excerpt from: what the heck is work anyway? by alexander kjuerulf rather than try to come up with...

TRANSCRIPT

Excerpt from: What the heck is work anyway?by Alexander Kjuerulf

Rather than try to come up with the most correct definition of work, i.e. one that would make sense in an economical, sociological and psychological perspective, I’d rather try to find a definition of work or rather a view of work, that promotes happiness at work in most normal kinds of work.

This immediately eliminates some definitions:• If work is simply that you do because you have to, then happiness at work is

almost impossible by definition.• If work is only what you do for money, it eliminates all volunteer work.• If work is only what you do for a purpose, then all aspects of your job that

are not productive are no longer work.

I’m not claiming to have the answer yet, but as I see it here are some elements of a definition if work that is conducive to happiness:• Work is something you choose to do. You may not have a choice of whether

or not to work but you have choice in what work you do.• Work is something you’re valued for. Either someone pays you for your work

or someone takes the time and resources to organize your work.• Work is an activity where you make a positive difference for someone else.

Quick sharing from PwC report

They are arguing for students familiar with data analytics, but also…• Business leaders often lament skill gaps, and we believe

demand will continue to exceed the supply of candidates who have an analytical mindset, technical skills, and a foundation for leadership. So while skills in data analytics will be desired, we believe broader business acumen, global awareness, relationship skills, and leadership abilities will be just as coveted. This broad base will equip students to not only solve challenges, but also to frame these issues in a broader context, so they can ask the right questions—the ones that lead to root causes and solutions.

Quick sharing from PwC report

They are arguing for students familiar with data analytics, but also…• Business leaders often lament skill gaps, and we believe

demand will continue to exceed the supply of candidates who have an analytical mindset, technical skills, and a foundation for leadership. So while skills in data analytics will be desired, we believe broader business acumen, global awareness, relationship skills, and leadership abilities will be just as coveted. This broad base will equip students to not only solve challenges, but also to frame these issues in a broader context, so they can ask the right questions—the ones that lead to root causes and solutions.

Quick sharing from PwC report

They are arguing for students familiar with data analytics, but also…• Business leaders often lament skill gaps, and we believe

demand will continue to exceed the supply of candidates who have an analytical mindset, technical skills, and a foundation for leadership. So while skills in data analytics will be desired, we believe broader business acumen, global awareness, relationship skills, and leadership abilities will be just as coveted. This broad base will equip students to not only solve challenges, but also to frame these issues in a broader context, so they can ask the right questions—the ones that lead to root causes and solutions.

CHAPTER 7

CASH AND RECEIVABLES CONTINUED

Sommers – ACCT 3311

Supported by a formal promissory note.

A negotiable instrument.

Maker signs in favor of a Payee.

Interest-bearing (has a stated rate of interest) OR

Zero-interest-bearing (interest included in face amount).

Notes Receivable

Generally originate from:

Customers who need to extend payment period of

an outstanding receivable.

High-risk or new customers.

Loans to employees and subsidiaries.

Sales of property, plant, and equipment.

Lending transactions (the majority of notes).

Notes Receivable..

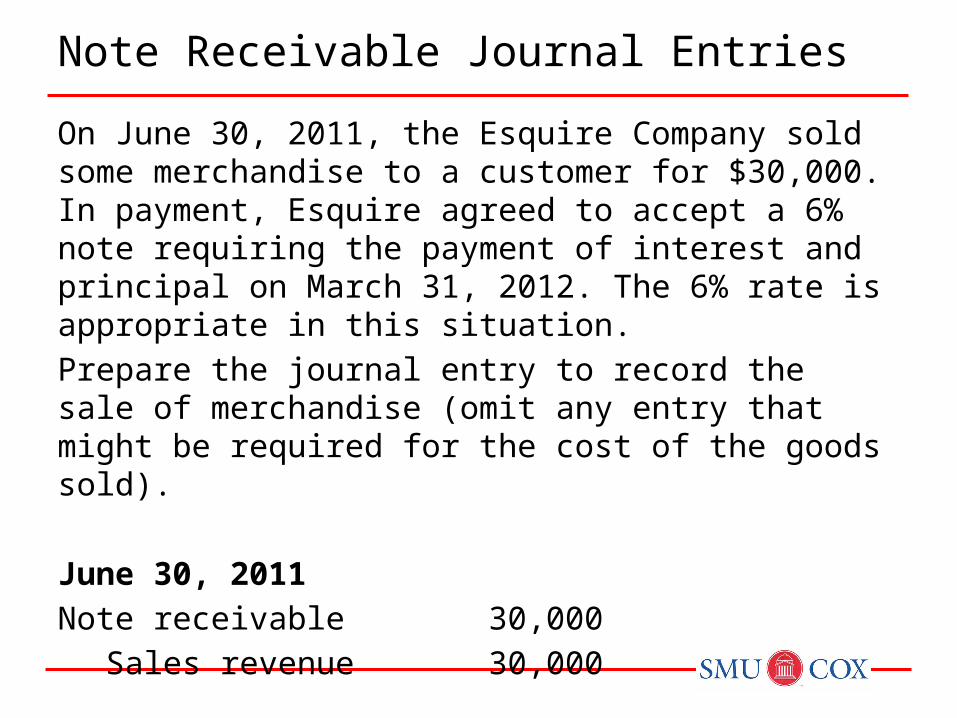

Note Receivable Journal Entries

On June 30, 2011, the Esquire Company sold some merchandise to a customer for $30,000. In payment, Esquire agreed to accept a 6% note requiring the payment of interest and principal on March 31, 2012. The 6% rate is appropriate in this situation.

Prepare the journal entry to record the sale of merchandise (omit any entry that might be required for the cost of the goods sold).

June 30, 2011

Note receivable 30,000

Sales revenue 30,000

Note Receivable Journal Entries

On June 30, 2011, the Esquire Company sold some merchandise to a customer for $30,000. In payment, Esquire agreed to accept a 6% note requiring the payment of interest and principal on March 31, 2012. The 6% rate is appropriate in this situation.

Prepare the journal entry at December 31, 2011.

December 31, 2011

Interest receivable 900

Interest revenue 900

($30,000 x 6% x 6/12) = 900

Note Receivable Journal Entries

On June 30, 2011, the Esquire Company sold some merchandise to a customer for $30,000. In payment, Esquire agreed to accept a 6% note requiring the payment of interest and principal on March 31, 2012. The 6% rate is appropriate in this situation.

Prepare the journal entry at March 31, 2012.

March 31, 2012

Cash 31,350

Interest revenue 450

Interest receivable 900

Note receivable 30,000

($30,000 x 6% x 3/12) = 450

Illustration: Morgan Corp. makes a loan to Marie Co. and receives in exchange a three-year, $10,000 note bearing interest at 10 percent annually. The market rate of interest for a note of similar risk is 12 percent. How does Morgan record the receipt of the note?

0 1 2 3

1,000 1,000 Interest$1,000

$10,000 Principal

4

i = 12%

n = 3

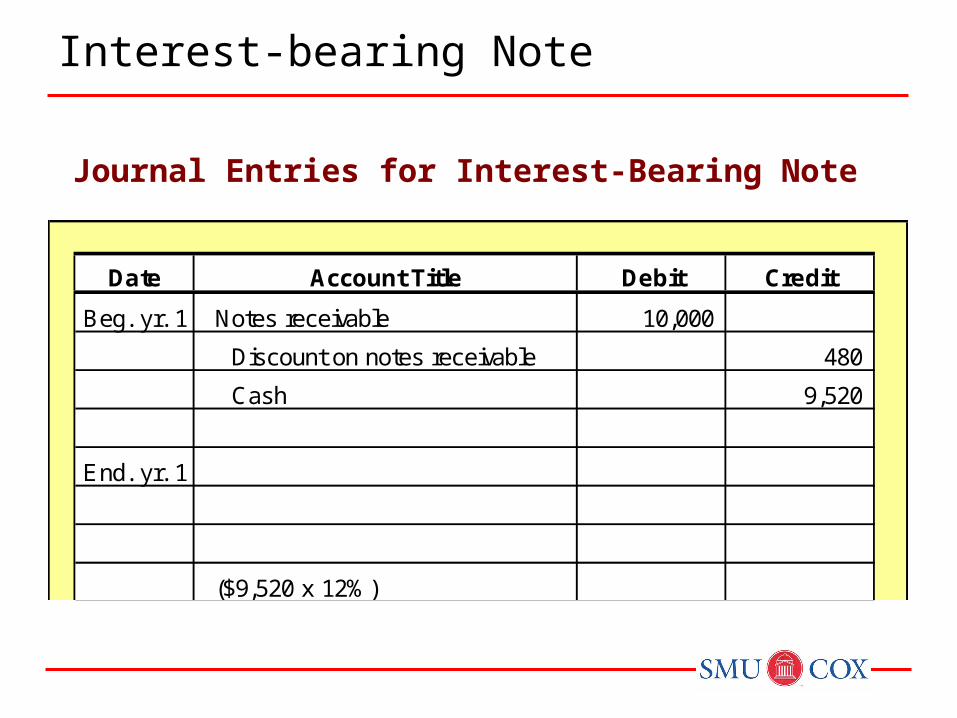

Interest-bearing Note

FV=10,000, pmt=1,000, n=3, i=12% => PV=9,520

Illustration: How does Morgan record the receipt of the note?

Notes Receivable 10,000

Discount on Notes Receivable 480

Cash 9,520

Interest-bearing Note

Illustration 7-15

Interest-bearing Note

Journal Entries for Interest-Bearing Note

Date Account Title Debit Credit

Beg. yr. 1 Notes receivable 10,000

Discount on notes receivable 480

Cash 9,520

End. yr. 1

($9,520 x 12%)

Cash 1,000

Discount on notes receivable 142

Interest revenue 1,142

Interest-bearing Note

Q7-15 What is “imputed interest”?Imputed interest is the interest ascribed or attributed to a situation or circumstance which is void of a stated or otherwise appropriate interest factor. Imputed interest is the result of a process of interest rate estimation called imputation.

In what situations is it necessary to impute an interest rate for notes receivable?An interest rate is imputed for notes receivable when (1) no interest rate is stated for the transaction, or (2) the stated interest rate is unreasonable, or (3) the stated face amount of the note is materially different from the current cash price for the same or similar items or from the current market value of the debt instrument.

Discussion Question

Discussion Question

Q7-15 Continued – What are the considerations in imputing an appropriate rate?

In imputing an appropriate interest rate, consideration should be given to the prevailing interest rates for similar instruments of issuers with similar credit ratings, the collateral, and restrictive covenants.

Non-Interest Bearing Note

On April 30, 2011, the Rangers Company sold some merchandise to a customer for $40,000. Rangers agreed to accept a payment of $40,000 on April 30, 2016. A 6% interest rate is appropriate in this situation.

Prepare the journal entry to record the sale of merchandise (omit any entry that might be required for the cost of the goods sold).

FV=40,000, pmt=0, n=5, i=6% => PV=29,890

April 30, 2011

Note receivable 40,000

Discount on note receivable 10,110

Sales revenue 29,890

Non-Interest Bearing Note

On April 30, 2011, the Rangers Company sold some merchandise to a customer for $40,000. Rangers agreed to accept a payment of $40,000 on April 30, 2016. A 6% interest rate is appropriate in this situation.

Prepare the amortization schedule.

Cash Interest Amort Balance4/30/2011 29,890 4/30/2012 4/30/2013 4/30/2014 4/30/2015 4/30/2016

Non-Interest Bearing Note

On April 30, 2011, the Rangers Company sold some merchandise to a customer for $40,000. Rangers agreed to accept a payment of $40,000 on April 30, 2016. A 6% interest rate is appropriate in this situation.

Prepare the amortization schedule.

Cash Interest Amort Balance4/30/2011 29,890

4/30/2012 -

1,793 1,793 31,683 4/30/20134/30/20144/30/20154/30/2016

Non-Interest Bearing Note

On April 30, 2011, the Rangers Company sold some merchandise to a customer for $40,000. Rangers agreed to accept a payment of $40,000 on April 30, 2016. A 6% interest rate is appropriate in this situation.

Prepare the amortization schedule.

Cash Interest Amort Balance4/30/2011 29,890

4/30/2012 -

1,793 1,793 31,683

4/30/2013 -

1,901 1,901 33,584 4/30/20144/30/20154/30/2016

Non-Interest Bearing Note

On April 30, 2011, the Rangers Company sold some merchandise to a customer for $40,000. Rangers agreed to accept a payment of $40,000 on April 30, 2016. A 6% interest rate is appropriate in this situation.

Prepare the amortization schedule.

Cash Interest Amort Balance4/30/2011 29,890

4/30/2012 -

1,793 1,793 31,683

4/30/2013 -

1,901 1,901 33,584

4/30/2014 -

2,015 2,015 35,599

4/30/2015 -

2,136 2,136 37,735

4/30/2016 -

2,265 2,265 40,000

Non-Interest Bearing Note

On April 30, 2011, the Rangers Company sold some merchandise to a customer for $40,000. Rangers agreed to accept a payment of $40,000 on April 30, 2016. A 6% interest rate is appropriate in this situation.

Prepare the journal entry at December 31, 2011.

December 31, 2011

Discount on note receivable 1,195

Interest revenue 1,195

(1,793 X 8/12)

Cash Interest Amort Balance4/30/2011 29,890

4/30/2012 -

1,793 1,793 31,683

4/30/2013 -

1,901 1,901 33,584

4/30/2014 -

2,015 2,015 35,599

4/30/2015 -

2,136 2,136 37,735

4/30/2016 -

2,265 2,265 40,000

Non-Interest Bearing Note

On April 30, 2011, the Rangers Company sold some merchandise to a customer for $40,000. Rangers agreed to accept a payment of $40,000 on April 30, 2016. A 6% interest rate is appropriate in this situation.

Prepare the journal entry at December 31, 2012.

December 31, 2012

Discount on note receivable 1,865

Interest revenue 1,865

(1,793 X 4/12) + (1,901 X 8/12)

Cash Interest Amort Balance4/30/2011 29,890

4/30/2012 -

1,793 1,793 31,683

4/30/2013 -

1,901 1,901 33,584

4/30/2014 -

2,015 2,015 35,599

4/30/2015 -

2,136 2,136 37,735

4/30/2016 -

2,265 2,265 40,000

Non-Interest Bearing Note

On April 30, 2011, the Rangers Company sold some merchandise to a customer for $40,000. Rangers agreed to accept a payment of $40,000 on April 30, 2016. A 6% interest rate is appropriate in this situation.

What is the balance of the note at December 31, 2012?

31,683 + (1,901 X 8/12) = 32,950

Cash Interest Amort Balance4/30/2011 29,890

4/30/2012 -

1,793 1,793 31,683

4/30/2013 -

1,901 1,901 33,584

4/30/2014 -

2,015 2,015 35,599

4/30/2015 -

2,136 2,136 37,735

4/30/2016 -

2,265 2,265 40,000

Non-Interest Bearing Note

On April 30, 2011, the Rangers Company sold some merchandise to a customer for $40,000. Rangers agreed to accept a payment of $40,000 on April 30, 2016. A 6% interest rate is appropriate in this situation.

Prepare the journal entry at April 30, 2016.

April 30, 2016

Discount on note receivable 755

Interest revenue 755

(2,265 X 4/12)

Cash 40,000

Note receivable 40,000

Cash Interest Amort Balance4/30/2011 29,890

4/30/2012 -

1,793 1,793 31,683

4/30/2015 -

2,136 2,136 37,735

4/30/2016 -

2,265 2,265 40,000

Notes Received for Property, Goods or Services

In a bargained transaction entered into at arm’s

length, the stated interest rate is presumed to be

fair unless:

1. No interest rate is stated, or

2. Stated interest rate is unreasonable, or

3. Face amount of the note is materially different

from the current cash sales price.

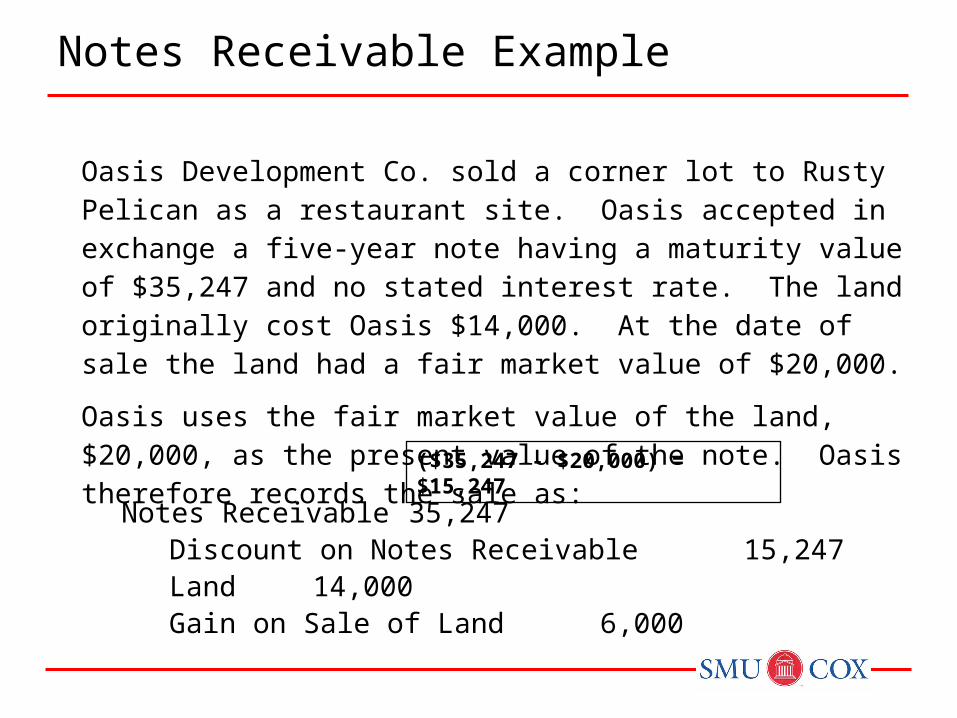

Oasis Development Co. sold a corner lot to Rusty Pelican as a restaurant site. Oasis accepted in exchange a five-year note having a maturity value of $35,247 and no stated interest rate. The land originally cost Oasis $14,000. At the date of sale the land had a fair market value of $20,000.

Oasis uses the fair market value of the land, $20,000, as the present value of the note. Oasis therefore records the sale as:

Notes Receivable 35,247Discount on Notes Receivable 15,247Land 14,000Gain on Sale of Land 6,000

($35,247 - $20,000) = $15,247

Notes Receivable Example

Discussion Question

Q7-16 What is the fair value option? Where do companies that elect the fair value option report unrealized holding gains and losses?

The fair value option gives companies the option of using fair value as the measurement basis for financial instruments. The Board believes that fair value measurement for financial instruments provides more relevant and understandable information than historical cost. If companies choose the fair value option, the receivables are recorded at fair value, with unrealized gains or losses reported as part of net income.

Short-Term reported at Net Realizable Value (same as

accounting for accounts receivable).

Long-Term - FASB requires companies disclose not only

their cost but also their fair value in the notes to the

financial statements.

► Fair Value Option. Companies have the option to use

fair value as the basis of measurement in the financial

statements. Adjustments to value go through net income.

Valuation of Notes Receivable

Owner may transfer accounts or notes receivables to another company for cash.

Reasons:

Competition. Sell receivables because money is tight. Billing / collection are time-consuming and costly.

Transfer accomplished by:

1. Secured borrowing

2. Sale of receivables

Disposition of Receivables

Disposition of Receivables

Secured borrowing• Now

Cash XXX

Payable XXX

Get cash sooner, have A/R and payable on books

• Later

Cash XXX

A/R XXX

Payable XXX

Cash XXX

Sale of Receivables• Now

Cash XXX

A/R XXX

Get cash sooner, but have nothing else on books

• Later

Nothing

The FASB

concluded that a

sale occurs only if

the seller surrenders

control of the

receivables to the

buyer.

Three conditions

must be met.

Secured borrowing vs. Sale

Factors are finance companies or banks that buy receivables from businesses for a fee.

Illustration 7-17

Sale of Receivables

Sale Without Recourse

Purchaser assumes risk of collection Transfer is outright sale of receivable Seller records loss on sale Seller uses Due from Factor (receivable) account to

cover discounts, returns, and allowances

Sale With Recourse Seller guarantees payment to purchaser Financial components approach used to record transfer

Sale of Receivables

1. Segregate the different types of receivables that a company

possesses, if material.

2. Appropriately offset the valuation accounts against the proper

receivable accounts.

3. Determine that receivables classified in the current assets

section will be converted into cash within the year or the

operating cycle, whichever is longer.

4. Disclose any loss contingencies that exist on the receivables.

5. Disclose any receivables designated or pledged as collateral.

6. Disclose the nature of credit risk inherent in the receivables.

Presentation of Receivables

Discussion Question

Q7-21 What is the accounts receivable turnover ratio, and what type of information does it provide?

The accounts receivable turnover ratio is computed by dividing net sales by average net receiv ables outstanding during the year. This ratio is used to assess the liquidity of the receivables. It measures the number of times, on average, receivables are collected during the period. It provides some indication of the quality of the receivables and how successful the company is in collecting its outstanding receivables.

This Ratio used to:

Assess the liquidity of the receivables.

Measure the number of times, on average, a company

collects receivables during the period.

A/R Turnover Ratio

RELEVANT FACTS - Similarities

The accounting and reporting related to cash is essentially the same under both IFRS and GAAP. In addition, the definition used for cash equivalents is the same.

Like GAAP, cash and receivables are generally reported in the current assets section of the balance sheet under IFRS.

Similar to GAAP, IFRS requires that loans and receivables be accounted for at amortized cost, adjusted for allowances for doubtful accounts.

IFRS

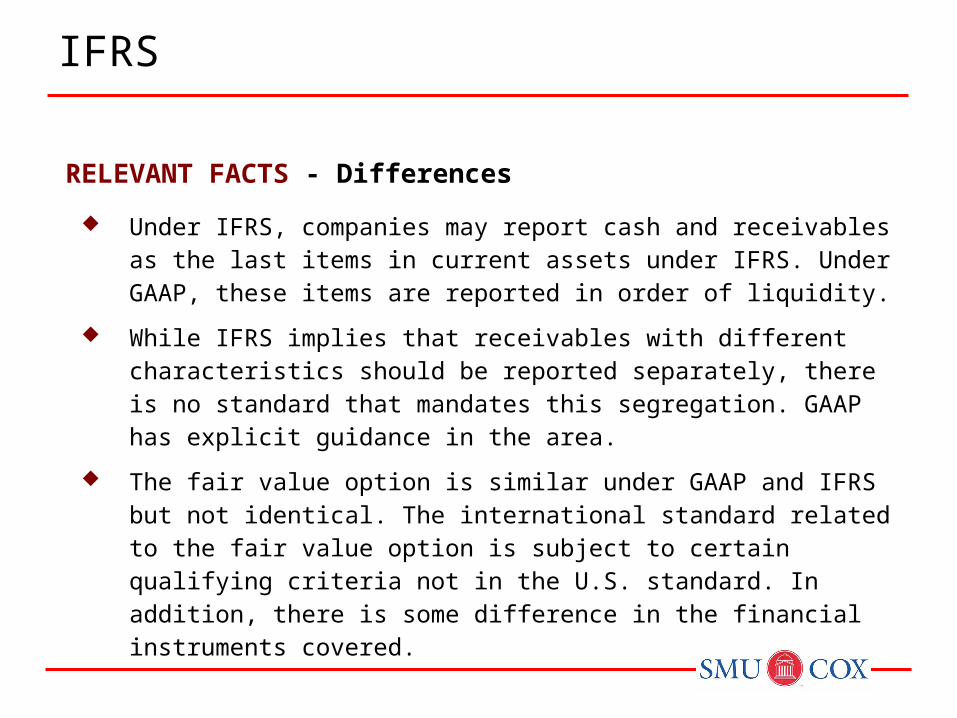

RELEVANT FACTS - Differences

Under IFRS, companies may report cash and receivables as the last items in current assets under IFRS. Under GAAP, these items are reported in order of liquidity.

While IFRS implies that receivables with different characteristics should be reported separately, there is no standard that mandates this segregation. GAAP has explicit guidance in the area.

The fair value option is similar under GAAP and IFRS but not identical. The international standard related to the fair value option is subject to certain qualifying criteria not in the U.S. standard. In addition, there is some difference in the financial instruments covered.

IFRS

RELEVANT FACTS - Differences

Under IFRS, bank overdrafts are generally reported as cash. Under GAAP, such balances are reported as liabilities.

IFRS and GAAP differ in the criteria used to account for transfers of receivables. IFRS is a combination of an approach focused on risks and rewards and loss of control. GAAP uses loss of control as the primary criterion. In addition, IFRS generally permits partial transfers; GAAP does not.

IFRS

Receivables Journal Entries

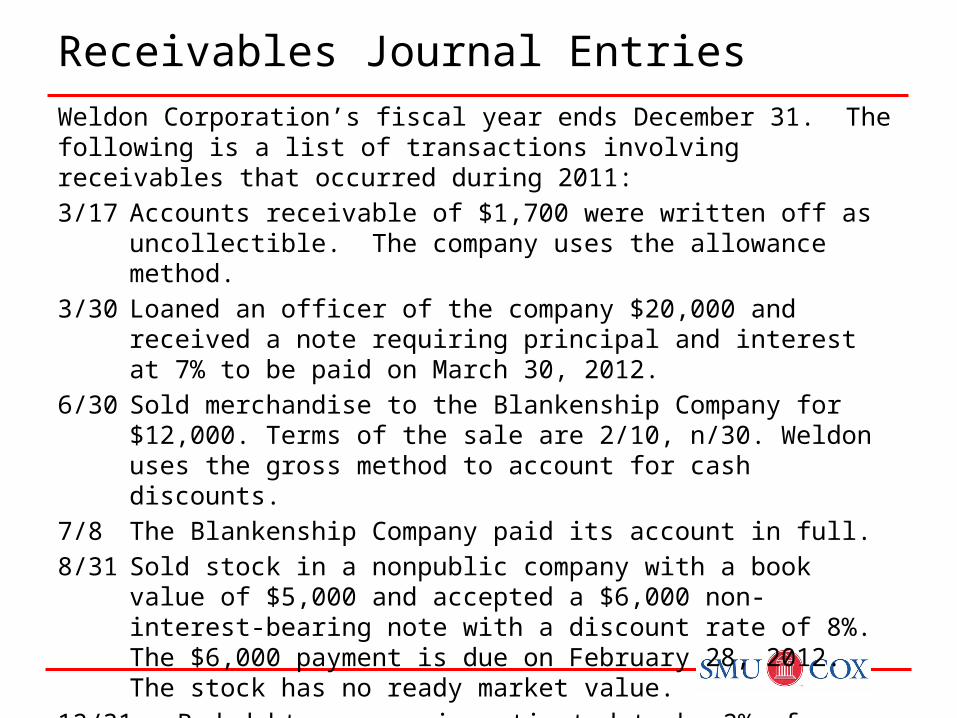

Weldon Corporation’s fiscal year ends December 31. The following is a list of transactions involving receivables that occurred during 2011:

3/17 Accounts receivable of $1,700 were written off as uncollectible. The company uses the allowance method.

3/30 Loaned an officer of the company $20,000 and received a note requiring principal and interest at 7% to be paid on March 30, 2012.

6/30 Sold merchandise to the Blankenship Company for $12,000. Terms of the sale are 2/10, n/30. Weldon uses the gross method to account for cash discounts.

7/8 The Blankenship Company paid its account in full.

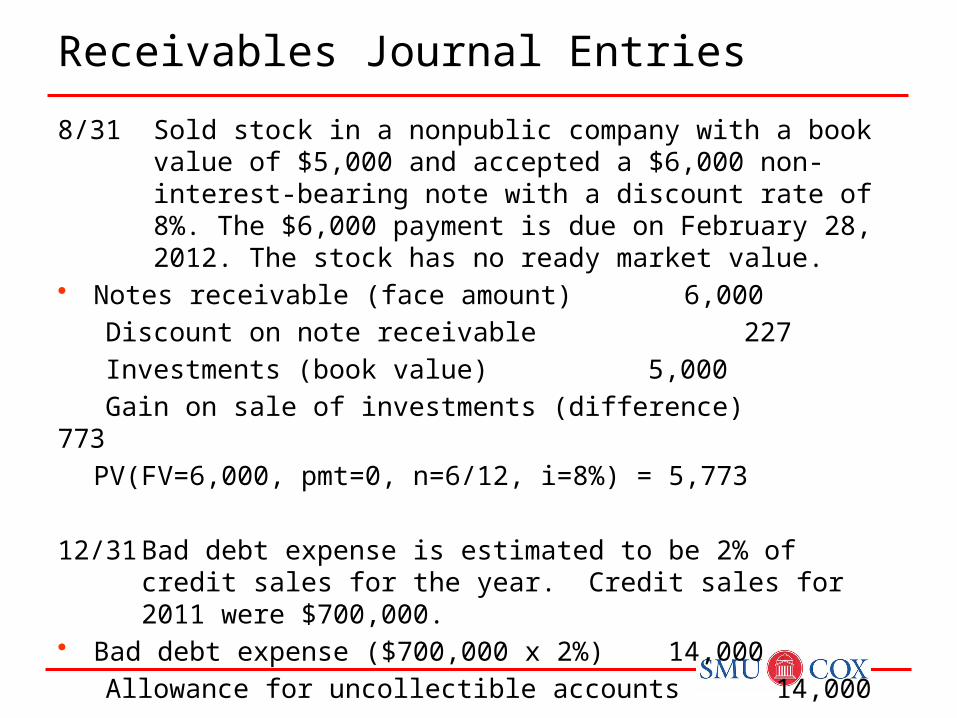

8/31 Sold stock in a nonpublic company with a book value of $5,000 and accepted a $6,000 non-interest-bearing note with a discount rate of 8%. The $6,000 payment is due on February 28, 2012. The stock has no ready market value.

12/31 Bad debt expense is estimated to be 2% of credit sales for the year. Credit sales for 2011 were $700,000.

Prepare all journal entries.

Receivables Journal Entries

3/17 Accounts receivable of $1,700 were written off as uncollectible. The company uses the allowance method.

• Allowance for uncollectible accounts 1,700

Accounts receivable 1,700

3/30 Loaned an officer of the company $20,000 and received a note requiring principal and interest at 7% to be paid on March 30, 2012.

• Note receivable 20,000

Cash 20,000

Receivables Journal Entries

6/30 Sold merchandise to the Blankenship Company for $12,000. Terms of the sale are 2/10, n/30. Weldon uses the gross method to account for cash discounts.

• Accounts receivable 12,000

Sales revenue 12,000

7/8 The Blankenship Company paid its account in full.• Cash ($12,000 x 98%) 11,760

Sales discounts ($12,000 x 2%) 240

Accounts receivable 12,000

Receivables Journal Entries

8/31 Sold stock in a nonpublic company with a book value of $5,000 and accepted a $6,000 non-interest-bearing note with a discount rate of 8%. The $6,000 payment is due on February 28, 2012. The stock has no ready market value.

• Notes receivable (face amount) 6,000

Discount on note receivable 227

Investments (book value) 5,000

Gain on sale of investments (difference) 773

PV(FV=6,000, pmt=0, n=6/12, i=8%) = 5,773

12/31 Bad debt expense is estimated to be 2% of credit sales for the year. Credit sales for 2011 were $700,000.

• Bad debt expense ($700,000 x 2%) 14,000

Allowance for uncollectible accounts 14,000

Receivables Journal Entries

Adjusting Entries:

To accrue interest earned on note receivable from loan to officer.• Interest receivable 1,050

Interest revenue ($20,000 x 7% x 9/12) 1,050

To accrue interest earned on note receivable from sale of stock.• Discount on note receivable 154

Interest revenue ($5,773 x 8% x 4/12) 154