finance for climate action - luxflag · pdf filefinance for climate action christopher...

TRANSCRIPT

Finance for Climate Action

Christopher Knowles, EIB

LuxFLAG Breakfast Seminar

Luxembourg, 25 November 2015

Climate Science – What Is The Problem?

2European Investment Bank Group

Source: IPCC

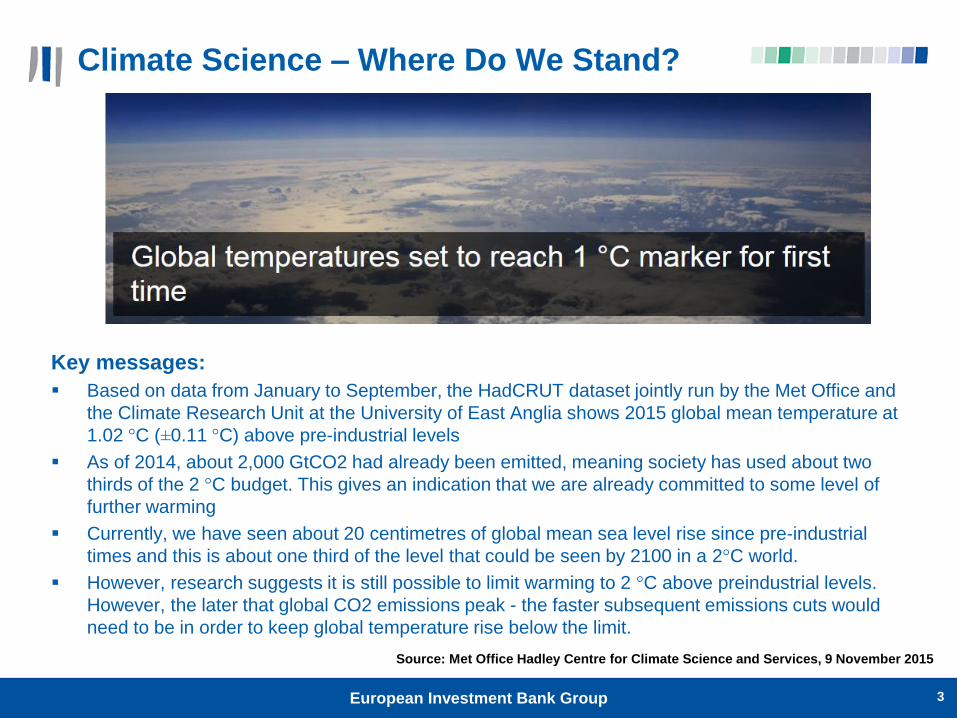

Climate Science – Where Do We Stand?

3European Investment Bank Group

Source: Met Office Hadley Centre for Climate Science and Services, 9 November 2015

Key messages:

Based on data from January to September, the HadCRUT dataset jointly run by the Met Office and

the Climate Research Unit at the University of East Anglia shows 2015 global mean temperature at

1.02 °C (±0.11 °C) above pre-industrial levels

As of 2014, about 2,000 GtCO2 had already been emitted, meaning society has used about two

thirds of the 2 °C budget. This gives an indication that we are already committed to some level of

further warming

Currently, we have seen about 20 centimetres of global mean sea level rise since pre-industrial

times and this is about one third of the level that could be seen by 2100 in a 2°C world.

However, research suggests it is still possible to limit warming to 2 °C above preindustrial levels.

However, the later that global CO2 emissions peak - the faster subsequent emissions cuts would

need to be in order to keep global temperature rise below the limit.

Laudato Si – Demand Side

4

There is an urgent need

to develop sources of

renewable energy.

Pope Francis

Picture: Wikimedia

European Investment Bank Group

To Get to 2°C Will Require An Additional

$8.6 trillion of Investment into Clean Energy over The Next 25 years

5

Source: Bloomberg New Energy Finance

● If the world is to stay on track to limit global warming to below a 2°C rise average temperatures, world emission must drop

sharply over the coming decades.

● A significant portion of abatement must come from the energy sector. In line with the IPCC’s carbon budget, we estimate that

to keep within a 2°C trajectory will require clean energy investment to double – or an additional $8.6 trillion over the next 25

years.

Note: Estimate based on XXXGt of the carbon budget apportioned to the power sector (IPCC). Investment by

technology assumed to be in the same proportions as in our base case forecast

INVESTMENT IN CLEAN ENERGY OUT TO 2040, BY

FIVE-YEAR PERIOD AND CUMULATIVE TOTAL

($TRILLION)An additional $8.6 trillion of

investment is needed by 2040

to stay on track for 2°C

GLOBAL POWER GENERATION MIX IN 2040, BNEF

FORECAST VS 2°C SCENARIO

25%

1%

18%

5%

14%

23%

14%

23%

10%

16%

8%

13%

6%11%

2% 4%2% 3%

2%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

BNEF forecast Needed for 2°C

Other

Offshore wind

Biomass/WtE

Small-scale PV

Utility-scale PV

Nuclear

Onshore wind

Hydro

Gas

Coal0

2

4

6

8

10

12

14

16

18

20

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2015-2020 2021-2025 2026-2030 2031-2035 2036-2040

024681012141618200.00.51.01.52.02.53.03.54.04.55.0

2015-2020 2021-2025 2026-2030 2031-2035 2036-2040

Needed for 2°C

BNEF forecast BAU

Cumulative total needed for 2°C (right-hand y-axis)

BNEF forecast total (right-hand y-axis)

024681012141618200.00.51.01.52.02.53.03.54.04.55.0

2015-2020 2021-2025 2026-2030 2031-2035 2036-2040

Needed for 2°C

BNEF forecast BAU

Cumulative total needed for 2°C (right-hand y-axis)

BNEF forecast total (right-hand y-axis)

European Investment Bank Group

Global Landscape of Climate Finance 2015

6

Source: Climate Policy Initiative

European Investment Bank Group

New Investment in Clean Energy ($BN)

7

$60bn

$88bn

$128bn

$175bn

$205bn

$206bn

$273bn

$318bn$295bn

$268bn

$318bn

46%

46%

36%

17%

0.4%

33%

16%

-7%

-9%

19%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Note: Total values include estimates for undisclosed deals. Includes corporate and government R&D, and spending for

digital energy and energy storage projects (not reported in quarterly statistics).

Source: Bloomberg New Energy Finance

European Investment Bank Group

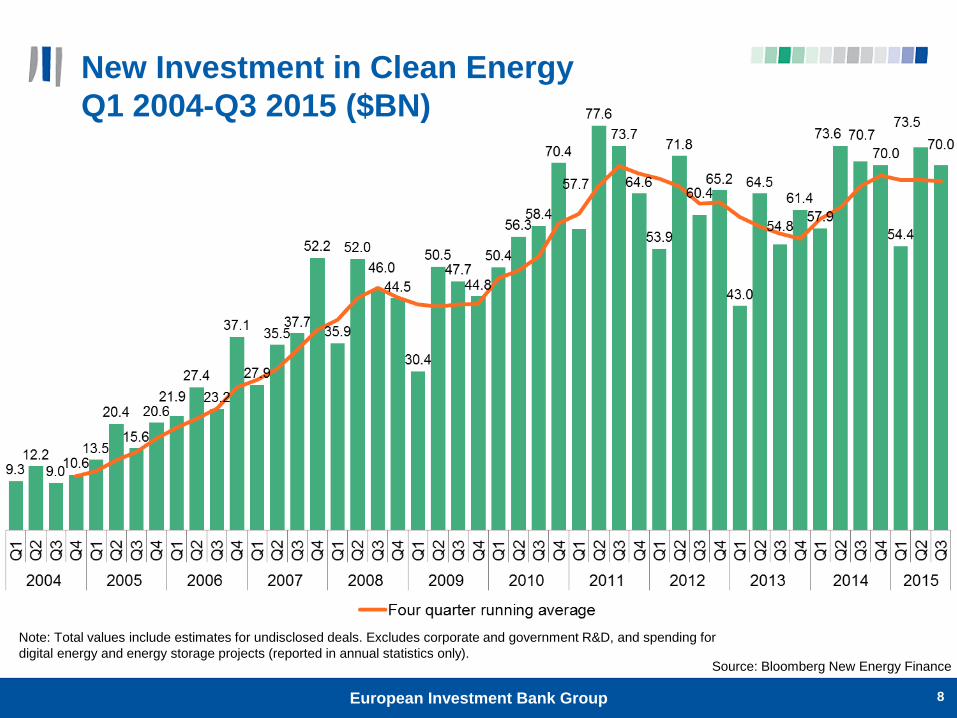

New Investment in Clean Energy

Q1 2004-Q3 2015 ($BN)

8

Note: Total values include estimates for undisclosed deals. Excludes corporate and government R&D, and spending for

digital energy and energy storage projects (reported in annual statistics only).Source: Bloomberg New Energy Finance

European Investment Bank Group

New Investment in Clean Energy by Region

($BN)

9

$28bn$39bn

$53bn$75bn

$90bn $91bn

$126bn $133bn$109bn

$75bn $83bn$13bn

$24bn

$44bn

$58bn

$62bn$50bn

$68bn

$85bn

$74bn

$65bn$74bn

$19bn

$26bn

$31bn

$42bn

$52bn$65bn

$80bn

$99bn

$113bn

$127bn

$161bn

46%

46%

36%

17%

0.4%

33%

16%

-7%

-9%

19%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

EMEA AMER APAC

Note: Total values include estimates for undisclosed deals. Includes corporate and government R&D, and spending for

digital energy and energy storage projects (not reported in quarterly statistics).Source: Bloomberg New Energy Finance

European Investment Bank Group

10

APAC New Investment in Clean Energy

by Sector Q1 2004-Q3 2015 ($BN)

Note: Total values include estimates for undisclosed deals. Excludes corporate and government R&D, and spending for

digital energy and energy storage projects (reported in annual statistics only).Source: Bloomberg New Energy Finance

European Investment Bank Group

EMEA New Investment in Clean Energy

by Sector ($BN)

11

Note: Total values include estimates for undisclosed deals. Excludes corporate and government R&D, and spending for

digital energy and energy storage projects (reported in annual statistics only).Source: Bloomberg New Energy Finance

European Investment Bank Group

Many Clean Energy Sources Are Already

Competitive

12

0 100 200 300 400 500

NuclearCHP

Coal firedNatural gas CCGT

Geothermal - flash plantLandfill gas

Large hydroSmall hydro

Wind - onshoreGeothermal - binary plant

Municipal solid wasteBiomass - incinerationBiomass - gasification

Biomass - anaerobic digestionPV - c-Si tracking

PV - c-SiPV - thin film

Wind - offshoreSTEG - tower & heliostatSTEG - parabolic trough

STEG - LFRMarine - tidal

Marine - wave

Q2 2013 central H1 2014 central

8441037

US China Europe AustraliaFossil technologies:

Onshore

wind as low

as $37/MWh

PV projects

as low as

$58/MWh

Note: LCOEs for coal and CCGTs in Europe and Australia assume a carbon

price of $20/t. No carbon prices are assumed for China and the US. Source: Levelised cost of electriicity 2014, Bloomberg New Energy Finance

European Investment Bank Group

Private Investments in Onshore Wind

and Solar PV

13

Source: Climate Policy Initiative

European Investment Bank Group

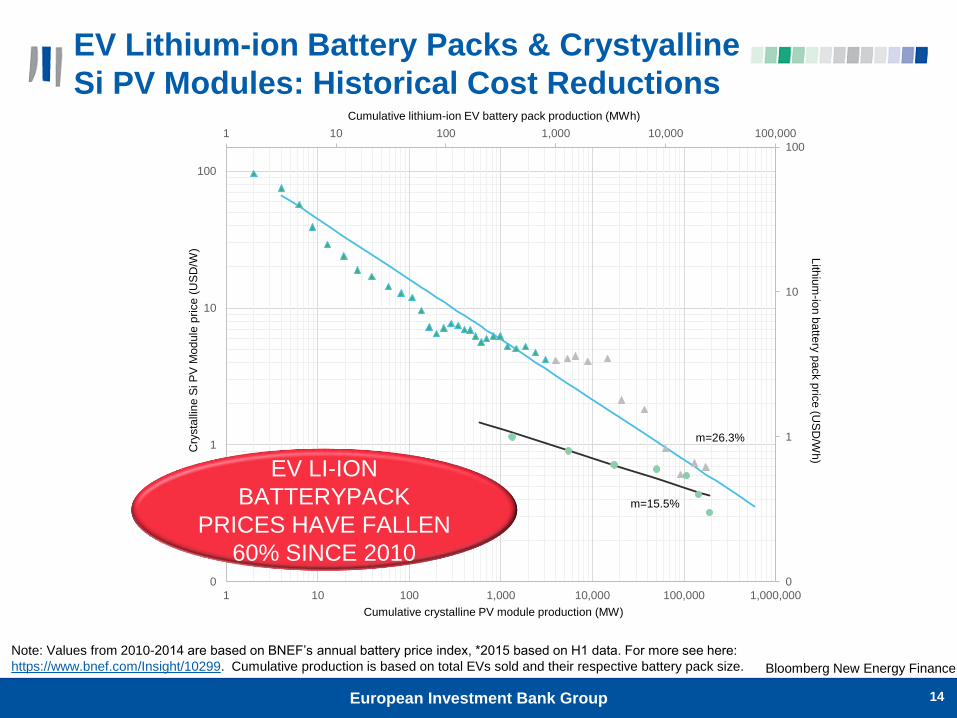

EV Lithium-ion Battery Packs & Crystyalline

Si PV Modules: Historical Cost Reductions

14

1 10 100 1,000 10,000 100,000

0

1

10

100

0

1

10

100

1 10 100 1,000 10,000 100,000 1,000,000

Cumulative lithium-ion EV battery pack production (MWh)

Cumulative crystalline PV module production (MW)

Cry

sta

llin

e S

i P

V M

od

ule

pri

ce

(US

D/W

)

Lith

ium

-ion

ba

ttery

pa

ck p

rice

(US

D/W

h)

m=15.5%

m=26.3%

EV LI-ION

BATTERYPACK

PRICES HAVE FALLEN

60% SINCE 2010

Note: Values from 2010-2014 are based on BNEF’s annual battery price index, *2015 based on H1 data. For more see here:

https://www.bnef.com/Insight/10299. Cumulative production is based on total EVs sold and their respective battery pack size. Bloomberg New Energy Finance

European Investment Bank Group

UK LCOE by Technology

H2 2015 ($/mwh)

15

0 50 100 150 200 250

Wind - onshore

Natural gas CCGT

Coal

PV - c-Si (U)

Note: Natural gas CCGT and coal includes a carbon cost of $26/tonneSource: Bloomberg New Energy Finance

European Investment Bank Group

The Economist Cover, “Sheikhs versus Shale”

December 2014

16

Source: The Economist

European Investment Bank Group

WTI Crude Oil Prices, 2000–2015

($2015 / barrel)

17

0

20

40

60

80

100

120

140

160

180

2000 2002 2004 2006 2008 2010 2012 2014

or ?Note: The Green line represents the WTI Spot price, and has been adjusted for

inflation and is represented here in real 2015 US$

Source: Bloomberg New Energy Finance, EIA,

World Bank

European Investment Bank Group

Coal

18

The coal business in

the United States

has kind of died, so

we’re out of the coal

business now.

Bill Koch

Picture: Forbes

European Investment Bank Group

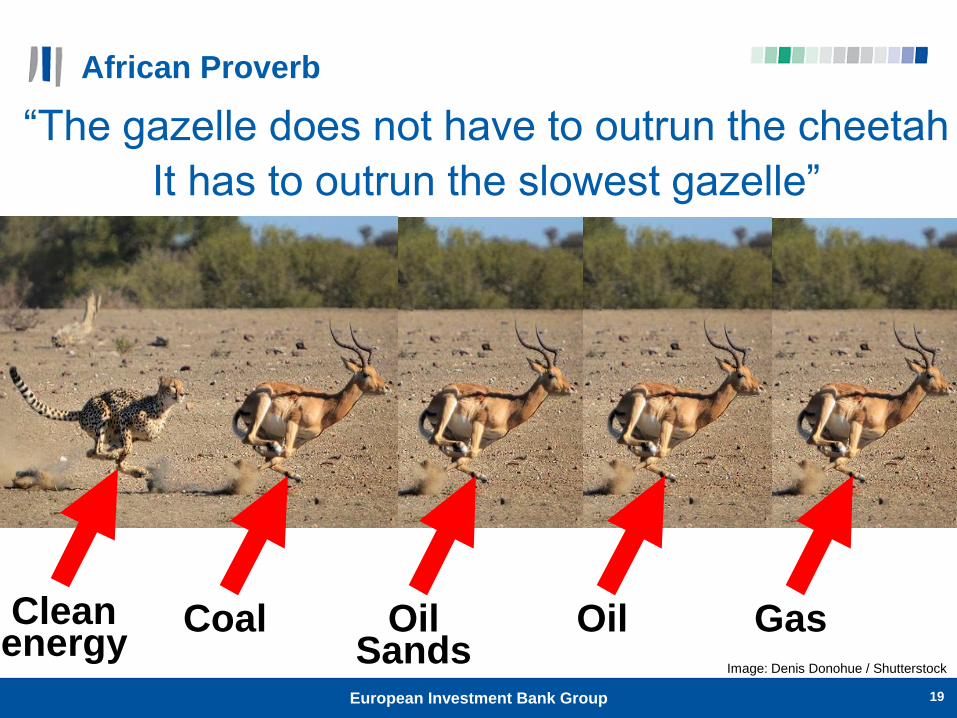

African Proverb

19

“The gazelle does not have to outrun the cheetah

It has to outrun the slowest gazelle”

Cleanenergy

Coal OilSands

Oil GasImage: Denis Donohue / Shutterstock

European Investment Bank Group

However, Challenges for Clean Energy

Investments Remain

20

No long-term policy certainty RE energy technologies

often lack track record

Retroactive changes to

regulatory frameworks

Higher upfront unit

capital cost

Regulatory changes

(e.g. Basel III & Solvency

II) lead to shorter-term

project finance (5-7 yrs

instead of 10-15 yrs)

Very sensitive to cost of

capital due to frontloading of

investment

Many utilities lack balance

sheet for investment

Current trend: shorter debt tenors

& earlier refinancing necessary

Renewable energy (RE) project

perceived as less reliably profitable

Earlier refinancing requirements

may require “refinancing premium”

Challenges lead

to financing

gap and fewer

new projects

while opposite

is needed!

Global Level Project Level

European Investment Bank Group

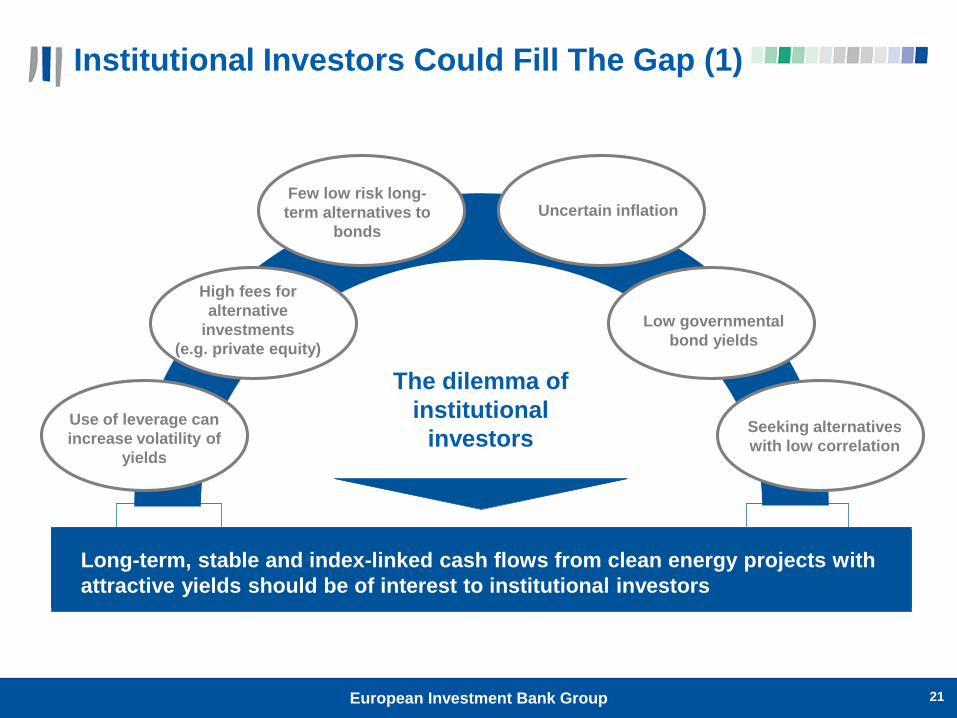

Institutional Investors Could Fill The Gap (1)

21

Few low risk long-

term alternatives to

bonds

High fees for

alternative

investments

(e.g. private equity)

The dilemma of

institutional

investors

Uncertain inflation

Low governmental

bond yields

Use of leverage can

increase volatility of

yields

Seeking alternatives

with low correlation

• Institutional investors currently lack investment opportunities

• Should be interested in long-term, stable and index-linked cash flows from

renewable energy (RE) projects

Long-term, stable and index-linked cash flows from clean energy projects with

attractive yields should be of interest to institutional investors

European Investment Bank Group

Institutional Investors Could Fill The Gap (2)

22

Re-directing even a small fraction of institutional investors’ allocations

could provide significant capital flows to clean energy investments

Institutional investors’ assets under management Potential for more

RE investment

exists

~USD 83 trillion

under management

by institutional

investors (2012)

Only a small portion

(1%) invested in

infrastructure

Even less in clean

energy such as RE

European Investment Bank Group

Need To Address Barriers to Clean Energy

Investments for Institutional Investors

23

Need to transform long-term finance need for low carbon into an investable

product that can be assessed within existing risk/reward framework

Acknowledge different risk/reward appetite from institutional investors

Main difficulty for

institutional

investors: “low

carbon” not an

investment class

Investments in RE

projects require

special knowledge

and capacity to

assess underlying

assets, which only

few institutional

investors have

Typical institutional investors’ asset allocation

Source: IFC (adapted)

Possible

asset

classes

European Investment Bank Group

What Is the European Investment Bank?

EIB is the EU’s long-term lending bank set up in 1958 by the

Treaty of Rome, headquartered in Luxembourg

EIB shareholders are the 28 EU Member States

Largest multilateral lender and borrower in the world

Around 400 projects annually in more than 160 countries

Around 10% of financing is for projects outside the EU

Financing is in support for EU priority objectives (climate change,

infrastructure, energy, SMEs, regional development, etc.)

24European Investment Bank Group

Green Bond Issuance

Outstanding environmental bonds

issued by MDBs (size > USD 100m)^

^Source: market data collected by Credit Agricole CIB; as of 27 April 2015

ADB4% AFDB

4%

EBRD1%

EIB45%

IBRD26%

IFC15%

NIB5%

CAB issuance to date: EUR 9bn equivalent in 10 currencies

EUR CAB due 2019 - largest green bond in the market at EUR 3bn

Focus on EUR & USD, tenors up to 10 years

EIB CAB issuance by currency*

EUR54%

GBP14%

SEK11%

USD9%

ZAR3%

CHF3%

AUD2%

BRL2%

TRY1%

JPY0.4%

*As of 23 April 2015

25European Investment Bank Group

EIB Climate Awareness Bonds – Key Features

Scale: Largest green bond issuer to date (EUR 9bn) and in 2014 (EUR 4.3bn)

Liquidity: Largest green bond (EUR 3bn), liquid size in USD and GBP

Capacity: Large flow of climate action lending

Green Bond curve in EUR: two references in 5- and 12-yr tenors

Clear sector focus: Projects in Renewable Energy and Energy Efficiency

Quality: Project due diligence expertise, applying high EU standards

Transparency: Detailed reporting on use of proceeds (audited sustainability report

+ dedicated newsletter) and policies (required as Aarhus signatory)

Project impact reporting (2014 CAB newsletter) released 27th March 2015

Verification / audit: external audit of reporting on the use of proceeds

Exposure to EIB credit, not projects: CABs rated pari passu with other EIB bonds

(AAA/Aaa/AAA)

No premium charged - priced like other EIB bonds of same size & maturity

Open to SRI and mainstream investors

26European Investment Bank Group

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

2010 2011 2012 2013 2014

EUR

m

Renewable Energy Energy efficiency RD & I Transport Other & miscellaneous** Adaptation

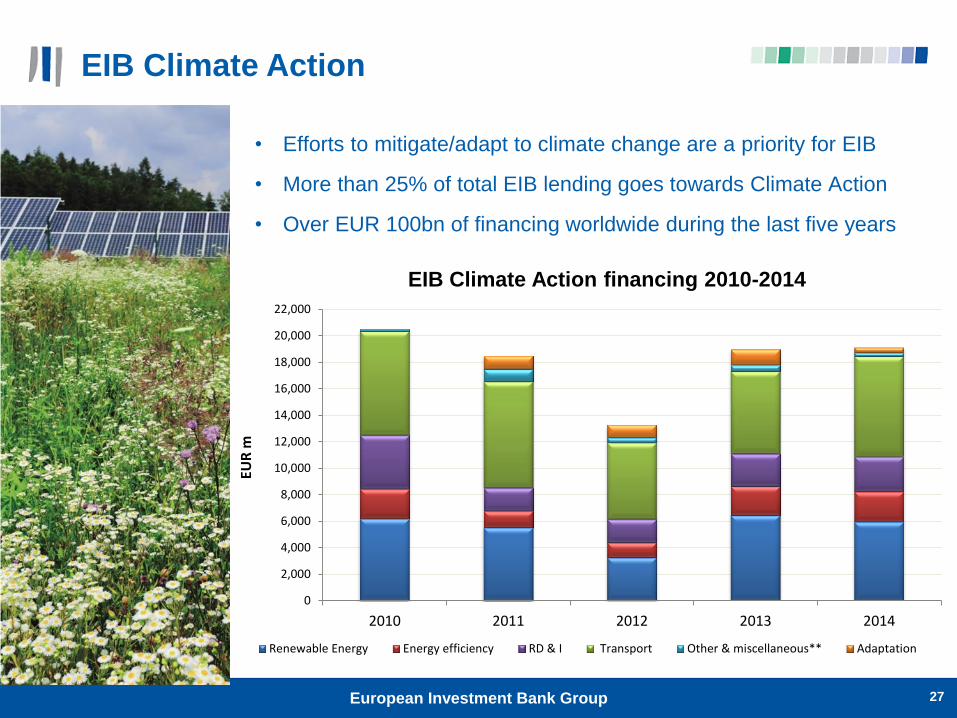

EIB Climate Action

• Efforts to mitigate/adapt to climate change are a priority for EIB

• More than 25% of total EIB lending goes towards Climate Action

• Over EUR 100bn of financing worldwide during the last five years

27

EIB Climate Action financing 2010-2014

European Investment Bank Group

EIB Financing Instruments

The EIB has an extensive range of instruments to finance public and private

sectors at investment and sub-investment grades of risk to its disposal

28

EIB lending instrument for Investment Grade operations

Special Activities

For low and sub investment Grade operations

Project Finance

Direct Loans

Project

Project finance with

direct project risk

LGTT/RSFF

(Mezzanine)

Equity through

Funds

Intermediated Loans

Banks

Public Sector

Financing

European Investment Bank Group

Fund Investments

29European Investment Bank Group

Fund investments demonstrate the EIB’s catalytic effect

Efficient use of EIB capital through a leverage effect

Policy test upfront and project driven (i.e. primary focus on the underlying

assets in terms of fit with EIB objectives and economic benefit)

Can invest time to work with a fund manager from concept stage

Can go into segments not quite mainstream yet

(e.g. bio-diversity, land decontamination, land use/carbon)

Can support start-up teams and new concepts

Can play different management roles alongside investment

€10 EIB commitment

€100 of Equity

available to projects

that meet

EIB objectives €90 third party

commitments

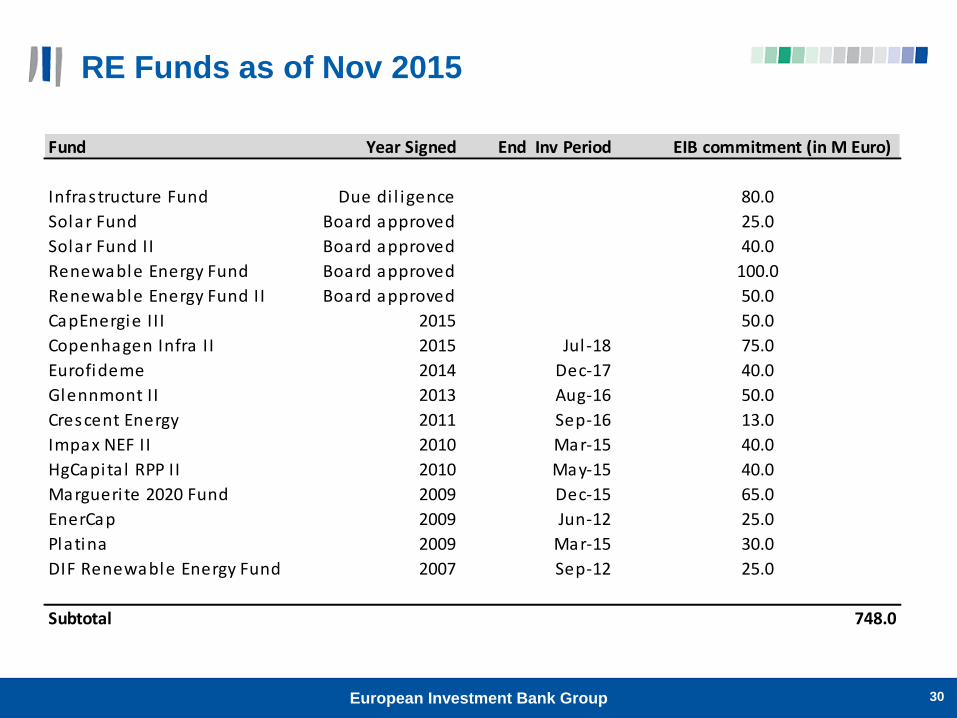

RE Funds as of Nov 2015

30European Investment Bank Group

Fund Year Signed End Inv Period EIB commitment (in M Euro)

Infrastructure Fund Due di l igence 80.0

Solar Fund Board approved 25.0

Solar Fund II Board approved 40.0

Renewable Energy Fund Board approved 100.0

Renewable Energy Fund II Board approved 50.0

CapEnergie II I 2015 50.0

Copenhagen Infra II 2015 Jul -18 75.0

Eurofideme 2014 Dec-17 40.0

Glennmont II 2013 Aug-16 50.0

Crescent Energy 2011 Sep-16 13.0

Impax NEF II 2010 Mar-15 40.0

HgCapita l RPP II 2010 May-15 40.0

Margueri te 2020 Fund 2009 Dec-15 65.0

EnerCap 2009 Jun-12 25.0

Platina 2009 Mar-15 30.0

DIF Renewable Energy Fund 2007 Sep-12 25.0

Subtotal 748.0

By Energy Source

RE Funds Signed Exposure Analysis – Nov 2015

By Country

France22,4%

UK10,9%

Sweden10,2%

Germany10,5%

Ireland8,2%

Poland7,5%

Finland5,8%

Italy3,8%

Portugal3,7%

Spain2,8%

Benelux2,6%

Romania1,7%

Croatia1,0%

Cyprus0,9%

Slovakia0,6%

Czech0,3%

Bulgaria0,2%

Greece0,0% Other EU

1,6%Non EU

5,2%

PV Solar 24%

Onshore Wind48%

Offshore Wind10%

Hydro4%

Biomass7%

Other7%

31European Investment Bank Group

Example Sustainable Land Use Fund: Althelia

32

The Althelia Climate Fund is an innovative, pilot sustainable land use

investment fund.

Focus: nature conservation and sustainable forestry management, in particular

REDD+ (tropical forest conservation activities that reduce greenhouse gas (GHG)

emissions by avoiding deforestation and forest degradation, protecting and

enhancing forest carbon stocks)

EIB cornerstone investment with BNP Paribas, FMO (Netherlands

Development Finance Company), FinnFund & Church of Sweden. Fund

closed in 2013 with EUR 60m+ in commitments

Project investments: generate revenues from forest carbon stock

conservation and non-carbon sources (e.g. non-timber forest products,

sustainable agriculture and other services/commodities)

Risk mitigation: Althelia finalised negotiations for an USAID guarantee to partially

offset the price risk for generated carbon credits (so-called Advanced Market

Commitment)

Good example of new market segment with policy risk mitigation

European Investment Bank Group

New Initiative: Natural Capital Facility (NCF)

33

Promote Green Infrastructure (GI), conservation, adaptation to climate

change Financing GI: urban, rural, built structures using nature

Natural Conservation: site preservation, recreation activities

Ecosystem-based Climate Adaptation: marine/coastal protection, natural management of basins,

rivers/canals

Water Cycle catchment management: rainwater collection, SUDS, natural wastewater filtration, flood

defence

Projects optimised through use of market-based instruments (e.g. PES and

Offsetting Credits) Payment for Ecosystem Services (provided by biodiversity, watershed etc.) on the principle of beneficiary

pays

Compensation and offsettings (for impacts on biodiversity, soil etc.) on the principle of polluter pays,

eventually subsequent “no net loss and securing net gain” with generation of offsetting credits

Soil and forest sequestration of carbon with generation of carbon credits

Pro-biodiversity businesses generating green services & commodities

markets / Nature-based climate change adaptation businesses Small pro-biodiversity businesses

Sustainable Forestry and Agriculture (including biomass), Sustainable Aquaculture

Nature-based processes or technologies for climate change adaptation

Waste: Remediation and regeneration of polluted land

Restoration of natural sinks absorbing waste

Recycling of organic waste including. bioenergy

European Investment Bank Group

Layered-Risk Funds

Layered-risk funds allow the issuance of different share tranches and notes to offer

investors different risk-return profiles.

The capital structure of such an investment vehicle typically rests upon the provision

of a first loss piece (termed junior C shares in the figure below) by donors.

Once the asset side of the fund develops, this structure allows the possibility to

issue notes to private investors who remain most senior in the cash waterfall.

34European Investment Bank Group

Example: Layered Debt/Equity Fund: EEEF

35

The European Energy Efficiency Fund (EEEF) is managed by Deutsche Bank

(www.eeef.eu) aims to provide market-based financing for commercially

viable public energy efficiency (70%) and renewable energy projects (30%)

within the European Union

Total size: EUR 265m (EUR 125 Mio EERP, EUR 75m EIB, EUR 60m CDP

and EUR 5m DB)

Beneficiaries: Local & regional Public authorities, but PPPs are possible

Financing in form of loans, guarantees, forfeiting schemes (to finance ESCO

projects).

Technical Assistance (grant) is available to structure projects

EEEF offers a layered risk/return structure for investors with a

fixed commitment of EU budget funds

European Investment Bank Group

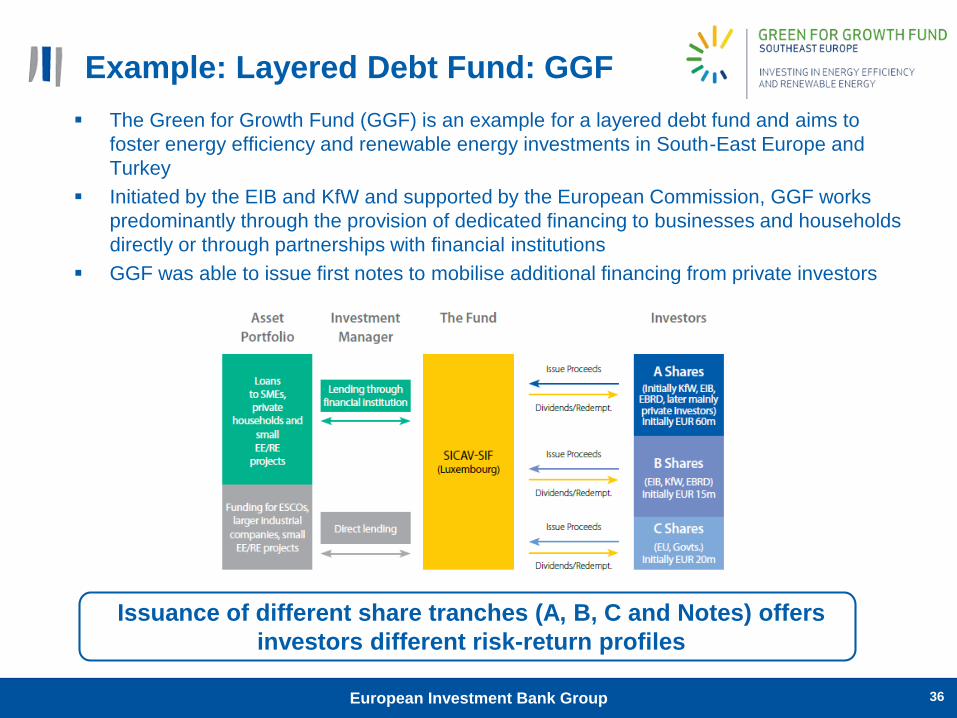

Example: Layered Debt Fund: GGF

The Green for Growth Fund (GGF) is an example for a layered debt fund and aims to

foster energy efficiency and renewable energy investments in South-East Europe and

Turkey

Initiated by the EIB and KfW and supported by the European Commission, GGF works

predominantly through the provision of dedicated financing to businesses and households

directly or through partnerships with financial institutions

GGF was able to issue first notes to mobilise additional financing from private investors

36

Issuance of different share tranches (A, B, C and Notes) offers

investors different risk-return profiles

European Investment Bank Group

Example: Fund of Funds: GEEREF

37

GEEREF is a fund of funds and provides global risk capital to energy

efficiency and renewable energy projects in developing countries and

economies in transition (African, Caribbean and Pacific region, non-EU

Eastern Europe, Latin America and Asia)

GEEREF is sponsored by the European Union, Germany and Norway and

advised by the European Investment Bank Group focusing on a triple bottom

line of people, planet and profit

GEEREF completed a fundraising campaign in June 2015 and raised over

EUR 110m in private capital in additional to the EUR 112m contributions from

the sponsors

GEEREF is one of the first instruments that has demonstrated that it is

possible to mobilise private financing by using public funds a risk capital in a

financing structure

European Investment Bank Group

Concept: Renewable Energy Platform for

Institutional Investors (REPIN)

38

REPIN bridges between short-term lenders and long-term institutional

investors

REPIN

Need to overcome “chicken and egg” dilemma: developers lack investment signals while institutional investors lack suitable products for RE investments

Guaranteed access to refinancing should stimulate more deal flow

Institutional investors have interest in long-term, stable and index-linked cash flows from operational RE projects

Regulatory changes (Basel III & Solvency II) should lead to shorter debt tenors and earlier RE refinancing requirements

Aggregation of projects and standardisation can streamline approval process and reduce transaction cost

Technical support required to structure suitable investments and reduce knowledge gaps

European Investment Bank Group

REPIN Concept: Key Objectives

39

Create more

RE deal flow

Focus is on

refinancing of

commercial

bank debt

Main objective

Free commercial lending capacity for further RE

investments2

Enable institutional investors with varying risk/reward

profiles to acquire mature long-term RE assets3

Lower cost of capital to improve RE project bankability:

provide commercial lenders with ‘guaranteed exit’ and

remove refinancing risk premium from equity1

Key elements

Ultimate goal: simultaneously stimulate deal flow and engage

institutional investors to increase overall RE financing

European Investment Bank Group

REPIN Concept: Structure

40

Straight pass-through of

loans from a project or

portfolio

Banks

Renewable Energy Platform for

Institutional Investors (REPIN)

Equity

provider

Other

sponsors

RE debt

providerInstitutional

Investors

for example:for example: for example:

Pension

funds

Insurers

& Re-

insurer

Other

asset

manager

Issuance of notes from a

portfolio

Securitisation of loan

portfolio(s)

Sets eligibility requirements for

operational projects

Helps sourcing projects/portfolios

Develops eligibility requirements

with investors

Provides quality assurance

Service

provider(s)

Financial

intermediary

Due diligence

Project

risk/rating

Project /loan

monitoring Underwriting of REPIN

(if required)

Structuring/Arranging

Credit enhancement

Credit

enhancement

(if required)

Insurer/ Re-

insurer Insurance

Warranty protection

European Investment Bank Group

Project Bond Credit Enhancement (PBCE)

41

The PBCE instrument:

Ensures debt service for the Project

Bond Investors up to the total size of

the instrument

Provides additional liquidity to avoid

default, and acts as a first-loss debt

piece

Credit enhances project bonds from

a typical BBB- rating by up to 3

notches (to A-)

Can be provided as either a funded

(subordinated loan) or unfunded

(letter of credit) instrument

Once drawn (unfunded), mezzanine

debt repaid by junior cash sweep

Project

Bonds

PBCE up

to 20% of

total

Project

Bond issue

Project

Company

(e.g.

PPP/PFI)

Equity

Project

Bond

Investors

PBCE

European Investment Bank Group

The Greater Gabbard OFTO

42

Project

• Electricity transmission assets connecting the 140 wind

turbines of the 504MW Greater Gabbard offshore wind

farm to the UK onshore grid

• Construction completed

• Concession of 20 years

Financing

(Bond)

• Size: GBP 305.1m, publicly listed, long term, amortising

senior debt with a tenor of 19 years

• Rating: A3 (with the PBCE)

• Pricing: 125bps over benchmark UK Gilt rate or 4.317%

• Bookbuilding: 3x oversubscribed

PBCE

(L/C)

• Size: GBP 45.8m initially (15% of Bond), amortising with

Bond

European Investment Bank Group

PF4EE

43

Private Finance for Energy Efficiency (PF4EE) is a joint instrument of

the EIB Group and the European Commission (EC) to support the

financing of energy efficiency (EE) investments.

PF4EE supports eligible EE investments identified by schemes

developed within EU Member States and is made up of 3 components:

PF4EE Energy Efficiency Loan: an EIB financing with long tenor and

flexible allocation rules

PF4EE Risk Sharing Facility: Up to 80% coverage of credit losses on a

loan by loan basis up to a given amount

PF4EE Expert Support Facility: A technical consultancy services aiming

at supporting EE financing at Financial Intermediary level

European Investment Bank Group

PF4EE - Structure

44

Financial

Intermediary

(FI)

PF4EE RSF

Cash transfers to

cover up to 80%

of losses.

Delegation Agreement

Eligible EE

Investments

Member State

EE Programme

National EE Action Plan and

EU Directives Compliant

Final Recipients

Expert Support Facility

Trustee

Cash deposit

EIB EE Loan

Benefits of PF4EE:

Better financing conditions because lower credit risk profile and adapted refinancing.

Lower security/collateral requirements due to the Risk Sharing Facility.

Global financing solution, if blended with EE grants from Member State EE

programme.

European Investment Bank Group

45

Contacts

Christopher Knowles

Head

Climate Change &

Environment

European Investment Bank

100, boulevard Konrad Adenauer

L-2950 Luxembourg

Martin Berg

Investment Officer

Climate Change &

Environment

For more information please contact:

European Investment Bank Group