fig. 1 outstanding balances in chinese bond fig. 2 ... · december 2015, 98 per cent increased from...

TRANSCRIPT

1

The People's Bank of China (PBoC) extended the trading hours for Renminbi to 23:30 starting on 4 January 2016. The extended hours of onshore market was matched by the HKEx’s after-hours futures trading, which can serves as an efficient risk management tool for investors.

HKEx’s USD/CNH futures contract recorded a monthly ADV of 2,071 contracts (US$207 Mn notional) in December 2015, 98 per cent increased from November 2015. Open Interest reached 24,018 contracts (US$ 2,402 Mn notational) on 31 December 2015, close to the all-time high record of 23,887 in February 2014.

HKEx's Chief China Economist, Dr Ba sees that China’s domestic bond market is expected to remain active and keep growing in 2016, and bond defaults are expected to return to more normal levels.

Interview with Michele Leung of S&P: the recent rally in China’s local bond market is liquidity driven more than fundamental play, thanks to the volatilities in equity market.

Inside Fixed Income and Currency (FIC) Monthly Newsletter

For more information, please email [email protected]

Issue No 12

December 2015

Monthly Highlights

Sources: HKEx, WIND, Bloomberg

From the Chief Economist’s Vantage Point

Outlook: China’s Bond Market in 2016

Contributed by Dr. Ba Shusong, Chief China Economist, HKEx

With the IMF’s decision to include Renminbi into its SDR basket, more and more overseas institutional investors started to

increase their RMB holdings. Demand for Renminbi assets inevitably rose, especially for bonds. Given a number of factors,

China’s domestic bond market is expected to remain active and keep growing in 2016. Bond defaults are expected to return to

more normal levels.

I. Mainland bond markets reform has been speeding up with market volume growing fast

The CSRC has published new administrative measures for corporate bond issuance and trading, which extended the scope of

corporate bond issuers to all corporate entities, simplified issuance approval procedures, and emphasised the importance of

regulation during and after a transaction. The NDRC has published proposals on the further liberalisation of the corporate bond

market, including adjustments to improve the approval efficiency for corporate bond issues. Meanwhile, the NAFMII (National

Association of Financial Market Institutional Investors) is working to regulate issuers by tiers and categories, lower the issuance

threshold(s) for super and short-term commercial papers (SCPs), and raise the efficiency of private placement notes (PPNs)

issuance. It also aims to reform the registration of issues, liquidity, rankings and quotas of non-financial corporate debt financing

vehicles. Together, these measures provide a healthy environment and a sound regime for the bond market to develop rapidly .

As of the end of November 2015, the value of outstanding Chinese bonds stood at RMB46.8 trillion, up 30% from the RMB36

trillion at the end of 2014. It was the fastest growth in six years.

As of the end of October 2015, direct financing accounted for 21.22% of public financing, and bond financing under direct

financing accounted for 16.78% of public financing.

Fig. 1 Outstanding Balances in Chinese Bond

Markets and YOY Growth

Fig. 2 Maturities of Local Government Debt

Outstanding

2

For more information, please email [email protected] Sources: WIND, Bloomberg

II. Debt replacements have been proceeding steadily with local debt market likely to expand fast

1) By the end of 2015, about RMB16 trillion of local government debts will remain outstanding

According to arrangements by relevant authorities, screenings of outstanding local government debts have been completed.

According to statistics, as at the end of 2015, local government debt will stand at RMB16 trillion, of which RMB15.4 trillion will be

local government debt outstanding at the end of 2014 and RMB600 billion will be additional debt approved by the NPC for local

governments in 2015.

Of the RMB15.4 trillion of local government debt outstanding at the end of 2014, RMB9.1 trillion was general debt and RMB6.3

trillion was designated debt. Their maturity structures were shown in figure 2.

2) Local debt market likely to grow fast as debt replacements continue in an economic downturn

In terms of new debt for local governments, the quota of RMB0.6 trillion for 2015 has been completely allotted. Considering the

downward pressure on China’s overall economy and local governments’ huge demand for capital, China is expected to further

raise the ceiling for local government debt in the coming years.

At the end of 2014, there was RMB15.4 trillion of local government debt outstanding, of which RMB 14.2 trillion was debt to be

replaced, after taking out the RMB1.2 trillion of local government bonds. It is likely China will allow the replacement to be

completed over a period of time to alleviate possible market impact. If the transition is to last three years, for instance, about

RMB4 trillion to RMB5 trillion of bonds for debt replacement would be issued a year.

In terms of actual implementation, the MOF has granted a total debt-replacement quota of RMB3.2 trillion in three phases. Local

debt outstanding at the end of November 2015 amounted to RMB4.6 trillion. Excluding new issues in the future, upon the

replacement of all debt, the value of local government bonds outstanding should be around RMB16 trillion.

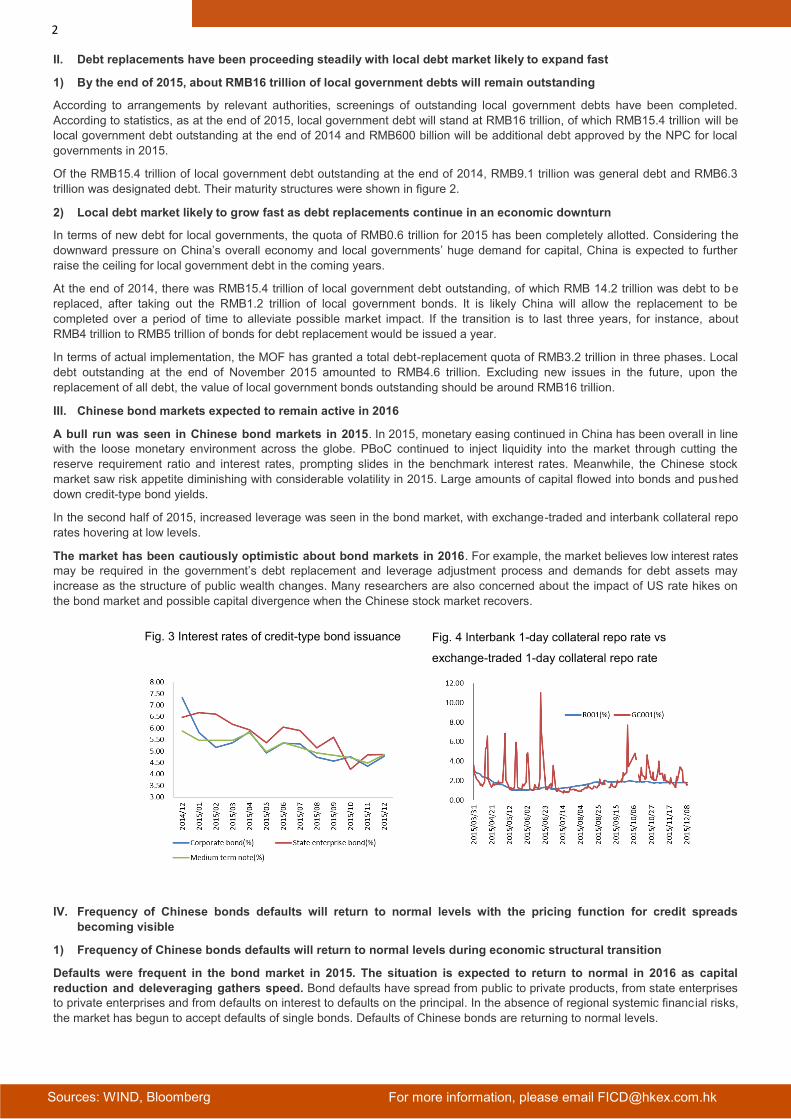

III. Chinese bond markets expected to remain active in 2016

A bull run was seen in Chinese bond markets in 2015. In 2015, monetary easing continued in China has been overall in line

with the loose monetary environment across the globe. PBoC continued to inject liquidity into the market through cutting the

reserve requirement ratio and interest rates, prompting slides in the benchmark interest rates. Meanwhile, the Chinese stock

market saw risk appetite diminishing with considerable volatility in 2015. Large amounts of capital flowed into bonds and pushed

down credit-type bond yields.

In the second half of 2015, increased leverage was seen in the bond market, with exchange-traded and interbank collateral repo

rates hovering at low levels.

The market has been cautiously optimistic about bond markets in 2016. For example, the market believes low interest rates

may be required in the government’s debt replacement and leverage adjustment process and demands for debt assets may

increase as the structure of public wealth changes. Many researchers are also concerned about the impact of US rate hikes on

the bond market and possible capital divergence when the Chinese stock market recovers.

IV. Frequency of Chinese bonds defaults will return to normal levels with the pricing function for credit spreads

becoming visible

1) Frequency of Chinese bonds defaults will return to normal levels during economic structural transition

Defaults were frequent in the bond market in 2015. The situation is expected to return to normal in 2016 as capital

reduction and deleveraging gathers speed. Bond defaults have spread from public to private products, from state enterprises

to private enterprises and from defaults on interest to defaults on the principal. In the absence of regional systemic financial risks,

the market has begun to accept defaults of single bonds. Defaults of Chinese bonds are returning to normal levels.

Fig. 3 Interest rates of credit-type bond issuance

Fig. 4 Interbank 1-day collateral repo rate vs

exchange-traded 1-day collateral repo rate

3

For more information, please email [email protected] Sources: WIND, Bloomberg

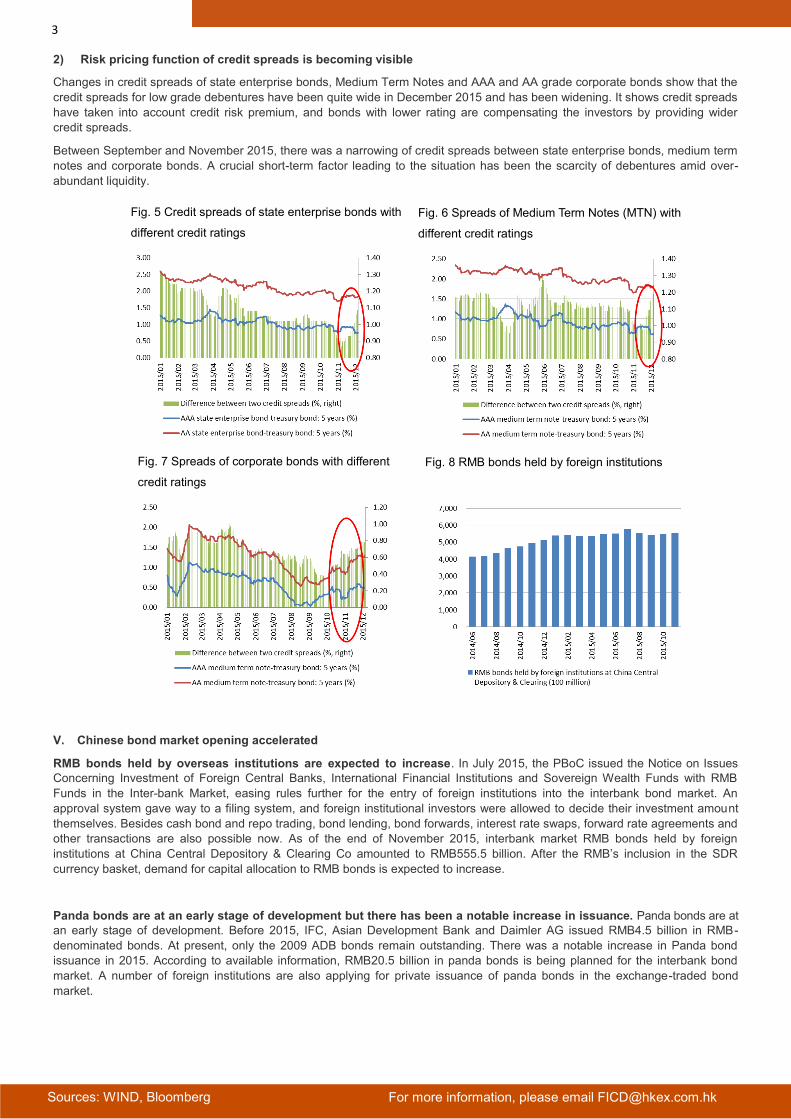

2) Risk pricing function of credit spreads is becoming visible

Changes in credit spreads of state enterprise bonds, Medium Term Notes and AAA and AA grade corporate bonds show that the

credit spreads for low grade debentures have been quite wide in December 2015 and has been widening. It shows credit spreads

have taken into account credit risk premium, and bonds with lower rating are compensating the investors by providing wider

credit spreads.

Between September and November 2015, there was a narrowing of credit spreads between state enterprise bonds, medium term

notes and corporate bonds. A crucial short-term factor leading to the situation has been the scarcity of debentures amid over-

abundant liquidity.

V. Chinese bond market opening accelerated

RMB bonds held by overseas institutions are expected to increase. In July 2015, the PBoC issued the Notice on Issues

Concerning Investment of Foreign Central Banks, International Financial Institutions and Sovereign Wealth Funds with RMB

Funds in the Inter-bank Market, easing rules further for the entry of foreign institutions into the interbank bond market. An

approval system gave way to a filing system, and foreign institutional investors were allowed to decide their investment amount

themselves. Besides cash bond and repo trading, bond lending, bond forwards, interest rate swaps, forward rate agreements and

other transactions are also possible now. As of the end of November 2015, interbank market RMB bonds held by foreign

institutions at China Central Depository & Clearing Co amounted to RMB555.5 billion. After the RMB’s inclusion in the SDR

currency basket, demand for capital allocation to RMB bonds is expected to increase.

Panda bonds are at an early stage of development but there has been a notable increase in issuance. Panda bonds are at

an early stage of development. Before 2015, IFC, Asian Development Bank and Daimler AG issued RMB4.5 billion in RMB-

denominated bonds. At present, only the 2009 ADB bonds remain outstanding. There was a notable increase in Panda bond

issuance in 2015. According to available information, RMB20.5 billion in panda bonds is being planned for the interbank bond

market. A number of foreign institutions are also applying for private issuance of panda bonds in the exchange-traded bond

market.

Fig. 5 Credit spreads of state enterprise bonds with

different credit ratings

Fig. 6 Spreads of Medium Term Notes (MTN) with

different credit ratings

Fig. 7 Spreads of corporate bonds with different

credit ratings

Fig. 8 RMB bonds held by foreign institutions

4

For more information, please email [email protected] Sources: WIND, Bloomberg

Table 1 Panda bond issuance in 2015

An important contributing factor is the narrowing of spreads between Mainland and overseas markets. To international

investors/issuers, a currency commonly used to denominate asset prices will increasingly become a currency with an investment

characteristic; and a currency commonly used to denominate debt prices will increasingly become a currency with a financing

characteristic. A currency’s characteristic decides how it is used in the international market. Spread levels are a key factor that

decides whether a currency has an investment or financing characteristic. Take the Japanese Yen as an example. The currency

has an obvious financing characteristic, mainly because interest rates are very low in Japan. The RMB has an obvious

investment characteristic. An important reason for this is that interest rates in China are higher than in other developed

economies, which also explains the sluggish performance of panda bonds in recent years. Nevertheless, since 2015, China has

lowered its reserve requirement ratio five times and interest rates five times. Its monetary policy is relatively relaxed now with

one-year benchmark lending rate down from 5.35% at the beginning of the year to 4.35%, and one-year benchmark deposit rate

down from 2.5% at the beginning of the year to 1.5%. This has created the conditions for panda bond issuance.

Fig. 9 China’s one-year benchmark lending and

deposit rates

Issue time Issuer Issue size

Sep 2015 Hong Kong and Shanghai Banking Corporation Limited RMB1 billion

Sep 2015 Bank of China (Hong Kong) Limited RMB10 billion

Oct 2015 China Merchants Holdings (Hong Kong) Co Ltd RMB500 million

Nov 2015 British Columbia of Canada RMB6 billion

Dec 2015 Government of South Korea RMB3 billion

5

For more information, please email [email protected] Sources: Bloomberg

China Macro Update Regulatory/Policy Developments

■ Offshore Chinese banks are selling a record

amount of RMB-denominated certificates of

deposit as China takes steps to curb outflows of

the currency. Sales jumped to an unprecedented

RMB66.1 billion (US$10.2 billion) this month, data

compiled by Bloomberg show. That comes after

Hong Kong’s RMB deposits, the world’s largest,

shrank to the smallest in two years. The Chinese

government has in the past month imposed

restrictions on RMB outflows, including ordering a

halt to offshore banks borrowing from domestic

markets through bond repurchases, and

suspending new applications in a program that

allows domestic investors to buy overseas assets

denominated in the currency. The measures are

aimed at making it harder for speculators to short

the RMB in the offshore market.

■ China will allow limited convertibility of the RMB in

three free trade zones (FTZ) in Guangdong,

Fujian and Tianjin, a move further liberalising its

capital account after its currency was admitted to

the IMF's reserve basket. Onshore institutions that

are registered in the FTZs and that do not fall into

negative lists each will be able to freely convert up

to US$10 million worth of RMB annually.

Multinational companies based in these FTZs also

will be allowed to do cross-border two-way cash

pooling within a corporate group.

Macro Economy Update

■ "Flexible" and "forceful" are the key words

emerging from a meeting of China's leaders that

focused on the danger of allowing economic

growth to slow too much. Statements released

Monday at the culmination of a Central Economic

Work Conference emphasised the need to create

monetary conditions for structural reforms that

include restraining the country's reliance on credit.

Market/Product Developments

■ Trading in Shanghai will end at 11:30 p.m. local

time starting on 4 January, instead of the current

4:30 p.m., the People’s Bank of China (PBoC)

said in a statement on 23 December, adding that

permitting foreign institutions with significant

volumes to trade in the onshore foreign-exchange

market will help narrow the gap between the

currency’s rates at home and abroad.

■ The China Foreign Exchange Trading System

(CFETS) introduced an RMB trade-weighted index

(TWI) on 11 December. The PBoC highlighted this

index on its website as an important and more

appropriate reference for the market that has

overly fixated on the bilateral USD-RMB exchange

rate.

Key Research Reports/Conferences

■ The RMB is now the second most active currency

between Japan and Mainland China/Hong Kong

with the RMB accounting for 7 per cent of

payments, by value, compared to 3 per cent two

years ago, according to SWIFT’s latest RMB

tracker.

6

For more information, please email [email protected]

HKEx’s USD/CNH Futures

Sources: HKEx, Bloomberg

Product Highlights

■ HKEx’s USD/CNH futures contract recorded a monthly ADV of 2,071 contracts (US$207 Mn notional) in December 2015, 98

per cent increased from November 2015. Open Interest reached 24,018 contracts (US$ 2,402 Mn notational) on 31

December 2015, close to the all-time high record of 23,887 in February 2014.

■ Trading volume was high in the March 2016, June 2016 and December 2016 contracts, which accounted for 57 per cent of

total monthly volume in December. Open interest was high in the June 2016, December 2016 and March 2017 contracts,

which accounted for 65 per cent of total open interest at the end of December.

RMB FX Market Dynamics

Offshore RMB FX Market Comments

■ The Hong Kong-traded offshore yuan hit an intraday low

of 6.5965 on 30 December morning, its weakest since late

September 2011.

■ According to market forecast data from Bloomberg, the

USD/CNH rate will most likely stay within the range of 6.5

to 6.6 before the first quarter of 2016.

■ The spread between the onshore and offshore markets for

the yuan has been growing since the devaluation,

approaching 1,000 pips towards the end of December. On

the heels of this recent divergence between onshore and

offshore Yuan, China has suspended some foreign banks

from trading FX.

7

For more information, please email [email protected] Sources: Bloomberg, WIND, NAFMII

Onshore Bond Market Dynamics

Offshore Bond Market Dynamics

Offshore RMB Bond Market Comments

■ There was only two primary issuance in the CNH space

this month with RMB 4.5bn of new issues. Deposits in

Hong Kong increased by 1.2per cent MoM to RMB 864.2bn

at the end of November. The total remittance of RMB for

cross-border trade settlement amounted to RMB 508.9bn

in November, compared to RMB 410.8bn in October.

■ Total issuances plunged 55 per cent year-on-year in 2015

to RMB 79.7bn, the lowest level since 2012, according to

Wind data. As long as the onshore bond market continues

to provide favorable funding levels to issuers, offshore

RMB corporate bond supply is expected to remain low.

Onshore RMB Bond Market Comments

■ Onshore bond issuance decreased 11.4 per cent to

RMB2.3 trillion in December from RMB2.6 trillion in

November.

■ Total issuances on the exchanges has increased

substantially in 2015, almost double the issuance

number and triple the issuance value seen in 2014.

The top three contributions come from the categories

of LGB, corporate bond, and ABS, accounting for

more than 80% of the increase.

■ China’s Panda bond market is gaining plenty of

traction as four Panda bonds have been issued since

China reopened the market in the end of September.

And with a pair of sovereign issuers eager to launch

their deals, the asset class is set to soon eclipse dim

sum bonds.

8

For more information, please email [email protected] Sources: Bloomberg, CFETS

Onshore/Offshore Short-Term Interest Rate Dynamics

Onshore/Offshore RMB STIR Market Comments

■ The offshore CNH liquidity has been drained up by the on-

offshore arbitrage flow and seasonal holiday effect recently.

■ Following the PBoC actions of suspending some foreign

banks from FX trading, the cost of borrowing yuan in Hong

Kong decreased substantially from 7.9 per cent to 5.5 per

cent on 30 December.

■ The CNH HIBOR yield curve is generally uptrend in

December as the yields on the short-end increased

substantially from the lower level seen in November.

9

For more information, please email [email protected]

Despite the slowdown in Chinese economy and currency weakness, the local bond market, as represented by the S&P China Bond Index, rallied 6.63% YTD, data as of Dec 3, 2015. The Chinese corporate market has been expanding rapidly, the market value grew 21 times to CNY 11 trillion since December 2006, it currently represents 33% of overall market exposure, see exhibit 1. The credit spreads are also trading tighter and now reached a 5-year low (see exhibit 2) .Yet the market argued the recent rally is liquidity driven more than fundamental play, thanks to the volatilities in equity market.

If we take a closer look, the volatility of Chinese equities is 8 times of the Chinese bonds in the past year. The total return of Chinese bonds is relatively robust, compared with the negative returns in the equity market. Please see exhibit 3 for the statistics, note these returns are in USD and already accounted for the currency fluctuation.

While the spreads tightened significantly with the bond rally, the recent default headlines shed light on the emerging credit risks. For example, Sinosteel, a centrally-owned SOE, postponed its option exercise date and deferred its interest payment. It received broad attention as it is the first onshore enterprise bond to default. It has also shown that SOEs are not immune to the economic slowdown and implicit government support should no longer be presumed. In fact, the majority of the outstanding corporate bonds are issued by local or central SOE.

Traditionally, investors have used credit ratings as an assessment of the credit worthiness of a borrower. According to the S&P China Bond Index, over 51% of overall exposure are rated A or above by at least one of the local rating agencies; of which, 27% are being rated as AAA. Nevertheless, there may be discrepancies between ratings by Chinese local rating agencies versus corresponding global ratings, if any. Note while some of the local rating agencies are established via joint ventures with international players, the onshore corporates are not typically rated by international rating agencies at the bond level, only issuer level ratings are available. This lack of consistency and transparency make it more difficult for investors to gauge the credit quality of the corporate bonds.

Hence, it is increasingly important for investors to have tools to screen for high quality bonds in midst of market volatilities. S&P Dow Jones Indices launched the S&P China High Quality Corporate Bond 3-7 Year Index earlier this year in response to measure such market. The index adopted a two-tier approach in order to identify the high quality corporate bonds in China. Securities must satisfy the following two ratings criteria in order to be eligible for inclusion:

Issuers must be rated investment grade by at least one of the international rating agencies (S&P, Moody’s and Fitch). The

minimum credit rating for investment grade is BBB-/Baa3/BBB-.

Expert Corner

Contributed by Michele Leung, Director of Fixed Income Indices, S&P Dow Jones Indices

Chinese Corporate Bonds: The Rally and Beyond

Exhibit 3: Index Comparison

Index 1Yr Return 1Yr Risk 1Yr Risk Adj Return

S&P China BMI (US Dollar) -3.32% 29.07% -0.1143

S&P China Composite

Select Bond Index (USD) 3.30% 3.38% 0.9770

Exhibit 1 Exhibit 2

Exhibit 4

Source: S&P Dow Jones Indices

10

For more information, please email [email protected]

For more information about the USD/CNH Futures,

please visit: http://www.hkex.com.hk/rmbcurrencyfutures

If you have any question , please contact us at:

Address: 10/F One International Finance Centre

1 Harbour View Street, Central, Hong Kong

Email: [email protected]

DISCLAIMER All information contained herein is provided for reference only. While HKEx endeavors to ensure the accuracy, reliability and completeness of the information, neither it, nor any of its affiliates makes any warranty or representation, express or implied, or accept any responsibility or liability for, the accuracy, completeness, reliability or suitability of the information for any particular purpose. HKEx accepts no liability whatsoever to any person for any loss or damage arising from any inaccuracy or omission in the information or from any decision, action or non-action based on or in reliance upon the information.

The information does not, and is not intended to, constitute investment advice or a recommendation to make any kind of investment decision. Any person who intends to use the information or any part thereof should seek independent professional advice. Modification of the information in whole or in part, in any form or by any means are strictly prohibited without the prior written permission of HKEx.

Futures involve a high degree of risk. Losses from futures trading can exceed your initial margin funds and you may be required to pay additional margin funds on short notice. Failure to do so may result in your position being liquidated and you being liable for any resulting deficit. You must therefore understand the risks of trading in futures and should assess whether they are right for you. You are encouraged to consult a broker or financial adviser on your suitability for futures trading in light of your financial position and investment objectives before trading.

Securities must be rated ‘AAA’ by at least one of the following local Chinese rating agencies

China Chengxin International Credit Rating Co., Ltd

China Lianhe Credit Rating Co. Ltd.

Dagong Global Credit Rating Co., Ltd.;

Shanghai Brilliance Credit Rating & Investors

Service Co., Ltd.

Pengyuan Credit Rating Co. Ltd

The S&P China High Quality Corporate Bond 3-7 Year Index currently tracks 40 corporate bonds with yield-to-maturity at 3.71%. Its total return has been 8.70% YTD, outperforming its benchmark, the S&P China Corporate Bond Index, which rose 7.81% in the same period.

Disclaimer: This content is for general information purposes only and should not be used as a substitute for consultation with professional advisors.

Source: S&P Dow Jones Indices

Michele Leung is Director, Fixed Income Indices, at S&P Dow Jones Indices. With over 10

years of investment experience, Michele has solid product knowledge across different assets

class and particularly in fixed income. Michele oversees the creation and management of

Asian fixed income indices. Michele currently provides marketing collaterals and blogs, which

are available on www.spdji.com

Prior to joining S&P Dow Jones Indices, Michele was senior associate at China International

Capital Corporation. And previously, Michele was the fixed income product specialist in J.P.

Morgan Private Bank. Michele is also a chartered Financial Risk Manager (FRM).

Michele holds a Bachelor of Applied Science in Civil Engineering from University of British

Columbia and a Master of Science in Investment Management from University of Science and

Technology.

Exhibit 5