experiments on risk taking and evaluation periods misread as evidence of myopic loss aversion ganna...

TRANSCRIPT

Experiments on Risk Experiments on Risk Taking and Evaluation Taking and Evaluation Periods Misread as Periods Misread as Evidence of Myopic Loss Evidence of Myopic Loss AversionAversion

Ganna Ganna PogrebnaPogrebna

June 30, 2007June 30, 2007

Blavatskyy, Pavlo and Ganna Pogrebna (2007) “Experiments Experiments on Risk Taking and Evaluation on Risk Taking and Evaluation Periods Misread as Evidence of Periods Misread as Evidence of Myopic Loss AversionMyopic Loss Aversion”

Presentation OverviewPresentation Overview

IntroductionIntroduction Experimental evidenceExperimental evidence

Gneezy and Potters (QJE, 1997)Gneezy and Potters (QJE, 1997) Haigh and List (JF, 2005)Haigh and List (JF, 2005) Langer and Weber (JEBO, 2005)Langer and Weber (JEBO, 2005) Bellemare et al. (EL, 2005)Bellemare et al. (EL, 2005)

Reexamination of experimental Reexamination of experimental resultsresults

DiscussionDiscussion Conclusion Conclusion

IntroductionIntroduction

Bernartzi and Thaler (1995) propose MLA as Bernartzi and Thaler (1995) propose MLA as an explanation for equity premium puzzlean explanation for equity premium puzzle

MLA combines two behavioral concepts:MLA combines two behavioral concepts: Loss aversionLoss aversion Mental accounting (how often evaluate financial Mental accounting (how often evaluate financial

outcomes)outcomes) MLA: MLA:

lotteries with positive EV and a possibility of a lotteries with positive EV and a possibility of a lossloss

If frequently evaluated – losses are more likely to If frequently evaluated – losses are more likely to be detected…be detected…

… … which averts loss averse investors which averts loss averse investors

Experimental EvidenceExperimental Evidence

Subjects choose how much of their Subjects choose how much of their endowment ($1-$4) to invest into a risky endowment ($1-$4) to invest into a risky lottery:lottery: If If xx invested, lottery yields – invested, lottery yields –xx with prob. 2/3 with prob. 2/3

and 2.5and 2.5xx with prob. 1/3 with prob. 1/3 Two treatments:Two treatments:

(H) make 9 investment decisions in 9 rounds(H) make 9 investment decisions in 9 rounds (L) make 3 investment decisions each (L) make 3 investment decisions each

binding for 3 consecutive rounds (only binding for 3 consecutive rounds (only cumulative earnings for three rounds are cumulative earnings for three rounds are observed)observed)

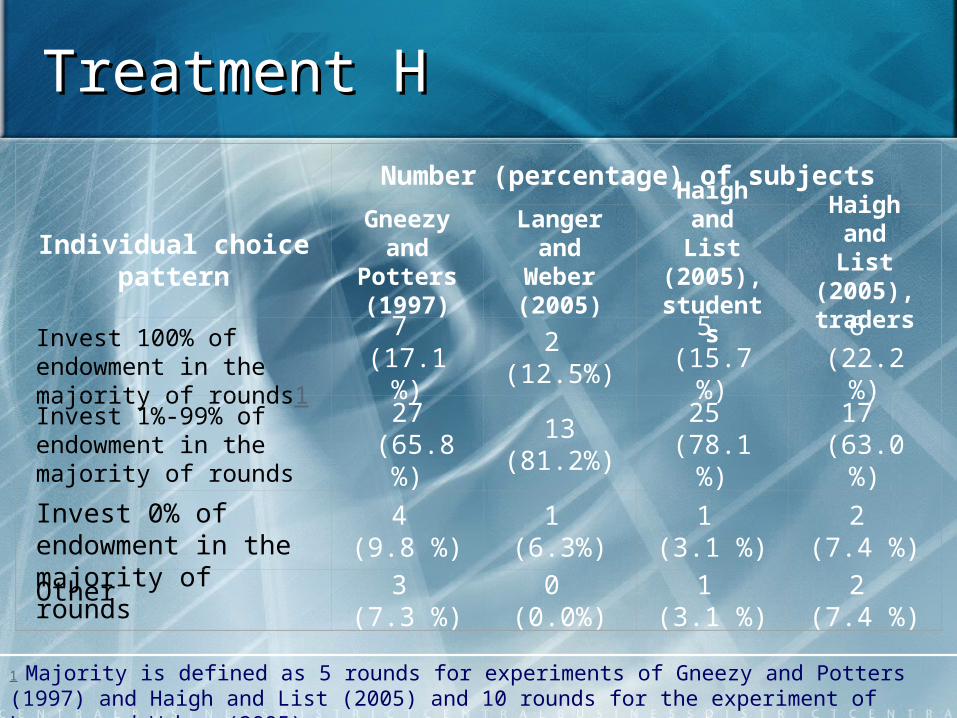

Treatment HTreatment H

Individual choice pattern

Number (percentage) of subjects

Gneezy and

Potters (1997)

Langer and

Weber (2005)

Haigh and List (2005),

students

Haigh and List (2005), traders

Invest 100% of endowment in the majority of rounds1

7 (17.1 %)

2 (12.5%)

5 (15.7 %)

6 (22.2 %)

Invest 1%-99% of endowment in the majority of rounds

27 (65.8 %)

13 (81.2%)

25 (78.1 %)

17 (63.0 %)

Invest 0% of endowment in the majority of rounds

4 (9.8 %)

1 (6.3%)

1 (3.1 %)

2 (7.4 %)

Other 3 (7.3 %)

0 (0.0%)

1 (3.1 %)

2 (7.4 %)

1 Majority is defined as 5 rounds for experiments of Gneezy and Potters (1997) and Haigh and List (2005) and 10 rounds for the experiment of Langer and Weber (2005).

Treatment LTreatment L

Individual choice pattern

Number (percentage) of subjects

Gneezy and

Potters (1997)

Langer and

Weber (2005)

Haigh and List (2005),

students

Haigh and List (2005), traders

Invest 100% of endowment in the majority of rounds 15

(35.7 %)3

(15.0%)6

(18.8 %)10

(37.0 %)

Invest 1%-99% of endowment in the majority of rounds

27 (64.3 %)

17(85.0%)

26 (81.2 %)

17 (63.0 %)

Invest 0% of endowment in the majority of rounds

0 (0.0 %)

0 (0.0%)

0 (0.0 %)

0 (0.0 %)

ObservationObservation

In the majority of rounds subjects invest In the majority of rounds subjects invest an intermediate fraction of their initial an intermediate fraction of their initial endowment.endowment.

Only a handful of subjects abstain from Only a handful of subjects abstain from betting. betting.

12%-22% (15%-37%) of subjects 12%-22% (15%-37%) of subjects consistently bet all their endowment on consistently bet all their endowment on the risky lottery in treatment H (L).the risky lottery in treatment H (L).

Let us now focus on subjects who Let us now focus on subjects who consistently bet an intermediate fraction consistently bet an intermediate fraction of their endowment on the risky lottery.of their endowment on the risky lottery.

Theoretical PredictionTheoretical Prediction

An individual betting amount x on the An individual betting amount x on the lottery in treatment H receives utilitylottery in treatment H receives utility

An individual betting amount x on the An individual betting amount x on the lottery in treatment H obtains utilitylottery in treatment H obtains utility

LetLet

andand

32315.2 wxwxxU H

278327145.72775.0427195.0 wxwxwxwxxU L

32

315.2

w

w

2783

27145.72775.0427195.0

w

www

Predicted Behavior in Predicted Behavior in Treatments H and L Treatments H and L According to MLAAccording to MLA

Index of loss aversion

Betting on the risky lottery in treatment H

everything anything nothing nothing nothing

Betting on the risky lottery in treatment L

everything everything everything anything nothing

Testable ImplicationsTestable Implications

A.A. % of subjects, who bet all their endowment % of subjects, who bet all their endowment on the risky lottery, is higher in treatment L on the risky lottery, is higher in treatment L than in treatment H; - than in treatment H; - confirmedconfirmed

B.B. % of subjects, who abstain from betting, is % of subjects, who abstain from betting, is higher in treatment H than in L; - higher in treatment H than in L; - confirmedconfirmed

C.C. % of subjects, who bet all their endowment % of subjects, who bet all their endowment in treatment L, is higher than the in treatment L, is higher than the percentage of subjects, who bet an percentage of subjects, who bet an intermediate fraction of endowment in intermediate fraction of endowment in treatment H; - treatment H; - violatedviolated

D.D. % of subjects, who bet nothing in treatment % of subjects, who bet nothing in treatment H, is higher than the percentage of subjects, H, is higher than the percentage of subjects, who bet an intermediate fraction of their who bet an intermediate fraction of their endowment in treatment L.endowment in treatment L. - - violatedviolated

InconsistencyInconsistency

The majority of subjects bet an intermediate The majority of subjects bet an intermediate fraction of their endowmentfraction of their endowment

The fraction of subjects who consistently The fraction of subjects who consistently bet an intermediate fraction of their bet an intermediate fraction of their endowment is nearly identical across two endowment is nearly identical across two treatmentstreatments

Between 65% and 85% across different Between 65% and 85% across different experimentsexperiments

Their intermediate bets are not significantly Their intermediate bets are not significantly different across two treatments (except for different across two treatments (except for the field experiment of Haigh and List the field experiment of Haigh and List (2005)). (2005)).

Inconsistency, Inconsistency, continuedcontinued MLA can explain this finding only if for the MLA can explain this finding only if for the

majority of subjects in both treatments. majority of subjects in both treatments. But for that we need to assume unconventional But for that we need to assume unconventional

parameterizations of cumulative prospect theory parameterizations of cumulative prospect theory

In contradiction with the existing experimental In contradiction with the existing experimental evidence (e.g. Tversky and Kahneman (1992), evidence (e.g. Tversky and Kahneman (1992), Abdellaoui (2000)). Abdellaoui (2000)).

Moreover in this case MLA cannot explain Moreover in this case MLA cannot explain implications A and B that apparently lead to implications A and B that apparently lead to statistically significant difference between statistically significant difference between aggregateaggregate choice patterns in treatments H and choice patterns in treatments H and L.L.

DiscussionDiscussion

Decreasing risk aversionDecreasing risk aversion Mixture modelMixture model Fechner model of random errorsFechner model of random errors Financial asset pricing modelFinancial asset pricing model

Fechner model of random Fechner model of random errorserrors

FMRE, continuedFMRE, continued

Fechner model suggests that an individual Fechner model suggests that an individual evaluates risky lotteries according to a evaluates risky lotteries according to a deterministic decision theory, but this deterministic decision theory, but this evaluation is affected by random errors. evaluation is affected by random errors.

The smaller the difference between two lotteries The smaller the difference between two lotteries in terms of utility, the more likely are random in terms of utility, the more likely are random errors to reverse deterministic preferences. errors to reverse deterministic preferences.

A simple model of expected value maximization A simple model of expected value maximization combined with a Fechner model of random combined with a Fechner model of random errors explains the experimental data. errors explains the experimental data.

FMRE, continuedFMRE, continued

Consider an individual who places bets in both Consider an individual who places bets in both treatments according to a simple algorithm. treatments according to a simple algorithm. Starting from status quo, she compares betting Starting from status quo, she compares betting zero versus betting a fraction of her zero versus betting a fraction of her endowment.endowment.

According to the Fechner model of random errors According to the Fechner model of random errors (e.g. Fechner (1860)) an individual prefers to (e.g. Fechner (1860)) an individual prefers to abstain from betting rather than to bet in abstain from betting rather than to bet in treatment H iftreatment H if

And in treatment L ifAnd in treatment L if

032315.20

0278327125.027642715.70

FMRE, continuedFMRE, continued

The chance of observing zero bet isThe chance of observing zero bet is H:H: L: L: Since for any positiveSince for any positive the likelihood that an individual abstains the likelihood that an individual abstains

from betting is higher in H than L.from betting is higher in H than L. probability that an individual bets 100% is probability that an individual bets 100% is

H: H:

and L:and L: an individual is more likely to invest 100% an individual is more likely to invest 100%

in L rather than in H.in L rather than in H.

616 prob

212 prob

62

16 12

FMRE, continuedFMRE, continued

Probability that an individual bets an Probability that an individual bets an intermediate fraction of her endowment isintermediate fraction of her endowment is

H:H: L:L: Which of these two probabilities is larger Which of these two probabilities is larger

depends on the additional assumptions depends on the additional assumptions about the step size and the function . about the step size and the function .

Chances of observing an intermediate bet Chances of observing an intermediate bet can be of a similar magnitude in both can be of a similar magnitude in both treatments.treatments.

166616...616

11

122

.

Financial asset pricing Financial asset pricing modelmodel

ConclusionConclusion

We reexamine the experimental evidence on We reexamine the experimental evidence on risk taking and evaluation periods.risk taking and evaluation periods.

Behavioral patterns of the majority of Behavioral patterns of the majority of subjects contradict to the MLA explanation:subjects contradict to the MLA explanation:

Subjects invest intermediate fractions of Subjects invest intermediate fractions of their endowmenttheir endowment

These intermediate bets do not appear to These intermediate bets do not appear to vary greatly across treatments with different vary greatly across treatments with different length of evaluation period. length of evaluation period.

Alternative explanationsAlternative explanations

Conclusion, continuedConclusion, continued

Experiments on risk taking and evaluation Experiments on risk taking and evaluation periods have been incorrectly interpreted as periods have been incorrectly interpreted as evidence of MLA. (critique of loss aversion evidence of MLA. (critique of loss aversion literature by Plott and Zeiler (2005, 2006)). literature by Plott and Zeiler (2005, 2006)).

The question of comparing expected utility The question of comparing expected utility theory and MLA approaches in the laboratory theory and MLA approaches in the laboratory remains unanswered. remains unanswered.

There is much work to be done in developing There is much work to be done in developing a model, which would allow to explain the a model, which would allow to explain the data on risk taking and evaluation periods. data on risk taking and evaluation periods.