ez crisis: a consensus narrative - centre for …cepr.org/sites/default/files/ez crisis consensus...

TRANSCRIPT

EZ Crisis: A Consensus Narrative

These slides are taken from “Rebooting the Eurozone: Step 1 – agreeing a crisis narrative”, CEPR Policy Insight

No.85by Richard Baldwin, Thorsten Beck, Agnès Bénassy-Quéré, Olivier Blanchard, Giancarlo Corsetti, Paul de Grauwe, Wouter den Haan, Francesco Giavazzi, Daniel Gros, Sebnem Kalemli-Ozcan, Stefano Micossi, Elias Papaioannou, Paolo Pesenti, Christopher Pissarides,

Guido Tabellini and Beatrice Weder di Mauro

Feel free to use, change, and distribute these slides, but please cite CEPR Policy Insight No.85 as the source

Today’s situation: EZ Crisis: a long way from recovery

The Eurozone Crisis is far from finished…

• Lacklustre growth and bleak economic prospects

• “Jobless Europe” for the youth

• Extremist views and nationalistic tendencies

…fragilities and imbalances are still present.

• Non-performing banking loans

• Feedback loops between banks and the sovereign via debt holdings

• Risky interest rate normalization

The causes of the EZ crisis The core reality

EZ crisis as a ‘sudden stop’ crisis

• Abrupt end of capital flows slow growth increased public debt

and deficit public debt crisis

EZ Crisis amplifiers

• No lender of last resort

• No devaluation possibilities

• Vicious feedback cycle between banks and government

• Predominance of banking financing

• Rigid labor and product market

EZ crisis: a consensus narrative Plan of lecture

• Building up problems

• Triggers of the crisis

• Phase one: failed bailouts and contagion

• Phase two: contagion spreads to the core

• Denouement

Building up problems

• Sharp drop in borrowing costs and the disappeared spreads

• Critical intra-EZ imbalance

• Current account deficits

• Investment versus saving

• Competitive imbalance

• Public debt build up (not the driving force!)

• Private debt build up

• EZ banks’ cross-border lending

• Crisis prelude

Sharp drop in borrowing costs and the disappeared spreads

0

2

4

6

8

10

12

14

16

Jan

-19

90

Ap

r-19

91

Jul-

199

2

Oct

-199

3

Jan

-19

95

Ap

r-19

96

Jul-

199

7

Oct

-199

8

Jan

-20

00

Ap

r-20

01

Jul-

200

2

Oct

-200

3

Jan

-20

05

Ap

r-20

06

Jul-

200

7

10 yr gov't bond yields (%)

Greece

Ireland

Italy

Spain

Portugal

Austria

Belgium

France

Germany

Lux'g

NL

Finland

0

2

4

6

8

10

12

14

16

Jan

-19

90

Jan

-19

91

Jan

-19

92

Jan

-19

93

Jan

-19

94

Jan

-19

95

Jan

-19

96

Jan

-19

97

Jan

-19

98

Jan

-19

99

Jan

-20

00

Jan

-20

01

Jan

-20

02

Jan

-20

03

Jan

-20

04

Jan

-20

05

Jan

-20

06

Jan

-20

07

10 yr gov't bond yields (%)

France

Germany

Italy

Japan

UK

US

Source: OECD online database with author’s elaboration.

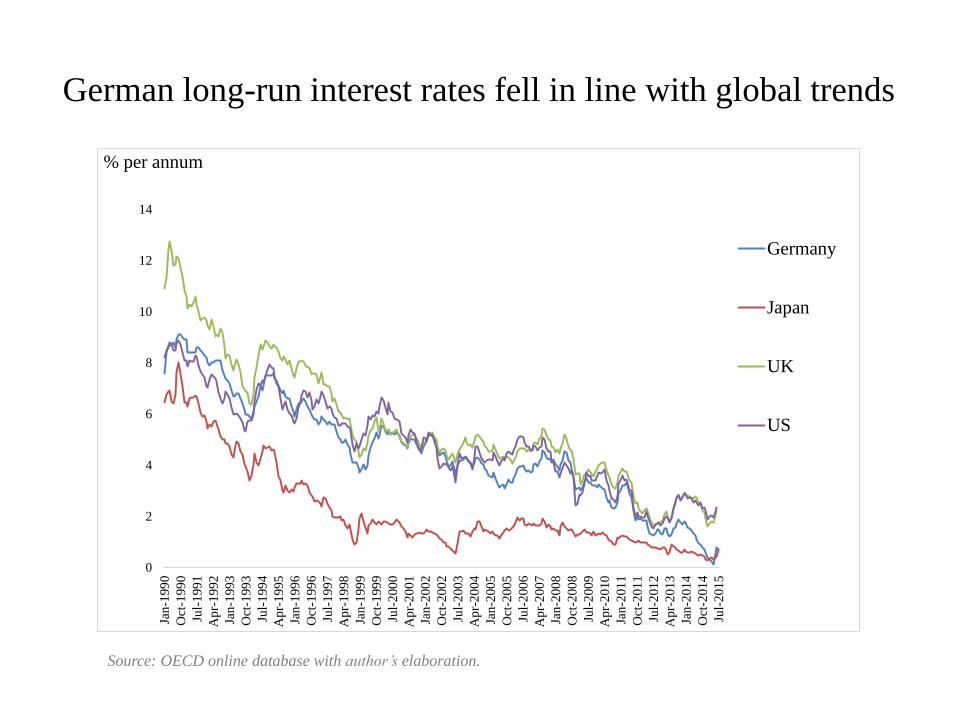

German long-run interest rates fell in line with global trends

0

2

4

6

8

10

12

14

Jan

-199

0

Oct

-199

0

Jul-

199

1

Ap

r-1

992

Jan

-199

3

Oct

-199

3

Jul-

199

4

Ap

r-1

995

Jan

-199

6

Oct

-199

6

Jul-

199

7

Ap

r-1

998

Jan

-199

9

Oct

-199

9

Jul-

200

0

Ap

r-2

001

Jan

-200

2

Oct

-200

2

Jul-

200

3

Ap

r-2

004

Jan

-200

5

Oct

-200

5

Jul-

200

6

Ap

r-2

007

Jan

-200

8

Oct

-200

8

Jul-

200

9

Ap

r-2

010

Jan

-201

1

Oct

-201

1

Jul-

201

2

Ap

r-2

013

Jan

-201

4

Oct

-201

4

Jul-

201

5

% per annum

Germany

Japan

UK

US

Source: OECD online database with author’s elaboration.

Critical intra-EZ imbalancecurrent account imbalances

Greece

Ireland

Italy

Portugal

Spain

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

% of own GDP

Germany

Belgium

France

NL

Finland

-4

-2

0

2

4

6

8

10

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

% of own GDP

Peripheral EZ members generally ran current deficits while Core members general

ran current account surpluses

Critical intra-EZ imbalanceSaving and investment imbalances

10

13

16

19

22

25

28

31Savings (% of GDP)

Germany

NL

Belgium

France

EZ

10

13

16

19

22

25

28

31

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

Savings (% of GDP)

Greece

Ireland

Italy

Portugal

Spain

EZ

16

19

22

25

28

31

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

Investment (% of GDP)

Greece

Ireland

Italy

Portugal

Spain

EZ

16

19

22

25

28

31

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

Investment (% of GDP)

Germany

NL

Belgium

France

EZ

GIIPS generally saved less and invested more than average while Core EZ nations

generally saved more and invest less the average

Critical intra-EZ imbalancePublic debt fell in most EZ nations

Government debt ratios improved for most EZ nations (especially Ireland and Spain)

but Portuguese and Greek debt burdens soared

Greece

Ireland

Italy

Portugal

Spain

EZ

40

60

80

100

120

140

160

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

EZ

Finland

Germany

NL

France

Belgium

Austria

40

60

80

100

120

140

160

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

Debt-to-GDP ratio(1990=100)

Critical intra-EZ imbalanceBank debt rose rapidly in some EZ nations

Rapid accumulation of bank debt was a problem especially in Ireland, Spain, Italy and

France

Ireland

Spain

Italy

Greece

Portugal70

90

110

130

150

170

190

210

2000

2001

2002

2003

2004

2005

2006

2007

Total bank assets to GDP

France

Finland

Belgium

Austria

Germany

NL70

90

110

130

150

170

190

210

2000

2001

2002

2003

2004

2005

2006

2007

Total bank assets to GDP

House prices rose in the GIIPS more than in the US

while Germany’s fell

Note: 1999 Q1=100.

Source: OECD online database. House price indices in real terms.

Total landing from core countries’ bank to the periphery

(billion euros)

Prelude and Phase One of the Crisis in EZ Periphery

Greek deficit deceit Greek bailout Irish bailout Portuguese bailout Greece

Ireland

Portugal

0

2

4

6

8

10

12

14

16

18

Sep

-2008

Oct

-20

08

Nov-2

00

8

Dec

-20

08

Jan-2

00

9

Feb

-20

09

Mar

-20

09

Apr-

2009

May

-20

09

Jun-2

009

Jul-

20

09

Aug-2

00

9

Sep

-20

09

Oct

-20

09

Nov

-2009

Dec

-20

09

Jan-2

01

0

Feb

-20

10

Mar

-20

10

Apr-

20

10

May

-20

10

Jun-2

010

Jul-

20

10

Aug-2

01

0

Sep

-20

10

Oct

-20

10

Nov-2

01

0

Dec

-20

10

Jan-2

011

Feb

-20

11

Mar

-20

11

Apr-

20

11

May

-20

11

Jun-2

011

Jul-

20

11

Aug

-2011

Sep

-20

11

Oct

-20

11

Nov-2

01

1

Prelude Phase One

Spreads

Note: The spreads are the difference between national 10-year government bound yields and those of Germany, in

percentage points.

Source: OECD online database with author’s elaboration.

Summary of pre-crisis imbalances

1999 to 2007 (% of own GDP) Bank assets (% of GDP) %

Cumulative current account balance

Cumulative budget deficit

2000 to 2008 increase

(p.p.)Bank assets,

2008Debt-GDP ratio, 2008

Excess inflation

(1999-2007)Portugal -96 -36 44% 262% 72 7.5Greece -84 -47 36% 173% 109 9.9

Spain -60 2 121% 296% 39 9.2Ireland -21 14 464% 783% 43 11.6Italy -8 -26 85% 235% 102 1.8EZ -2 -17 94% 335% 69 0.0France 6 -23 180% 395% 68 -2.9Austria 16 -19 305% 379% 69 -3.2Germany 27 -19 18% 316% 65 -4.8Belgium 47 -5 83% 392% 92 -1.1NL 48 -5 -9% 375% 55 2.8Finland 61 33 101% 197% 33 -4.9Lux'g 98 23 -577% 2367% 14 5.5

Note: ‘Excess’ inflation is the nation’s cumulative inflation rate minus that of the EZ average.

Source: OECD online database with author’s elaboration.

Triggers of the crisis

• October 2009: Greece budget

deficit unmasked

• Six-moth attempt of ‘self rescue’

– failed

• Greece trapped into a public debt

vortex

• Debt loop

• Austerity loop

Phase One: failed bailouts and contagion

• Failed bailouts - Greece’s borrowing cost continued to soar

• Contagion in the periphery

• Public debt vortexes: Portugal

• Bank debt vortexes public debt vortexes: Ireland

Greek deficit deceit Greek bailout Irish bailout Portuguese bailout Greece

Ireland

Portugal

0

2

4

6

8

10

12

14

16

18

Sep

-2008

Oct

-2008

Nov-2

008

Dec

-2008

Jan-2

009

Feb

-2009

Mar

-2009

Apr-

2009

May

-2009

Jun-2

009

Jul-

2009

Aug-2

009

Sep

-2009

Oct

-2009

Nov-2

009

Dec

-2009

Jan-2

010

Feb

-2010

Mar

-2010

Apr-

2010

May

-2010

Jun-2

010

Jul-

2010

Aug-2

010

Sep

-2010

Oct

-2010

Nov-2

010

Dec

-2010

Jan-2

011

Feb

-2011

Mar

-2011

Apr-

2011

May

-2011

Jun-2

011

Jul-

2011

Aug-2

011

Sep

-2011

Oct

-2011

Nov-2

011

Prelude Phase One

Spreads

Figure : Prelude and Phase One of the Crisis in EZ Periphery

Phase Two: contagion spreads to the core

• Mismanagement of the bailouts give rise to a general fear

• Pro-cyclical fiscal tightening further stoking contagion

• Self-feeding panic: Good equilibrium, bad equilibrium

Fiscal policy turned pro-cyclical from 2010

Note: Inspired by Carrot and de Castro (2015) with author’s elaborating using IMF WEO data.

Pro-cyclical fiscal policy, 2010 to 2014

% of own potential GDP

bill EUR % %

2010 to 2014 swing 2010 to 2014 swing Share of EZ swing Share EZ 2014 GDP

Greece 7% 14 4% 2%Ireland 28% 49 14% 2%Italy 2% 28 8% 16%Portugal 9% 17 5% 2%Spain 5% 53 16% 11%EZ 4% 340 100% 100%Austria 1% 2 1% 3%Belgium 0% 2 0% 4%Finland 0% 0 0% 2%France 2% 46 13% 21%Germany 4% 108 32% 29%

Luxembourg 1% 1 0% 0%

Netherlands 2% 15 5% 6%

Phase Two: contagion spreads to the core

Spreads started to rise for Belgium, France and Austria – as well as

Italy and Spain

Greek bailout Irish bailout Portuguese bailout 2nd Greek bailout

Spain

Italy

Belgium

France & Austria

0

1

2

3

4

5

6

7

May

-2010

Jun-2

010

Jul-

2010

Aug-2

010

Sep

-2010

Oct

-2010

Nov-2

010

Dec

-2010

Jan-2

011

Feb

-2011

Mar

-2011

Apr-

2011

May

-2011

Jun-2

011

Jul-

2011

Aug-2

011

Sep

-2011

Oct

-2011

Nov-2

011

Dec

-2011

Jan-2

012

Feb

-2012

Mar

-2012

Apr-

2012

May

-2012

Jun-2

012

Jul-

2012

Aug-2

012

Sep

-2012

Oct

-2012

Nov-2

012

Dec

-2012

Jan-2

013

Feb

-2013

Phase One Phase Two

Spreads

Denouement

• Agreement on Banking Union and the Fiscal compact

• Draghi’s “whatever it takes”

Draghi speech

0

5

10

15

20

25

30

35

40

Jan

-…

Oct

-…

Jul-

…

Ap

r…

Jan

-…

Oct

-…

Jul-

…

Ap

r…

Jan

-…

Oct

-…

Jul-

…

Ap

r…

Jan

-…

Oct

-…

Jul-

…

Ap

r…

Jan

-…

Oct

-…

Jul-

…

Ap

r…

Jan

-…

Oct

-…

Jul-

…

Ap

r…

Jan

-…

Oct

-…

Jul-

…

Ap

r…

Jan

-…

Oct

-…

Jul-

…

Ap

r…

Jan

-…

Oct

-…

Jul-

…

10 yr gov't bond yields (%)

Greece

Ireland

Italy

Spain

Portugal

Austria

Belgium

France

Germany

Lux'g

NL

Finland

Figure: Yields converged again after Draghi’s intervention

Proximate causes, and causes of the causes

Proximate cause

• Sudden stop in inter-EZ lending

• Loss of independent monetary policy after euro adoption

Cause of the cause

• Policy failures that allowed the imbalance to get so large

• Failure to control national debt

• Failure to control excessive bank leverage

• Lack of institutions to absorb shocks at the EZ level

• Failings in real-time crisis management

Concluding remarks

This essay has identified proximate causes, the causes of the proximate

causes of the RZ crisis and provide and crisis narrative.

How we got here…

• Fundamental design flaws of the EMU

…the way ahead

• Lots of suggestions, no consensus

• Both on where to go, and on how

• We need a systematic rethinking how to get Europe working again

The End