final draft-imane helmy

TRANSCRIPT

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 1/34

The effect of microcredit on poverty

reduction and women empowerment

By

Imane Abdel Fattah Helmy

Research Methodology PaperSubmitted to the Management Department

Faculty of Management TechnologyThe German University in Cairo

Student registration number: 10-4543

Group number: T11Name of Supervisor: Ms. Raghda El-Ebrashi

Date: Thursday January 22nd , 2009

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 2/34

Table of Contents:

1. Introduction…………………………………………………………………………..1

2. Literature Review.........................................................................................................2 2.1.Overview on poverty…………………………………………………………….2

2.1.1. Background and definitions.

2.1.2. Types of poverty.

2.1.3. Case studies of poverty in developing countries.

2.2. Overview on microcredit………………………………………………………...8

2.2.1. Characteristics of the microcredit programs.

2.2.2. The effect of gender differences on the effectiveness of the

microcredit programs.

2.2.3. A successful model of the microcredit programs: The Grameen

bank. . The effect of microcredit on poverty reduction and women

empowerment………………...………………………………………………....14

2.3.1. The effect of microcredit on poverty reduction.

2.3.2. The effect of microcredit on women empowerment.

2.3.3.Criticism about the microcredit programs.

3. Methodology……………………………………………………………………...…20

4. Conclusion…………………………………………………………………………..23

5. References…………………………………………………………………………...24

6.Appendix……………………………………………………………………….……27

6.1. Appendix 1: The Grameen Bank versus the commercial banks.

6.2. Appendix 2: The questionnaire.

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 3/34

II

Table of Figures:

Figure 1: Grameen Bank memebership…………………………………..13

Figure 2: Distribution of Grameen Bank members………………………14

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 4/34

1

1. Introduction:

The developing countries all over the world suffer from a complex multidimensional

problem which is poverty. Poverty can not be simply described as the low level of

income or low standard of living because it results in other difficulties like illiteracy,

vulnerability to health problems, powerlessness and low productivity (Adjasi and Osei

2007: 449). After decades of economic development, the roots of poverty still exist and

the income gap between rich and poor is critically increasing. For instance, 80 percent

of the world population are living in the developing countries and contribute only by 20

percent to the world income (Hossain 2000: 185). Also, about 1.2 billion persons live

on less than $ 1 a day and more than 2.8 billion people live on less than $ 2 per day

(Todaro and Smith 2006: 193). Consequently, poverty alleviation instruments are

gaining more interest among developing countries and many questions arise regardingthe impact of microcredit on the poverty reduction of its beneficiaries, who account for

10 million households all over the world (Chowdhury el al. 2005: 298-299, Adjasi and

Osei 2007: 449).

This study is exploring the effect of microcredit on poverty reduction and women

empowerment by investigating whether lending the poor collateral-free loans to run

income-generating activities helps in poverty alleviation and increases the bargaining

power of the women. Recently, the microcredit is perceived as a magic tool for poverty

eradication, especially after its great success in Bangladesh that was replicated by

several nations including the developed countries like The United States of America

(Chowdhury el al. 2005: 298-299). Since its first Summit in 1997, the microcredit

became the most popular approach used to eradicate the worldwide poverty and it is

argued that the microcredit empowers women both economically and socially by

increasing their contribution to the income of their family (Elahi and Danopoulos 2004:

643, Schultz et al. 2006: 51). Therefore, the impact of microcredit on poverty

eradication and women empowerment needs further examination.

The remainder of this paper is organized as follows. The next section gives an

overview on poverty measures and types then discusses three case studies of poverty in

the developing countries. This section is followed by describing the features of the

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 5/34

2

microcredit programs and discussing the effect of gender differences on the

effectiveness of microcredit then we will represent a successful model of the

microcredit programs which is the Grameen Bank. Afterward, the effect of microcredit

on poverty reduction and women empowerment will be examined before highlighting

some criticism about the microcredit programs. Finally, in the last two sections, the

methodology of the study will be described followed by the conclusion.

2. Literature Review:

2.1. Overview on poverty:

2.1.1. Background and definitions:

"Don't ask me what poverty is because you met it outside my house. Look at the houseand count the number of holes. Look at the utensils and the clothes I am wearing. Look

at everything and write what you see. What you see is poverty."

-Poor man in Kenya

(Quoted in: Todaro and Smith 2006: 7)

According to Todaro and Smith (2006: 54), absolute poverty is the inability to

satisfy the basic needs (such as food, cloths and shelter) due to the lack of the minimum

level of income required by a person to be able to survive. Ullah and Routray (2007:

237-238) agreed with Todaro and Smith (2006) by defining poverty as the inability to

reach a certain level of income because of the lack of adequate ownership and control

over resources.

Consistent with the previous definitions, the poor are individuals with mean per

capita income below the minimum level required for meeting the basic subsistence

(Adjasi and Osei 2007:450, Ullah and Routray 2007: 238). This minimum level of

income is usually measured by $1a day and it is known as the international poverty line

(Todaro and Smith 2006: 202-203). As indicated by Perkins et al. (2006: 207-208), the

poverty line is the possess of a specific amount of taka or pesos or dollars to spend

daily. This poverty line varies from one country to another based on the per capita cost

of its basket of good.

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 6/34

3

Siddique (1998:1095) mentioned that the headcount ratio, calculated based on the

number of people below the poverty line, is the most commonly used poverty measure.

In addition, another study by Ullah and Routray (2007: 239-240) revealed that the

poverty gap is one of the best measures of poverty as it shows the distance between the

consumption level and the poverty line. For instance, the greater the distance between

the consumption level of the poor and the poverty line the higher the poverty gap.

On the other hand, Adjasi and Osei (2007: 449-450) argued that poverty has a

complex nature and it can be analyzed from quantitative and qualitative perspectives.

Thus, to reach a fair assessment of the poverty status, multiple factors such as food

consumption, health, education and housing should be examined. Moreover, they

described poverty as the vulnerability to minor shock in the society such as weathershocks, the availability of limited choices, the lack of power and the deprivation from

social rights like the freedom of speech.

Sadeq (2006: 136) indicated that poverty is a multidimensional phenomenon that

should not be restricted to the low level of income as it involves other non-income

factors like poor health, illiteracy rate and lack of access to physical facilities. Perkins

et al. (2006: 207-208 ) agreed with Sadeq (2006) by defining poverty as a

multidimensional phenomenon that goes beyond the GDP per capita and encompass

basic health, education, access to safe drinking water and the ability to resist to natural

disasters and economic downturns.

Sen (1997) developed an approach to measure poverty called "The Capability

approach". This approach is used to measure the well being of the human functionings.

Functionings were defined as the various things that an individual can do or can be.

These functions vary from elementary functions such as adequate education and

nourishment to complex functions like being happy and having self-respect. The set of

functionings is known as capability and it reveals what a person can do while reflecting

his freedom to choose. Hence, this approach defines poverty as the absence of the

capability to function at the minimum level required within the society. Also, it is

worthy to say that Sen's capability approach played a critical role in shaping the

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 7/34

4

concept of the human development used nowadays to define poverty (Selim and

Mabughi 2006: 190-192).

2.1.2. Types of poverty:

It has been pointed out by Dao (2004: 500) that 63 percent of the poverty all over

the world is concentrated in rural areas. For instance, Mwenda and Muuka (2004: 144)

stated that 70 percent of the total African population and 80 percent of the poor in the

African continent live in rural areas. In addition, Ghosh (2002: 87) indicated that

poverty affects 22 percent of the rural population versus 12 percent of the urban

population in India. Moreover, Ullah and Routary (2007: 238-239) mentioned that the

total population in Bangladesh was 129.2 million in 2001, of whom 80 percent lives in

rural areas and suffers from poverty and unequal access to land.

One of the main aspects of the rural poverty, as described by Ullah and Routary

(2007: 238), is the unemployment and the underemployment due to the limited job

opportunities available outside the agriculture sector. Also, these opportunities are

growing slowly compared to the growth rate of the demand for them. For instance, Dao

(2004:500) mentioned that two-thirds of the rural poor are employed by the owners of

the lands as small farmers and low paid workers.

Dao (2004: 501-502) stated that the major causes of rural poverty are the low level

of productivity as measured by the value added per worker, the unequal income

distribution due to the concentration of lands ownership in few hands, the

discrimination based on race or gender and the large family size that results in high

dependency rate. Another reason for rural poverty, mentioned by Ghosh (2002: 89), is

neglecting the rural areas and excluding them from the reform plans. For instance, the

basic needs of the rural sector like access to electricity, clean water and communication

are not considered as priorities in the planning process that is usually class biased.

Hossain (2000:189) indicated that rural poverty is caused by limited access to the land

as well as high illiteracy rate and the large dependence on agriculture activities.

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 8/34

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 9/34

6

earn their own income and send their children to school. That is why if any country can

not ensure the right of education, freedom and equality for its women, it is more likely

than other countries to suffer from underdevelopment (Zhibin 2008: 29-30).

As Siddique (1998:1097-1099) mentioned, Bangladesh had introduced some

measures in order to fight women poverty and improve the status of women. For

instance, they introduced some measures to encourage the enrolment of girls in schools

and launched quotas to ensure the participation of women in political issues. Also, they

set up legal measures to protect women from violence. In addition, a lot of non-

governmental organizations in Bangladesh applied an integrated development system

that carries out different types of activities regarding women development such as

health, family planning, education and vocational training.

2.1.3. Case studies of poverty in developing countries:

2.1.3.1. Poverty in Bangladesh:

It has been pointed out by Hossain (2000: 189-190) that almost the half of the

population in Bangladesh fall below the poverty line. Moreover, in 1992 the statistics

revealed that 68.3 percent of children under the age of six years suffer from

malnutrition. Also, a major problem in Bangladesh is the rapid population growth

despite the implementation of successful family planning services. Another common

problem in Bangladesh is the inequality of landholding which worsens the problem of

poverty since lands are concentrated among few people while the majority of rural poor

suffer from low wages and low purchasing power.

Zapalska et al. (2007: 85) stated that the per capita income in Bangladesh is $350

which makes Bangladesh one of the poorest nations in this world. Also, the poor in

Bangladesh are characterized by the lack of food and the poor medical services. In

addition, Siddique (1998: 1095) added that the rural poor in Bangladesh suffer from

low income and unemployment while urban poor suffer from malnutrition and diseases.

Consequently, poverty in Bangladesh is a heritage that passes from one generation to

another (Zapalska et al. 2007: 85).

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 10/34

7

2.1.3.2. Poverty in Malaysia:

A study by Siwar and Kasim (1997: 1526-1533) showed that the poor in Malaysia

are characterized by a large family size, low education level, low per capita income and

low employment status due to the lack of necessary skills. The study identified some

causes of this poverty like the migration of the rural poor to the urban areas in order to

find better job opportunities and the migration of foreigners, who represent the half of

the poor residing in the urban areas of Sabah.

The solutions implemented by the government of Malaysia in order to fight poverty

were divided into four components: (1) Employment creation, (2) Provision of housing,

(3) Development of growth centers and (4) NADI programs. The government

encouraged the growth of the industrial and service sectors through incentives to createmore job opportunities in these areas. Also, they implemented some projects that aimed

at providing low cost houses with physical facilities to the poor. As for the growth

centers, the government created centers to improve the standard of living of the poor.

Finally, the NADI program intended to provide access to electricity, water and health

care in the poor houses (Siwar and Kasim1997: 1528-1529).

2.1.3.3. Poverty in Ghana:

According to Adjasi and Osei (2007: 450-461), Ghana has been a victim of poverty

and debt problems for a long time. A survey conducted in 1999 revealed that five out of

ten regions in Ghana had more than 40 percent of its population living in poverty. Even

though the decrease in poverty incidence from 51.7 percent between 1991 and 1992 to

39.5 percent in 1998-1999, the level of poverty in Ghana is still high especially in the

rural areas. Moreover, the study showed that the level of poverty is higher in

households where the head is illiterate compared to the households headed by parents

who are educated.

Illiteracy was indentified to be one of the main consequences of poverty in Ghana.

For instance, the results of the study by Adjasi and Osei (2007: 454) showed that 87

percent of the mothers and 70 percent of the fathers are illiterate. As for housing, only

14 percent of the households live in apartments while the remaining percentage live in

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 11/34

8

rooms and huts. Moreover, one third of the population relies on the water of rivers and

lakes as their main source of water and 60 percent depends on kerosene as their lighting

source instead of electricity.

2.2. Overview on microcredit:

2.2.1. Characteristics of the microcredit programs:

In the "Microcredit Summit" held in February 1997 in Washington, DC, the

microcredit programs had been defined as programs that lend the poor, mainly women,

small loans in order to enhance self-employment and income generating activities

(Elahi and Danopoulos 2004: 643-645, Zapalska et al. 2007: 86). Furthermore,

Chowdhury el al. (2005: 298) defined microcredit as small collateral-free loans given to

a jointly liable group of borrowers in order to reduce poverty through self-employment.They added that the loans are usually given to the poor through institutions or non-

profit organizations.

There are some common features shared among the microcredit programs. For

instance, the size of the loan is usually small (about US $ 100) and the repayment

period is short (about a year). In addition, the borrowers of money are poor households,

mostly women, who are called micro-entrepreneurs. Also, a common purpose of the

loans is to create self-employment and income-generating activities in the informal

sector (Elahi and Danopoulos 2004: 645, Zapalska et al. 2007: 86).

Elahi and Danopoulos (2004: 646) mentioned that the theory of microcredit is

described as "social consciousness-driven capitalism". This means that the microcredit

programs create capitalist enterprises aiming at maximizing the profit while taking into

consideration the welfare of its customers. This description clearly contradicts with the

Neo-classical production theory that was based on the assumption that individuals run

business while being motivated only by profit-maximization which excluded those who

care about the welfare of human beings. For instance, Hassan and Guerrero (1997:

1494) indicated that the revenue generated by the Grameen Bank is used to raise more

loanable funds as well as training employees and group borrowers to improve their

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 12/34

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 13/34

10

and assets ownership. The results of the study revealed that the credit provided to

women affect these behaviors more significantly than the credit provided to men. For

example, a 1 percent increase in the credit provided to women increase the probability

of the enrollment of girl in school by 1.86 percent and the enrollment of boy by 2.4

percent. Hence, the study concluded that the microcredit programs are more effective

when the borrowers are women.

Hassan and Guerrero (1997: 1509-1510) supported the results of Pitt and Khandker

(1998) when he indicated that the annual reports of the Grameen Bank showed that the

projects run by women are more successful than the projects run by men. Also, in 1992

the recovery rate of the loans was 89 percent for men and 97 percent for women.

Moreover, Zhibin (2008: 32) noted from a study of ten Chinese microcredit projectsthat the rate of paying back the loans is higher when all the borrowers are women than

the pay-back rate when borrowers are composed of men and women. Finally, Zapalska

et al. (2007: 86-87) added that women are more successful as borrowers than men

because they have better attitudes toward microcredit and self-employment.

2.2.3. A successful model of the microcredit programs: The Grameen

Bank:

Elahi and Danopoulos (2004: 650) indicated that Yunus was inspired to found the

Grameen Bank when he met a widow mother of two children, Sufiya Khatun, who

symbolized all the injustices that a society could commit against its women. Hussain el

al. (2001: 26) added that Sufiya was weaving bamboo stools that she sells and earns

two cents a day. When Yunus was surprised because of the low income she earns, she

informed him that her moneylender was the buyer of the final products so he is the one

who set the prices that hardy cover the cost of raw materials. At this moment, Yunus

decided to give Sufiya and other 42 villagers small loans to be repaid from the profits

they earn and two years later, in 1976, he established the Grameen Bank.

In 1983, the Grameen Bank was charged to operate as a national bank. It had 75

branches in five districts in Bangladesh and in 1994 it expanded its operation to cover

30000 villages (Hassan and Guerrero 1997: 1489, Mwenda and Muuka 2004: 147).

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 14/34

11

Recently, the Grameen Bank model is implemented in 50 countries like Asia, Australia

and Europe. It lent two million people in Bangladesh more than $1 billion and

employed about 14000 staff (Hussain el al. 2001: 27, Hossain 2000: 192, Zapalska et

al. 2007:86).

The fundamental belief of the Grameen Bank is that people do not create poverty

but the institutions and the policies surrounding them result in their poverty. It is not

the lack of skills, ideas and innovations that make the poor people poor because they

may possess some skills that are underutilized (Elahi and Danopoulos 2004: 645,

Hussain el al. 2001: 31). A common notion shared at the Grameen Bank is that the

main problem of poor lies behind the lack of capital given their productive capacity

(Hassan and Guerrero 1997: 1489, Hossain 2000: 192).

The Grameen Bank has rejected the basic methodology of the conventional banks

and developed its own methodology by giving loans to the poor without collateral as

loan security which contradicts with all conventional banks (Hassan and Guerrero

1997: 1489, Elahi and Danopoulos 2004: 645, Hossain 2000: 192). Hassan and

Guerrero (1997: 1504) mentioned that the maximum limit of a loan is US $ 125 to be

repaid in 50 equal installments. Also, the interest rate charged by the bank is 20 percent

which could be higher than the market rate yet it is lower than the rate charged in the

informal markets.

Hussain el al. (2001: 29) pointed out that the poor who meet the screening criteria of

the bank like being landless, not having cash or property can borrow money in forms of

groups of five people. Each member in the group receives his own loan, yet they are

jointly liable for the five loans invested in income generated activities (Hassan and

Guerrero 1997: 1503, Pitt and Khandker 1998: 959, Chowdhury el al. 2005: 300).

Usually, the members of the group come from the same village, know each other and

have similar needs; however, they can not be from one family in order to avoid family

bias (Hassan and Guerrero 1997: 1503, Hussain el al. 2001: 27).

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 15/34

12

One of the distinctive features of the Grameen Bank is the accumulation of savings

since the borrowers are required to save one Taka per week in order to constitute the

group fund that can be borrowed by any member in case of illness, emergencies or

social commitment. Moreover, the group fund enable the members to buy a share of the

stock of the bank at the cost of 100 Taka (US $ 2.5) which make the poor become

owners of the bank and take part of the board of directors (Hassan and Guerrero 1997:

1500, Hussain el al. 2001: 27-31, Hossain 2000: 193).

It has been pointed out by Hussain el al. (2001: 27) that the Grameen Bank is

different from the traditional banks that give loans and wait for the return. The

Grameen Bank offers the borrowers business expertise beside money and its vision is

broader than finance as it is the only bank in this world that promotes birth control andclean environment in its lending policy. Hassan and Guerrero (1997: 1512) agreed with

Hussain el al. (2001) as they mentioned that the original purpose of the Grameen Bank

was to offer credit and reduce poverty; however, their founders realized that credit is

not sufficient so they established a welfare program that helps poor in education,

health, housing, family planning and environment protection.

Hassan and Guerrero (1997: 1490-1492) indicated that the charismatic leadership of

Dr Yunus could be one of the critical success factors of the Grameen Bank. Also, the

decentralized administration system of the bank, organized into four independent

levels: head office, zone office, area offices and field branches that coordinate with

each other, has been a key factor in attaining its success. Moreover, the employees of

the Grameen Bank possess the necessary skills since the bank offers them training

sessions and they are highly motivated because their salaries depend on their

performance. Furthermore, Hussain el al. (2001: 27) mentioned that the trust shared

among the members of the Grameen Bank due to their regular interaction is the secret

of its visionary success.

Hossain (2000: 194) mentioned that one of the Grameen Bank employees stated

three reasons that are considered as the secret of the Grameen Bank success. First, the

payment of installments is scheduled on a weekly basis which facilitates the pay back

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 16/34

13

of the loans. Second, the bank ensures that loans are used for the purpose they were

borrowed for. For example, the employees physically check if a loan borrowed for the

purpose of building a house resulted in building this house or not. Third, the

commitment of the employees and their punctuality in distributing the loans is reflected

on the borrowers so they paid the installments regularly.

The model of the Grameen Bank is considered as one of the most successful

attempts to increase the involvement of poor women in productive activities (Hassan

and Guerrero 1997: 1509). Consequently, women represent the major customers of the

Grameen Bank (Hassan and Guerrero 1997: 1509, Hussain el al. 2001: 29). As Figure 1

shows, in 1994 the total number of the Grameen Bank members was about two million

members of whom women represented the majority. Also, figure 2 indicates that theparticipation of men in the Grameen Bank has been decreasing over the years while

women participation had steadily increased. For illustration, women membership had

increased from 65 percent in 1985 to 94 percent in 1994 (Hassan and Guerrero 1997:

1489-1510). In addition, recent figures show that 95 percent of the Grameen Bank

customers are women (Hussain el al. 2001: 27).

Figure 1: Grameen Bank membership

Source: (Hassan and Guerrero 1997: 1490)

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 17/34

14

Figure 2: Distribution of the Grameen Bank members

Source: (Hassan and Guerrero 1997: 1490)

2.3. The effect of microcredit on poverty reduction and women

empowerment:

2.3.1. The effect of microcredit on poverty reduction:

The Report of the Task Forces on Bangladesh Development Strategies mentioned

three approaches for poverty eradication. The first approach is investing in social

sectors like health and education to improve the standard of living and enhance the

human capabilities. The second one is encouraging growth oriented programs that have

a strong effect on the rural poverty. The third approach is promoting the targeted

income and the employment generating programs to support the vulnerable poor who

were previously excluded from the market based development process (Hossain

2000:190, Siddique 1998: 1098).

The microcredit programs are considered as growth oriented programs that aim at

reducing poverty by empowering the poor and giving them the opportunity to

contribute to the growth of their society through self-employment (Hossain 2000:190-

191). The microcredit programs are recognized all over the world as a key instrument

to alleviate poverty and to create a sustainable human development process.

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 18/34

15

Consequently, the international donor community and the non-governmental

organizations were encouraged in the general assembly of the United Nations passed in

1997 to integrate the microcredit programs in their strategies and to adopt policies that

support its development (Hossain 2000:191, Elahi and Danopoulos 2004: 647).

As pointed out by Chowdhury el al. (2005: 299), there are more than 1000 non-

governmental organizations in Bangladesh that run microcredit programs. Moreover,

Zapalska et al. (2007: 89) indicated that the innovative approach of Bangladesh, which

introduced the microcredit programs, has significantly eradicated the poverty of several

families and helped hem get out of the poverty trap. For instance, a study conducted by

Chowdhury el al. ( 2005: 298-303) on a sample of 954 participants of the microcredit

programs in Bangladesh revealed that microcredit is associated with a reduction in thepoverty of the participants especially with the long run participation in the programs.

Hossain (2000: 191-194) stated that the Grameen Bank, which is the biggest micro-

lender in Bangladesh, reduced poverty from 59 percent in 1991-1992 to 53 percent in

1995-1996. Also, more than 160,000 families who borrowed money from the Grameen

Bank were able to built new houses, sent their children to school and improve their

standard of living. Hussain el al. (2001: 32) agreed with Hossain (2000) by mentioning

that the Grameen Bank represents a successful example of a poverty alleviation

initiative that is appreciated by several international organizations. Moreover, it has

been pointed out by Hassan and Guerrero (1997: 1510) that the Grameen Bank had

improved the social life and the self-esteem of the poor beside the enhancement of their

economic conditions.

Siwar and Kasim (1997: 1534) mentioned that the achievements of the Grameen

Bank in Bangladesh and its branches in many countries like Asia and Malaysia indicate

that microcredit is a powerful tool for poverty reduction and the improvement of the

socio-economic conditions of the poor. Consequently, one of the main aims of their

study was to come up with some policy options for an entrepreneurship program that

will be implemented in Malaysia to fight poverty. This program will give interest free

loans to the poor in order to start their own small enterprises. Also, training courses to

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 19/34

16

the participants such as project management, marketing and accounting will be

organized. The researchers conducted an empirical study on a sample of 510 persons in

Malaysia and the results showed that 63 percent of the sample will be interested in this

program as a way to reduce their poverty.

Schultz et al. (2006: 62) gave an example of a woman who received microcredit

and invested the loan in income-earning activity so she was able to pull her family out

of poverty. Bakhita, a mother of seven children, got her first credit in 1997 followed by

two other credits and started selling cloths and utensils to women. Before receiving

these loans, she was not able to afford the fees of her children schools so they stopped

going to school and they started to sell water. However, after getting the three loans and

starting her project, Bakhita was able to build a new house and pay the fees of herchildren education who were all enrolled again in schools.

2.3.2. The effect of microcredit on women empowerment:

According to Mahmud (2003: 580-581), women empowerment is a multi-

dimensional notion that can be defined from different perspectives. In the development

process, women empowerment has been viewed as the improvement of women well-

being. This well-being can be absolute like improving the welfare of women with

respect to education, health, nutrition and ownership of assets or relative like improving

the position of women in the household compared to men. In addition, Ackerly (1995:

56) developed an idea about women empowerment. He said that women empowerment

takes place when the woman invests money in a successful business, her husband stop

hitting her, she takes part in family decisions and she sends her kids to school (Osmani

2007: 697).

Kabeer (1999: 436f) refers to empowerment as the different processes that enable

women to be able to choose after being denied from this ability (Mahmud 2003: 584-

585, Schultz el al. 2006: 53). On the other hand, Chen and Mahmud (1995) identified

four dimensions of empowerment: material, cognitive, perceptual and relational. While

material empowerment occurs when women acquire material resources such as land

and assets, cognitive empowerment occurs when women recognize their own skills

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 20/34

17

which increase their self-esteem. Also, perceptual empowerment takes place when the

perception of the society toward women changes and this lead to increasing their social

prestige and values. Finally, relational empowerment occurs when the gender

inequality in relationships within the family and the whole society disappears (Mahmud

2003: 585).

Schultz el al. (2006: 53-54) mentioned that women participation in the microcredit

programs improve their material welfare and give them more rights within the

household. Also, microcredit helps women gain some degree of independence by

participating in group meetings and discussions. In addition, Osmani (2007: 698) has

clearly shown that several studies conducted with the aim of measuring the effect of

microcredit on women empowerment found out that microcredit reduced domesticviolence against women, increased women involvement in the decision making

process, improved women self-worth and increased the education of daughters.

Likewise, Mwenda and Muuka (2004: 146) indicated that access to microcredit

increases women empowerment and children education.

Osmani (2007: 696-697) pointed out that microcredit was originally designed to

improve the income earning power of women; however, it was also able to empower

women in a broader sense. For instance, when women contribute to the cash income of

the family, their power within the household increases and their self-esteem raises.

Furthermore, borrowing the loan and running an income-generating activity enable

women to enlarge their social networks and come out of the narrow limits of their

household to the broad society and this increases their self confidence.

Mahmud (2003: 579) mentioned that one of the most noticeable transformations in

the life of women in Bangladesh is the increase in their access to microcredit as a part

of several programs designed by non-governmental organizations to fight poverty. He

added that the effect of these programs was not limited to poverty eradication but it was

expanded to include women empowerment. For instance, Hossain (2000: 196) stated

that the Grameen Bank was able to empower its women borrowers and many of them

become economically independent from their husband. Moreover, Hassan and Guerrero

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 21/34

18

(1997: 1510) indicated that the Grameen Bank has a positive and a noteworthy impact

on improving women decision making within the household.

Osmani (2007: 695-702) had empirically tested, using a sample of the Grameen

Bank borrowers, whether women access to microcredit improves their bargaining

power within the household. The study reported that microcredit has a positive effect

on women bargaining power as measured by the value of assets (land and non-land)

that women own as well as their judgment about their ability to support themselves if

left alone. Another study by Mahmud (2003: 589-602) revealed that women

participation in microcredit programs encourages women's self-employment, improves

their welfare and increases their active role in the decision making process.

2.3.3. Criticism about the microcredit programs:

Zhibin (2008: 32) indicated that some critics argued that microcredit negatively

affects women by increasing their workload and mental stress. Similarly, Mahmud

(2003: 582) mentioned that some opponents of the microcredit claimed that the

microcredit programs increase the pressure on women by the family and the financial

organizations to pay the loan installments on time which create a new form of social

burden upon women.

It has been argued that poor are not able to run an activity and generate income as

they lack the necessary business skills. This means that access to credit is not the only

constraint on increasing the income of the poor because still the lack of human capital

and labor productivity can affect the increase in income. Moreover, microcredit has

been accused by replicating an old credit theory developed by Adam Smith (1937) who

said that individuals can self- employ their skills to their best interests if they are given

access to credit. Hence, microcredit did not bring out any innovative theory (Elahi and

Danopoulos 2004: 645-648).

The Grameen Bank has been criticized by charging high interest rate (20 percent)

which is greater than the interest rate charged by the conventional banks (10-15

percent) (Hussain el al. 2001: 32, Hossain 2000: 196). In addition, Hassan and

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 22/34

19

Guerrero (1997: 1515-1516) indicated that the Grameen Bank takes funds from donors

then puts them in commercial banks that pay higher interest rates and by this way it is

making profit from granted donations.

A study conducted by Hoque (2004: 22-30), to assess the effect of microcredit on

poverty alleviation using data from one of the biggest microcredit provider in

Bangladesh, which is Bangladesh Rural Advancement Committee, concluded that the

microcredit has a minimal effect on the improvement of the economic conditions of its

participants as well as the eradication of their poverty because the loans are not usually

used in productive activities. In other words, the microcredit programs are criticized by

having an insignificant effect on poverty since the microcredit policies do not ensure

that loans are invested in income earning activities.

From exploring the previous literature review, we found a huge gap in investigating

the impact of combining microcredit with non-financial services, e.g. education, health

care, vocational training, technical courses, on poverty reduction and women

empowerment in Egypt. The credit by itself may be an insufficient tool to reduce

poverty if it is not associated with other social services because poverty is a

multidimensional problem that is not restricted to the level of income but it

encompasses food, shelter, health and education. Consequently, the research question

that this study seeks to answer is: "What is the effect of combining microcredit with

other social services on poverty alleviation and women empowerment in Egypt?".

Hypothesis 1: Combining the microcredit with other social services has a positive

effect on poverty reduction in Egypt.

Hypothesis 2: Combining the microcredit with other social services empowers the

Egyptian women.

In order to obtain a multifaceted view of poverty, we measure poverty reduction by

the raise in the level of income, the reduction in health expenditures, the improvement

of the literacy rate and the housing conditions. As for women empowerment, it is

measured by the increase in the ownership of material assets, self-esteem, social

network and the reduction in the domestic violence against women. The social services

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 23/34

20

provided with the microcredit include illiteracy eradication programs, health care,

technical and business training like marketing courses, vocational training and project

management.

3. Methodology:

In order to test the previously mentioned hypotheses, a quantitative method that

combines surveys and interviews will be employed. Since we are aiming at

investigating the impact of providing some social services with the microcredit on

poverty reduction and women empowerment, a survey will be a valid tool to draw

statistical conclusions about this effect using a questionnaire to test the improvements

that took place after receiving the microcredit and the social services. However, due to

the cultural barriers and the high rate of illiteracy among the poor in Egypt, a structuredface-to-face interview is highly needed in order to clarify the purpose of the study and

the meanings of the questions.

The interviewer will introduce the objective of the study and its level of

confidentiality then the questions will be explained to the participants before recording

the answers. Also, the questionnaire of the study will be divided into three sections.

The first section will include the screening criteria and the demographic data like the

level of education, the family size, the martial status and the type of the social services

that the respondent receives. The second section will measure the effect of the

microcredit and social services, if any, on poverty reduction and the third section will

focus on their impact on women empowerment.

The sample of the study will consist of one hundred Egyptian poor who received

small loans and social services from non-governmental organizations and one hundred

poor who received the microcredit from governmental institutions, like Nasser Social

Bank and the Social Fund for Development, without any social services. The second

group of beneficiaries will act as a control group to measure the impact of microcredit

on poverty reduction and women empowerment then it will be compared to the other

group in order to determine the effect of combining microcredit with social services on

poverty alleviation and women empowerment. The sample will include men and

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 24/34

21

women, yet it is expected that higher percentage of women will be included since the

majority of the microcredit beneficiaries are women. This target group was chosen to

have precise up-to-date information provided directly from the beneficiaries of the

microcredit instead of relying on data and documents provided by governmental or

non-governmental institutions.

The participation of the two groups in the microcredit programs should be at least

five years since it has been pointed out by Hassan and Guerrero (1997: 1499) that the

beneficiaries of the microcredit programs need about five years to improve their

economic conditions and raise their income above the poverty line. Likewise, women

empowerment is a long-run process that needs time to take root in the society (Osmani

2007: 697). Consequently, in order to measure the impact of combining the microcreditwith social services on poverty alleviation and women empowerment, the participation

of the sample in the programs should be five years or more.

The sample of the study will be chosen from the district of Old Cairo, the area of

Ain El Sira, using the stratified random sampling which is one of the probability

techniques. From the total population in Ain El Sira, which account for twenty

thousand persons, those who took small loans and social services offered by non-

governmental organizations from five years or more are one thousand persons. This

relevant population will be divided into three stratums according to the area where they

live (Blocks, Slums and the area of El Gayara) then one hundred persons will be

randomly selected from each stratum.

As for the control group, it will be chosen from Nasser Social Bank and the Social

Fund for Development using the simple random sampling technique. Each beneficiary,

who is a resident of Old Cairo, will be assigned a unique number than one hundred

numbers will be randomly chosen from the list. We choose the area of Old Cairo as it is

one of the poorest areas in Cairo where several organizations operate in order to

develop the region and improve its economic and social conditions. Also, a sample of

one hundred persons was selected to accurately represent the relevant population.

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 25/34

22

During the first two weeks of the research, the questionnaire will be designed then

we will contact two non-governmental organizations in Old Cairo, the Social Fund for

Development and Nasser Social Bank, in the following two weeks, to get the list of

names and the addresses of the target group. The fieldwork of the study will last for

two months since gathering the data will be done through in-home visits to the poor

which is expected to consume more time. Also, it is worthy to note that four employees

from the non-governmental organizations, the Social Fund for Development and Nasser

Social Bank will assist in the fieldwork by offering guidance in the area of Old Cairo.

Afterward, data will be analyzed in two weeks, using the "Statistical Package for the

Social Sciences" software, and during the last two weeks the findings of the study will

be presented and the research will be finalized.

Limitations:

The findings of the study can not be generalized to all the microcredit programs in

Egypt because the sample was limited to one urban area in Cairo and it excluded the

rural areas in other governorates and in Upper Egypt. Moreover, the majority of the

sample consists of illiterate individuals which increase the probability of the response

error due to the incomplete knowledge or the misunderstanding of the questions, even

though the interpretation provided by the interviewer, especially for the questions that

measures the self-esteem, the domestic violence or the social network. Also, the

response bias may increase for some questions regarding the raise in the level of

income, the health expenditures and the material assets ownership because the

participants may provide inaccurate information regarding these matters.

Due to the limited scope of the study, other issues, such as the effect of microcredit

on poverty reduction in the United States of America, the social and the cultural

adjustments of the microcredit model in Egypt and a comparison between the impact of

microcredit on poverty reduction in a developing country like Egypt and a developed

country like the United States of America, were not explored in the current paper.

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 26/34

23

4. Conclusion:

In this paper, we examined the impact of the microcredit on poverty reduction and

women empowerment by exploring whether lending the poor small loans to enhance

their self-employment helps in poverty alleviation and increases the bargaining power

of the women. The paper started by identifying the quantitative and the qualitative

measures of poverty followed by the types of poverty such as rural and women poverty.

Afterward, three case studies of poverty in Bangladesh, Ghana and Malaysia were

presented followed by defining the microcredit programs. After exploring the impact of

gender differences on the effectiveness of the microcredit, we found that the projects

run by women are more successful than the projects run by men because targeting

women improves the welfare of the whole family.

After presenting a successful model of the microcredit which is the Grameen Bank,

we highlighted the difference between this bank and the conventional banks then we

explored the impact of the microcredit on poverty reduction and women empowerment.

The findings showed that microcredit significantly eradicates the poverty of its

beneficiaries and helps hem get out of the poverty trap besides improving their social

life. Likewise, women participation in the microcredit programs improve their material

welfare, give them more rights within the household, reduce domestic violence and

increase their involvement in the decision making process. Finally, some criticisms

against the microcredit, like charging high interest rate and increasing the burden on its

beneficiaries to pay the installments, were highlighted.

In our opinion, the findings of the study support the popularity of the microcredit all

over the world by illustrating its positive effect on poverty reduction and women

empowerment. This significant effect is consistent with the replication of the

microcredit programs in several countries with the hope of escaping poverty by

enhancing self-employment and improving the status of women. Furthermore, we think

that the opponents of the microcredit did not provide enough evidence to support their

claims. For instance, the Grameen Bank is not charging a high interest rate as it has

been argued because its interest rate is lower than the rate charged by the commercial

banks and the moneylenders (Hossain 2000: 197).

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 27/34

24

Also, the study conducted by Hoque (2004: 22-30) based all its data on the

Bangladesh Rural Advancement Committee, which is one of the microlender in

Bangladesh, to reach its conclusion about the minimal effect of the microcredit on the

economic conditions of its participants. Therefore, the results of this study can not be

generalized to the microcredit programs all over the world because the sample was

selected from one single institution. Moreover, the study did not mention the duration

of the sample participation in the program which is a key factor that may affect the

findings of the research as it has been pointed out by Hassan and Guerrero (1997: 1499)

that it takes the participants about five years to improve their economic conditions and

increase their level of income.

.

5. References:

Adjasi, C.K.D., Osei, K.A. (2007), Poverty profile and correlates of poverty in Ghana.

In: International Journal of Social Economics, vol. 34, No 7, pp. 449-471

Chowdhury, M.J.A., Ghosh, D., Wright, R.E. (2005), The impact of micro-credit on

poverty: evidence from Bangladesh. In: Progress in Development Studies, vol. 5, No

4, pp. 298-309

Dao, M.Q. (2004), Rural poverty in developing countries: an empirical analysis. In:

Journal of Economics Studies, vol. 31, No 6, pp. 500-508

Elahi, K.Q., Danopoulos, C.P. (2004), Microcredit and the Third World: Perspectives

from moral and political philosophy. In: International Journal of Social Economics,

vol. 31, No 7, pp. 643-654

Gosh, B.N. (2002), Allocative inefficiency and rural poverty in India. In: International

Journal of Social Economics, vol. 29, No. 1/2, pp. 87-96

Hassan, M.K., Guerrero, L.R. (1997), The experience of the Grameen Bank of

Bangladesh in community development. In: International Journal of Social

Economics, vol. 24, No 12, pp. 1488-1523

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 28/34

25

Hoque, S. (2004), Micro-credit and the Reduction of Poverty in Bangladesh. In: Journal

of Contemporary Asia, vol. 34, No 1, pp. 21-32

Hossain, I. (2000), Micro-Credit and Good Governance: Models of Poverty Alleviation.

In: Southeast Asian Journal of Social Science, vol. 28, No 1, pp. 185-208

Hussain, M.M., Maskooki, K., Gunasekaran, A. (2001), Implications of Grameen

banking system in Europe: prospects and prosperity. In: European Business Review,

vol. 13, No 1, pp. 26-41

Mabughi, N., Selim, T. (2006), Poverty as Social Deprivation: A Survey. In: Review Of

Social Economy, vol. LXIV, No 2, pp. 181-204

Mahmud, S. (2003), Actually how Empowering is Microcredit? In: Development and

Change, vol. 34, No 4, pp. 577-605

Mwenda, K.K., Muuka, G.N. (2004), Towards best practices for micro finance

institutional engagement in African rural areas. In: International Journal of Social

Economics, vol. 31, No 1/2, pp. 143-158

Osmani, L.N.K. (2007), A BREAKTHROUGH IN WOMEN’S BARGAINING

POWER: THE IMPACT OF MICROCREDIT. In: Journal of International

Development, vol. 19, pp. 695-761

Perkins, D.H., Radelet, S., Lindauer, D.L. (2006). Economics of Development, W.W.

Norton & Company, New York

Pitt, M.M., Khandker, S.R. (1998), The Impact of Group-Based Credit Programs onPoor Households in Bangladesh: Does the Gender of Participants Matter? In: Journal

of Political Economy, vol. 106, No 5, pp. 958-996

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 29/34

26

Sadeq, A.M. (2002), Waqf , perpetual charity and poverty alleviation. In: International

Journal of Social Economics, vol. 29, No 1/2, pp. 135-151

Schultz, U., Maccawi, A., El-Fatih, T. (2006), The Credit Helps me to Improve my

Business: The Experiences of Two Microcredit Programs in Greater Khartoum. In:

The Ahfad Journal, vol. 23, No 1, pp. 50-65

Siddique, M.A.B. (1998), Gender issues in poverty alleviation: a case study of

Bangladesh. In: International Journal of Social Economics, vol. 25, No 6/7/8,

pp. 1095-1111

Siwar, C., kasim, M.Y. (1997), Urban development and urban poverty in Malaysia. In:International Journal of Social Economics, vol. 24, No 12, pp. 1524-1535

Todaro, M.P., Smith, S.C. (2006). Economic Development, Pearson Education Limited,

the United States of America

Ullah, A.K.M.A., Routray, J.K. (2007), Rural poverty alleviation through NGO

interventions in Bangladesh: how far is the achievement? In: International Journal of

Social Economics, vol. 34, No 4, pp. 237-248

Zapalska, A.M., Brozik, D., Rudd, D. (2007), The success of micro-financing. In:

Problems and Perspectives in Management, vol. 5, No 4, pp. 84-90

Zhibin, L. (2008), Chinese Women and Poverty Alleviation: Reflections and Prospects

for the Future. In: Chinese Sociology and Anthropology, vol. 40, No 4, pp. 27-37

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 30/34

27

6. Appendix:

6.1. Appendix 1: The Grameen Bank versus the commercial banks:

Table 1: Advantages and disadvantages of the Grameen Bank and commercial banks

Source: (Hussain el al. 2001: 33)

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 31/34

28

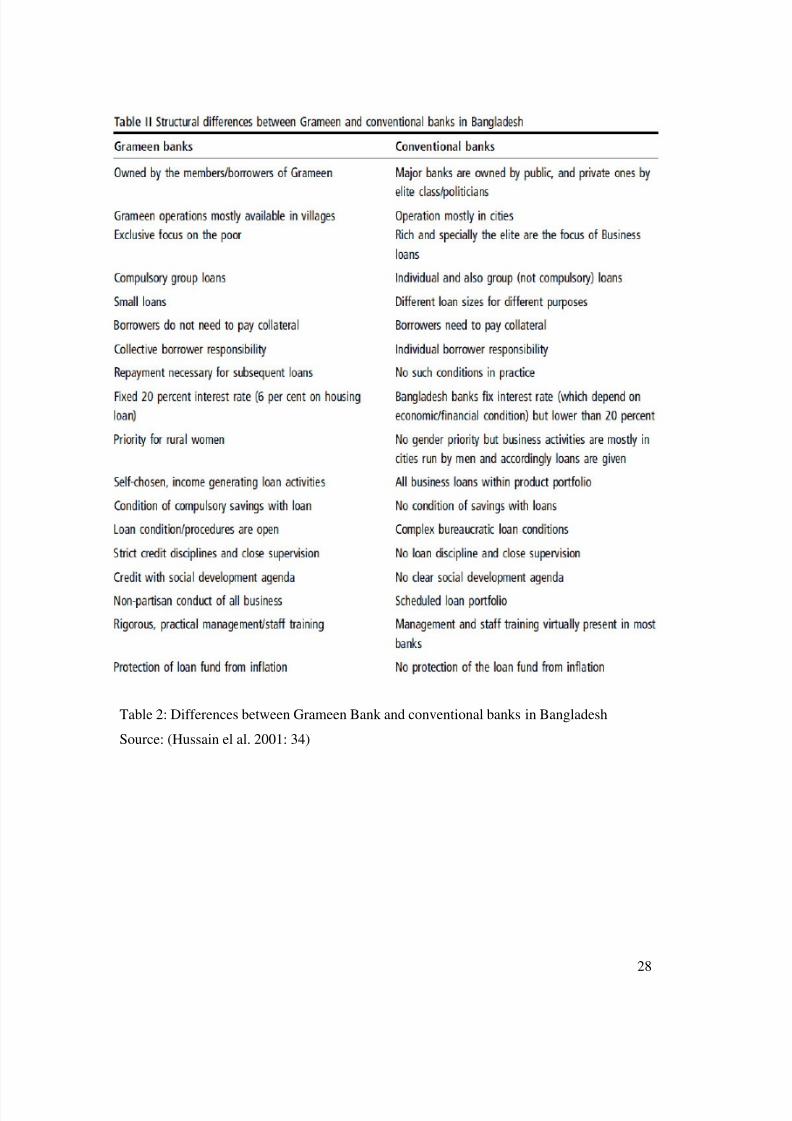

Table 2: Differences between Grameen Bank and conventional banks in Bangladesh

Source: (Hussain el al. 2001: 34)

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 32/34

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 33/34

30

2- Health expenditure:

Compared to your situation before receiving the microcredit, your monthly health

expenditures are…..?

Higher The same Less

3- Housing conditions:

Your house is made of…?

Wood Wall Straw/mud

Cement Brick Concrete

4-

Literacy:What is your level of education?

Primary Secondary Diploma

University None Others

Section III: Women empowerment:

(N.B. please skip this section if the respondent is a male).

1- Material assets ownership:

a) You share in the income of the family, versus your husband income, is…?

Higher The same Less

b) Do you have any personal savings accumulated for your personal use?

Yes

No

2- Social Network:

a) Do you trust the lending group to which you belong?

Yes

No

8/3/2019 Final Draft-Imane Helmy

http://slidepdf.com/reader/full/final-draft-imane-helmy 34/34

b) When you need consultation or assistance in your project, you usually ask…?

Husband

An employee of the lender institution

None

3- Decision making:

Compared to your situation before receiving the microcredit, your contribution to

the decision making within is the household is…..? (e.g. decision about the

number of children to have, decision about children education)

Higher The same Less

4- Domestic violence:

Are you usually exposed to any type of domestic violence, e.g. physical like

beating, Economic like controlling your money or social like controlling your

relationship and social contacts?

Yes

No

5- Children education:

a) Are your children educated?

Yes

No

If Yes, was it your decision to send them to school?

YesNo

Thank you so much