february 2018 - tidewater midstream · 3 high growth, pure play ngl infrastructure business...

TRANSCRIPT

February 2018

2

DisclaimerForward Looking Information

In the interests of providing Tidewater Midstream and Infrastructure Ltd. (“Tidewater” or the “Corporation”) shareholders and potential investors with information regardingTidewater, including management’s assessment of future plans and operations relating to the Corporation, this document contains certain statements and information that areforward-looking statements or information within the meaning of applicable securities legislation, and which are collectively referred to herein as “forward-looking statements”. Theuse of any of the words "anticipate", "continue", "estimate", "expect", "may", "will", "project", "should", "believe", "plan", "intend" and similar expressions are intended to identifyforward-looking statements. Forward-looking statements are often, but not always, identified by such words. Forward-looking statements in this document include, but are not limitedto statements and tables (collectively “statements”) with respect to: plans to construct a natural gas pipeline from the BRC to TransAlta’s Sundance and Keephills power plants,expected cost of such project and associated take or pay agreement; potential egress and demand options including for petrochemical, technology, industrial and power use;infrastructure plans with respect to the proposed Pipestone Montney Sour Deep Cut Gas Plant including its potential expansion; plans with respect to natural gas storage infrastructure;the potential to connect newly acquired infrastructure to BRC and provide customers with a new large scale egress solution; projections to increase long term contracts and diversify tocustomers with strong balance sheets; plans to connect Tidewater’s Montney assets to its Edmonton infrastructure/egress hub; benefits generated from an integrated processing andinfrastructure network; the increasing relevance of Tidewater’s Deep Basin network, driving utilization and EBITDA growth upward; anticipated margin improvements for Tidewater’sEdmonton assets resulted from the reduction of certain fees, costs and tariffs; Tidewater’s plans to build out its Edmonton Energy Hub over the next two to three years and thepotential to add propylene, polypropylene and iso-octane production; anticipation of significant improvement in margins by eliminating third party rail transloading fees, eliminatingtrucking costs and reduced pipeline tariffs at the Acheson facility; target annual EBITDA/share growth over the next 24 months and target EBITDA levels; subsequent acquisitions andstrategies for acquisitions, capital projects and expenditures; strategic initiatives; anticipated producer activity and industry trends; and anticipated performance. Readers arecautioned not to place undue reliance on forward-looking statements, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. Bytheir nature, forward-looking statements involve numerous assumptions, as well as known and unknown risks and uncertainties, both general and specific, that contribute to thepossibility that the predictions, forecasts, projections and other forward-looking statements will not occur and which may cause Tidewater’s actual performance and financial results infuture periods to differ materially from any estimates or projections of future performance or results expressed or implied by the forward-looking statements. These assumptions, risksand uncertainties include, among other things: receipt of third party, regulatory and governmental approvals and consents; Tidewater’s ability to successfully implement strategicinitiatives and whether such initiatives yield the expected benefits; failure to consummate definitive agreements related to contemplated projects; future operating results;fluctuations in the supply and demand for natural gas, natural gas liquids (“NGLs”), and iso-octane; assumptions regarding commodity prices; demand for potential egress options;activities of producers, competitors and others; the weather; assumptions around construction schedules and costs, including the availability and cost of materials and serviceproviders; fluctuations in currency and interest rates; credit risks; marketing margins; potential disruption or unexpected technical difficulties in developing new facilities or projects;unexpected cost increases or technical difficulties in constructing or modifying processing facilities; Tidewater’s ability to generate sufficient cash flow from operations to meet itscurrent and future obligations; its ability to access external sources of debt and equity capital; changes in laws or regulations or the interpretations of such laws or regulations;political and economic conditions; that any required commercial agreements can be negotiated and completed; and other risks and uncertainties described from time to time in thereports and filings made with securities regulatory authorities by Tidewater.

Readers are cautioned that the foregoing list of important factors is not exhaustive. The forward-looking statements contained in this document are made as of the date of thisdocument or the dates specifically referenced herein. For additional information please refer to Tidewater’s public filings available on SEDAR at www.sedar.com. All forward-lookingstatements contained in this document are expressly qualified by this cautionary statement.

Any financial outlook or future-oriented financial information, as defined by applicable securities legislation, has been approved by management of Tidewater as of October 31, 2017.Such financial outlook or future-oriented financial information is provided for the purpose of providing information about management's current expectations and goals relating to thefuture of Tidewater. Readers are cautioned that reliance on such information may not be appropriate for other purposes.

TransAlta LOI

Tidewater and TransAlta have entered into a letter of intent (“LOI”) for Tidewater to construct a 120 km natural gas pipeline from the BRC to TransAlta’s power generating units atSundance and Keephills. The pipeline will be supported by a 15 year take-or-pay agreement with TransAlta. The completion of this project and execution by Tidewater of the take-or-pay agreement with TransAlta will be subject to negotiation of a definitive form of agreement between Tidewater and TransAlta.

Non-GAAP Financial Measures

This presentation refers to “EBITDA” and “Adjusted EBITDA”, which do not have any standardized meaning prescribed by generally accepted accounting principles in Canada (“GAAP”).EBITDA is calculated as income or loss before interest, taxes, depreciation and amortization. Adjusted EBITDA is calculated as EBITDA adjusted for incentive compensation, unrealizedgains/losses, non-cash items, transaction costs and other items considered non-recurring in nature.

Tidewater Management believes that EBITDA and Adjusted EBITDA provide useful information to investors as they provide an indication of results generated from the Corporation’soperating activities prior to financing, taxation and non-recurring/non-cash impairment charges occurring outside the normal course of business. Management utilizes Adjusted EBITDAto set objectives and as a key performance indicator of the Corporation’s success. In addition to its use by Management, Tidewater also believes Adjusted EBITDA is a measure widelyused by securities analysts, investors and others to evaluate the financial performance of the Corporation and other companies in the midstream industry. Investors should becautioned that EBITDA and Adjusted EBITDA should not be construed as alternatives to earnings, cash flow from operating activities or other measures of financial results determined inaccordance with GAAP as an indicator of the Corporation’s performance and may not be comparable to companies with similar calculations.

For more information with respect to financial measures which have not been defined by GAAP, including reconciliations to the closest comparable GAAP measure, see the “Non-GAAPand Additional Measures” section of Tidewater’s most recent MD&A which is available on SEDAR. 2

3

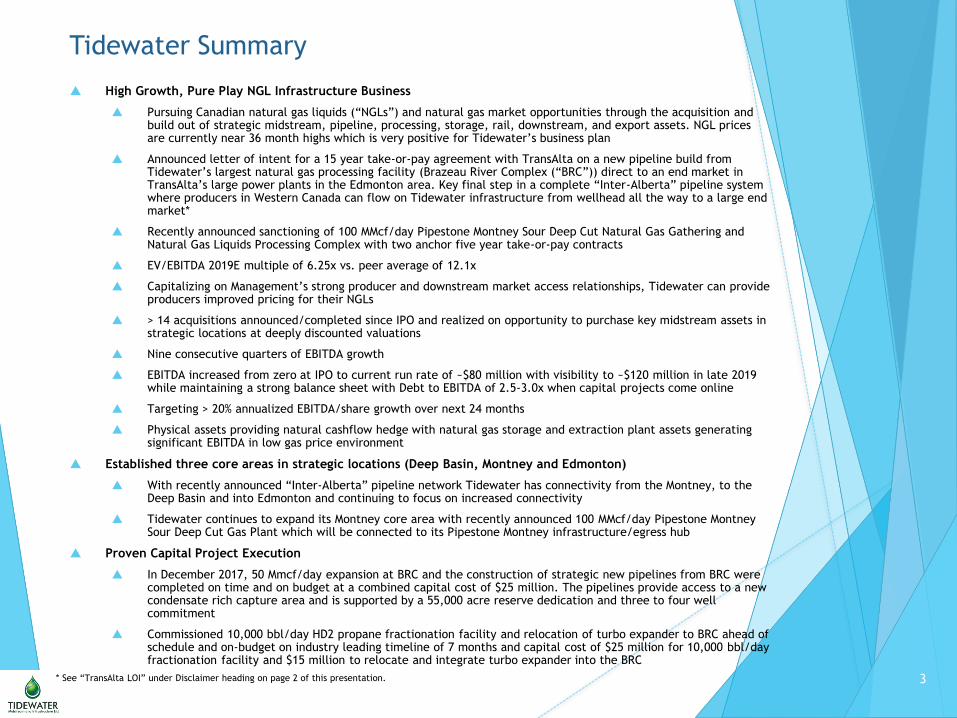

High Growth, Pure Play NGL Infrastructure Business

Pursuing Canadian natural gas liquids (“NGLs”) and natural gas market opportunities through the acquisition and build out of strategic midstream, pipeline, processing, storage, rail, downstream, and export assets. NGL prices are currently near 36 month highs which is very positive for Tidewater’s business plan

Announced letter of intent for a 15 year take-or-pay agreement with TransAlta on a new pipeline build from Tidewater’s largest natural gas processing facility (Brazeau River Complex (“BRC”)) direct to an end market in TransAlta’s large power plants in the Edmonton area. Key final step in a complete “Inter-Alberta” pipeline system where producers in Western Canada can flow on Tidewater infrastructure from wellhead all the way to a large end market*

Recently announced sanctioning of 100 MMcf/day Pipestone Montney Sour Deep Cut Natural Gas Gathering and Natural Gas Liquids Processing Complex with two anchor five year take-or-pay contracts

EV/EBITDA 2019E multiple of 6.25x vs. peer average of 12.1x

Capitalizing on Management’s strong producer and downstream market access relationships, Tidewater can provide producers improved pricing for their NGLs

> 14 acquisitions announced/completed since IPO and realized on opportunity to purchase key midstream assets in strategic locations at deeply discounted valuations

Nine consecutive quarters of EBITDA growth

EBITDA increased from zero at IPO to current run rate of ~$80 million with visibility to ~$120 million in late 2019 while maintaining a strong balance sheet with Debt to EBITDA of 2.5-3.0x when capital projects come online

Targeting > 20% annualized EBITDA/share growth over next 24 months

Physical assets providing natural cashflow hedge with natural gas storage and extraction plant assets generating significant EBITDA in low gas price environment

Established three core areas in strategic locations (Deep Basin, Montney and Edmonton)

With recently announced “Inter-Alberta” pipeline network Tidewater has connectivity from the Montney, to the Deep Basin and into Edmonton and continuing to focus on increased connectivity

Tidewater continues to expand its Montney core area with recently announced 100 MMcf/day Pipestone Montney Sour Deep Cut Gas Plant which will be connected to its Pipestone Montney infrastructure/egress hub

Proven Capital Project Execution

In December 2017, 50 Mmcf/day expansion at BRC and the construction of strategic new pipelines from BRC were completed on time and on budget at a combined capital cost of $25 million. The pipelines provide access to a new condensate rich capture area and is supported by a 55,000 acre reserve dedication and three to four well commitment

Commissioned 10,000 bbl/day HD2 propane fractionation facility and relocation of turbo expander to BRC ahead of schedule and on-budget on industry leading timeline of 7 months and capital cost of $25 million for 10,000 bbl/day fractionation facility and $15 million to relocate and integrate turbo expander into the BRC

Tidewater Summary

* See “TransAlta LOI” under Disclaimer heading on page 2 of this presentation.

4

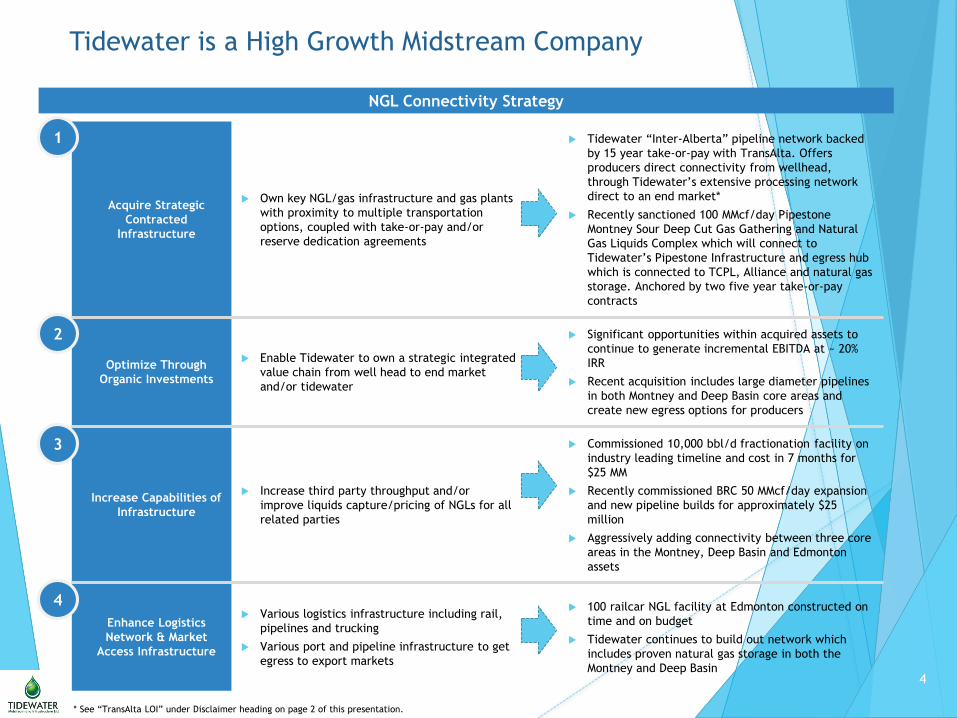

Tidewater is a High Growth Midstream Company

NGL Connectivity Strategy

Acquire Strategic

Contracted

Infrastructure

Own key NGL/gas infrastructure and gas plants

with proximity to multiple transportation

options, coupled with take-or-pay and/or

reserve dedication agreements

Tidewater “Inter-Alberta” pipeline network backed

by 15 year take-or-pay with TransAlta. Offers

producers direct connectivity from wellhead,

through Tidewater’s extensive processing network

direct to an end market*

Recently sanctioned 100 MMcf/day Pipestone

Montney Sour Deep Cut Gas Gathering and Natural

Gas Liquids Complex which will connect to

Tidewater’s Pipestone Infrastructure and egress hub

which is connected to TCPL, Alliance and natural gas

storage. Anchored by two five year take-or-pay

contracts

Optimize Through

Organic Investments

Enable Tidewater to own a strategic integrated

value chain from well head to end market

and/or tidewater

Significant opportunities within acquired assets to

continue to generate incremental EBITDA at ~ 20%

IRR

Recent acquisition includes large diameter pipelines

in both Montney and Deep Basin core areas and

create new egress options for producers

Increase Capabilities of

Infrastructure

Increase third party throughput and/or

improve liquids capture/pricing of NGLs for all

related parties

Commissioned 10,000 bbl/d fractionation facility on

industry leading timeline and cost in 7 months for

$25 MM

Recently commissioned BRC 50 MMcf/day expansion

and new pipeline builds for approximately $25

million

Aggressively adding connectivity between three core

areas in the Montney, Deep Basin and Edmonton

assets

Enhance Logistics

Network & Market

Access Infrastructure

Various logistics infrastructure including rail,

pipelines and trucking

Various port and pipeline infrastructure to get

egress to export markets

100 railcar NGL facility at Edmonton constructed on

time and on budget

Tidewater continues to build out network which

includes proven natural gas storage in both the

Montney and Deep Basin

1

2

3

4

* See “TransAlta LOI” under Disclaimer heading on page 2 of this presentation.

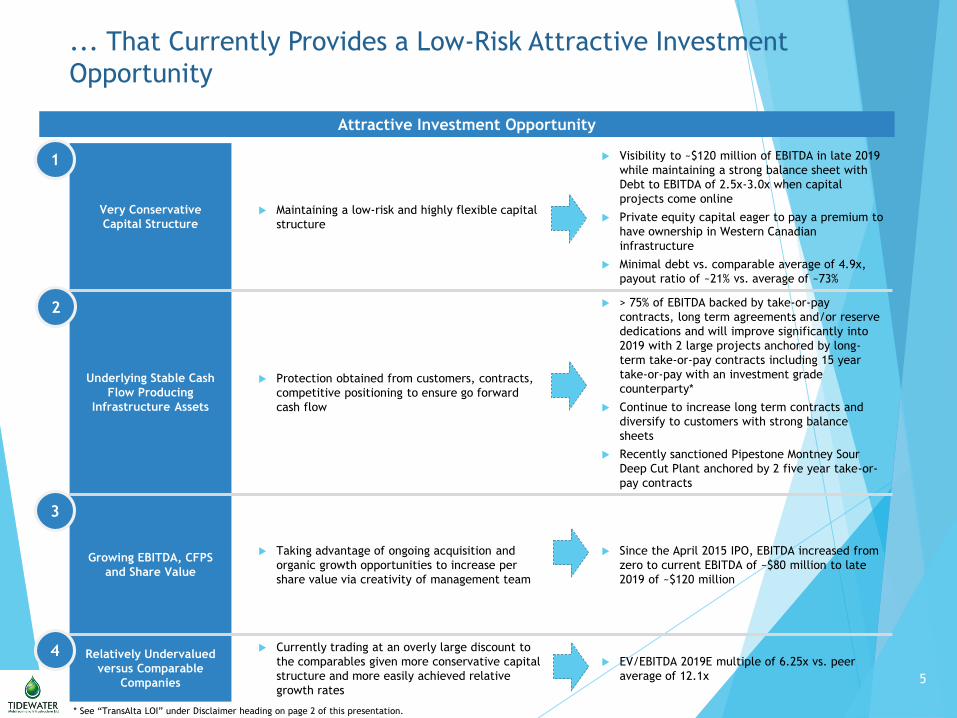

5

Very Conservative

Capital Structure Maintaining a low-risk and highly flexible capital

structure

Visibility to ~$120 million of EBITDA in late 2019

while maintaining a strong balance sheet with

Debt to EBITDA of 2.5x-3.0x when capital

projects come online

Private equity capital eager to pay a premium to

have ownership in Western Canadian

infrastructure

Minimal debt vs. comparable average of 4.9x,

payout ratio of ~21% vs. average of ~73%

Underlying Stable Cash

Flow Producing

Infrastructure Assets

Protection obtained from customers, contracts,

competitive positioning to ensure go forward

cash flow

> 75% of EBITDA backed by take-or-pay

contracts, long term agreements and/or reserve

dedications and will improve significantly into

2019 with 2 large projects anchored by long-

term take-or-pay contracts including 15 year

take-or-pay with an investment grade

counterparty*

Continue to increase long term contracts and

diversify to customers with strong balance

sheets

Recently sanctioned Pipestone Montney Sour

Deep Cut Plant anchored by 2 five year take-or-

pay contracts

Growing EBITDA, CFPS

and Share Value

Taking advantage of ongoing acquisition and

organic growth opportunities to increase per

share value via creativity of management team

Since the April 2015 IPO, EBITDA increased from

zero to current EBITDA of ~$80 million to late

2019 of ~$120 million

Relatively Undervalued

versus Comparable

Companies

Currently trading at an overly large discount to

the comparables given more conservative capital

structure and more easily achieved relative

growth rates

EV/EBITDA 2019E multiple of 6.25x vs. peer

average of 12.1x

... That Currently Provides a Low-Risk Attractive Investment

Opportunity

Attractive Investment Opportunity

1

2

3

4

* See “TransAlta LOI” under Disclaimer heading on page 2 of this presentation.

6

Consistently Driving Towards New Egress & Demand Tidewater continues to pursue additional egress options/new markets in addition to existing

process/storage infrastructure to yield better margins for our customers products

Tidewater has expanded/is expanding the capabilities of its network to include incremental markets for our customers products

Connecting Tidewater’s network to egress network of TCPL and Alliance

Frac commissioned

Railcar NGL facility constructed

Storage facilities commissioned

LOI signed for direct pipe connection to Transalta coal power plants being converted to natural gas

Further storage expansion/additions

Petrochemical plants that increase low cost local gas consumption

Power intense technology based facilities that benefit from low cost gas producing low cost power

Tidewater Incremental Egress & Demand Options

Gas Processing Networks and Egress Gas storage Petrochemical Technology/Power Industrial/Power

Montney Deep

BasinEdmonton

New

Pipestone

Gas Plant

New BRC

Frac

New Rail

Facility

TCPL and

Alliance

Connection

Montney Deep

Basin

Ethane

Demand

Propane

DemandCrypto

CurrencyBlockchain Manufacturing

Natural Gas

Demand

Butane

Demand

Ammonia GTL Methanol

Fertilizer

77

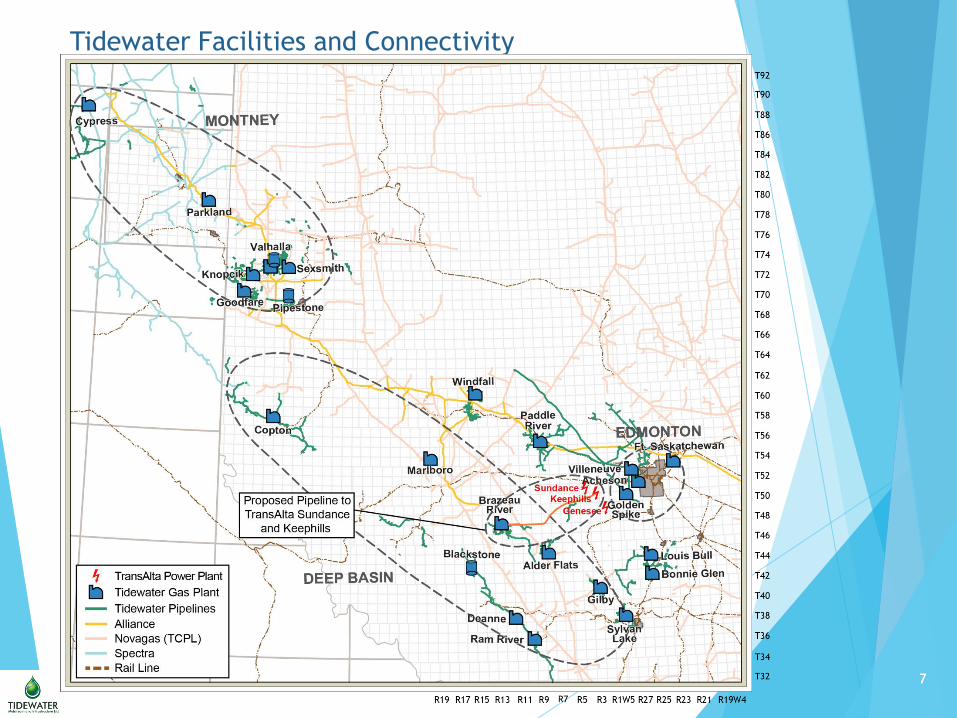

Tidewater Facilities and Connectivity

88

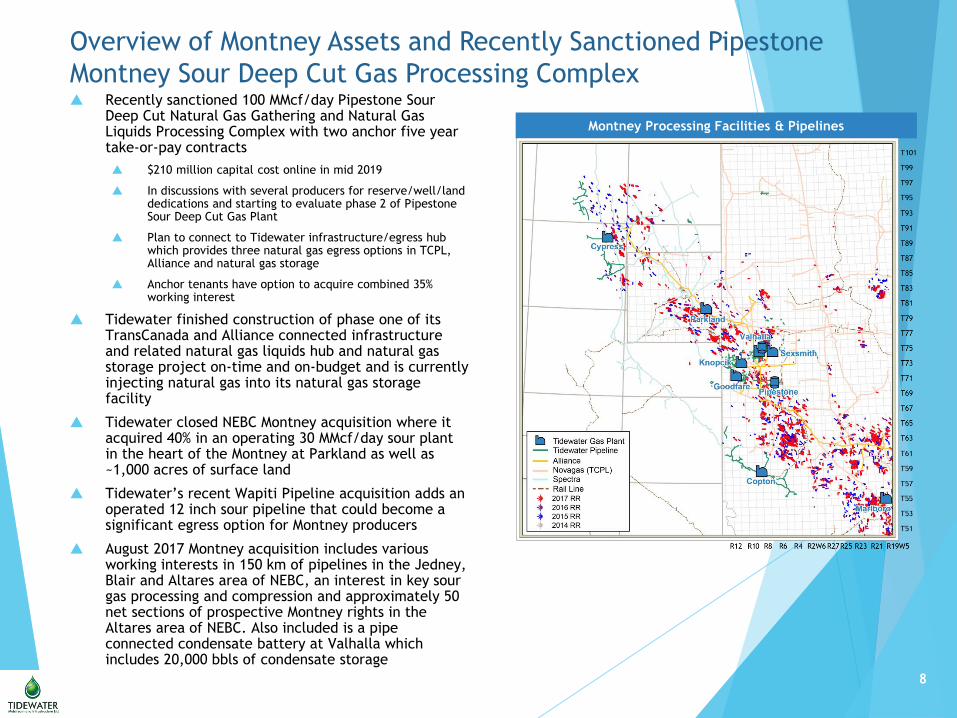

Overview of Montney Assets and Recently Sanctioned Pipestone

Montney Sour Deep Cut Gas Processing Complex

Montney Processing Facilities & Pipelines

Recently sanctioned 100 MMcf/day Pipestone Sour Deep Cut Natural Gas Gathering and Natural Gas Liquids Processing Complex with two anchor five year take-or-pay contracts

$210 million capital cost online in mid 2019

In discussions with several producers for reserve/well/land dedications and starting to evaluate phase 2 of Pipestone Sour Deep Cut Gas Plant

Plan to connect to Tidewater infrastructure/egress hub which provides three natural gas egress options in TCPL, Alliance and natural gas storage

Anchor tenants have option to acquire combined 35% working interest

Tidewater finished construction of phase one of its TransCanada and Alliance connected infrastructure and related natural gas liquids hub and natural gas storage project on-time and on-budget and is currently injecting natural gas into its natural gas storage facility

Tidewater closed NEBC Montney acquisition where it acquired 40% in an operating 30 MMcf/day sour plant in the heart of the Montney at Parkland as well as ~1,000 acres of surface land

Tidewater’s recent Wapiti Pipeline acquisition adds an operated 12 inch sour pipeline that could become a significant egress option for Montney producers

August 2017 Montney acquisition includes various working interests in 150 km of pipelines in the Jedney, Blair and Altares area of NEBC, an interest in key sour gas processing and compression and approximately 50 net sections of prospective Montney rights in the Altares area of NEBC. Also included is a pipe connected condensate battery at Valhalla which includes 20,000 bbls of condensate storage

99

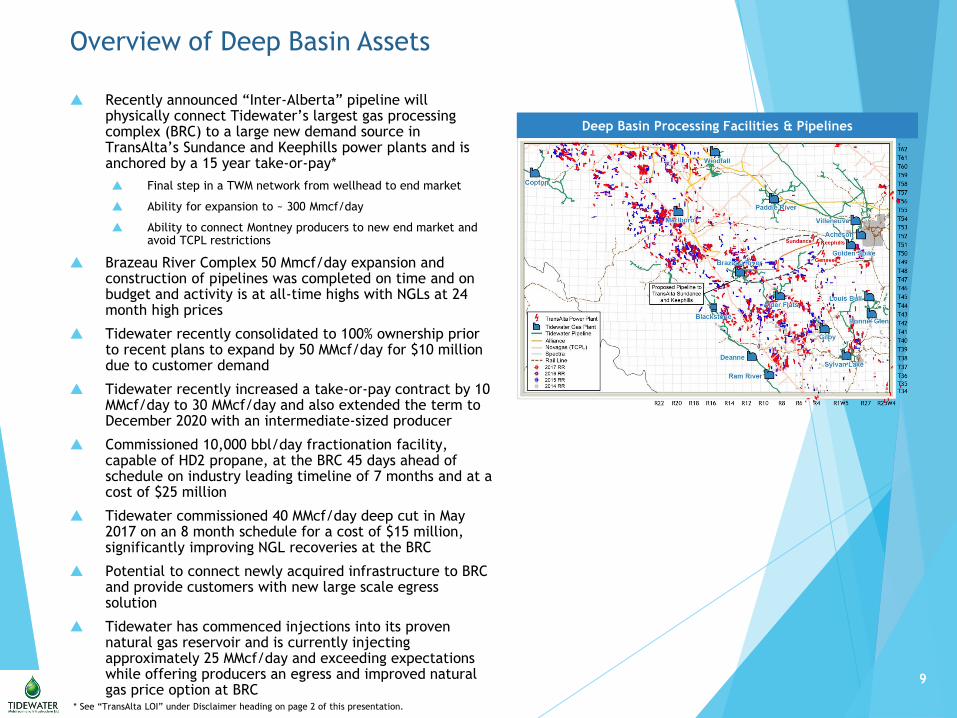

Overview of Deep Basin Assets

Deep Basin Processing Facilities & Pipelines

Recently announced “Inter-Alberta” pipeline will physically connect Tidewater’s largest gas processing complex (BRC) to a large new demand source in TransAlta’s Sundance and Keephills power plants and is anchored by a 15 year take-or-pay*

Final step in a TWM network from wellhead to end market

Ability for expansion to ~ 300 Mmcf/day

Ability to connect Montney producers to new end market and avoid TCPL restrictions

Brazeau River Complex 50 Mmcf/day expansion and construction of pipelines was completed on time and on budget and activity is at all-time highs with NGLs at 24 month high prices

Tidewater recently consolidated to 100% ownership prior to recent plans to expand by 50 MMcf/day for $10 million due to customer demand

Tidewater recently increased a take-or-pay contract by 10 MMcf/day to 30 MMcf/day and also extended the term to December 2020 with an intermediate-sized producer

Commissioned 10,000 bbl/day fractionation facility, capable of HD2 propane, at the BRC 45 days ahead of schedule on industry leading timeline of 7 months and at a cost of $25 million

Tidewater commissioned 40 MMcf/day deep cut in May 2017 on an 8 month schedule for a cost of $15 million, significantly improving NGL recoveries at the BRC

Potential to connect newly acquired infrastructure to BRC and provide customers with new large scale egress solution

Tidewater has commenced injections into its proven natural gas reservoir and is currently injecting approximately 25 MMcf/day and exceeding expectations while offering producers an egress and improved natural gas price option at BRC

* See “TransAlta LOI” under Disclaimer heading on page 2 of this presentation.

1010

Overview of Edmonton Assets

Edmonton Processing Facilities & Pipelines

Tidewater has over 800 km of key pipelines and valuable right of ways at Edmonton, 600 acres of heavy industrial land at Edmonton/Fort Saskatchewan, and 3 key extraction plant licenses

Edmonton assets provide egress/takeaway options for natural gas and NGL production throughout the Deep Basin and Tidewater is now tied into some of the largest industrial consumers of natural gas in Western Canada

Over the next 2 to 3 years, Tidewater plans to build out its Edmonton Energy Hub on its 600 acres of heavy industrial land and improve connectivity to major hubs at Edmonton

Includes the potential for propylene and polypropylene production and/or iso-octane production as Tidewater has received several expressions of interest from various off-take and joint venture parties who Tidewater management has worked with in the past for these products

Tidewater anticipates a significant improvement in margins by eliminating third party rail transloading fees, eliminating trucking costs and reduced pipeline tariffs at the Acheson facility

Fort Saskatchewan Ethane Extraction plant successfully reactivated and online and on-time and on-budget at >100% IRR

In May 2017 closed the acquisition of a 70 MMcf/day deep cut facility and successfully reactivated the facility in July 2017 ahead of schedule and under budget

11

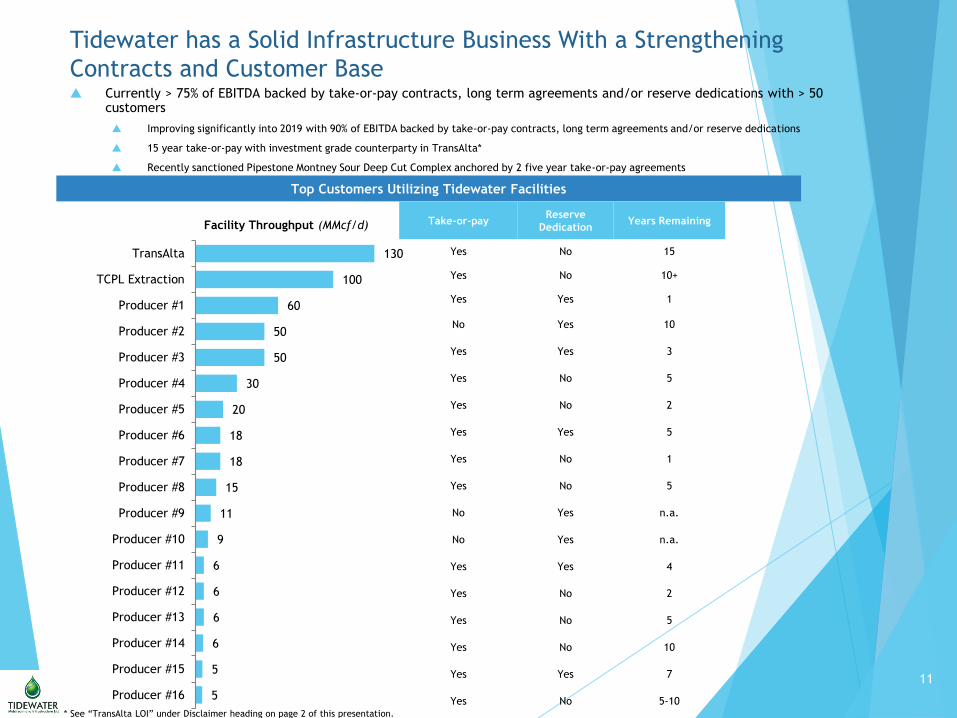

Tidewater has a Solid Infrastructure Business With a Strengthening

Contracts and Customer Base Currently > 75% of EBITDA backed by take-or-pay contracts, long term agreements and/or reserve dedications with > 50

customers

Improving significantly into 2019 with 90% of EBITDA backed by take-or-pay contracts, long term agreements and/or reserve dedications

15 year take-or-pay with investment grade counterparty in TransAlta*

Recently sanctioned Pipestone Montney Sour Deep Cut Complex anchored by 2 five year take-or-pay agreements

Top Customers Utilizing Tidewater Facilities

Facility Throughput (MMcf/d)

5

5

6

6

6

6

9

11

15

18

18

20

30

50

50

60

100

130

Producer #16

Producer #15

Producer #14

Producer #13

Producer #12

Producer #11

Producer #10

Producer #9

Producer #8

Producer #7

Producer #6

Producer #5

Producer #4

Producer #3

Producer #2

Producer #1

TCPL Extraction

TransAlta

Take-or-payReserve

DedicationYears Remaining

Yes No 15

Yes No 10+

Yes Yes 1

No Yes 10

Yes Yes 3

Yes No 5

Yes No 2

Yes Yes 5

Yes No 1

Yes No 5

No Yes n.a.

No Yes n.a.

Yes Yes 4

Yes No 2

Yes No 5

Yes No 10

Yes Yes 7

Yes No 5-10* See “TransAlta LOI” under Disclaimer heading on page 2 of this presentation.

12

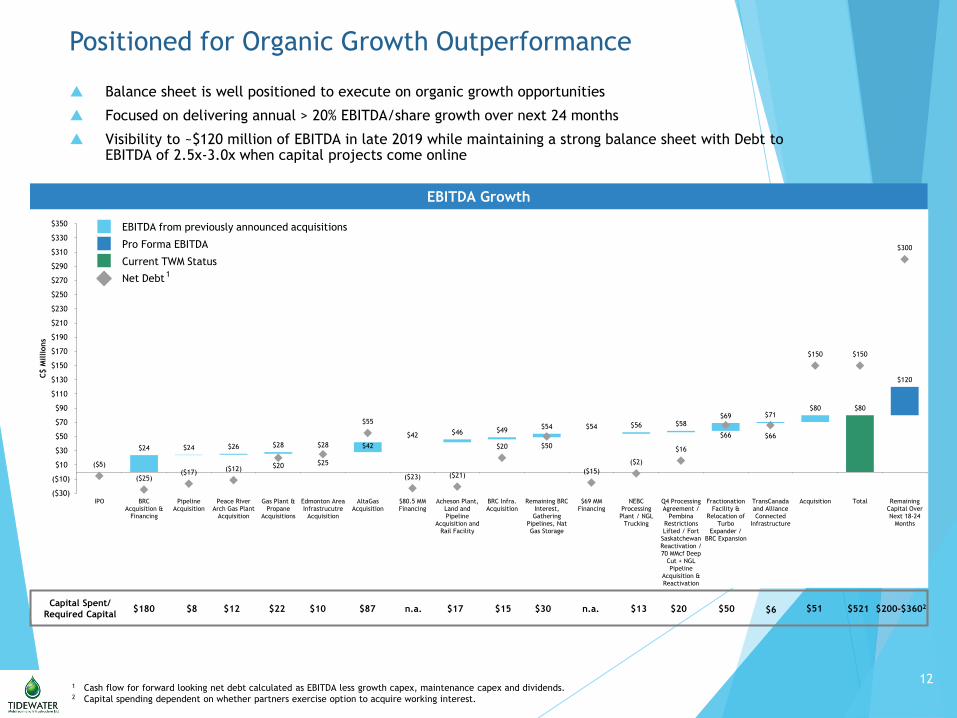

$54

$80

-

$24 $24 $26 $28 $28 $42

$42 $46 $49 $54 $54 $56 $58

$69 $71 $80 $80

$120

($5)

($25)($17)

($12) $20 $25

$55

($23) ($21)

$20 $50

($15)

($2)

$16

$66 $66

$150 $150

$300

($30)

($10)

$10

$30

$50

$70

$90

$110

$130

$150

$170

$190

$210

$230

$250

$270

$290

$310

$330

$350

IPO BRCAcquisition &

Financing

PipelineAcquisition

Peace RiverArch Gas Plant

Acquisition

Gas Plant &Propane

Acquisitions

Edmonton AreaInfrastrucutre

Acquisition

AltaGasAcquisition

$80.5 MMFinancing

Acheson Plant,Land andPipeline

Acquisition andRail Facility

BRC Infra.Acquisition

Remaining BRCInterest,Gathering

Pipelines, NatGas Storage

$69 MMFinancing

NEBCProcessing

Plant / NGLTrucking

Q4 ProcessingAgreement /

PembinaRestrictionsLifted / Fort

SaskatchewanReactivation /70 MMcf Deep

Cut + NGLPipeline

Acquisition &Reactivation

FractionationFacility &

Relocation ofTurbo

Expander /BRC Expansion

TransCanadaand AllianceConnected

Infrastructure

Acquisition Total RemainingCapital OverNext 18-24

Months

C$ M

illions

Positioned for Organic Growth Outperformance

EBITDA Growth

EBITDA from previously announced acquisitions

Net Debt

Pro Forma EBITDA

Capital Spent/

Required Capital$180 $8 $12 $22 $10 $87 n.a. $17 n.a. $20 $50 $6 $521

Current TWM Status

$200–$3602

1 Cash flow for forward looking net debt calculated as EBITDA less growth capex, maintenance capex and dividends.2 Capital spending dependent on whether partners exercise option to acquire working interest.

1

$15 $30 $13 $51

Balance sheet is well positioned to execute on organic growth opportunities

Focused on delivering annual > 20% EBITDA/share growth over next 24 months

Visibility to ~$120 million of EBITDA in late 2019 while maintaining a strong balance sheet with Debt to EBITDA of 2.5x-3.0x when capital projects come online

13

Date Asset Type Buyer Seller Description Value ($MM) EBITDA Multiple Contract Disclosure

2/6/2018NGL and Gas Pipeline &

FractionationStonepeak Targa Resources

Development JVs on Grand Prix Pipeline, Gulf Coast

Express Pipeline and Frac Train$960 - Volume Commitment

1/8/2018 Gas G&PRiverstone

Goldman SachsLucid Energy Group

The JV acquired Lucid Energy II from Lucid Energy, a

portfolio company of EnCap Flatrock

Lucid II owns 1,700 miles of gas gathering pipelines

and 585 MMcf/d processing capacity in norhern

Delaware Basin

$1,600 -Area Dedication & Volume

Commitment

11/9/2017 Crude Pipeline BlackRockNGL Energy Partners

SemGroup CorpGlass Mountain Pipeline (SemGroup 50/NGL 50) $600 24.0x ToP & Area Dedication

10/2/2017 Crude Pipeline GIPEnergy & Minerals Group

Laredo Petroleum Medallion Pipeline (EMG 51/Laredo 49) $1,825 34.5x Area Dedication

8/1/2017 Gas Pipeline Blackstone Energy Transfer Partners 32.44% stake in Rover Pipeline $1,570 12.5x ToP

6/6/2017 Terminal SemGroup Alinda Capital Partners Houston Fuel Oil Terminal Company $2,100 15.0x ToP

4/17/2017 Gas G&P Blackstone EnCap Flatrock EagleClaw Midstream Ventures $2,000 26.7x Fee Based

2/9/2017 Gas Gathering System Williams Partners Western Gas Partners33.75% stake in Roma and Liberty gathering systems

through asset swap$155 16.5x -

High Multiple US Midstream Deals

Source: PLS, Company Filings, Equity Research, Credit Research.1 Reflects annualized cash flow currently as outlined on conference call. Transcript references high teens multiple with addition of Omega expansion project.2 Based on annualized 1H2017 adjusted EBITDA.3 Based on expected first year EBITDA (pro rata).4 Based on SemGroup guidance 2018E EBITDA.5 Based on 2017E EBITDA from Moody's analysis on May 30, 2017.6 Based on Q1-Q3 2016 annualized adjusted EBITDA.

1

4

5

6

2

3

14

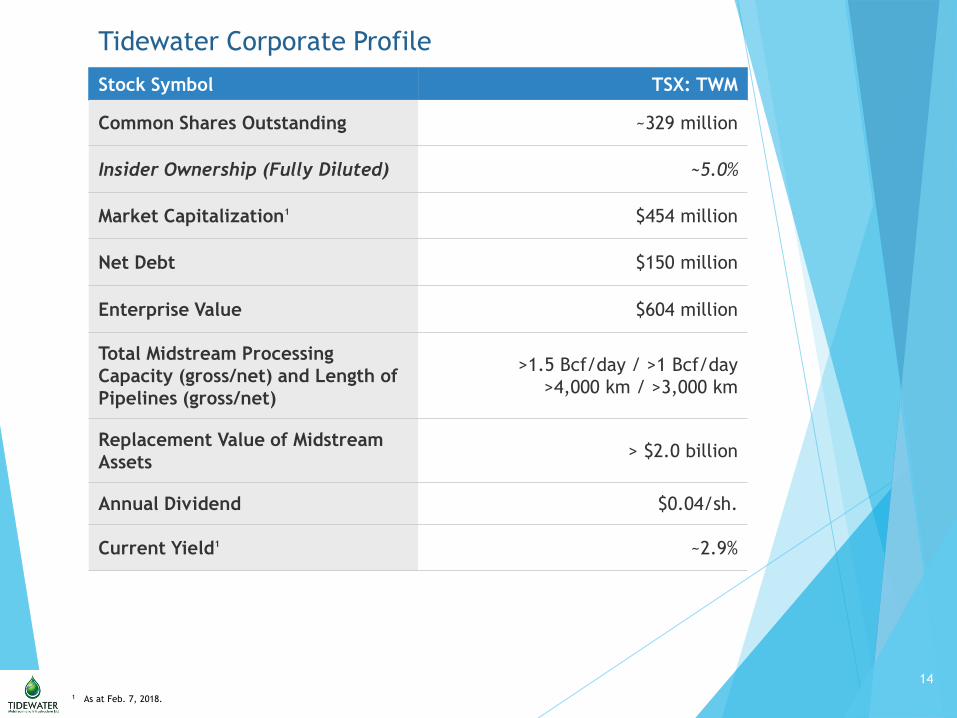

Stock Symbol TSX: TWM

Common Shares Outstanding ~329 million

Insider Ownership (Fully Diluted) ~5.0%

Market Capitalization1 $454 million

Net Debt $150 million

Enterprise Value $604 million

Total Midstream Processing

Capacity (gross/net) and Length of

Pipelines (gross/net)

>1.5 Bcf/day / >1 Bcf/day

>4,000 km / >3,000 km

Replacement Value of Midstream

Assets> $2.0 billion

Annual Dividend $0.04/sh.

Current Yield1 ~2.9%

Tidewater Corporate Profile

1 As at Feb. 7, 2018.

15

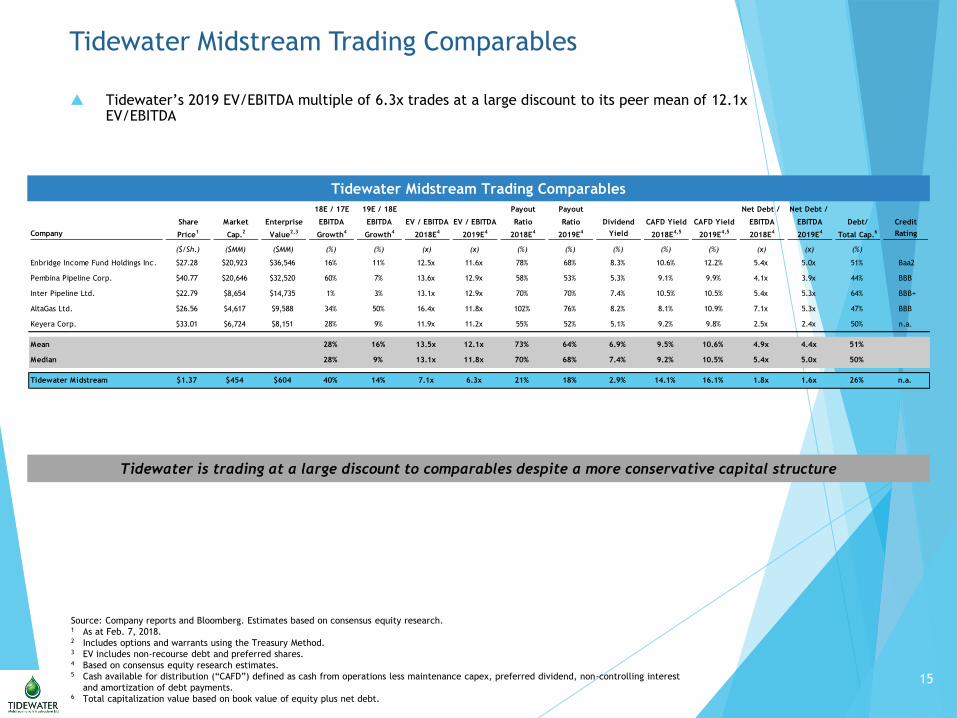

Tidewater Midstream Trading Comparables

Source: Company reports and Bloomberg. Estimates based on consensus equity research.1 As at Feb. 7, 2018.2 Includes options and warrants using the Treasury Method.3 EV includes non-recourse debt and preferred shares.4 Based on consensus equity research estimates.5 Cash available for distribution (“CAFD”) defined as cash from operations less maintenance capex, preferred dividend, non-controlling interest

and amortization of debt payments.6 Total capitalization value based on book value of equity plus net debt.

Tidewater is trading at a large discount to comparables despite a more conservative capital structure

Tidewater’s 2019 EV/EBITDA multiple of 6.3x trades at a large discount to its peer mean of 12.1x EV/EBITDA

Tidewater Midstream Trading Comparables

18E / 17E 19E / 18E Payout Payout Net Debt / Net Debt /

Share Market Enterprise EBITDA EBITDA EV / EBITDA EV / EBITDA Ratio Ratio Dividend CAFD Yield CAFD Yield EBITDA EBITDA Debt/ Credit

Company Price1

Cap.2

Value2,3

Growth4

Growth4

2018E4

2019E4

2018E4

2019E4 Yield 2018E

4,52019E

4,52018E

42019E

4Total Cap.

6 Rating

($/Sh.) ($MM) ($MM) (%) (%) (x) (x) (%) (%) (%) (%) (%) (x) (x) (%)

Enbridge Income Fund Holdings Inc. $27.28 $20,923 $36,546 16% 11% 12.5x 11.6x 78% 68% 8.3% 10.6% 12.2% 5.4x 5.0x 51% Baa2

Pembina Pipeline Corp. $40.77 $20,646 $32,520 60% 7% 13.6x 12.9x 58% 53% 5.3% 9.1% 9.9% 4.1x 3.9x 44% BBB

Inter Pipeline Ltd. $22.79 $8,654 $14,735 1% 3% 13.1x 12.9x 70% 70% 7.4% 10.5% 10.5% 5.4x 5.3x 64% BBB+

AltaGas Ltd. $26.56 $4,617 $9,588 34% 50% 16.4x 11.8x 102% 76% 8.2% 8.1% 10.9% 7.1x 5.3x 47% BBB

Keyera Corp. $33.01 $6,724 $8,151 28% 9% 11.9x 11.2x 55% 52% 5.1% 9.2% 9.8% 2.5x 2.4x 50% n.a.

Mean 28% 16% 13.5x 12.1x 73% 64% 6.9% 9.5% 10.6% 4.9x 4.4x 51%

Median 28% 9% 13.1x 11.8x 70% 68% 7.4% 9.2% 10.5% 5.4x 5.0x 50%

Tidewater Midstream $1.37 $454 $604 40% 14% 7.1x 6.3x 21% 18% 2.9% 14.1% 16.1% 1.8x 1.6x 26% n.a.