exchange rate rules the theory, performance and prospects ...978-1-349-05166-3/1.pdf · exchange...

TRANSCRIPT

EXCHANGE RATE RULES

The Theory, Performance and Prospects of the Crawling Peg

Of the dozens of conferences on international monetary economics to have been held in the last decade, a handful stand out as having marked important advances in the subject- perhaps most notably Wingspread I {1972) which clarified the monetary prerequisites for successful maintenance of a ftxed exchange rate, and Stockholm (1975) which ftrst articulated the asset market approach to exchange rate determination. Several participants in the Rio conference on the crawling peg (1979) ranked it alongside those earlier outstanding successes. The theme of the conference, the design of rules to guide and to limit exchange rate flexibility, reflected the widespread disquiet with the existing 'non-system' of nationally-managed but internationally-unregulated floating. The question posed was whether, and if so how, the literature of the 1960s on the crawling peg - and the experience of a number of countries with the system in the 1970s - might help to design something more coherent.

This book contains the papers and comments presented to the Rio conference, which collectively comprise the most exhaustive treatment of the crawling peg to date. Written by authors from four continents, the papers cover a wide range of views, a wide variety of analytical techniques, and a wide range of topics - theoretical modelling, a study of the impact on uncertainty, country studies, comparative studies, as well as a background paper by John Williamson (who was one of the early pioneers of analysis of the crawling peg). The book will be indispensable reading for all economists interested in the future of the international monetary system, as well as for policy-makers in semi-industrialised countries, many of which will certainly be considering using a crawling peg in future years irrespective of what happens to the system as a whole. A number of the papers should become standard supplementary reading for courses in international monetary economics.

John Williamson, the editor of this volume, is currently Professor at the Pontiffcia Universidade Catolica do Rio de Janeiro. He has previously been a lecturer at the University of York, Professor at the University of Warwick, and Visiting Professor at MIT, as well as a consultant at HM Treasury and adviser at the IMF. His publications include The Crawling Peg (Princeton Essays in International Finance) and The Failure of World Monetary Reform.

Also by John Williamson

THE FAILURE OF WORLD MONETARY REFORM, 1971-74 THE FINANCING PROCEDURES OF BRITISH FOREIGN TRADE

(with Stephen Carse and Geoffrey E. Wood)

EXCHANGE RATE RULES The Theory, Performance and Prospects of the Crawling Peg

Edited by John Williamson

Proceedings of a conference sponsored by the Ford Foundation, the Assoscia~;'lro Nacional de Centros de Pos Graduacao em Economia and the Pontiffcia Universidade Catolica do Rio de Janeiro, held in Rio de Janeiro

M

Selection, editorial matter and Chapter I © John Williamson 1981 Chapters 2-12 inclusive © The Macmillan Press Ltd 1981

Softcover reprint of the hardcover 1st edition 1981 978-0-333-28057-7

All rights reserved. No part of this publication may be reproduced or transmitted, in any form or by any means,

without permission

First published 1981 by THE MACMILLAN PRESS LTD

London and Basingstoke Companies and representatives

throughout the world

ISBN 978-1-349-05168-7 ISBN 978-1-349-05166-3 (eBook) DOI 10.1007/978-1-349-05166-3

Typeset in Great Britain by STYLESET LIMITED

Salisbury . Wiltshire

Contents

List of Participants

A Semantic Caution

Introduction John Williamson

PART ONE: THEORY

1 The Crawling Peg in Historical Perspective

John Williamson

Comment Ricardo Ffrench-Davis Alexander Swoboda

2 Monetary Control and the Crawling Peg

Ronald McKinnon

Comment Pedro Malan Bijan B. Aghevli

3 Exchange Rate Rules and Macroeconomic Stability

Rudiger Dornbusch

The Analysis of Floating Exchange Rates and the Choice

ix

xi

xiii

3

31 35

38

50 53

55

Between Crawl and Float 68

Stanley W. Black

Comment Pedro Aspe Alexander Swoboda

82 85

vi CONTENTS

4 Purchasing Power Parity as a Rule for a Crawling Peg 88

Hans Genberg

Comment Michael Mussa 107 Harman Lehment 110

PART TWO: PERFORMANCE 111

5 The Crawling Peg and Exchange Rate Uncertainty 113

Donald V. Coes

Comment Michael Mussa 137

6 The Crawling Peg: Brazil 140

Roberto Fendt

Exchange Rate Policies in Chile: The Experience with the Crawling Peg 152

Ricardo Ffrench-Davis

Comment William G. Tyler 175 Andre Lara-Resende 178

7 Crawling Peg Systems and Macroeconomic Stability: The Case of Argentina 1971-8 181

Ana Martirena-Mantel

Experience with the Crawling Peg in Colombia 207

Miguel Urrutia

Comment Carlos Diaz Alejandro 221 Carlos Rodriguez 224

Juan Carlos de Pablo 228

CONTENTS vii

8 Exchange Rate Policies in Peru, 1971-9 230

Denise Williamson

Portugal's Crawling Peg 243

Rudiger Dornbusch

Floating Versus Crawling: Israel1977-9 by Hindsight 252

Michael Bruno and Zvi Sussman

Comment Jorge Braga de Macedo Peter Roof

9 The Impact of the Float on LDCs: Latin American Experience in the 1970s

Edmar Bacha

272 279

282

Experiences of Asian Countries with Various Exchange Rate Policies 298

Bijan B. Aghevli

Comment Chaiyawat Wibulswasdi 319 Leopoldo Solis 322

PART THREE: PROSPECTS 325

10 Inflation and Growth: Exchange Rate Alternatives for Mexico 327

Guillermo Ortiz and Leopoldo Solis

Comment Roberto Fendt Stanley W. Black

11 The European Monetary System - An Approximate

347 349

Implementation of the Crawling Peg? 351

Niels Thygesen

viii CONTENTS

United States Economic Interests and Crawling Peg Systems 371

Thomas D. Willett

Comment Richard N. Cooper 384 Hans Genberg 387

12 Concluding Session: Panel Discussion

John Williamson 391 Michael Mussa 394

Carlos Diaz Alejandro 396 Niels Thygesen 397

Richard N. Cooper 400

Index 409

List of Participants

Bijan B. Aghevli, International Monetary Fund Pedro Aspe Armella, Instituto Tecnoldgico Autonomo de Mexico Edmar Bacha, PUC-RJ Stanley W. Black, Vanderbilt University Michael Bruno, Falk Institute, Jerusalem Donald V. Coes, University of IDinois and FUNCEX-RJ Richard N. Cooper, State Department Carlos F. Diaz Alejandro, Yale University Rudiger Dornbusch, Massachusetts Institute of Technology Roberto Fendt, FUNCEX-RJ Ricardo Ffrench-Davis, CIEPLAN, Santiago Hans Genberg, Graduate Institute of International Studies, Geneva Pentti J. K. Kouri, New York University Andre Lara-Resende, PUC-RJ Harman Lehment, Institut fur Weltwirtschaft, Kiel Jorge Braga de Macedo, Yale University Pedro S. Malan, PUC-RJ Ana Martirena-Mantel, Instituto Torcuata Di Tella, Buenos Aires Ronald I. McKinnon, Stanford University Michael Mussa, University of Chicago Guillermo Ortiz, Banco de Mexico Juan Carlos de Pablo, Buenos Aires Rogert Pringle, Consultative Group on International Economic and Monetary Affairs Carlos Rodriguez, Centro de Estudios Macroeconornicos de Argentina Peter Ruof, Ford Foundation Leopoldo Solis, Banco de Mexico Alexander Swoboda, Graduate Institute of International Studies, Geneva Niels Thygesen, University of Copenhagen William G. Tyler, University of Florida Miguel Urrutia Montoya, FEDESARROLLO, Bogota Chaiyawat Wibulswasdi, Bank of Thailand Denise Williamson, IBGE-RJ John Williamson, PUC-RJ

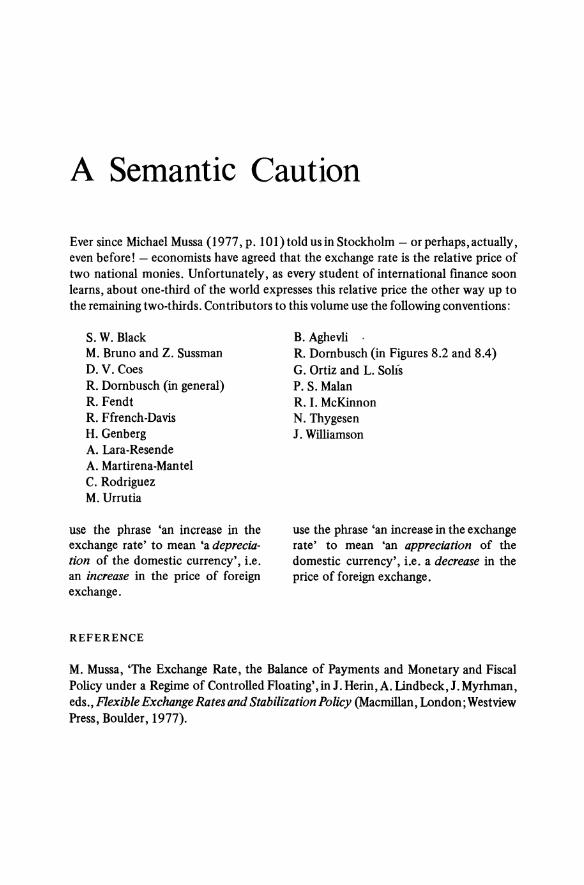

A Semantic Caution

Ever since Michael Mussa (1977, p. lOl)told us in Stockholm- or perhaps, actually, even before! - economists have agreed that the exchange rate is the relative price of two national monies. Unfortunately, as every student of international finance soon learns, about one-third of the world expresses this relative price the other way up to the remaining two-thirds. Contributors to this volume use the following conventions:

S. W. Black M. Bruno and Z. Sussman D. V. Coes R. Dornbusch (in general) R. Fendt R. Ffrench-Davis H. Genberg A. Lara-Resende A. Martirena-Mantel C. Rodriguez M. Urrutia

use the phrase 'an increase in the exchange rate' to mean 'a depreciation of the domestic currency', i.e. an increase in the price of foreign exchange.

REFERENCE

B. Aghevli . R. Dornbusch (in Figures 8.2 and 8.4) G. Ortiz and L. Solis P. S. Malan R. I. McKinnon N. Thygesen J. Williamson

use the phrase 'an increase in the exchange rate' to mean 'an appreciation of the domestic currency', i.e. a decrease in the price of foreign exchange.

M. Mussa, 'The Exchange Rate, the Balance of Payments and Monetary and Fiscal Policy under a Regime of Controlled Floating', in J. Herin, A.lindbeck, J. Myrhman, eds., Flexible Exchange Rates and Stabilization Policy (Macmillan, London; Westview Press, Boulder, 1977).

Introduction John Williamson

Many economists have been disappointed by the experience of six years of managed floating. Given that the adjustable peg remains unworkable because of the extent of capital mobility, and that the textbook alternatives of permanently fixed and freely floating exchange rates remain as remote as ever, it seemed natural to seek renewed analysis of the crawling peg. That was the purpose of the papers presented to the conference held in Rio de Janeiro in October 1979 and gathered together in this book. As will be found, the task was approached not just by a series of theoretical papers, but also by an examination of the experiences of the semi-industrialised countries that have used the system.

The first paper in the book is a rather lengthy background paper which I wrote and circulated several months before the conference met. After staking the claim of the term 'crawling peg' to official adoption, I provide a survey of the academic literature on the origin of the proposal, of past discussion of its pros and cons, of the variants that were suggested, and of more recent analysis of questions like stability. This is followed by a brief history of official discussion of the idea. The next section of the paper reports the nine countries that have used the system, for periods ranging from two to twelve years. I make no attempt at appraisal of their experiences, since a major aim of the conference was to do exactly that through the country studies, but I do draw attention to the fact that these countries have been highinflation, semi-industrialised countries rather than the major convertible-currency countries at the centre of the system whom the academic authors of the 1960s thought they were addressing. This observation suggested that it would be profitable to consider during the conference both (a) the appropriateness of the crawling peg for the type of countries that have already used it, and (b) whether it might have a wider potential role in the future as a base for a more structured international monetary system.

Since the crawling peg comes in so many variants, it seemed that it might be useful to try to focus discussion on one particular version. The last section of my paper suggested for this purpose a version close to the actual practices of most of the countries that have already used a crawling peg, in which the peg is adjusted essentially in order to neutralise the inflation differential between the country and its trading partners/competitors. This may be termed a 'PPP-guided crawling peg'. In an attempt to think through how this type of idea might be incorporated in the rules of a structured international monetary system, I suggested that participating countries might be required (i) to avoid individual peg changes greater than a certain

xiv INTRODUCTION

size; (ii) to keep their 'real peg' within a specified band around a level estimated to represent purchasing power parity (PPP); and (iii) to accept that their agreed PPP target could be altered only subject to IMF approval, and at a maximum rate of (say) 3 per cent per annum. Naturally a structured international monetary system would require rules on subjects other than exchange rates, and during the conference I had occasion to mention the form that I could conceive the two essential rules complementary to (i) to (iii) might take. Since these rules inevitably appear somewhat technical on first acquaintance and this is not the place to develop them at length, I relegate them to a note, 1 and say here merely that the basic idea involves reversing the roles traditionally assigned to reserves and domestic credit. Instead of countries having their national actions constrained by limits on reserve availability and being free subject to those constraints to follow whatever credit policy they please, countries would accept to be bound by certain rules governing domestic credit expansion and would be provided with whatever reserves were necessary to sustain their pursuit of policies consistent with those rules. The aim would be to make the crawling peg invulnerable to speculative crises, while providing adequate assurance against monetary indiscipline.

However, for better or worse my ideas on the sort of rules that should accompany a crawling peg adopted on a general basis had not crystallised when I wrote the background paper, and hence were only introduced ad hoc into the conference rather than as one of its basic topics. The papers invited, and the discussion, were centred around the theme of the crawling peg as an exchange rate regime, rather than around a vision of the form that a reformed international monetary system might take.

The theoretical section of the book begins with a paper by Ronald McKinnon entitled 'Monetary Control and the Crawling Peg'. It presents the most critical appraisal of crawling to be found among the main papers. McKinnon argues that adoption of what he terms 'passive crawling', i.e. the use of a formula (including PPP) to guide exchange rate changes, is liable to upset expectations and thereby destabilise the monetary system. The only context in which he saw a case for 'passive crawling' was in 'fmancially repressed' developing countries which wish to exploit the inflation tax but need to prevent the inflation distorting their external economic relations. What he termed 'active crawling'- i.e. the pre-announcement of a schedule of exchange rates, preferably involving a decelerating rate of depreciation and finally leading to a fixed rate - received a more sympathetic treatment as a useful technique for developing countries wanting to follow the Chilean road to stabilisation. Towards the end of the conference, McKinnon conceded that some developed countries might also fmd this a useful tool on the path to financial stabilisation.

The contrast between 'passive' and 'active' crawling provided the principal occasion for those skirmishes in the monetarist controversy that are customary at such conferences. There were repeated exchanges which (as I argue in my concluding comments) can be understood in terms of whether or not the 'Law of One Price' was accepted as a sedous explanation of the determination of national price levels. Those who endorsed tQ.is part of 'global monetarism' saw a useful role for 'active

INTRODUCTION XV

crawling' and naturally rejected 'passive crawling' as prone to lead to instability and even hyperinflation. Those who rejected the view that national price levels are determined essentially through arbitrage tended to be more concerned with the distortions of the real economy resulting from inappropriate, or violently oscillating, real exchange rates.

Rudiger Dornbusch's theoretical paper deals with the case for and against a governmentally-managed, as opposed to a market-determined, exchange rate. His first result is that, even without money illusion and with rational expectations, a managed exchange rate can reduce the shortfall of output below full employment involved in restoring equilibrium (after, say, a real shock that requires worsened terms of trade) as compared to either a fixed or a floating exchange rate. He goes on to show that the cost of an activist policy that attempts to exploit these opportunities is greater asymptotic variability of the price level, thus establishing a modernised version of the unemployment/inflation trade-off in which (in a stochastic setting) an activist policy can on average raise output, but only at the cost of greater long-run variability of prices. It will be interesting to see whether Keynesians find this an adequate basis for renewed confidence in the worth of activist policies designed to stabilise output. Even those who would be happy to buy this rationale for activist policies, and pay the price in terms of enhanced variability of inflation, will - as always - have to consider whether it is realistic to expect the quality of management to be sufficiently high to create an expectation that the potential gains will be realised. And even if the case for activist policy is accepted, that need not translate into endorsement of the crawling peg. As Pentti Kouri emphasised in discussion, there are circumstances in which the discontinuous exchange rate changes that are precluded by adoption of a crawling peg would be myopicallyoptimal responses to the receipt of new information. One also needs to ask whether those myopic advantages are sufficient to justify the stimulation of portfolio switches that is inevitable when exchange rates may be changed abruptly. Only those who are both convinced by the case for activist management and weigh maintenance of speculative confidence as more important than guaranteed promptness of desirable changes will necessarily rate the crawling peg the optimal regime.

Dornbusch's comparison between a floating and a managed exchange rate uses the simplest possible model of the former, in which the rate adjusts to maintain continuous current account balance. The next paper, by Stanley Black, uses in contrast an asset-market model of short-run exchange rate determination (which in fact owes much to Dornbusch's work), to model an economy characterised by five 'stylised facts': a J-curve, less than infinitely elastic demand for exportables, limited capital mobility, instantaneous adjustment of financial but not of goods markets, and downward stickiness of wages and prices. He employs this model to compare the responses of economies with a fixed nominal exchange rate, a fixed real exchange rate, and a floating exchange rate to various types of disturbances, concluding that the crawling peg allows a smoother adjustment to monetary disturbances, but that (in its fixed real rate form) it would jeopardise the ability to adjust to real disturbances. He then examines the past behaviour of a selection of real and monetary variables in samples of industrialised countries and of LDCs during the 1970s, and

xvi INTRODUCTION

shows that monetary disturbances have historically been much greater relative to real disturbances in LDCs than in the developed countries. This finding, together with the characteristically greater capital mobility among developed countries, is then offered as an explanation of why developed countries have not followed the example of the semi-industrialised countries in adopting crawling.

Hans Genberg's paper is specifically directed at evaluating the suitability, and mode of implementation, of a PPP rule, which he does by examination of historical experience and by verbal consideration of a variety of theoretical factors, rather than by construction of a formal model. Like Black, he analyses the reactions of the system to a variety of types of shock. He concludes (like Black) that a PPPguided crawl should deal well with disturbances of a purely monetary nature, that it would be likely to reduce ratchet effects and vicious circles, and (in contrast to McKinnon) that it should induce more stabilising speculative behaviour than a float. He observes, however, that other systems might also be able to achieve these desirable ends, while (again paralleling Black's conclusions) a strict PPP rule would preclude ability to accommodate real disturbances. Assuming that the longer-run changes in real exchange rates actually observed were desirable in order to secure adjustment, Genberg shows that variations of as much as 10-20 per cent would have been required over a five-year period by the industrialised countries. Even a permitted 'real crawl' of 3 per cent per annum would, on these figures, have proved barely adequate to the task of accommodating needed real adjustments. Furthermore, there are major unresolved problems in identifying the circumstances in which real exchange rate adjustments are called for, and there is therefore a danger that a PPP-guided crawl might degenerate into an engine of inflation as (say) a real appreciation required by a real shock was resisted rather than accepted.

The discussion following this paper revealed general agreement on two points: (i) that a rigid PPP rule that gave no scope for changes in the real exchange rate would be a disaster; (ii) that any PPP rule would tend to eliminate the negative feedback from the external sector that provides a check to an inflationary spiral under a fixed exchange rate. Some participants concluded from these points that the use of macroeconomic policy in order to stabilise any real variable, including the real exchange rate, was undesirable in principle. Others conceded the dangers of trying to stabilise a real variable at what might be, or become, a disequilibrium rate, but evidently held that the risk was worth taking. (If one believes in stabilisation policy at all, it hardly makes sense to stabilise something that fundamentally does not matter, like a nominal value.) There is a natural analogy with the internal dimension of stabilisation policy, which can certainly become an engine of inflation if directed at the maintenance of an unemployment target that is, or becomes, different from the natural rate.

While Genberg's paper concludes the first part of the book, readers may like to note that several subsequent papers also contain formal macroeconomic model building. This applies in particualr to the first part of Ana Martirena-Mantel's paper, Section II of the Bruno-Sussman paper, and (with emphasis on the financial sector) to section IV of the Ortiz-Solis paper.

The second part of the book is concerned with evaluating what can be learned

INTRODUCTION xvii

on the basis of past experience with the crawling peg. It is opened by Donald Coes' paper on the impact of the Brazilian crawling peg on the price uncertainty facing exporters, and thus on the level of exports. In addition to its role in evaluating the crawling peg, this paper should provide a useful introduction for the non-specialist to the important but highly technical literature on uncertaintly that is evolving. Coes' conclusion is that there is rather strong evidence in support of the presupposition that greater exchange rate uncertainty can be expected to inhibit trade. Although his analysis was challenged on a number of technical points, it constitutes an important addition to the available body of evidence. Until recently, this seemed to be all negative; but, in conjunction with the work of Diaz Alejandro (1976, pp. 66-9) on Colombia and that of Rana (1979) on several Asian countries, it creates a presumptive case that exchange rate instability imposes significant allocative costs.

The next seven papers provide country studies on seven of the nine countries that have up to now employed the crawling peg in a reasonably systematic way. The papers reflect fascinating contrasts in style of analysis, in the theoretical predispositions of their authors, and in the varied experiences of the seven semiindustrialised countries involved. Since my purpose in inviting these papers was not that of providing a comparative study of macroeconomic policy-making in open semi-industrialised economies, I can without immodesty claim that the papers (together with the Ortiz-Solis paper on Mexico in the following part) perform that function rather well.

These papers also suggest some tentative conclusions about the suitability of the crawling peg for more general adoption. The ('passive') crawling peg gets good marks for stabilising the real exchange rate, promoting non-traditional exports, and limiting disruptive flows of short-term capital - though it is repeatedly emphasised that the latter achievement has to be viewed in the context of countries whose currencies were not convertible and where capital mobility is therefore much lower than among the main industrial countries. The role of crawling in promoting rational macroeconomic management is more ambiguous. The record does not reveal any major disasters, such as afflicted virtually all of these countries either/both immediately before and/or after the change to/from crawling- the Colombian reserve exhaustion of 1966, the Chilean crisis in the Allende years, the Peruvian debt crisis, the Portuguese slide into chronic external deficit, the Argentine or Israeli inflationary explosions. But one could hardly claim that the crawling peg has never been associated with failures of economic management: the Peruvian austerity, stagflation in Argentina and Chile, the threat to Colombia's non-traditional exports posed by positive supply shocks, and the post-1974 acceleration of Brazilian inflation. And, as always, there is the problem of identifying which events can legitimately be ascribed to a particular policy. Suffice it to say that the conferees did not reach agreement, and hence readers will have to decide for themselves.

In order to enable this volume to serve as a reasonably comprehensive reference work on experience with the crawling peg as of late 1979, it may be useful to add a paragraph on the experiences of countries other than the seven covered in the volume. One other case of unambiguous crawling is that of Korea, which adopted

xviii INTRODUCTION

a policy of gradual devaluation in 1968 and maintained the crawl until June 1971, when the policy was interrupted by an abrupt step devaluation followed by six months of a pegged rate. The crawl was resumed at the end of the year for a further six months, before being newly pegged to the US dollar in June 1972. (See Frank, Kim and Westphal, 1975.) The other unambiguous case is that of Uruguay, which adopted the policy in 1972, motivated by a chronic inflation. Apart from a stabilisation of a few months in 1975, a 'passive crawl' was maintained until 1978, when Uruguay, like Argentina, moved to a pre-announced crawl. This policy has, as in Argentina, been associated with a vast capital inflow and, to all appearances (though see the Comment of Rodriguez) an increasing overvaluation as inflation has outstripped depreciation. It has even been argued that the system is unstable, in that a capital inflow causes monetary expansion, which accelerates inflation, which raises the nominal interest rate, which - with a fixed schedule for depreciation -increases the real dollar interest rate, and thus the capital inflow. The next closest case to a crawling peg was that of South Vietnam in the years 1972-5, when the currency was indeed devalued frequently and in fairly modest steps, but in a sufficiently erratic way and in sufficiently unusual circumstances as to preclude any possibility of drawing conclusions of general validity. Other cases that have sometimes been claimed to be the application of a crawling peg seem to have been either the ad hoc spacing out of a once-for-all depreciation (Bangladesh, 1978) or changes in the dollar intervention points consequent on a policy of pegging to a basket of currencies or the SDR (e.g. Saudi Arabia).

The remaining two papers in this part analyse a particular aspect of the exchange rate issue with reference to a specific geographical area. Edmar Bacha's paper is concerned with the implications of exchange rate flexibility among the industrialised countries for the countries of Latin America, as represented specifically by Brazil, Chile, Costa Rica and Guatemala. He documents the continued dollar domination of the region, the consequences of generalised floating for the behaviour of real effective exchange rates, the effect of dollar domination in reducing the impact of increased uncertainty, and the price that is paid to secure that protection. He concludes that there is a case for moving away from exclusive use of the dollar as vehicle and reserve currency. Bijan Aghevli's paper deals with the implications of the exchange rate policies adopted by eight Asian countries, which he notes bear a systematic relation to their relative inflation rates: fast-inflating countries have pegged to the dollar, while the slower inflaters have floated (an interesting reversal of the Latin American pattern). He presents statistical tests designed to assess the contributions of domestic monetary expansion and of imported inflation (defined to include the inflationary effects of currency depreciation) to domestic inflation in these eight countries; it transpires that both factors were significant, but that the first was the more important in every country except India. This finding is, of course, conspicuously inconsistent with the view that national price levels are determined principally by arbitrage. Similarly, both domestic credit expansion and changes in the real exchange rate are shown to have influenced the balance of payments in the theoretically expected direction, with the former again being the dominant factor except in India. These facts, in conjunction with the reluctant

INTRODUCTION xix

exchange rate adjustment that characterises these countries in the same way that it has always characterised all other countries that have practised the adjustable peg, have resulted in a very clear association between inflation differentials on the one hand and the evolution of the real exchange rate, and of reserves, on the other. There could scarcely be a more emphatic empirical repudiation of the claim that monetary policy has no systematic influence on real variables.

The fmal part of the book contains three papers centred on an attempt to assess the future potential for the crawling peg. The first of these papers considers whether the crawling peg might provide a solution to the problem of finding a suitable exchange rate regime for a semi-industrialised country, Mexico, with a long history of exchange rate stability until the 1976 crisis that led to a sharp depreciation and official adoption of 'floating'. (It is rather a funny form of floating, in as much as the peso never varies in terms of the dollar; Ortiz and Solis christen it a 'fixed float'!) The main theme of the paper is the threat of dollarisation of the Mexican economy and the stimulus to this process that would be given by depreciation of the peso relative to the dollar. Since Ortiz and Solis treat the crawling peg as a technique to allow Mexico to tolerate a rate of inflation higher than is compatible with maintenance of a fixed exchange rate (which is indeed very much the role that it has fulfilled elsewhere in Latin America), they conclude that the dollarisation problem tips the balance against a strategy of crawling to accommodate the high inflation that would be the· cost of high growth. The analysis of the dollarisation problem is a fascinating contribution to the emergent literature on currency substitution, but I have to confess myself unconvinced by the corollary drawn for exchange rate policy. If Mexico is indeed in a position to reduce inflation, why be content with stopping at the US rate? why not use a crawl to permit a better price performance? And if there is great uncertainty about just how much success can be hoped for, then surely the most certain way of undermining the peso is to declare that the peso is at best going to go down with the dollar but may sink even faster?

The next paper is by Niels Thygesen on the European Monetary System. The crux of Thygesen's argument is that in its later years the snake had begun to operate pretty much as a (decision-variant) crawling peg, in that individual realignments were sufficiently small to be implemented without imposing discrete changes in market exchange rates, and that it was this largely unnoticed change in practice from the rules of the old Bretton Woods system that enabled the snake, against many academic predictions, to survive. Since the intention is to operate the EMS in the same way (an intention that was implemented in the first realignment), there is no reason why the EMS should not succeed. Prognostications of doom based on a belief that EMS is recreating a mini Bretton Woods system have simply not understood what is happening in Europe. Thygesen does not emphasise the converse implication: that the success in maintaining pegged exchange rates among a group of countries between which there is conspicuously high capital mobility demonstrates that it is not only in countries with exchange controls that a crawl can limit disruptive capital movements.

The final paper, by Thomas Willett, deals with US interests in proposals that would involve replacing floating by crawling. (Unhappily Willett was not in the end

XX INTRODUCTION

able to attend the conference, but his paper was discussed in his absence.) Willett argues that the United States is the prototypical case of a country that satisfies the conditions of an optimum currency area, and as such can have no interest in pursuing the replacement of floating by a system involving greater restraints on national policy-making. However, he also argues that, if other countries were anxious to move to a system based on crawling, the costs to the United States would be sufficiently marginal to justify a sympathetic American reception, as an investment in good international relations. This judgment, however, carries an important proviso (endorsed by one of his discussants, Richard Cooper): that the change should not be accompanied by a reinstatment of convertibility or asset settlement obligations on the United States, since the cost of these (in terms of constraints on macroeconomic policy formation) would be unacceptable. It is easy to understand the feeling that 'the tail should not be allowed to wag the dog' that underlies this condition. At the same time, it seems rather unlikely that the rest of the world will ever find a Dollar Standard more acceptable than it did in the early 1970s- and a pegged-rate system without international constraints on US policies would amount to a Dollar Standard. Hence a key question in any future attempt to construct a structured international monetary system would almost certainly be the US reaction to the type of proposal alluded to in note 1 above, in which financial constraints would be accepted but would be free of the gambling dangers ofbattling with speculators that are imposed by a reserve constraint. However, the acceptability of such ideas was not even posed, let alone discussed, at the conference.

The book is completed by an account of the concluding panel discussion. I do not think I can claim that this revealed sufficient unanimity to justify brief summarisation. My own views evolved, but were not overturned, in ·the course of the conference; but (for example) Michael Mussa clearly remained unconvinced by the whole idea of using PPP as a norm, Richard Cooper about the wisdom of ruling out discrete exchange rate changes, and Carlos Diaz Alejandro about the relevance of the experience of semi-industrialised countries for the industrialised countries. In the absence of greater evidence of full-hearted conversion to right thinking, it is fortunate that publication of the proceedings provides the opportunity to turn the debate over to the profession at large.

NOTES

1. The first rule would require that countries accepted a target for domestic credit expansion (DCE) determined by an agreed formula, and that reserve changes would be allowed to produce a one-for-one impact on the money supply. Deviation from this target would, beyond some agreed proportion, result in increasing penalties. The type of formula for target DCE would be:

DCE/(money supply)= ag+ {3(P/P)t-t + -yD + li(C-C*)

where o: =estimated income elasticity of demand for money; g = estimated trend rate of real growth;

INTRODUCTION xxi

D = estimated deflationary gap (either world or national, or a weighted average of the two, either current or forecast);

C =current account balance, adjusted for the impact of temporary factors beyond the country's own control;

C* = target current account balance. Naturally one would require 1 > ~ > 0 to ensure stability. Monetarists would presumably wish to set 'Y = 0.

The second rule would provide unlimited access to balance of payments finance to countries that observed their DCE targets, and deny the right to intervene in the foreign exchange markets to countries that violated their targets. 2. I have never understood why everyone who does not speak German seems to regard sticking with the international norm as acceptable inflation performance. Indeed, I suspect that this attitude is a part of the explanation for global doubledigit inflation: it has permitted the cumulative acceleration that has been witnessed over the past two decades.

REFERENCES

Diaz Alejandro, C. Foreign Trade Regimes and Economic Development: Colombia (NBER, New York, 1976).

Frank, C. R., Kim, K. S. and Westphal, L., Foreign Trade Regimes and Economic Development: South Korea (NBER, New York, 1975).

Rana, Pradumna, 'The Impact of Generalized Floating on Trade Flows and Reserve Needs: Selected Asian Developing Countries', Vanderbilt University PhD Thesis, 1979 (to be published by Garland).