

30 | P a g e

Statutory Financial Reports These are required by and prepared in accordance with Federal or State legislation. As their content is prescribed by law, their structure tends to be fairly similar from club to club. The main form of statutory financial report is the annual financial report that is provided to the club’s members. Management Accounts These are prepared by clubs in order to assess their financial performance or position and to assist management and directors to make informed decisions about their club operations. As these reports are for internal use, the structure and content of management accounts varies significantly from club to club. There are a number of major differences, advantages and disadvantages, between statutory reports and management accounts. These differences are compared in the following table.

Finance for Club Boards

31 | P a g e

Comparison

Statutory reports Management accounts

Purpose For members and Regulators

For board and management

Content Dictated by the relevant legislation

Format largely standard

Includes annual financial report and quarterly report

Flexible

Dependent on the needs of the users

Frequency Once per year for Annual Report (Corporations Act 2001)

Quarterly report (Registered Clubs Regulation 1996)

As often as required

Generally prepared on a monthly basis and provided in advance of board meetings

Timeliness Annual Report to ASIC within four months of financial year-end

Quarterly report within 48 hours of the statements being adopted by the board.

As soon as possible for effective decision making

Advantages

Information can usually be found easily

Prepared in accordance with Australian Accounting Standards enabling comparisons to be drawn between other businesses and clubs.

Can provide information on financial performance of competitors given that they are publicly available

Structure and content tailored.

Access can be restricted, mitigating confidentiality considerations.

Often automatically generated by internal accounting software.

Quick to prepare and provide timely and relevant information

Disadvantages

Often lengthy and can be difficult to understand

Publicly available, enabling access by competitors

Required to be audited, therefore can be costly

Lack of detail, including detailed trading reports for each business unit or club location

Unless properly tailored, can often be lengthy, complicated and provide too much detail.

This can interfere with the objectives of the report.

Not audited or required to be prepared with in accordance with the Australian Accounting Standards, therefore potentially reducing the accuracy of the reports.

Finance for Club Boards

32 | P a g e

Statutory Financial Reports

Statutory financial reports are any financial report that a club is required by law to prepare. As noted previously, the structure, content and timing of such reports is governed by legislation. Clubs are liable for fines and penalties, if such reports are not prepared in accordance with statutory requirements. There are two main types of statutory financial reports that are prepared by registered clubs in NSW:

Quarterly financial reports, and

Annual financial reports.

Annual Financial Reports

As outlined in the Corporations Act the following are the club obligations in relation to Annual and Quarterly reporting:

Clubs can no longer distribute concise financial reports.

Members must make a standing election whether to receive a copy of the financial report. They can elect not to receive a copy.

Those members who chose to receive a copy then elect whether they receive a hard copy or an electronic copy of the full financial report.

Annual Reporting

Once members have elected their mode of delivery, the full Annual Financial Report must be provided to members the earliest of 21 days before the next Annual General Meeting (AGM) or 4 months after the clubs end of financial year date (sent by email or post as requested). What must be sent?

Directors Report

Financial Report

Auditors Report

Notice of Annual General Meeting

Full Financial Report (no concise report)

There is no longer a need to display reports on the clubs website, but you can continue to do so, (you might like to check your club’s constitution)

Finance for Club Boards

33 | P a g e

Quarterly Reporting

The club is required to prepare Quarterly Financial Reports, and a copy must be provided to those members who request a copy, (either by mail or post). A sign must be displayed at the club and on the clubs website noting the Quarterly Accounts are available. Quarterly financial statements are required to be prepared in accordance with Regulation 47H of the Registered Clubs Regulation 1996

Finance for Club Boards

34 | P a g e

Annual Financial Statements

The Components of the Annual Financial Report

The key components that are required in the annual financial report include the following:

1. Balance Sheet (also known on statement of financial position). The balance sheet should also be generated on a monthly basis to allow directors and management to review and analyse

2. Statement of Comprehensive Income (or better known as the Profit and Loss Statement)

3. Statement of Cash flows 4. Notes to the financial statements 5. Independent auditor’s report and lead auditor’s independence

declaration 6. Directors’ report 7. Directors’ declaration

Understanding all components of the annual financial statement is critical. These financial statements provide information on how the club is operating financially and why. Once this is understood, the information can be analysed to show the clubs areas of strengths and weaknesses for a given period.

Finance for Club Boards

35 | P a g e

UNDERSTANDING THE BALANCE SHEET (Statement of Financial Position) In this section, we explore the different components of the Balance Sheet. Learning outcomes:

Explain the meaning and purpose of the Balance Sheet

Understand what is an asset on a Balance Sheet

Explain the distinction between current assets and non-current assets

Understand the different types of current and non-current assets

Understand what a liability is on a balance sheet

Explain the distinction between current and non-current liabilities

Understand the different types of current and non-current liabilities

Understand the importance of debt on the Balance Sheet and being fully informed regarding the debts maturity profile

Understand the meaning of members equity

Explain and apply the Balance Sheet equation

Understand the definition of solvency

Identify and apply various ratios that can be used to assess short term solvency

Identify and apply Balance Sheet ratios that can be used to assess long term solvency

Identify limitations of the Balance Sheet

Finance for Club Boards

36 | P a g e

Key Components of the Annual Report

1. Balance Sheet (Also known as the Statement of Financial Position)

Let’s assume you are applying for a loan to put a swimming pool in your backyard. You go to the Bank asking to borrow the money, and the Bank asks for a list of your assets and liabilities. You pull out a piece of paper and write down everything you own of value (your house, money in savings account, car, furniture, etc.). Then at the bottom of the page you write down all of your debt (your mortgage, car payments, credit cards, etc.). You subtract all your debts from the value of all your assets, and you come up with your net worth.

Congratulations, you just created a Balance Sheet!

The Balance Sheet, also known as the Statement of Financial Position, provides a snapshot of a club’s financial position as at a particular point in time. It lists, in detail, the various assets owned by the club, what the club owes to third parties, and the net value of the club (members equity)

Finance for Club Boards

37 | P a g e

Elements of Balance Sheet

The three elements of the balance sheet are: Assets: are items of value owned by the club. The asset must have some future economic benefit to the club and it must be possible and reliable to measure the cost or value of such benefit. E.g. Cash, property, accounts receivable, equipment, furniture. Liabilities: are amounts owed by the club to external parties and include funds available to support the clubs operations by way of loans, for example, trade creditors, loans from banks, income tax payable. Equity: also known as member equity, is the accumulated funds from the operations of the club. It is the difference between assets and liabilities. Similar to our swimming pool finance example, the assets of the club minus the liabilities of the club equal the net worth of the club.

Finance for Club Boards

38 | P a g e

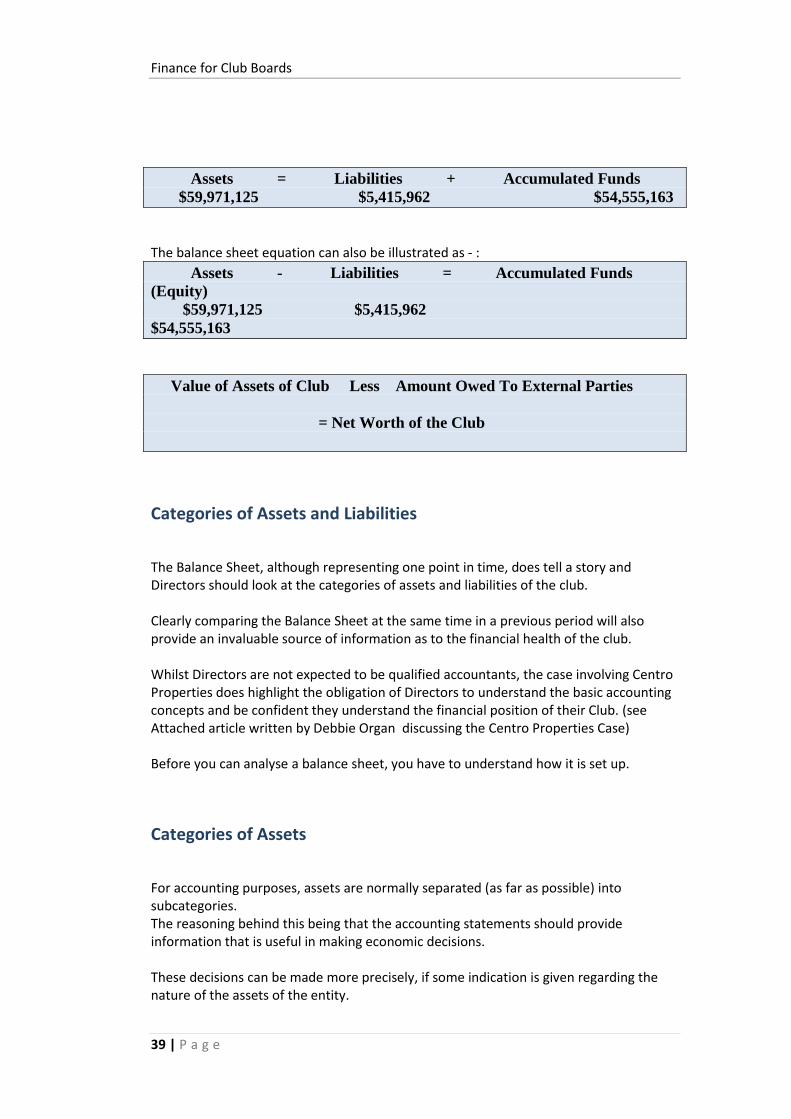

The following is an example of what a typical Club Balance Sheet looks like.

In the example for Example Club above, assets of $59.971m have been funded through liabilities of $5.415m and accumulated funds of $54.555m.

Finance for Club Boards

39 | P a g e

Assets = Liabilities + Accumulated Funds

$59,971,125 $5,415,962 $54,555,163

The balance sheet equation can also be illustrated as - :

Assets - Liabilities = Accumulated Funds

(Equity)

$59,971,125 $5,415,962

$54,555,163

Value of Assets of Club Less Amount Owed To External Parties

= Net Worth of the Club

Categories of Assets and Liabilities

The Balance Sheet, although representing one point in time, does tell a story and Directors should look at the categories of assets and liabilities of the club. Clearly comparing the Balance Sheet at the same time in a previous period will also provide an invaluable source of information as to the financial health of the club. Whilst Directors are not expected to be qualified accountants, the case involving Centro Properties does highlight the obligation of Directors to understand the basic accounting concepts and be confident they understand the financial position of their Club. (see Attached article written by Debbie Organ discussing the Centro Properties Case) Before you can analyse a balance sheet, you have to understand how it is set up.

Categories of Assets

For accounting purposes, assets are normally separated (as far as possible) into subcategories. The reasoning behind this being that the accounting statements should provide information that is useful in making economic decisions. These decisions can be made more precisely, if some indication is given regarding the nature of the assets of the entity.

Finance for Club Boards

40 | P a g e

The Categories used in Australia are:

Current Assets, and

Non-Current Assets (sometimes referred to as long term assets or fixed assets).

Current Assets

Whilst there are a number of ways current assets can be defined in accounting terms, the most applicable for the hospitality industry is: “a current asset means an asset that is held primarily for trading purposes or for the short term and is expected to be realized within 12 months of the reporting date”. As these assets are easily turned into cash, which is why they are sometimes referred to as ‘liquid assets.' Examples of the Current Assets include:

Cash: clubs cash holding will mostly be cash in the Bank, but a portion may also include petty cash or cash waiting to be banked in a safe Accounts Receivable: amounts owing to club by third parties, usually being customers who owe money for sale of goods or services to them (e.g. a function at a club) for which they are yet to pay Inventories: usually stock which the club has purchased for sale which remains unsold Prepayments: are payments made in advance for goods and or services. For example, prepaying for stock which will be delivered in the future, or services such as general insurance paid for in advance in the period in which they will be used (that is, they will be used with in the year after the balance sheet date).

Finance for Club Boards

41 | P a g e

Non-Current Assets

Most texts refer to non-current assets as ‘fixed assets’. “Non-Current Assets generally include those assets which were acquired with the intention of retaining them for the purposes of generating income over a number of years.” The term “non-current asset” is now applicable in Australia. (A non-current asset defined in accounting terms as “all assets that are not current assets: AASB 101). Examples of Non-Current Assets include:

Land and buildings: usually the land and buildings which house the club premises Plant and equipment: the infrastructure the club owns enables it to produce its goods and services including gaming machines, kitchen equipment, computer equipment etc. Investments: can be savings for a rainy day such as investments in shares, investment properties, or long term interest bearing securities. Intangibles: intangibles are non-physical assets that the club has bought (or valued) that hold value to the club and help it generate income (E.g. patents, brand and trades names etc.). The most common intangible in clubs is poker machine entitlements. These entitlements can be bought and sold, although the market price for these depends on demand at the time and regulatory restrictions for sale of the same. (Value of these should therefore be conservative as an inflated value can provide inflated security to directors/members) In the case of Example Club Limited, you will see the club has Intangible Assets of $678,946. Looking at note 14 to the accounts shows that this consists of 464 poker machine entitlements.

Finance for Club Boards

42 | P a g e

Review Activity 1

Before you progress: Explain in your own words the difference between current and non-current assets and why is it important to classify into sub groups?

What current and non-current assets are in your clubs Balance Sheet?

Categories of Liabilities

As is the case with assets, liabilities are classified into two classes:

Current Liabilities, and

Non-Current Liabilities

Current Liabilities

The definition of current liabilities is similar to that of current assets and can be defined in a number of ways in accounting terms, the most applicable for the hospitality industry is: “A current liability is a liability that is due to be settled within 12 months of the Balance Sheet date”.

Finance for Club Boards

43 | P a g e

Examples of current liabilities include: Bank Overdraft: An overdraft occurs when money is withdrawn from the clubs bank account and the available balance falls below zero. In this situation, the account is said to be ‘overdrawn’. If the club has a prior agreement with the Bank for an ‘overdraft limit’, then the club can withdraw funds, up to that limit, without being in default of the banking arrangements. Interest (usually higher than normal loan interest rates) is applied to the debit balance on a daily basis.

Many clubs have overdraft limits established on their accounts to allow for short term working capital needs, for example, where substantial tax payments are due. The advantage of an overdraft facility is that it is fairly easy to establish an overdraft limit, it is flexible and interest is only paid on amounts borrowed. The disadvantages of an overdraft however, is it cannot (and should not) be used for large borrowings or long term needs, as interest on overdrafts are higher than traditional loans, and Banks can change limits at any time or ask for money to be repaid immediately without notice. Irrespective of how other loans are negotiated or reviewed, an overdraft by definition is ‘repayable on demand’, for example, if your Bank suddenly becomes nervous about your club or the industry generally, they can demand payment of the full overdraft amount immediately. This has repercussions for the club, if you cannot repay, as you are immediately in default, which causes a cross default on all other banking facilities. Therefore, such a facility should be used with caution.

Trades and Other Payables: Amounts due to regular trade suppliers for goods and services received by the Balance Sheet date but not yet paid.

Loans and Borrowings: Amounts borrowed from third parties to help finance the Club. They may also be referred to as interest bearing liabilities and loans. E.g. bank loans, or other bonds and debentures. These loans are due and expected to be paid within 12 months of the Balance Sheet date. They should also include the current portion of any long term debt due, that is the same amount you have to pay during the next year as part of, say a 10 year loan.

Employee Benefits: This represents money owed to employees in the form of wages, bonuses, annual leave, sick leave, superannuation and long service leave entitlements which are expected to be paid or fall due within 12 months of the balance date.

Provisions: Are estimates for transactions and events occurring by the Balance Sheet date, but not yet paid, and expected to be realized within the next 12 months. Sometimes it can be difficult to estimate and it is not known exactly when it will be paid.

Finance for Club Boards

44 | P a g e

Examples of provisions expected to be settled within one year include provisions for tax payments, provision for link jackpots and member’s bonus point’s obligations, provisions for restructuring costs etc. Accruals: Also called accrued expenses, this item is usually included in payables creditors payable and is typically estimated for expenses incurred by the Balance Sheet date but not yet invoiced by Suppliers. E.g. Electricity used between the date covered by the last invoice and the Balance Sheet date, or interest due on borrowings not paid by the Balance Sheet date. Other Current Liabilities: Perhaps the most common other current liability you could see on a Club Balance Sheet is ‘Membership fees paid in advance’ (refer to Example Club Limited). Membership subscriptions represent annual membership fees paid by the Clubs members. The Club should recognise membership subscriptions pro-rata over the term of the membership and any unearned (unused) portion is included as ‘current liabilities’.

Non-Current Liabilities

A non-current liability is defined in accounting terms as: ‘A liability which is not a current liability’. These liabilities represent money the Club owes one year or more into the future. Examples of non-current liabilities include:

Loans and Other Borrowings – May also be referred to as ‘bank debt’. This represents money the Club has borrowed that does not need to be paid back for several years (by definition greater than one year).

IMPORTANT NOTE When an item has been classified as a non-current liability and becomes due for settlement within 12 months, it should be reclassified as a current liability. (See article written by Debbie Organ, Learning and Development Executive, ClubsNSW. Attached at the end of this section). This is important information for clubs. The reclassification of the item may reveal the club has liquidity and solvency problems if the club does not have the capacity to meet the repayment. For example, the club has a 10 year bank loan that was settled nine years ago. The club may have a good relationship with its Bank and expect that the Bank will merely renew the loan, and therefore it may continue to classify the loan as a non-current liability.

Finance for Club Boards

45 | P a g e

As noted in the article, this was the issue which Centro Properties directors faced, and the directors signed accounts which did not correctly classify substantial debt (over $2 billion) as current debt. Accounting standards require that such a loan must be classified as a current liability. Unless firm arrangements in writing have been completed (approved by the Bank and documents executed) for the loan to be extended beyond 12 months, that is, before the end of the accounting period. It is important for the club’s management and directors to be fully informed of the amount of the clubs debt, the interest payable and the maturity structure of the debt (timing of clubs obligations) so that they can properly assess the entities capacity to continue as a going concern. Employee Benefits: This represents money owed to employees in the form of wages, bonuses, annual leave, sick leave, superannuation and long service leave entitlements which are expected to be paid in the future but not within the next 12 months.

Other Liabilities: You may find your club has an entry called “other liabilities”. This is a ‘catch-all’ category where the Club can consolidate their miscellaneous debt.

You would normally find an explanation (in the notes to the accounts) of what makes up these liabilities. Often they consist of provisions, deferred tax liability, accrued expenses, etc. Generally, you should take the time to look at the various other liabilities the club has. Most will be self-explanatory and as a general rule, if classified as ‘other liabilities’ are not considered as important as the individual liabilities discussed above.

Members Equity

Member equity is the net worth of the club. It represents the net worth of the club after all creditors and debts have been paid. In the case of clubs, members’ equity is the accumulated profits (or losses) the club has generated. Looking at the members’ funds for Example Club Limited, member’s equity declined from $54,555,163 in 2011. This represents the $850,854 loss the Club recorded in 2011 as shown in the clubs income statement.

Finance for Club Boards

46 | P a g e

Well Done! You now understand what the Club Balance Sheet is and what the categories within the balance represents.

Finance for Club Boards

47 | P a g e

SO WHAT CAN THE BALANCE SHEET TELL YOU?

Club Solvency and Liquidity

The Directors of the club, in issuing the Annual Report must confirm that to the best of their knowledge the club can meet its obligations when due, therefore the club is solvent. WHAT ARE INDICATIONS OF INSOLVENCY (unable to meet obligations as they fall due?) In a 2003 decision the Courts referred to a check list of indicators of insolvency including:

Continuing losses

Liquidity Ratio less than 1

Overdue taxes

Poor relationship with Bank including inability to borrow

No access to alternative finance

Suppliers going on COD basis

Dishonoring cheques and issuing post dated cheques

Inability to produce timely accounts

Special arrangements with selected creditors and financiers

Solicitors, Letters, Judgments, etc. There would be a few cases where all of these indications are present just as there would be cases of insolvency where none or few were present.

Sometimes insolvency can be indicated (if not proved) by looking at the Balance Sheet.

Finance for Club Boards

48 | P a g e

The Club directors and management should endeavor to answer such questions as:

Does the club have enough cash to repay its debts tomorrow?

Does the club have enough cash to repay its debts if due in six months?

Will the club have enough cash to repay the loan if it is due in five years? In examining these questions, we need to:

Examine working capital and ratios to assist with short term decisions

Examine ratios concerning the long term decision

Short Term Solvency Indicators

Working Capital Working Capital arguably reveals more about the financial position of any business than almost any other calculation. It tells you what would be left if the club raised all of its’ short term assets and used them to pay off all of the clubs short term liabilities. The more working capital the club has, the less financial strain on the club. Working Capital is the easiest of all balance sheet calculations. It is represented by the current assets of the club minus its current liabilities.

WORKING CAPITAL = CURRENT ASSETS – CURRENT LIABILITIES One of the main advantages of looking at the working capital position is being able to foresee any financial difficulties that may arise. Even a club with millions of dollars in fixed assets will quickly find itself in trouble if it cannot pay its monthly bills. A club that fails to properly plan for its working capital requirements is likely to experience difficulties (financial pressure on clubs increased borrowings and late payment to creditors).

Liquidity Ratios

Further looking into the clubs’ working capital, Liquidity Ratio’s test whether the club will be able to pay its debts as and when they fall due, this is, “Is the club solvent?”

CURRENT ASSETS CURRENT RATIO = CURRENT LIABILITIES

Finance for Club Boards

49 | P a g e

An acceptable current ratio varies by industry; suggest an acceptable minimum ratio of 2:0 is the general norm (that is, current assets twice the value of current liabilities.) Generally speaking, the more liquid the current assets, the smaller the current ratio can be without concern, however, there should be a reasonable buffer of current assets over current liabilities as an indication of the club to pay its debts as when they fall due. As the current ratio approaches 1 (one) or below (which means the club has a negative working capital), the clubs liquidity should be reviewed. Clubs that have ratios around or below 1 should be those that have inventories that can be immediately converted to cash. If this is not the case, and the current ratio is low, this is a cause for concern and the Clubs liquidity should be reviewed and monitored.

Review Activity 2: Balance Sheet

Review the Balance Sheet for Example Club Limited and calculate the club’s working capital. What can be ascertained about this clubs working capital position?

Calculate the current ratio for Example Club Limited and comment on the result.

When looking at your clubs current ratio, interpretation (as with all other ratios) only makes sense when compared to the industry norm. This, however, is also not as straightforward as it sounds, as industry norms will vary based on the size and overall financial strength of each club. Also, any industry norm (for even like size clubs) will be the average, rather than the best, and so care has to be exercised. The club should also compare the ratio to trends in previous years. A trend showing a declining ratio would be cause for concern.

Finance for Club Boards

50 | P a g e

CURRENT ASSETS – INVENTORY ACID TEST (or quick ratio) = CURRENT LIABILITES If the club has concerns regarding its current ratio trends, the club may wish to use a more sensitive measure. This ratio, known as the Acid test of quick ratio, simply excludes the inventory from the current assets and compares the remaining current assets with the current liabilities. The reasoning behind the exclusion of inventory is that it will take time to turn into cash. It first has to be sold and then, where applicable, the debtors have to pay before the club can use the cash to pay creditors.

Long Term Solvency Ratios

To consider long term solvency, we look for ratio’s that assist in answering the last of the 3 (three) questions posed: “Will the club have enough cash to repay a loan if it is due in five years?” Therefore, will the club survive and remain a growing concern. Looking at our balance sheet, financial risk is the amount of Debt Finance compared to equity (member’s funds). TOTAL DEBT GEARING RATIO = MEMBERS FUNDS The debt to equity ratio measures how much money the club should safely be able to borrow over long periods of time. It does this by comparing the clubs total debt (including short term and long term debt) and dividing it by member’s equity. The result you get after dividing debt by equity is the percentage of the club that is indebted or leveraged. The acceptable debt to equity ratio will depend on economic factors, industry specific conditions and general feeling towards credit, however, as a general rule, debt to equity ratio’s over 45% - 50% should be looked at more closely, compared to like clubs, and compared to the gearing of the club in previous years.

Finance for Club Boards

51 | P a g e

According to a Club index for the Hunter and Central Coast region, gearing ratios for 2009-2011 are: INDUSTRY AVERAGE INDSTRY AVERAGE 10/11 9/10 GEARING: 0.58 0.49 (source: the Hunter and Central Coast, Club Index, 2009-2011 Forsythes accountants) As an industry, consider why gearing levels might have increased in 2010-2011? The reason is club borrowing increased considerably during this time. This followed a significant investment in capital improvements by clubs in the periods following the introduction of outdoor smoking bans. Since this time, capital investment in the industry has generally declined allowing clubs to reduce their overall gearing. Of course with consumer confidence currently low, poor consumer spending could be an issue, reducing revenue at a time when clubs are carrying higher debt levels. Monitoring of the clubs liquidity position would therefore be a priority. A club with debt to equity ratios above 50% (especially increased up on the previous year) together with a low working capital, and poor current and quick ratios, is a sign of serious financial weakness.

Understanding Your Debt to Assets

This ratio measures the percentage of a business's assets that are financed with debt, and can be calculated using the following formula:

Total Liabilities Debt to Assets = Total Assets This measures the percentage of assets being financed by liabilities. For example, if the club had $10 million of debt on its balance sheet and $15 million of assets, then clubs debt ratio is: Debt Ratio = $10,000,000 $15,000,000 = 0.67: 1 or 67%

Finance for Club Boards

52 | P a g e

This means that for every dollar of the clubs assets, the clubs has $0.67 of debt. A ratio above 1.0 indicates that the club has more debt than assets. The debt ratio also quantifies how leveraged a Club is. When the debt ratio is high, the Club has a lot of debt relative to its assets. It is thus carrying a bigger burden in the sense that debt repayments take a significant amount of the club's cash flows, and a hiccup in financial performance, or a rise in interest rates, could result in default. When the debt ratio is low, debt repayments payments don't command such a large portion of the company's cash flows, and the company is not as sensitive to changes in business or interest rates from this perspective. However, a low debt ratio may also indicate that the club has an opportunity to use leverage as a means of responsibly growing the business that it is not taking advantage of.

Congratulations, you now have the tools necessary to read and understand a balance sheet!

Review Activity 3: Balance Sheet

Review the Balance Sheet for Example Club Limited and calculate:

a) The club’s gearing ratio

b) The club’s debt to asset ratio

What do the results show about the long-term solvency of Example Club Limited?

Finance for Club Boards

53 | P a g e

Limitations of a Balance Sheet