fin 351: lecture 4 stock and its valuation the application of the present value concept

TRANSCRIPT

FIN 351: lecture 4

Stock and Its Valuation

The application of the present value concept

Today’s agenda

Review what we have learned in the last lecture

Stock and its valuation• Some terminology about a stock

• Value a stock

• Simple dividend discount model

• Dividend growth model

What have we learned in the last lecture

Bond? How to value a bond? Yield to maturity and spot rates? Term structure of interest rates and yield

curve?

Some questions

A bond that pays annual coupon is issued with a coupon rate of 4%, maturity of 30 years, and a yield to maturity of 7%, what will be the rate of return if you buy it now and hold it for one year and the yield to maturity in the next year will be 8%?

What is a stock?

A (common) stock is a financial claim that has the following properties:• A right to receive dividends after creditors

have been paid

• A right to vote at the annual meeting

• A limited liability security

Dividends are periodic cash flows to share holders

Stocks & Stock Market

Primary Market - Place where the sale of new stock first occurs.

Secondary market - market in which already issued securities are traded by investors.

P/E ratio - Price per share divided by earnings per share.

Dividend yield- Dividends per share divided by the stock price

Values of stocks

Book Value of a stock- the value according to the balance sheet in the accounting.

Market Value of a stock – the value according to the traded stock prices in the market.

Stock valuation

When you want to invest in a stock, you are very interested in whether the stock is under-priced or over-priced. To find out, you need to value the stock

Two simple approaches to price a stock• Simple dividend discount model

• Dividend growth model

We will apply these two approaches to real stocks, for example, IBM

Simple dividend discount model: valuing IBM We will first use the dividend discount model to value

the International Business Machine.• What does the company do?

http://finance.yahoo.com/• Symbol “IBM”

• Trades on the NYSE We see price is recently $180

• hit “detailed”

• we see the company is paying $3 dividend per share (we will do an annualized problem for simplicity, here we assume that all the earnings are paid out as dividends)

Valuing IBM (continue)

Let’s suppose IBM is going to continue paying $3 dividend per share, forever

We are planning to buy the stock and hold it forever Of course, we must be able to draw the cash flow

diagram

PV???

$3 $3$3 $3 $3 $3

Yr1 Yr2 Yr3 Yr4 Yr5 Time=infinity

Valuing IBM (continue)

How much is IBM worth?• Suppose the required rate of return by the

investor is 10%.

The present value of future dividend cash flows should equal the price of IBM.

30$1.0

31 r

CPV

Valuing IBM (3)

Clearly, the price calculated using this simple model is below the current market price

Why?• we have undervalued the stock

• the market has overvalued the stock Let’s be humble and assume the former

• where did we go wrong?

Valuing IBM (4)

Sensitivity of our answer to discount rate:

Clearly, this is still not the answer

Discount rate Price

7%

8%

9%

11%

$42.9

$37.5

$33.3

$27.27

Valuing IBM (5)

What if the dividend is not constant ? Suppose the dividend were to grow at 4% per

year:• the next dividend will be $3

• in two years we will receive $3.12

• and so on … Can we derive the formula for a growing

perpetuity?• define g ≡ 4% the growth rate

• define C ≡ 3 the dividend received in year one

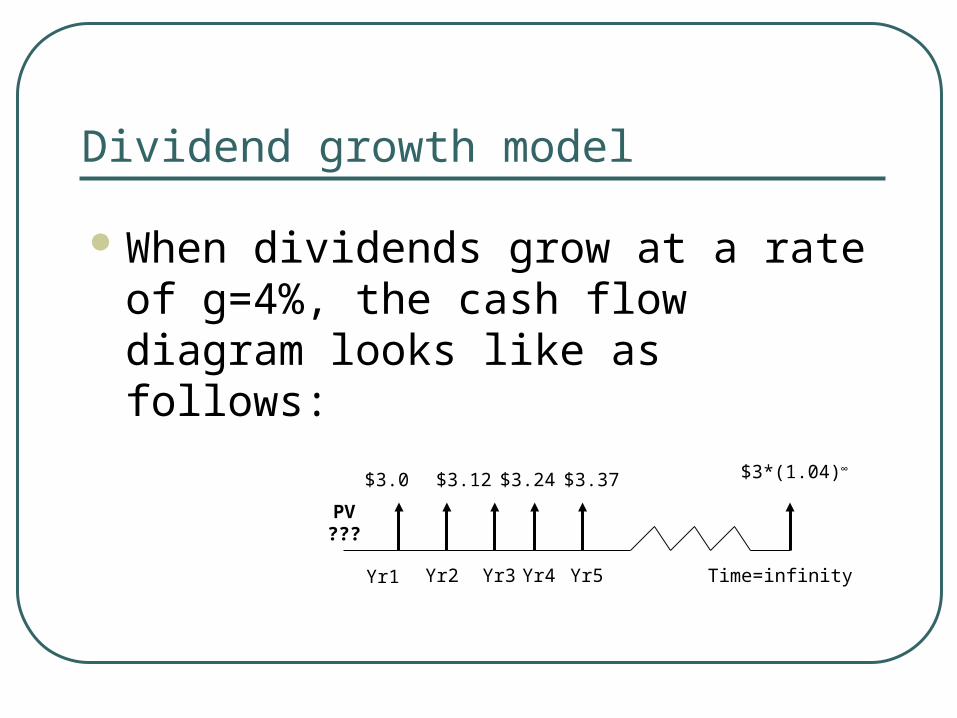

Dividend growth model

When dividends grow at a rate of g=4%, the cash flow diagram looks like as follows:

PV???

Yr1 Yr2 Yr3 Yr4 Yr5 Time=infinity

$3.0 $3*(1.04)∞$3.12 $3.37$3.24

Dividend growth model (2)

Based on the diagram, we have the math equation:

)1(

)1(

)1(

)1(

)1(

)1(1 3

2

2 r

gC

r

gC

r

gCrC

PV

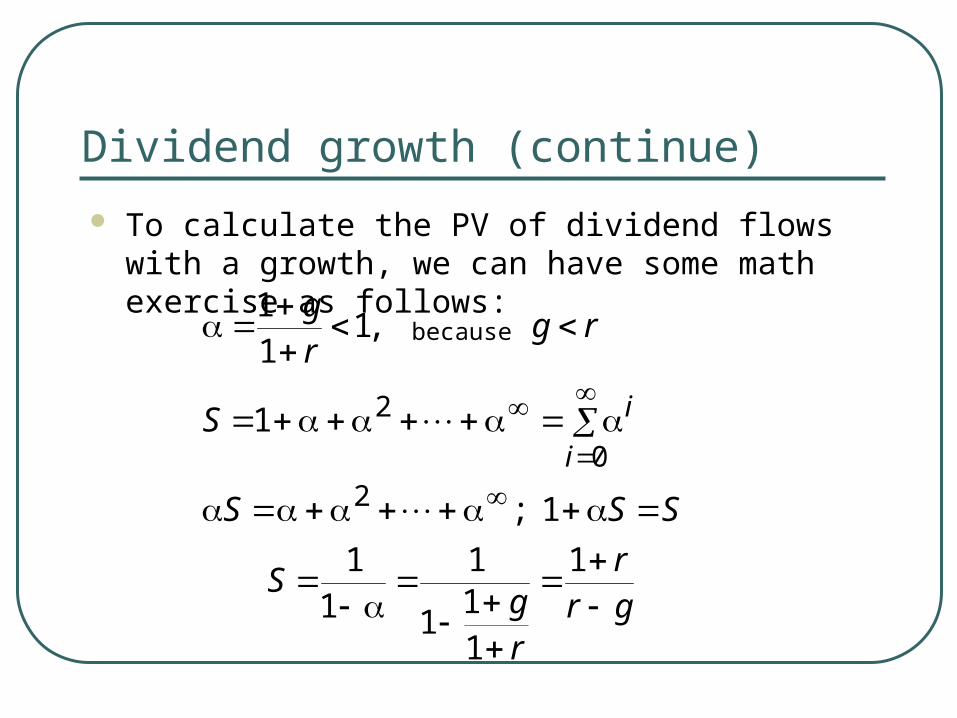

Dividend growth (continue)

To calculate the PV of dividend flows with a growth, we can have some math exercise as follows:

grr

rg

S

SSS

S

rgrg

i

i

1

11

1

11

1

1;

1

,111

20

2

because

Dividend growth (continue)

How to calculate dividend perpetuity with a growth:

grC

grr

rC

SrC

rC

rg

rC

r

grg

rC

r

gC

r

gC

r

CPV

i

i

i

i

11

1111

1

)1(

)1(11

11

)1(

)1(

)1(

)1(

)1(

00

21

Dividend growth model (5) Do you think that this formula makes sense ?

When g increases, what will happen to the stock price?

When r increases, what will happen to the stock price?

When g =0, what happens? When g>r, what will happen to the stock price?

• In order to use the formula, r must be greater than g.

gr

CPV

Back to the valuation of IBM Sensitivity of our answer to growth rate of dividends Next year’s dividend is still $3.0 Discount rate is constant at 10%

Certainly, we are close, but g=5% is reasonable?

Growth rate Stock price

1%

2%

3%

4%

5%

$33.3

$37.5

$50.0

$60.0

$75.0

Sensitivity analysis with respect to discount and growth rates

Discount rate

Dividend Growth rate

1%

2%

3%

4%

5%

5.5%

6% 7% 8% 9% 10% 11% 12%

60

75

75100

60 50 43 38 33 30

273033384350

300

150

600

100

200

150

60 50

75

100

120

43

50

43

43

38

55

3338

46

60

6786

75

60 50

Stock price

Another way of looking at stock valuation

Suppose stock A pays dividend of $3 every year, with a discount rate of 10%. What is the stock price now in the following three cases• (a) hold it for ever

• (b) hold for five years

• (c) hold it for twenty years

Another example

Suppose stock A pays dividend of $3 next year, with a constant dividend growth rate of 5% and a discount rate of 10%. What is the stock price now in the following three cases• (a) hold it for ever

• (b) hold for one year

• (c) hold it for two years

More on the dividend discount model

So far, we have used the dividend cash flows to calculate the stock price.

In the real world, can we apply this formula to figure out the stock prices for all the stocks? How?

How to decide on the growth rate

If a firm chooses to pay a lower dividend, and reinvest the funds, the stock price may increase because future dividends may be higher.

Payout Ratio - Fraction of earnings paid out as dividends

Plowback Ratio - Fraction of earnings retained by the firm.

More on the dividend growth

Growth can be calculated by the return on equity times the plowback ratio

Let g= the dividend growth rate

g = return on equity X plowback ratio

Example

Our company forecasts to pay a $5.00 dividend next year, which represents 100% of its earnings. This will provide investors with a 12% expected return. Instead, we decide to plow back 40% of the earnings at the firm’s current return on equity of 20%. What is the value of the stock before and after the plowback decision?

Solution

Our company forecasts to pay a $5.00 dividend next year, which represents 100% of its earnings. This will provide investors with a 12% expected return. Instead, we decide to plow back 40% of the earnings at the firm’s current return on equity of 20%. What is the value of the stock before and after the plowback decision?

P0

5

1267

.$41.

No Growth With Growth

Solution

Our company forecasts to pay a $5.00 dividend next year, which represents 100% of its earnings. This will provide investors with a 12% expected return. Instead, we decide to plow back 40% of the earnings at the firm’s current return on equity of 20%. What is the value of the stock before and after the plowback decision?

P0

5

1267

.$41.

No GrowthWith Growth

g

P

. . .

. .$75.

20 40 08

3

12 08000

The present value of growth opportunities

If the company did not plowback some earnings, the stock price would remain at $41.67. With the plowback, the price rose to $75.00.

The difference between these two numbers (75.00-41.67=33.33) is called the Present Value of Growth Opportunities (PVGO).

PVGO again

Present Value of Growth Opportunities (PVGO) - Net present value of a firm’s future investments.

Valuing Common Stocks

Expected rate of return - The percentage yield that an investor forecasts from a specific investment over a set period of time. Sometimes called the holding period return (HPR).

Expected return

Expected Return – the ratio of the profit over the initial cost

Here, P1 is the expected price in period 1, P0 is the current price and Div1 is the expected dividend payment in period 1.

Expected Return

rDiv P P

P1 1 0

0

An example

Example: A stock pays dividend of $3 every year. The current stock price is

$100. The expected price is $110 for the next year. If you hold the stock this year,

what is the expected rate of return?

My solution

The expected return is 13/100=13%• P0=$100

• P1=$110

• Div=$3

Another example

Imagine Corporation has just paid a dividend of $0.40 per share. The dividends are expected to grow at 30% per year for the next two years and at 5% per year thereafter. If the required rate of return in the stock is 15%, calculate the current stock price.

Solution

Answer: First: visualize the cash flow pattern;

• C1, C2 and P2 Then, you know what to do? P0 = [(0.4 *1.3)/1.15] + [(0.4 *

1.3^2)/(1.15^2)] + [(0.4 * 1.3^2*1.05)/((1.15^2 * (.15 -.05))] = $6.33