final results 2015 - jkx – home/media/files/j/jkx/download-centre/...novo-nikolaevskoye complex -...

TRANSCRIPT

Final results 2015 A fresh perspective – 21 March 2016

2

Disclaimer

This presentation contains certain forward-looking statements that are subject to the usual riskfactors and uncertainties associated with the oil and gas exploration and production business.

Whilst JKX believes the expectations reflected herein to be reasonable in light of the informationavailable to them at this time, the actual outcome may be materially different owing to factors beyondthe Group’s control or within the Group’s control where, for example, the Group decides on a changeof plan or strategy.

The Group undertakes no obligation to revise any such forward-looking statements to reflect anychanges in the Group’s expectations or any change in circumstances, events or the Group’s plansand strategy. Accordingly no reliance may be placed on the figures contained in such forward lookingstatements

Agenda

3

Summary

Financial review

Operations review

Our markets

Outlook

Focus on cash conservation to meet financial obligations

Bond repayment of $5.7m and $12.3m made in February 2015 and 2016 respectively

Average production of 8,996 boepd (2014: 9,919 boepd)

Development drilling suspended in Ukraine due to negative investment climate

Repair of well-27 in Russia completed Six mining plots (production licences)

awarded in Hungary

Summary 2015Operating in a challenging environment

4

Agenda

5

Summary

Financial review

Operations review

Our markets

Outlook

Financial summary 2015 Focus on maintaining liquidity

Revenue down at $88.5m resulting from lower oil and gas production and realisations in both Ukraine and Russia denominated in the US Dollar : Ukraine: $7.65/Mcf (2014: $9.93/Mcf) Russia: $1.68/Mcf (2014: $2.60/Mcf)

Loss from operations of $10.7m due to lower Ukrainian and Russian revenues

Exceptional items of $64.9m include $51.1m impairment charge; $10.9m provision to cover for the rental

fees cases in Ukraine as a result of recent court judgement;

$3.0m provision for legal fees to be paid as a result of the finding of the Supreme Court that the restrictions placed on certain shareholders in 2013 were invalid

Capex spend cut significantly to offset the reduced cash generated from operating activities

6

Key Financials

($m) 2014 2015 Change%

Group revenue 146.2 88.5 (39.5)

Profit/ (Loss) from operations beforeexceptional items

11.6 (10.7) >(100)

Exceptional items (pre-tax) (72.5) (64.9) 10.5

Loss from operations after exceptional items (60.9) (75.6) (24.1)

Cash from operations 58.4 12.8 (78.1)

Capital expenditure 42.3 8.7 (79.4)

Realised gas price ($ per Mcf) 5.74 4.20 (26.8)

Realised oil price($ per bbl) 90.79 49.75 (45.2)

Group revenueReduction in revenues due to lower production and prices

7

Group revenue declined by 39.5% to $88.5m mainly due to lower oil and gas production and realisations in both Ukraine and Russia

Group gas realisations were 26.8% lower at $4.20/Mcf largely due to the weakening of the Ukrainian Hryvnia and Russian Rouble

Group oil realisations were 45.2% lower at $49.75/bbl in line with international oil prices

146.2 (22.6)

(19.1)

(4.9) (11.1)

88.5

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2014 Ukraine gas price (70%)and volume (30%) effect

Ukraine oil price (61%)and volume (39%) effect

Ukraine LPG price (76%)and volume (24%) effect

Russia price (79%) andvolume (21%) effect

2015

Group revenue ($m)

Loss from operationsImpacted by lower revenues and exceptional charges

8

Profit affected by $57.7m decrease in revenues as discussed on slide 7 Group operating costs down primarily due to suspended drilling programme, reduced manpower costs

and devaluation of the Ukrainian Hryvnia and Russian Rouble DD&A charge reduced by $6.3m largely as a result of lower production in Ukraine and Russia Production based taxes decreased by $19.3m mainly due to the lower gas tax rates applied due to the

Interim Award of the Arbitration Case of 28% as opposed to 55% rate applied from 1 August 2014 to 31 December 2014, lower production in Ukraine and lower gas tax rates in Russia as a result of implementation of a new tax regime on 1 July 2014

11.6

(10.7)

(75.6)

7.2

6.319.3

2.6

(57.7)

(64.9)-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

Profit fromoperations 2014

(beforeexceptional items)

Sales Operating costs DD&A Production basedtaxes

Administrative andother expenses

Loss fromoperations (beforeexceptional items)

2015

Exceptional items Loss fromoperations (after

exceptional items)2015

Loss from operations ($m)

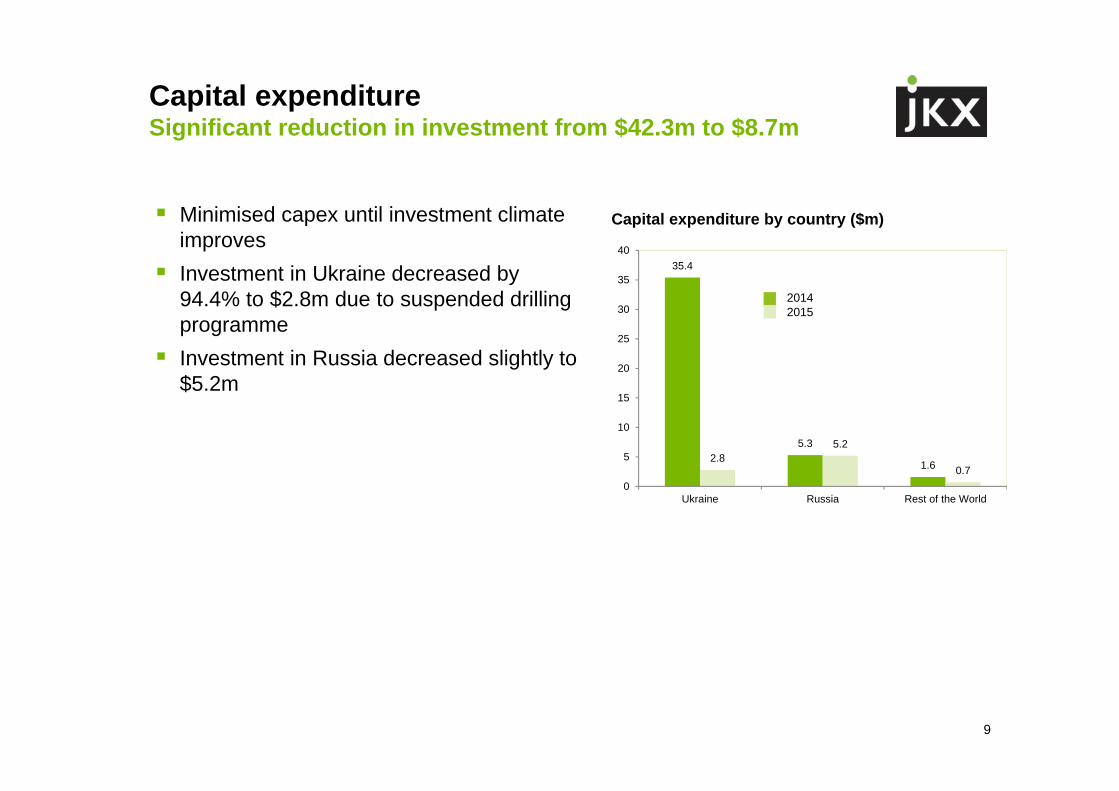

Minimised capex until investment climate improves

Investment in Ukraine decreased by 94.4% to $2.8m due to suspended drilling programme

Investment in Russia decreased slightly to $5.2m

Capital expenditure Significant reduction in investment from $42.3m to $8.7m

9

35.4

5.3

1.62.8

5.2

0.70

5

10

15

20

25

30

35

40

Ukraine Russia Rest of the World

20142015

Capital expenditure by country ($m)

Movement in cashConserving cash to meet financial obligations

Key factors: Cash generated from operations of $12.8m Capex programme reduced to manage liquidity Maturity of $2.7m of the treasury bills purchased in 2014 Bond repayment made of $5.7m in February 2015. Subsequently to the year-end, bond

repayment of $12.3m was made in February 2016

10

Movement in cash ($m)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

31 December2014

Cash fromoperations

Interest paid Income taxpaid

Purchase ofproperty, plant

andequipment

and intangibleassets

Interestreceived

Treasury Bills Bondrepayment

Restrictedcash

Effect ofexchange

rates on cashand cash

equivalents

31 December2015

(3.0) (0.7)

(6.2) (5.7)(1.2)

2.71.6

12.8

25.425.9

0.2

Agenda

11

Summary

Financial review

Operations review

Our markets

Outlook

Operational summary 2015Key developments

12

Ukraine Elizavetovskoye – Maintained stable production from 3 wells Ignatovskoye – Production optimisation Mochanovskoye – Increased production and wireline intervention. Stage one of the

waterflood pilot was completed Novo-Nikolaevskoye complex - A seismic rock physics and inversion study ongoing to

de-risk additional drilling locations

Russia Koshekhablskoye - Steady production from wells 15, 20 and 25 Completion of repairs on Well 27 Gas Processing Facility (GPF) upgrade to 60 MMcfd completed in Q3 2015

Hungary No production in 2015 Six Mining Plots (production licences) were awarded over the former Hernad I and

Hernad II Exploration Licences Farmout process underway

Reserves & production

Group Reserves of 95.7 MMboe, reserves replacement ratio of 42% for 2015 (annualproduction of 3.28 Mmboe)

Production averaged 8,996 boepd, down 9.3% from 9,919 boepd in 2014 (increased to 10,553 boepd in January 2016 following repair of Well 27 in Russia)

Rudenkovskoye Field Pre-abandonment test in R12Z resulted in

significant additional production Ignatovskoye Field Successful re-acidisation in Ignatovskoye in

IG138 and IG124Z Molchanovskoye Field Recompletion of M169 into upper Devonian as

part of waterflood project Pre-abandonment test in M36 resulted in

significant additional production Novo-Nikolaevskoye Complex An ongoing seismic rock physics, inversion and

reservoir characterization study, aim to de-risk additional drilling locations and leads in Zaplavskoye Exploration License

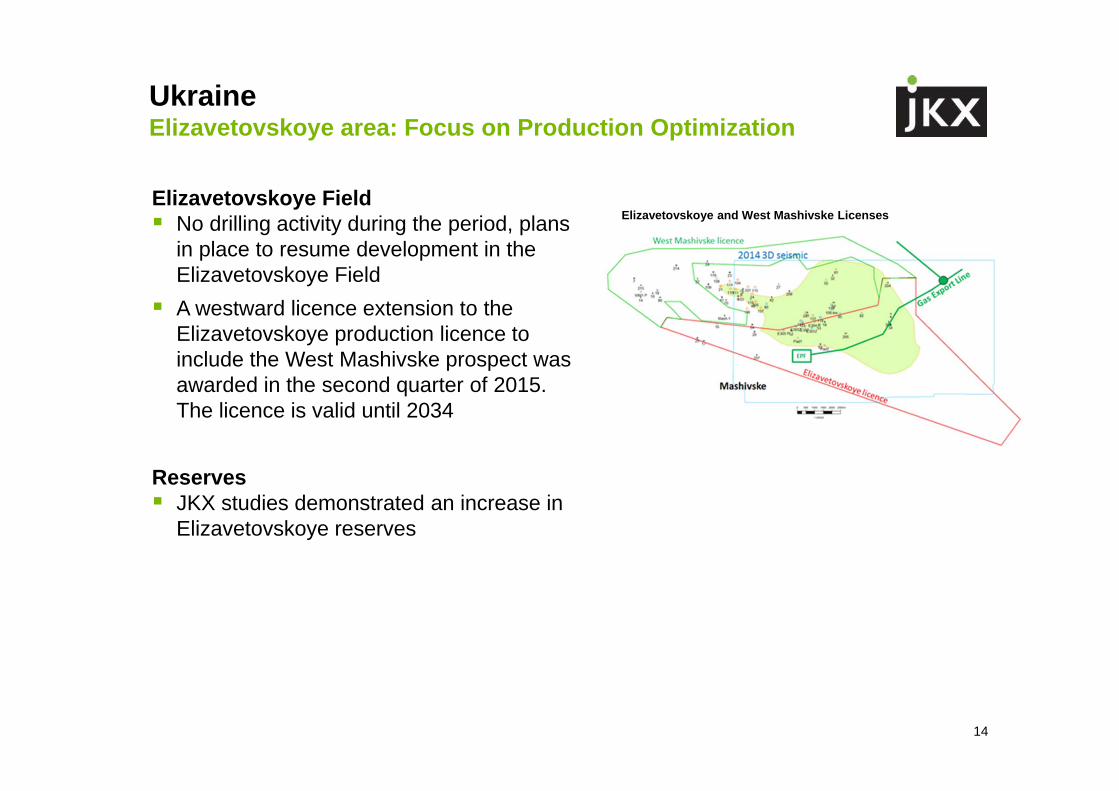

UkraineNovo-Nik area: Focus on Production Optimization

13

Novo-Nikolaevskoye Complex

Reserves JKX studies demonstrated a decrease in IGN and ZAPL reserves, and an increase in in

MOL, NN and RUD reserves.

Elizavetovskoye Field No drilling activity during the period, plans

in place to resume development in the Elizavetovskoye Field

A westward licence extension to the Elizavetovskoye production licence to include the West Mashivske prospect was awarded in the second quarter of 2015. The licence is valid until 2034

Reserves JKX studies demonstrated an increase in

Elizavetovskoye reserves

Ukraine Elizavetovskoye area: Focus on Production Optimization

14

Elizavetovskoye and West Mashivske Licenses

Tubing repairs in well 27 completed in Q4 2015

Steady production from Wells 15, 20, 25 and 27 by the end of the year

Obligation to re-enter and sidetrack well-09 to the Callovian reservoir has been deferred until 2019

Programme to recomplete with chrome tubing is currently under review

RussiaKoshekhablskoye field: well-27 came back on line

15

Agenda

16

Summary

Financial review

Operations review

Our markets

Outlook

Ukraine Domestic prices remain significantly above European hubs, while Ukraine

continues to increase the share of European gas in gas imports Gas market rules continue to evolve with full implementation of new Law on

Gas market expected by 2017 Combination of price differential and new market rules create opportunities for

gas imports/trading activity Gas royalty rates reduced from 55% to 29% from January 2016

Russia Regulated price to continue increasing at 7-8% per year (lower than inflation) Independent producers continue to expand domestic market share and

pushing for domestic market reform and access to gas exports Russia moving towards spot (hub) sales both in the domestic market and

abroad

Our core marketsChallenging environment

17

Agenda

18

Summary

Financial review

Operations review

Our markets

Outlook

Re-evaluating the Field Development Plan in Ukraine with global best practices in mind and establishing our centre of technical expertise in Kiev

Maximising the cash generation of the asset in Russia, while reviewing additional development and monetisation options

Rebuilding the Field Development Plan in Hungary and Slovakia using best practices and then adapting this goal for local execution

Continuing to look for cost reductions across the Group Pursuing a favourable result in the arbitration case against the Ukrainian

government We are committed to rebuilding investor confidence and trust in JKX through

regular open communication with shareholders

Outlook for 2016Strategy to restore shareholder value at JKX

19

20

Our markets

Appendices

Group reserves

21

Total remaining reserves as at 31 December 2015

Loss for the yearImpacted by operations, fair value of derivative and taxation

22

$32.8m decrease in taxation mainly due to lower profitability of Ukrainian operations and recognition of deferred tax assets in respect of Russian tax losses carried forward to future periods

$11.0m decrease in fair value on derivative liability is associated with the convertible bond since its placement on 19 February 2013. As the Company’s share price has increased from 12.00 pence at 31 December 2014 to 27.25 pence at 31 December 2015 and the conversion right of the put option has become more valuable, a charge of $1.9m versus a credit of $9.1m in 2014 has been recognised

* Difference due to rounding

(22.0)(25.8)

(81.4)*

(3.3)32.8

(22.3)

(11.0)

(55.7)-90

-80

-70

-60

-50

-40

-30

-20

-10

0

Profit after tax 2014(before exceptional

items)

Movement in profitfrom operations in

2015

Fair value onderivative liability

Net finance chargesand other

Decrease intaxation, other than

on exceptional items

Loss after tax(before exceptional

items) 2015

Exceptional items,net of tax

Loss after tax (afterexceptional items)

2015

Loss for the year ($m)