february 2011 management presentation madrid … · and other statements pertaining to our future...

TRANSCRIPT

Company ProfileCompany Profile

Management PresentationMeeting the Financial Community

Madrid, 15 February 2011Michele Cinaglia, ChairmanNiccolò Bossi, M&A and IR

Forward looking stateForward looking statementment 11

This communication contains statements that constitute “forward-looking statements,”including (but not limited to) statements related to the implementation of strategic initiatives and other statements pertaining to our future business development and economic performance. While these forward-looking statements represent our judgments and future expectations concerning the development of our business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations. These factors include but are not limited to: (1) general market and macro-economic trends, (2) legislative developments, governmental and regulatory trends, (3) competitive pressures, (4) technological developments, (5) changes in the financial position or creditworthiness of our customers, obligors and counterparties, and developments in the markets in which they operate, (6) management changes and changes to our Business Group structure and (7) other key factors that we have indicated could adversely affect our business and financial performance, such factors being described elsewhere in this document and in our past and future filings and reports.

Engineering is not under any obligation to (and expressly disclaims any such obligation to) update or alter its forward-looking statements, whether as a result of new information, future events, or otherwise.

For additional information on such risks, we ask you to consult Engineering’s filings with Borsa Italiana and CONSOB as well as to consult the applicable Italian laws.

Engineering at a glanceEngineering at a glance 22

Engineering is the major Italian Information Technology Group and a leading IT multinational in Italy, Europe and Latin America. It is ranked as the fifth company in its sector over the Italian market, according to annual revenues. In 2009, revenues reached €724.0 M, of which nearly 7% came from the international market and EBITDA exceeded €93.6 M. The company employs more than 6,400 professionals and approximately 2,000 external resources, and boasts a customer portfolio of over 1000 firms, with operations in 37 sites in Italy and three abroad.The company enjoys a healthy financial position, with a net debt of €49.3 M as of September 2010 (0.57x EBITDA 2009). Further, it expects a significant improvement by the end of the year.

The Group, has gradually evolved from a pure System Integrator to an Integrated IT Solutions and Services Provider, with an offering that ranges from system integration and consultancy, the outsourcing of IT systems and business processes, application management and software development.These business lines, which operate across the vertical divisions, drive the Group’s performance, which exceeds that of the corresponding market.

OutlineOutline

CAGR 00CAGR 00--09 09 ItalianItalian IT MarketIT Market 1.6%1.6%

CAGR 00CAGR 00--09 Engineering 09 Engineering RevenuesRevenues 16.5%16.5%Source Assinform, EITO, JCF

Brasil

Belgium

Italy

Delaware (USA)

Engineering, listed since December 2000 on the Milan Stock Exchange FTSE STAR segment, maintains a simple ownership structure with 67% held by the two founders (Mr. Cinaglia and Mr. Amodeo), with the remaining 33% being free-floating.Major financial institutions focused on long-term investments continue to bet on the stock, aware of the strength of the Group’s business model and the reliability of the Management.Since the IPO, the Group has concluded several extraordinary deals.Thanks to an accurate scouting approach and attentive deal execution, Engineering has consistently integrated assets and people in order to broaden the spectrum of owned solutions and to reach a wider potential customers portfolio.

Servizi Telematici Siciliani

Engineering at a glanceEngineering at a glance 33

StructureStructure

ENGINEERING INTERNATIONAL BELGIUM

ENGIWEB SECURITY

OVER IT

ENGINEERING.IT

ENGINEERING SARDEGNA

SITEL

NEXEN

ENGINEERING TRIBUTI

ENGO

ENGINEERING DO BRASIL

75%

100%

95%

100%

70%

60% 100%

100%

100%

25%

75%

25%

ENGINEERING INTERNATIONAL INC.

100%

100%

Sicilia e Servizi Venture

65%

Cinaglia Family

Amodeo Family

Market

Outstanding Participations

35%35%

32%32%

12%12%

21%21%

Ownership Structure as of 30 September 2010. Mkt Cap 10 Feb 2010

FreeFree FloatFloat 33%33%

# shares: 12,500,000

Current Mkt Cap: 291M

IT SectorIT Sector 44

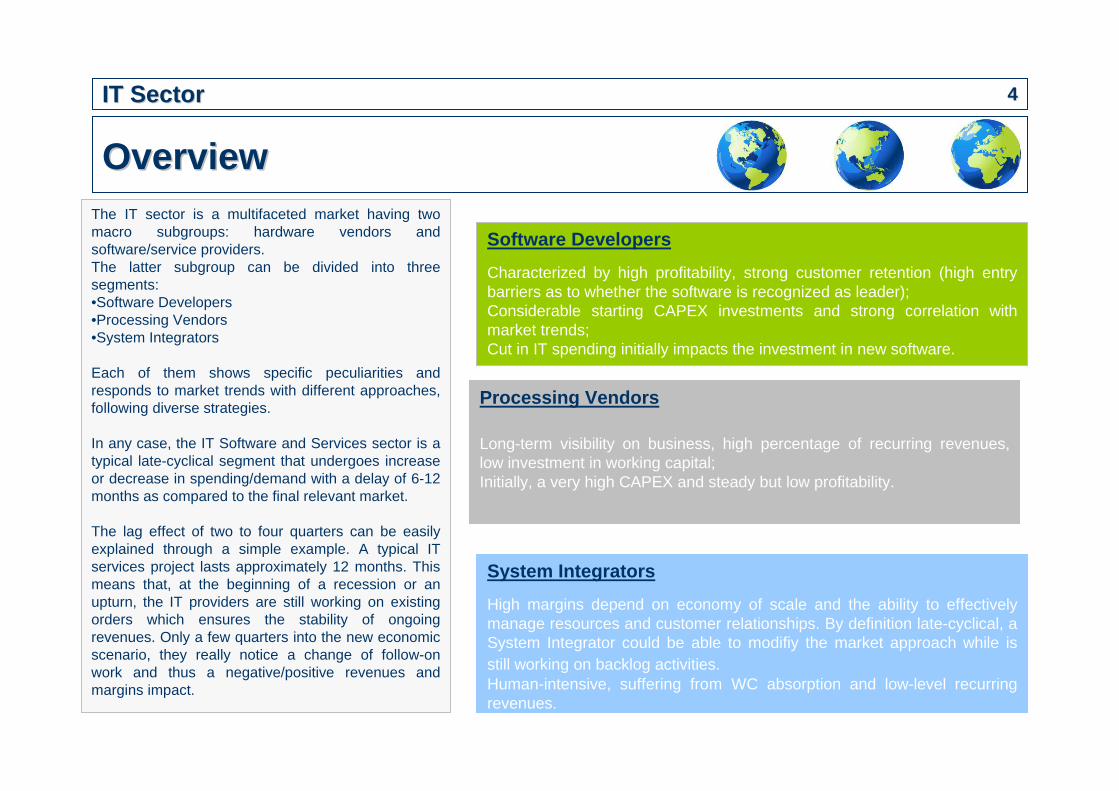

OverviewOverviewThe IT sector is a multifaceted market having two macro subgroups: hardware vendors and software/service providers.The latter subgroup can be divided into three segments:•Software Developers•Processing Vendors•System Integrators

Each of them shows specific peculiarities and responds to market trends with different approaches, following diverse strategies.

In any case, the IT Software and Services sector is a typical late-cyclical segment that undergoes increase or decrease in spending/demand with a delay of 6-12 months as compared to the final relevant market.

The lag effect of two to four quarters can be easily explained through a simple example. A typical IT services project lasts approximately 12 months. This means that, at the beginning of a recession or an upturn, the IT providers are still working on existing orders which ensures the stability of ongoing revenues. Only a few quarters into the new economic scenario, they really notice a change of follow-on work and thus a negative/positive revenues and margins impact.

Software Developers

Characterized by high profitability, strong customer retention (high entry barriers as to whether the software is recognized as leader);Considerable starting CAPEX investments and strong correlation withmarket trends;Cut in IT spending initially impacts the investment in new software.

Processing Vendors

Long-term visibility on business, high percentage of recurring revenues, low investment in working capital;Initially, a very high CAPEX and steady but low profitability.

System Integrators

High margins depend on economy of scale and the ability to effectivelymanage resources and customer relationships. By definition late-cyclical, a System Integrator could be able to modifiy the market approach while isstill working on backlog activities.Human-intensive, suffering from WC absorption and low-level recurringrevenues.

IT SectorIT Sector 55

Changes in Changes in clientclient demandsdemands

RationalisationRationalisationMergersMergersCostCost--CuttingCutting

SupplierSupplier ConsolidationConsolidation

NeedNeed ResponseResponse EffectEffect

New TechnologiesNew TechnologiesNew New UtilisationUtilisationCompetitive Competitive AdvantageAdvantage

ConsultancyConsultancySystem System IntegrationIntegrationOutsourcingOutsourcing

FocusFocus on on valuevalueInvestmentsInvestments in in R&DR&DSoftware Software developmentdevelopmentBusinessBusiness--criticalcritical solutionssolutions

Broad proposition and goodmarket understanding Strong IT Strong IT playerplayer selectionselectionBusinessBusiness

EconomicsEconomicsAggregationAggregation of of activitiesactivities in fullin full--service service contractscontracts withwith a a flexibleflexible, ,

economicaleconomical structurestructure

EmphasisEmphasis on on marginsmargins forfor lowlowprofileprofile servicesservices and premium and premium

forfor HVA HVA solutionssolutions

Engineering Engineering -- Business ModelBusiness Model 66

OrganizationOrganization

ERP ECMIT Security

Plant ManagementSystem Broadband & MediaManaged Operations

System System Int.Int. & & ConsultancyConsultancy

OutsourcingOutsourcing

SoftwareSoftware

Finance Industry Telco UtilitiesResearchResearch and and DevelopmentDevelopment

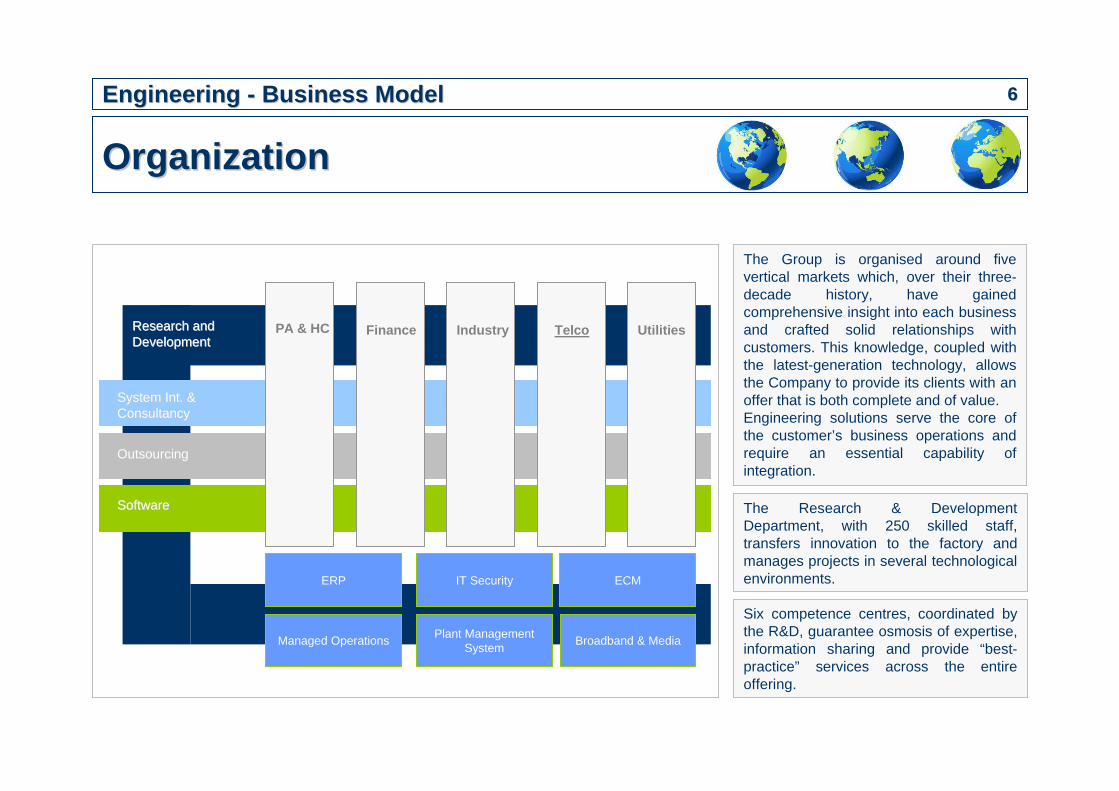

The Research & Development Department, with 250 skilled staff, transfers innovation to the factory and manages projects in several technological environments.

The Group is organised around five vertical markets which, over their three-decade history, have gained comprehensive insight into each business and crafted solid relationships with customers. This knowledge, coupled with the latest-generation technology, allows the Company to provide its clients with an offer that is both complete and of value.Engineering solutions serve the core of the customer’s business operations and require an essential capability of integration.

Six competence centres, coordinated by the R&D, guarantee osmosis of expertise, information sharing and provide “best-practice” services across the entire offering.

PA & HC

Engineering Engineering -- Business ModelBusiness Model 77

Projects delivered abroad 7% of total revenue

OperationsOperations

38.938.9

PA & HCPA & HC

System Integration and Consultancy

Outsourcing and AM

Software

53.153.1

35.735.7

11.211.2

IndustryIndustry** FinanceFinance

TLCTLC

27.927.9 22.722.710.510.5

From Official 2010 1H AccountsSplit by Business Lines and

Markets% on Net Revenues

*Industry-aggregate utilities

Engineering Engineering -- Business ModelBusiness Model 88

Customer BaseCustomer Base

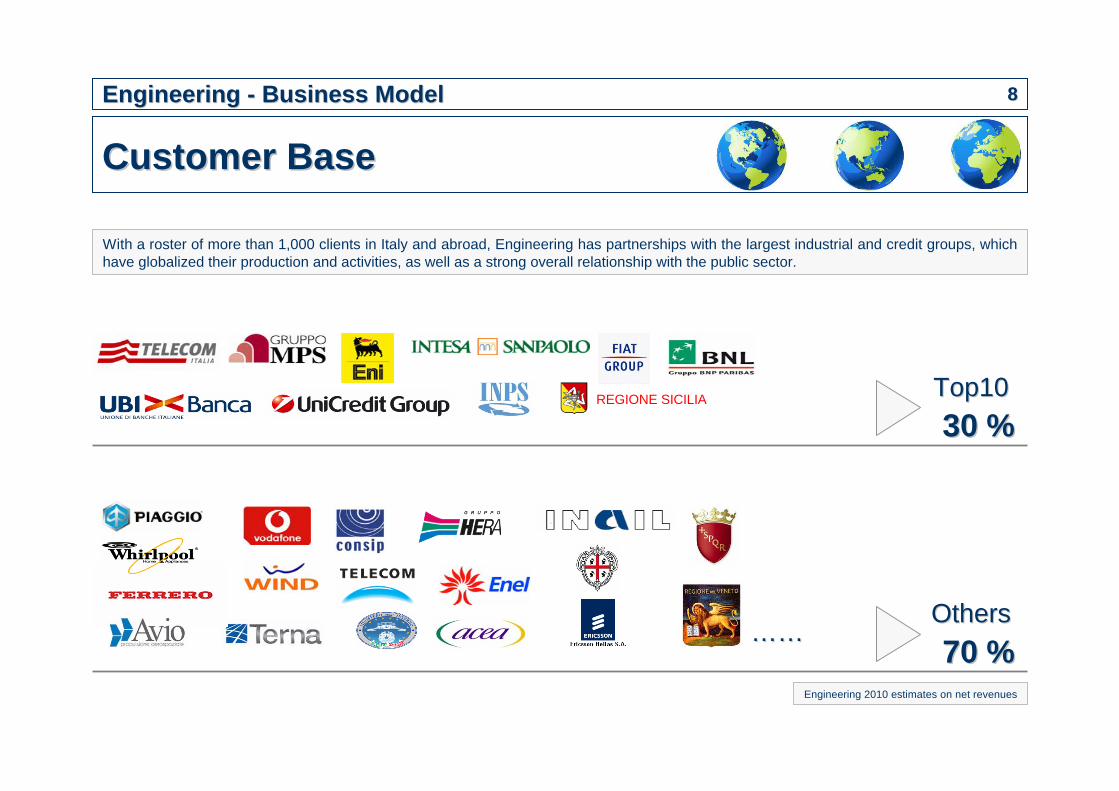

With a roster of more than 1,000 clients in Italy and abroad, Engineering has partnerships with the largest industrial and credit groups, which have globalized their production and activities, as well as a strong overall relationship with the public sector.

30 %30 %REGIONE SICILIA

70 %70 %

Top10Top10

OthersOthers…………

Engineering 2010 estimates on net revenues

Engineering Engineering -- Business ModelBusiness Model 99

Margins & Contract LengthsMargins & Contract Lengths

ContractContract lengthlength

MarginsMargins

System System IntegrationIntegration

ConsultancyConsultancy

AMAM

OutsourcingOutsourcing

Software Software licensinglicensing and and maintenancemaintenance feesfees

1Y1Y0%0% 2Y2Y 3Y3Y 4Y4Y 5Y5Y

Group EBITDAGroup EBITDA

VISIBILITYVISIBILITY

Working Capital REQUIREMENTWorking Capital REQUIREMENT

++++--

--

RecurringRecurringCustomCustom

6m6m

Strategic analysisStrategic analysis

SWOTSWOT

1010

Quality of management and skilled staffVery high customer retentionExperience and successful track record in M&A dealsBusiness model with high entry barriers, broad

proposition and predictable evolution

StrengthsStrengths WeaknessesWeaknesses

Limited geographic diversificationInvestment in WC due to PA exposureInsufficient liquidity of stock

OpportunitiesOpportunities

EU Commission contractsConsolidator over the Italian ICT market thanks to a

sound financial structure and a leadership positionGrowing revenues visibility and better cash flow due

to the outsourcing of service offeringsSteady growth of Brazilian activities (higher

profitability, lower tax rate, booming market)

Flat situation of the relevant ICT Italian marketStress on prices

RisksRisks

SWOTSWOT

1111

QualityQuality of Management and of Management and skilledskilledstaffstaff

The CEO and front-line TOP Management of the Group are instrumental in developing the business strategy of the Group and forging customer relationships. Furthermore, they are able to keepup with technology, business and regulatory changes whilemaintaining a clear understanding of the direct and indirect effectson the market.

A key factor in success is also dependent upon our ability toattract, train and retain highly skilled technical and salespersonnel.

We have a history of successful relationships with the mostimportant Italian firms-banks and the public administration.The top players in every different market/sector are provided byEngineering with solutions and services since the 1980s.

Our market share and the retention rate of our clients, along withhigh customer satisfaction, are essential to an understanding of our leadership.

We have grown continuously over the past 30 years, thanks toan attentive and balanced strategy of internal and externalinvestments.We have made and will continue to make acquisitions of companies, products and technologies we believe couldcomplement or expand our business, augment our market coverage, enhance our technical capabilities or offer growthopportunities.Our success also depends on our ability to complete the integration of acquired business in an efficient and effectivemanner.

It doesn’t exist in our cluster of comparables, nor is any othercompany able to provide clients with the full array of solutionswithin our range of capabilities.

The very good mix among software development, system integration and outsourcing creates a virtuoso circle thatenables Engineering to convey its broad proposition effectivelyand with high returns.

VeryVery high high customercustomer retentionretention

ExperienceExperience and and successfulsuccessful track track record in record in M&AM&A dealsdeals

Business model Business model withwith high entry high entry barriersbarriers, , broadbroadpropositionproposition and and predictablepredictable evolutionevolution

StrengthsStrengths

Strategic analysisStrategic analysis

OutlookOutlook

FY10EFY10E

Guidance 730730--760760

Management Expectations

ValueValue of Productionof Production

Guidance

Management Expectations

EBITDAEBITDA

1212

Data in mln €. Source of Consensus: JCF. * NWC/Revenues

750750--760760Analyst Consensus 741741

Analyst Consensus8484--8888

8888> 88> 88

Management Expectations

NFPNFPAnalyst Consensus (24.6)(24.6)

(10 )(10 )

Our current expectations are in the high end of the guidance in terms of revenues and margins.Also, in comparison to the averageconsensus we are slightly ahead and definitively much better in terms of final net debt, where we approach a cash-positive position.All this is due to an extremely positive 4Q, which the Group is historically ableto achieve.Better-than-expected cash inflowmakes the net working capital investment ratio* at the end of the yearconsiderably lower than the ‘09 result.

The Group again demonstrates itsability to outperform the relevant market in a negative scenario, in which the outlook was unclear and IT spendingoverall has decreased to a markeddegree.

OutlookOutlook

Business expectationsBusiness expectations

1313

Business Business LinesLines

MarketMarket

System System IntegrationIntegration and and consultancyconsultancy

AM AM –– OutsourcingOutsourcing

SoftwareSoftware

PAPA

IndustryIndustry, , ServicesServices, , UtilitiesUtilities

FinanceFinance

TLCTLC

ShortShort--termterm trendtrend

==While the macroeconomic scenario seems to lack excitement and the IT spending trend appears flat or evendeclining, the diversification of the Group’s revenue stream and the dynamics of a consolidating market make the outlook less unfavourablethan some analysts might suggest.

We are incrementally more positive, looking at:• Robust growth in demand of Outsourcing services;• A double-digit rise in revenues fromforeign activities;• The outset of some large and long-term projects with the public and private sectors (FS and EU Commision);• A moderate recovery of booking in the TLC sector;• A sound financial position and a market leadership that could boost new M&A deals in Italy and abroad.

It is worth noting that the introduction of new rules on risk management and compliance in the Finance sector couldrepresent a trigger for the software business line (which is known as a higher-margin business).

EconomicsEconomics

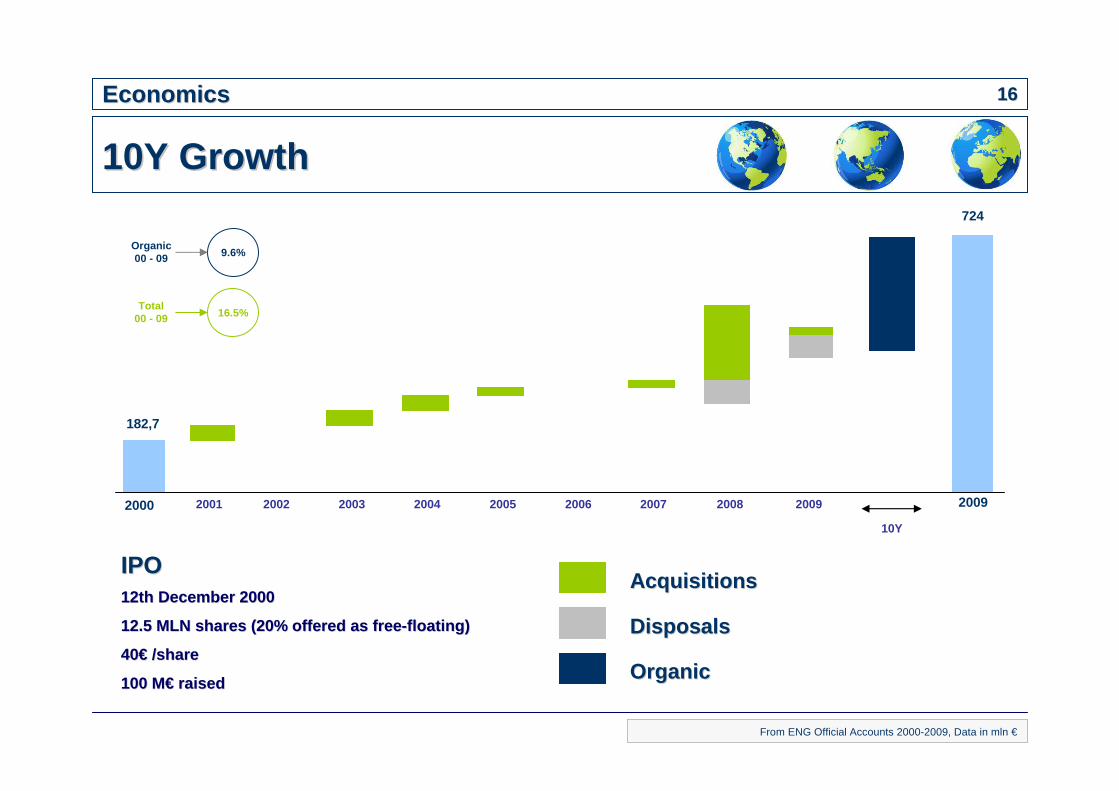

10Y 10Y GrowthGrowth

1414

256,5276,1

322,3

388,3

182,7215,8

425,6

CAGR00 - 09 16.5%

457.1

737.8724

305319

328371

212277

400

CAGR00 - 09 14.7%

456

746727.7

ValueValue of Productionof Production OrdersOrders

9.3%9.3%

12.5%12.5%13.4%*13.4%*

16.0%16.0%

6.8%6.8%

EBITDA %EBITDA %

IASIAS

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

AtosAtos

EU ICT EU ICT CompaniesCompanies

Engineering GroupEngineering Group

200254

260257

88140

248

CAGR00 - 09 19.4%

261

417

433

BacklogBacklog

Source Assinform, EITO, JCF From ENG Official Accounts 2000-2009, Data in mln €, Margins on net revenues. 2009 EBITDA resulting from extraordinay contribution of some 5mln € (12.7% net)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

EconomicsEconomics

10Y 10Y GrowthGrowth

1155

137165

176195

129 132

217

CAGR00 - 09 8.3%

232 234264

232

332374

457

207217

512

CAGR00 - 09 16.2%

516

822 801EquityEquity AssetsAssets

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

From ENG Official Accounts 2000-2009, Data in mln €

Capital Capital EmployedEmployed

82

124156

212

5479

237CAGR00 - 09 21.1%

227

264

302

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 NFPNFP

74.853.1

55.140.5

26.4

(17.1)(20.3)

5.1

(30)(38)

Cash

Debt

NFP

EconomicsEconomics

10Y 10Y GrowthGrowth

1166

From ENG Official Accounts 2000-2009, Data in mln €

182,7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

IPOIPO12th 12th DecemberDecember 20002000

12.5 MLN 12.5 MLN sharesshares (20% (20% offeredoffered asas freefree--floatingfloating))

4040€€ /share/share

100 100 MM€€ raisedraised

724

2009

AcquisitionsAcquisitions

DisposalsDisposals

OrganicOrganic

Organic00 - 09 9.6%

Total00 - 09 16.5%

10Y

Financial CommunityFinancial Community

AnalystAnalyst coveragecoverage

1717

SpecialistSpecialist sincesince 20112011

CoverageCoverage sincesince 20072007

CoverageCoverage sincesince 20072007CoverageCoverage sincesince 20092009

CoverageCoverage sincesince 20032003

FormerFormer SpecialistSpecialist and and CoverageCoverage sincesince20082008

Company ProfileCompany Profile 1818

Thanks for yourattention!

Engineering Ingegneria Informatica SPAVia San Martino della Battaglia 5600185 ROMA – ItalyTel. +39 06 49 20 11www.eng.it

Niccolò BossiDirector of M&A and Investor RelationsStrada 1, Palazzo F/720090 Assago Milanofiori, MI – ItalyTel. + 39 02 66 72 [email protected]