factors affecting pev sales in california: 2010-2015

TRANSCRIPT

Factors Affecting PEV Sales in California: 2010-2015

J.R. DeShazo, Tamara Sheldon, Richard Carson, SamuelKrumholz

ARB Research Seminar: September 12, 2017 Sacramento, California

Overview of Topics

1. PEV sales in California: temporal & spatial 2. Factors predicting PEV Sales 3. Rebate uptake and new vehicle introductions 4. Effects of HOV-lane access on PEV sales 5. Demand for BEVs and PHEVs* 6. Effects of rebate policies on PEV sales 7. Correlation of gas prices with PEV sales

*The data set used and the findings of this project relate to state of the market and the CVRP program circa 2013 and are not 2representative of the current market or program.

Selected High-level Findings

• Growth has been rapid but spatially concentrated.

• Have not yet reached typical middle incomehybrid buyers.

• HOV-lane access has had the largest effect compared to other policies but varies spatially.

• Rebate policies have had positive influence on sales.

• Falling gas prices are negatively correlated with PEV sales.

3

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Data Behind the Study

• PEV Sales only California 2010-2015 – Census tract, county, region – HIS, AFDC, ACS, State voting data

• HOV analysis based through 2014 • New Car Buyer Survey 2014 State-wide • Gas Prices and PEV Sales 2010-2015

4

UCLA _J~k1n S..-hlwl :),/ l'ubli,;: AffJ.irs

Luskin Center FOCI INNOVATION

Broader Context

5

■ ■

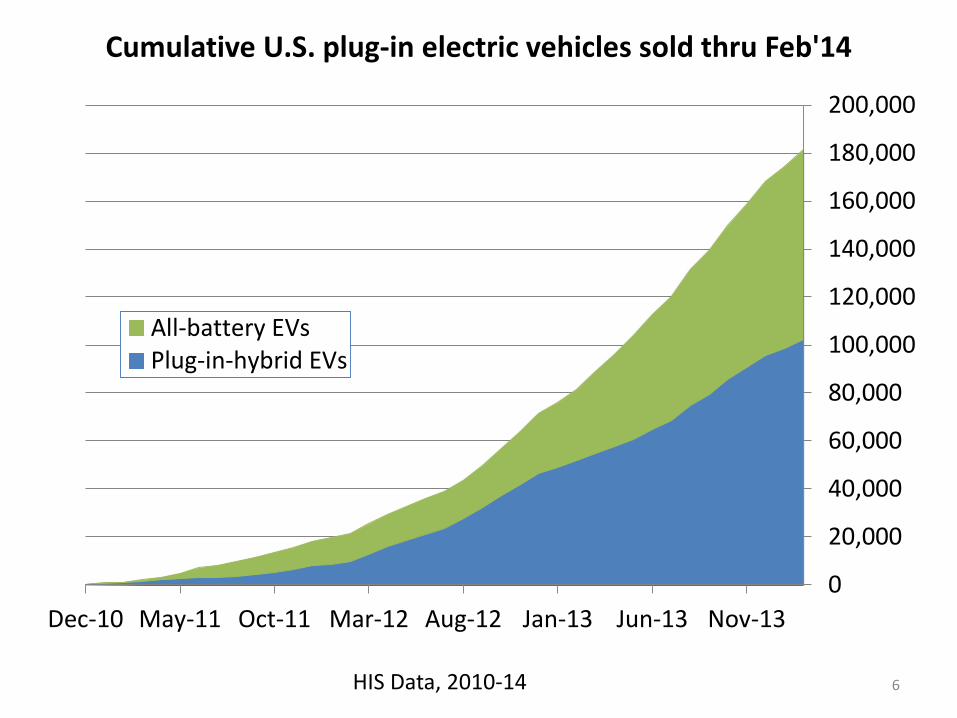

Cumulative U.S. plug-in electric vehicles sold thru Feb'14

All-battery EVs Plug-in-hybrid EVs

200,000

180,000

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

0 Dec-10 May-11 Oct-11 Mar-12 Aug-12 Jan-13 Jun-13 Nov-13

HIS Data, 2010-14 6

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Takeaway: PEV sales have grown rapidly. California has experienced

77% annual growth rates from 2010-2015.

7

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100% Percent of US cumulative plug-in vehicle sales thru Feb'14

All-battery EVs Plug-in-hybrid EVs

Dec-10 May-11 Oct-11 Mar-12 Aug-12 Jan-13 Jun-13 Nov-13

HIS Data, 2010-14 8

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Takeaway: Battery Electric Vehicles and Plug-in Hybrid Vehicles

comprise roughly equal shares of the early market.

9

Table 3~1: Sales of P£V .M-0dels Released by Year and Body in wliforuia, 2010- 2014

Release Year Model Body Safes• Top 10 Ranking

liESlA FtOADSTER Luxury Coupe 156

2010 NISSAN LEAF Hatdlback 25,206 2 INliE RNATIONAL EST AR van 37 a-t EVROlfl VOLT Hatdlback 2.6,197 1 SMARTCAR FORTWO Coupe 2.,122 9

2011 AZURE TR'.ANSIT CONNECT van 5,9

MITSUBJSH I I-Ml EV Hatdlback .25:5 BMWACTN'E E Luxury Coupe 457 FORD FOCUS !ELECTRIC Hatchback 1,209 liES1A MODEL S Luxuiry Hatch back 15,521 4

2012 HONDA FIT EV Hatdlback 92 TOYOTA RAV4 EV SUV 2.,221 8 ASKER KARMA Luxury Sedan 270 TOYOTA P RIUS PLUG-IN Hatdlback 18,163 3 OiEVROlET SPARK Hatdlback 1,338 10 AATSOO Hatdlback 7,736 6

2013 FORD rC.JMAX EINE RGI Hatdlback 6,002 7 HONDAACCORDPLUG-tN Sedan 589 FORD FUSI ON EN ERGI Sedan 7,945 5 BMW 13 BEV PlU Hatdlback 896 MER CE DES-Bf N1Z B-OLASS B'CL Hatchback 56:5 KlA SOUl EV SUV 286 fADI LlAC EUR Luxury Coupe 302

2014 PORSo-t E PA!NAM ERA S HYB Luxuiry Sedan 202 M CLA.REIN P~ PLU Luxuiry Coupe 1:5 BMW 13 REI( HYB Hatdlback 1,040 PORSo-t E 918. SPY P LU Luxury Coupe 14 VOLkSWAGEN GOLF SPR PLU Hatdlback 219

Source~ IHS 2010-2014

10

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Takeaway: Automakers have supplied over 28 PEV models within

the first five years.

11

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Among higher-income groups, the rate of sales of PEVs is approaching

that of hybrids (HEVs)

12

Figure 3-3: PEV and HEV Sales as a Proportion of All California New Vehicle Sales {Dec 2010 -

May2015)

al CD 0

.c:. CD > ~ CD z -0 C 0 t:: 0 a. 0 ~

Q_

a, 0 0

4D 0

0

... 0 ci

N 0 0

0 0 0

PEV lfoJblid

2011 2012 2013 2014 2015

Source: /HS 2010-2015 13

Figure 3-6: PEV Monthly Sales in California by Tract SES Quartile: 3 Month Moving Average

(Dec 2010 - May 2015)

-a, cu «> ::,,.

£j C 0

~ > llJ 0...

C, C> .. ..,

C> C> C, ..,

C> C> .. ....

C> C, C, ....

C> C, .. C, C, C,

C, C, .. C,

~ SES 2nd~ 3rd~ lowesl

2014

Source: /HS 2010-2015 14

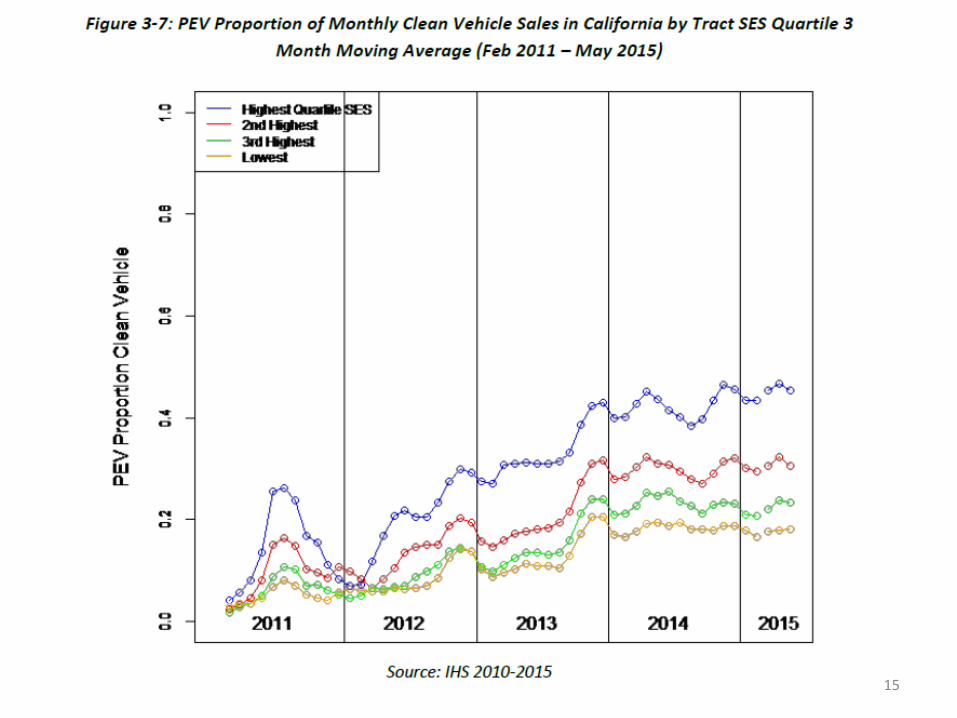

Figure 3•7: PEV Proportion of Monthly Clean Vehicle SaJes in California by Tract SES Quartile 3

Month Moving Average (Feb 2011 - May 2015)

CD 0 .c CD

> C a, CD

0 C 0 t: 0 0.. 0 ~

0...

> w 0...

a, C,

"' C,

-,:j

... C,

C! C,

- 1-igheslQuallle - 2nd~ - 3n1 ~ - Lowest

A

~ _.o

2012 2013 2014 2015

Source: /HS 2010-2015 15

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Takeaway: Households in highest SES quartiles are purchasing PEVs at

rates comparable to the rates that the general population has

purchased hybrids.

16

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

PEV sales have been persistently spatially concentrated

17

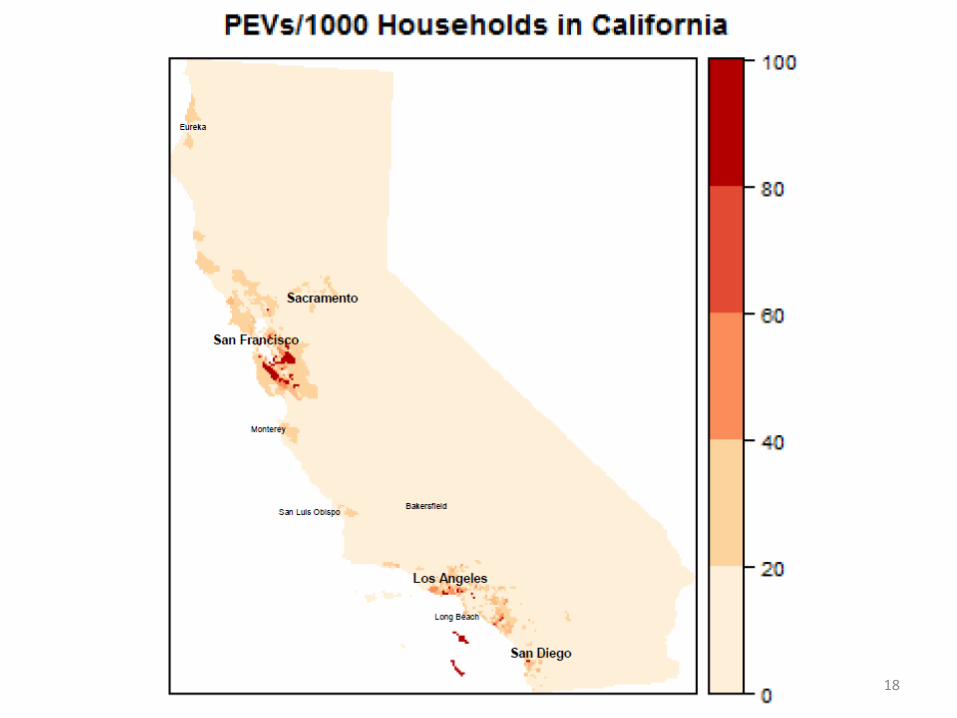

PEV·s/11000 Hous,e holds in ·C,alil ornia 100

Eureka

80

Sacramento

60

Mon.:erey

40

S 31 LUI& 0 01'.spo

, Los Angeles ... . . ....... .._ ·.

20

Long Bu en ~

Sa~, Diego

• ._ ________________________ ___. --~ 0 18

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Takeaway: PEV purchases are concentrated in a few regions.

19

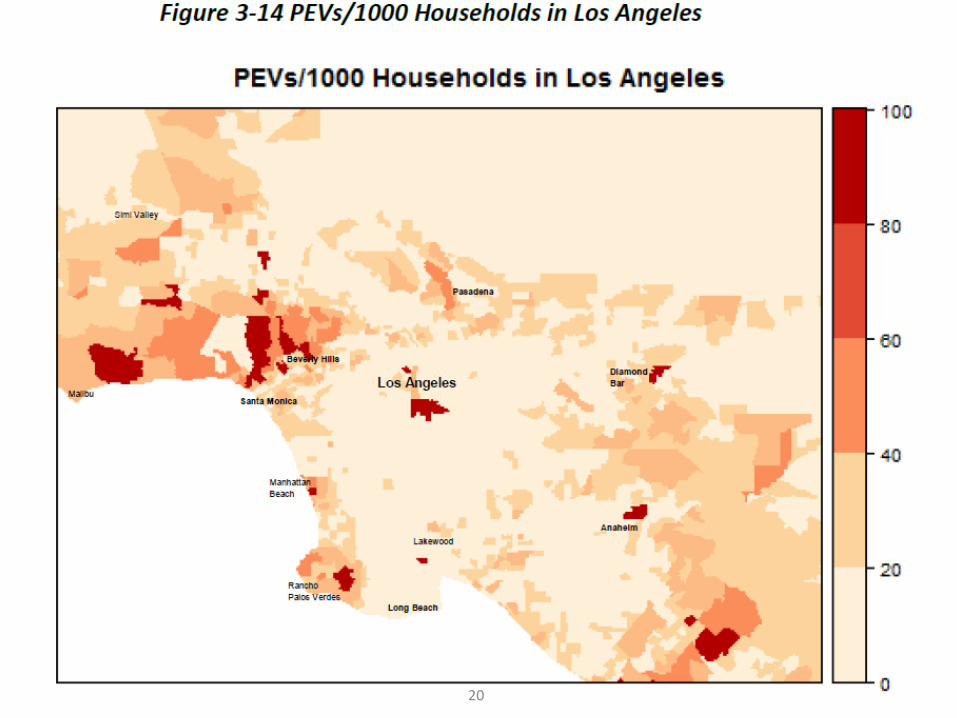

Figure 3-14 PEVs/1000 Households in Los Angeles

PE·Vs/1 00Qi Hous,eholds in IL10 ,s Angeles,

r _.,. ia I,- ·~~

srrlvaue:y

~ Pasaaena

~ ,~Hll8 ' .. al!~---... Los Angeles

Mau Santa Monica

~

• ... Mann~ • ..... t..,

Lale°-tNOOCI .. .. .. Rancno

.,~~ Pa106 Va-GK

Long Bea.en

Olamona ,..•• ..

• A.nanetrn

100

80

60

,.,, ·-n,

20

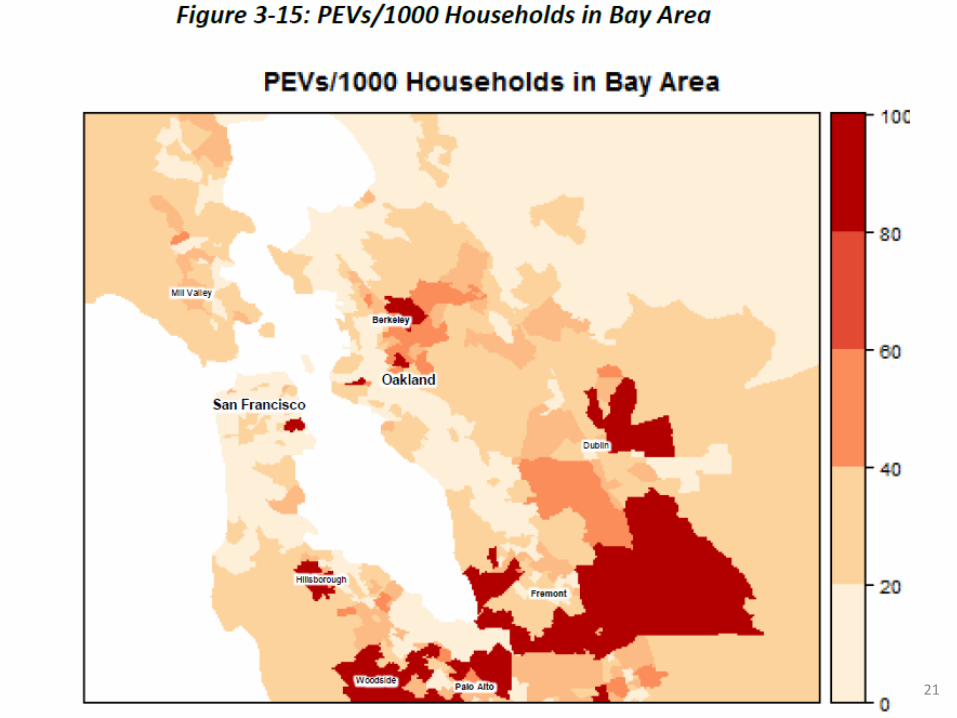

Figure 3-15: PEVs/1000 Households in Bay Area

PEVs/10001 Households, in Bay Area 10 (

80

MII V;t'.ef " -~ • ... 60 ....,.. Oakland

San Francisco ... '

~ 40

~ --Hll~Dorougn

"ft' 20

21

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Takeaway: PEV adoption varies within metropolitan areas.

22

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Household income and wealth are strongly and positively associated

with early PEV sales

23

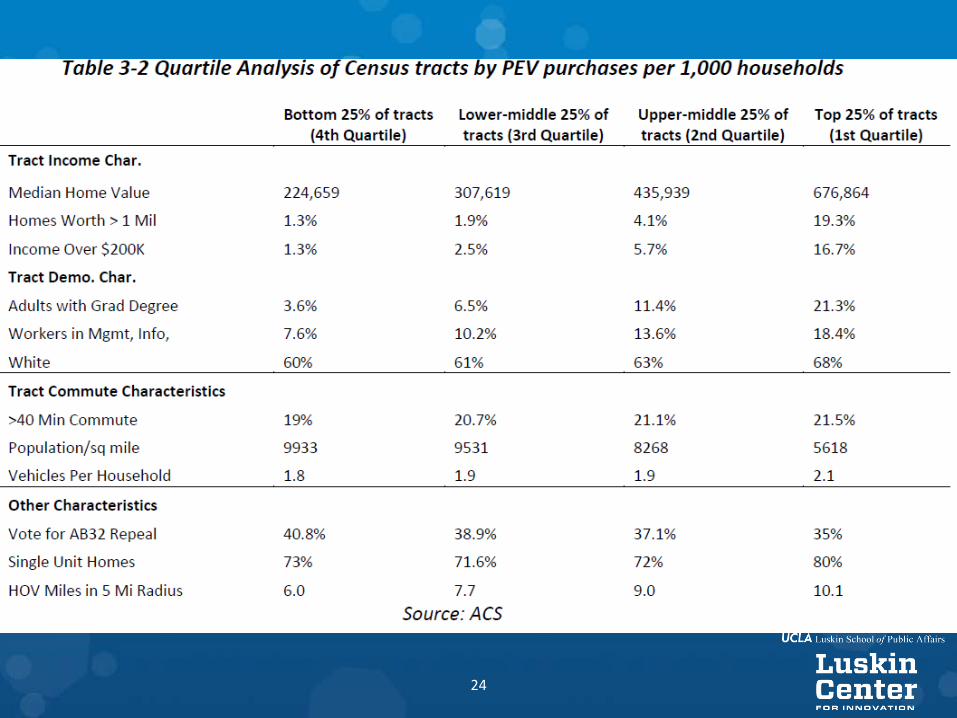

Tract Income Char.

Median Home Value

Homes Worth > 1 Mil

Income Over $200K

Tract Demo. Char.

Adults wit h Grad Degree

Workers in Mgmt, Info,

White

Tract Commute Characteristics

>40 Min Commute

Population/sq mile

1/P.hid P.s PP.r HnusPholrl

Other Characteristics

Vot e for AB32 Repeal

Single Unit Homes

HOV Miles in ~ Mi Kadius

Bottom 25% of t racts (4th Quarti le)

224,659

1.3%

1.3%

3.6%

7.6%

60%

19%

9933

1.8

Lower-middle 25% of tracts {3rd Quartile)

307,619

1.9%

2.5%

6.5%

10.2%

61%

20.7%

9531

1.9

38.9%

71.6%

40.8%

73%

b.O I.I

Source: ACS

Upper-middle 25% of tracts (2nd Quarti le)

435,939

4.1%

5.7%

11.4%

13.6%

63%

21.1%

8268

1.9

37.1%

72%

9.0

Top 25% of tracts (1st Quarti le)

676,864

19.3%

16.7%

21.3%

18.4%

68%

21.5%

5618

J.1

35%

80%

10.1

24

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Takeaways: Neighborhoods with higher incomes, wealth, education, and access to HOV lanes tend to be positively associated with PEV sales.

25

Table 4-1 : Abbreviated Regression Models Predicting New PEV Purchases per capita

(1) (2) (3) (4) (5) VARIABLES PEV/ 1000 HH PEV/1000 HH PEV/ 1000 HH PEV/1000 HH PEV/ 1000 HH

Percent Income Over $200k 12.04*** 9.414*** 8.214*** 6.733*** 7.129***

(0.170) (0.252) (0.277) (0.337) (0.325) Med ian Home Value 3 .361 *** 2.248*** 1.661 *** 0.171

(0.196) (0.206) (0.207) (0.247) Percent Adults with Masters

1.591 *** 1.498*** 1.516*** Degree

(0.212) (0.210) (0.197) Percent Income $150-$200k 1.513*** 1.422*** 1.462***

(0.162) (0.194) (0.184) Percent Homes Worth Over 1

1.743*** 2.344*** Mil($)

(0.275) (0.263) Med ian Rent 0 .896*** 0.521 ***

(0.149) (0.147)

Earn >$75k and Commute Alone 0 .367* 0.197 (0.205) (0.199)

HOV Miles in 5 Mile Radius 1.728*** (0.0899)

Percent Homes Worth $150--0.901 ***

$300k (0.107)

Percent Asian 0.945***

(0.116) Constant 11.84*** 11.84*** 11.84*** 11.84*** 11.84***

(0.0960) (0.0930) (0.0910) (0.0898) (0.0863) Obse rvations 7,855 7,855 7,855 7,855 7,855 R-squared 0.667 0 .687 0 .701 0 .709 0.731 Source: American Community Survey 2013-2015; IHS 2010-2015

Sta ndard e rrors in pa re nt heses ***p<0.01, **P<0.05, *p<0.1 26

Table 4-6: Characteristics of Tracts by Quartile of Used PEV Sales per capita

1st 2nd 3rd 4th Quart ile Quart ile Quartile Quartile

Tract Income Characteristics:

Median Home Value 333,701 436,355 444,437 522,180

Homes Worth > $1 Mil 0.041 0.075 0.074 0.106

Income Over $200K 0.039 0.07 0.072 0.108

Tract Demographic Characteristics:

Adu lts with Grad Degree 0.075 0.134 0.121 0.149

Workers in Mgmt, Info or Finance 0.104 0.142 0.136 0.149

White 0.612 0.69 0.64 0.652

Tract Commute Characteristics

>40 Min Commute 0.199 0.2 0.206 0.221

Population Density (population/sq. mile) 9423.458 8036.919 8411.439 6242.145

Vehicles Per Household 1.815 1.814 1.9 2.05

Other Characteristics:

Vote for AB32 Repeal 0.387 0.395 0.376 0.367

Single Unit Homes 0.733 0.67 0.704 0.8

HOV M iles in 5 Mi Rad ius 7.124 5.482 8.64 10.07

Source: American Comm unity Survey 2013-2015; IHS 2010-2015 27

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Takeaways: Neighborhoods purchasing used PEVs tend to have higher income

and education but less so than neighborhoods purchasing new PEVs.

28

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

HOV Lane Access Policies Have

Boosted PEV Sales

29

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

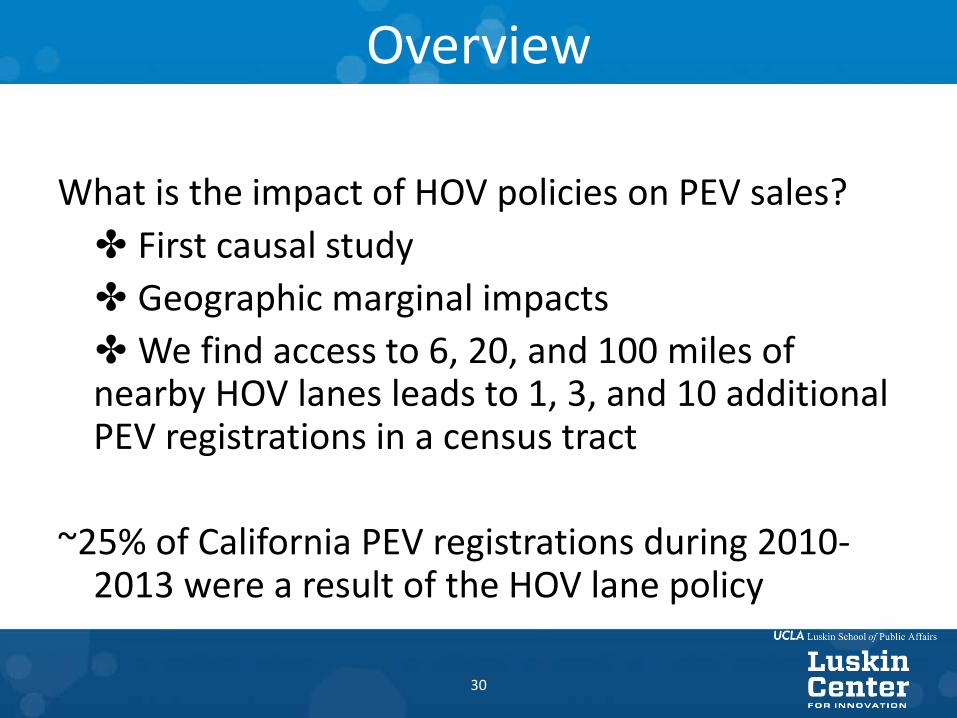

Overview

What is the impact of HOV policies on PEV sales? ✤ First causal study ✤ Geographic marginal impacts ✤ We find access to 6, 20, and 100 miles of nearby HOV lanes leads to 1, 3, and 10 additional PEV registrations in a census tract

~25% of California PEV registrations during 2010-2013 were a result of the HOV lane policy

30

Ventura

- HOV lanes

Miles of HOV Lanes

within 30 Milos

0.0 - 7.9

- 8.0- 63.3

63.4 - 142.8

- 142.9 . 278.9

- >279 0 4 8 16Miles

' ' I I

31

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

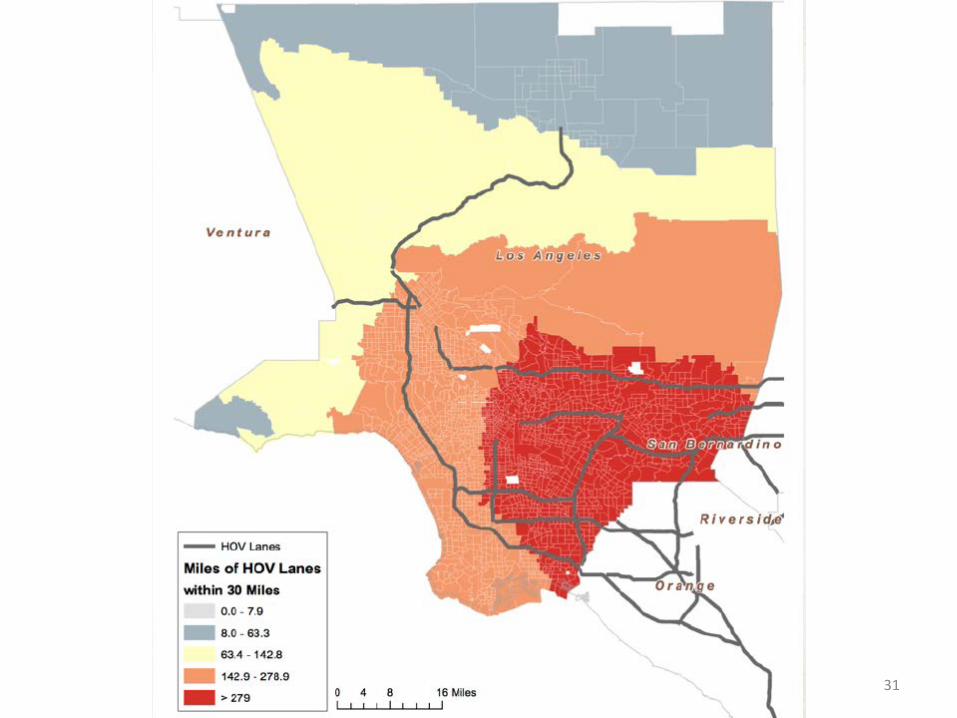

Takeaway: Access to HOV lanes varies systematically with metro

areas.

32

@ SlniValey

Number of PEVs

~ 0-1

2-5

6-22

~ 23 - 391

0 3.5 ~ I I I I I

14 Miles I

..... ■ I Lanciiteill .. ■

0

9

Fulerton

Ananem

Westmlnste• Sel'lll>Ana

Yotballnda

Orange

rusun 33

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

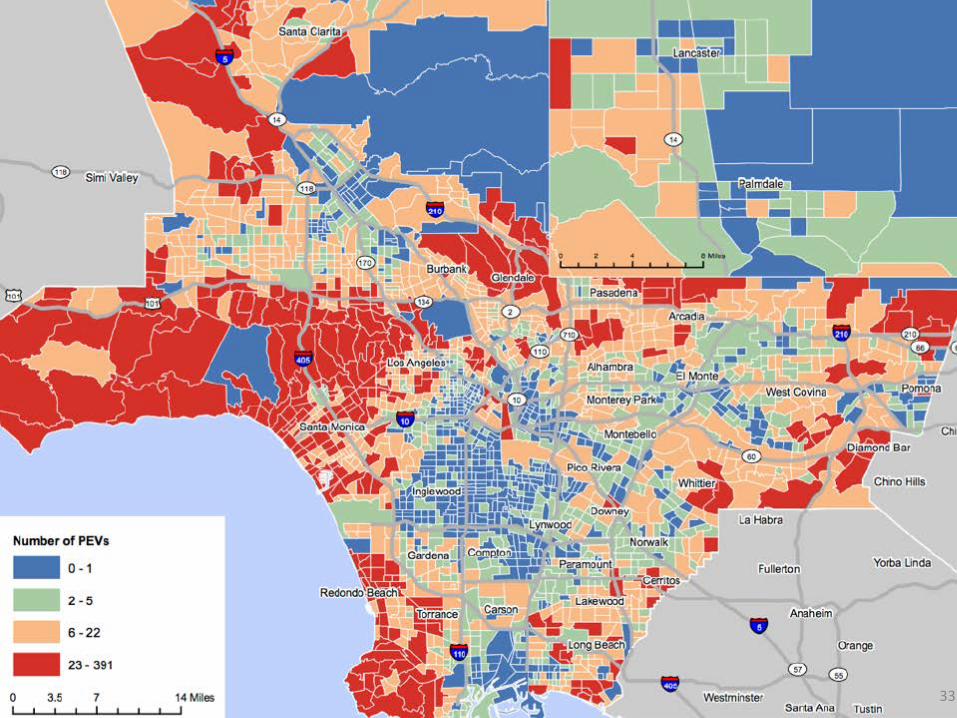

Takeaway: Neighborhood adoption of PEVs is not correlated with access

to HOV lanes.

34

18

16

~ 14 ru v, 12 > w 0.. 10 a, > ~ 8 ru -:::s 6 E ::s u 4

2

0

--Lower 95% Cl - Mea n Response - Upper 95% Cl

1 10 19 28 37 46 55 64 73 82 91 100

HOV Lanes within a 30-mile Radius of Census Tract

35

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Takeaway: PEV adoption is higher in areas with greater HOV access.

36

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

New Car Buyer Market Holds Diverse Preferences for BEVs and PHEVs

37

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

New car buyer survey by UCLA in 2013 • 1261 prospective new car buyers in California

• Household and vehicle data

• Vehicle choice experiments » Allow us to identify preferences for vehicles that do not currently exist but are

likely to in the future

» Allow us to identify preferences along different dimensions of heterogeneity

Caltrans “2010-2012 California Household Travel Survey” • Cross-check representative sample of new car buyers

• Cross-check vehicle class share with revealed preference data

38

State and Federal differentiated BEV and PHEV Rebates are critical factors in

the early market growth

UCLA Lu,J..n Sd1oc,l of I' Jbh,: :\:lall'i-

Luskin Center FOCI IN N OVATtON

Three major consumer segments for BEVs and PHEVs

32% express smallest disutility for BEVs while findingPHEVs comparable in utility to ICEs

42% of respondents express large disutility for BEVswhile finding PHEVs comparable in utility to ICEs.

26% express large disutility for both BEVs and PHEVs.

40

Takeaway: There are three distinct market segments. Two of these

segments require larger rebates for BEVs compared to PHEVs to induce

comparable sales of both.

41

UCLA Luskin S..:ho-;)l ••l l'ubli~ ,\ffJns

Luskin Center F'OQ INNOVATION

Rebate Policies Have Boosted PEV Sales

42

UCLA Luskin S..:ho-;)l ••l l'ubli~ ,\ffJns

Luskin Center F'OQ INNOVATION

Max Level of Incentives Across States, 2014 Maximum Possible Incentive Per Vehicle

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

WV CO GA IL LA MD CA MA TX PA SC CA UT BEV BEV PHEV PHEV

43

Takeaway: State PEV rebates levels vary widely.

UCLA Luskin S..:ho-;)l ••l l'ubli~ ,\ffJns

Luskin Center F'OQ INNOVATION

Automakers and Dealers

Routinely use rebates, cash back, and discounts to sell vehicles and capture market share.

Some past deals available to consumers….

45

FIND YOUR TAG, GET $2,000 CUSTOMER CASH $1,000 DOWN PAYMENT ASSISTANCE $1,500 OPTION PACKAGE DISCOUNT

+ $2,000 PURCHASE BONUS CASH

$6,500 ~~It\5

ON SELECT 2015 VEHICLES IN STOCK WHEN YOU FINANCE THROUGH SELECT LENDERS

Get up to $3,000 Factory Cash Back on a New 2015 Avalon.

46

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Research Questions for PEV market in 2014: How many additional PEV sales are associated

with the 2014 CVRP program?

How can better targeting of the 2014 CVRP program increase the cost effectiveness and improve equity outcomes?

47

UCLA Luskin S..:ho-;)l ••l l'ubli~ ,\ffJns

Luskin Center F'OQ INNOVATION

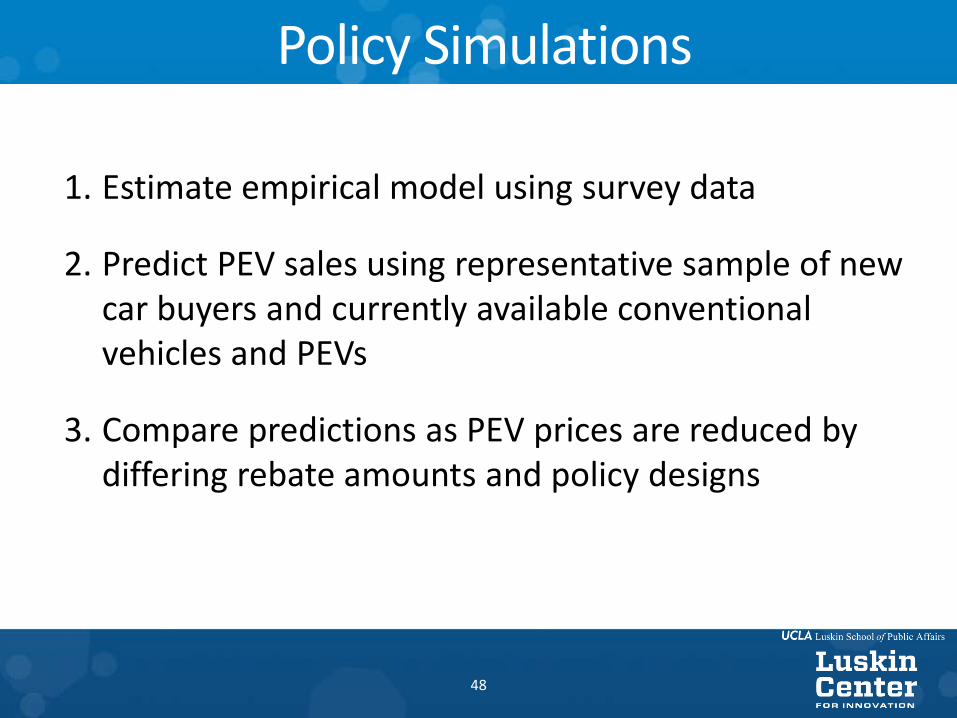

Policy Simulations

1. Estimate empirical model using survey data

2. Predict PEV sales using representative sample of new car buyers and currently available conventional vehicles and PEVs

3. Compare predictions as PEV prices are reduced by differing rebate amounts and policy designs

48

UCLA Luskin S..:ho-;)l ••l l'ubli~ ,\ffJns

Luskin Center F'OQ INNOVATION

CVRP Policy Comparison

1. Baseline (2013) policy

2. Price cap for vehicle eligibility

3. Income-tested policies

49

UCLA Luskin S..:ho-;)l ••l l'ubli~ ,\ffJns

Luskin Center F'OQ INNOVATION

Judging the Performance of Alternative CVRP Policies

Compare over 3-year policy period:

• Total additional PEVs purchased

• Cost per induced vehicle purchase

• Total program cost

• Equity: distribution of rebate funding across consumer income classes

(*Income defined for individuals not households.)

50

BEV PHEV Policy Income

Rebate Rebate

~ Under $25k $2,500 $1,500 0 c... $25-$50k $2,500 $1,500 0 :J d Ill

$50-$75k $2,500 $1,500 $75-$100k $2,500 $1,500

:J .... "' .... • . <n

$100-$175k $2,500 $1,500 $2,500 $1,500

Baseline BEVs Sold

mm 6,349

19,822 4,060

Baseline PHEVs Sold

6,203

18,667 16,981 35,735

3,371

Addt'I BEVs Addt'I Additional Total PEVs Sold PHEVs Sold PEVs Sold Sold

775 1,278 664 963 645 1,001 985 1,250 557 389

9,699 158,335

UCLA Luskin ~,hool ,,; l'ubli;: ,\tfaus

Luskin Center F'OQ INNOVATION

California Baseline Rebate Policy • Rebate is estimated to induce 9,699 PEV purchases

• Higher preference for PHEVs over BEVs

• Lower income classes have a lower preference for both PHEVs and BEVs

51

Policy

-~ 0 Cl. 0 ::::, cJ "' ::::, .... RI .... Vl

Policy

-~ 0 Cl. 0

a "' ::::, .... B!

Policy

-~ 0 Cl. 0

a "' ::::, .... fl Vl

Income BEV

Rebate PHEV

Rebate Baseline

BEVs Sold

Baseline PHEVs Sold

Under $25k ----$25-$50k 18,191

$50-$75k 10,313 18,667

$75-$100k 6,349 16,981 $100-$175k 19,822 35,735 Over$175k 4,060 3,371

Income I R::~e I PHEV Rebate I BEV Budget

Under $25k $8,431,349 $25-$50k $17,101,072 $50-$75k $27,442,629 $75-$100k $17,484,884

$100-$175k $52,018,618 Over$175k $11,541,233

Addt'I BEVs Addt'I Additional Total PEVs

Sold PHEVs Sold PEVs Sold Sold

775 1,278 664 963 645 1,001

9,699 158,335

985 1,250 557 389

PHEV Budget ITotal PEVs I Total Cost

Sold ($ Millions) $10,383,030 $29,202,579 $29,444,460

158,335 -$26,973,264

$55,478,170 $5,639,740

Additional Additional Total Cost- Addt'I Dollar Needed to Total Cost Total Cost• PEVs Sold PEVs Sold* Effectiveness Induce One Addt'I PEV* ($ Millions) ($ Millions)

Allocative Equity

9,699 N/A $30,017 N/A $291 N/A 42%

• C:nmn;irnci tn St;it w; Oun Pnlirv

California Baseline Rebate Policy • 42% of the value of the rebates is allocated to consumers making less than $75,000

52

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Targeting of Rebates to Lower-Income Households Would Increase

Cost Effectiveness and Equity Outcomes

53

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Principles for more cost effective rebates

Target consumers who otherwise would not have purchased PEVs. – Consumers have a lower preference for BEVs than

PHEVs so offer relatively more generous rebates for BEVs.

Target consumers who are more responsive to the rebates offered. – Lower income rather than higher income consumers.

54

Under$2Sk , $25-$50k

$S0-$7Sk $75-$100k $100-$175k

Policy I Income

QI

"' Under$25k

~ n,

QI in QI

·;;; ... E >"' u 0 u ~ .!: u

0 Ill) QI .f: c.. e-;;; >

c.. ..c ..c QI

, $25-$50k

$S0-$7Sk

$75-$100k

$100-$175k a: •

9,434

BEV Rebate

-265

(-3%)

* Compared to Status Quo Policy

I PHEV Rebate I

$22,743

6,065 18,191 10,313 18,667 6,349 16,981

19,822 35,735 4,060 3,371

BEV Budget

$34,009,626 $38,472,680 $21,681,786

-$7,274 (-24%)

$0 $0 $0

2,610 528 639

PHEV Budget

$215

$38,679,027 $62,401,798 $19,305,549

-$77 (-26%)

$0 $0 $0

9,434 158,090

I Total PEVs I Total Cost

Sold ($ Millions)

158,090 -100%

Income-Tested Rebate Levels • One of the most cost-effective policies and one of lowest total program costs

• 100% of rebates allocated to households with incomes less than $75,000

• Superior to baseline policy

55

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Falling Gas Prices are Statistically Correlated with Falling PEV Sales

56

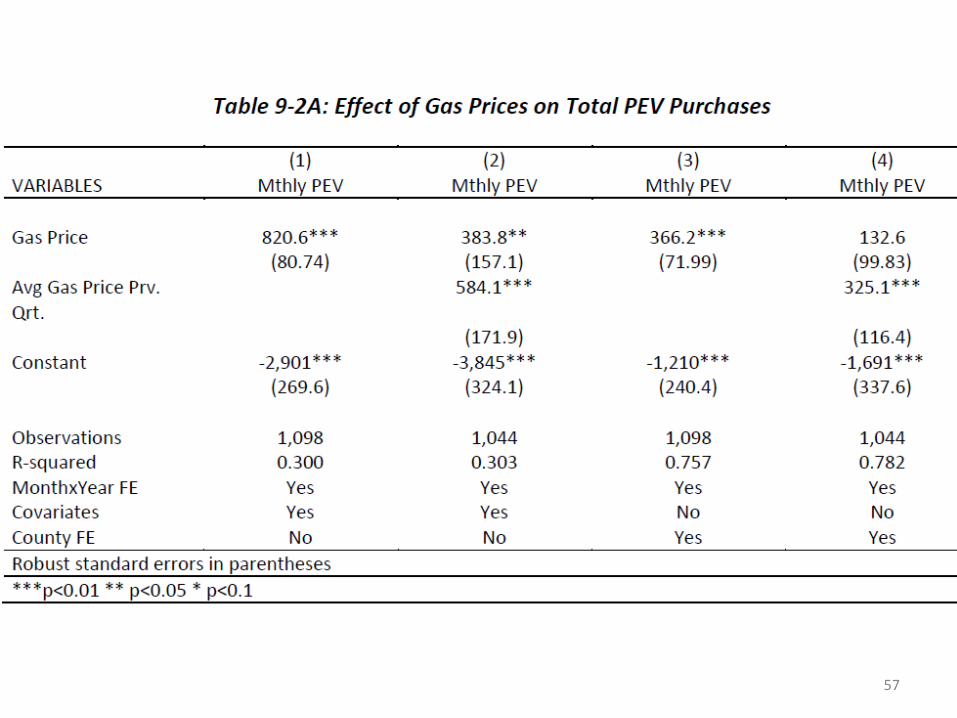

Table 9-2A: Effect of Gas Prices on Total PEV Purchases

(1) (2) (3) (4) VARIABLES Mthly PEV Mt hly PEV Mthly PEV Mthly PEV

Gas Price 820.6* * * 383.8* * 366.2* * * 132.6 {80.74) (157.1) {71.99) (99.83)

Avg Gas Price Prv. 584.1 * * * 325 .1 ** * Qrt .

(171.9) (116.4) Constant -2 901 * * * I -3 845* * * I -1 210* * * I -1 691 * * * I

(269.6) (324.1) (240.4) (337.6)

Observations 1,098 1,044 1,098 1,044 R-squared 0.300 0.303 0.757 0.782 Mont hxYear FE Yes Yes Yes Yes Covariates Yes Yes No No

County FE No No Yes Yes

Robust standa rd errors in parent heses

* * * p<0.01 * * p<0.05 * p<0.1

57

Takeaway: Higher gas prices are associated with higher PEV sales.

58

Gas Price

Lagged Qrt Gas Price

Model 1: County Fixed-

Fff P.r.t.~

Model 2: county Hxed [ ffect s (Log)

Model 3: NB Census- I ract

Table 9-6: Simulations of the effects of increasing gas prices on PEV sales

Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

$3.00 $3.00 $3.00 $3.00 $4.00 $4.00

$3.00 $3.00 $3.00 $3.00 $3.00 $3.33

156 156 156 156 289 397

l~b l~b l~b l ~b lUb 113

156 156 156 156 196 187

Month 7

$4.00

$3.67

505

:219

178

1-'ct Change

Month 8 Month 8 to

Month 4

$4.00

$4.00

614 293%

llb 4~%

169 8%

UCLA I u~kin Scho-'.l l oj Puhli:: Att:tm

Luskin Center P"C:,R 1,,11,,ovP.TIOl\,I

59

Takeaway: Gas price increases are expected to increase PEV sales but

the magnitude is uncertain.

60

UCLA Luskn St..hoo. ()/ l'uhh,;:. ,\tfoirs

Luskin Center FOR INNOVATION

Concluding remarks

• Spatially purchase patterns follow new car buyer trends.

• Strong support for CVRP and EFMP Plus-Up Reforms.

• Need for fuller representation of PEVs in larger body type vehicles.

61