final study on poultry catastrophic disease - … their risk management relies on geographic...

TRANSCRIPT

Final Study for the Study on Poultry Catastrophic Disease

Final Study on Poultry Catastrophic Disease

Deliverable 2: Final Study

Order Number: D15PD00012

Submitted to:

USDA-RMA

COTR: Jaime Padget

6501 Beacon Drive

Kansas City, Missouri 64133-6205

Submitted by:

Watts and Associates, Inc.

4331 Hillcrest Road

Billings, Montana59101

Delivery Date: September 30, 2015

This document includes data that shall not be disclosed outside of the Government and shall not be duplicated, used,

or disclosed, in whole or in part, for any purpose. The Government shall have the right to duplicate, use, or disclose

the data to the extent provided in Order No. D15PD00012. All pages of this document are subject to this restriction.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

i

Table of Contents

Section I. Executive Summary ........................................................................................................ 1 Section II. Sector Descriptions ....................................................................................................... 5

II.A. Broiler Sector ..................................................................................................................... 6

II.B. Turkey Sector ................................................................................................................... 12 II.C. Layer Sector ...................................................................................................................... 20 II.D. Game Birds ....................................................................................................................... 31

Section III. Stakeholder Input ....................................................................................................... 34 Section IV. Existing Program Review .......................................................................................... 46

Section V. Data Availability and Applicability Assessment ........................................................ 58

Section VI. Pricing Methodologies Investigations ....................................................................... 69

VI.A. Broiler Sector .................................................................................................................. 69 VI.B. Turkey Sector .................................................................................................................. 70 VI.C. Layer Sector .................................................................................................................... 71 VI.D. Game Bird Sector............................................................................................................ 75

Section VII. Risk Assessments ..................................................................................................... 76 VII.A. Broiler Sector................................................................................................................. 76

VII.B. Turkey Sector................................................................................................................. 82 VII.C. Layer Sector ................................................................................................................... 86 VII.D. Game Bird Sector .......................................................................................................... 91

Section VIII. Research Findings ................................................................................................... 95

Section IX. Summary of Feasibility Assessment ........................................................................ 104

List of Tables

Table 1. Top Broiler Integrators, United States, 2013 .................................................................... 7 Table 2. Economic Indicators–Broiler, United States .................................................................. 10

Table 3. Broiler Production by States, 20141 ................................................................................ 11

Table 4. Top U.S. Turkey Processors in 2014 .............................................................................. 17 Table 5. Geographic Distribution of 2014 Turkey Production in the United States..................... 18

Table 6. Economic Indicators – Turkeys, United States ............................................................... 19 Table 7. 2014 United States Egg Production by State .................................................................. 24

Table 8. Economic Indicators – Layer Segment United States .................................................... 27 Table 9. Top Ten Egg Production Companies: 2013 ................................................................... 28 Table 10. Top Ten States (in order of Value Sold): Number of Farms Reporting Layers

2012 Census of Agriculture .......................................................................................... 29

Table 11. Game Birds Reported in 2012 Census of Agriculture by Inventory............................. 33 Table 12. Important Diseases by Poultry Industry Sector ............................................................ 59 Table 13. Census of Agriculture Poultry Species for which Data are Collected and Reported ... 60 Table 14. Sample Census of Agriculture Arkansas State-level Annual Sales:

Chickens by Operation Size ......................................................................................... 61

Table 15. Sample Census of Agriculture California County-level Single Period Inventory:

December Chukar Inventory ........................................................................................ 61

Table 16. Sample of NASS Reported Condemnation Data: Chicken Condemnations

Due to Diseases in 2014 by Number of Head .............................................................. 62 Table 17. APHIS Report on the Status of OEI Reportable Diseases in the

United States in 2012 ................................................................................................... 64

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

ii

Table 18. NASS Reported Condemnations of Chickens Due to Diseases in 2014 ...................... 65 Table 19. Poultry Diseases with NPIP Protocols for Response .................................................... 65 Table 20. Poultry Diseases Topics Addressed in the 2004 Report of the Committee on

Transmissible Diseases of Poultry and Other Avian Species - USAHA ..................... 66

Table 21. Poultry Diseases Topics Addressed in the 2014 Report of the Committee on

Transmissible Diseases of Poultry and Other Avian Species - USAHA ..................... 66 Table 22. Poultry Yearbook Egg Prices 1955 to 2004 .................................................................. 74 Table 23. Prices Received 1996 to 2014 ....................................................................................... 74 Table 24. Broiler Catastrophic Disease List: Available Vaccinations and

NPIP Protocol Inclusion ............................................................................................... 80

Table 25. Turkey Catastrophic Disease List: Available Vaccinations and

NPIP Protocol Inclusion ............................................................................................... 85 Table 26. Layer Catastrophic Disease List: Available Vaccinations and

NPIP Protocol Inclusion ............................................................................................... 88 Table 27. Waterfowl Catastrophic Disease List: Available Vaccinations and

NPIP Protocol Inclusion ............................................................................................... 92 Table 28. Game Bird Catastrophic Disease List: Available Vaccinations and

NPIP Protocol Inclusion ............................................................................................... 93 Table 29. Ready-to-Cook Poultry - A Quality Summary of Specifications for Standards of

Quality for Individual Carcasses and Parts .................................................................. 97

Table 30. Summary of U.S. Standards for Quality of Individual Shell Eggs ............................... 99

List of Appendices

Appendix A. Poultry Grower Contracts

Appendix B. Stakeholder Input

Exhibit 1. Listening Session Agenda

Exhibit 2. Sample Listening Session Press Release

Appendix C. State Veterinarians

Appendix D. APHIS Stakeholder Registry Reports

List of Attachments

Attachment I. Poultry-Grading Manual

Attachment II. United States Classes, Standards, and Grades for Poultry AMS 70.200 et seq.

Attachment III. Egg-Grading Manual

Attachment IV. United States Standards, Grades, and Weight Classes for Shell Eggs AMS 56

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

1

SECTION I. EXECUTIVE SUMMARY

The Statement of Work (SOW) for Order Number D15PD00012 identifies the objectives of the

project as “…to obtain information and to determine if providing poultry catastrophic disease

coverage would benefit agricultural producers; to help poultry producers and Congress

understand how these risks are being, or could be addressed by the crop insurance system; to

find and evaluate any existing policies or plans of insurance that provide coverage for any and

all poultry catastrophic disease events; and, to determine what practical challenges are present

that need to be overcome in order to create actuarially sound products related to a poultry

catastrophic disease event.”1

The sheer size and complexity of the commercial poultry industry are two of its defining

features. The industry produces meat and eggs from numerous species as well as live birds.

Each of these sectors has different characteristics. For the egg sector, the birds are a capital

resource rather than a crop, although there are some analogies to a wheat plant being the capital

resource that produces the grain crop. Table and breaking eggs are used as a food, while

hatching eggs are used to produce laying hens and meat birds. Game bird hatching eggs are used

to produce game birds for meat as well as live game birds for release. The production cycle for

eggs can last a year or more, while the production cycle for meat and live birds is much shorter.

For broilers, live chicks and poults, a production cycle may be completed in a matter of weeks.

Much of the poultry meat industry is vertically integrated. Integrators typically control feed

production, grow-out, transportation, slaughter, processing, and wholesale distribution and may

control brood egg production and hatching. Production facilities and services are provided by

contracted growers whose compensation depends on meeting objectives such as growth rates,

disease control, feed efficiency, etc. The major sector stakeholders, the integrators, consequently

have remarkable control of their products and vast market power relative to contract growers.

There are many fewer contract growers in the layer sector than in the meat sectors. Nonetheless,

many of the producers in the layer sector are also vertically integrated.

Large integrators generally indicated their preferred risk management for disease does not

involve catastrophic disease loss insurance. Instead, their risk management relies on geographic

isolation of production and strict biosecurity measures required of growers. On the other hand,

the low margins for growers and the limited options for alternative uses of their facilities create a

situation where downtime following a disease event is a major concern. Yet the appropriate

response to a catastrophic disease event is to mandate a longer downtime before introducing a

healthy flock. If a United States Department of Agriculture (USDA) Risk Management Agency

(RMA) policy were to be offered to growers to address their greatest risk management concerns,

changes in the Act would be required to establish indisputably a grower’s insurable interest not

only due to loss of a “crop” but also due to the inability to use their production facilities. While

this is somewhat analogous to prevented planting coverage offered for field and row crops, it

differs in the respect that the period of loss is not a crop year but rather one or more production

cycles. Insurance coverage addressing such an extended period of loss is allowed under

Subsection 508(l)2 for trees including losses due to disease and partial indemnification

1 USDA, RMA, 2014, SOW, Order Number D15PD00012, page 19. 2 Optional Coverage under the Crop Insurance section (7 U.S.C. 1508) of 75-30 - Agricultural Adjustment Act of 1938 &

Federal Crop Insurance Act as amended through P.L. 113–79, Enacted February 7, 2014.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

2

addressing such an extended period of loss for trees is offered under Section 531(f).3

Nonetheless, for contract growers of poultry, the ownership of the crop most often resides with

the integrator and therefore the issue of insurable interest in the foregone productive value of

their facilities remains even if the long-term losses due to destruction of the capital asset can be

addressed.

A small cohort of traditional producers of poultry exists, especially in the layer sector and in

niche markets for meat and live birds. These include producers of “free range” poultry and

poultry raised for ethnic markets. The strongest interest for disease insurance among owners of

poultry is in this group, although here too the most substantial interest was for managing risk due

to the downtime following a disease outbreak.

As this report neared completion, the Contractor identified an offer of insurance for business

interruptions resulting from depopulations due to Highly Pathogenic (HP) Avian Influenza (AI).

This offer appears to be underwritten by an international consortium and is available as a

standard policy and on a surplus line basis. Although the Contractor examined policy materials,

the examination was constrained by a confidentiality agreement. However, the Contractor is

permitted to indicate business interruption coverage is offered following depopulation due to a

government action resulting from a verified HPAI infection. Fixed costs identified in the policy,

as well as continuing expenses and lost profits are indemnifiable until either the end of the

insurance period or the release of the facility for repopulation. Coverage is available for both the

poultry meat and layer sectors.4 The reader should note, the Federal Crop Insurance Act requires

that “no program may be undertaken [by the Federal Crop Insurance Corporation] if insurance

for the specific risk involved is generally available from private companies.”5

Poultry industry data, including estimates derived by the USDA National Agricultural Statistics

Service (NASS) from surveys, are available for the larger sectors of the industry: chickens

(including layers and the eggs they produce), ducks, and turkeys. Production data on other

sectors of the poultry industry are geographically limited, sporadic, and in many cases anecdotal.

The proprietary nature of poultry industry data and contracts has made it particularly difficult to

obtain farm-level data. Such data is important for development of an actuarially-sound crop

insurance product.

Two commercial services provide price data on poultry for a fee. These price data focus on

wholesale and retail markets rather than on farm-level sales. NASS and the USDA Economic

Research Service (ERS) estimate “prices received” values for poultry based on live-weight-

equivalent prices calculated by subtracting processing costs from ready-to-cook wholesale prices

and multiplying that result by the dressing percentage.6

3 Supplemental Agricultural Disaster Assistance section (7 U.S.C. 1508).of 75-30 - Agricultural Adjustment Act of 1938 &

Federal Crop Insurance Act as amended through P.L. 113–79, Enacted February 7, 2014. 4 J.D. Goff, Vice President, National Accounts Underwriting, James Allen Insurance; personal communication, July and August

2015; B. Satterfield, Executive Director, Delmarva Poultry Industry, Inc., personal communication, August 2015. 5 Federal Crop Insurance Act, 7 U.S.C. 1508(l). 6 USDA, ERS, LDPM: Livestock, Dairy, and Poultry Outlook Catalog, http://www.ers.usda.gov/publications/ldpm-livestock,-

dairy,-and-poultry-outlook.aspx, Livestock, Dairy, and Poultry Outlook, June 16, 2015, “U.S. red meat and poultry forecasts”

table, http://usda.mannlib.cornell.edu/usda/current/LDP-M/LDP-M-06-16-2015.pdf, accessed July 2015.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

3

Over the course of 6 on-site and 4 telephone listening sessions, the Contractor gathered feedback

from more than 120 stakeholders. While there were several common themes in the stakeholder

feedback, there were differences in emphasis regionally and by sector. Representatives from

major integrators, the owners of a majority of the birds producing meat, indicated no interest in

catastrophic disease insurance. They noted widespread disease outbreaks have the potential to

increase their profits as prices rise. Even when diseases affect their own production, the size and

internal diversification of the larger integrators limits the potential “catastrophic” impact because

a single affected flock represents a small percentage of the total birds in production. However,

this attitude is not reflected by contract growers. These growers frequently have heavily

leveraged operations and a disease outbreak that results in the loss of even a single production

cycle can cause bankruptcy. While a majority of listening session attendees who spoke

expressed concerns related to diseases, many growers expressed the opinion that most of this risk

could be controlled by proper biosecurity. However, recent losses in the Midwest suggest that

current biosecurity protocols may not be sufficient to avoid losses.

The USDA Animal and Plant Health Inspection Service (APHIS) offers programs providing

indemnities to poultry producers and integrators who incur disease losses resulting from

depopulation. APHIS determines the net present value for commercial birds which have been

“taken” as a part of a disease management program. The APHIS values for meat and live birds

for release are generally based on the price of day-old birds offered by mail order hatcheries plus

an estimated cost of feeding the birds from birth to the age attained at the time of depopulation.

APHIS considers market pricing for marketable birds, the productive potential of layers, and the

value of the intellectual property rights in breeding stock, when appropriate. Consequently,

APHIS valuations are on a one-off basis. Furthermore, the percentage of the value of the taken

poultry paid by APHIS is not always perceived as consistent by the industry. Since the

integrators generally own the birds APHIS indemnities are not always distributed between

integrators and contract growers, although growers have received some share of APHIS

payments for some depopulations.

Private insurance has been offered by the Catlin Group (Bermuda) and Lloyd’s (London) on a

surplus line basis for coverage for all mortality risks of livestock, including disease and down

time. The premiums for such insurance are high. Furthermore, after the recent outbreak of

HPAI, offers for mortality insurance and business interruption with disease listed as an insurable

cause of loss have been withdrawn.

The Contractor considered alternate insurance designs to address widespread disease events in

poultry. None of these alternative designs met all the RMA insurance development feasibility

criteria. The most substantial barriers were imposed by the Crop Insurance Act, RMA’s enabling

legislation. The Crop Insurance Act has been interpreted to preclude provision of insurance for

rent and labor payments to growers because the authority for indemnities is limited to “… losses

of the insured commodity…”7

Due to the sporadic and catastrophic nature of the proposed causes of loss, traditional

quantitative rating approaches would be difficult to implement and most likely rates would need

to be established for broad geographic regions. The biggest potential customers for catastrophic

7 Federal Crop Insurance Act, 7 U.S.C. 1508(a)(1).

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

4

disease insurance, the large integrators, are generally satisfied with their non-insurance risk

management strategies. It is smaller producers who would be most likely to purchase the

insurance. Consequently, the distribution of the insurance liability is unlikely to mirror the

distribution of poultry throughout the country. Underwriting or policy language to address the

short production cycle will be required to avoid adverse selection. While pricing meat birds will

be relatively straight-forward, establishing a value for breeders, layers, and pullets will introduce

complications in establishing the insurance pricing. These confounding factors and the very thin

margins for the on-farm component of the poultry income stream means the cost of insurance

may create opportunities for movement in the supply curve, at least regionally if not nationally.

From RMA’s perspective, there are the fundamental questions regarding the insurability of the

grower’s interest, and non-trivial questions regarding identification, measurement, and tracking

of the value of a livestock “crop.” Moreover, the proprietary and closely guarded nature of

production data makes the prospect for development of meaningful premium rates without a

significant uncertainty load questionable. Furthermore, the existing reinsurance agreements with

Approved Insurance Providers (AIPs) are likely not appropriate, barring meaningful adjustments,

for livestock mortality products. In light of the many issues identified in this study, including the

failure of insurance approaches for the poultry industry to meet some of the RMA criteria of

feasibility, the Contractor believes it is currently not feasible to develop catastrophic disease

insurance for the poultry industry without substantive changes in the current crop insurance

paradigm. Any development effort to address catastrophic disease coverage would have to be

very large in scope and include broad authority to request formal USDA counsel positions

regarding legal authority for coverage so policy language could be appropriately structured;

recommend potential changes to federal reinsurance agreements; utilize potentially alternative

quantitative and qualitative data methods in ratemaking; require unique underwriting standards

based on biosecurity practices; and operate under an indefinite and likely extended timeline to

accommodate structural changes that would be appropriate to support the approval and

implementation of the potential product.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

5

SECTION II. SECTOR DESCRIPTIONS

The Statement of Work (SOW) for Order Number D15PD00012 identifies the objectives of the

project as “…to obtain information and to determine if providing poultry catastrophic disease

coverage would benefit agricultural producers; to help poultry producers and Congress

understand how these risks are being, or could be addressed by the crop insurance system; to

find and evaluate any existing policies or plans of insurance that provide coverage for any and

all poultry catastrophic disease events; and, to determine what practical challenges are present

that need to be overcome in order to create actuarially sound products related to a poultry

catastrophic disease event.”8 This document is the Final Study required by that SOW.

The U.S. commercial poultry industry includes production of more than 15 species of

domesticated fowl and commercial game-birds, production of eggs from these species for

hatching, and production of eggs from a limited number of these species for direct consumption

by humans. Commercial poultry species endemic to the United States and raised for meat

include geese and turkeys, as well as several species of ducks, pheasant and quail.9 Chickens,

emu, guinea hens, ostrich, and additional species of duck, pheasant, and quail were introduced

and are now grown commercially in the United States. Since disease can be transmitted from

wild populations to commercial flocks and susceptibility to disease may be influenced by the

bird’s origins, differences among the species grown commercially, including differences between

endemic and introduced species, may impact the risks to the commercial flocks.

Production of all poultry and eggs comprises approximately $43 billion of the U.S. agricultural

economy.10

The financial impact of the three major commercial poultry sectors (broilers, layers,

and turkeys) collectively in the U.S. agricultural economy is comparable to the financial impact

of soybeans. There is also a large processing added-value component in all poultry sectors. This

increases the impact of the poultry industry on the overall U.S. economy. Furthermore, although

feed costs and costs for transporting feed have led to some concentration of poultry production in

the states producing the feed crops, additional production occurs near population centers. This

bifurcation of production locales has contributed to the geographic balance in the poultry sector

and in the overall U.S. agricultural economy.

To provide clarity, the Contractor defines below the terms poultry producer, grower, and

integrator as they are used in this report.

Poultry Producer: A person owning poultry and growing poultry or eggs for sale into

markets for human consumption.

Grower: A person retained under contract by the owner of poultry or an agent of that

owner to manage the growth of poultry for delivery of mature birds or eggs to the owner.

Integrator: A person who owns poultry being grown for sale into markets for human

consumption as well as associated enterprises to provide inputs, services, or processing of

the eggs or poultry.

8 USDA, RMA, 2014, SOW, Order Number D15PD00012, page 19. 9 Some classification systems include turkeys as members of the pheasant family. 10 USDA, NASS, 2012 Census of Agriculture, Table 2,

http://www.agcensus.usda.gov/Publications/2012/Full_Report/Volume_1,_Chapter_1_US/st99_1_002_002.pdf, accessed April

2015.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

6

Much of the poultry industry is vertically integrated. A small number of very large firms have

“integrated” many elements of production, marketing, and sales. Integrators for poultry meat

production may control feed production, brood egg production, hatching, grow-out,

transportation, slaughter, initial processing (preparation of a marketable whole bird), further

processing to retail products such as lunch meat, and wholesale distribution. Although

integrators play a smaller role in egg production, they may control feed production, layer

hatching and grow-out, transportation, processing, and wholesale distribution. Furthermore, this

same level of integration characterizes many egg producers, including most of the larger

producers. Consequently, the major sector stakeholders have a tremendous amount of control of

their products and vast market power relative to their contract growers. Even relatively small

egg and poultry producers/integrators may own and manage many aspects of their businesses

(e.g., rearing of birds, feeding, housing, husbandry, and marketing of their product) and are

capable of managing many elements of the process.

II.A. Broiler Sector

The term ‘broiler’ is the poultry industry name for a young chicken raised for meat. With the

value of broiler production in 2014 totaling almost $33 billion,11

broilers account for about two

thirds of the farm-level value of production and sales of poultry products in the United States.7,12

The broiler sector is dominated by vertically-integrated agribusiness firms. People in the

industry refer to these firms as either broiler companies or integrators. In the government

literature they are occasionally called “dealers” or “contractors.” In 2013, 15 vertically

integrated firms controlled almost 90 percent of U.S. broiler production (Table 1).13

Consolidation in the industry has resulted in “…significant structural change in recent

decades…the industry has evolved to a structure including vertical integrators that contract with

producers to raise their animals under strict specifications.” Under this integrated structure,

“Vertically integrated companies in a supply chain are united through a common owner. Usually

each member of the supply chain produces a different product or service, and the products

combine to satisfy a common need…”14

To avoid confusion in the discussions in this report, the

Contractor will avoid using the term “producer,” except in those cases where the definition

provided earlier specifically applies, and will generally refer to either integrators or contract

growers.

11 USDA, NASS, 2014, Poultry Production and Value, 2014 Summary,

http://usda.mannlib.cornell.edu/usda/current/PoulProdVa/PoulProdVa-04-30-2015.pdf, accessed November 2014. 12 The Poultry Site, Poultry News, “Value of US Poultry Production Has Doubled in 14 Years”,

http://www.thepoultrysite.com/poultrynews/33264/value-of-us-poultry-production-has-doubled-in-14-years, accessed

December 2014. 13 WATT Poultry USA, 2014, 2013 Top Broiler Producing Companies,

http://www.wattagnet.com/Worldtoppoultry/US_broiler_producers.html, accessed November 2014. 14 National Chicken Council, Vertical Integration, http://www.nationalchickencouncil.org/industry-issues/vertical-integration/,

accessed July 2015.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

7

Table 1. Top Broiler Integrators, United States, 2013 Integrator Percent of Market

Tyson Foods 25.3%

Pilgrim’s Pride 17.5%

Perdue Farms 7.6%

Koch Foods 7.3%

Sanderson Farms 5.3%

Wayne Farms 3.9%

Mountaire Farms 3.8%

Foster Farms 3.4%

George's 3.4%

Peco Farms 2.3%

Keystone Farms 2.2%

Simmons Foods 2.2%

House of Raeford Farms 2.1%

O.K. Foods 1.8%

Fieldale Farms 1.8%

Source: After WATT Poultry USA, 2014, 2013 Top Broiler Producing

Companies, http://www.wattagnet.com/Worldtoppoultry/US_broiler_producers.htm

l, accessed November 2014. The Contractor converted weekly

numbers in that report to annual processed numbers.

II.A.1. The Crop

Modern commercial broilers, typically known as Cornish crosses or Cornish-Rocks, are specially

bred for large-scale, efficient meat production and grow much faster than egg or traditional dual-

purpose breeds. Modern commercial broilers are noted for having very fast growth rates, a high

feed conversion ratio, and low levels of activity. Broilers often reach a harvest weight of four to

five dressed pounds in only eight weeks. Commercial broilers have white feathers and yellowish

skin. These birds also lack the typical “hair”15

characterizing many breeds that requires singeing

after plucking. Both male and female broilers are slaughtered for their meat. The genetic lines

for most broilers produced in the United States are managed by three companies: Aviagen Inc.,

Hubbard LLC (Americas), and Avian Technology Intl LLC.16

These companies also have

substantial international sales of chicks and parent stock (e.g., Aviagen reports sales in 130

countries).

Growers own the broiler houses, provide labor, and generally have the responsibility to manage

biosecurity, house preparations, and litter. The vast majority of broiler production operations are

managed under a contractual structure that dictates both the manner in which the enterprise is

managed and how returns are distributed. The impact of these contracts on grower enterprises is

the central focus of literature regarding risk management in the poultry industry.

At the outset, it is important to clarify that farm-level broiler prices, receipts, and values reported

by various agencies, including NASS, are calculated or estimated values. They are not the

values received by broiler growers which are dictated by the contractual agreement entered into

between the grower and integrator. The published “prices received” values are live-weight-

equivalent prices calculated by subtracting processing costs from ready-to-cook wholesale prices

15 A filoplumes consists primarily of the rachis, the main shaft of a feather. In some breeds filoplumes lie under the contour

(surface) feathers providing support. 16 WattAgNet, 2014, Who’s Who.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

8

and multiplying that result by the dressing percentage. These values are useful only as industry-

wide indicators of the relative price trends. While this report includes these values to a limited

extent, the more important descriptive data are the number of broilers produced, the pounds of

broiler meat produced, the number of broiler houses, and the relative impact of a catastrophic

disease. The revenue growers actually receive is a contracted payment for capital and labor

services rendered. Payment is based on pounds of bird delivered multiplied by the contract

price, which is derived from a two-part, piece-rate tournament scheme, i.e., a base rate plus an

incentive determined by the grower’s performance relative to others in the tournament.

Enterprise Structure

An analysis of broiler operations reported by the ERS in 2014 provides the best snapshot of

broiler production.17

Grower contracts dominate the industry, with only about 0.4 percent of

birds produced by independent poultry producers and 0.3 percent produced on integrator-

operated farms. Few details about the contracts themselves are available. In spite of recent legal

and legislative actions freeing growers to share information about their contracts, and in spite of

repeated requests for redacted copies of contracts from growers, integrators, and crop experts, the

Contractor obtained only two contracts (Appendix A). ERS reports that almost 94 percent of the

contracts contain performance-based payment incentives; however, most of these broiler

contracts have tournament or similar competitor-comparison-based incentive payments. The

contracts obtained by the Contractor contain language providing the grower with performance-

based incentives coupled with tournament-based performance payments. Under the tournament

system, the integrator sets an average price for raising the chickens (e.g., 5 cents per pound live

weight). The growers are ranked. The top-ranking growers can be paid a premium of up to 25

percent. Since the contract price is a tournament average, the poorest performing growers will

receive less than the average. The grower’s ranking is largely based on feed conversion rates:

how much weight the broilers gained compared to how much feed the birds have consumed.

ERS reported that in 2010, less than one fifth of contracts made provisions for catastrophic risk

payments from the integrator to the grower.18

Both of the contracts reviewed by the Contractor

have catastrophic risk payment clauses. Based on the underlying cause of the loss, the integrator

provided some compensation to the grower in the event of a catastrophic event. It should be

noted, one contract obtained by the Contractor did include compensation for losses due to

uncontrollable disease.

The turnover in farms producing broilers is relatively low. About one third of all broiler

operations have been in business for at least 20 years. These older operations tend to be smaller

and to have lower levels of technology. Only 4.5 percent of farms (6.6 percent of production by

weight) produced broilers for 5 years or less. These newer operations have houses that are 11

years old on average. This suggests many new growers are operating on farms that had

previously been operated by others or that economic restructuring of older operations resulted in

their listing as having been in operation for 5 years or less. Just under half of the new operations

had new houses. Newer operations tend to incorporate a larger number of houses. New

17 MacDonald, J.M., USDA, ERS, 2014, Technology, Organization, and Financial Performance in U.S. Broiler Production,

Economic Information Bulletin No. 126. http://www.ers.usda.gov/media/1487788/eib126.pdf, accessed December 2014. 18 Ibid.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

9

operations with new houses also tend to carry a higher debt load compared to new operations

using older houses.19

Since newer operations tend to be larger, they also tend to have more substantial investment in

housing and technology. These newer operations are more reliant on income from the poultry

operations rather than from a range of “crops” and more sensitive to changes in energy price and

contract settlement terms. New large operations typically receive longer term contracts.20

Furthermore, in at least one of the contracts reviewed by the Contractor, the integrator offered a

minimum guaranteed payment for new house construction based on dollars per 1,000 birds

placed and the type of the new construction.

Though commercial broiler farms have seen a modest increase in average size since the 2010

poultry report, the “contract poultry growers are relatively small and specialized farms.”21

From

a production perspective, the Southeast and Mid-South offer comparative advantages of climate,

land prices, cost of implementing required environmental policies, and lack of alternative uses

for the land. Poultry is susceptible to extreme weather conditions and requires access to ample

supplies of water for maintenance and growth. Consequently, poultry can be raised less

expensively in warmer climates in regions where ample water is available.

Growers with no debt have a cash flow cushion to withstand market risks due to variability in the

number of flocks in a contract for a given year. Conversely, both net incomes and cash flows of

growers with substantial debt are more susceptible to problems due to flock inventory variations.

II.A.2. The Industry

While the agricultural segment of the U.S. economy has grown slightly on a relative percentage

basis from 1999 to 2014, the broiler sector share of the total U.S. agricultural economy declined

from 8.04 percent to 8.02 percent (Table 2). This decline occurred in spite of increases in

production, consumption, and exports of meat from broiler chickens.

19 Ibid. 20 Ibid. 21 Ibid.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

10

Table 2. Economic Indicators–Broiler, United States Year Gross Domestic Product

1 Agricultural Cash Receipts

2 Value of Broilers

3

1999 9,660.60 187,814,689 15.1

2000 10,284.80 192,097,825 14

2001 10,621.80 200,026,456 16.7

2002 10,977.50 194,588,257 13.4

2003 11,510.70 215,971,148 15.2

2004 12,274.90 237,853,261 20.4

2005 13,093.70 240,897,821 20.9

2006 13,855.90 240,623,888 17.7

2007 14,477.60 288,545,936 21.5

2008 14,718.60 316,093,638 23.2

2009 14,418.70 291,376,034 21.8

2010 14,964.40 322,174,469 23.7

2011 15,517.90 368,667,940 23

2012 16,163.20 404,823,995 24.8

2013 16,768.10 401,313,896 30.8

2014 17,418.90 407,392,615 32.7

Source: 1 Bureau of Economic Analysis, 2015, National Income and Product Accounts Table 1.1.5, Gross Domestic Product,

http://www.bea.gov/iTable/iTable.cfm?ReqID=9&step=1#reqid=9&step=1&isuri=1, accessed July 2015. 2 In Nominal dollars, USDA, ERS, 2015, Farm and Income Wealth Statistics, Annual cash receipts by commodity,

http://www.ers.usda.gov/data-products/farm-income-and-wealth-statistics/cash-receipts-by-commodity.aspx#.VFutk_nF9qW, accessed July 2015.

3 USDA, ERS, 2015, Poultry Production and Value,

http://usda.mannlib.cornell.edu/MannUsda/viewDocumentInfo.do?documentID=1130, accessed July 2015.

The southern and mid-Atlantic states form the major broiler producing areas of the United States

(Table 3). Although number of head, pounds produced, and value all track relatively closely,

variations in the harvest weight of birds lead to modest differences between percent of head

produced and of pounds produced. The ERS estimated value produced is based on a constant

price.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

11

Table 3. Broiler Production by States, 20141

State

Number

Produced

(1,000 head)

Percent of

Number

Head

Produced

Pounds Produced

(1,000 pounds)

Value of

Production2 (1,000

dollars)

Percent of

Pounds/Value

Produced

Georgia 1,324,200 15.50 7,547,900 4,808,012 14.69

Alabama 1,061,500 12.42 6,050,600 3,854,232 11.78

Arkansas 969,800 11.35 6,012,800 3,830,154 11.70

North Carolina 795,200 9.31 6,043,500 3,849,710 11.76

Mississippi 727,200 8.51 4,508,600 2,871,978 8.78

Texas 591,800 6.93 3,550,800 2,261,860 6.91

Kentucky 308,000 3.60 1,724,800 1,098,698 3.36

Missouri 288,500 3.38 1,384,800 882,118 2.70

Maryland 287,800 3.37 1,554,100 989,962 3.03

Virginia 262,000 3.07 1,441,000 917,917 2.80

Delaware 244,100 2.86 1,733,100 1,103,985 3.37

South Carolina 232,500 2.72 1,650,800 1,051,560 3.21

Oklahoma 205,300 2.40 1,334,500 850,077 2.60

Pennsylvania 181,300 2.12 997,200 635,216 1.94

Tennessee 180,600 2.11 939,100 598,207 1.83

West Virginia 95,300 1.12 371,700 236,773 0.72

Ohio 75,600 0.88 430,900 274,483 0.84

Florida 66,700 0.78 386,900 246,455 0.75

Wisconsin 53,400 0.62 224,300 142,879 0.44

Minnesota 46,800 0.55 280,800 178,870 0.55

Other States3 546,500 6.40 3,204,900 2,041,521 6.24

United States Total 8,544,100

51,373,100 32,724,667

1 Broiler production including other domestic meat-type strains. 2 Live weight equivalent price, derived from ready-to-cook prices minus processing costs, then multiplied by a dressing percentage. 3 California, Illinois, Indiana, Iowa, Louisiana, Michigan, Nebraska, New York, Oregon, and Washington combined to avoid disclosing

individual operations.

Source: USDA, ERS. April 2015, Poultry - Production and Value 2014 Summary,

http://usda.mannlib.cornell.edu/usda/current/PoulProdVa/PoulProdVa-04-30-2015.pdf, accessed July 2015

Nationally, broiler production decreased 5.5 percent from 2008 to 2014, from 9.01 billion birds

in 2008 to 8.54 billion birds in 2014. Over the same time, weight per bird increased by 7.5

percent, from 5.594 pounds to 6.013 pounds. The combined decrease in bird numbers and

increase in bird weight resulted in a 1.98 percent increase in total weight produced, from 50.4

billion pounds in 2008 to 51.4 billion pounds in 2014. The average weight per bird by

geographic area masks bi-modal production pattern resulting from two genetic body weight

groupings. Lighter birds are grown for the whole bird and parts markets and heavier birds are

grown for the breast market (with the remaining meat from the heavy birds going into processed

products and export markets). There are some differences in price per pound for these two

“types.”

Alabama, Arkansas, and Georgia accounted for fewer than 40 percent of the production in 2014

when two of these states (Georgia and Alabama) produced more than 1 billion birds.

Mississippi, North Carolina, and Texas comprise a second production tier, with harvests over

half a billion. Some states, primarily in the northeast and mountain states, reported little or no

commercial broiler production in 2014.22

22 USDA, NASS, 2015, Broiler Production by State Million Head, 2014,

http://www.nass.usda.gov/Charts_and_Maps/Poultry/brlmap.asp, accessed July 2015.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

12

Despite substantial research, the Contractor was unable to identify national data other than the

USDA NASS Census of Agriculture (Census) data at the county level for broilers. NASS annual

statistics do not include number of growers or county-level statistics in estimates derived from its

annual surveys. There are fragmented data available from a few state and county agencies and

industry associations. Farm-level data have not been obtained despite requests of people who

attended the listening sessions. Integrators, who have the most complete farm-level records for

substantial grower populations, consider all their data proprietary.

The 2012 Census reported 32,935 farms with “Broiler and other meat-type chickens sold,” a 21.5

percent increase over the 2007 reported 27,091 farms. NASS reported that 15,334 growers

produced more than 100,000 birds in 2012, and 41 percent of those growers produced more than

500,000 birds. A total of 7,183 farms were located in the 3 states ranked highest in broiler

production, and 42 percent of farms with reported sales over 100,000 birds were located in the

same 3 states. Commercial broiler production is organized and operated around broiler houses,

the major farm-level capital investment. No consistent national dataset that reported the number

of houses or houses per farm was identified.

Under the integrator/grower contract structure, the broiler enterprise might seem a safe haven for

the grower. However, this is not the case; growers must be concerned about performance of the

birds they are raising under contract. Broiler production is influenced by disease, weather,

equipment, building environment, and the quality of feed provided by the integrator. Also,

growers are not free from domestic and international market outcomes, even with a contracted

payment. The potential of subsequent contracts, and, to a lesser extent, the payment and

incentive provisions of the production contracts depend upon the integrator’s inventory of

processed meat and short- and intermediate-run market forecasts.

II.B. Turkey Sector

The United States is the world’s largest producer of turkeys. U.S. turkey production reached 7.5

billion pounds in 2012, with a total estimated farm-gate value of almost $5.5 billion. In 2013

these production numbers fell slightly to 7.2 billion pounds and $4.8 billion.23

While most

turkey produced in the United States is consumed domestically, the United States exports more

turkeys and turkey products than any other country. Brazil, with the second largest production,

harvested 1.1 billion pounds of turkey and Canada harvested 319 million pounds in 2013, while

the European Union-27 collectively produced 4.2 billion pounds.24

The average estimated price

received by U.S. turkey producers during 2013 was almost 67 cents per live-weight pound.25

In 2012, the United States exported almost 798 million pounds of turkey and turkey products (up

14 percent from 2011), valued at $678.9 million (up 13 percent). The majority of exported

turkey products are lower value parts (drumsticks, feet, wings, gizzards, livers, and hearts) and

ground or mechanically deboned meat. In 2012, Mexico was the biggest market for U.S. turkey,

23 USDA, RMA, 2014, Poultry - Production and Value, 2013 Summary,

http://usda.mannlib.cornell.edu/usda/current/PoulProdVa/PoulProdVa-04-29-2014.pdf, accessed December 2014. 24 After The Poultry Site, Global Poultry Trends 2013: US Produces Half the World’s Turkey Meat,

http://www.thepoultrysite.com/articles/3177/global-poultry-trends-2013-us-produces-half-the-worlds-turkey-meat, accessed

December 2014. 25 USDA, RMA, 2014, Poultry - Production and Value, 2013 Summary,

http://usda.mannlib.cornell.edu/usda/current/PoulProdVa/PoulProdVa-04-29-2014.pdf, accessed December 2014.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

13

accounting for over half of U.S. exports. The same year China imported more than $70.5 million

worth of turkey meat and both Canada and Hong Kong continued to import large amounts of

meat from the U.S. turkey industry.26

Many importers of U.S. production use turkey meat with

other meats to produce sausage. Competition from exporters of turkeys and turkey products,

particularly from Brazil, is likely to slow the growth of U.S. turkey exports.

U.S. per capita consumption of turkey has increased from 0.8 pounds in 191027

to 16.0 pounds in

2013.28

This reflects the evolution from a seasonal market (between Thanksgiving and New

Year’s Day) for a single-turkey product (whole birds), to a year-round, diversified, value-added

product line. Nonetheless, the whole turkey continues to be the most popular turkey product,

although its sale is no longer associated solely with the holiday season. The structure of the

turkey sector, with a wide variety of processed products, has changed turkey production into a

year round activity.

The average retail price for whole frozen turkeys in the United States in 2013 was $1.65 per

pound.29

Many processed turkey products have a substantial value-added component. A review

of internet grocery store prices shows some of these products retail at prices in excess of $9.00

per pound. Smoked and roasted turkey lunchmeats; ground breast meat; pre-roasted and ready-

to-roast turkey rolls; heat-and-eat turkey dinners; and turkey sausage, hot dogs, “bacon,”

“pastrami,” and “ham” illustrate the breadth of turkey products currently available. These

products have a substantial impact on total integrator revenues, but have limited effects on prices

received by growers.

II.B.1. The Crop

Turkeys are large birds in the order Galliformes, genus Meleagris. In the United States, turkeys

are raised only for meat (i.e., not for table eggs). Turkey meat is relatively lean when compared

to the meat of other domestic poultry species. The domesticated turkey is a descendant of the

wild turkey, Meleagris gallopavo. The dominant commercial breed of turkeys in the United

States is the Broad-breasted White (similar to “White Holland,” but a distinct breed). Most

commercial breeds have been selected for size as well as meat types and distribution. Since

2009 U.S. producers have raised over 250 million turkeys annually; even with the declining

number of turkeys raised, the average weight in 2013 (30.3 pounds) has enabled the total

production in pounds to remain relatively constant since 2008. That year the average weight was

29.0 pounds.30

Heritage breeds more closely resemble their wild ancestors and can breed naturally.31

Heritage

turkey breeds include Beltsville Small White, Black Spanish, Bourbon Red, Chocolate, Jersey

26 Marsh Laux, Agriculture Marketing Resource Center, Turkey Profile,

http://www.agmrc.org/commodities__products/livestock/poultry/turkey-profile/, accessed December 2014. 27 Ibid. 28 National Chicken Council, Per Capita Consumption of Poultry and Livestock, 1965 to Estimated 2014, in Pounds,

http://www.nationalchickencouncil.org/about-the-industry/statistics/per-capita-consumption-of-poultry-and-livestock-1965-to-

estimated-2012-in-pounds/, accessed December 2014. 29 USDA Economic Research Service Turkey Sector: Background & Statistics, http://www.ers.usda.gov/topics/in-the-

news/turkey-sector-background-statistics.aspx, accessed December 2014. 30 USDA, NASS, April 2014, Turkey Industry Overview,

http://www.nass.usda.gov/Publications/Highlights/2013_Turkey_Industry/, accessed December 2014. 31 The Broad-breasted White are propagated by artificial insemination.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

14

Buff, Lavender/Lilac, Narragansett, Royal Palm, Slate, Standard Bronze, White Holland, and

White Midget.32

These niche market birds command less than one percent of the U.S. market.33

While these breeds were originally selected for flavor and productivity (i.e., conversion of feed

to meat), they require more time to reach maturity than does the Broad-breasted White and are

less amenable to production in houses.

As with many Galliform species, the turkey hen (female) is smaller than the tom (male). Both

hens and toms are raised commercially. Hens are more likely to be marketed as whole birds. A

higher percentage of toms are processed into turkey products, such as lunchmeats, or sold to

restaurants and food services. Parts from both hens and toms may be diverted to export markets.

Mature Broad-breasted White toms are so large they are not able to fertilize hens naturally.

Consequently, semen is collected from toms and hens are inseminated artificially. Many hens

can be inseminated from each collection, so fewer breeding toms than hens are required. The

meat from culled breeders is used primarily in processed meat products.

In commercial production, turkey brood farms supply eggs to hatcheries, which may hatch eggs

from other species as well. After approximately 28 days, the hatched turkey poults are sexed,

boxed, and shipped to the grow-out facilities (a collection of turkey “houses”). At these

facilities, hens are raised separately from toms due to their different growth rates. Rations for

both sexes and all age cohorts generally include corn meal and soybean meal with added

vitamins and minerals. The feed mix is amended to achieve protein, carbohydrate, and fat levels

appropriate for the age cohort.

Most turkey grow-out facilities raise 50,000 to 75,000 birds with an average of 3.5 “turns” per

year (175,000 to more than 260,000 birds a year). Many of the larger facilities have a single

structure (the brood house) with the capacity to house as many as 100 thousand poults. Poults

are raised with an average density of one square foot per bird. Each of these brood houses

generally serves two grow-out houses. Consequently, 7 broods can be raised in a year to produce

the livestock for 3.5 grow-out production cycles per year in each of the grow-out houses. On

larger farms, multiple houses may be stocked, although normally all the birds on the farm are the

same age. This stocking approach helps to prevent diseases being passed among birds in

different age cohorts.

The majority of U.S. turkeys are grown in controlled-environment confinement houses or in pole

barns. The windowless confinement houses use modern systems of environmental control

(heating, ventilation, and lighting). Ventilation systems provide sufficient oxygen for the normal

growth and development and remove ammonia, carbon dioxide, dust, moisture, and heat.

Confinement houses may contain as many as 50,000 birds. Depending on the degree of

automation of the environmental control, feeding, and drinking systems, a single employee may

provide all the necessary labor for a confinement house.

32 Heritage Turkey Foundation, 2014, What is a Heritage Turkey, http://heritageturkeyfoundation.org/, accessed April 2015, and

American Livestock Breeds Conservancy, 2014, Breed Information – ALBC Conservation Priority List,

http://www.livestockconservancy.org/index.php/heritage/internal/conservation-priority-list#Turkeys, accessed April 2015. 33 Grace Communications Foundation, Talking Turkey, http://www.sustainabletable.org/432/talking-turkey, accessed April 2015.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

15

Environmental control within pole barns is more rudimentary. Consequently, labor requirements

are greater and stocking densities are lower. Turkey poults reared in pole barns are generally

raised in environmentally-controlled houses to 5 or 6 weeks of age. In the pole barns, the birds

are raised in natural light, supplemented during the winter months with electric light. In the

North, there is often limited control of temperature or ventilation in pole barns. The floor area of

turkey pole barns ranges from 10,000 to more than 20,000 square feet. Automated feeders and

watering systems maximize production, although the cost of such systems may limit their use.

Turkeys in the pole barns are raised on litter (wood shavings) and allowed to move freely within

the barn.

After removal of a flock, a two- to four-week period is allowed before a new flock is placed in

turkey brood and grow-out houses. During this time, the house is cleaned and disinfected. Old

litter is generally replaced after a flock is removed from turkey brood houses; however, wastes

may be removed from turkey grow-out houses just once each year. The decision on the timing of

cleaning of the grow-out houses is driven largely by the cost of labor and bedding. However,

following a disease outbreak, more extensive cleaning is required.

In most commercial operations, stocking densities in brood houses are set initially to maximize

production, and only change as a result of “normal” mortality until harvest. Hens in grow-out

houses are raised at a density of one per 2.5 square feet. Turkey hens consume about 40 pounds

of feed in their lifetime with a feed conversion rate (pounds of feed per pound of weight gain) of

about 2.5. Ten percent mortality during brooding and grow-out is assumed for planning the size

of the houses and the initial population. For harvest, the hens are collected in “modules” or

small cages, which are generally loaded onto flatbed trailers. Some additional mortality occurs

during transportation. Those losses are generally not considered when an integrator evaluates a

grower’s rank. However, the long-term trends of such losses may impact an integrator’s

decisions about levels of restocking. Slaughter and processing are mechanized to minimize

processing time.

Toms are raised at a density of 3 to 4 square feet per bird in the grow-out houses. Stocking

densities in contract grower operations are generally based on the recommendations of the

integrator. Toms consume about 90 pounds of feed during their lifetime with a feed conversion

rate of about 2.9. Commercial toms, which are more aggressive than hens, have a higher

mortality than the hens. Injurious pecking behavior can be a problem in enclosed confinement

houses. This behavior is usually controlled by reducing the light levels or by beak-trimming.

Some growers provide vegetable material or small objects for the turkeys to maneuver to distract

the birds from their aggressive behaviors. Toms are harvested at about 18 weeks (i.e., slightly

less than 3 production cycles each year). Some contract growers and producers reduce the

density of older toms by moving a portion of the birds into houses vacated by the hens when they

are harvested. This may reduce mortality marginally as the large birds compete for space and

feed. The harvest process for toms is essentially the same as that for hens.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

16

Free-range birds represent a small niche market in the turkey sector. The only requirement for

labeling with the term ‘free-range’ is the birds have access to the outdoors.34

Housing for free-

range birds is usually of the pole barn type. Natural daylight and green food may be available on

the range, but some source of food is generally provided in the barn. Slower growing strains,

low nutrient density feed, low stocking density, and longer production cycles characterize this

minor sector of the crop.

A typical turkey facility (a group of brood and grow-out houses with supporting storage) costs

well over $1 million. A typical facility will have one or two brooder houses and four to six

grow-out houses. Most individual houses are larger than 25,000 square feet. Depending on the

location, the house may have supplemental lighting, heat, ventilation, and automated feed and

watering systems. Most new turkey operations are funded with borrowed money. Loans from

an integrator are often based on a six or seven year payback. Typically, bank loans for a facility

have a longer term. In either case, the loan structures assume year round production.

Contract growers furnish the land, facilities, and labor under contract. They are paid based on

the grade, live weight, and feed conversion ratios of the birds delivered to the processing plant.

Each integrator contract is reported to be unique; and contracts between an integrator and

individual contract growers may also be quite different, taking into consideration such things as

the physical services available at a facility, mortality experience, and historic and current feed

conversion ratios. If the grower realizes a return of $7 to $8 per bird, the facility described as

“typical” may generate a cash flow of $1.25 million to $2.5 million per year. Cost of production

is more difficult to assess under the current integrator/contract grower industry structure. In

many cases, the integrator owns the turkeys, supplies feed, medicine, vaccines, and pays a grow-

out supervisor. The grow-out supervisor monitors the turkeys’ health and growth and decides

when veterinary attention, primarily medications or vaccinations, are required.

During the course of this project, the Contractor spoke with representatives of several operations

that fit neither the typical contract grower nor the typical producer paradigm. These operations

own the turkeys produced under a contract with an integrator and bear all the associated financial

risks in regard to losses from disease, price fluctuations, and poor weight gain. Twelve of the

fifteen members of the Minnesota Turkey Association Board of Directors fall into this unique

category.

II.B.2. The Industry

The U.S. turkey sector is dominated by vertically integrated agribusiness firms. In the second

half of the 20th

Century, after a period of decline in the sector, turkey hatcheries began providing

financing for the purchase of poults, while feed companies provided financing for both feed and

poults as a means to stimulate feed sales. These financial arrangements eventually evolved into

production contracts that shifted risk from grower to integrator. Under contract, the grower

provides the buildings, equipment, and labor; the integrator, who is usually involved in a variety

of post-harvest processing activities, provides poults, feed, veterinary services, and managerial

assistance. Most growers receive a fee per bird or per pound and contracts may provide

34 USDA, Food Safety and Inspection Service, 2014, Food Labeling: Meat and poultry Labeling Terms,

http://www.fsis.usda.gov/wps/portal/fsis/topics/food-safety-education/get-answers/food-safety-fact-sheets/food-labeling/meat-

and-poultry-labeling-terms/meat-and-poultry-labeling-terms, accessed April 2015.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

17

performance incentives for feed conversion and reduced mortality rates. Most, but not all,

integrators produce both whole bodied and further processed turkey products. The major turkey

integrators and their associated production for 2014 are documented in Table 4.

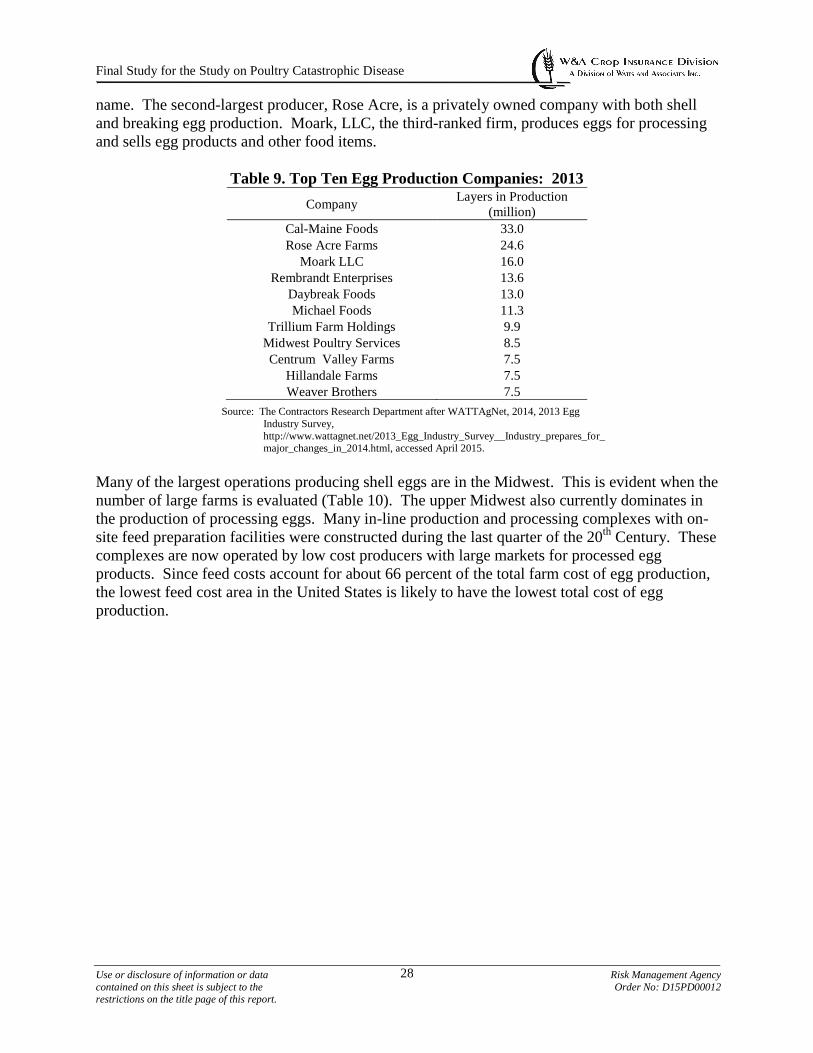

Table 4. Top U.S. Turkey Processors in 2014

Processor Live Weight Processed

(million pounds)

Butterball, LLC 1,300.0

Jennie-O Turkey Store 1,250.0

Cargill Value Added Meats 1,071.0

Farbest Foods, Inc. 411.0

Hillshire Brands Company (formerly Sara Lee) 402.0

Kraft Foods, Inc. (Oscar Mayer) 280.0

Perdue Farms, Inc. 277.0

Foster Farms 270.7

Virginia Poultry Growers Coop. 239.0

West Liberty Foods 216.3

Cooper Farms 205.0

Michigan Turkey Producers 190.0

Dakota Provisions 179.0

Hain Pure Protein Corp. 172.0

Turkey Valley Farms 145.0

Prestage Foods 140.0

Norbest, Inc. (Western Sales LLC) 82.0

Zacky Farms, LLC 68.3

Northern Pride Inc. 40.0

Whitewater Processing 30.0

Empire Kosher Poultry, Inc 25.2

Koch's Turkey Farm 15.2

Jaindl Turkey Sales, Inc 11.0

Source: The Contractor’s Research Department after Watt Poultry USA, 2014.

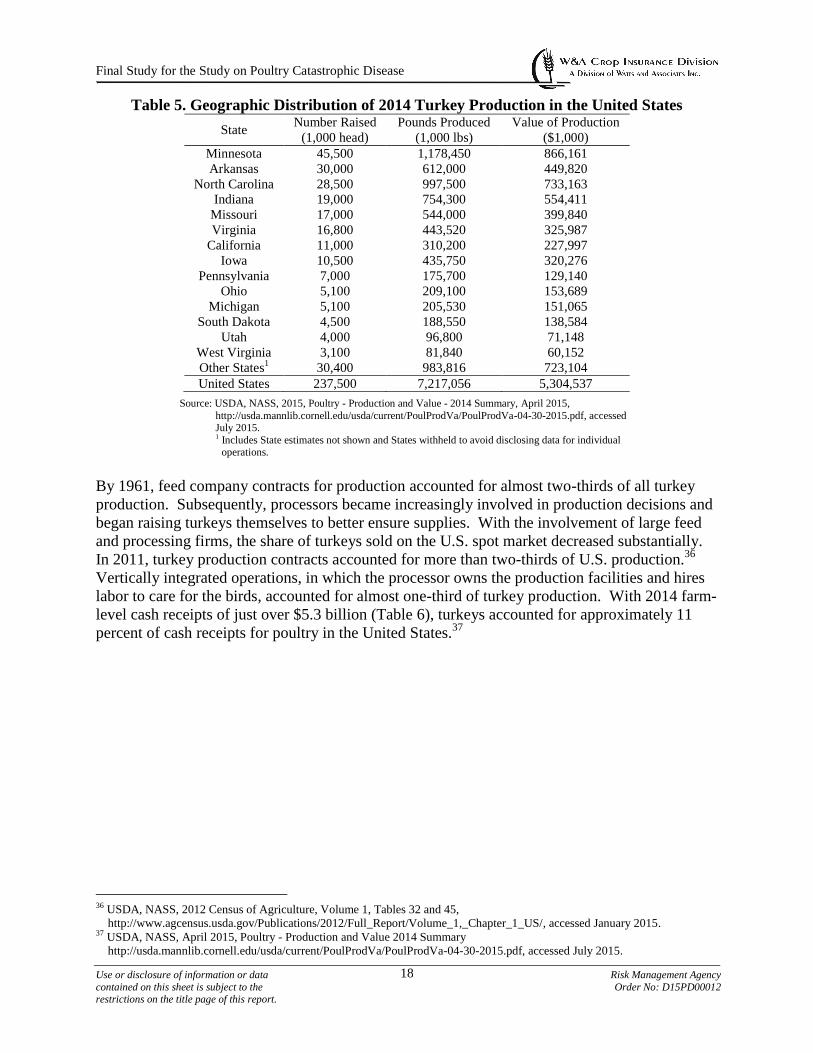

Turkey production is scattered throughout the United States. However, over half of all the

turkeys raised for slaughter in the United States in 2014 were raised in four states: Minnesota,

Arkansas, North Carolina, and Indiana (Table 5). While U.S. consumers eat more turkey per

capita and as a population than any other national consumer population, the U.S. turkey industry

is also more reliant on exports than most U.S. agricultural sectors. In the last decade, the peak

year for turkey production in the United States was 2008. Since that year, the number of turkeys

produced in the United States has declined from a high of 273 million to just 238 million in

2014. According to NASS, turkey production in 2014 was 7.2 billion pounds with a total farm-

level value of just over $5.3 billion. The market year average price per pound in 2013 was 67

cents per pound.35

35 USDA, NASS, 2014, Highlights, Turkey Industry Overview,

http://www.nass.usda.gov/Publications/Highlights/2013_Turkey_Industry/, accessed December 2014; USDA, NASS, 2015,

Quick Stats, http://quickstats.nass.usda.gov/results/5487DA7B-D988-3DF0-8884-2E407CE067F6, accessed June 2015.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

18

Table 5. Geographic Distribution of 2014 Turkey Production in the United States

State Number Raised

(1,000 head)

Pounds Produced

(1,000 lbs)

Value of Production

($1,000)

Minnesota 45,500 1,178,450 866,161

Arkansas 30,000 612,000 449,820

North Carolina 28,500 997,500 733,163

Indiana 19,000 754,300 554,411

Missouri 17,000 544,000 399,840

Virginia 16,800 443,520 325,987

California 11,000 310,200 227,997

Iowa 10,500 435,750 320,276

Pennsylvania 7,000 175,700 129,140

Ohio 5,100 209,100 153,689

Michigan 5,100 205,530 151,065

South Dakota 4,500 188,550 138,584

Utah 4,000 96,800 71,148

West Virginia 3,100 81,840 60,152

Other States1 30,400 983,816 723,104

United States 237,500 7,217,056 5,304,537

Source: USDA, NASS, 2015, Poultry - Production and Value - 2014 Summary, April 2015,

http://usda.mannlib.cornell.edu/usda/current/PoulProdVa/PoulProdVa-04-30-2015.pdf, accessed July 2015. 1 Includes State estimates not shown and States withheld to avoid disclosing data for individual

operations.

By 1961, feed company contracts for production accounted for almost two-thirds of all turkey

production. Subsequently, processors became increasingly involved in production decisions and

began raising turkeys themselves to better ensure supplies. With the involvement of large feed

and processing firms, the share of turkeys sold on the U.S. spot market decreased substantially.

In 2011, turkey production contracts accounted for more than two-thirds of U.S. production.36

Vertically integrated operations, in which the processor owns the production facilities and hires

labor to care for the birds, accounted for almost one-third of turkey production. With 2014 farm-

level cash receipts of just over $5.3 billion (Table 6), turkeys accounted for approximately 11

percent of cash receipts for poultry in the United States.37

36 USDA, NASS, 2012 Census of Agriculture, Volume 1, Tables 32 and 45,

http://www.agcensus.usda.gov/Publications/2012/Full_Report/Volume_1,_Chapter_1_US/, accessed January 2015. 37 USDA, NASS, April 2015, Poultry - Production and Value 2014 Summary

http://usda.mannlib.cornell.edu/usda/current/PoulProdVa/PoulProdVa-04-30-2015.pdf, accessed July 2015.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

19

Table 6. Economic Indicators – Turkeys, United States Year Gross Domestic Product

1 Agricultural Cash Receipts

2 Value of Turkeys

3

1999 9,660.60 187,814,689 2.8

2000 10,284.80 192,097,825 2.8

2001 10,621.80 200,026,456 2.8

2002 10,977.50 194,588,257 2.7

2003 11,510.70 215,971,148 2.7

2004 12,274.90 237,853,261 3.1

2005 13,093.70 240,897,821 3.2

2006 13,855.90 240,623,888 3.6

2007 14,477.60 288,545,936 4.0

2008 14,718.60 316,093,638 4.5

2009 14,418.70 291,376,034 3.6

2010 14,964.40 322,174,469 4.4

2011 15,517.90 368,667,940 4.9

2012 16,163.20 404,823,995 5.4

2013 16,768.10 401,313,896 4.8

2014 17,418.90 407,392,615 5.3

Source: 1/ Bureau of Economic Analysis, 2015, National Income and Product Accounts Table 1.1.5, Gross Domestic Product,

http://www.bea.gov/iTable/iTable.cfm?ReqID=9&step=1#reqid=9&step=1&isuri=1, accessed July 2015.

2/ In Nominal dollars, USDA, ERS, 2015, Farm and Income Wealth Statistics, Annual cash receipts by commodity,

http://www.ers.usda.gov/data-products/farm-income-and-wealth-statistics/cash-receipts-by-commodity.aspx#.VFutk_nF9qW, accessed July 2015.

3/ USDA, ERS, 2015, Poultry Production and Value,

http://usda.mannlib.cornell.edu/MannUsda/viewDocumentInfo.do?documentID=1130, accessed July 2015.

On farms either owned by the integrators or managed under grower contracts, the integrator

generally provides the stock, feed, veterinary services, production technical support, and

transportation. The grower provides the growing facilities and day-to-day care and management

of the birds. The impact of production contracts on turkey enterprises are not as well

documented as are the impacts of production contracts on broiler enterprises.

The relative importance of direct production in the turkey sector to the U.S. agricultural and

overall economies is approximately one-fifth that of the broiler sector (see for example, Tables 3

and 5). However, it should be noted there are considerably more value-added processing

activities in the turkey sector than in the broiler sector. This amplifies the financial effects of

turkey production in the general economy.

Substantial research by the Contractor identified the NASS Census as the only source of national

turkey data at the county level. The 2012 Census documents some limited commercial turkey

production in every state.38

NASS annual statistics do not include number of growers or county-

level statistics in its annual surveys because there are insufficient numbers of growers in most

counties to allow reporting of results under the disclosure rules followed by NASS. There are

fragmentary data available from a few state and county agencies and industry associations.

These data do not provide the comprehensive and consistent descriptions available for other

enterprises.

38 USDA, RMA, Census of Agriculture, 2012 Census Volume 1, Chapter 2: State Level Data, Table 19,

http://www.agcensus.usda.gov/Publications/2012/Full_Report/Volume_1,_Chapter_2_US_State_Level/st99_2_019_019.pdf,

accessed January 2015.

Final Study for the Study on Poultry Catastrophic Disease

Use or disclosure of information or data Risk Management Agency

contained on this sheet is subject to the Order No: D15PD00012 restrictions on the title page of this report.

20

Commercial turkey production is organized and operated around turkey houses, the major farm-

level capital investment. No dataset documenting the total number of houses by county or

houses per farm was identified. The 2012 Census reported 19,956 farms growing turkeys, a 15.8

percent increase over the 17,226 farms reported in the 2007 Census. NASS reported 833

growers produced more than 100,000 birds in 2012.39

Of the 19,956 operations, 1,903 grew

turkeys under contract, producing slightly more than two-thirds of the turkeys reported to have

been sold.40

The turkey sector has evolved to fewer than 25 highly specialized, vertically integrated

agribusiness firms. Under the grower/integrator structure, the turkey contract growers must be

concerned about performance of the contracted birds. Turkey production is influenced by

disease, weather, equipment, building environment, and the quality of feed. Also, growers are

not free from the effects of domestic and international market changes, even with a contracted