exchange rates and exchange rate regimes international finance 130440-1165

TRANSCRIPT

Exchange rates and exchange rate regimes

International Finance 130440-1165

International Finance 130440-1165

Lecture outline

The notion of the exchange rate

Types of exchange rate regimes

Types of exchange rate

The equilibrium on the currency market

International Finance 130440-1165

Exchange rate

The price of one currency expressed in another

currency

Direct quotation – the price of the foreign

currency expressed in domestic currency

Indirect quotation the price of the domestic

currency expressed in foreign currency

International Finance 130440-1165

Types of ER regimes

Free floating/ Managed floating

Crawling band

Crawling peg

Fixed band

Fixed ER (hard peg)

Currency board

Monetary union

International Finance 130440-1165

Free floating

A currency’s ER may fluctuate free versus other currencies ER

A currency’s exchange rate is determined by the demand and

supply

Managed floating- central bank interventions

Examples

the majority of key currencies: EUR, USD, GBP, JPY, CHF

International Finance 130440-1165

Crawling band

The ER fluctuates within a band around a central

parity, the band is adjusted periodically at a

preset rate

Examples

CLP (Chile), COP (Columbia) , VEB (Venezuela)

International Finance 130440-1165

Fixed band system

The ER may fluctuate within a fixed band around

the central parity

Example:

ERM/ERM II- a system aimed at stabilizing the

ER of euro area candidate countries

International Finance 130440-1165

Crawling peg

The ER is fixed at a central parity, the parity is

periodically adjusted at a preset rate

Example:

RMB (China)

International Finance 130440-1165

Fixed ER (hard peg)

The ER is pegged to another currency, to a

basket of currencies or to another value e.g.

gold

Example:

RMB (China) till 2005 – currency pegged to

USD

International Finance 130440-1165

Currency board system

The ER is pegged to a foreign currency at a set and

fixed exchange rate

The domestic monetary base issuance is 100% backed

by reserves of the foreign anchor currency

Examples: LTL (Lithuania), EEK (Estonia)– pegged to

EUR

HKD (Hong Kong), BMD (Bermuda) – pegged to USD

International Finance 130440-1165

Monetary union

Two or more states using the same currency

Unilateral and multilateral monetary union

Unilateral - euroisation, dollarisation

Multilateral- EMU

International Finance 130440-1165

„De iure” and „de facto” classification

Free floating- mostly developed economies

Peg to the EUR- 40 countries

Peg to the USD- 70 countries

International Finance 130440-1165

Advantages and disatvantages of floating

Adjustment of the balance of payments +

Adjustment after shocks + Volatility concerning foreign trade and

investment –

The fear of floating –

International Finance 130440-1165

Advantages and disatvantages of pegs

Stability concerning foreign trade and

investment +

Possibility to „import” monetary stability +

Higher risk of speculative attacks – Constraint for the domestic economic policy-

The need of large reserves –

International Finance 130440-1165

Impossible trinity

International Finance 130440-1165

No single currency regime is right for all countries or at all

times.

J.A. Frankel

International Finance 130440-1165

Exchange rate regime choices

Estonia

Argentina

China

Estonia

Currency board

1992-1999 ER pegged to DEM, since 1999 to

EUR

Reasons for CB introduction in Estonia Inflation up to 300% in the early 90-ties

Small open economy- outward oriented economic policy

Goal the join the EU (later the euro area)

International Finance 130440-1165

Estonia- CPI

0%

20%

40%

60%

80%

100%

Source: Estonian Central Bank

International Finance 130440-1165

Argentina

Currency board

ER pegged to USD 1991- 2002

Reasons for introduction: Hyperinflation till 1990

Large macroeconomic imbalances

International Finance 130440-1165

Argentina

CPI

-200

0

200

400

600

800

1000

1200

1400

1600

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

%

Results: Monetary stability

achieved External shocks-

liquidity crunch- late 90-ties

Overvalued peso due to wrong peg

Floating since 2002-extreme depreciation of the peso

International Finance 130440-1165

China

Fixed ER

1997-2005 peg against the USD

Export oriented strategy

2005- switching from the USD peg to a basket

crawling peg

Reasons for switching RMB undervalued

Large global imbalances

International Finance 130440-1165

Current account balance

-50

0

50

100

150

200

250

300

350

400

450

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

billions USD

Revaluation of the RMB Gradual movement towards more flexible ER Lifting capital controls

Source: IMF

International Finance 130440-1165

Types of exchange rate

Nominal and real ER

Nominal ER- the price of a currency expressed

in a foreign currency

Real ER - the price of commodities of one

country expressed in prices of foreign

commodities -ratio of the domestic price level

and the foreign price level

International Finance 130440-1165

Types of ER

Billateral and effective

Billateral- the price of a currency

expressed in a foreign currency

Effective- ER weighted with the shares of

trade partners in the whole foreign trade

International Finance 130440-1165

Equlibrium on the currency market

The state of equilibrium is reached when the

supply of a foreign currency equals the demand

for this currency

Appreciation / Depreciation

Revaluation / Devaluation

International Finance 130440-1165

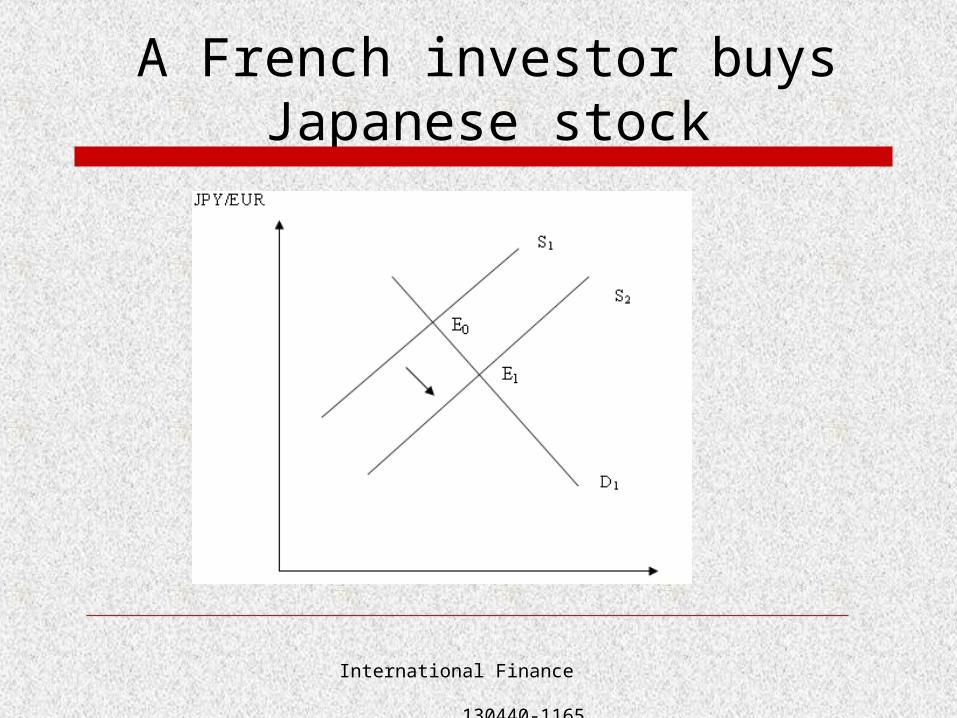

Depreciation and appreciation

Demand and supply on the FX market

Companies involved in foreign trade

Foreign investors

Central banks

International Finance 130440-1165

A French investor buys Japanese stock

International Finance 130440-1165

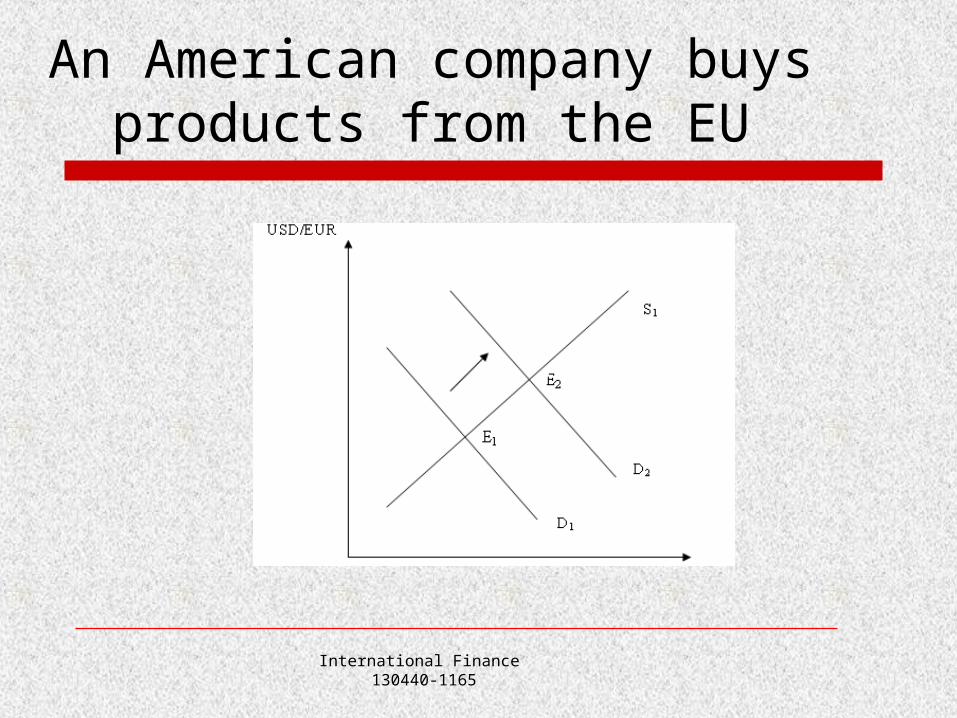

An American company buys products from the EU

International Finance 130440-1165

Factors determining the exchange rate in the short term

Fundamental economic values

Trends

Events

International Finance 130440-1165

Fundamental economic values

GDP growth rate

Interest rates

Prices

International Finance 130440-1165

Growth rate

International Finance 130440-1165

Interest rate

International Finance 130440-1165

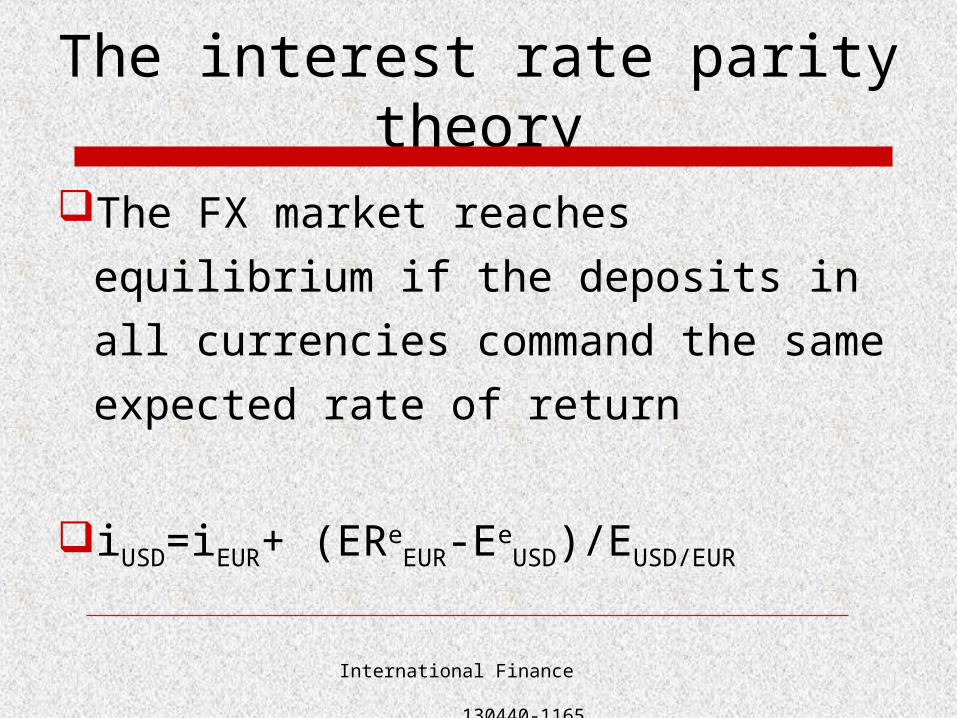

The interest rate parity theory

The FX market reaches equilibrium if the

deposits in all currencies command the

same expected rate of return

iUSD=iEUR+ (EReEUR-Ee

USD)/EUSD/EUR

International Finance 130440-1165

The interest rate parity theory

Example:

iUSD=10%, iEUR= 6%

Expected 8% USD depreciation p.a.

the expected rate of return in EUR is 4%

higher than in USD higher demand for

EUR unequlibrium ER changes

International Finance 130440-1165

The interest rate parity theory

If iUSD > iEUR USD appreciates

If iUSD < iEUR USD depreciates

International Finance 130440-1165

Prices

International Finance 130440-1165

Trends

Inflationary path

Fiscal developments

Expectations

Example:

PLN - introduction of direct inflation

targeting appreciation of PLN

International Finance 130440-1165

Events

Sudden decisions concerning economic policy

Market psychology

Example:

Hungarian ER regime switch depreciation of

HUF + market psychology depreciation of all

currencies in the region

International Finance 130440-1165

Summing up

ER regime choice depends on the

features of the economy

No ER regime is right for all countries or

at all times

Impossible trinity

International Finance 130440-1165

Summing up

Equlibrium in the short term depends on

market participants actions Fundamental values

Trends

Events

International Finance 130440-1165

References

P. Krugman, M.Obstfeld, International economics: theory

and policy. Part II, Pearson, Addison Wesley, Boston

2009

A. Budnikowski, Międzynarodowe stosunki gospodarcze,

PWE, Warszawa 2004

J. Frankel, No single currency regime is right for all

countries or at all times, Essays in International Finance,

1999.

International Finance 130440-1165