fin 351: lecture 6 introduction to risk and return where does the discount rate come from?

TRANSCRIPT

FIN 351: lecture 6

Introduction to Risk and Return

Where does the discount rate come from?

Today’s learning objective

Introduction to risk• How to measure investment performance

• Rates of Return

• 73 Years of Capital Market History

• Measuring risk and risk premium

• Risk & Portfolio Diversification

Two types of risk • How to measure systematic risk

CAPM

How to measure the performance of your investment

Suppose you buy one share of IBM at $74 this year and sell it at the expected price of $102. IBM pays a dividend of $1.25 for your investment• What profit do you expect to make for your

investment?

• What profit do you expect to make for one dollar investment?

Solution

Profit in total =102-74+1.25=$29.25 Profit per one dollar=29.25/74=0.395 or

39.5%

Rates of Return

39.5%or .395=

= ReturnPercentage 741.25 + 28

Price Share Initial Dividend +Gain Capital =return of rate expectedor Return Percetage

CostProfit =return of rate expectedor Return Percetage

Rates of Return

D iv id e n d Y ie ld = D iv id e n d In i t ia l S h a re P r ic e

C a p i t a l G a in Y ie ld = C a p i t a l G a inIn i t i a l S h a r e P r i c e

yieldgain capital yield Dividend =return Percentage

Rates of Return

%1.7or 017.74

1.25= Yield Dividend

%37.8or 378.74

28= YieldGain Capital

Rates of Return

Nominal vs. Real

rateinflation + 1rate nominal + 1=rate real+1

37.3% rate real

373.1=rate real+1.016 + 1.395 + 1

Suppose that the inflation rate is1.6%

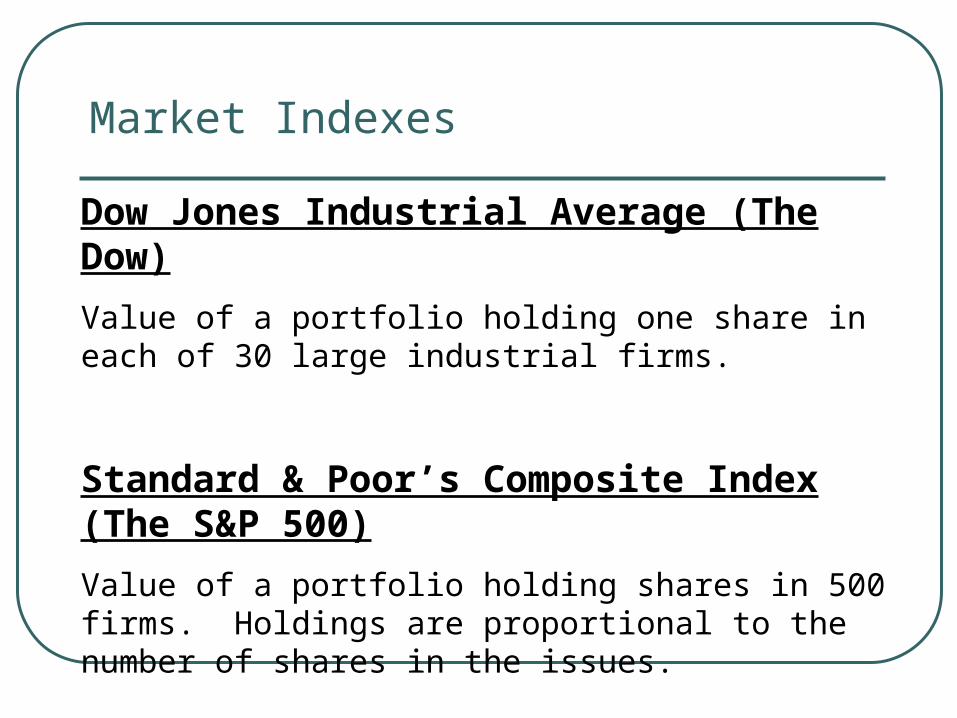

Market Indexes

Dow Jones Industrial Average (The Dow)

Value of a portfolio holding one share in each of 30 large industrial firms.

Standard & Poor’s Composite Index (The S&P 500)

Value of a portfolio holding shares in 500 firms. Holdings are proportional to the number of shares in the issues.

The performance of $0.1 investment

0.1

10

1000

1930

1940

1950

1960

1970

1980

1990

1998

Common StocksLong T-BondsT-Bills

Volatility of portfolios

-60

-40

-20

0

20

40

60

26 30 35 40 45 50 55 60 65 70 75 80 85 90 95

Common Stocks

Long T-Bonds

T-Bills

Volatility

Year

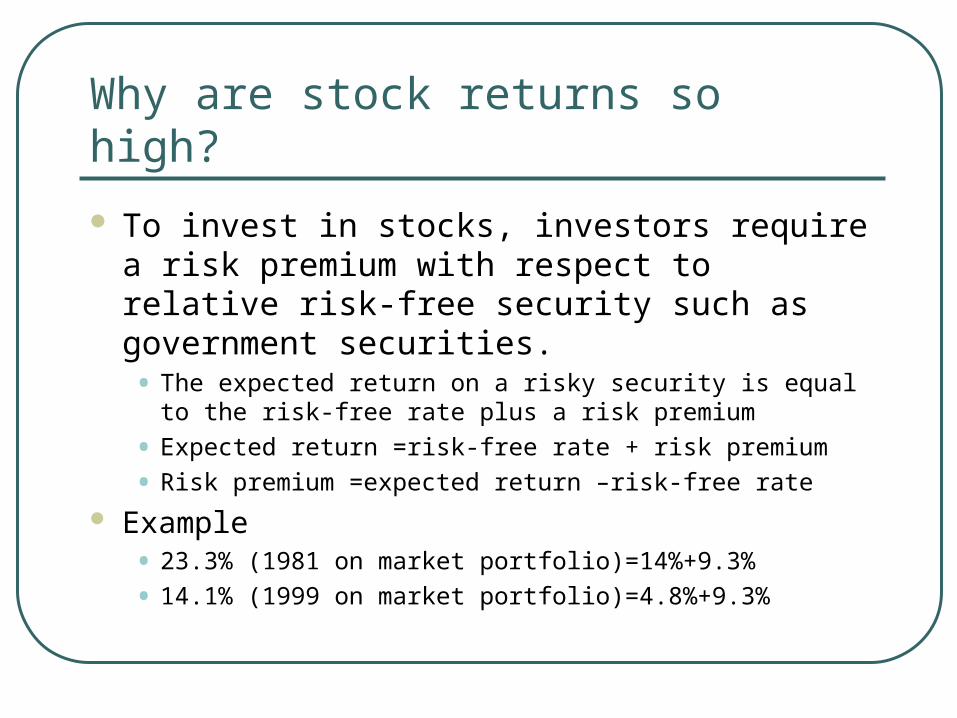

Why are stock returns so high?

To invest in stocks, investors require a risk premium with respect to relative risk-free security such as government securities.• The expected return on a risky security is equal to the risk-

free rate plus a risk premium

• Expected return =risk-free rate + risk premium

• Risk premium =expected return –risk-free rate

Example• 23.3% (1981 on market portfolio)=14%+9.3%

• 14.1% (1999 on market portfolio)=4.8%+9.3%

How to Measure Risk

We can use the variance or the standard deviation of the expected rate of return to measure risk.

Variance or standard deviation measure weighted average of squared deviation of each observation from the mean.

Some formula

Suppose that there are N states, then the expected rate of return (mean) is

The variance of the rate of return is

The standard deviation

iN

iirprEr

1)(

2

1

2 )(*)( rrprVarN

iii

2/1

1

2)()(

N

iii rrprVar

Example of risk

Stock A has the following returns depending on the state of the economy next year as follows:

State of economy Probability of the state Return rate

Good

Average

Bad

0.6

0.3

0.1

20%

10%

-5%

Measure risk (continue)

First, calculate the mean return or the expected rate of return. Here N=3 (three states)

Expected rate of return is r-bar= p1*r1+p2*r2+p3*r3=0.6*0.2+0.3*0.1+0.1*(-0.05)

=14.5% The variance of return is

p1*(r1- r-bar)2+p2*(r2- r-bar)2+p3*(r3-r-bar)2

=0.003325 The standard deviation is 0.0577=5.7%

Two types of risks

Unique Risk - Risk factors affecting only that firm. Also called “firm-level risk.”

Market Risk - Economy-wide sources of risk that affect the overall stock market. Also called “systematic risk.”

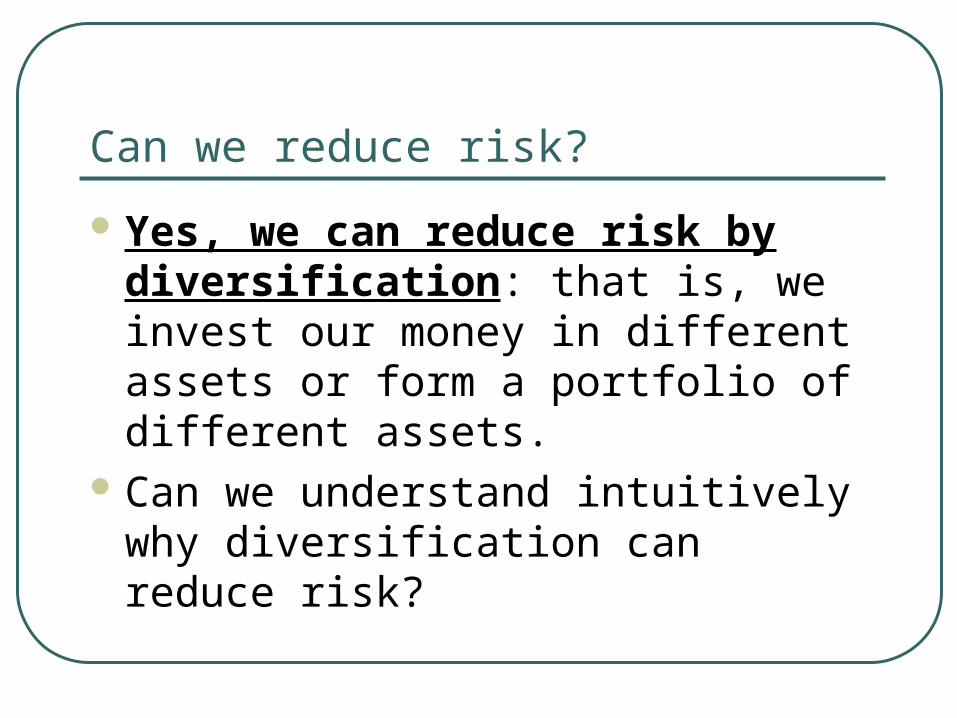

Can we reduce risk?

Yes, we can reduce risk by diversification: that is, we invest our money in different assets or form a portfolio of different assets.

Can we understand intuitively why diversification can reduce risk?

Portfolio weights

Let W be the total money invested in a portfolio, a set of assets.

Let xi be the proportion of total wealth invested in asset i. Then xi is called portfolio weight for asset i. The sum of portfolio weights for all the assets in the portfolio is 1, that is,

11

N

iix

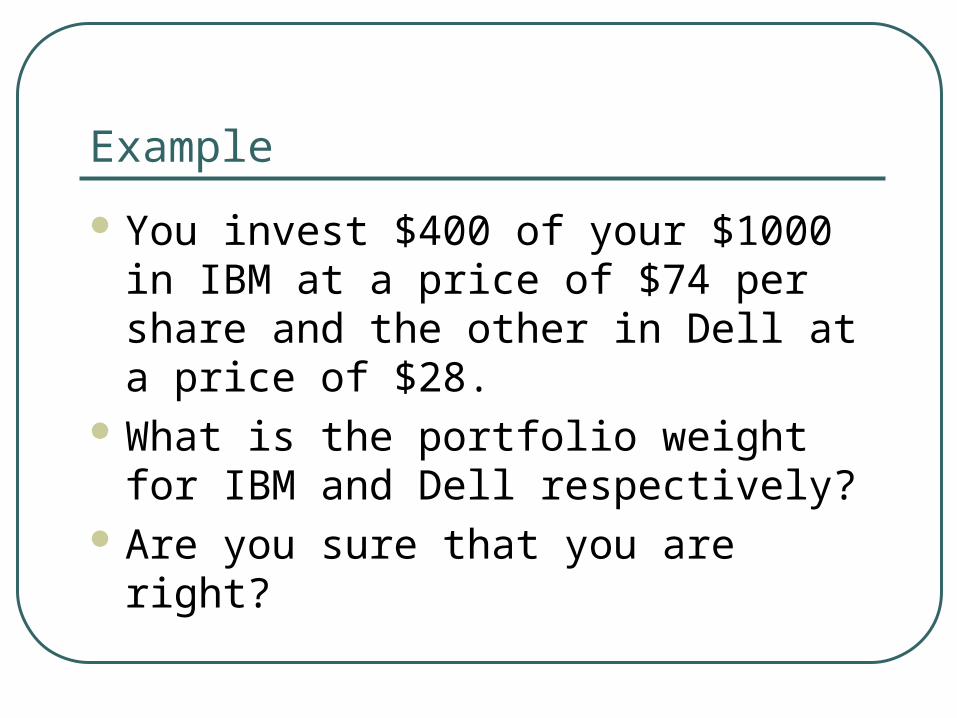

Example

You invest $400 of your $1000 in IBM at a price of $74 per share and the other in Dell at a price of $28.

What is the portfolio weight for IBM and Dell respectively?

Are you sure that you are right?

Solution

xIBM=400/1000=0.4

xDell=600/1000=0.6

xIBM+xDell=1

Some formula for portfolios

The return of a portfolio is the weighted average of

returns of the stocks in the portfolio. That is,

The expected return of a portfolio is the weighted average of expected returns of the stocks in the

portfolio. That is, i

N

iirxR

1

iN

iirxR

1

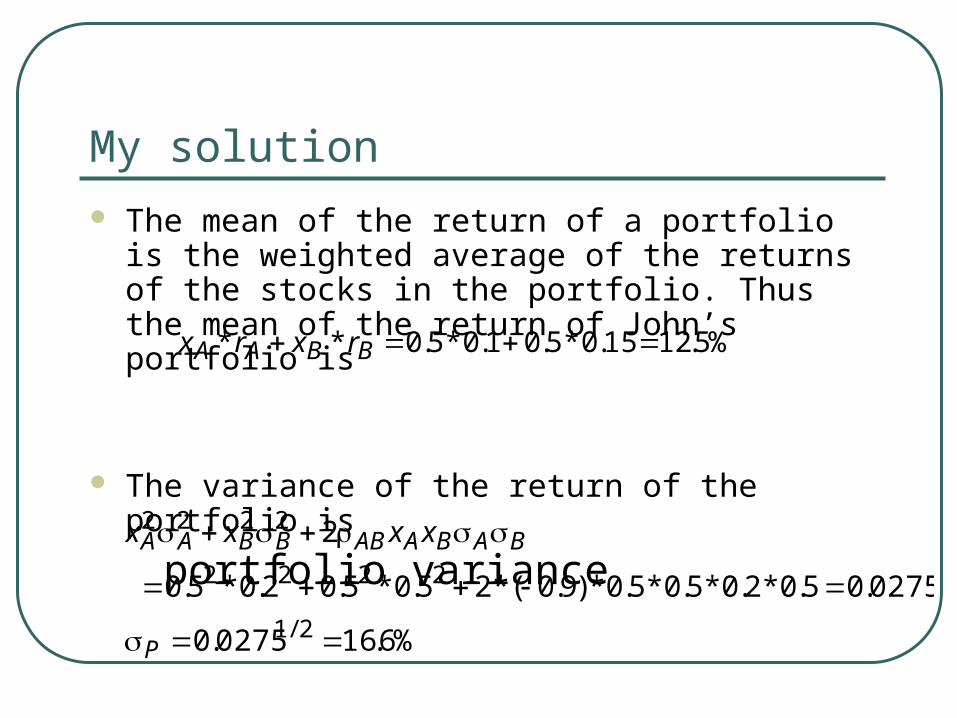

Risk and Diversification (example)

John puts his money half in stock A and half in stock B, as shown in the following.

What is the mean and variance of the return of John’s portfolio?

5.0,5.0,9.0%,50

%20%,15%,10

BAABB

ABA

xx

rr

My solution The mean of the return of a portfolio is the weighted

average of the returns of the stocks in the portfolio. Thus the mean of the return of John’s portfolio is

The variance of the return of the portfolio is

portfolio variance

%5.1215.0*5.01.0*5.0** BBAA rxrx

%6.160275.0

0275.05.0*2.0*5.0*5.0*)9.0(*25.0*5.02.0*5.0

2

2/1

2222

2222

P

BABAABBBAA xxxx

Risk and Diversification

05 10 15

Number of Securities

Po

rtfo

lio

sta

nd

ard

dev

iati

on

Market risk

Uniquerisk

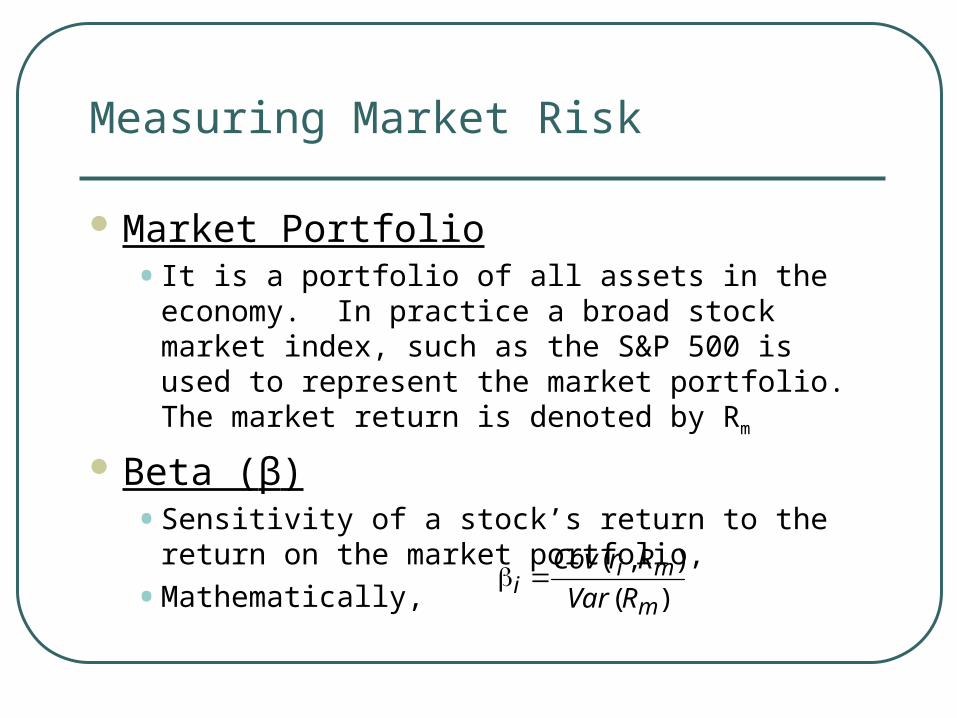

Measuring Market Risk

Market Portfolio • It is a portfolio of all assets in the economy. In

practice a broad stock market index, such as the S&P 500 is used to represent the market portfolio. The market return is denoted by Rm

Beta (β) • Sensitivity of a stock’s return to the return on the

market portfolio,

• Mathematically, )(

),(

m

mii RVar

RrCov

An intuitive example for Beta

Turbo Charged Seafood has the following % returns on its stock, relative to the listed changes in the % return on the market portfolio. The beta of Turbo Charged Seafood can be derived from this information.

Measuring Market Risk (example, continue)

Month Market Return % Turbo Return %

1 + 1 + 0.8

2 + 1 + 1.8

3 + 1 - 0.2

4 - 1 - 1.8

5 - 1 + 0.2

6 - 1 - 0.8

Measuring Market Risk (continue)

When the market was up 1%, Turbo average % change was +0.8% When the market was down 1%, Turbo average % change was -0.8% The average change of 1.6 % (-0.8 to 0.8) divided by the 2% (-1.0 to 1.0) change in the market produces a beta of 0.8. β=1.6/2=0.8

Another example

Suppose we have following information:

State Market Stock A Stock B

bad

good

-8% -10%

38%

-6%

24%32%

a. What is the beta for each stock?

b. What is the expected return for each stock if each scenario is equally likely?

c. What is the expected return for each stock if the probability for good economy is 20%?

Solution

a.

b.

c.

09.0)06.0(*5.024.0*5.0

14.0)1.0(*5.038.0*5.0

B

A

r

r

75.040.0

30.0

)08.0(32.0

)06.0(24.0

2.140.0

48.0

)08.0(32.0

)1.0(38.0

B

A

0)06.0(*8.024.0*2.0

004.0)1.0(*8.038.0*2.0

B

A

r

r

Portfolio Betas

Diversification reduces unique risk, but not market risk.

The beta of a portfolio will be an weighted average of the betas of the securities in the portfolio.

What is the beta of the market portfolio?

What is the beta of the risk-free security?

in

iip x

1

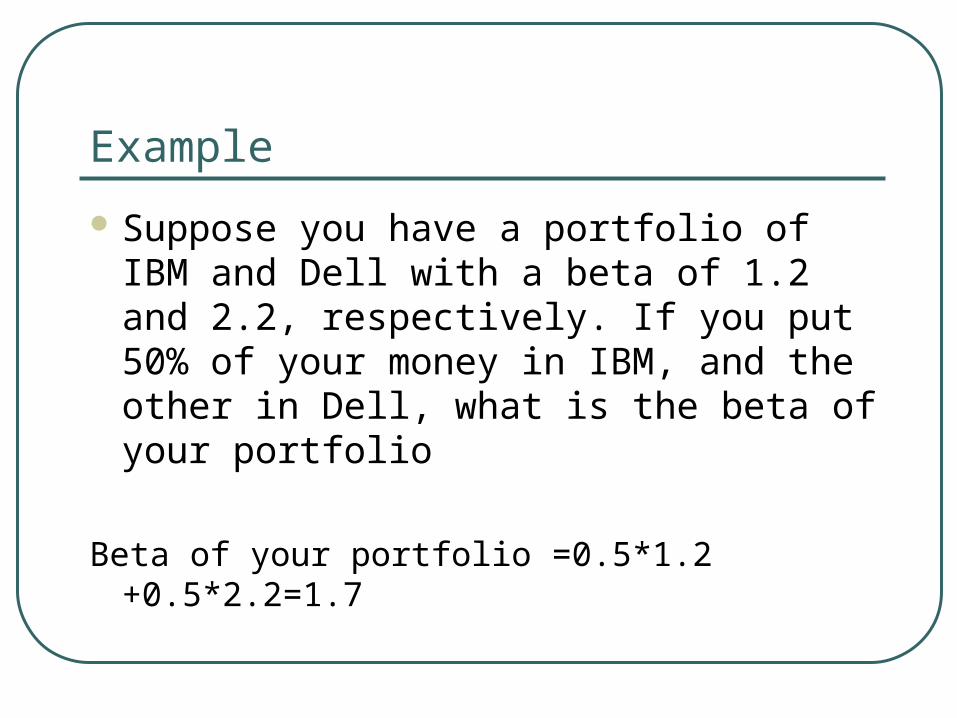

Example

Suppose you have a portfolio of IBM and Dell with a beta of 1.2 and 2.2, respectively. If you put 50% of your money in IBM, and the other in Dell, what is the beta of your portfolio

Beta of your portfolio =0.5*1.2 +0.5*2.2=1.7

Market risk and risk premium

Risk premium for bearing market risk• The difference between the expected return

required by investors and the risk-free asset.

• Example, the expected return on IBM is 10%, the risk-free rate is 5%, and the risk premium is 10% -5%=5%

• If a security ( an individual security or a portfolio) has market or systematic risk, risk-averse investors will require a risk premium.

CAPM (Capital Asset Pricing Model)

The risk premium on each security is proportional to the market risk premium and the beta of the security.• That is,

)( fmifi rRrr

portfoliomarkettheforpremiumriskrR

iurityforpremiumriskrr

fm

fi

sec

Security market line

0

2

4

6

8

10

12

14

16

0 0.2 0.4 0.6 0.8 1 1.2

Beta

Exp

ecte

d R

etu

rn (

%)

. The graphic representation of CAPM in

the expected return and Beta plane

rf

Security Market Line

Rm