exports of goods & services and imports - the … of goods & services and imports ca. n.c....

TRANSCRIPT

Exports of Goods & Services and Imports

CA. N.C. Hegde

Intensive Study Course on FEMA

The Chamber of Tax Consultants

22 December 2017

2

Content..

Its turnover for any of these 5 years < INR 25 crore

Overview Measures for export promotion Mid-term review of FTP 2015-20 Definition FEMA Provisions Declaration Exemption from Declaration Other exports Invoicing of software exports Agency commission on exports Dispatch of documents Realization of export proceeds Advance against exports/

Reduction in invoice value Extension of time for realization Write-off of export bills Refund of export proceeds Setting up of offices abroad Trade fairs, Consignment exports,

Overseas warehouses Start-ups Project exports & Service exports

Overview Definition IDPMS – Revised procedure w.e.f.

October 2016 Forms & Payments for imports Time limit for settlement Third party payment Advance remittance Receipt of import bills/ documents Evidence of import Extension & Write-off Miscellaneous Merchanting Trade Issue of shares against legitimate

dues

EXPORTS IMPORTS

EXPORTS

4

Overview:

Framework

Foreign Trade Policy,

2015-2020 [The

Handbook of Procedures]:

*DGFT Guidelines

*IEC

FEMA, 1999:

*Section 2(l) –Definition

*Section 7 – Export

of goods & services

*Section 8 –Realization &

repatriation of

foreign exchange

*Section 9 –Exemption from

realization &

repatriation

Foreign Exchange Management

(Export of Goods and Services)

Regulations, 2015 –RBI Notification No. FEMA 23(R)/ 2015-

RB dated 12 January 2016

(amended upto 23 June 2017)

Foreign Exchange Management

(Current Account Transactions) Rules,

2000

RBI FED Master Direction No.

16/2015-16 dated 1 January 2016

(updated as on 16 November 2017)

5

Measures for export promotion:

FTP 2015-2020 announced on 1 April 2015 with a focus on supporting manufacturing & services exports

Merchandise Exports from India Scheme (MEIS) introduced to incentivize export of merchandise manufactured in India

Launching of the Services Exports from India Scheme (SEIS) with a view to reward export of notified services

The Niryat Bandhu Scheme implemented to mentor and facilitate new & potential exporters including exporters from MSMEs

Interest Equalization Scheme on pre & post shipment credit launched to provide cheaper credit to exporters

Access to duty free raw materials & capital goods for export purposes through schemes like Advance Authorization, Duty Free Import Authorization (DFIA), Export Promotion Capital Goods (EPCG) & drawback/ refund of duties

6

Mid-term review of FTP 2015-2020 released on 5 December2017 – Key Highlights:

Ineligible categories under SEIS pruned to expand the scope of the Scheme

SEIS incentive increased by 2% for specified services

Increase in MEIS incentive by 2% for exports by MSMEs & labour intensive industries

Self-certification of duty free raw materials/ inputs under Advance Authorization Scheme

To remove ambiguity, Government to notify negative list of capital goods not permissible under the EPCG Scheme

Clubbing allowed of two or more EPCG authorization issued to same person

Shifting of capital goods between units of IEC holder allowed without payment of duty

Concept of DTA sale from EOU on concessional & full duty, removed

Transfer of manufactured goods from one EOU to another allowed on payment of applicable GST & Compensation Cess

EOUs may import/ procure from bonded warehouse in DTA without payment of customs duty, IGST & Compensation Cess

DGFT has activated a single window for resolving all foreign trade related issues

Other measures related to trade facilitation, ease of doing business & deemed exports

7

Definition:

Section 2(l) of FEMA, 1999:

“export”, with its grammatical variations and cognate expressions, means—(i) the taking out of India to a place outside India any goods,

(ii) provision of services from India to any person outside India;

Regulation 2(iv) of the Foreign Exchange Management (Export of Goods & Services) Regulations, 2015:

'export' includes the taking or sending out of goods by land, sea or air, on consignment or

by way of sale, lease, hire-purchase, or under any other arrangement by whatever name

called, and in the case of software, also includes transmission through any electronic media

8

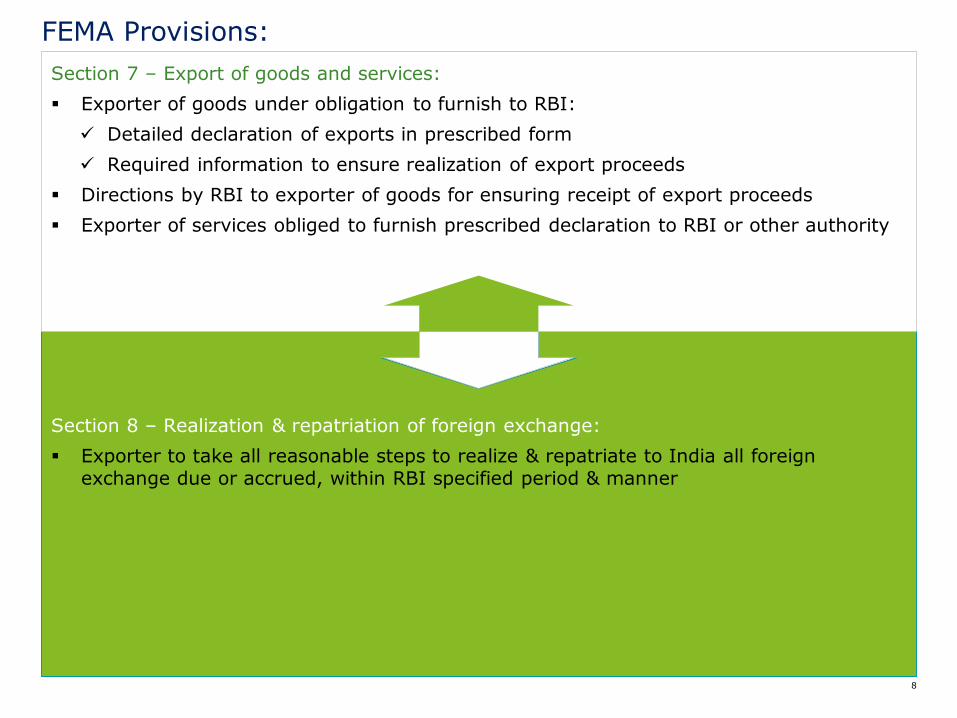

FEMA Provisions:

Section 8 – Realization & repatriation of foreign exchange:

Exporter to take all reasonable steps to realize & repatriate to India all foreign exchange due or accrued, within RBI specified period & manner

Section 7 – Export of goods and services:

Exporter of goods under obligation to furnish to RBI:

Detailed declaration of exports in prescribed form

Required information to ensure realization of export proceeds

Directions by RBI to exporter of goods for ensuring receipt of export proceeds

Exporter of services obliged to furnish prescribed declaration to RBI or other authority

9

Declaration:

• Submission in duplicate to the Customs at the shipment port

• Customs will record the declared & assessed value

• For goods to be sent by post, Form to be countersigned by AD Bank & then postal authority will allow export

• Form also available online

Form EDF- Export of goods from non EDI ports:

• To be filed with STP / EPZ / SEZ authorities not later than 30 days from date of last invoice raised in the month

• A common Form for single as well as bulk exports

• Form also available online

Form Softex –Export of software other than in physical form:

Submission of Form dispensed as declaration subsumed in the Shipping Bill

Form SDF – Export of goods from EDI ports:

No Form prescribed

Export of services:

Declaration by Exporter

10

Exempt from Declaration: (1/2)

Trade samples of goods and publicity material supplied free of payment

Personal effects of travellers

Ship stores / trans-shipment cargo and goods supplied under Government / military orders

Gift of goods, the value of which is not more than INR 5 lakhs

Aircrafts / aircraft engines /spare parts for overhauling / repairs abroad subject to re-import within 6 months of export

Goods imported free of cost on re-export basis

Following goods re-exported by units in EPZ / SEZ/ EHTP / STP / FTZ with relevant approval:– Defective goods to be replaced, or goods imported on loan basis, or goods imported

free of cost found surplus after production

Replacement goods exported free of charge per Foreign Trade Policy

Goods sent for testing or for repair subject to re-import

Defective goods exported for repair & re-import under AD Bank’s certificate

Exports permitted by the RBI

11

Exempt from Declaration: (2/2)

Waiver of EDF allowed by AD Banks in specified cases for export of goods free of cost for export promotion:– For Status Holder exporters - lower of 2% of average annual export realization in 3

preceding licensing years or Rs. 10 lakhs– For others - 2% of average annual exports in 3 preceding FYs subject to a ceiling of

Rs. 5 lakhs

Re-export of unsold rough diamonds from SNZ of Customs – Entry of such diamonds is not permitted into DTA

12

Other exports:

Exports requiring prior RBI approval:– Export of goods on hire purchase, lease, etc.– Exports on Elongated credit terms

AD Banks may:– Provide EDF approval for export of goods for re-imports after repairs, testing,

maintenance, calibration, etc.– Provide guarantee on account of exports from India– Allow export of goods pursuant to job work undertaken abroad by SEZ units– Allow export of goods and services by SEZ units to DTA units

Other permissible transactions (subject to compliance with conditions):– Short Shipments and Shut out Shipments– Counter Trade Arrangements involving adjustment of exports against imports– Exports by Indian partners towards equity participation in overseas JV/WOS– Mid-sea trans-shipment of catch by deep sea fishing vessels

13

Invoicing of software exports:

For long duration contracts: at least once a month or on reaching milestone as per the contract; last invoice to be raised not later than 15 days from date of contract completion

For ‘one shot operation’ contracts: within 15 days from date of transmission

Valuation as per declaration in Form SOFTEX

14

Agency commission on exports:

Permissible - no ceiling subject to declaration in Forms EDF / SOFTEX, valid agreement

The relative shipment has been made

Payment either by remittance or by deduction from invoice value

Specific conditions for commission payment relating to counter trade arrangements through escrow a/c in USD

Commission payment prohibited on exports by Indian partners towards equity participation in overseas JV/WOS & on exports under Rupee Credit Route; except that commission upto10% of invoice value permitted on exports of tea & tobacco

Issues: Whether agency commission can be paid on receipt of advance remittance? Whether payment of commission is permissible before shipment of goods?

15

Dispatch of documents:

Export documents to be submitted to AD Banks within 21 days from date of export or date of certification of Form SOFTEX

AD Banks to normally dispatch shipping documents to their overseas branches, correspondent

AD Banks can submit documents direct to the consignees or their agents:– If advance payment or irrevocable LC has been received– In case of regular exporter based on standing, track record, realization arrangements

AD Banks to permit Status Holder Exporters / SEZ units to dispatch export documents to the consignees outside India subject to basic conditions

AD Banks can regularize direct dispatches for exports upto USD 1 million per export shipment:– if the export proceeds have been realized in full– The exporter is a regular customer of the bank for minimum 6 months– Exporter’s a/c is KYC / AML compliant, transaction is bonafide, etc.

16

Realization of export proceeds: (1/3)

Invoice may be denominated in INR / freely convertible currency

Realization to be in freely convertible forex or INR (specific exports) through Banks or other specified forms, e.g. international credit card, etc.– Settlement in currencies not having a direct exchange rate permitted subject to

conditions

Realization in gold, silver, precious metals, etc. by Gem & Jewellery units in SEZ & EOU

Exporter not to take actions resulting in delay in realization or the full export value not being realized

AD Banks to generate Electronic Bank Realization Certificate (eBRC) from the EDPMS

Third party realization for exports allowable subject to:– Firm irrevocable order / tripartite agreement in place or mention in invoice/ order– AD Banks’ satisfaction with the bona fides of the transaction (FATF, etc.)– To be routed through banking channel only– Third party remittance to be declared in the Form EDF– Exporter responsible to realize & repatriate the proceeds from the third party– Outstanding would be reported in XOS in exporter’s name

Time period for realization of proceeds:– Export of goods / software / services – within 9 months from date of export– Exports to warehouse outside India– within 15 months from date of shipment– ‘Date of export’ explicitly clarified for software as ‘Date of invoice’– Can similar inference be drawn for goods & services?

17

Realization of export proceeds: (2/3)

Netting off permissible for SEZ units, of export receivables against import payables if both pertain to same party i.e. same Indian entity & foreign buyer/ supplier– Netting off permissible for entities other than SEZs?– Netting off when imports & exports are with different entities in the same group?

RBI may consider application from exporters having good track record for opening foreign currency account in or outside India

Receipt in foreign currency account:– EEFC – 100% of export– Special Account by SEZ unit – 100% of export– Diamond Dollar Account Scheme– RFC (D) – receipts by resident individuals

Online Payment Gateway Service Providers (OPGSPs)– through AD Banks for export value not exceeding USD 10,000

Exports to sanctioned countries:– Payments received from an open cover country shall be permitted third party

payments– Delay in realization of export proceeds permitted subject to satisfaction of AD Bank

Re-import into India within the stipulated period deemed to be full realization

Forfaiting and Export factoring on non-recourse basis permissible for financing of export receivables

18

EEFC A/c: (3/3)

Account to be a non-interest bearing current account

Credit facilities not permitted against security of EEFC balances

Eligible to credit 100% of forex earnings subject to the condition that:– Total accruals in a calendar month to be converted into INR on or before the last day

of the succeeding month after adjusting for utilization of the balances for approved purposes or forward commitments

– What is meant by forward commitment?

AD Banks may permit utilization of EEFC balances by exporters, to extend trade loans to overseas importers or to repay packing credit advances to the extent of actual exports

19

Advances against exports/ Reduction in invoice value:

Advance against exports

Goods to be exported / shipment made within 12 months from date of advance,else refund requires prior RBI approval, except where export agreement provides terms otherwise

RBI approval required for export beyond 12 months

AD Banks may allow exporters to receive advances for goods which take more than a year to manufacture subject to conditions

Long term export advances uptomaximum tenure of 10 years to be utilized for execution of long termsupply contracts subject to conditions (3 years track record, capacity, NPA rupee loan can’t be repaid, etc.)

Interest can be paid within permissible ceiling (LIBOR + 100 basis points)

Due diligence & follow up by AD Banks to ensure export performance within stipulated time

Reduction in invoice value

Prepayment of usance bill – cash discount - permissible as per agreement or to extent of proportionate interest at prime rate / LIBOR for unexpired period

Other cases with prescribed conditions -Permissible through AD Banks upto 25% of the invoice value or higher value within parameters stipulated

AD Banks to allow undrawn balance for difference in weight, quality, etc. upto10% of the full export value

issue: Can excess billing be reduced/ refunded without RBI approval?

20

Extension of time for realization:

Extension by AD Banks: Allowed upto 6 months at a time beyond the stipulated realization period, provided that:

– The reasons for not realizing are beyond the exporter’s control– The export transactions are not under investigation– The exporter declares that the proceeds will be realized within the extended period

For extension beyond 1 year from date of export, additionally:‒ Total outstanding does not exceed USD 1 million or 10% of average export

realizations during preceding three FYs, whichever is higher

If suit is filed against buyer, then extension irrespective of the amount outstanding

Cases to be referred to RBI:– Exporter expects to realize if further extension (beyond above) is allowed– Cases not covered under general permission

21

Write-off of export bills:

Write-off - Limits with respect to total export proceeds realized during the previous calendar year:– 10% for self write-off by Status Holder Exporter – 5% for self write-off by all other exporters– 10% for write-off with prior AD Bank approval– All other cases require prior RBI approval

Some conditions for self write-off:– Outstanding for a year or more and all efforts for realization made– Overseas party not traceable or declared insolvent– Goods destroyed by importing country authorities for regulatory reasons– Undrawn balance of an export bill not exceeding 10% of invoice value– Cost of legal action is disproportionate– Bills drawn for difference between LC value & actual export value, or between

provisional & actual freight charges, but were dishonored

For self write-off, CA Certificate to be submitted to the AD Bank certifying export realization in preceding calendar year, write-off already availed of during the year, EDF to be written off, invoice details, etc.

Write-off not permissible of: exports under investigation, exports to countries with externalization problem

Cases not covered above to be referred to the RBI’s Regional Office

22

Refund of export proceeds:

AD Banks through whom the export proceeds were originally realized, may consider requests for refund of export proceeds of goods being re-imported into India due to poor quality

While permitting such refunds, AD Banks to:– Verify the exporter’s track record & the bonafides of the transaction– Call for a certificate issued by DGFT / Customs that no incentives have been availed

against the export, or the proportionate incentives, if any, have been surrendered– Obtain an undertaking from the exporter that the goods will be re-imported within 3

months from the remittance date– Ensure that all procedures as applicable to normal imports are adhered to

23

Setting up of offices abroad:

Indian entities can set up branch or representative office abroad subject to ceilings

Remittance for initial expenses: higher of 15% of average annual sales/ income/ turnover during last two FYs or 25% of net worth

Remittance for recurring expenses: 10% of average annual sales/ income/ turnover during last two FYs, provided that the overseas office:– Conducts normal business activities of the Indian entity– Does not enter into any contract / agreement in contravention of FEMA– Does not create any financial liabilities (including contingent) for head office in India– Repatriates surplus funds abroad to India – no overseas investment allowed without

prior approval of RBI

Immovable property can be acquired for business purpose / residential purpose of staff within above ceilings

Reporting to AD Bank - opening of overseas bank account and audited yearly prescribed statements

Issues:– Can branch acquire assets other than the above?– Can Indian entities pay directly to overseas vendors on behalf of overseas branch?

24

Trade fairs, Consignment exports, Overseas warehouses:

Participation in Trade Fairs Abroad:– Permissible per compliance framework including foreign currency account abroad, EDF

waiver, etc.– Sale at discount permitted; Unsold goods can be sold in third country– Gift of unsold goods also possible (USD 5,000 per exhibition / per fair)

Consignment Exports:– Permissible as per compliance framework / undertaking for realization of proceeds

within stipulated timeframe– Freight and marine insurance must be arranged in India– Agents can deduct their expenses / remuneration and remit net proceeds – original

bills / receipts requirement stipulated– Issue: Can realization be lower or higher than declared value at the time of export?

Overseas warehouses‒ Permissible through AD Banks per compliance framework - initially for one year,

renewal thereafter‒ Export outstanding <5% of exports made during the previous FY‒ Minimum export turnover of USD 100,000 during the last FY‒ Period of realization to be applicable

25

Start-ups:

Revised definition by DIPP vide Notification dated 23 May 2017: An ‘entity’ shall be regarded as a startup upto 7 years (10 years for biotechnology startups) from the date of its incorporation, interalia if: :– Its turnover for any of these years < INR 25 crore– It works for innovation, development, improvement of products, processes, services,

or is a scalable business model with a high potential of employment generation or wealth creation

– Entity = private limited company, registered partnership firm, LLP

RBI Circular No. 51 dated 11 February 2016:– Start-ups with overseas subsidiaries permitted to open a Foreign currency account

abroad (FCA) to pool earnings out of exports/sales made– Start-ups’ overseas subsidiary also permitted to pool the receivables into FCA– Balances for exports due in FCA, to be repatriated into India within 9 months– Permitted to avail facilities provided by Online Payment Gateway Service Providers

(OPGSP) for value not exceeding USD 10,000– Appropriate contractual agreement between startup, overseas subsidiary and

concerned customer necessary– Issue: Are there any rules / restriction for utilization of pooled money?

26

Project exports & service exports - Background: (1/3)

Project Exports:– Export of Engineering goods (as stipulated) on deferred payment terms– Execution of turnkey projects abroad• Rendering of services like designing, civil construction & erection / commissioning

of plant /factory along with supply of machinery, equipment and materials– Execution of civil construction contracts abroad• Erection and civil construction contract and supply of construction material /

equipment going into the civil works

Service Exports:– Management & technical consultancy services, where contract execution involves grant

of fund based/ non-fund based facilities from Indian banking system or deferred payment terms

Foreign Exchange Management (Exports of Goods and Services) Regulations, 2015 applicable along with Memorandum of Instruction on Project & Service Exports (PEM), July 2014 read with RBI AP Dir Series Circular No. 39 dated 14 January 2016 & other circulars issued from time to time

27

Project exports – Approving authorities & procedure: (2/3)

AD or EXIM Bank (directly or through AD) are authorized to approve Project exports– Prior clearance from EXIM bank for its financial participation / guarantee

Consultation with ECGC if its counter guarantee is required

Indian sub-contractors of prime contractors also eligible to participate and any change in such sub-contractors requires compliance / approval

No application required at bid stage which can be given post-award of contract, subject to conditions in PEM

Application post-award to be within 15 days of execution of contract (6 sets) (Forms DPX 1 / PEX1 /TCS1)

AD / EXIM Bank to deal expeditiously with the approval of application post-award

Application to AD / EXIM Bank with an undertaking (Form PEX 2) for re-import of equipment exported outside India for execution of contracts

Service exports - No prior approval for facilities for contracts undertaken on ‘cash terms’ – Approval of AD / EXIM Bank will be required for contracts requiring facilities like

opening foreign currency bank account , site office abroad, etc.

No approval for pure supply of goods contracts (at least 90% proceeds realized within 6 months and balance in maximum 2 years and no fund / non-fund facility from the AD)

28

Project exports – Key facilities & compliances: (3/3)

Key Facilities

Bid bond / guarantee by AD Bank

Corporate guarantee

Opening of foreign currency bankaccounts abroad / in India subject toconditions

Buyer’s Credit/ Supplier’s Credit

Establishment of site / liaison offices

Fund based facility in India / abroad andguarantees in connection with same

Third country purchases

Inter-project transfer of machinery/ funds

Deployment of temporary cash surpluses

Payment of overseas agency commission

Export of construction equipment fromIndia

Key Compliances

Declaration of the exports/ consumables–EDF/SDF forms– Approval number and date to be

mentioned

Half yearly progress reports (June andDecember) within 1 month to approvingauthority – Form DPX-2

Quarterly reporting (Form AB) within 10 days from close of quarter– Total value of shipment effected and

advance payment / deferred installments received

Details of own corporate guarantee to bereported to AD / EXIM Bank within 15 days from issue of such guarantees

Compliances & reporting specified on completion of project

IMPORTS

30

Overview:

Framework

Foreign Trade Policy,

2015-2020 [The

Handbook of Procedures]:

*DGFT Guidelines

*IEC

*Import Licenses,

where applicable

FEMA, 1999:

*Section 2(p) –Definition

*Section 5 –Current account

transactions

Foreign Exchange Management

(Current Account Transactions) Rules,

2000

RBI FED Master Direction No.

17/2016-17 dated 1 January 2016

(updated as on 12 January 2017)

31

Definition:

Section 2(p) of FEMA, 1999:

“import”, with its grammatical variations and cognate expressions, means bringing into India any goods or services

32

Key development in year 2016:

The RBI constituted a Working Group comprising representatives from Customs, DGFT, SEZ, FEDAI & select AD Banks, to suggest putting in place a comprehensive & a robust IT- based system in order to enhance the ease of doing business & to facilitate efficient processing & effective monitoring of all import transactions

The Group recommended the “Import Data Processing and Monitoring System” (IDPMS) on the lines of EDPMS

To track the import transactions through IDPMS, Customs modified the BoE format to display the AD Code of the bank concerned, as reported by the importers

Under the IDPS, primary data on import transactions from Customs & SEZ first flows to the RBI secured server & thereafter depending on the AD code is shared with the respective banks for taking the transactions forward

AD Banks to enter every subsequent activity viz. document submission, outward remittance data, etc. in IDPMS so as to update the RBI database on a real time basis

The IDPMS went live w.e.f. 10 October 2016

33

IDPMS – Revised procedure effective October 2016:

AD Banks to create ORMs for all import remittances for which evidence of import is pending receipt

Based on the AD code declared by the importer, Banks shall download the BoE issued by EDI ports from “BOE Master” in IDPMS

For non-EDI ports, importer’s AD Bank shall upload the BoE data as per message format “Manual BOE reporting” on daily basis on receipt of BoE from the customer/Customs

AD Banks shall enter BoE details (BoE number, port code & date) for ORM associated with advance payment as per the message format “BOE settlement”

For payments after receipt of BoE, AD Banks shall generate ORM as per the message format “BOE settlement”

Multiple ORMs can be settled against single BoE & also multiple BoE can be settled against one ORM

On settlement of ORM with evidence of import, AD Banks to issue an acknowledgement slip containing importer's name, address, code number, BoE number & date, the amount of import, recap advice on number & amount of BoE & ORM not settled for the importer

importer to preserve the printed ‘Importer copy’ of BoE as evidence of import and acknowledgement slip

34

Forms & Payments for imports:

Form A1 – Dispensed & AD Banks to obtain all requisite details; Form A2 - for all other overseas payments

Import license required for goods included in the negative list of the DGFT

For all other cases, AD Banks to freely open LCs and allow remittances for import payments after ensuring requisite details & bonafide of the transaction

AD Banks can give guarantees on behalf of importers (replacement imports covered)– For import of services, cap of USD 500,000 (for PSU, MoF approval required for

guarantee exceeding USD 100,000)

Forex purchased to be used for payment for imports or other permitted purposes– AD Banks to ensure that the importer furnishes evidence of import & that goods of

value equivalent to the remittance have been imported

Payment permitted:– Through international credit/ debit card for import of goods – In INR, towards meeting expenses on boarding , lodging, travel, etc. to & from &

within India of a person resident outside India, who is on a visit to India– By crossed cheque /draft for import of gold or silver in accordance with law– In INR to a non-whole time director resident outside India who is on an official visit to

India & entitled to payment of sitting fees, travel expenses etc. as per the company’s Memorandum /Articles of Association or agreement entered /resolution passed, subject to compliance with applicable law

Subject to conditions, fresh remittance for replacement permitted in case goods are lost-in-transit, damaged, short supplied

35

Time limit for settlement & Interest:

Time limit for settlement of import payments:– 6 months from date of shipment, except where amounts are withheld towards

guarantee of performance, etc.– Import of books allowed without time limit restriction– AD Banks to permit belated settlement (maximum upto 3 years) due to financial

difficulties, disputes, etc.• The import transactions should not be under investigation • For extension beyond 1 year, import dues not to exceed USD 1 million or 10% of

the average import remittances during the preceding 2 FYs, whichever is lower– Trade Credits i.e. Buyer’s & Supplier’s Credit, regulated by the prevalent provisions

on ECB and Trade Credits– Extension beyond above to be referred to the RBI’s Regional Office– Extension to be reported in IDPMS

Interest on import bills:– Payment of interest (@ Trade Credit rate) allowed on delayed payments not

exceeding 3 years– Pre-payment of usance bills – only after reducing proportionate interest on

unexpired portion of usance– Interest payment to be reported in IDPMS

36

Third party payment:

Allowable by AD Banks as under:– Firm irrevocable purchase order / tripartite agreement in place or mention in invoice

/order– AD Banks satisfied with the bonafides of the transaction (FATF, etc.)– Invoice & BoE contain narration related to payment to be made to third party– Importer complies with extant regulations relating to imports

37

Advance remittance:

Permissible without any ceiling but if advance exceeds USD 500,000 for services or USD200,000 for goods then unconditional irrevocable standby LC or guarantee from international bank of repute situated outside India required; guarantee of AD Bank in India if based on a counter guarantee by international bank, will also do

Non-PSU importer of goods can avail higher advance ceiling upto USD 5 million without aforesaid guarantee based on track record and bonafides in accordance with internal guidelines of the AD Bank

PSUs not satisfying above condition to obtain waiver from MoF if advance exceeds USD 100,000

Physical import within 6 months (3 years in case of capital goods)

If no imports then advance to be repatriated back or utilized for other permitted purposes

Advance to be given direct to manufacturer (supplier)

AD Banks to ensure creation of ORMs and marking off in IDPMS

Special provisions for advance remittance for import of rough diamonds and for aircrafts /helicopter / other aviation related purchases

38

Receipt of import bills/ documents:

AD Banks to ensure generation of ORMs and compliance with IDPMS

Receipt of documents by importer directly from overseas supplier - AD Banks to remit if:– Value of import bill does not exceed USD 300,000– Import bills received by WOS of foreign companies from their principals– Import bills received by Status Holder Exporters / EOU / SEZ / PSU– Import bills received by limited companies including private companies

Receipt of documents by the AD Banks directly from overseas supplier:– Financial standing / track record of the importer customer relevant– Report to be obtained on the overseas supplier from an international banker or credit

agency in cases where value of import bill exceeds USD 300,000

39

Evidence of import: (1/2)

Physical imports– BoE number, port code and date for marking evidence of import under IDPMS – Customs Assessment Certificate / Postal Appraisal Form or Courier BOE for import

by post / courier– Exchange control copy of the Ex-bond BOE or BOE issued by customs authorities for

goods stored in FTWZ or SEZ units, customs bonded warehouses, etc.• BoE number, port code and date for marking evidence of import to be submitted

under IDPMS– Delivery against acceptance – evidence to be verified from IDPMS

• On failure to produce documents for genuine reasons (non-arrival of consignment, delay in delivery/ customs clearance), AD Banks may allow time not exceeding 3 months from remittance to submit the evidence

– AD Banks shall create ORM and perform document submission, outward remittance data, matching with ORM, closing of transactions etc. as per IDPMS

CEO / Auditor Certificate in lieu of BOE– Amount of remittance not exceeding USD 1,000,000 or its equivalent; or– Importer is a listed company with Rs. 100 Cr net worth (last audited B/Sh) or– Importer is a PSU or government company– Autonomous body / scientific association whose accounts are audited by CAG– ORM to be created & BoE to be downloaded from “BoE Master “in IDPMS for EDI

ports. For Non-EDI ports, duplicate copy/customs certified copy have to be submitted or BoE waiver obtained from RBI

40

Evidence of import: (2/2)

Non-Physical Imports through internet / datacom channels / emails / fax, etc– CA certificate that the software /design / drawing has been received by the importer– Customs authorities to be kept posted by the importer– ORM not applicable– Practical difficulty in:

• Verification of imports through internet• Informing the custom authorities about such internet imports

Follow up for evidence of import:For all unsettled ORM i.e. on failure to receive the import evidence within 3 months from the date of remittance of foreign exchange, AD Banks to rigorously follow-up for the next 3 months, including issuing registered letters to the importer

41

Extension & Write-off:

AD Banks may allow extension for submission of BoE– Extension to be reported in IDPMS as per the message “Bill of Entry Extension”

AD Banks may permit closure of BoE/ ORM in IDPS towards write-off of:– Upto 5% of invoice value if the AD Bank is satisfied that the amount as per BoE

varies from the actual remittance due to operational reasons– Transactions of any value, if the write-off is due to quality issues, short shipment or

destruction of goods by authorities, subject to satisfactory documentation– Appropriate ‘Adjustment indicator’ to be recorded in IDPMS

While allowing write off, AD Banks to ensure that:– The case is not under litigation or investigation– There is a system to carry out random sample check of write-off of import bills

The guidelines for evidence of import in lieu of BOE will apply

Extension & write-off cases other than the above to be referred to RBI Regional Office

42

Miscellaneous: (1/2)

Import of Equipment by BPO companies:– General permission to install equipment overseas at international Call Centres– Approval of Ministry of Communication and Information Technology / other

authorities required– AD Banks to allow remittance based on commercial judgment, transactions

bonafides & contract terms– Remittance made directly to the overseas supplier’s account – Certificate from CEO / auditor of importer company that the goods have actually

been imported & installed at overseas site– Compliance with IDPMS guidelines applicable

Import of other precious metals (Platinum /Palladium/Rhodium/ Silver/Rough, Cut & Polished Diamonds / Precious and Semi-precious Stones)– Supplier’s and buyer’s credit should not exceed 90 days from date of shipment– Clean credit by supplier should not exceed 180 days from date of shipment– KYC, AML guidelines, credentials of supplier, close monitoring of transactions

envisaged

Import of platinum /silver on unfixed price basis– Import on outright purchase basis subject to passing of ownership at the time of

import– Price can be fixed later as when importer sells to customer

43

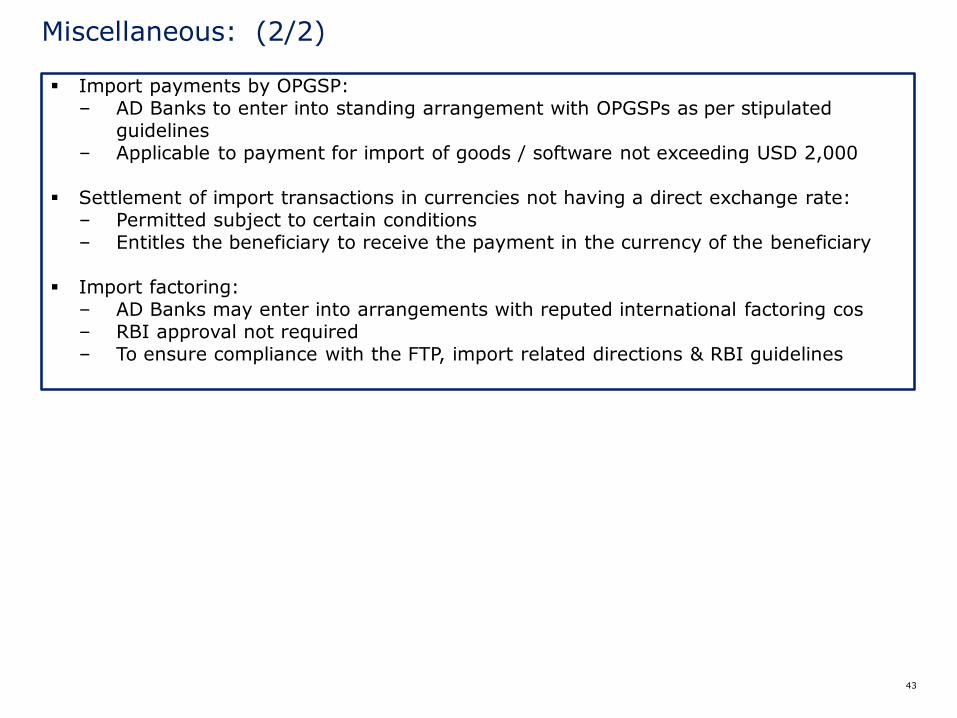

Miscellaneous: (2/2)

Import payments by OPGSP:– AD Banks to enter into standing arrangement with OPGSPs as per stipulated

guidelines– Applicable to payment for import of goods / software not exceeding USD 2,000

Settlement of import transactions in currencies not having a direct exchange rate:– Permitted subject to certain conditions– Entitles the beneficiary to receive the payment in the currency of the beneficiary

Import factoring:– AD Banks may enter into arrangements with reputed international factoring cos– RBI approval not required– To ensure compliance with the FTP, import related directions & RBI guidelines

44

Merchanting Trade:

Merchanting trade refers to offshore sourcing for offshore supply i.e.– Goods acquired should not enter the DTA; and– State of goods should not undergo any transformation

Goods permissible for import / export under FTP – genuine trade and not financial intermediaries

Both legs to be routed through same AD Bank – ensure one-to-one matching case

Entire deal to be completed within 9 months with no outlays of forex beyond 4 months:– Commencement date: Earlier of date of shipment / export leg receipt or import leg

payment– Completion date: Later of date of shipment / export leg receipt or import leg payment

Short term credit available to the extent not backed by advance remittance

AD Banks to ensure advance against export leg is earmarked for payment for import leg – short term deployment in interest bearing account allowed

Advance payment for import leg on demand allowable – general guidelines to be adhered

Payment for import allowed from balance in EEFC account

AD Banks to report defaults in any leg to the RBI Regional Office on half yearly basis

Issue: whether deal can be multiparty and whether trade can be in same country or different countries imperative?

45

Issue of shares against legitimate dues:

RBI Circular 31 dated 17 September 2014 – Issue of equity shares against legitimate dues:– Scheme over and above the issue of shares / convertible debentures to Non-resident

against lump-sum technical know-how fee, royalty, ECBs as stipulated and import payables for capital goods, etc.

– Issue of equity shares against any other funds payable by the investee company remittance of which does not require permission of the Government of India or RBI

– The equity shares shall be issued in accordance with the extant FDI guidelines on sectoral caps, pricing guidelines, applicable tax laws etc.

– Issues:• Issue of convertible preference shares/ debentures covered?• Whether overdue current account payments covered?

PRACTICAL INSIGHTS

47

Case Study 1 – Third party import payables:

100% holding

F Co. (Parent)

I Co. (WOS)

India

Outside India

VendorsPayment for sale made

to I Co.

Assets acquired were capitalized in the books of I Co. with the corresponding liability

depicted as amount payable to F Co.

Whether the aforesaid liability can be converted into ECB / equity?

3rd party import payables permissible, subject to

conditions – refer Slide 36

48

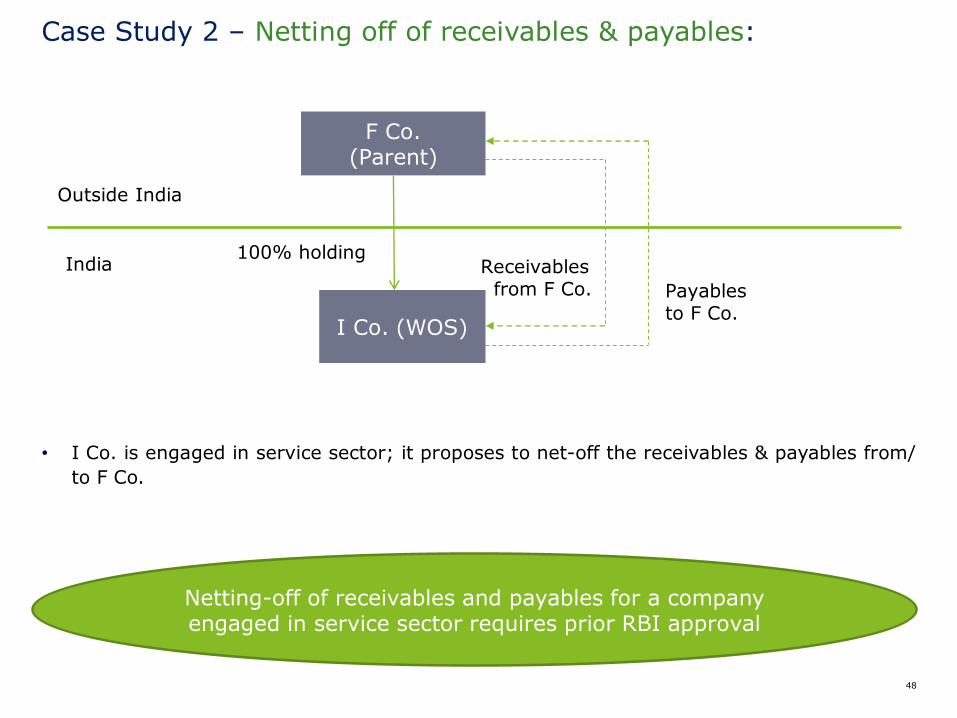

Case Study 2 – Netting off of receivables & payables:

• I Co. is engaged in service sector; it proposes to net-off the receivables & payables from/

to F Co.

Netting-off of receivables and payables for a company engaged in service sector requires prior RBI approval

100% holding

F Co. (Parent)

I Co. (WOS)

India

Outside India

Receivables from F Co. Payables

to F Co.

49

Case Study 3 – Invoicing in foreign currency for local sales:

• Can I Co. raise invoice on vendors in foreign currency?

Except for transactions with SEZ/ EOU/ EPZ/ EHTP/ STP,

transactions between two residents cannot be settled in

foreign currency

100% holding

F Co. (Parent)

I Co. (WOS)

Purchase of capital goods

India

Outside India

Vendors

Invoice

50

Case Study 4 – Deemed ECB:

• F Co. paid directly to vendors towards rent and travelling expenses on behalf of I Co.

• Auditors accounted the same as short term borrowing in the books of account of I Co.

Direct payment to vendors by F Co. on behalf of I Co. triggers provisions for Deemed ECB

100% holding

F Co. (Parent)

I Co. (WOS)

India

Outside India

Vendors

Reimbursement of expenses

51

Case Study 5 – EDF waiver:

• I Co. 2 places purchase order on F Co. for some components

• As some of the components are to be procured from India, F Co. places order with its

group company – I Co. with an instruction to deliver goods to I Co. 2

• Considering that goods do not cross the borders of India, custom documents are not

available, I Co. proposes for EDF waiver

RBI approval required for such an arrangement

Places sub-order with an instruction to deliver goods to I Co. 2

F Co. (Parent)

I Co.

India

Outside IndiaPO

I Co. 2Supplies goods

52

Case Study 6 – Merchanting trade:

• The Indian intermediary books the order from the buyer, places the order with the

supplier, supervises & coordinates the shipment of goods from the supplier’s country and

delivers the same in buyer’s country

• A merchanting trade transaction involves import of goods from a foreign seller & export

of the same goods to a foreign buyer by an Indian merchant. The Indian merchant

receives sales consideration for exports from overseas buyer & pays the purchase price

for imports to the overseas supplier through an AD Bank in foreign exchange in India

Merchanting trade is subject to conditions

Order placing

Supplier

Intermediary

India

Outside India

Buyer

Import

53

Case Study 7 – Reduction in export invoice:

• I Co. exported pharmaceutical products to F Co

• Due to change in market conditions & increased competition, the price of the

pharmaceutical products dropped

• F Co. & I Co. decided to reduce the invoice amount

• Reduction by I Co. in the invoice is exceeding the limit prescribed

Reduction in invoice value is permitted subject to prescribed limits – else AD bank / RBI approval required

100% holding

F Co. (Parent)

I Co. (WOS)

India

Outside India

Receivables from F Co. Export

to F Co.

Thank You

55

Abbreviations:

AML Anti-Money LaunderingBoE Bill of EntryCAG Comptroller and Auditor GeneralDGFT Directorate General of Foreign TradeDTA Domestic Tariff AreaECB External Commercial BorrowingsEDI Electronic Data InterchangeEDPMS Export Data Processing & Monitoring SystemEEFC Exchange Earners’ Foreign CurrencyEHTP Electronic Hardware Technology ParkEOU Export Oriented UnitEPZ Export Processing ZoneEXIM Export Import Bank of IndiaFATF Financial Action Task ForceFDI Foreign Direct InvestmentFEDAI Foreign Exchange Dealers Association of IndiaFEMA The Foreign Exchange Management Act, 1999Forex foreign exchangeFTZ Free Trade ZoneFY Financial YearGST Goods and Services TaxIGST Integrated Goods and Services TaxIDPMS Import Data Processing & Monitoring SystemIEC Importer Exporter CodeINR Indian RupeesJV Joint VentureKYC Know Your Client

LC Letter of CreditMOF Ministry of FinanceMSME Micro, Small & Medium

EnterprisesORM Outward Remittance MessagePSU Public Sector UndertakingRBI Reserve Bank of IndiaRFC(D) Resident Foreign Currency

(Domestic)SEZ Special Economic ZoneSNZ Special Notified ZoneSTH/PTH Star/ Premier Trading HouseSTP Software Technology ParkWOS Wholly Owned SubsidiaryXOS Export Outstanding Statement