final august investor presentation

TRANSCRIPT

1

INVESTORPRESENTATION

AUGUST 2017

Cautionary Statements

This presentation includes "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended. These statements express a belief, expectation or intention and are generally accompanied by words that convey

projected future events or outcomes. The forward-looking statements include statements about the company’s corporate strategies, future operations, development

plans and appraisal programs, our drilling inventory and locations, estimated production, rates of return, reserves, projected capital expenditures, projected operating

and other costs, operational optimization initiatives, anticipated efficiency improvements and cost reductions, liquidity and capital structure. We have based these

forward-looking statements on our current expectations and assumptions and analyses made by us in light of our experience and our perception of historical trends,

current conditions and expected future developments, as well as other factors we believe are appropriate under the circumstances. However, whether actual results

and developments will conform with our expectations and predictions is subject to a number of risks and uncertainties, including the volatility of oil and natural gas

prices, our success in discovering, estimating, and developing oil and natural gas reserves, the availability and terms of capital, our timely execution of hedge

transactions, credit conditions of global capital markets, changes in economic conditions, regulatory changes and other factors, many of which are beyond our

control.

We refer you to the discussion of risk factors in Part I, Item 1A – “Risk Factors” of our Annual Report on Form 10-K for the year ended December 31, 2016 and in

comparable “Risk Factors” sections of our Quarterly Reports on Form 10-Q filed after such Form 10-K. All of the forward-looking statements made in this

presentation are qualified by these cautionary statements. The actual results or developments anticipated may not be realized or, even if substantially realized, they

may not have the expected consequences to or effects on our company or our business or operations. Such statements are not guarantees of future performance

and actual results or developments may differ materially from those projected in the forward-looking statements. We undertake no obligation to update or revise any

forward-looking statements.

The SEC permits oil and natural gas companies, in their filings with the SEC, to disclose only proved, probable and possible reserves, as each is defined by the SEC.

At times we use the terms "EUR" (estimated ultimate recovery) and “recoverable reserves” that the SEC’s guidelines prohibit us from including in filings with the SEC.

These estimates are by their nature more speculative than estimates of proved, probable or possible reserves and, accordingly, are subject to substantially greater

risk of being actually realized by the company. For a discussion of the company’s proved reserves, as calculated under curren t SEC rules, we refer you to the

company’s amended Annual Report on Form 10-K referenced above, which is available on our website at www.sandridgeenergy.com and at the SEC’s website at

www.sec.gov.

1

Forward Looking Statement

www.sandridgeenergy.com

SandRidge EnergyWith a strong balance sheet, we have built a portfolio of three project areas with competitive project IRRs and significant location

inventories. Investment will continue with the development of both our NW STACK and North Park Niobrara oil projects and high-

graded harvest of our Mississippian position, with total company oil production turning the corner in late 2017.

2 www.sandridgeenergy.com

• $563MM of liquidity

including $145MM cash1

• Moderate level of outspend

• Protect the balance sheet

• High-graded harvest

• Cash flow generation

• Continued cost reductions

• Well design innovation

• 50% of 2017 D&C Capex

• Expands drilling inventory

• Dominant acreage position

held by production or unit

• Multiple benches and tighter

spacing upsides

• >80% oil resource

• 50% of 2017 D&C Capex

• Meramec & Osage

• 70k net acres in 3 counties

‐ Major, Woodward &

Garfield Counties

• Increased oil exposure

(1) Cash balance as of July 31st

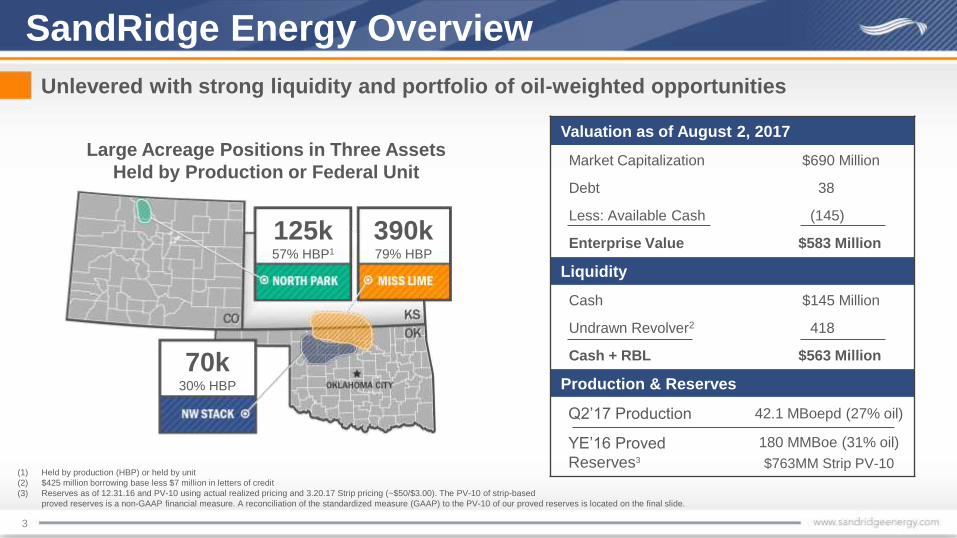

Valuation as of August 2, 2017

Market Capitalization $690 Million

Debt 38

Less: Available Cash (145)

Enterprise Value $583 Million

Liquidity

Cash $145 Million

Undrawn Revolver2 418

Cash + RBL $563 Million

Production & Reserves

Q2’17 Production 42.1 MBoepd (27% oil)

YE’16 Proved

Reserves3

180 MMBoe (31% oil)

$763MM Strip PV-10

3

SandRidge Energy Overview

Unlevered with strong liquidity and portfolio of oil-weighted opportunities

(1) Held by production (HBP) or held by unit

(2) $425 million borrowing base less $7 million in letters of credit

(3) Reserves as of 12.31.16 and PV-10 using actual realized pricing and 3.20.17 Strip pricing (~$50/$3.00). The PV-10 of strip-based

proved reserves is a non-GAAP financial measure. A reconciliation of the standardized measure (GAAP) to the PV-10 of our proved reserves is located on the final slide.

390k79% HBP

125k57% HBP1

70k30% HBP

Large Acreage Positions in Three Assets

Held by Production or Federal Unit

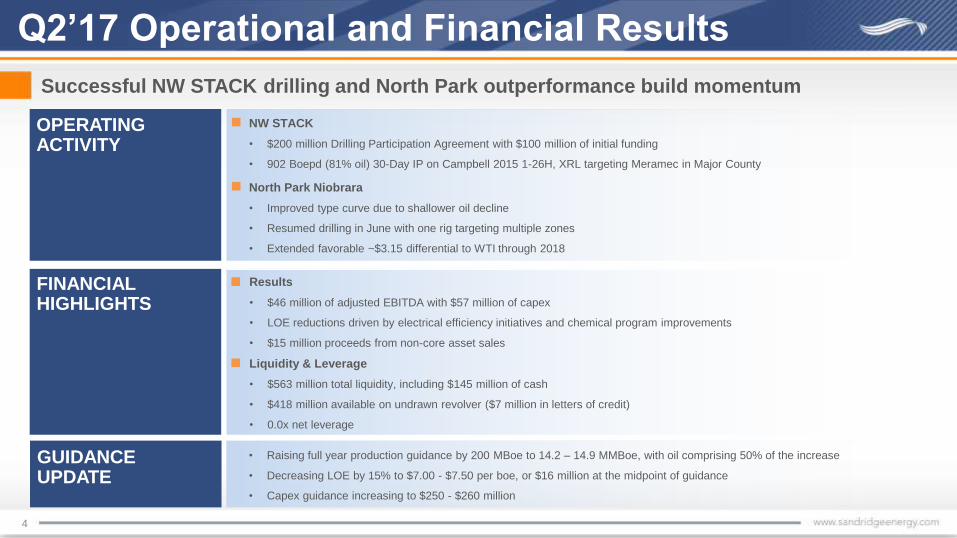

NW STACK

• $200 million Drilling Participation Agreement with $100 million of initial funding

• 902 Boepd (81% oil) 30-Day IP on Campbell 2015 1-26H, XRL targeting Meramec in Major County

4

Q2’17 Operational and Financial Results

GUIDANCE UPDATE

Successful NW STACK drilling and North Park outperformance build momentum

FINANCIAL HIGHLIGHTS

North Park Niobrara

• Improved type curve due to shallower oil decline

• Resumed drilling in June with one rig targeting multiple zones

• Extended favorable ~$3.15 differential to WTI through 2018

Results

• $46 million of adjusted EBITDA with $57 million of capex

• LOE reductions driven by electrical efficiency initiatives and chemical program improvements

• $15 million proceeds from non-core asset sales

Liquidity & Leverage

• $563 million total liquidity, including $145 million of cash

• $418 million available on undrawn revolver ($7 million in letters of credit)

• 0.0x net leverage

• Raising full year production guidance by 200 MBoe to 14.2 – 14.9 MMBoe, with oil comprising 50% of the increase

• Decreasing LOE by 15% to $7.00 - $7.50 per boe, or $16 million at the midpoint of guidance

• Capex guidance increasing to $250 - $260 million

OPERATING ACTIVITY

5

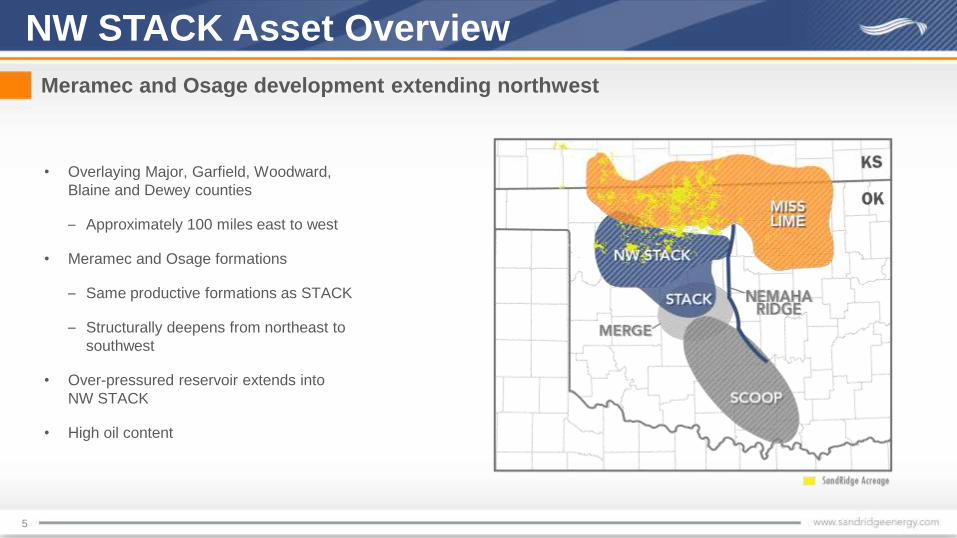

NW STACK Asset Overview

Meramec and Osage development extending northwest

• Overlaying Major, Garfield, Woodward,

Blaine and Dewey counties

– Approximately 100 miles east to west

• Meramec and Osage formations

– Same productive formations as STACK

– Structurally deepens from northeast to

southwest

• Over-pressured reservoir extends into

NW STACK

• High oil content

6

NW STACK Primary Targets

Meramec 5,800’-12,400’ TVD

• Interbedded shales, sands, and

carbonates

• Thickness from 50’-160’

• Matrix porosity development in limey-sand

zones with some secondary fracturing

Osage 5,900’-12,500’ TVD

• Limestone and cherts

• Thickness from 450’-1,300’

• Natural fracturing enhances productivity

7

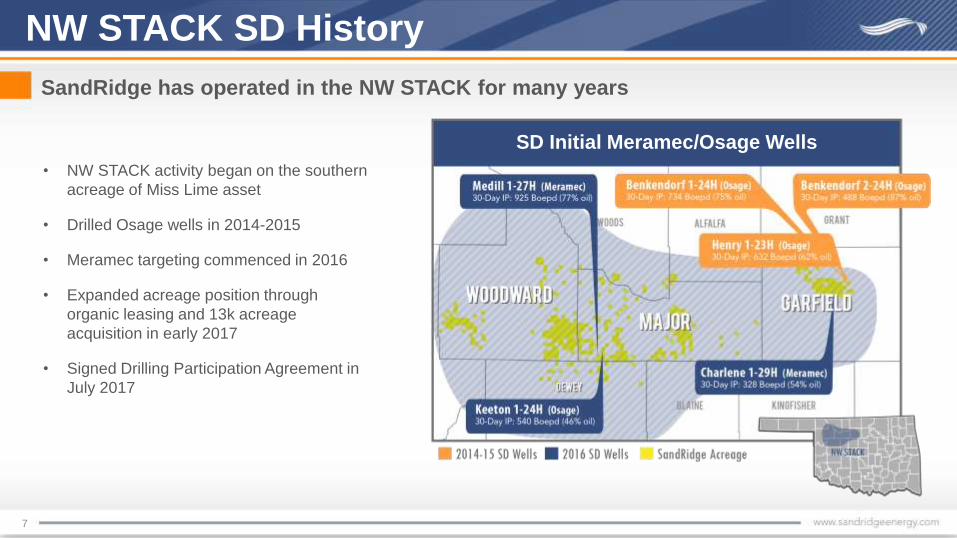

NW STACK SD History

SandRidge has operated in the NW STACK for many years

• NW STACK activity began on the southern

acreage of Miss Lime asset

• Drilled Osage wells in 2014-2015

• Meramec targeting commenced in 2016

• Expanded acreage position through

organic leasing and 13k acreage

acquisition in early 2017

• Signed Drilling Participation Agreement in

July 2017

SD Initial Meramec/Osage Wells

8

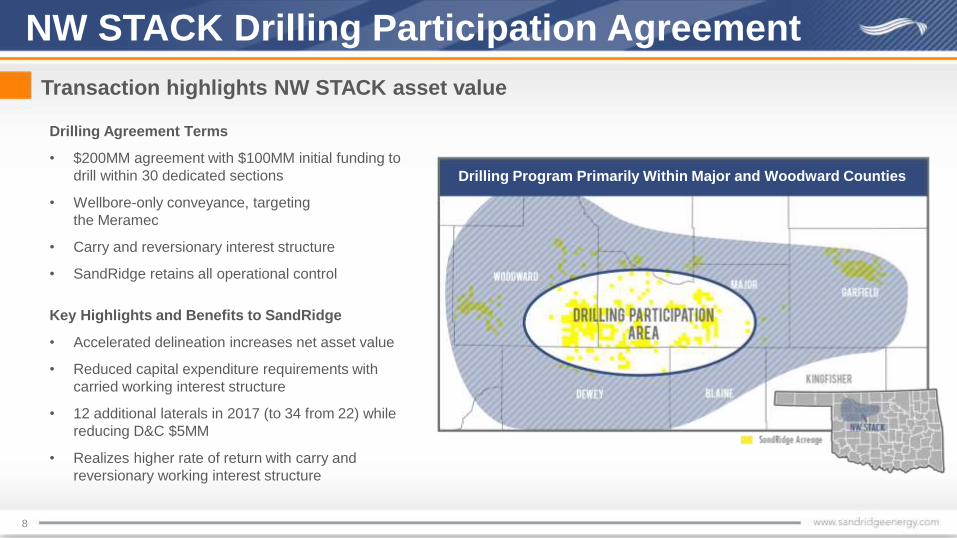

NW STACK Drilling Participation Agreement

Transaction highlights NW STACK asset value

Drilling Agreement Terms

• $200MM agreement with $100MM initial funding to

drill within 30 dedicated sections

• Wellbore-only conveyance, targeting

the Meramec

• Carry and reversionary interest structure

• SandRidge retains all operational control

Key Highlights and Benefits to SandRidge

• Accelerated delineation increases net asset value

• Reduced capital expenditure requirements with

carried working interest structure

• 12 additional laterals in 2017 (to 34 from 22) while

reducing D&C $5MM

• Realizes higher rate of return with carry and

reversionary working interest structure

Drilling Program Primarily Within Major and Woodward Counties

9

NW STACK Activity

Delineating NW STACK alongside other operators

20 Rigs from 12 OperatorsSandRidge Activity

• 2017 D&C capex of $60-65MM

• 34 laterals planned for 2017

• Targeting $3.3MM D&C per lateral

• Drilling Meramec formation

• Retaining Osage as upside

• Optimizing completion designs

• Coring and 3D seismic enhance

reservoir characterization

10

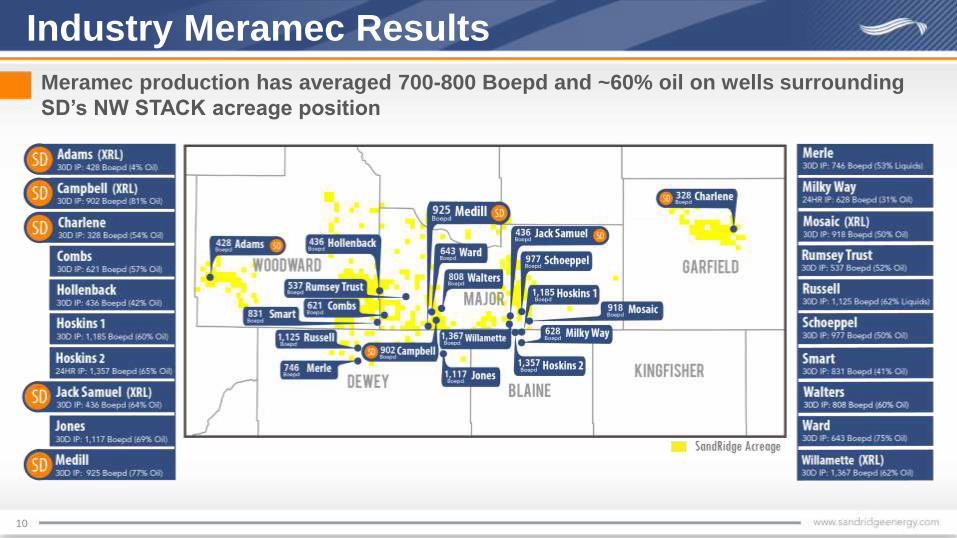

Industry Meramec Results

Meramec production has averaged 700-800 Boepd and ~60% oil on wells surrounding

SD’s NW STACK acreage position

11

Industry Osage Results

Osage production has averaged 700-800 Boepd and ~40% oil on wells surrounding

SD’s NW STACK acreage position

12

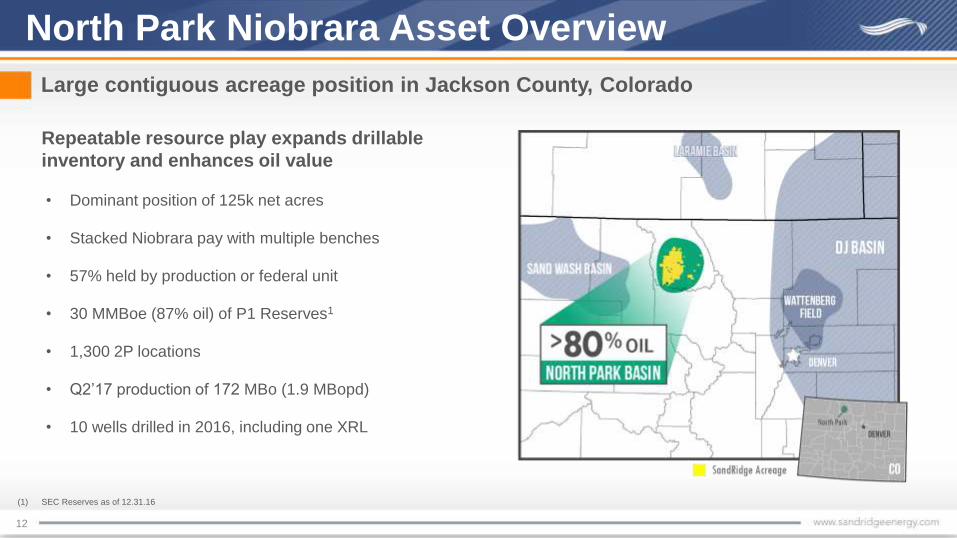

• Dominant position of 125k net acres

• Stacked Niobrara pay with multiple benches

• 57% held by production or federal unit

• 30 MMBoe (87% oil) of P1 Reserves1

• 1,300 2P locations

• Q2’17 production of 172 MBo (1.9 MBopd)

• 10 wells drilled in 2016, including one XRL

North Park Niobrara Asset Overview

Large contiguous acreage position in Jackson County, Colorado

Repeatable resource play expands drillable

inventory and enhances oil value

(1) SEC Reserves as of 12.31.16

13

North Park Niobrara Analogous to Wattenberg

North Park’s gross Niobrara interval ranges from 460 - 500 feet thick

14

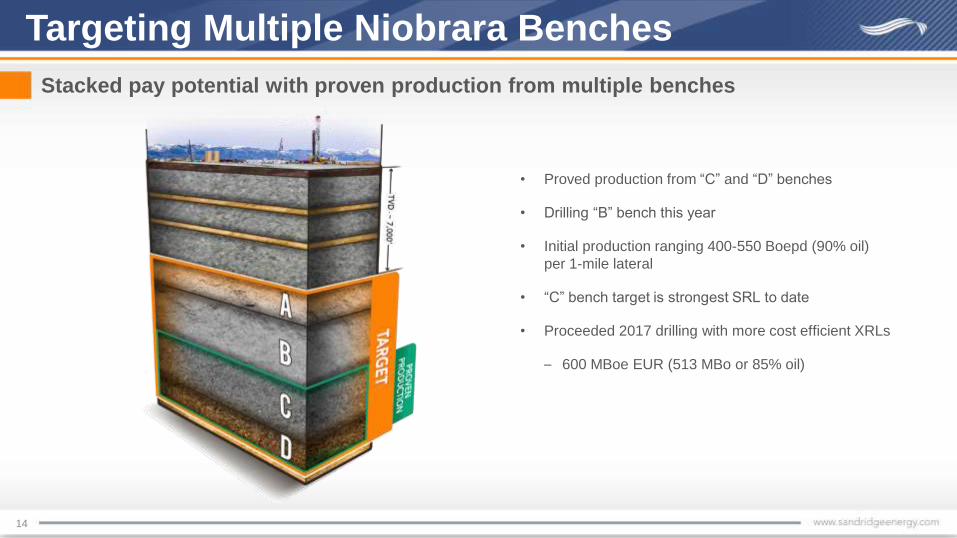

Targeting Multiple Niobrara Benches

Stacked pay potential with proven production from multiple benches

• Proved production from “C” and “D” benches

• Drilling “B” bench this year

• Initial production ranging 400-550 Boepd (90% oil)

per 1-mile lateral

• “C” bench target is strongest SRL to date

• Proceeded 2017 drilling with more cost efficient XRLs

– 600 MBoe EUR (513 MBo or 85% oil)

RABBITEARS UNIT

24k Net Acres

SURPRISE UNIT22k Net Acres

PETERSON RIDGE UNIT

22k Net Acres

15

North Park Geology Update

Increased subsurface understanding with additional seismic and core analysis

• Integrating 3D seismic for well placement and targeting

– 117 square miles of seismic from three surveys

including 61 square miles of 3D seismic obtained this

year

• Core collection and analysis will aide in stimulation, well

spacing and reservoir characterization

– Over 500 feet of core being collected in 2017

– Previous core of 300 feet collected in 2007

16

North Park Niobrara Uniform Thickness

Consistent thickness across entire acreage position

17

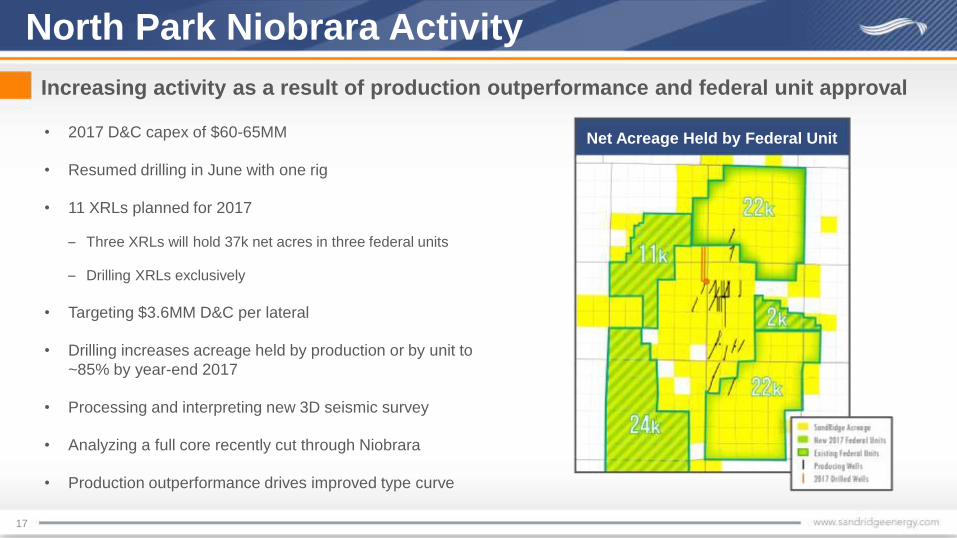

• 2017 D&C capex of $60-65MM

• Resumed drilling in June with one rig

• 11 XRLs planned for 2017

– Three XRLs will hold 37k net acres in three federal units

– Drilling XRLs exclusively

• Targeting $3.6MM D&C per lateral

• Drilling increases acreage held by production or by unit to

~85% by year-end 2017

• Processing and interpreting new 3D seismic survey

• Analyzing a full core recently cut through Niobrara

• Production outperformance drives improved type curve

North Park Niobrara Activity

Increasing activity as a result of production outperformance and federal unit approval

Net Acreage Held by Federal Unit

18

2016 Niobrara Program Success

2016 Drilling Results

Note: 30-Day IP rates shown above

10 wells drilled in 2016, outperforming type curve

Lowered costs, optimized completions, drilled first XRL and “C” bench wells

19

Optimized completions from 2016 drilling program

Niobrara Oil Production

DAILY OIL RATE CUMULATIVE OIL

20

Niobrara Type Curve Update

Jet Pump Installed

Shallower decline vs initial estimates drive value improvement

Type Curve Cumulative Oil Production (MBo)

Initial Current

90 Days 66 66

180 Days 103 113

365 Days 139 164

50 Years 513 513

XRL TYPE CURVE UPLIFT IMPROVED ECONOMICS

• PV-10 increase of ~$1MM

• IRR uplift

21

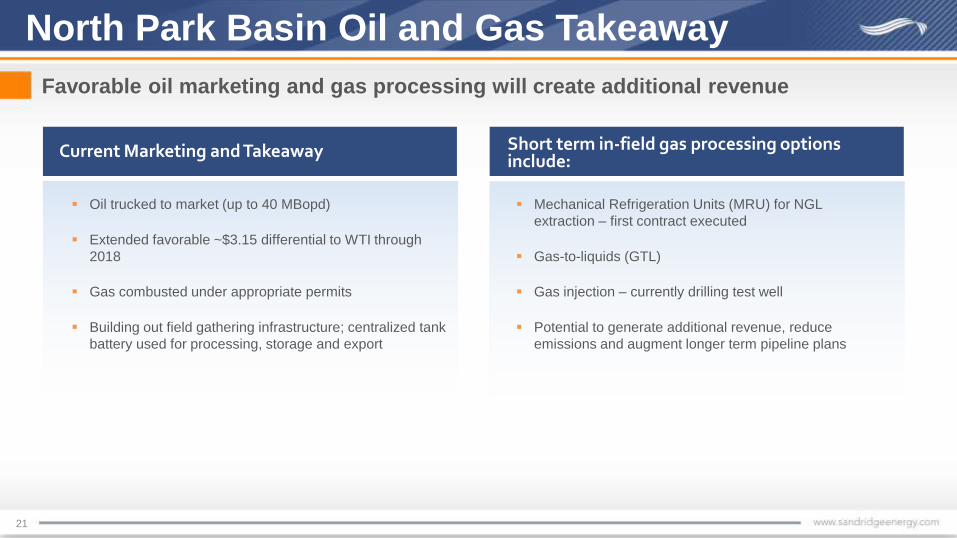

North Park Basin Oil and Gas Takeaway

Favorable oil marketing and gas processing will create additional revenue

Current Marketing and Takeaway Short term in-field gas processing options include:

Mechanical Refrigeration Units (MRU) for NGL

extraction – first contract executed

Gas-to-liquids (GTL)

Gas injection – currently drilling test well

Potential to generate additional revenue, reduce

emissions and augment longer term pipeline plans

Oil trucked to market (up to 40 MBopd)

Extended favorable ~$3.15 differential to WTI through

2018

Gas combusted under appropriate permits

Building out field gathering infrastructure; centralized tank

battery used for processing, storage and export

APPENDIX

22

23

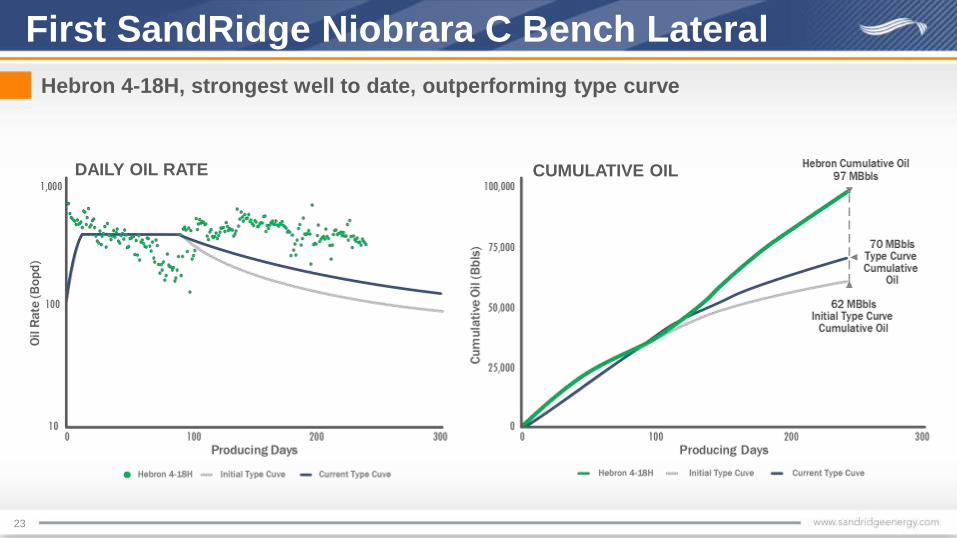

First SandRidge Niobrara C Bench Lateral

Hebron 4-18H, strongest well to date, outperforming type curve

DAILY OIL RATE CUMULATIVE OIL

Jet Pump Installed

24

First SandRidge Niobrara XRL

Castle 1-17H, in line with current type curve

DAILY OIL RATE CUMULATIVE OILJet Pump Installed

Jet Pump Installed

25

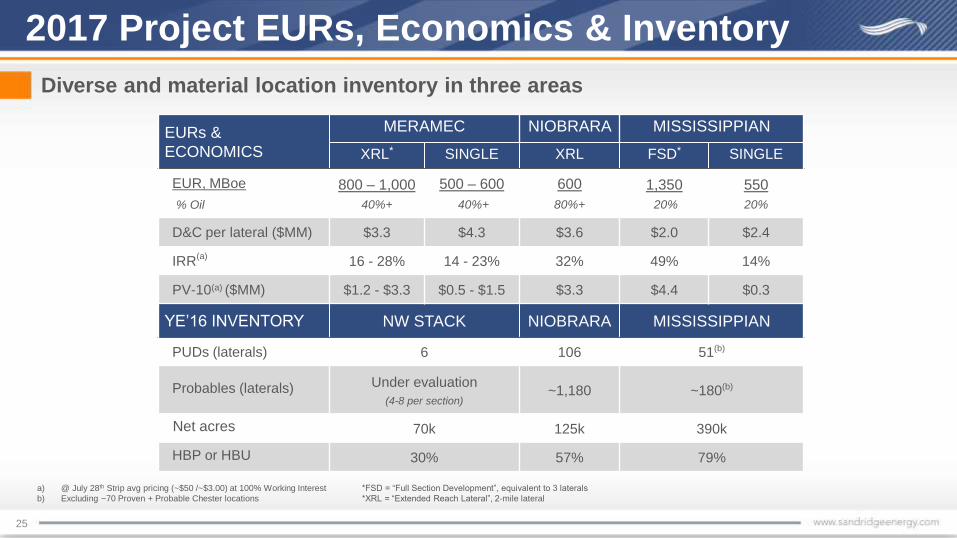

2017 Project EURs, Economics & Inventory

EURs &

ECONOMICS

MERAMEC NIOBRARA MISSISSIPPIAN

XRL* SINGLE XRL FSD* SINGLE

EUR, MBoe

% Oil

800 – 1,000

40%+

500 – 600

40%+

600

80%+

1,350

20%

550

20%

D&C per lateral ($MM) $3.3 $4.3 $3.6 $2.0 $2.4

IRR(a)

16 - 28% 14 - 23% 32% 49% 14%

PV-10(a) ($MM) $1.2 - $3.3 $0.5 - $1.5 $3.3 $4.4 $0.3

YE’16 INVENTORY NW STACK NIOBRARA MISSISSIPPIAN

PUDs (laterals) 6 106 51(b)

Probables (laterals) Under evaluation

(4-8 per section)~1,180 ~180(b)

Net acres 70k 125k 390k

HBP or HBU 30% 57% 79%

a) @ July 28th Strip avg pricing (~$50 /~$3.00) at 100% Working Interest

b) Excluding ~70 Proven + Probable Chester locations

Diverse and material location inventory in three areas

*FSD = “Full Section Development”, equivalent to 3 laterals

*XRL = “Extended Reach Lateral”, 2-mile lateral

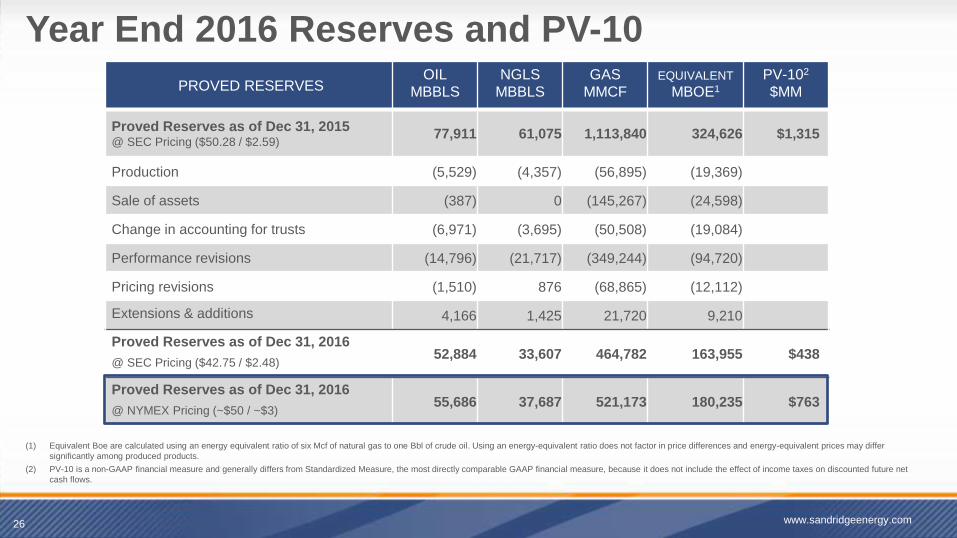

Year End 2016 Reserves and PV-10

26

PROVED RESERVES OIL

MBBLS

NGLS

MBBLS

GAS

MMCFEQUIVALENT

MBOE1

PV-102

$MM

Proved Reserves as of Dec 31, 2015@ SEC Pricing ($50.28 / $2.59)

77,911 61,075 1,113,840 324,626 $1,315_

Production (5,529) (4,357) (56,895) (19,369)

Sale of assets (387) 0 (145,267) (24,598)

Change in accounting for trusts (6,971) (3,695) (50,508) (19,084)

Performance revisions (14,796) (21,717) (349,244) (94,720)

Pricing revisions (1,510) 876 (68,865) (12,112)

Extensions & additions 4,166 1,425 21,720 9,210

Proved Reserves as of Dec 31, 2016

@ SEC Pricing ($42.75 / $2.48)52,884 33,607 464,782 163,955 $438_

Proved Reserves as of Dec 31, 2016

@ NYMEX Pricing (~$50 / ~$3)55,686 37,687 521,173 180,235 $763_

(1) Equivalent Boe are calculated using an energy equivalent ratio of six Mcf of natural gas to one Bbl of crude oil. Using an energy-equivalent ratio does not factor in price differences and energy-equivalent prices may differ

significantly among produced products.

(2) PV-10 is a non-GAAP financial measure and generally differs from Standardized Measure, the most directly comparable GAAP financial measure, because it does not include the effect of income taxes on discounted future net

cash flows.

www.sandridgeenergy.com

Four Quarters of Trailing Actuals

27

ACTUALS

PRODUCTION Q3’16 Q4’16 Q1’17 Q2’17

Oil (MMBbls) 1.3 1.2 1.1 1.0

Natural Gas Liquids (MMBbls) 1.1 1.0 0.9 0.9

Total Liquids (MMBbls) 2.4 2.2 2.0 1.9

Natural Gas (Bcf) 13.1 12.8 11.8 11.3

Total (MMBoe) 4.6 4.3 4.0 3.8

Daily Oil Equivalent (MBoepd) 49.6 47.2 44.2 42.1

PRICING REALIZATIONS

Oil (differential below WTI) $2.11 $2.28 $2.71 $2.26

NGLs (realized % of WTI) 31% 30% 32% 29%

Gas (differential below Henry Hub)1 $0.54 $0.93 $0.96 $1.11

COSTS PER BOE

LOE1 $8.68 $5.76 $6.28 $6.59

Adj. G&A – Cash2 $3.88 $3.08 $3.43 $3.70

% OF NET REVENUE

Severance Taxes 2.3% 2.7% 3.2% 3.1%

(1) Q4’16 marks beginning of accounting policy change to book gas transportation fee as a net from revenue, rather than a lease operating expense

(2) Adjusted G&A - Cash is a non-GAAP financial measure as it excludes from G&A non-cash compensation, severance, bad debt allowance, and other non-recurring items. The most directly comparable GAAP measure for Adjusted

G&A - cash is General and Administrative Expense. Information to reconcile this non-GAAP financial measure to the most directly comparable GAAP financial measure is not available at this time, as management is unable to

forecast the excluded items for future periods.

www.sandridgeenergy.com

Updated 2017 Guidance

28

CAPEX GUIDANCE ($MM) UPDATED PREVIOUS

D&C $140 - $150 $109 - $119

Other E&P 108 99

Total Exploration and Production $248 - $258 $208 - $218

General Corporate 2 2

Total Capital Expenditures $250 - $260 $210 - $220

TOTAL COMPANY PRODUCTION

Oil (MMBbls) 4.1 – 4.3 4.0 – 4.2

Natural Gas Liquids (MMBbls) 3.1 – 3.3 3.0 – 3.2

Total Liquids (MMBbls) 7.2 – 7.6 7.0 – 7.4

Natural Gas (Bcf) 42.0 – 43.5 42.0 – 43.5

Total (MMBoe) 14.2 - 14.9 14.0 - 14.7

www.sandridgeenergy.com

PRICING REALIZATIONS UPDATED PREVIOUS

Oil (differential below WTI) $2.75 $2.75

NGLs (realized % of WTI) 28% 26%

Gas (differential below Henry Hub) $1.00 $1.00

COSTS PER BOE

LOE $7.00 - $7.50 $8.00 - $9.00

Adj. G&A – Cash1 $4.25 - $4.50 $4.25 - $4.50

% OF NET REVENUE

Severance Taxes 3.00% - 3.25% 2.75% - 3.00%

(1) Adjusted G&A - Cash is a non-GAAP financial measure as it excludes from G&A non-cash compensation, severance, bad debt allowance, and other non-recurring items. The most directly comparable GAAP measure for Adjusted

G&A - cash is General and Administrative Expense. Information to reconcile this non-GAAP financial measure to the most directly comparable GAAP financial measure is not available at this time, as management is unable to

forecast the excluded items for future periods.

2017 Capital Expenditures Detail

29

CAPEX GUIDANCE ($MM) UPDATED PREVIOUS

Mid-Continent D&C $60 - $65 $65 - $70

North Park D&C 60 - 65 20 - 25

Other - D&C1 20 24

Total Drilling & Completion $140 - $150 $109 - $119

OTHER E&P

Land, G&G and Seismic $46 $40

Infrastructure2 18 7

Workovers 30 37

Capitalized G&A and Interest 14 15

Total Other E&P $108 $99

NON E&P

General Corporate 2 2

Total Capital Expenditures

(excl. A&D and P&A)$250 - $260 $210 - $220

GROSS LATERAL SPUDS UPDATED PREVIOUS

Mid-Continent3 34 22

North Park 22 6

Total Laterals 56 28

NET LATERAL SPUDS

Mid-Continent3 17 17

North Park 22 6

Total Laterals 39 23

(1) 2016 Carryover, Coring, Non-Op and SWD

(2) Infrastructure: Production Facilities, Pipeline ROW and Electrical

(3) Updated lateral count includes 12 Drilling Participation Agreement laterals

www.sandridgeenergy.com

30

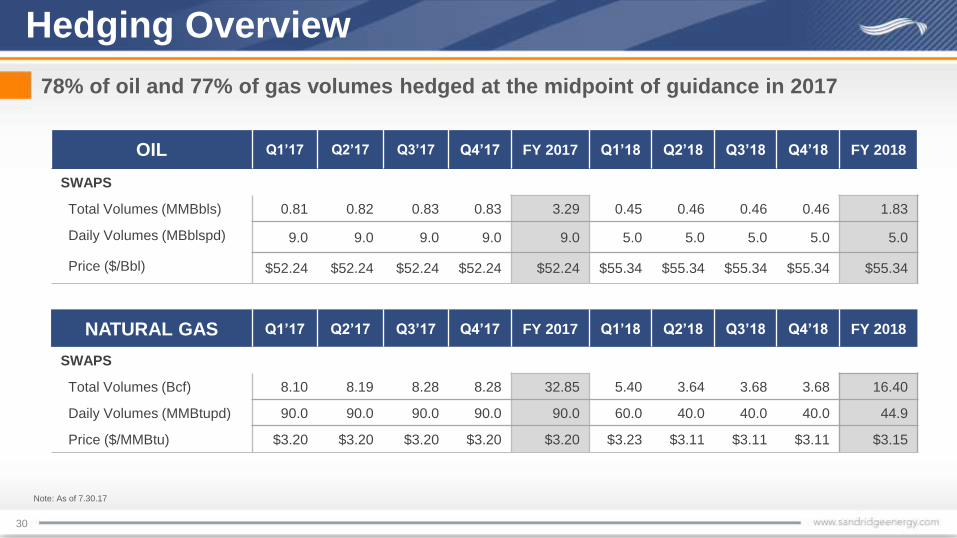

Hedging Overview

78% of oil and 77% of gas volumes hedged at the midpoint of guidance in 2017

OIL Q1’17 Q2’17 Q3’17 Q4’17 FY 2017 Q1’18 Q2’18 Q3’18 Q4’18 FY 2018

SWAPS

Total Volumes (MMBbls) 0.81 0.82 0.83 0.83 3.29 0.45 0.46 0.46 0.46 1.83

Daily Volumes (MBblspd) 9.0 9.0 9.0 9.0 9.0 5.0 5.0 5.0 5.0 5.0

Price ($/Bbl) $52.24 $52.24 $52.24 $52.24 $52.24 $55.34 $55.34 $55.34 $55.34 $55.34

NATURAL GAS Q1’17 Q2’17 Q3’17 Q4’17 FY 2017 Q1’18 Q2’18 Q3’18 Q4’18 FY 2018

SWAPS

Total Volumes (Bcf) 8.10 8.19 8.28 8.28 32.85 5.40 3.64 3.68 3.68 16.40

Daily Volumes (MMBtupd) 90.0 90.0 90.0 90.0 90.0 60.0 40.0 40.0 40.0 44.9

Price ($/MMBtu) $3.20 $3.20 $3.20 $3.20 $3.20 $3.23 $3.11 $3.11 $3.11 $3.15

Note: As of 7.30.17

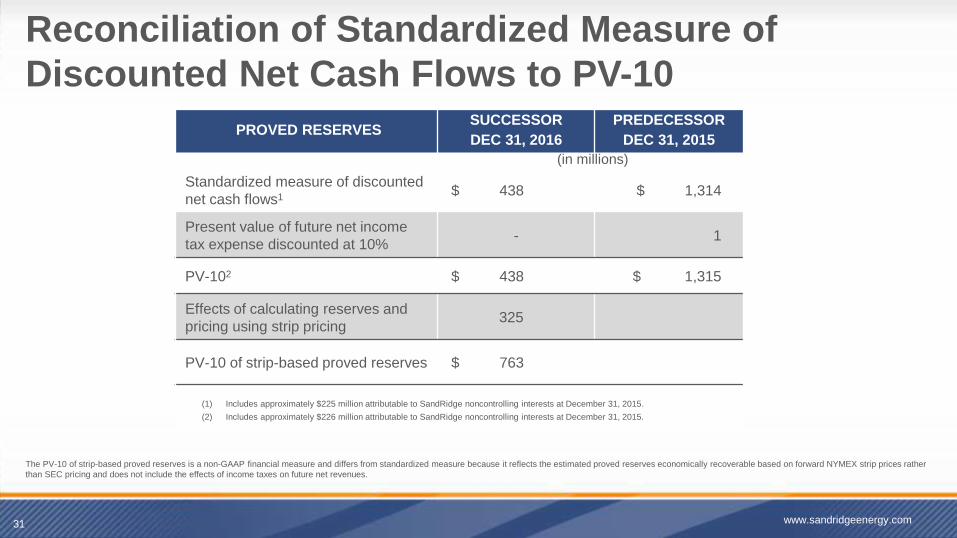

Reconciliation of Standardized Measure of

Discounted Net Cash Flows to PV-10

31 www.sandridgeenergy.com

The PV-10 of strip-based proved reserves is a non-GAAP financial measure and differs from standardized measure because it reflects the estimated proved reserves economically recoverable based on forward NYMEX strip prices rather

than SEC pricing and does not include the effects of income taxes on future net revenues.

PROVED RESERVES SUCCESSOR

DEC 31, 2016

PREDECESSOR

DEC 31, 2015

((in millions)

Standardized measure of discounted

net cash flows1$ 438 $ 1,314

Present value of future net income

tax expense discounted at 10%- 1

PV-102 $ 438 $ 1,315

Effects of calculating reserves and

pricing using strip pricing325

PV-10 of strip-based proved reserves $ 763

(1) Includes approximately $225 million attributable to SandRidge noncontrolling interests at December 31, 2015.

(2) Includes approximately $226 million attributable to SandRidge noncontrolling interests at December 31, 2015.