export-import bank of india -...

TRANSCRIPT

1

EXPORT-IMPORT BANK OF INDIA

OCCASIONAL PAPER NO. 147

INDIAN ELECTRONIC INDUSTRY :PERSPECTIVES AND STRATEGIES

© Export-Import Bank of IndiaMarch 2011

EXIM Bank’s Occasional Paper Series is an attempt to disseminate the findings of research studies carried out in the Bank. The results of research studies can interest exporters, policy makers, industrialists, export promotion agencies as well as researchers. However, views expressed do not necessarily reflect those of the Bank. While reasonable care has been taken to ensure authenticity of information and data, EXIM Bank accepts no responsibility for authenticity, accuracy or completeness of such items.

2

3

CONTENTS

Page No. List of Tables 5List of Exhibits 7 List of Boxes 9Executive Summary 111. Introduction 472. Global Scenario 493. Indian Scenario 804. Challenges, Government Policies and Strategies 111Annexure1. Production of Electronic Products 1402. World Export of Telecommunications Equipment 1413. World Export of Computer and Related Equipment 1424. World Export of Electronic Components 1435. World Export of Audio and Video Equipment 1466. Export of Other ICT 148 (Information and Communication Technology) Goods7. Major players in the Telecommunications Equipment Industry 1518. Annual Plan of Department of Information Technology 2010-11 1529. India’s Exports and Imports of Telecommunications Equipment 15310. India’s Exports and Imports of Computer and Related Equipment 15411. India’s Exports and Imports of Electronic Components 15612. India’s Exports and Imports of Audio and Video Equipments 16013. India’s Exports and Imports of other ICT goods 163

Project Team:

Mr. S. Prahalathan, General Manager, Research and Planning GroupMs. Renuka Vijay, Manager, Research and Planning Group

4

5

Table No. Title Page No.

1 Market Segmentation of Select Sub-Sectors of Electronic 53 Industry in Asia Pacific Region (2009)

2 Improvement Trends for Integrated Circuits Enabled by 55 Feature Scaling

3 Exports of Select Electronic Goods in the World 56

4 Leading Exporters and Importers of Select Electronic Goods 57

5 Exports and Imports of Select Electronic Items from China 62

6 Exports and Imports of Select Electronic Items from Singapore 65

7 Exports and Imports of Select Electronic Items from Hong Kong 68

8 Exports of Electronics from Japan 73

9 Imports of Electronics by Japan 74

10 Electronics Production in India 82

11 Demand for Colour TVs 85

12 Overall Market Share of Key Players 87

13 Revenue of Telecom Equipment Industry 97

14 Top 10 players in Telecommunications Equipment Industry 98

15 India’s Major Export Destinations and Import Sources of 108 Electronic Products (2009-10)

16 Contribution of Different Items and Categories of Electronic Goods 110

17 R&D Expenditure in India by Sectors (2009-10) 114

18 Benefits Available for EHTP/STP/EOU and SEZ Units 120

LIST OF TABLES

6

7

Exhibit No. Title Page No.

1 Growth Cycle of World Electronics Industry 49

2 Segment-wise Production of World Electronic Industry 2008 50

3 Estimated Growth of Electronics Market in the World 51 (2013 vs 2008)

4 Estimated Growth in Production of Electronics in the 51 World (2013 vs 2008)

5 Region-wise Production of World Electronic Industry 2008 52

6 Exports of Electronic Goods in the World 56

7 Major suppliers of Office and Telecom Equipment to EU 27 (2009) 58

8 Major suppliers of Office and Telecom Equipment to USA (2009) 59

9 Major suppliers of Office and Telecom Equipment to China (2009) 59

10 Production of Electronics Products in China 61

11 China’s Consumption of Electronic Components in Manufacturing 62

12 Global Production by Japanese Electronics Industry 72

13 Domestic Production by Japanese Electronics Industry 72

14 Phases of Development 80

15 Production of Electronics Hardware in India 81

16 Percentage Share of Electronics Production in GDP 83

17 Growth of Consumer Electronics Market in India 84

18 Production of Consumer Electronics in India 85

19 Demand for Colour TV (Size-wise) 86

20 Trend in Demand for Colour TVs 86

21 Growth of Computer Hardware Market in India 89

LIST OF EXHIBITS

8

Exhibit No. Title Page No.

22 Production of Computers in India 90

23 Total PC Sales 90

24 Total Desktop Sales in Business and Households. 91

25 Production of Industrial Electronics in India 92

26 Growth of Subscriber Base in India 94

27 Wireless Services Segment: Service Provider Market 94 Share as on 30.12.2010

28 Wireline Service Segment: Service Provider Market 95 Share as on 30.12.2010

29 Telecom Equipment Production in India 100

30 Telecom Equipment Exports 100

31 Production of Strategic Electronics in India 102

32 Production of Components in India 104

33 India’s Exports and Imports of Electronic Goods 105

34 India’s Major Export Destinations (region-wise) 2009-10 107

35 India’s Major Source Countries (region-wise) 2009-10 107

36 Gross Domestic Expenditure on R&D as Percentage of GDP for Select Countries (2008 or latest available year) 114

9

Box No. Title Page No.

1 Automotive Electronics Council (AEC) 75

2 Information Technology Agreement 77

3 Next Generation Network (NGN) 99

4 Seminonductor Industry in India 106

5 Electronic Manufacturing Services (EMS) 109

6 Restriction of Hazardous Substances (RoHS) 117

7 Electronic Hardware Technology Park (EHTP) Scheme 119

8 EMC Certification Scheme 131

LIST OF BOXES

10

11

INTRODUCTION

Worldwide, the electronic industry is one of the most flourishing and extremely diversified sectors, growing at a rapid pace with the invention of innovative technologies and growing customer inclination towards electronic goods and services. The industry has been experiencing phenomenal and remarkable changes over the years, and is being distinguished with other industries by way of technological developments. The key segments of the electronic industry are electronic components industry, computer and office equipments, telecommunications, consumer electronics and industrial electronics.

GLOBAL SCENARIO

Production

World electronics production is estimated to be Euro 1.13 trillion in 2008. Telecom and data processing equipments are the two largest segments accounting for 25%, and 21%, respectively, of the total world electronics production in the year 2008. Industrial and medical

electronics accounted for 18% share, and audio-video equipments accounted for 15% share in world production of electronics. Automotive (8%), aerospace & defence (7%), and home appliances (6%) are other sub-sectors in electronic production.

Until 2013, the total word electronics production is expected to grow at a CAGR of 2.7%. The major difference among the growth in geographical areas will be their capacity to recover from the recent market downturn. In this respect, China is expected to outperform other regions.

China (growth of 7%) is expected to show the highest growth followed by other Asia Pacific countries (5.8%). Europe and North America are expected to show deceleration in their production owing to the recovery phase after the economic recession. Production is expected to grow by 3% in 2013 with the Asian countries likely to dominate the market space. Other Asia Pacific countries and China are expected to show the highest growth of 7.1% and 6.9%, respectively. Production in 2008 was estimated at Euro 778.4 billion, which is expected to grow to Euro 898.6 billion in 2013.

EXECUTIVE SUMMARY

12

Major Production Centres

Analysis of region-wise production of electronics reveals that Asian countries dominate the production scenario of electronics in the world, with China being the largest producer, with 26% share in total world production, followed by Europe (22%), North America (18%), and the rest of Asia Pacific countries with 16% of total production in 2008. Even though Asian countries have been dominating the production scenario, developed economies have not lost their significance in the electronics industrial landscape. Europe and North America still stand at 2nd and 3rd positions, respectively, in terms of electronics production in the world, together representing up to 40% of the world electronics production in 2008.

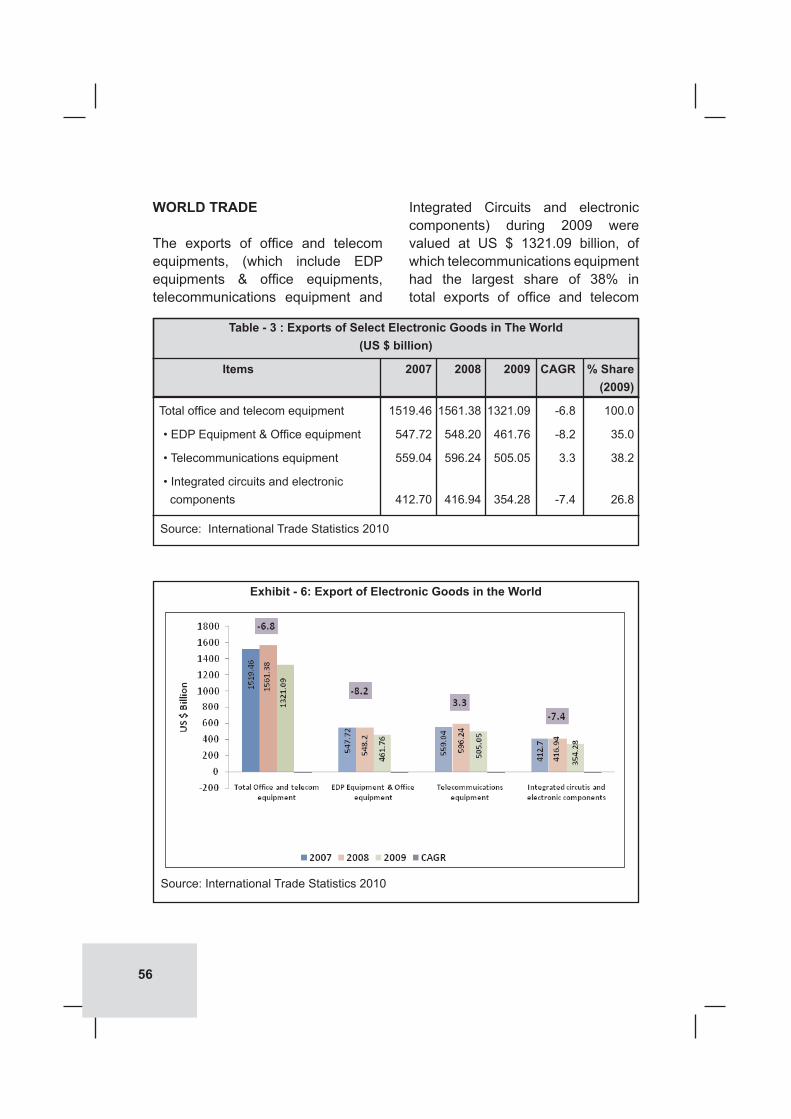

World Trade

The world exports of office and telecom equipments (which include EDP equipments & office equipments, telecommunications equipments and Integrated Circuits and electronic components), during 2009 were valued at US $ 1321.09 billion, of which telecommunications equipment had the largest share (38%). EDP equipment & office equipment, and Integrated Circuits and electronic components had a share of 35%, and 27%, respectively. The major countries / regions exporting most

of the electronic goods include: EU (27), China, Hong Kong, USA, Singapore and Korea Republic; and the major importing countries in the world include: EU (27), USA, China and Hong Kong. However, all the categories have shown a decline over the previous year owing to the economic slowdown that took place during 2008 and 2009.

CHINA’S ELECTRONIC INDUSTRY

Electronics Industry is the largest industry in China, and is growing at an average 20% per annum. China is one of the largest producers of TVs, recorders, VCD players, telephones, and holds a leading edge in semiconductor and computer industry. Growing indigenous demand, and a large number of overseas manufacturers aiming for economizing costs have boosted the electronic industry in China.

The production of electronic products has been rising in China, at a CAGR of around 20% over the last decade. One of the main reasons for this level of growth has been the increase in consumption of electronic components for manufacturing, which has led to an increase in demand. During 2009, exports and imports had declined due to the economic slowdown. China was the largest exporter of EDP equipment and office equipment in 2009 with a share of 33.9% in the total world exports. In the case of imports, China

13

was the largest importer of integrated circuits and electronic components in the year 2009, with a share of 32.8% in the total world imports.

It is reported that the digitization of electronics has also been largely favouring the development of Chinese electronics industry. Also, the convergence of electronic applications, technologies and products favour the development of wide range of portfolios by the Chinese electronic conglomerates. While sourcing critical components from abroad, Chinese electronic industry developed its manufacturing output through partnership with international players and outsourcing services, mainly through assembly work. The technology transfer has also been benefiting the Chinese electronics industry in achieving self-sufficiency, by developing home-grown standards for mass market digital products. Component manufacturing in China is also developing fast to provide a comprehensive supply chain, and support the growth in local production.

SINGAPORE’S ELECTRONIC INDUSTRY

Singapore’s electronics industry has been an important pillar of the country’s economy over the last 40 years. It is also a key demand driver for the chemicals, logistics and precision engineering industries, as

well as an important capability enabler for various sectors like avionics, medical technology and clean energy. The investment projects in 2009 are expected to contribute SGD 1.8 billion in variable account per annum to Singapore’s Gross Domestic Product (GDP) when they are fully implemented. This is generated by electronics investment commitments, of SGD 4.9 billion, in manufacturing FAI (Fixed Asset Investment) in 2009, or 41.5 per cent of total manufacturing FAI.

Singapore has become a world-class electronics manufacturing hub with end-to-end R&D capabilities. Presently, the industry is made up of various important strands. The biggest area is in semiconductors, which consists of integrated circuit (IC) design, wafer fabrication, and assembly and test activities. The sector employs around 3,500 R&D engineers working on IC design, process development, packaging and test engineering and embedded software development.

During 2009, exports and imports of electronic goods had declined due to the economic slowdown. Singapore was one of the major exporters as also importers of office and telecom equipment in the world. Singapore was the largest exporter of integrated circuits and electronic components in the year 2009, with a share of 62% in the total world exports.

14

EDB (Economic Development Board of Singapore, Government of Singapore) has identified four growth areas for this industry – green electronics, bioelectronics, plastic electronics and security products. Currently, these smart products contribute about 10% of the country’s electronics output, which is expected to increase to 30% by 2020. Green electronics refer to energy efficient solutions for applications such as lighting, automotive and computing. Another novel method of reducing reliance on traditional sources of energy is through energy harvesting. Such IC designs are able to capture and convert ambient energy into electricity. Improving healthcare remains a top priority, and developing bioelectronics will be beneficial for all. Singapore is ready to propel this new growth segment forward with its base of core electronics capabilities and existing strengths in material physics and biotechnology.

HONG KONG’S ELECTRONICS INDUSTRY

As of 2007, the Hong Kong’s electronic Industry comprises about 500 establishments engaging nearly 10,000 persons with a gross output of nearly HK$ 8 billion. Electronic industry in the year 2007 accounted for 4% of total establishments in the manufacturing sector; about 6% in the total employment in the manufacturing sector; about 5% in the value of gross

manufacturing output; and about 7% share in manufacturing value added.The electronics industry has been seen as a medium for developing globally competitive niches in newly developing markets; thus, Hong Kong Government has clearly outlined explicit objectives and industry policies to encourage research, design and manufacturing in electronics industry. There has been rapid increase in major investments by the Hong Kong Government on infrastructural development to support the emergence of new businesses. Institutions such as Hong Kong Industrial Technology Center (HKITC), Hong Kong’s Applied Research Council and other special research facilities have been set up to support the growth of electronics industry. Direct investment in manufacturing was left to the private sector.

Hong Kong’s electronic industry is one of the largest merchandise export earners, and is one of the largest exporters of calculators, radios, telephone sets, sound recording apparatus (including DVD/VCD recorders / players) in the world.

One-fourth of Hong Kong’s electronics exports comprise of finished goods, majority of them being durable products for domestic consumption. Audio-visual (AV) equipment, consisting of radios and optical discs players, hi-fi equipment, TV sets, video cassette recorders,

15

digital versatile disc (DVD) players/recorders, and MP3 players are some of the major finished products. Moreover, Hong Kong exports a variety of computer products too, such as desk-top/notebook computers and magnetic and optical disk drives, as well as telecommunications products like corded and cordless telephones. Other items with smaller export value include calculators, electronic dictionaries and translators, batteries and personal security/smoke alarms.

Electronic parts and components constitute about three-fourth of Hong Kong’s electronics exports. In particular, a large amount of semi-conductors are re-exported to China for further production. Hong Kong also produces and exports a variety of parts for telecommunications items, AV equipments, office machines and computers, as well as components like resistors, capacitors, inductors, crystals, resonators, speakers, switches, buzzers, liquid crystal displays (LCDs), printed circuit boards (PCBs) and transformers. Hong Kong also re-exports a large volume of semiconductors to China for outward processing production.

The success of Hong Kong’s electronics industry also lies in efficient management. Against the fast changing markets, Hong Kong companies emphasize quick response to ensure effective marketing services to their customers, and to monitor the

changing product trends. Moreover, due to the growing concern of quality conscious buyers, more and more companies have strengthened their quality assurance systems. This is evidenced by a growing number of Hong Kong companies accredited with ISO 9000 - an internationally recognized standard for quality management system, and ISO 14000 - a standard for environmental management system, amid the growing concerns for environmental protection.

Of late, most electronic manufacturers in Hong Kong have relocated the labor-intensive production processes to China, while, their Hong Kong offices are mainly responsible for product development, quality control, management, marketing and logistic support. Due to the relocation of production facilities, most companies have been re-classified as non-manufacturing establishments, despite the fact that they have manufacturing activities across the boundary. However, there are a number of companies still maintaining the high value-added and/or capital-intensive production in Hong Kong, e.g. IC packaging/testing, production of multi-layer PCBs, lead-frame bonding and PCB assembly by surface mount technology (SMT) for high-value products.

There are also a number of large Hong Kong companies marketing

16

electronic products under their own brand names, including Truly, V-Tech, Group Sense, Venturer, GP and SMC. Their sales network covers not only the advanced countries, but also emerging economies like Latin America and Eastern Europe.

As for parts and components, many manufacturers produce custom-made products for famous global companies, e.g. parts and accessories of computers, recorders, and radio receivers, as well as components/modules like PCBs and LCDs. Meanwhile, standard components are usually exported directly to distributors and manufacturers in overseas markets. Electronic parts and components from Japan, Taiwan, the US and South Korea are sometime assembled in Hong Kong and are then re-exported into the market. This can be seen in the rising number of multinational manufacturers setting up offices in Hong Kong.

JAPANESE ELECTRONIC INDUSTRY

Japan is the largest manufacturer of consumer electronics in the world. Japanese companies have a reputation for high quality and innovation, especially in audio and video segments.

Global production by Japanese electronics and IT companies is estimated to rise 11% in 2010, to

¥ 43.7 trillion. The trend of recovery is expected to continue in 2011, when production is forecast to increase 4%, to ¥ 45.5 trillion. Production by Japanese electronics and IT companies accounted for a significant share (21%) in the world production in 2010. Although Japanese companies are facing increasing competition worldwide, production is seen growing in line with the introduction of products taking advantage of environment-related and other technologies.

Domestic production by the Japanese electronics industry is estimated to increase 13% in 2010, to ¥ 15.3 trillion. Special demand was seen for flat-panel TVs and other products due to the Eco-Point System, and for automobiles due to Government support. This demand also contributed and increased the demand for electronic components and devices. Progress will continue towards the establishment of global production structures. In this environment, though domestic production is forecast to increase by 2%, to ¥ 15.7 trillion in 2011, this level is still 15% below that was achieved for the year 2008.

The exports of electronics from Japan increased by 17.8% during the period April-October 2010 compared to the corresponding period in the previous year. Electronics components and devices constituted a large share in the exports (77.7%) from Japan, followed by industrial electronics

17

equipment with 13.6% share, and consumer electronics equipment with 8.8% share in total exports from Japan. In the case of imports, during January – October 2010, imports increased by 27% to a value of ¥ 6.68 trillion. Constituting a share of 50.7%, electronic components and devices were the largest imported item, followed by industrial electronic equipments (37.8%) and consumer electronic equipments (11.5%).

SELECT GLOBAL TRENDS

Global electronic firms are increasingly using their core competency to expand their global consumer base. The firms are focusing on technology, product development and manufacturing capabilities through aggressive innovation. Innovation is also being used in development of new business models, business processes, and management of services. For example, Apple Inc. innovated a new business model from being a provider of innovative products to a provider of lifestyle product (Apple I-Pad). Introduction of this product changed the trends in delivery of contents.

Global electronic manufacturing firms are also moving their locations to take advantage of low-cost global talent, and manufacturing operations to increase operational efficiency.

Improvement in profitability is being undertaken through concentration on high-growth-low-competition areas, such as industrial / medical electronics and aerospace / defence electronics. Automotive electronics is another growth area which is having a small share in the electronic industry, and in order to revive the same, the Automotive Electronics Council has been commissioned by leading industry players.

Global firms are focusing on five major areas, viz.,

• Developing an understanding of both domestic and international customers for creating value propositions;

• Implementing new business models that help them in achieving the value propositions;

• Establishing the ability to shift the resources among diverse lines of business with exit and entry strategies;

• Making decisions efficiently and communicating to stakeholders; and,

• Attracting and retaining global talent at competitive price.

Electronic industry in many developed countries are facing challenges associated with human resources, as the

18

workforce is expected to come down drastically in the medium term. In such a situation, many electronic firms are dependent on global labour market place for their requirements. This may, however, call for managing the workforce by standardizing human capital data and sharing of knowledge. Such trends may pose challenges of globalizing and unifying the mindsets of employees. Systems and processes need to be established to deploy human resources based on global priorities. Firms are helping their employees to understand the need for customer focus and cultural integration.

Over the past few years, the electronics manufacturing services (EMS) industry has quickly diversified its list of value-added services for OEM (Original Equipment Manufacturers) customers. As a result, EMS firms are beefing up their logistics offerings as well, providing a variety of outbound shipping services to OEMs that do not build up inventory, and are aiming to transport high-tech products to customers, as fast as possible, by establishing organizations devoted to marketing and managing outbound, customer-facing functions.

New applications, or improvement in existing applications based on energy saving (home, transport, industry), good living/wellbeing (living place, para-medic and medical applications) and protection (personal security, tracking), are likely to be in demand in the years to come.

The analog-to-digital conversion has introduced many new standards in audio and video, which greatly improves the quality and affordability of the multimedia digital experience. Further, with the proliferation of broadband, accessing the media has become easy and rewarding for consumers.

The impact of recession on electronics goods industry was significant resulting in project cancellations, postponement, market opportunity review, or combining with other projects. The design, resources of people, capital and tools were reduced in many cases, and then kept in a frozen state. However, from around middle of 2009, situation has started improving and this has been enabled, first by low inventories, and next by robustness of select market segments. Still, the industry is holding a very cautious view of this recovery and deliberated if there could be further turbulence

19

ahead. Thus, the resource constraints on new product designs have continued to remain a challenge even though forward looking sales plans are turning more and more optimistic. The recovery in electronics industry is expected to fully bloom in 2 or 3 years, i.e. by 2012 or 2013. This presents a huge market potential which cannot be served with only the existing products, and there will be a glut of new designs. Thus, it is reasonable to expect that companies will place major emphasis on new product designs, starting from 2010, as the demand is projected to grow strongly.

The nature of new product demand in a post-recessionary phase is somewhat different from the demand that would be prevalent in a continuous growth period. While the latter is broad based, the former is likely to be very selective, as resource availability for investments, and R&D would be gradual and companies would like to make safer bets. In addition to being selective, companies would also like to look for product opportunities with shorter timeframes for return on investment, which would lead to new designs that are somewhat incremental in nature.

After being battered by the economic downturn, the electronics distribution industry is emerging with a more positive outlook and a new strategy. The industry is optimistic about the long-term outlook. Most of the manufacturers and distributors are planning to take a more customer-focused approach and are expected to furnish more services. Acquiring more customers, including OEMs and EMS firms, has become a major priority, as well as strengthening relationships with current ones. Additionally, distributors are expected to offer more supply chain management solutions and value-added services even to smaller customers, as they seek to establish themselves as the most capable product and service providers.

INDIAN SCENARIO

The start of Indian electronics industry could be traced to the sixties, when the Government took the initiatives of manufacturing space and defence electronic products. This was followed by developments in consumer electronics, mainly the manufacturing of transistor radios, black and white TVs, calculators and other audio products; later in 1980s, manufacture of colour televisions also started. Late 1980s, saw the advent of computers and telecom products.

20

Production

Indian electronics hardware production increased from ` 50,500 crore in 2004-05 to ` 97,260 crore in 2008-09, with a cumulative annual growth rate of 17.3%. The production of electronics hardware in the country is estimated to have grown from ̀ 97,260 crore in 2008-09 to ` 109,940 crore in 2009-10, a growth of 13%. The slower rate of growth of production during 2009-10 is attributed to the global economic slowdown.

Communication and broadcasting equipment took the largest share (29%) in India’s electronics production in the year 2009-10, followed by consumer electronics (27.4%), computers (13.1%), industrial electronics (12.4%), components (12.2%) and strategic electronics (6.3%).

The share of electronics production in India’s GDP has been growing over the years, with increasing importance of this sector. From a share of 1.6% in India’s GDP in 2001-02, the share has increased to 1.95% in 2009-10.

The demand for electronics hardware is being fuelled by the relatively high growth rate of the Indian economy, aspirations of the younger generation, and the large middle class population in India, with increasing disposable income. Thus, there is significant opportunity for stepping up production

of electronics hardware in the country. India has the potential to develop and manufacture electronic hardware for the global markets and gain higher global share besides meeting the country’s future requirement in the converging areas of information, communication and entertainment.

Consumer Electronics

Consumer electronics include electronic equipments meant for everyday use and are most often used in entertainment, communications, and to enhance office productivity. Some of the major products under consumer electronics include personal computers, telephones, MP3 players, audio equipments, televisions, calculators, GPS automated navigation systems, digital cameras and playback and recording of video media such as DVDs, VHSs or camcorders.

Indian consumer electronic market witnessed consistent increase in its market value over the years, from US $ 2.9 billion in 2004 to US $ 4.2 billion in 2008, witnessing a CAGR of 9.7%. Growth rate was the highest in 2006 (of 12.5%), and comparatively during 2008, the industry witnessed a slower growth of 7.7%. Datamonitor has projected that the Indian consumer electronics market is expected to witness a CAGR of 6.1% during the period 2009-2013.

21

Indian electronics industry has been picking up again after the slowdown in the world economy. Rebounding consumer sentiments, strong demand for consumer durables, and stimulus package, have played a significant role in reversing the slowdown that set in more than a year ago. During 2009-10, the production of consumer electronics sector is estimated to be ` 30,150 crore, as against the production level of ` 25,550 crore in 2008-09, registering a growth of about 18%. Within this sector, the colour television segment is the largest contributor.

Computers

The computer hardware market consists of the computers, storage, and other devices segments. The computers segment comprises: desktops and laptops. Storage segment includes memory sticks, CD packs, hard disks and other data storage devices. The other devices segment include: computer peripherals, PDAs, organizers, calculators and satellite navigation systems.

The growth of computer hardware market in India during 2008 was 15.6% over the year 2007. Indian computer hardware market witnessed impressive growth rates in its market value over the years, from US $ 2 billion in 2004 to US $ 3.7 billion in 2008, witnessing an impressive CAGR

of 16.6%. Growth rates witnessed an increasing trend from 15% in 2005 over 2004, to 18.5% in 2007 over 2006, and a moderate decline in 2008, of 15.6%, over 2007.

According to Datamonitor, the computer hardware market is projected to grow at a CAGR of 17% during the period 2009-2013. The market value of India’s computer hardware market is thus expected to be US $ 8.1 billion in 2013.

The overall production of the computer segment of the Indian electronics industry in 2009-10 is estimated to be valued at ` 14,430 crore, a growth rate of 7% over the previous year. The year 2003-04 witnessed the highest growth of 60% over the previous year, owing to increased demand for computers in India. However, during the year 2008-09, the production of computers witnessed a decline of (-) 15%, owing to the global slowdown that had engulfed the countries world over.

The total PC (Personal Computer) sales during 2009-10 was 8.03 million units, including desktop computers and notebooks (including netbooks); the value of sales is expected to have registered a growth of about 18.2% in 2009-10 over the year 2008-09. Out of the total PC sales, the total sale of desktops was 5.52 million units, and that of notebooks & netbooks at 2.51 million units. During 2010-11 the

22

total PC sales is estimated to be 9.76 million units, of which 6.20 million units included the desktop sales and the rest 3.56 million units included notebooks and netbooks sales. While desktop sales is expected to increase by 12.3% in 2010-11 over the previous year, that of notebooks & netbooks is expected to increase by (-) 41.8% over 2009-10. The overall consumption in the PC market was led by telecom, banking and financial service sectors, education and households segments.

The overall consumption in the computer market was led by businesses and households. Businesses included telecom, banking and financial services sectors and education. Over the years, the business sector has been dominating the computer industry sales. However, lately the share of households has also started increasing. From a share of 22% in 2003-04, in total PC sales, the households segment has increased its position with a share of 42% in 2009-10. Going forward, with signs of revival in the domestic economy, the industry is expected to show positive growth for PC and other IT products for the year 2010-11.

Industrial Electronics

The industrial electronics segment includes critical hardware technologies and systems with built-in software. It is a very challenging area

which is multidisciplinary in nature requiring high level of technical skill in designing systems for applications in a variety of industrial sectors of the economy. Even though India has been having significant expertise in conceptualizing such systems and its erection and commissioning, the sector is very largely dependent on import of critical hardware and associated software. Large projects are implemented with total import of C&I (commercial and industrial) packages from abroad without any knowledge of its design. In most cases, this leads to higher initial cost and a much higher maintenance cost in the long run.

Industrial electronics is a very high technology oriented area needing very high R&D investments. Therefore, there are limited numbers of global players as far as R&D is concerned. The leading suppliers of the industrial electronics and controls, operating in India include Siemens, Rockwell Automation (Allen-Bradley), Asea Brown Bovery, Schneider, L&T, Honeywell, Mitshubishi, Emerson etc. A number of small-scale units have also come up in the recent past owned by technocrats having expertise in integrated solutions for automation and control instrumentation and software.

During the year 2009-10, the production of industrial electronics is estimated to be ` 13,630 crore, as

23

against ` 12,740 crore in the fiscal year 2008- 09, registering a growth of about 7%. During 2008-09 also, this segment witnessed a growth of 7% in its production. However, it was much lesser than the growth witnessed in 2007-08 (of 14.5%) over 2006-07. The main reason for deceleration in production growth could be the overall slowdown in the world economy.

The Department of Information Technology, Government of India, through its Industrial Applications Programme is endeavouring to support this sector, particularly the SMEs, by providing proven indigenous technologies wherever possible. Several technologies developed through national collaborative programme have been applied for field demonstration. This includes energy related equipment for improvement of electric power quality, controllers in the area of automation systems, equipment for railway traction, etc. A large collaborative programme on Intelligent Transportation System, which includes various technology modules for application in the road transportation sector has also been launched by the Department of Information Technology.

This sub-sector continues to play a very important role towards the manufacturing value added and economic growth. State-of-art industrial electronics equipment and systems, automation technologies,

networking systems and various other stand-alone instrumentations are increasingly applied in manufacturing processes like steel, textiles, cement, power, chemical and refineries. Transportation sector, particularly the Indian Railways, are increasingly adopting latest electronic equipments for their locomotive and signaling systems.

Communication and Broadcasting Sector

Telecommunications is one of the few sectors in India, which has witnessed the most fundamental, structural and institutional reforms since 1991. In recent times, India has emerged as one of the fastest growing telecom markets in the world. The communication technology has taken a big leap forward and received the national recognition as the key driver for development and growth.

The telecom services have been recognized the world-over as an important tool for socioeconomic development of a nation. Telecommunication is one of the prime support services needed for rapid growth and modernization of various sectors of the economy. It has become especially important in recent years because of enormous growth of information technology and its significant potential for the impact on the rest of the economy. The telecom sector, which has the multiplier effect

24

on the economy, has a vital role to play, by way of contributing to the growth in efficiency.

The overall telephone connections stood at 621.28 million at the end of the financial year 2009-10. Out of this, the share of wireless subscribers stood at 584.32 million as compared to 391.76 million in 2008-09, witnessing a growth of 192.56 million connections or a share of 49.15%. The rural subscribers reached 190.88 million, as compared to the level of 111.63 million in the 2008-09, excluding CDMA, which works out to a growth of about 71% over 2008-09. It was reported that 32.67% of total wireless subscribers are now in rural areas. The total number of wireline connections was 36.96 million, while in the rural areas it stood at 9.93 million.

The gross telephone subscribers in the country crossed 764.76 million at the end of November 2010 (of which wireless telephone subscribers are about 729.57 million). The overall tele-density reached 64.34% in November 2010. With such subscriber base, India is now second largest telecom market in Asia (next to China), having second largest mobile subscriber base in the world. At the end of November 2010, total broadband connections in the country have reached 10.71 million. In the broadcasting sector, apart from All India Radio, there are around 250 FM Radio stations in operation.

India has currently achieved a distinction of having the world’s lowest call rates (1-2 US cents), the fastest sales of mobile phones, production of world’s cheapest mobile handset, and the fastest growth in number of wireless phone subscribers (about 14 million per month).

The data collated by the Department of Telecom, Government of India shows that production of telecom equipment in India during 2009-10 stood at ` 510 billion, witnessing a growth of 4.5% over 2008-09.During 2010-11, telecom equipment production is estimated to grow by 5% to reach ` 535 billion.

India exported equipment worth ` 135 billion in 2009-10 as against ` 19 billion in 2006-07, a growth of 600%, underlining the growth potential of the sector. The pace of growth in manufacturing would accelerate over next 3 years considering the growth of subscribers. According to Department of Information Technology, telecom equipments worth ` 3500 billion to ` 5000 billion would be required in India by 2015.

Indian telecommunication sector has a lot of growth potential; however, India needs to focus on upgrading technology and services, which requires R&D investments. R&D is very important in telecom sector because it has the potential of bringing immense value to the

25

country. In India, R&D spending in telecom sector is expected to grow due to 3G, 4G/WiMax, LTE deployments all over the world, which would boost equipment and telecom devices demand. According to telecom regulatory authority of India, it is estimated that for 3G alone the investment would be of the order of US $ 15 billion, and demand for network elements would translate into requirement for components, test and auxiliary equipments. The overall investment requirement is expected to be of the order of US $ 100 billion. Major objective and focus should be on undertaking advance research, developing world class human resources, and establishing effective academia-industry interface. Apart from this, Indian telecom sector should also focus on promoting international cooperation with leading institutions, organizations and countries in the world.

Strategic Electronics

Strategic electronics has become one of the important areas in the electronic industry due to the criticality of the technology development targeting two aspects, viz., a) the technology applicable to the strategic sector, like defence purposes; and b) the emerging state-of-the-art technology in the civilian applications. The strategic electronic sector envelops satellite based communication, navigation and surveillance systems,

radars, navigational aids, sonars, underwater electronic system, infra-red based detection and ranging system, disaster management system, internal security system, etc. The Indian strategic electronic industry has been able to meet the bulk of the requirements of India’s defence and paramilitary forces.

There has been consistent growth in production of strategic electronics. In the year 2008-09, production of strategic electronics in India was valued at ` 6,840 crore, a growth of 20% over the previous year. The production data for the year 2009-10 is estimated to be ` 6,980 crore, registering a marginal growth of about 2%. However, this is much lower than the growth rate witnessed in 2008-09 over 2007-08. This was mainly because of reduced military spending in some sectors and the troubled global economy. At the national level, various research institutions are developing strategic systems, and the public sector undertakings and some of the private agencies are mainly contributing to the growth in production.

It is expected that military and aerospace semiconductors are expected to witness growth in the coming years, as suppliers are likely to be looking forward for the end-product growth coming to the market over the next few years. This growth is due to technological advances

26

which are driving the demand due to changes in national military policies, and as a result of the substantial backlog of undelivered orders in aerospace. Prior to the era of computers and consumer electronics, military electronics consumed almost all of the world’s semiconductors. Although the market share of military electronics in the consumption of semiconductors has been reduced, semiconductors nonetheless perform critical roles in the military electronics segment.

In the overall industrial market, which includes military and aerospace applications, more designs are being used in digital signal processing, sensors, analog circuitry for automation, measurement, security, and other growing areas. While volumes of shipment in the end-equipments are lower and growth is limited, the increasing electronics content, requiring semiconductors, is driving an average growth of 5% per year for military / aero chips. The forecast for military and aerospace semiconductors shows that the year 2010 would be a growth year for this market, with revenue likely to approach US $ 2.6 billion.

Components

The growth in production of components industry has been driven mainly by growth in consumer electronics and mobile sector. This

sector faced serious challenges, with regard to growth and competitiveness, due to historical reasons, as well as the business environment prevailed in the year 2009. Historically, Indian electronics components sector had not kept pace with the rest of the world, and was saddled with out-dated technology, low volumes and high costs, making it globally uncompe-titive. However, the technological gap has been narrowing down.

The total production of electronic components was valued at ` 13,360 crore in the year 2009-10, a growth of 11% over the previous year. Electronic components with major share in production include: CD-R, Colour Picture Tubes (CPT), PCBs, DVD-R, connectors, semiconductor devices, ferrites, and resistors. It is estimated that the serviceable market for professional grade components such as PCBs, semiconductor devices, connectors, wound components, antennas, are likely to go up due to indigenous manufacture of electronic products, such as mobile phones, set top boxes, DVD players. Most of the top global semiconductor companies have set up their chip design centres in India. There is a major shift in 21 inch CTVs – from conventional CPTs (Colour Picture Tube) to Flat Screens. With decline in global demand for CRT (Cathode Ray Tube) TVs, India will be the largest user of this CRT (Cathode Ray Tube) technology in the next few years with demand spreading to rural

27

areas. India is also likely to become the global hub for manufacture of CRT (Cathode Ray Tube) TVs.

After the ITA- 1 (Information Technology Agreement) was implemented, most of the components are placed at zero customs duty, and the remaining will be converging soon to zero duty structure under the FTAs. Convergence of technologies have further resulted in functional changes - the functions that were performed by consumer electronics equipments till now, are being performed by telecom and IT products, eliminating the little difference that remained between components used in these different segments of equipments. Thus, practically all components today can be imported at zero customs duty.

An interesting phenomenon about Indian electronic component industry is that while it is relatively competitive in global markets, its competitive position is relatively weak in the domestic market, when compared to imports, especially from China and other Asian countries. Such imports are largely by assemblers in unorganized sector, who flood their products in the grey market, hurting the revenues of organized sector.

India has been relatively a strong player in the picture tube segment with large manufacturing facilities and new technologies. Other products / segments in which India is considered

to be relatively strong include: PCBs, connectors, passive components and other electromechanical components, such as relays, switches, contactors, fuses, etc. Manufacturers of these products range from large MNCs, who are focused on local as well as global markets, and medium as well as small scale Indian companies. Investments in these products, though widespread, are smaller compared to semiconductor manufacturing, and thus India has some strong players who have expertise and have been in business for long.

Exports and Imports

India has been largely an importer of electronic goods rather than an exporter of the same. Electronic goods were one of the most important items of imports in India. However, India’s export of electronic goods has been growing over the years. The growth trend has been positive even in the year 2008-09, in which most of the sectors have witnessed slowdown in exports. During the year 2008-09, the exports of electronic goods were valued at US $ 6.8 billion, which constituted 3.7% of the total exports from India. The share of electronic goods exports from India in the total exports to the world, have more or less remained around 2% to 4% over the years. During 2009-10, India’s electronics exports were valued at US $ 5.48 billion, with a share of 3.1% in India’s total exports. During

28

this period, electronic exports have witnessed a negative growth of -19%, over the previous year. During April – September 2010-11, the exports of electronic goods were US $ 3469.95 million, witnessing a growth of 10% over the corresponding period in the previous year. Imports during the same period amounted to US $ 10,110.58 million, a decline of -5.4% over the corresponding period in the previous year.

In the year 2009-10, the imports of electronic goods were valued at US $ 20.96 billion, a negative growth of (-) 9.2% over the previous year. During April-September 2010-11 the imports of electronic goods were valued at US $ 10.11 billion, a decline of 5.4% over the corresponding period in the previous year. Major export destinations for Indian electronic goods include USA (14.8%), Singapore (8.2%), UAE (8.2%), Germany (6.7%), Hong Kong (5.8%), and Netherlands (4.9%). In the case of imports too, Asian countries (74%) were the largest import sources for India, in the year 2009-10, followed by European Union (13%), America (8%) and Middle East (2%).

CHALLENGES AND STRATEGIES

CHALLENGES

Small Size / Scale of Operations

The size and scale of operation of majority of electronic manufacturing

units in India are small compared to global standards. This leads to non-operation of economies of scale in terms of cost disadvantage in production (low capacity translates into higher per unit cost), as well as catering limited ability to adhere to supply commitments. Non-operation of economies of scale offset the overall advantage of low-cost labour imanufacturing. The skewed tax structure in favour of small scale units had encouraged establishment of more small scale units in various locations across the country.

Low Level of Component Base

The Indian electronics components industry is restricted to passive components. Even here, relatively larger presence is only in few sectors. The low domestic volumes and import / customs procedures and regulations do not encourage stock and trade of components. In the case of mechanical parts, suppliers do exist with technical capability. However, the industry has not positioned itself to cater to the needs of high-volume customers and would need substantial up-gradation of management skills. Also, to cater to the emerging needs of semi-conductors industry, in all areas of manufacturing, including the Government sectors such as defence, space etc., it is essential that this area be given a major thrust under government policies.

29

Challenges Associated with Supply Chain and Logistics Management

While inadequate (roads, ports) and high cost of infrastructure (power) hinders the competitiveness of the Indian electronic industry in international market, the challenges of supply chain management and logistics solutions, which are essential for timely delivery of electronic products, are also affecting the competitive landscape of Indian electronics industry. While significant progress has been made in improving the Turn-Around-Time (TAT) for delivering products via road, it is yet to be streamlined to the international levels of 15-20 minutes as compared to a day or two in India.

Challenge of Shorter Product Life Cycle

New technologies, changing standards and shorter product life cycles constantly challenge the manufacturers of electronic goods. This challenge is also extended upto the vendors of capital equipment and machinery that are used in producing electronic goods. The vendors have to match short product cycles through quick response to changing technologies by producing equipments that will cater to production of new generation products. For example, communication equipments manufacturers are scrambling to bring to the market with products

embracing new technologies such as wireless Internet. Consequently, they bring to the market initial versions of products while revised versions are still under design. Test equipments vendors following this market are also forced to provide test equipments that can be easily upgraded in the future to accommodate revisions in specifications. Sometimes, the equipments need to be designed to accommodate the addition of emerging technologies. All these call for a high level of open systems design, modularity and flexibility in hardware and software architecture.

Low Level of Technology Absorption

The low volume of production implies that any capital equipment with a given technology used by an Indian company is not optimally utilized; while its physical life lasts for a longer time, technologically they become obsolete in a short span of time, calling for modernization and upgradation. Yet, most of the Indian companies prefer not to go for new technology / capital equipments as they are costly proposition in view of sub-optimal utilization of capital equipments.

Limited Facilities for Standards and Testing

In electronic hardware segment, technology is changing rapidly. Most of the countries in the world have laid

30

down standards for new products to ensure that low quality products are not dumped into the country. India has limited standard and testing facilities in the country and also have limited number of well-equipped labs (such as Electronic Regional Test Laboratories, and Society for Applied Microwave Electronics Engineering and Research). Electronic equipments need to perform properly at all times, and especially under adverse conditions, emergencies, or disasters. Achieving compliance to certification requirements will turn out to be difficult without adequate number of testing and standards facilities. Setting up of modern testing labs will help electronic product designers and manufacturers in achieving their compliance requirements as quickly and efficiently as possible.

Grey Market

Unlike black market goods, grey-market goods are not usually illegal. Instead, they are sold outside normal distribution channels by companies which may have no relationship with the producer of the goods. Frequently this form of parallel market occurs when the price of an item is significantly higher in one country than another. This situation is commonly prevalent with consumer electronic items. Traders buy the products where they are available at low cost, often at retail, but sometimes at wholesale, and sell at a price high

enough to provide a profit but below the normal market price. Because of the nature of grey markets, it is difficult to track the precise volume of grey-market sales. Grey-market goods are often new, but some grey market goods are used goods. A market in used goods is sometimes nicknamed a Green Market. According to industry estimates, the worst affected segments are premium watches, gaming consoles and digital cameras. As per some estimates, the grey market for premium watches is almost 50% of the total sales. While the grey market accounts for 30% of the gaming console market in India, it is 25% in the digital camera market.

Managing E-waste

As the demand for electronic goods is increasing, so is the challenge of managing the E-waste. E-waste means electronic goods that are no longer in use or may not be re-usable, including computers, home appliances, clocks and watches, electronic toys, medical devices and industrial equipments. According to some estimates, Mumbai tops the list of cities with around 12,000 tonnes of E-wastes, followed by Delhi (around 10,000 tonnes), Bangalore, Chennai, Kolkata and Ahmedabad (around 4,000 tonnes each). Though the challenge of managing E-waste in India is at a nascent stage, this may turn out to be a serious challenge at a later stage.

31

Low R&D Intensity

India is heavily dependent on imports of electronic goods, from countries like the U.S. and China, to meet its domestic demand. Lesser spending on research and development by electronics industry has increased India’s dependence on electronics imports which has been growing over the years. India has very low share in the total expenditure on R&D compared to other countries. While India’s share on R&D expenditure was 0.88% of GDP, China held a share of 1.44%. Israel was the country with the largest share in R&D expenditure with a share of 4.86%. The R&D intensity of electronic industry was 0.73% during 2009-10.

Low Penetration of Distribution Network

Due to the inadequate world-class infrastructure facilities in India, distribution of electronic goods across the country poses a great challenge. High cost of moving goods and inefficient storage adds to the problem. Not so well-developed distribution networks make the distribution challenging to penetrate the fastest growing rural areas economically. In addition, regular power cuts and poor road linkages make systematic production, assembly and delivery a challenging proposition. India also has limited availability of proper

storage and warehousing facilities in the rural parts of the country.

Shortage of Skilled Labour

The Indian electronics industry is undergoing a lot of changes with the advent of new technologies, new product standards and new emission norms. India has shortage in skilled labour in the electronics industry. Not enough industry-ready trained personnel are available. The talent pool is also concentrated in a few metros, and attracting such talent to Tier II cities and small towns is a difficult task. High attrition rate, due to the small pool of talent available, is another challenge faced by the industry. As the industry readies for a major growth in the future, it is imperative for the players, as also the policy makers to look at developing skills to meet the increasing demand.

Low Value Addition

Indian electronic industry faces the challenge of low value addition. Usage of electronics is pervasive in many other sectors as well, like automobile, aviation, etc. As the domestic electronic industry is not having a strong manufacturing base, most equipments are imported with hardly any value addition being done in India. R&D plays a very important role for value addition in the country. However in India R&D intensity is very low.

32

Complying with Environmental and Social Standards

Most Indian electronics goods are considered as relatively inferior in global markets. Limited awareness about environmental and social standards and the cost involved in obtaining the globally recognized certifications are the major reasons for limited number of manufacturers adhering to such standards.

STRATEGIES

Rapid Customer Response

To keep a step ahead of the competition, companies know that they must satisfy their customers’ changing demands - whether their customers are end-users or other industry suppliers. This means maintaining a customer-focused, forward-looking business strategy and keeping abreast of new standards and new technology developments. The solutions should address the complete range of requirements for organizations that are focused on ensuring quality of service (QoS)-starting from research and development (R&D) organizations to manufacturing, engineering, operations, information technology, and sales and marketing fields.

Adherence to Quality

Quality is a driving factor in the electronics goods industry - starting from end-user service providers all the way back to the development laboratories of the equipment manufacturers. Enterprises can gain competitive advantage only through offering unique products and services. Efforts should be made to concentrate not only on research and development but also in the adaptation of already existing technology to build distinctive technical competence and develop superior products and services.

Effective E-waste management

According to a Report by Centre for Environmental Studies, the best option for dealing with E-wastes is to reduce the volume of E-waste. Designers should ensure that the product is built for re-use, repair and/or upgradeability. Stress should be laid on use of less toxic, easily recoverable and recyclable materials, which can be taken back for refurbishment, remanufacturing, disassembly and reuse. Recycling and reuse of material are the next level of potential options to reduce E-waste. Recovery of metals, plastic, glass and other materials reduce the magnitude of E-waste. These options have a potential to conserve the energy, and keep the environment free of toxic material that would otherwise have been released.

33

Also suggestions were given on salvaging and combining usable parts which could be salvaged with other used equipment to create a working unit. It is labor-intensive to remove, inspect and test components and then reassemble them into complete working machines. Institutional infrastructures, including E-waste collection, transportation, treatment, storage, recovery and disposal, need to be established, at national and/or regional levels for the environmentally sound management of E-wastes. These facilities should be approved by the regulatory authorities, and if required, to be provided with appropriate incentives. Establishment of E-waste collection, exchange and recycling centers should be encouraged in partnership with governments, NGOs and manufacturers.

Ministry of Environment and Forests, Government of India has announced E-waste (Management and Handling) Rules 2010 for handling of E-waste by defining the responsibilities of stakeholders such as producers, dealers and recyclers among others. According to the E-waste (Management and Handling) Rules 2010, the producer of electronic goods, including household appliances, computers, toys and medical equipments shall be liable for collecting any E-waste generated while manufacturing, and will have to channelize it for recycling. In fact,

the producers’ responsibility will go beyond the boundaries of the manufacturing unit. They will set up collection centres for E-waste generated from `end of life’ of their products in line with the principle of `extended producer responsibility’ and ensure that such E-waste is channelized to a registered refurbisher. They shall also finance and organize a system to meet the costs involved in handling the E-waste. The rules moot a unique serial number or individual identification code for product tracking in the E-waste management system. Dealers have to make provision for collecting used appliances. Besides registering themselves with the respective State Pollution Control Boards, they will have to submit details of the collected waste annually. Even the consumers are expected to do their bit by ensuring that the electronic equipment, not fit for use, is deposited with the dealer or authorized collection centre.

Emphasizing the reduction in use of hazardous substances (RoHS) in the manufacture of electrical and electronic equipment over a three-year period, the Rules state that producers are expected to adhere to the prescribed minimum threshold limits to using such substances. Further, the import of used electrical and electronic equipment for charity shall not be allowed in the country, the Rules state. Further, the stakeholders shall be liable for any damage caused

34

to the environment or human health including third parties due to improper handling and disposal of E-waste. They shall inform the authorities of such damage and undertake to reinstate or restore the damage at their cost, failing which they shall be liable to pay the entire cost of remediation or restoration of the environment. Even the consumers shall be liable to deposit the E-waste with an authorised dealer or collection centre, failing which they shall be liable to pay a fine as specified for violation of the provision.

It may be mentioned that EU has already issued two directives, in 2006, one on Restriction of Hazardous Substances (ROHS), and the other one on Waste Electronics and Electrical Equipment (WEEE). The WEEE aims at management of electronics waste, especially the reuse, recycling and other forms of recovery of such wastes so as to reduce the disposal of waste. The Directive also seeks to improve the environmental performance of all operators involved in the life-cycle of electrical and electronic equipments, including the operators directly involved in treatment of electronics waste.

Establishing ‘National Electronics Mission’

A high-level Task Force for the Information Technology (IT) industry has recommended constitution of

‘National Electronic Mission’, a nodal agency for the electronics industry under the Department of Information Technology, Government of India, with direct interface to the Prime Minister’s Office (PMO). The Task Force has said that this nodal agency would help in the synchronized functioning of the industry through effective coordination across various ministries and Government departments. The main functions of the nodal agency would be to attract investments into India, promotion of Brand India, facilitating business in India, managing R&D fund and manufacturing of value added products. Some of the other recommendations which were given by the Task Force include: building of adequate basic, business and social infrastructure; favourable business policy and regulatory environment; fostering a sustainable ecosystem for innovation, R&D and manufacturing; and maintaining globally competitive tax regime.

Research & Development

India is heavily dependent on imports of electronic goods from countries like the U.S. and China to meet its domestic demand. Lesser spending on research and development by electronics industry has increased India’s dependence on electronics imports, which have been growing over the years. Hence, it is important to strengthen and develop the Research and Development programmes in the electronics industry. This will help in

35

improving the domestic electronic industry and will also promote the ‘Brand India’ products. Also through regressive research, India would be able to reduce its import dependency of electronic goods from other countries.

India has very low share in the total expenditure on R&D compared to other countries. While India’s share on R&D expenditure was 0.88% of GDP, China held a share of 1.44%. Israel was the country with the largest share of R&D in national GDP at 4.86%. The R&D intensity of electronic industry was 0.73% during 2009-10.

According to the Task Force on information technology industry, India should also focus on new and emerging areas that are likely to grow in importance over the next few decades. Some of the opportunities analyzed by the Task Force are in the areas such as: climate change and energy efficiency solutions, mobile software applications, and end to end clinical research applications.

Department of Information Technology, Government of India, has constituted a specialized group - R&D in Electronics - to conduct sponsored R&D activities across India at various academic institutions of higher learning and R&D laboratories, in the areas assigned to it through a variety of Plan programmes. The sophisticated projects assigned to the groups cover

key technological areas, such as developments in Nanotechnology, Medical Electronics, Microelectronics and Industrial Electronics. The major R&D initiatives of the Group has been in the development of Linac tubes, Automation and Intelligent Transportation Systems (ITS) technology, setting up of Nanoelectronics centers and Generic Nanometrology facilities. The industry should also focus on more R&D related activities.

Thrust to Semi-conductor Industry

India has an edge in semiconductor design, embedded systems and has the potential of becoming an engineering design house for the world. Combining with its software strength, Indian embedded technology is globally acclaimed and accredited. With increasing demand for domestic electronic goods and the availability of a pool of talented engineers, India is fast creating a footprint on the semiconductor roadmap. The Indian semiconductor industry is currently dominated by players engaged in chip designing activities.

As the semiconductor industry is going through the transition phase to newer technologies, semiconductor manufacturing and IC (integrated circuit) design are becoming increasingly interdependent as neither activity can be carried out without in-depth knowledge of the other. Coupled

36

with this is the fact that embedded software forms a significant part in the design of today’s System-on-Chips, where India is already seen as a leader.

India has to complement design and R&D expertise with local manufacturing, which would help in increasing the value addition. Global demand for semiconductors is growing, and therefore, if India can integrate its chip design services with fabrication facilities, it can result in growth of competitive manufacture of electronic products and thereby help achieve success in the domestic as well as global markets.

Developing and Improving ICT Interface in India

According to Telecom Regulatory Authority of India during 2009-10, the broadband subscriber base increased from 6.22 million to 8.77 million and the internet subscriber’s base increased from 13.54 million to 16.18 million over the previous year. The gross usage of Internet Telephony was 122.96 million minutes in 2009-10.

It may be mentioned that Information and Communication Technology (ICT) is changing the face of the contemporary world. The ICT has not only connected the world at one

single platform, but it is also helping the integration of various traditional societies into modern societies. Information and communication technology plays a very important role in the development of an economy especially because it addresses the problem of digital divide. More importantly, ICT enabled solutions can overcome the difficulties that hamper traditional solutions.

ICT enabled services are very important in all the major sectors of the economy such as manufacturing, education, healthcare, financial services and public services. ICT helps manufacturing sector because it has the potential to contribute towards income generation and poverty reduction. It enables countries to capture economic opportunities by increasing process efficiencies, promoting participation in expanded economic networks and generating opportunities for job creation. Development of ICT infrastructure and connectivity are one of the main indicators that investors look for as an indication of technological development in a country. Enhanced ICT interface helps the manufacturing companies fit seamlessly into value chain of multi-national corporations easier. Hence it is very essential to have ICT interface in the manufacturing sector. This would also enhance the demand for electronics products.

37

Brand Building Initiatives

More efforts should be taken by the manufacturers and sellers of electronic products in the country, to build ‘Made in India’ brand. Currently, in the global electronic industry, Indian products have limited level of competitive brand perception. Marketers see a brand as an implied promise with desired level of quality expected of from a product, which will enable them to continue with future purchases of the same product. This may increase sales by making a comparison with competing products more favorable.

Brand development is more important these days because customers have started becoming more conscious of the products they buy, and they are expecting products with good quality and standards. The advantage of branded products is the assurity that the quality will be good. Hence, Indian electronic firms should increase their focus on brand development and management, as it will help to create desirability in international markets for products manufactured in India. Further, the firms may strengthen the ‘Incredible India’ branding campaign and run it regularly through key international media.

Developing Market Sustenance

In order to be ahead of the competition, it is necessary for the Indian electronic

industry to aggressively handle the market and adopt measures for market sustainability. The Indian electronic firms should be able to identify the changing consumer needs and the industry standards so that they are in a better position competitively. They should also concentrate on taking care of the customers with sensitivity, speed and responsiveness by establishing effective channels of distribution and reaching out to them. This would help in building relationships for long-term sustenance in international market.

Also, Indian electronic industry should concentrate more on providing new generation products that maybe in demand in future. For example, Nanotechnology, which is widely regarded as the next technological revolution, has attracted the attention of scientists, researchers and technologists all over the world and is likely to have a profound effect on almost all industry sectors and application areas in the coming years. Department of Information Technology, Government of India, has taken measures for promoting emerging areas of technology like RFID (Radio Frequency Identification), smart cards, ubiquitous computing, perception engineering, scientific computing, nanotechnology, digital preservation and M-Commerce initiative.

38

Cluster Development

Micro, small and medium enterprises (MSME) sector has been recognized as an engine of growth all over the world. The sector is characterized by low investment requirement, operational flexibility, location wise mobility, and import substitution. Over the years, the small scale sector in the electronic industry in India has progressed from the production of simple consumer goods to the manufacture of many sophisticated and precision products like electronics control systems, micro wave components, electro medical equipments, etc. The process of economic liberalization and market reforms have further exposed these enterprises to increasing levels of domestic and global competition. The formidable challenges so generated for them have led to a novel approach of cluster development for the sector. As a result, private and public sector institutions, both at the Central and State levels are increasingly undertaking cluster development initiatives.

The major advantages of a cluster are the availability of common opportunities, which help them in creating a conducive ground for the development of inter-firm cooperation to promote collective production, collective innovation and collective learning. One of the major disadvantages in India is the technological and infrastructural

challenges. Cluster approach will help in meeting these challenges by creating an atmosphere of common infrastructure, technology and opportunities. Also, all companies may not have all the necessary skills to develop unique products and services by themselves; therefore cluster approach would serve this purpose and would also become the sources for increasing income, jobs and export growth. Clusters arise because they increase the productivity with which companies can compete. The development and upgrading of clusters is an important agenda for governments, companies, and other institutions. Cluster development initiatives are an important new direction in economic policy, building on earlier efforts in macroeconomic stabilization, privatization, market opening, and reducing the costs of doing business.

Clustering of technology companies in an area is very beneficial to developing new industries in a country. Taiwan is an illustrative success story. Taiwan’s Hsinchu Science Park, spread over 600 hectares has clusters of most of the semiconductor component manufactures, thus saving on time and cost for assembly. This Park includes independent wafer foundries, IC design companies, fabricators, as well as packaging and testing companies for the semiconductor industry, all at one place. The model is now being replicated by China and Malaysia as

39

well. In such clusters, one can find trained people more easily and form inter-relationships between suppliers and vendors that make development of products faster, cheaper, and even lead to better innovations. Most countries have typically evolved clusters naturally over a time period. India should also follow such models for the better development of the electronics industry.

Improved Standards and Testing Facilities

In electronic hardware segment, technology is changing rapidly. Most of the countries in the world have laid down standards for new products to ensure that low quality products are not dumped into the country. In Taiwan the Industrial Technology Research Institute (ITRI) helps the electronics industry to expedite the development and upgrading of new industrial technology.

Also, in the growing electronic industry, there is a strong need to evolve/adopt EMC (Electromagnetic Compliance) standards that are acceptable worldwide in order to avoid trade barriers. Limited awareness of such standards and compliances led to sub-standard and spurious products being dumped into the market. Many countries are using standards as non tariff barriers in order to restrict the imports of products from non-complying firms / countries. Dumping

is also creating grey market and thus the local manufacturing industry would get affected. Therefore, there is an urgent need to have Indian standards matching with international standards for all Electronics / IT products, which should be mandated to be followed for manufacture, imports and exports. For global trading of Indian products, it is essential that these products not only meet international EMC (Electromagnetic Compliance) standards but are also complying with other such standards.

India should also follow Taiwan’s example and develop similar standards and testing facilities, so that Indian products have global acceptance. This would help the industry grow and would enhance the acceptability of Indian products not only in advanced countries but also in the fast emerging markets of third world countries. Efforts may also be required to enhance the awareness of EMI/EMC (Electromagnetic Interference/ Electromagnetic Compliance) aspects for both users as well as manufacturers. If EMC (Electromagnetic Compliance) implementation is taken care of at an early stage of design, the increase in cost will be marginal. Apart from this, there is also a strong need to evolve and harmonize occupational stand-ards against EM (Electromagnetic) radiation to ensure against the health hazards of the end users of electrical and electronic goods. In India, EMC

40

compliance certification scheme, is followed to ensure standards to the products that are manufactured, exported and imported.

Technology Development and Sourcing