federal wage and hour law and recent developments in employee misclassification presented by barney...

TRANSCRIPT

Federal Wage and Hour Law And Recent Developments in Employee Misclassification

Presented by Barney M. Holtzman & Whitney Sedwick Meister

• Establishes a minimum wage for non-exempt employees ($7.25/hour)– Arizona Minimum Wage: $7.65/hour

• Distinguishes between covered (non-exempt) and excluded (exempt) employees

• Requires overtime payments for non-exempt employees

• Establishes overtime threshold (40 hours)• Specifies record-keeping requirements

The Fair Labor Standards Act (“FLSA”)

“White Collar” Exemptions

• The FLSA exempts certain employees from minimum wage and overtime requirements:– Executive– Administrative– Professional

Who is Exempt?

• Two tests must be satisfied:– Salary test

• Salary Level• Salary Basis - guaranteed minimum salary

for any work period during which any work is performed

– Duties test

Salary Level Test

• For most employees, the minimum salary level required for exemption is $455 per week.

• The $455 per week may be paid in equivalent amounts for periods longer than one week: – Biweekly: $910– Semimonthly: 985.83– Monthly: $1,971.66

Salary Basis Test

• Employee must regularly receive a predetermined amount of compensation each pay period.

• The compensation cannot be reduced because of variations in the quality of quantity of the work performed.

• The employee must be paid the full salary for any week in which the employee performs any work.

• The employee does not need to be paid for any workweek when no work is performed.

Deductions from Salary

• Generally, an employer may not “dock” an exempt employee’s salary based on a perceived lack of productivity on the employee’s part (though an employee may otherwise be disciplined).

• Improper deductions from exempt employees’ salaries expose employers to possible loss of those exemptions.

Permitted Salary Deductions

1. Absence from work for one or more full days for personal reasons2. Absence from work for one or more full days due to sickness or disability if deductions made under a bona fide plan, policy or practice of providing wage replacement benefits 3. To offset any amounts received as payment for jury fees, witness fees or military pay4. Good faith penalties imposed for violating safety rules of “major significance”5. Unpaid disciplinary suspension of one or more full days imposed in good faith for violations of workplace conduct rules

Effect of Improper Deductions

• Improper deductions from salary can result in the loss of the exemption:

- During the time period in which improper deductions were made

- For employees in the same job class- Working for the same managers

responsible for the improper deductions• Isolated or inadvertent improper deductions

will not result in the loss of exempt status if the employer reimburses the employee

Payroll Practices That Do Not Violate the Salary Basis Test

• Taking deductions from exempt employees accrued leave accounts

• Requiring exempt employees to keep track of and record their hours worked

• Requiring exempt employees to work a specified schedule

• Implementing bona fide, across-the-board schedule changes

• Paying bonuses

Executive Exemption Duties

• Primary duty of management;• Customarily and regularly directs the

work of two or more employees; and• Authority to hire or fire or having

suggestions and recommendations as to hiring, firing, advancement promotion or any other change of status to other employees to be given particular weight.

Administrative Exemption Duties

• Performance of office or non-manual work directly related to the management or general business operations of the employer or the employer’s customers; and

• Exercise of discretion and independent judgment with respect to matters of significance.

Learned Professional Exemption

• The employee’s primary duty must be the performance of work requiring advanced knowledge– In a field of science or learning– Customarily acquired by a prolonged

course of specialized intellectual instruction (academic degree is the best evidence that an employee meets this requirement)

Advanced Knowledge

• Predominantly intellectual in character• Includes work requiring the consistent

exercise of discretion and judgment• The advanced knowledge is generally used

to analyze, interpret or make deductions from varying facts or circumstances

• Not work involving routine mental, manual, mechanical, or physical work

• Cannot be attained at the high school level

Primary Duty• The principal, main, major or most

important duty that the employee performs.

• Factors to consider include, but are not limited to:– Relative importance & time spent on

exempt duties;– Relative freedom from direct supervision;

and– Whether employee spends more than 50%

of time performing exempt work.

Discretion and Independent Judgment

• The comparison and evaluation of possible courses of conduct, and acting or making a decision after the various possibilities have been considered

• Must be exercised with respect to “matters of significance,” which refers to the level of importance or consequence of the work performed

Discretion and Independent Judgment (cont’d)

• Factors include, but are not limited to whether the employee:– Has authority to formulate, interpret, or implement

management policies or operating practices– Carries out major assignments in conducting the

operations of the business– Performs work that affects business operations to a

substantial degree– Has authority to negotiate on behalf of and/or bind

the employer in matters that have significant financial and other business impact

Discretion and Independent Judgment (cont’d)

• Factors include, but are not limited to whether the employee:– Has authority to deviate from established

policies and procedures without prior approval

– Provides consultation or expert advice to management

– Is involved in planning business objectives– Investigates and resolves matters of

significance on behalf of management

Exemptions in Flux

• Others exemptions are in flux as a result of either litigation or action by the federal government:

• Outside sales exemption

• Computer professional exemption

• Caregiver/live-in domestic exemption

Outside Sales Exemption

• To qualify for the outside sales exemption, employees must satisfy two requirements:– Primary Duties:

• The primary duty must consist of making “sales” or obtaining orders or contracts for services or use of facilities for which consideration will be paid by a customer or client.

– Customary and Regular Work Away From Employer’s Place of Business:

• E.G., at a customer’s place of business or at a customer’s home

Outside Sales Exemption (con’t)

• Substantial litigation• In pharmaceuticals

sales industry:– In re Novartis Wage and

Hour Litigation: Following a court of appeals ruling that employees were non-exempt, Novartis settled nationwide class-wide overtime claims for $99.9 million

• By contrast, in Christopher v. SmithKline Beecham Corp., the Ninth Circuit ruled that a similar group of pharmaceutical sales employees were properly categorized as exempt

• The United States Supreme Court has accepted review of the Ninth Circuit’s decision

Computer Employees Exemption

• The computer employee exemption applies to computer systems analysts, computer programmers, software engineers and/or other “similarly skilled” workers in the computer field.

• To qualify for this exemption, employees in the computer field must be compensated on either:– (a) a salary or fee basis at a rate of not less than

$455 per week; or– (b) an hourly rate of not less than $27.63 per hour

Computer Employees Exemption (con’t)

• Exempt computer employees’ primary duties must involve:– Application of systems analysis techniques and procedures

(which includes consulting with users) to determine hardware, software or system functional specifications;

– Design, development, documentation, analysis creation, testing or modification of computer systems of programs, including prototypes, based on and related to user or system design specifications;

– Design, documentation, testing, creation or modification of computer programs related to machine operating systems; or any combination of these duties.

Computer Professional Update Act

• The Department of Labor takes a narrow view of the computer employee exemption.

• The “CPU Act” introduced in late 2011 in the Senate would amend the FLSA to apply the exemption to “information technology occupation[s] (including, but not limited to, work related to computers, information systems, components, networks, software, hardware, databases, security, internet, intranet, or websites) as an analyst, programmer, engineer, designer, developer, administrator, or other similarly skilled worker.”

• Also, the CPU Act would amend the primary job duties of exempt computer professionals to include activities such as debugging systems and enabling continuity of systems and applications.

Domestic and Caregiver Exemptions

• Under the FLSA employees who provide “companionship services” to the elderly and/or “infirm” are exempt from the minimum wage and overtime requirements of the law.

• The FLSA further exempts “live in” domestic workers from the overtime requirements of the Act.

Department of Labor Action On Domestic and Caregiver

Exemptions• December 27, 2011, the

DOL published a “notice of proposed rulemaking.”

• DOL proposes alteration of regulations concerning these exemptions.

• How would the exemptions change?

– Both exemptions would be limited to companions and/or live-in domestics hired directly by the family they serve.

– The exemptions would no longer be available for third-party employers.

Employee vs. Independent Contractor: Developing Issues

• Misclassification of employees as independent contractors results in potential lost wages for employees and lost tax revenues for the government.

• In September 2011, the DOL and IRS announced a joint effort to identify and to eliminate misclassification of employees as independent contractors.

Employee vs. Independent Contractor: the FLSA Test

• Requirements of the FLSA apply only to employer-employee relationships.

• Courts define “employer” and “employee” broadly.

• To determine whether a worker is an independent contractor as opposed to an employee for purposes of FLSA coverage, courts inquire into the “economic realities" of the relationship between the parties.

Employee vs. Independent Contractor: the FLSA Test (con’t)

• The FLSA “economic realities” test involves balancing several factors:– The degree of the alleged employer’s right to control the manner

in which an individual performs work for the benefit of the employer

– The alleged employee’s opportunity for profit or loss depending upon managerial skill

– The alleged employee’s investment in equipment or materials required for her work and/or her employment of assistants

– Whether the services provided require special skills– The degree of permanence in the working relationship– Whether the service rendered is an integral part of the alleged

employer’s business

Employee vs. Independent Contractor: the FLSA Test (con’t)

• No single factor is determinative of the “economic realities” of the working relationship.

• The company’s actual control or right to control the manner in which services are performed often is key in judicial determination of whether a worker is appropriately treated as an independent contractor.

Employee vs. Independent Contractor: the FLSA Test (con’t)

“Control” Issues• Talbert v. American Risk Insurance Co.:

Insurance adjuster hired on a temporary basis to handle claims files after Hurricane Ike was properly deemed an independent contractor because she “was expected to handle the files assigned to her with little or no day-to-day supervision . . . [and] ultimately controlled the number of hours she worked.”

Employee vs. Independent Contractor: the FLSA Test (con’t)

“Control” Issues (con’t)

• Thibault v. BellSouth Telecomm, Inc.: Cable splicer hired on a temporary basis to fix cable issues after Hurricane Katrina was appropriately treated as an independent contractor.

• The cable splicer was supervised only minimally in performance of his duties (e.g., provided with blueprints and left to repair cables on his own).

• Notably, the company actually set the cable splicer’s hours and required him to work alongside the company’s actual employees.

Employee vs. Independent Contractor: the FLSA Test (con’t)

“Control” Issues (con’t)

• Schultz v. Capital International Security, Inc.: Security agents were improperly treated as independent contractors rather than employees.

• Agents were given explicit direction from company as to performance of multiple job duties, including:– Performing rounds– Performing regular checks in locations on property where

contractors were present– Manner of opening doors for the Saudi prince whom they

guarded• Court concluded that these factors and others demonstrated “nearly

complete control” over how agents did their jobs.

Employee vs. Independent Contractor: Misclassification Risks

Under the FLSA• Exempt employees:

– If employees mischaracterized as independent contractors have been performing exempt work and otherwise meet requirements of an applicable exemption (e.g., salary basis, salary level), there may be relatively little liability under the FLSA.

• Non-exempt employees:– 2-3 years of back-pay– 2-3 years of unpaid

overtime– “Liquidated damages” in an

amount equal to unpaid wages and overtime

– Attorneys’ fees– Possibly treble damages

under Arizona’s wage payment statutes

Employee vs. Independent Contractor: the IRS Test

• As with the FLSA, “control issues” are key to the IRS’ determination as to whether a worker (or group of workers) is appropriately deemed an independent contractor.

• The IRS analysis involves three areas of inquiry:– Behavioral control– Financial control– The type of relationship between the parties

Employee vs. Independent Contractor: the IRS Test (con’t)

Behavioral Control• Who has the right to control what a worker does and how he or she

does it?

• Multiple factual issues are involved in this analysis, including:

• Specific training or instruction provided by the company to the worker• The manner in which the worker receives assignments• Who determines the methods by which work is performed• The worker’s daily routine and/or schedule (if any)• Where the worker performs services (e.g., at the company’s facilities or at

some other location)• Whether the worker is required, personally, to provide services to the

company• Who hires assistants or substitutes for the worker, if needed• Which party pays the assistants and whether the worker is reimbursed if he

or she pays the assistant

Employee vs. Independent Contractor: the IRS Test (con’t)

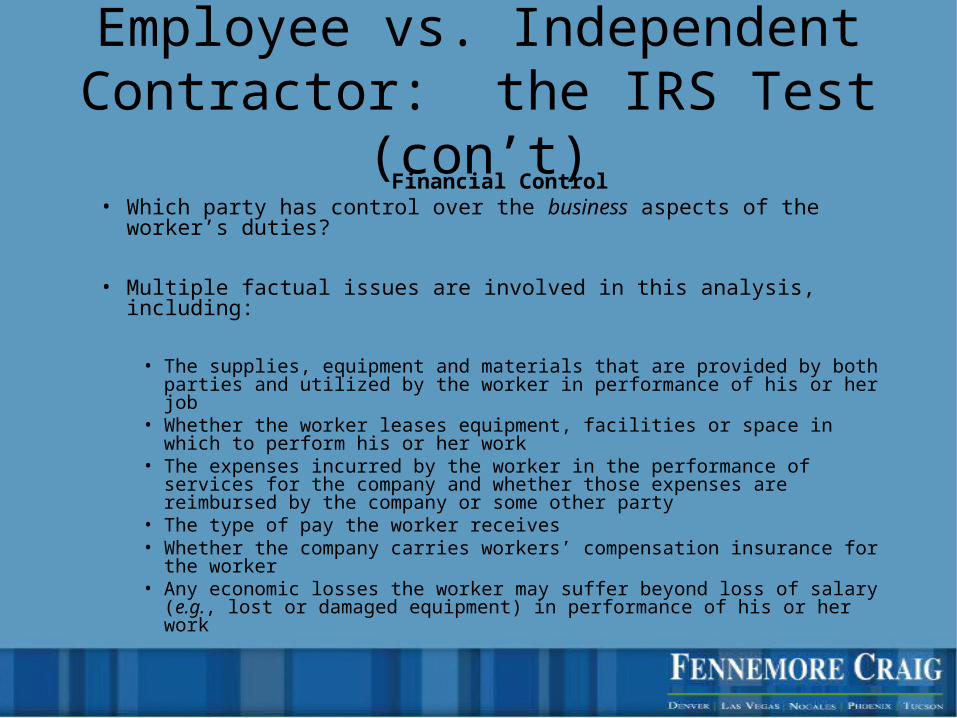

Financial Control• Which party has control over the business aspects of the worker’s

duties?

• Multiple factual issues are involved in this analysis, including:

• The supplies, equipment and materials that are provided by both parties and utilized by the worker in performance of his or her job

• Whether the worker leases equipment, facilities or space in which to perform his or her work

• The expenses incurred by the worker in the performance of services for the company and whether those expenses are reimbursed by the company or some other party

• The type of pay the worker receives• Whether the company carries workers’ compensation insurance for the

worker• Any economic losses the worker may suffer beyond loss of salary (e.g., lost

or damaged equipment) in performance of his or her work

Employee vs. Independent Contractor: the IRS Test (con’t)

Relationship Type• Does the relationship between the company and the worker

“look” like a traditional employer-employee relationship?

• The IRS has indicated that the following factual issues, among others, are key to this analysis:

• Whether there are written contracts between the parties• Whether the relationship gives rise to “employee type benefits” • The duration of the relationship • Whether the work performed by the worker is “a key aspect” of the

company’s business • Whether the parties’ relationship can be terminated by either party

without incurring liability

Employee vs. Independent Contractor: Risks Under the

Internal Revenue Code• Employment Taxes:

• Social security contributions• Workers’ compensation contributions• Federal Unemployment taxes• Federal Insurance Contributions Act taxes• Interest• Penalties

• Over time, these liabilities can grow to significant numbers

• President Obama’s 2010 budget assumed that the federal crackdown on misclassification would yield $7 billion over ten years!

Voluntary Classification Settlement Program (“VCSP”)

• The VCSP is a program that provides employers who have misclassified employees as independent contractors a limited shelter from back tax liability.

• Eligibility requirements:• Employer must have consistently treated workers as

non-employees• Employer must have filed all required Forms 1099 for the

workers for the previous three years• Employer must not be under an IRS audit of any kind• Employer must have no dispute with the IRS regarding

whether the workers are properly classified• Employer must not be under a current DOL or state

agency audit concerning worker misclassification

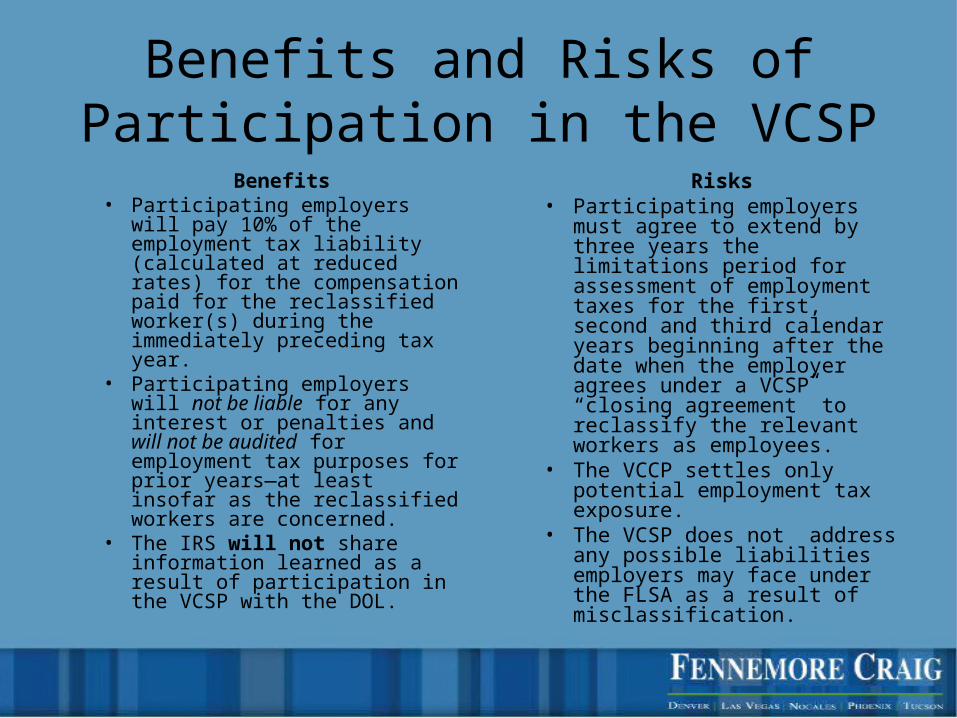

Benefits and Risks of Participation in the VCSP

Benefits• Participating employers will pay

10% of the employment tax liability (calculated at reduced rates) for the compensation paid for the reclassified worker(s) during the immediately preceding tax year.

• Participating employers will not be liable for any interest or penalties and will not be audited for employment tax purposes for prior years—at least insofar as the reclassified workers are concerned.

• The IRS will not share information learned as a result of participation in the VCSP with the DOL.

Risks• Participating employers must

agree to extend by three years the limitations period for assessment of employment taxes for the first, second and third calendar years beginning after the date when the employer agrees under a VCSP “closing agreement” to reclassify the relevant workers as employees.

• The VCCP settles only potential employment tax exposure.

• The VCSP does not address any possible liabilities employers may face under the FLSA as a result of misclassification.

Risk Management Practices

Internal Audit• Identify positions/contracts to review• Evaluate each of those positions/contracts

critically and ask:• Whether the worker performs exempt job duties;• Whether the worker otherwise meets exemption

requirements; and• Whether the company or the worker “controls” or

has the right to control the manner in which the worker delivers goods or services to the company.

Risk Management Practices

Internal Audit (con’t)• Develop a strategy for appropriately analyzing

job duties of workers at issue:• Job descriptions

• Useful only to the extent that they actually reflect what workers do on a day-to-day basis.

• Interviews• Interviewing managers and incumbents may provide a

clear picture of job duties.• However, interviews may not be privileged!• Targeted interviews with relevant managers are best.

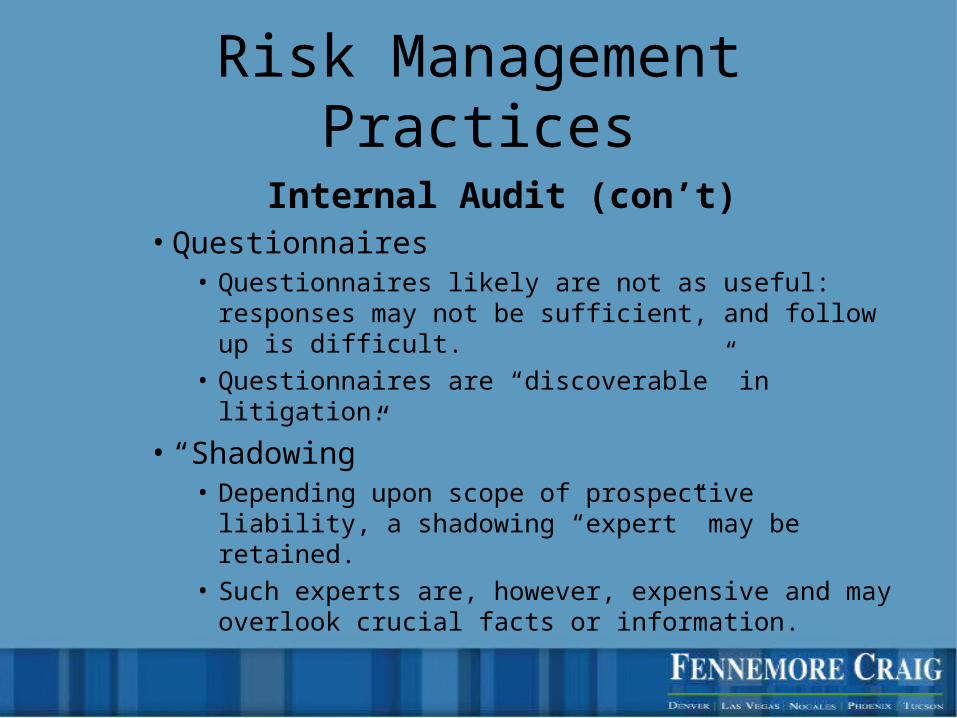

Risk Management Practices

Internal Audit (con’t)• Questionnaires

• Questionnaires likely are not as useful: responses may not be sufficient, and follow up is difficult.

• Questionnaires are “discoverable” in litigation.

• “Shadowing”• Depending upon scope of prospective liability, a

shadowing “expert” may be retained.• Such experts are, however, expensive and may overlook

crucial facts or information.

Questions

What’s New in Employment Law?

Fennemore Craig Labor & Employment Seminar

February 2012

John Balitis

Overview• Americans with Disabilities Act• Medical Marijuana Act• Social Media Updates• Minimum Wage Increase• EEOC Statistics for 2011• NLRB Posting Rule• Title VII Updates• Non-Competition Agreements• Family and Medical Leave Act

Americans with Disabilities Act

• High school diploma requirement may violate the ADA

• December 2, 2011 EEOC informal discussion letter

• Defining Disability– Severe obesity

• EEOC v. Resources for Human Development, No. 10-3322, 2011 U.S. Dist. LEXIS 140678 (E.D. La. Dec. 6, 2011)

– Migraines• Allen v. Southcrest Hospital, No. 11-5016, 2011 U.S. App. LEXIS

25488 (10th Cir. Dec. 21, 2011)

Medical Marijuana Act

• Overview of the Medical Marijuana law

• Judge Bolton’s January 4, 2012 decision

• Current obligations on employers

• How can a well-written drug policy help?

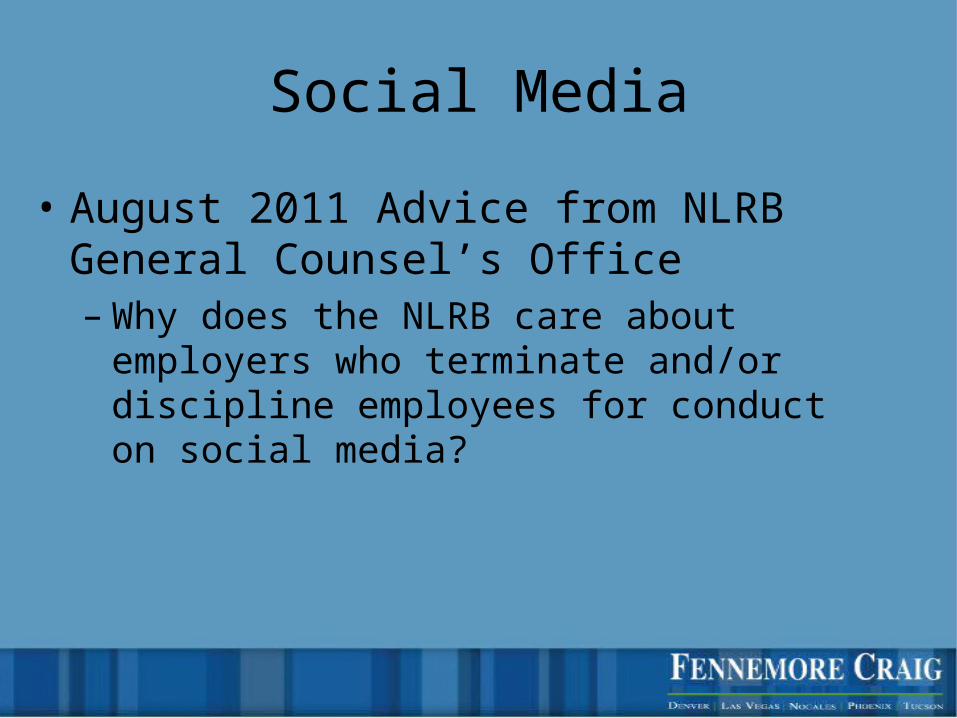

Social Media

• August 2011 Advice from NLRB General Counsel’s Office– Why does the NLRB care about employers

who terminate and/or discipline employees for conduct on social media?

Who owns social media accounts?

• PhoneDog lawsuit– Employer suing former employee over ownership of a

Twitter account – Account was started in association with PhoneDog

but now the former employee is using it as his own

• Similar Facebook and LinkedIn cases

• Lessons from social media litigation for employers?– Policies should clearly and unambiguously address

ownership of social media accounts– Act promptly upon termination of the employee to

remove their access to social media accounts– Consider entering into agreements with social media

workers

Minimum Wage Increase

•Effective January 1, 2012

•$7.65 an hour in Arizona

•Bonus fun fact: Payroll Card Account

EEOC Statistics for 2011• Highest number of charges for the EEOC in

its 46-year history: 99,947 • Highest amount of monetary relief for victims

of workplace discrimination: $364.6 million• EEOC filed 261 lawsuits• Mediation program: $170 million in monetary

benefits for complainants• National systemic enforcement program

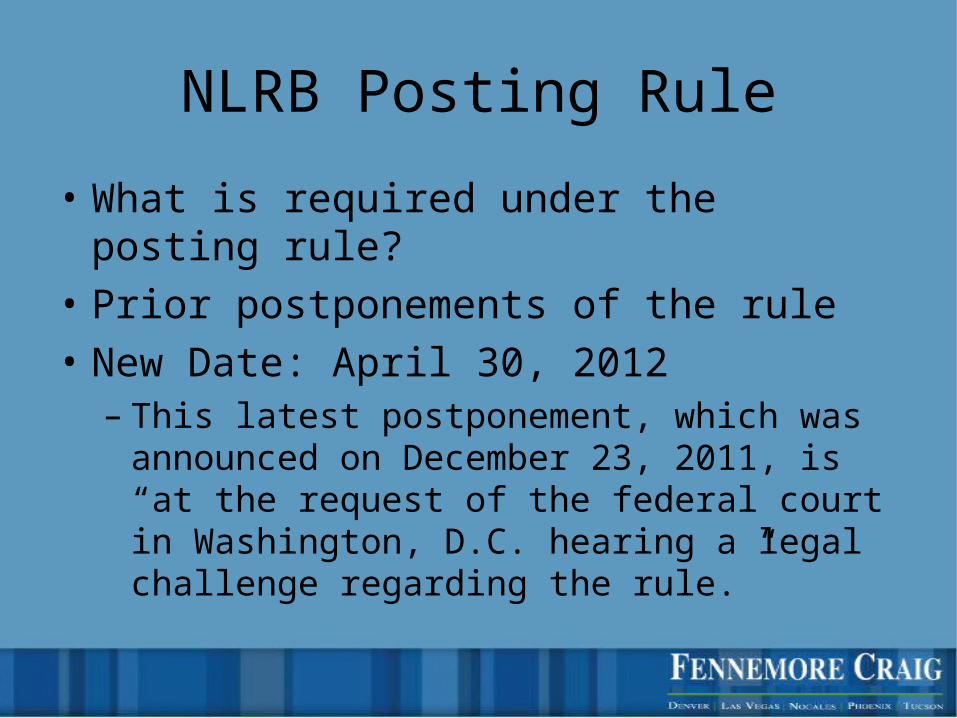

NLRB Posting Rule

• What is required under the posting rule?

• Prior postponements of the rule

• New Date: April 30, 2012– This latest postponement, which was

announced on December 23, 2011, is “at the request of the federal court in Washington, D.C. hearing a legal challenge regarding the rule.”

Title VII Updates

• Religion – A & F refuses to accommodate religious attire – Conservative Christian employee states claim for failure to

accommodate religious beliefs under Title VII• Weathers v. FedEx Corporate Services, Inc., No. 09 C 5493 (N.D.

Ill. November 1, 2011)

• Transgender protection– Current protections under Title VII– 11th Circuit case: found in favor of a transgender employee

claiming sex discrimination when her employer fired her after she announced plans to undergo a gender transition

– Guidance from Office of U.S. Personnel Management

Non-Compete Agreements

• Are your companies’ non-competition and non-solicitation contracts up to date?

• Recent Arizona case law regarding choice of law provisions– Pathway Med. Techs., Inc., v. Nelson, No.

CV11-0857, 2011 U.S. Dist. LEXIS 113075 (D. Ariz. Sept. 30, 2011)

Family and Medical Leave Act

• When does FMLA protection begin? – Pereda v. Brookdale Senior Living

Communities, Inc., No. No. 10-14723, 2012 U.S. App. LEXIS 492 (11th Cir. Jan. 10, 2012) (holding that the FMLA “protects a pre-eligibility request for post-eligibility leave.”)