exposure draft hedge accounting comments to be...

TRANSCRIPT

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Hedge accounting outreachExposure draft Hedge Accounting

Comments to be received by 9 March 2011

International Financial Reporting Standards

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

Introduction

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

3Principle-based standards

Principles Rules

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

4

Source of information (adapted from): www.iasplus.com

4Convergence ‘Map’

2011

2012

2010

2011

2012

2009

–

20112011

Permit from 2010

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

5Our work plan - Major Projects

Crisis (MoU)

Financial instruments

Consolidation

Derecognition

Other (Non MoU)

Insurance contracts

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Other (MoU)

Revenue recognition

Leases

Post-retirement benefits

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

6Consultation process 6

Discussion

paper

Exposure

Draft

Final

standardComment

analysis

Comment

analysis

Research:

Effective

date

9 – 15

months

9 – 15

months12 –18

months

Additional

input

Additional

input

Feedback

statement

2 year post

implementation

review

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

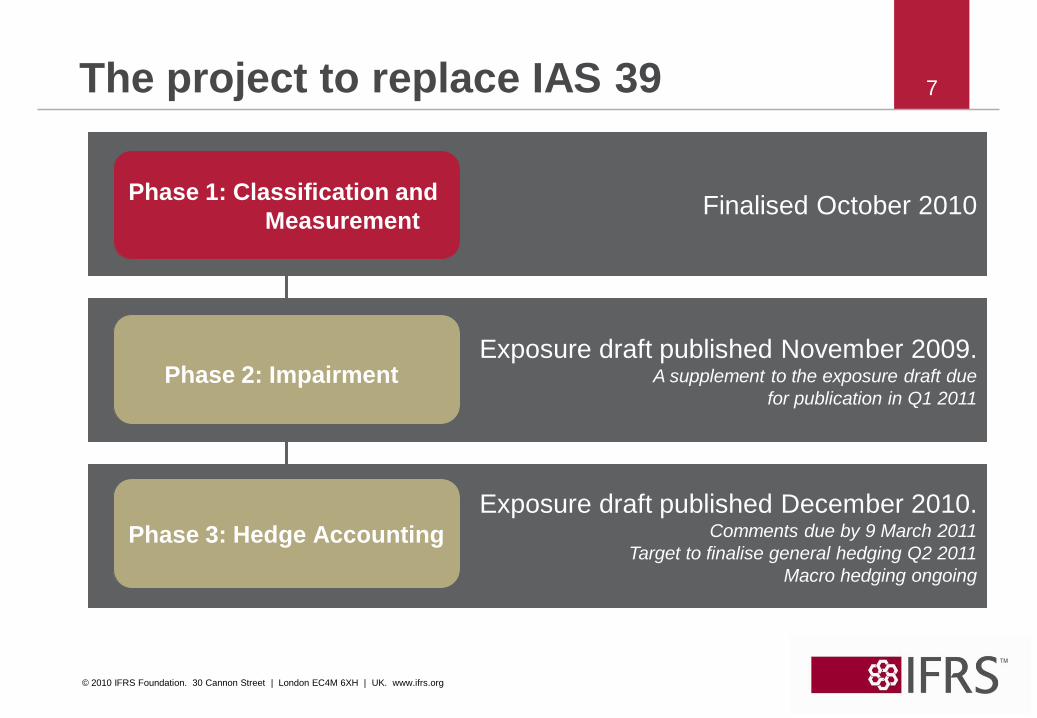

7

Exposure draft published December 2010.Comments due by 9 March 2011

Target to finalise general hedging Q2 2011

Macro hedging ongoing

Exposure draft published November 2009.A supplement to the exposure draft due

for publication in Q1 2011

Finalised October 2010

The project to replace IAS 39

Phase 1: Classification and

Measurement

Phase 2: Impairment

Phase 3: Hedge Accounting

International Financial Reporting Standards

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

Hedge Accounting Exposure draft

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

9Introduction

• The Board is considering hedge accounting comprehensively

• Overall approach:

– Use existing architecture

– Address specific problem areas

– Use clear and explicit principles

– Identify any exceptions clearly

– Consider application to portfolios

– Not opening hedge accounting for hedges of net investments in foreign operations

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

10Components of the hedge accounting model

Alternatives to

hedge accounting

Presentation and

Disclosure

Groups and net

positions

Discontinuation

and rebalancing

Effectiveness

assessment

Hedging instruments

Hedged items

Objective

Hedge accounting

(exposure draft)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

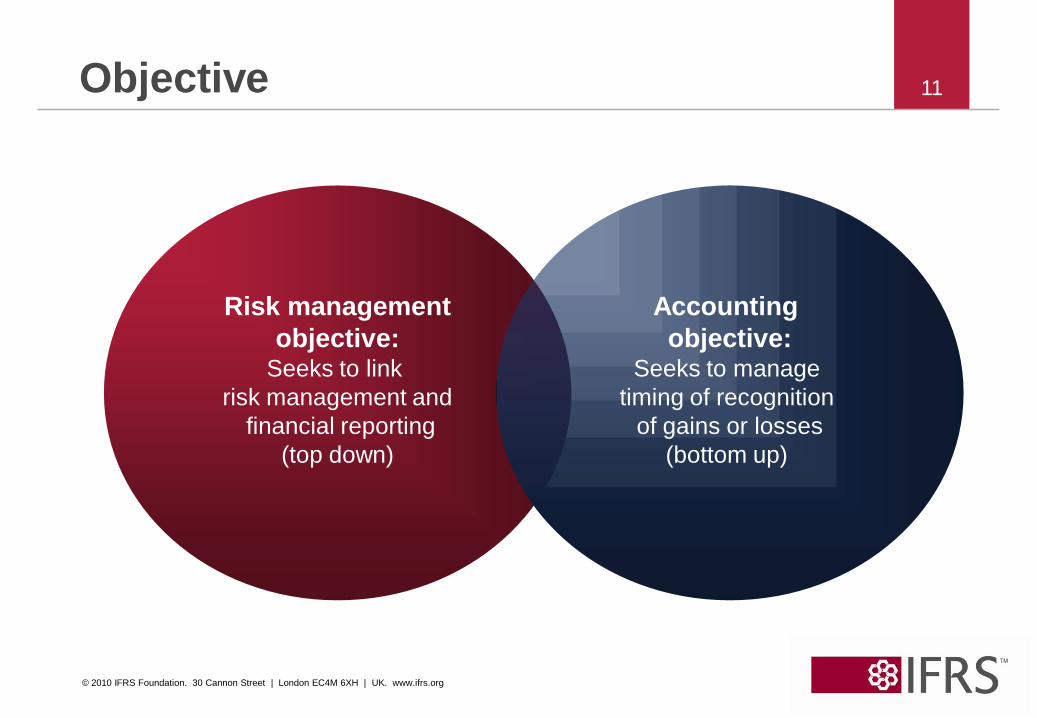

11Objective

Risk management

objective:Seeks to link

risk management and

financial reporting

(top down)

Accounting

objective:Seeks to manage

timing of recognition

of gains or losses

(bottom up)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

12Hedged items

Qualifying

hedged item

Entire item Component(identifiable and measurable)

Risk component Nominal component

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

13Hedged items: risk components

Benchmark

(eg interest

rate or

commodity

price)

Benchmark

(eg interest rate or

commodity price)

Variable

element

Fixed elementF

ina

ncia

l an

d n

on

-fin

an

cia

l

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

14Hedged items: risk components

• Proposals:

– LIBOR components in ‘sub-LIBOR’ interest bearing

financial instruments

– Designated risk component should not exceed the total cash

flows of the hedged item

– But: can still designate all the cash flows of the the hedged item

(for LIBOR risk!)

Retain the restriction in IAS 39

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

15Hedged items: aggregated exposures

Aggregated

exposure

IssuerCross-currency

Interest rate swap

Debt holderUS$

US$

€

€

€Interest rate swap

Not an eligible

hedged item

under IAS 39

Aggregated exposure—combination of: (a) another exposure and

(b) a derivative

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

16Hedged items: nominal components

• Proposals:

– Two types of nominal components:

– Percentage component (ie proportional to nominal amount of

item)

– Layer component

Type affects accounting outcome

– Layers eligible for groups of items and individual items

Exception: if a prepayment option exists (unless the strike price

is the fair value of the underlying)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

17Hedging instruments

Hedging

instruments

Qualifying

instrumentsDesignation

Entire item with exceptions for:•Intrinsic value and time value

•Spot element and interest element

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

18Time value of options

Time value

of options

Transaction related

hedged item

Time period

related hedged item

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

19Hedge effectiveness

Hedge

effectiveness

Hedge effectiveness requirements

(qualifying criteria):

1. Objective of effectiveness

assessment is met

2. More than accidental offset

Measuring and recognising

hedge ineffectiveness

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

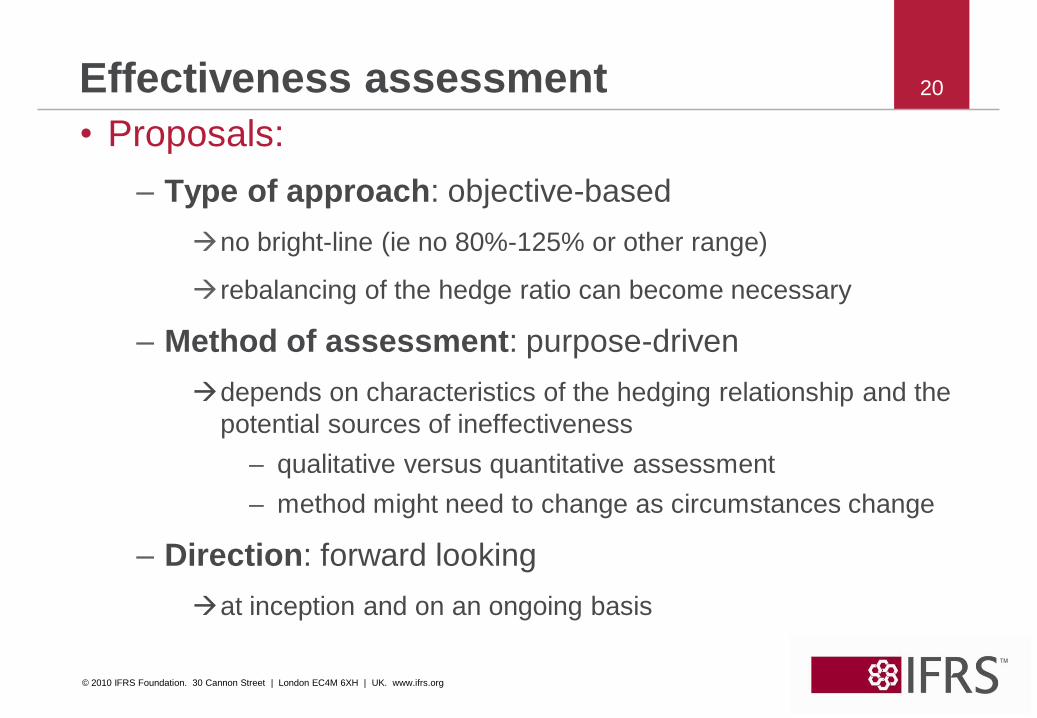

20Effectiveness assessment

• Proposals:

– Type of approach: objective-based

no bright-line (ie no 80%-125% or other range)

rebalancing of the hedge ratio can become necessary

– Method of assessment: purpose-driven

depends on characteristics of the hedging relationship and the

potential sources of ineffectiveness

– qualitative versus quantitative assessment

– method might need to change as circumstances change

– Direction: forward looking

at inception and on an ongoing basis

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

21Effectiveness assessment

Original

hedge ratio

Revised hedge ratio

New trend

Rebalancing

‘Perfect’ ratio with

benefit of hindsight

One (continuing) risk management and hedge

accounting relationship

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

22Effectiveness assessment

• Proposals:

– Objective of hedge effectiveness assessment

– Hedging relationship should produce an unbiased result and

minimise expected hedge ineffectiveness

Risk management determines the ‘optimal’ hedge ratio

ie no expectation that changes in the value of the hedging

instrument will systematically either exceed or be less than the

change in value of the hedged item such that they would produce a

biased result

this does not mean that a hedging relationship has to be expected

to be perfectly effective

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

23Discontinuation and rebalancing

Hedge relationship

does not meet the

effectiveness criteria

Risk management

objective remained

the same

The risk management

objective changed

Discontinue

hedge accounting

Other than

Accidental offsetAccidental offset

Discontinue

hedge accounting

Continue

Hedge accounting

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

24Discontinuation and rebalancing

• Proposals:

– Mandatory discontinuation

– When hedging relationship ceases to meet the qualifying criteria

– Discontinuation and restart

– Change in the risk management objective

– Adjusting a continuing hedging relationship

– Risk management objective remains the same but fail (or are about to fail) objective of hedge effectiveness assessment

– Revocation of designation prohibited

– When all the qualifying criteria are still met (including the risk management objective)

‘Rebalancing’

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

25Rebalancing

• Proposals:

– Rebalancing

– response to changes in the relationship between hedging

instrument and hedged item

evaluate whether changes in the extent of offset are:

– fluctuations around the hedge ratio versus

– an indication that the relationship between hedging

instrument and hedged item changes

– Continuation of the existing hedging relationship

different implications depending on whether hedging

instrument or hedged item is adjusted

– Update documentation

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

26Discontinuation

• Proposals:

– Partial discontinuation

– Consequence of some rebalancing scenarios

– Forecast transactions: insufficient headroom

– Some of the hedged volume is no longer highly probable

– Hedging relationship continues for volume that is still highly

probable

– History of downward adjustments of hedged forecast

volumes would affect the ability to forecast occurrence of

similar items

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

27Groups and net positions

Apply hedge

accounting model

for individual

items in addition to

meeting additional

requirements for:

Eligibility of a group

of items as

hedged items

Designation of a

component of a

nominal amount

Presentation Nil net positions

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

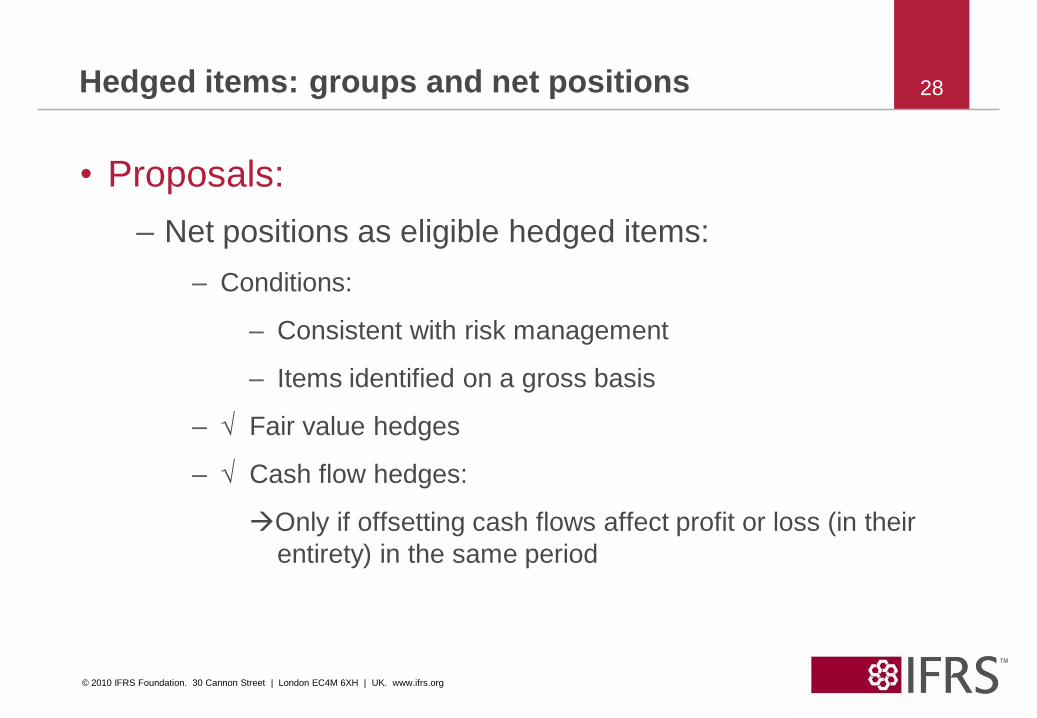

28Hedged items: groups and net positions

• Proposals:

– Net positions as eligible hedged items:

– Conditions:

– Consistent with risk management

– Items identified on a gross basis

– √ Fair value hedges

– √ Cash flow hedges:

Only if offsetting cash flows affect profit or loss (in their

entirety) in the same period

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

29Hedged items: groups and net positions

• Proposals:

– Change in fair value of individual hedged items need not

be proportional to that of the group

– Permit layer approach (eg bottom layer) to identifying

hedged items from a group

– Separate line item presentation of hedging instrument

gains or losses for net position hedges if group has

offsetting risks

– For example sales and purchases hedged for FX risk or interest

revenue and expense

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

30Presentation

Presentation

Cash flow hedges Fair value hedges

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

31Presentation: fair value hedges

• Balance sheet

– Hedged item

– Hedge adjustment (change in value of the hedge item)

– Hedging instrument

• Income statement (and OCI)

– Hedge ineffectiveness (income statement)

– Change in the hedged item (OCI)

– Change in the hedging instrument (OCI)

– Hedge ineffectiveness (OCI)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

32

Total entity risk exposure

(no specific disclosure requirements)

Disclosures: scope

Proposed scope for hedge accounting disclosures

Hedged exposure

(Exposure to

risks being

hedged)

IFRS 7

Disclosure

requirements

Significance of

financial instruments

for financial position

and performance

Nature and extent of

risks arising from

financial instruments

Entity’s exposure

attributable to the

hedged risk

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

33Disclosures proposed

Hedge accounting

disclosures

Risk management

strategy

The amount, timing

and uncertainty of

future cash flows

Effect of hedge

accounting on the

primary financial

statements

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

34Alternatives to hedge accounting

Alternatives

‘Own use’ scope exception

in IAS 39

Credit derivatives

(not proposed)

3 Alternatives

Proposed

consequential

amendment

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

35Hedges of credit risk using credit derivatives

• Issue:

– Difficult to isolate and directly measure the credit risk

component for hedge accounting purposes

– Fair value option too restrictive and not available for

most loan commitments

• Proposals:

– Board considered elective fair value accounting for part

of the nominal amount of the credit exposure

– Board does not propose elective fair value accounting

due to complexity

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

36Knock-on effects of other project phases

• Proposals:

– Embedded derivatives

– embedded derivatives are eligible hedging instruments only if

separated from their host contract

no longer available under IFRS 9 for asset host contracts

– Equity investments for which the OCI presentation

alternative is elected

– hedge accounting is not available for instruments designated at

fair value through OCI

– Impairment

– interaction of expected loss model with ‘highly probable’

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

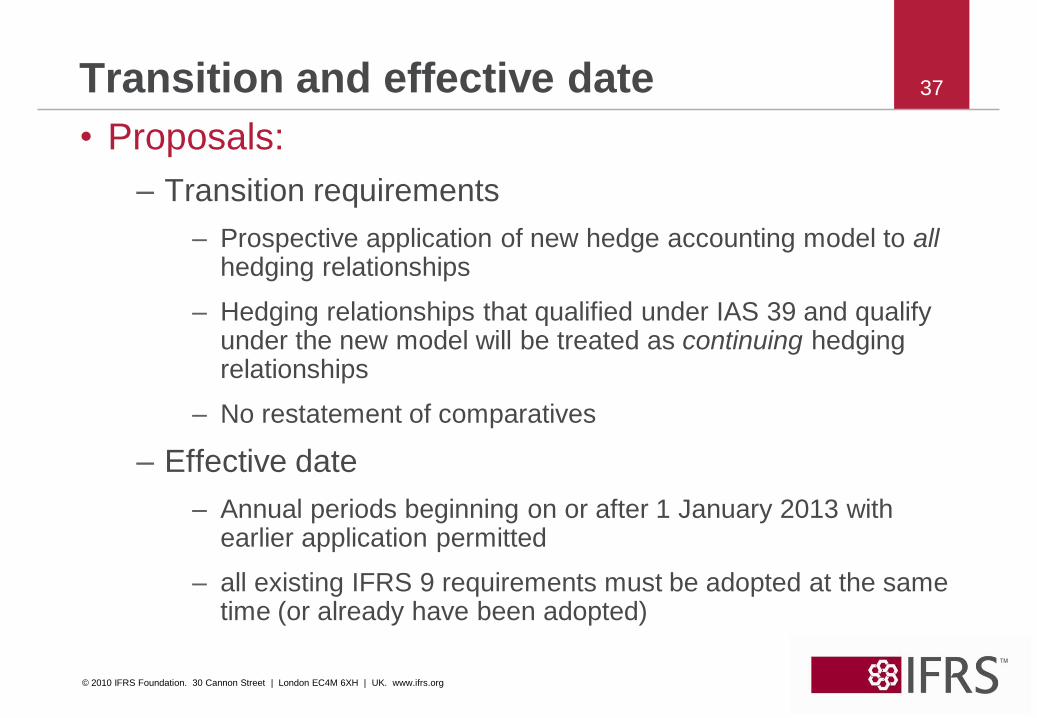

37Transition and effective date

• Proposals:

– Transition requirements

– Prospective application of new hedge accounting model to allhedging relationships

– Hedging relationships that qualified under IAS 39 and qualify under the new model will be treated as continuing hedging relationships

– No restatement of comparatives

– Effective date

– Annual periods beginning on or after 1 January 2013 with earlier application permitted

– all existing IFRS 9 requirements must be adopted at the same time (or already have been adopted)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

38Where we are and next steps…

• Exposure draft issued in Q4 2010

• Board continuing discussions on macro hedging

• Outreach activities

• Re-deliberations

• IFRS in Q2 of 2011

2010 2011

Q3 Q4 Q1 Q2 H2

Hedge accountingED

IFR

S

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

39Additional information

• The hedge accounting project page on the IASB website (www.ifrs.org) contains additional information on:

– Disclosures

– Hedge accounting mechanics

– Groups and net positions

– Risk components

– Effectiveness criteria

– Rebalancing

– Time value of options

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

40Questions or comments?

Expressions of individual views

by members of the IASB and

its staff are encouraged. The

views expressed in this

presentation

are those of the presenter.

Official positions of the IASB on

accounting matters are

determined only after extensive

due process and deliberation.