fin303 vicentiu covrig 1 financial statements and cash flow (chapter 3)

TRANSCRIPT

FIN303Vicentiu Covrig

1

Financial statements and cash flow

(chapter 3)

FIN303Vicentiu Covrig

2

Sources of Information

Annual reports Wall Street Journal Internet

- www.yahoo.com- www.smartmoney.com

Mergent online SEC

- EDGAR- 10K & 10Q reports

FIN303Vicentiu Covrig

3

The Annual Report Balance sheet – provides a snapshot of a firm’s

financial position at one point in time. Income statement – summarizes a firm’s

revenues and expenses over a given period of time.

Statement of cash flows – reports the impact of a firm’s activities on cash flows over a given period of time.

Statement of stockholders’ equity – shows how much of the firm’s earnings were retained, rather than paid out as dividends.

FIN303Vicentiu Covrig

4

Overview of D’Leon Inc. Snack food company that underwent major

expansion in 2010. So far, expansion results have been

unsatisfactory.- Company’s cash position is weak.- Suppliers are being paid late.- Bank has threatened to cut off credit.

Board of Directors has ordered that changes must be made!

FIN303Vicentiu Covrig

5

Balance Sheet: Assets2011

7,282632,160

1,287,3601,926,8021,202,950

263,160939,790

2,866,592

201057,600

351,200715,200

1,124,000491,000146,200344,800

1,468,800

CashA/RInventories

Total CAGross FALess: Dep.

Net FATotal Assets

FIN303Vicentiu Covrig

6

Balance Sheet: Liabilities and Equity

Accts payableNotes payableAccruals

Total CLLong-term debtCommon stockRetained earnings

Total EquityTotal L & E

2011524,160636,808489,600

1,650,568723,432460,000

32,592492,592

2,866,592

2010145,600200,000136,000481,600323,432460,000203,768663,768

1,468,800

FIN303Vicentiu Covrig

7

Income Statement 2011 2010 Sales $6,034,000 $3,432,000 COGS 5,528,000 2,864,000

Other expenses 519,988 358,672 Total oper. costs excl.

deprec. & amort. $6,047,988

$3,222,672

Depreciation and amortization 116,960 18,900 EBIT ($ 130,948) $ 190,428

Interest expense 136,012 43,828 EBT ($ 266,960) $ 146,600 Taxes (106,784) 58,640 Net income ($ 160,176) $ 87,960

FIN303Vicentiu Covrig

8

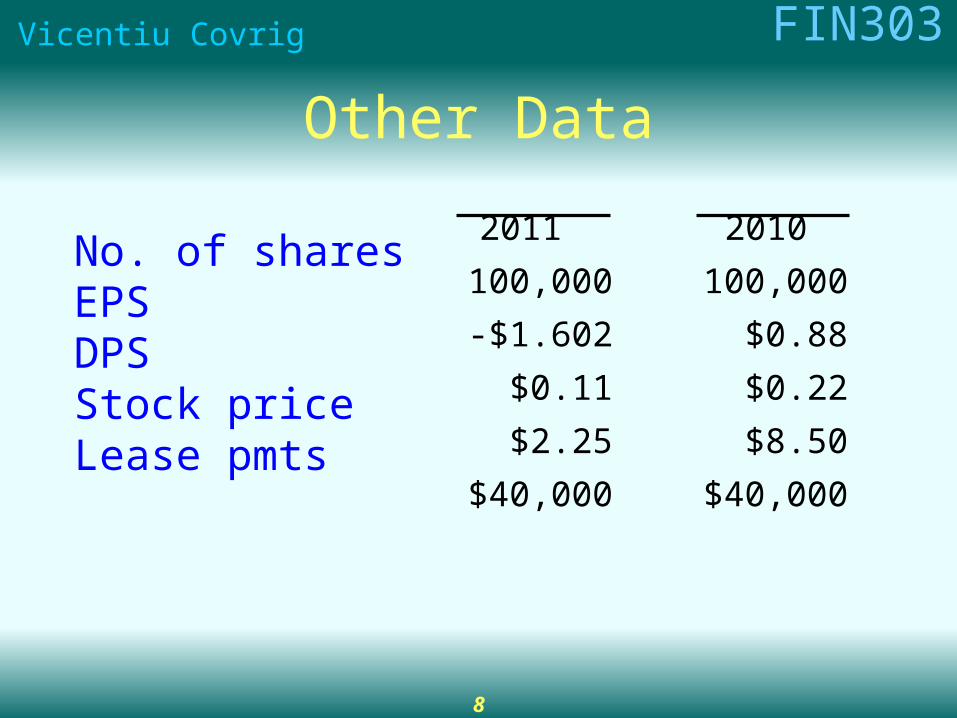

Other Data

No. of sharesEPSDPSStock priceLease pmts

2011

100,000

-$1.602

$0.11

$2.25

$40,000

2010

100,000

$0.88

$0.22

$8.50

$40,000

FIN303Vicentiu Covrig

9

Statement of Stockholders’ Equity (2011)

Total Common Stock Retained Stockholders’ Shares Amount Earnings Equity

Balances, 12/31/10 100,000 $460,000 $203,768 $663,768 2011 Net income (160,176) Cash dividends (11,000) Addition (subtraction)

to retained earnings (171,176) Balances, 12/31/11 100,000 $460,000 $ 32,592 $492,592

FIN303Vicentiu Covrig

10

Did the expansion create additional after-tax operating income?AT operating income = EBIT(1 – Tax

rate)

AT operating income11 = -$130,948(1 – 0.4)

= -$130,948(0.6)

= -$78,569

AT operating income10 = $114,257

FIN303Vicentiu Covrig

11

What effect did the expansion have on net operating working capital?

400,842$NOWC

042,913$)808,636$568,650,1($

)360,287,1$160,632$282,7($NOWC

payableNotes

sliabilitieCurrent

assetsCurrentNOWC

10

11

FIN303Vicentiu Covrig

12

Assessment of the Expansion’s Effect on Operations

SalesAT oper. inc.

NOWCNet income

2011

$6,034,000-78,569

913,042-160,176

2010

$3,432,000114,257

842,40087,960

FIN303Vicentiu Covrig

13

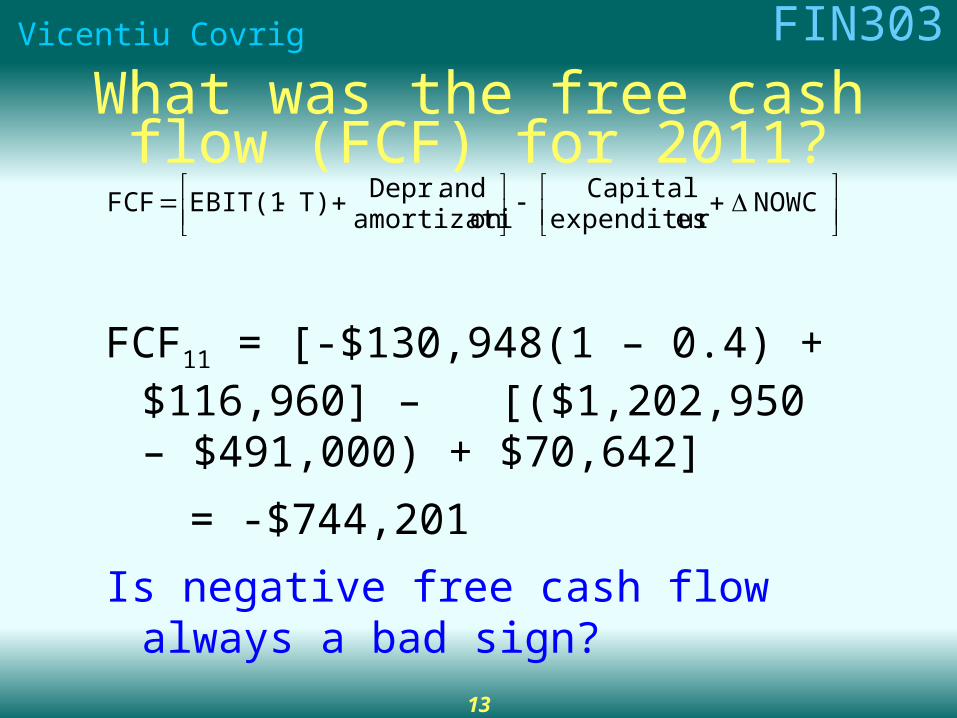

What was the free cash flow (FCF) for 2011?

NOWC

esexpenditurCapital

onamortizatiand Depr. T)EBIT(1 FCF

FCF11 = [-$130,948(1 – 0.4) + $116,960] – [($1,202,950 – $491,000) + $70,642]

= -$744,201

Is negative free cash flow always a bad sign?

FIN303Vicentiu Covrig

14

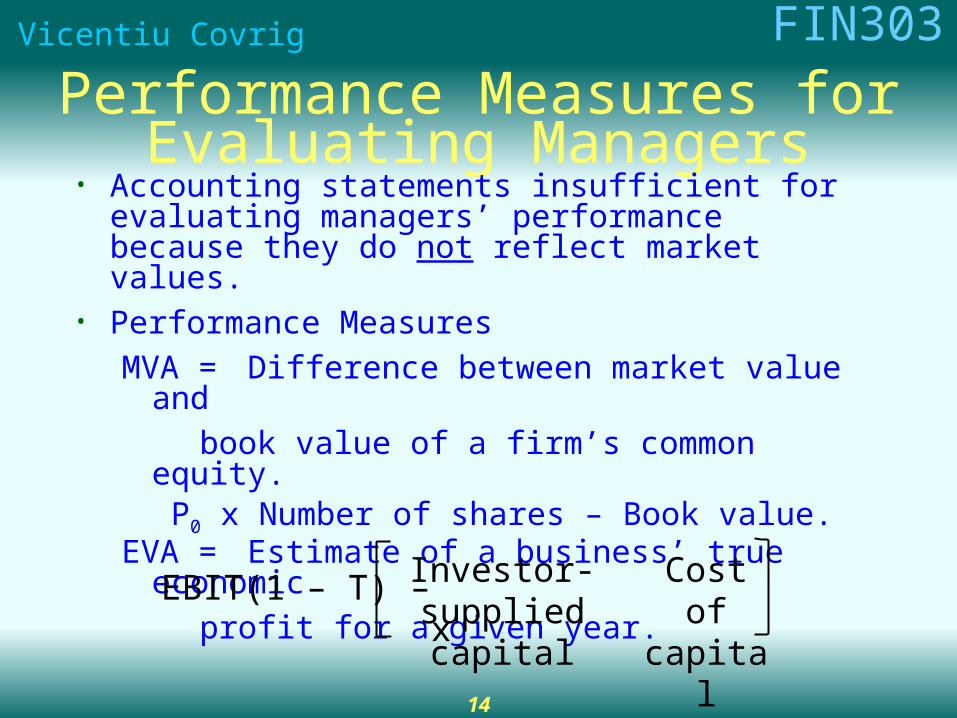

Performance Measures for Evaluating Managers

• Accounting statements insufficient for evaluating managers’ performance because they do not reflect market values.

• Performance Measures

MVA = Difference between market value and

book value of a firm’s common equity.P0 x Number of shares – Book value.

EVA = Estimate of a business’ true economic

profit for a given year.

Investor-supplied capital

Cost of capital

EBIT(1 – T) – x

FIN303Vicentiu Covrig

15

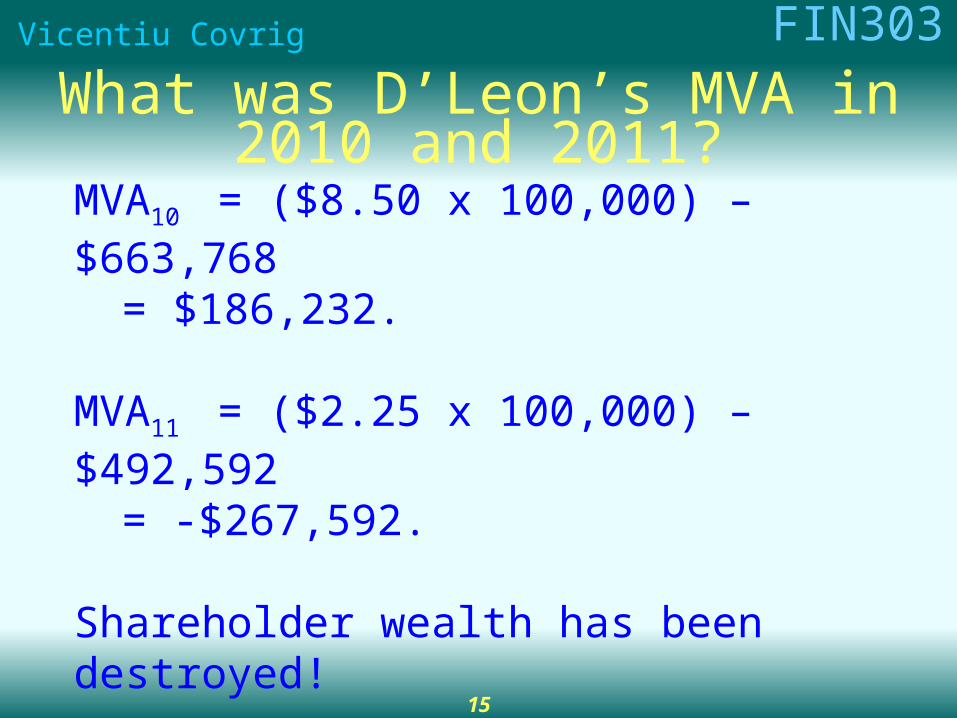

What was D’Leon’s MVA in 2010 and 2011?

MVA10 = ($8.50 x 100,000) – $663,768= $186,232.

MVA11 = ($2.25 x 100,000) – $492,592= -$267,592.

Shareholder wealth has been destroyed!

FIN303Vicentiu Covrig

16

What is the relationship between EVA and MVA?

If EVA is positive, then AT operating income > cost of capital needed to produce that income.

Positive EVA on annual basis helps to ensure MVA is positive.

MVA is applicable to entire firm, while EVA can be calculated on a divisional basis as well.

FIN303Vicentiu Covrig

17

Federal Income Tax System

FIN303Vicentiu Covrig

18

Corporate and Personal Taxes Both have a progressive structure (the

higher the income, the higher the marginal tax rate).

Corporations- Rates begin at 15% and rise to 35% for

corporations with income over $10 million, although corporations with income between $15 million and $18.33 million pay a marginal tax rate of 38%.

- Also subject to state tax (around 5%).

FIN303Vicentiu Covrig

19

Tax treatment of various uses and sources of funds

Interest paid – tax deductible for corporations (paid out of pre-tax income), but usually not for individuals (interest on home loans being the exception).

Interest earned – usually fully taxable (an exception being interest from a (muni”).

Dividends paid – paid out of after-tax income. Dividends received – taxed as ordinary income for

individuals (“double taxation”). A portion of dividends received by corporations is tax excludable, in order to avoid “triple taxation”.

FIN303Vicentiu Covrig

20

Tax Treatment of Various Uses and Sources of Funds

Dividends received: most investors pay 15% taxes through 2012. The rate is scheduled to rise after 2012. - Investors in the 10% or 15% tax bracket pay 0% on

qualified dividends through 2012. - Dividends are paid out of net income which has

already been taxed at the corporate level, this is a form of “double taxation”.

- A portion of dividends received by corporations is tax excludable, in order to avoid “triple taxation.”

FIN303Vicentiu Covrig

21

Learning objectives Annual report; Balance sheet; Income Statement items you see on the slides You DO NOT need to know the Statement of Cash Flows (3.4) Free Cash Flow MVA and EVA Taxes All the numerical problems on the slides and recommended below from end of

chapter You need to know to do After Tax Income problems and remember the formula

from page 81 Questions: ST-1, ST-2 a,b,c,d; 3-1 to 3-5; 3-73-9,3-10 Problems: 3-1, 3-2, 3-3, 3-5, 3-8, 3-9, 3-12