filing y our tax forms after selling y our employee … december 2014 summary filing y our tax forms...

TRANSCRIPT

tax s DECEMBER 2014

SUMMARY

Filing Your Tax Forms After Selling Your Employee Stock Purchase Plan (ESPP) Shares

Morgan Stanley has prepared the following information to assist you in understanding the tax consequences involved when selling shares from an ESPP. Included are sample forms and an explanation of the information for reporting the sale of these shares on your individual income tax return for 2014. Please retain all forms sent to you by Morgan Stanley to use when preparing your tax return. Morgan Stanley and its a�liates do not provide tax or legal advice. You should, therefore, seek tax advice based on your particular circumstances from an independent tax advisor of your choosing.

Q. What information do I need to file my tax return?A. The following pages describe the information you will need when you prepare your 2014 individual income tax return (Form 1040). Assemble the following forms when you are ready to prepare your tax return: Your Purchase Confirmation Form Form W-2, Wage and Tax Statement

from your employer Morgan Stanley’s Form 1099-B IRS Form 8949: Sales and Other

Dispositions of Capital Assets Schedule D (Form 1040): Capital

Gains and Losses

2 MORGAN STANLEY | 2014

filing your tax forms

Forms How to Obtain Questions?

Purchase Confirmation Form(or equivalent informationfrom your account, see nextpage for example)

This is mailed to your home at the time of your original purchase.

Call Morgan Stanley’s Customer Service Department at the toll-free number provided on the Tax Reporting Statement (Form 1099-B).

Form 1099-B Morgan Stanley sends this to you by February 15th* of the year following that in which the disposition occurs.

Call Morgan Stanley’s Customer Service Department at the toll-free number provided on the Tax Reporting Statement (Form 1099-B).

Form W-2 Your company will send this to you. Call your company’s payroll department.

IRS Form 8949 Visit your local IRS office or call (800) TAX FORM. You may also obtain this form via the Internet at www.irs.gov.

Call your local IRS office or consult your tax advisor.

Schedule D (Form 1040) Visit your local Internal Revenue Service (IRS) tax office or call (800) TAX FORM. You may also obtain this form via the Internet at www.irs.gov.

Call your local IRS office or consult your tax advisor.

Q. What is a Qualified 423 plan and how does it work?A. A Qualified 423 plan is considered a tax-qualified plan by the IRS if it is administered according to the regu-lations set out in Section 423 of the U.S. Internal Revenue Code and your company explicitly states it is intended to qualify under the Code. This allows participants to benefit from special tax considerations if shares are held at least two years from the grant date o�ering period and one year from the acquisition of the shares. Sales after

this time are identified as “qualified dispositions,” whereas sales during this time are identified as “disqualifying dispositions.” Compensation income for 423 plans is not taxed until the year of sale.

Q. What is a Non-qualified plan and how does it work?A. A Non-qualified plan is the term used for any other ESPP that is not struc-tured and administered as a Qualified Section 423 plan. These plans do not re-ceive any special tax consideration, and

compensation income on discounted Non-qualified plans is taxed the year shares are purchased.

Filing InformationThe following example reflects a salary of $45,000 and an acquisition of 200 shares of ABC Company stock. The exhibits will show you where you can find the information you need to pre-pare your individual tax return. These examples will show the results of stock sales for both Qualified Section 423 plans and Non-qualified plans.

* The Energy Improvement and Extension Act of 2008 changed the due date for providing Forms 1099 to recipients to February 15th.

Where do I get the information I need?

3MORGAN STANLEY | 2014

filing your tax forms

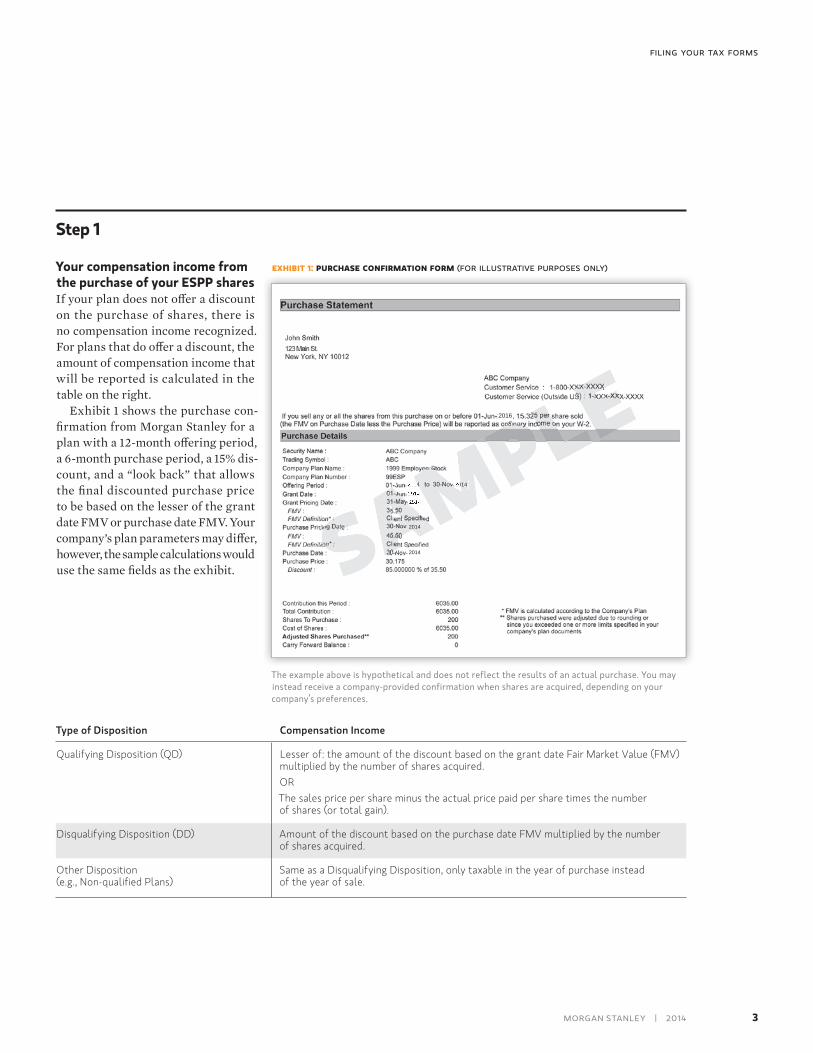

The example above is hypothetical and does not reflect the results of an actual purchase. You may instead receive a company-provided confirmation when shares are acquired, depending on your company’s preferences.

e p ase ma m for illustrati ur os s only

Type of Disposition Compensation Income

Qualifying Disposition (QD) Lesser of: the amount of the discount based on the grant date Fair Market Value (FMV) multiplied by the number of shares acquired.ORThe sales price per share minus the actual price paid per share times the number of shares (or total gain).

Disqualifying Disposition (DD) Amount of the discount based on the purchase date FMV multiplied by the number of shares acquired.

Other Disposition (e.g., Non-qualified Plans)

Same as a Disqualifying Disposition, only taxable in the year of purchase instead of the year of sale.

Your compensation income from the purchase of your ESPP sharesIf your plan does not o�er a discount on the purchase of shares, there is no compensation income recognized. For plans that do o�er a discount, the amount of compensation income that will be reported is calculated in the table on the right.

Exhibit 1 shows the purchase con-firmation from Morgan Stanley for a plan with a 12-month o�ering period, a 6-month purchase period, a 15% dis-count, and a “look back” that allows the final discounted purchase price to be based on the lesser of the grant date FMV or purchase date FMV. Your company’s plan parameters may di�er, however, the sample calculations would use the same fields as the exhibit.

Step 1

2014

2014

20142014

20142014

2016

sample

sample

2014sample

2014sample

2014

sample

2014

sample

2014

sample

2014

sample2014

sample2014

sample2014

sample2014

4 MORGAN STANLEY | 2014

filing your tax forms

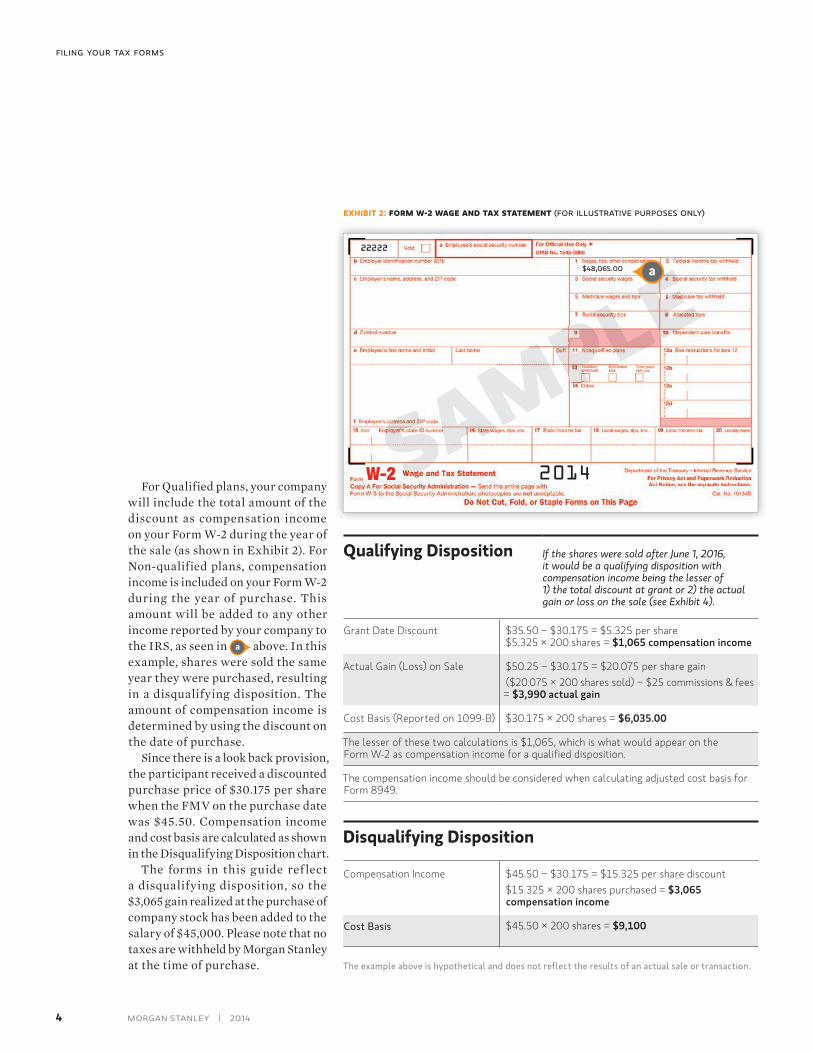

For Qualified plans, your company will include the total amount of the discount as compensation income on your Form W-2 during the year of the sale (as shown in Exhibit 2). For Non-qualified plans, compensation income is included on your Form W-2 during the year of purchase. This amount will be added to any other income reported by your company to the IRS, as seen in a §above. In this example, shares were sold the same year they were purchased, resulting in a disqualifying disposition. The amount of compensation income is determined by using the discount on the date of purchase.

Since there is a look back provision, the participant received a discounted purchase price of $30.175 per share when the FMV on the purchase date was $45.50. Compensation income and cost basis are calculated as shown in the Disqualifying Disposition chart.

The forms in this guide ref lect a disqualifying disposition, so the $3,065 gain realized at the purchase of company stock has been added to the salary of $45,000. Please note that no taxes are withheld by Morgan Stanley at the time of purchase.

e m a e a a s a eme for illustrati ur os s only

Compensation Income $45.50 − $30.175 = $15.325 per share discount$15.325 × 200 shares purchased = $3,065 compensation income

Cost Basis $45.50 × 200 shares = $9,100

2014

Qualifying Disposition If the shares were sold after June 1, 2016, it would be a qualifying disposition with compensation income being the lesser of 1) the total discount at grant or 2) the actual gain or loss on the sale (see Exhibit 4).

Disqualifying Disposition

sample

Grant Date Discount $35.50 − $30.175 = $5.325 per share $5.325 × 200 shares = $1,065 compensation income

Actual Gain (Loss) on Sale $50.25 − $30.175 = $20.075 per share gain($20.075 × 200 shares sold) − $25 commissions & fees = $3,990 actual gain

Cost Basis (Reported on 1099-B) $30.175 × 200 shares = $6,035.00

The lesser of these two calculations is $1,065, which is what would appear on the Form W-2 as compensation income for a qualified disposition.

The compensation income should be considered when calculating adjusted cost basis for Form 8949.

The example above is hypothetical and does not reflect the results of an actual sale or transaction.

a

5MORGAN STANLEY | 2014

filing your tax forms

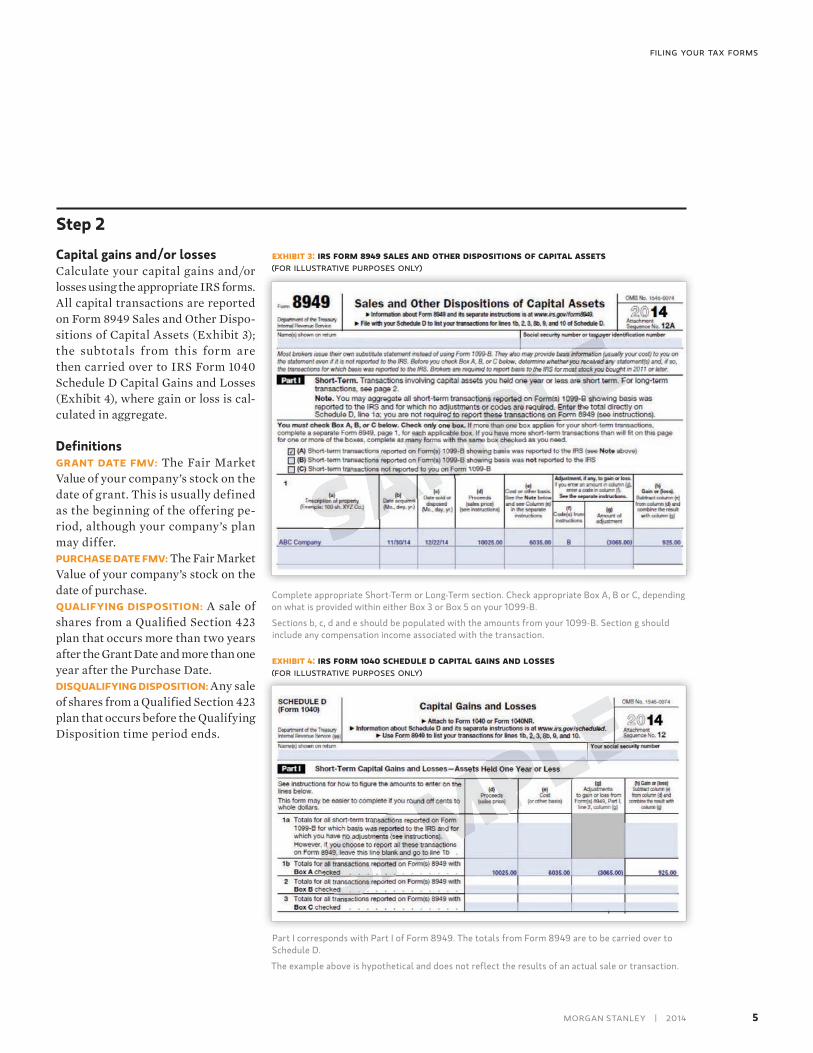

Capital gains and/or lossesCalculate your capital gains and/or losses using the appropriate IRS forms. All capital transactions are reported on Form 8949 Sales and Other Dispo-sitions of Capital Assets (Exhibit 3); the subtotals from this form are then carried over to IRS Form 1040 Schedule D Capital Gains and Losses (Exhibit 4), where gain or loss is cal-culated in aggregate.

DefinitionsThe Fair Market

Value of your company’s stock on the date of grant. This is usually defined as the beginning of the offering pe-riod, although your company’s plan may differ.

The Fair Market Value of your company’s stock on the date of purchase.

A sale of shares from a Qualified Section 423 plan that occurs more than two years after the Grant Date and more than one year after the Purchase Date.

Any sale of shares from a Qualified Section 423 plan that occurs before the Qualifying Disposition time period ends.

e s m s e le ap al a s a l ssesfor illustrati ur os s only

e s m sales a e sp s s ap al asse s for illustrati ur os s only

for only

sample

Step 2

sample

Complete appropriate Short-Term or Long-Term section. Check appropriate Box A, B or C, depending on what is provided within either Box 3 or Box 5 on your 1099-B.

Sections b, c, d and e should be populated with the amounts from your 1099-B. Section g should include any compensation income associated with the transaction.

Part I corresponds with Part I of Form 8949. The totals from Form 8949 are to be carried over to Schedule D.

The example above is hypothetical and does not reflect the results of an actual sale or transaction.

6 MORGAN STANLEY | 2014

filing your tax forms

THE MORGAN STANLEY ADVANTAGEFor nearly 80 years, Morgan Stanley has been a leader, innovator and resource for successful individuals and their families, as well as corporations, foundations and endowments. Our Financial Advisors work from an extensive knowledge base built on diverse skills, experience, training and professional interests. The Global Stock Plan Services unit of Morgan Stanley has over four decades of experience delivering advice and transaction support to stock plan administrators and participants. We are also a market leader in providing financial solutions to meet the specialized needs of executives, including #1 in 10b5-1 plans.*

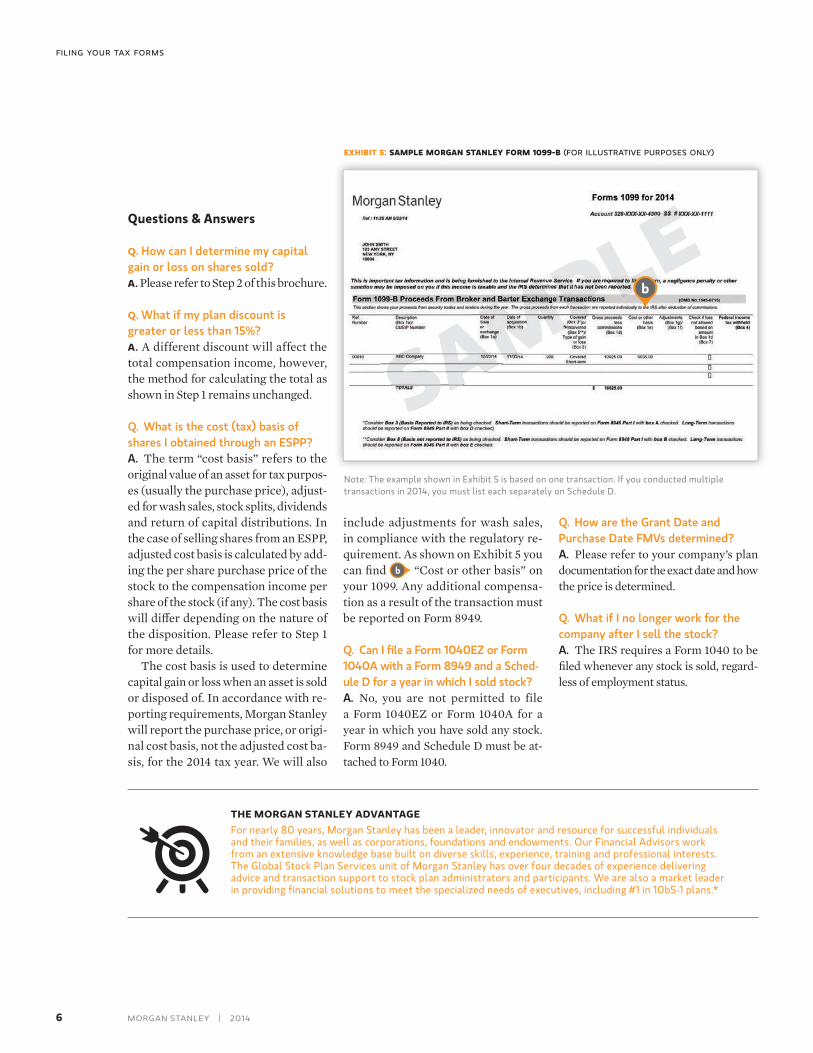

e sample m a s a le m for illustrati ur os s only

Note: The example shown in Exhibit 5 is based on one transaction. If you conducted multiple transactions in 2014, you must list each separately on Schedule D.

Questions & Answers

Q. How can I determine my capital gain or loss on shares sold?A. Please refer to Step 2 of this brochure.

Q. What if my plan discount is greater or less than 15%?A. A different discount will affect the total compensation income, however, the method for calculating the total as shown in Step 1 remains unchanged.

Q. What is the cost (tax) basis of shares I obtained through an ESPP?A. The term “cost basis” refers to the original value of an asset for tax purpos-es (usually the purchase price), adjust-ed for wash sales, stock splits, dividends and return of capital distributions. In the case of selling shares from an ESPP, adjusted cost basis is calculated by add-ing the per share purchase price of the stock to the compensation income per share of the stock (if any). The cost basis will di�er depending on the nature of the disposition. Please refer to Step 1 for more details.

The cost basis is used to determine capital gain or loss when an asset is sold or disposed of. In accordance with re-porting requirements, Morgan Stanley will report the purchase price, or origi-nal cost basis, not the adjusted cost ba-sis, for the 2014 tax year. We will also

include adjustments for wash sales, in compliance with the regulatory re-quirement. As shown on Exhibit 5 you can find b “Cost or other basis” on your 1099. Any additional compensa-tion as a result of the transaction must be reported on Form 8949.

Q. Can I file a Form 1040EZ or Form 1040A with a Form 8949 and a Sched-ule D for a year in which I sold stock?A. No, you are not permitted to file a Form 1040EZ or Form 1040A for a year in which you have sold any stock. Form 8949 and Schedule D must be at-tached to Form 1040.

Q. How are the Grant Date and Purchase Date FMVs determined?A. Please refer to your company’s plan documentation for the exact date and how the price is determined.

Q. What if I no longer work for the company after I sell the stock?A. The IRS requires a Form 1040 to be filed whenever any stock is sold, regard-less of employment status.

sampleb

This Page Left Intentionally Blank

© 2014 Morgan Stanley Smith Barney LLC. Member SIPC. CRC1040556 12/14 CS 8016420 11/14

* Source: Washington Service. Morgan Stanley ranked #1 in 10b5-1 market share from 2005 through 2013. Data from the period 2/1/2005 to 5/31/2009 reflects the formerly separate PDP businesses of the Global Wealth Management Group of Morgan Stanley & Co. LLC and the Smith Barney division of Citigroup Global Markets Inc. that now form Morgan Stanley Smith Barney LLC. This data also includes transactions from Morgan Stanley & Co. LLC. Information contained herein was obtained from sources believed reliable but the accuracy and completeness thereof cannot be guaranteed. Information contained herein is subject to change.

Morgan Stanley Smith Barney LLC (“Morgan Stanley”), its affiliates and Morgan Stanley Financial Advisors or Private Wealth Advisors do not provide tax or legal advice. Clients should consult their tax advisor for matters involving taxation and tax planning and their attorney for legal matters.

filing your tax forms