excel techniques in the financial world - · pdf fileexcel techniques in the financial world...

TRANSCRIPT

Excel Techniques in the Financial World

Kevin Kwan CFA, FRM

Desktop Build Group APAC, Bloomberg LP

July 2015

2 | © 2015 Global Association of Risk Professionals. All rights reserved.

The views expressed in the following material are the author’s and do not

necessarily represent the views of the Global Association of Risk

Professionals (GARP), its Membership or its Management.

Getting the data

"An investment in knowledge pays the best interest.“

- Benjamin Franklin

Getting the data

4 | © 2015 Global Association of Risk Professionals. All rights reserved.

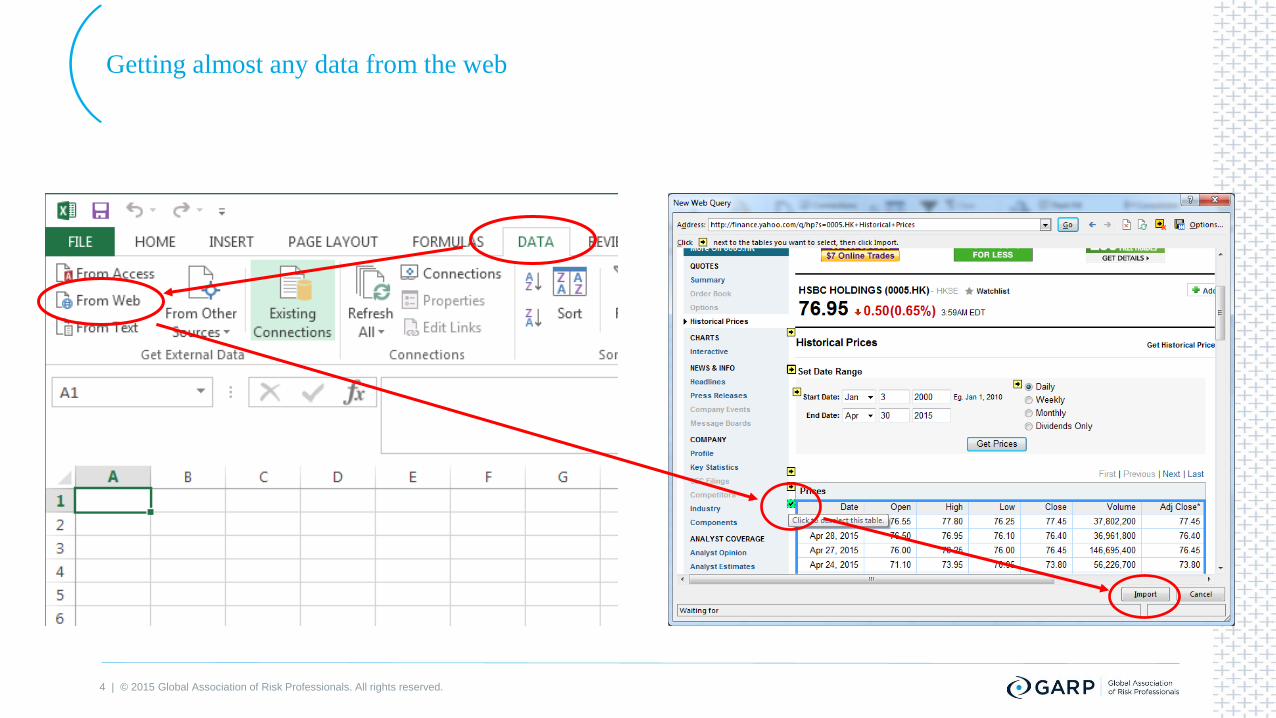

Getting almost any data from the web

5 | © 2015 Global Association of Risk Professionals. All rights reserved.

Getting almost any data from the web

6 | © 2015 Global Association of Risk Professionals. All rights reserved.

Defines which security information you are obtaining (Eg. 5 HK

Equity). Each data vender might have different ticker convention

More formal way to obtain data and Common data request structure

Tickers

Fields Defines what information you are obtaining relating to the above

ticker. Each data vender likely to have different fields convention

Dates

Optional

Parameters

Optional: Defines the point-in-time data or the date range of

historical data

Optional: Defines other data characteristics

7 | © 2015 Global Association of Risk Professionals. All rights reserved.

Using Excel 2013 Webservice formula:

=WEBSERVICE( Data Source s=Ticker & f=Field)

Data Source – http://download.finance.yahoo.com/d/quotes.csv?

Ticker – 0005.HK (0005.HK is the Yahoo ticker for HSBC listed in HKEx)

Field – b2 (b2 is the field name for Ask Price in Yahoo. Refer to Annex)

Example:

=WEBSERVICE("http://download.finance.yahoo.com/d/quotes.csv?s=0005.HK&f=b2")

Getting Yahoo finance data service onto Excel

8 | © 2015 Global Association of Risk Professionals. All rights reserved.

Real time data: =BDP( Ticker , Field , [Optional Parameter(s)] )

Historical data: =BDH( Ticker , Field , Start Date, End Date, [Optional

Parameter(s)] )

Reference data sets: =BDS( Ticker , Field , [Optional Parameter(s)] )

Example: =BDH("5 HK Equity","PX_Last", "20150505", "20150508") returns HSBC

historical price data from 5th May 2015 to 8th May 2015

Getting Bloomberg data onto Excel

9 | © 2015 Global Association of Risk Professionals. All rights reserved.

Drag and drop directly from FLDS to Excel

Bloomberg FLDS<GO>

Optimizing a

Portfolio

“The stock market is filled with individuals who know the price of

everything, but the value of nothing”

- Phillip Fisher

11 | © 2015 Global Association of Risk Professionals. All rights reserved.

Define your trading universe

This example will be benchmarked to HSI Index. Getting HSI members’ ticker and their

weighting, Annual Total Return and Volatility one year from now

Preparing to optimize your portfolio

=BDS("HSI Index", "INDX_MWEIGHT_HIST",

"END_DATE_OVERRIDE=20140526”

=BDP(A4 & " Equity",

"CUST_TRR_RETURN_HOLDING_PER",

"CUST_TRR_START_DT=20130526"),

"CUST_TRR_END_DT=20140526")

=BDH(A4 & " Equity", "VOLATILITY_260D",

"20140526")

12 | © 2015 Global Association of Risk Professionals. All rights reserved.

Yahoo does not provide return volatility data but we could calculate from historical price.

Preparing to optimize your portfolio (Yahoo data)

Return=Close – Previous day Close

=STDEV.S(Return)*SQRT(250)*100

13 | © 2015 Global Association of Risk Professionals. All rights reserved.

Preparing to optimize your portfolio

Create a column to store the weighting

of your new portfolio. Initially could set

to equal weighted. (Eg. 2% each)

Approximated Sharpe Ratio for the

benchmark portfolio

Approximated Sharpe Ratio to be

optimized (this is calculated from the

portfolio weighting in column G)

14 | © 2015 Global Association of Risk Professionals. All rights reserved.

Enabling Solver Add-in in Excel Option

Optimization steps

15 | © 2015 Global Association of Risk Professionals. All rights reserved.

Optimization steps

16 | © 2015 Global Association of Risk Professionals. All rights reserved.

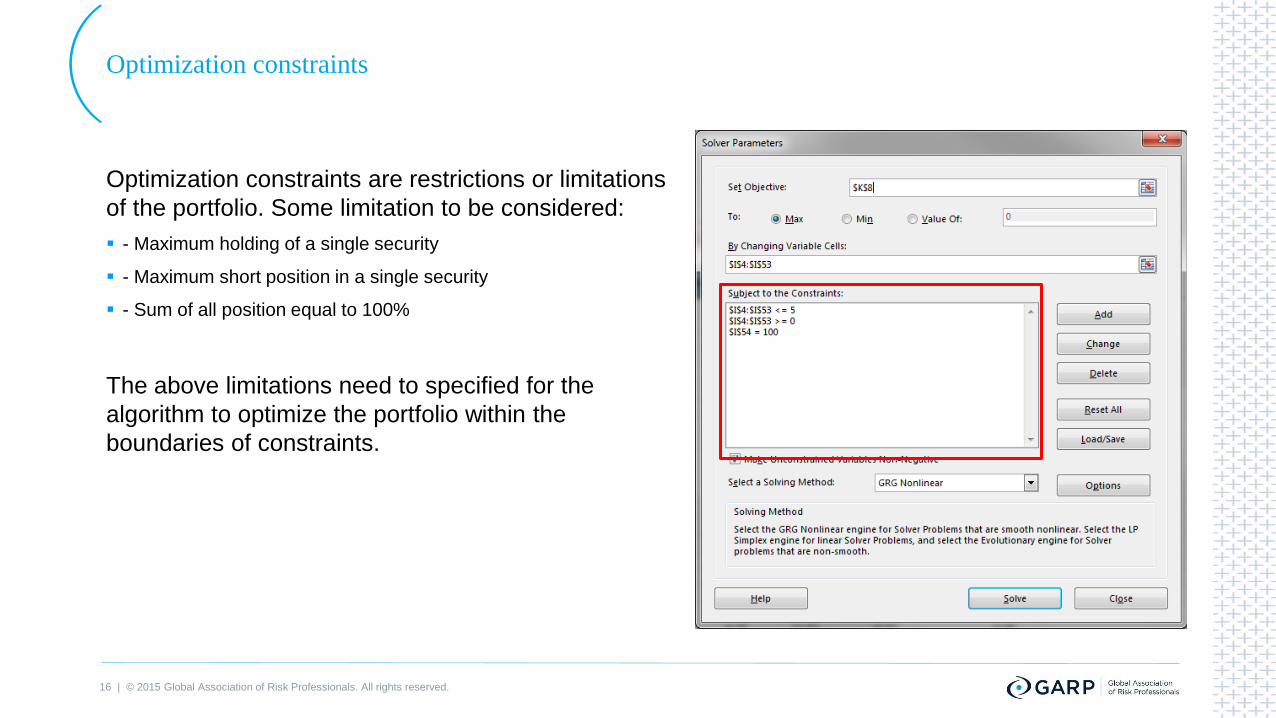

Optimization constraints are restrictions or limitations

of the portfolio. Some limitation to be considered:

- Maximum holding of a single security

- Maximum short position in a single security

- Sum of all position equal to 100%

The above limitations need to specified for the

algorithm to optimize the portfolio within the

boundaries of constraints.

Optimization constraints

17 | © 2015 Global Association of Risk Professionals. All rights reserved.

Optimized portfolio (no short position

allowed) using 12 months data 1 year

from now has a Approximated Sharpe

Ratio of 0.8. Optimized portfolio

suggested to hold:

5% of 11 HK

5% of 1199 HK

5% of 1 HK

etc

Optimized portfolio (no short position)

18 | © 2015 Global Association of Risk Professionals. All rights reserved.

Holding Per 5/27/2014 5/27/2015

HSI New Portfolio

Peroid Rtn% 22.39 31.23

Std. Dev 14.71 16.94

Sharpe 1.52 1.84

Optimized portfolio (no short position)

Return of Optimized Portfolio (no

short position) was 31.2% last

year comparing to HSI Index

return of 23.4%

19 | © 2015 Global Association of Risk Professionals. All rights reserved.

Optimized portfolio (short position

allowed) has a Approximated Sharpe

Ratio of 0.98 over a 12 months period 1

year from now and suggested to hold:

Short 2% of 101 HK

Long 5% of 1044 HK

Short 2% of 1088 HK

etc

**Note: In reality, some stocks are not available for

short selling and need to include these in the

optimization constraints

Optimized portfolio (with short position)

20 | © 2015 Global Association of Risk Professionals. All rights reserved.

Holding Per 5/27/2014 5/27/2015

HSI New Portfolio

Peroid Rtn% 22.39 40.72

Std. Dev 14.71 18.38

Sharpe 1.52 2.22

Optimized portfolio (with short position)

Return of Optimized Portfolio

(with short position) was 40.7%

last year comparing to HSI Index

return of 23.4%

21 | © 2015 Global Association of Risk Professionals. All rights reserved.

To set up a rebalance, add to columns to

define the MAX and MIN weighting of

each member in the new portfolio

For example, new weighting is ± 20% of

the original portfolio

Optimized portfolio (rebalance original weighting)

22 | © 2015 Global Association of Risk Professionals. All rights reserved.

Constraints for each portfolio member:

New Weighting of X <= Max allowed weighting of

X

New Weighting of X >= Min allowed weighting of X

Optimized portfolio (rebalance original weighting)

23 | © 2015 Global Association of Risk Professionals. All rights reserved.

Holding Per 5/27/2014 5/27/2015

HSI New Portfolio

Peroid Rtn% 22.39 28.12

Std. Dev 14.71 15.47

Sharpe 1.52 1.82

Optimized portfolio (rebalance original weighting)

Return of Optimized Portfolio

(with short position) was 28.1%

last year comparing to HSI Index

return of 23.4%

Annex 1: Some useful Excel templates

25 | © 2015 Global Association of Risk Professionals. All rights reserved.

Run XLTP<GO> on terminal

Bloomberg Excel Template Library

Key word search

Topic, Asset Classes, Role, and Geo

Filters

Click to view more details of the

template

Annex 2: Data Fields Tables

27 | © 2015 Global Association of Risk Professionals. All rights reserved.

Pricing Dividends

a: Ask y: Dividend Yield

b: Bid d: Dividend per Share

b2: Ask (Realtime) r1: Dividend Pay Date

b3: Bid (Realtime) q: Ex-Dividend Date

p: Previous Close

o: Open

Date

c1: Change d1: Last Trade Date

c: Change & Percent Change d2: Trade Date

c6: Change (Realtime) t1: Last Trade Time

k2: Change Percent (Realtime)

p2: Change in Percent

Yahoo data fields

Averages

c8: After Hours Change

(Realtime) m5: Change From 200 Day

Moving Average

c3: Commission m6: Percent Change From 200

Day Moving Average

g: Day’s Low m7: Change From 50 Day

Moving Average

h: Day’s High m8: Percent Change From 50

Day Moving Average

k1: Last Trade (Realtime) With

Time m3: 50 Day Moving Average

l: Last Trade (With Time) m4: 200 Day Moving Average

l1: Last Trade (Price Only)

t8: 1 yr Target Price

28 | © 2015 Global Association of Risk Professionals. All rights reserved.

Yahoo data fields (cont.)

Misc

w1: Day’s Value Change g1: Holdings Gain Percent

w4: Day’s Value Change

(Realtime) g3: Annualized Gain

p1: Price Paid g4: Holdings Gain

m: Day’s Range g5: Holdings Gain Percent

(Realtime)

m2: Day’s Range (Realtime) g6: Holdings Gain (Realtime)

52 Week Pricing Symbol Info

k: 52 Week High v: More Info

j: 52 week Low j1: Market Capitalization

j5: Change From 52 Week Low j3: Market Cap (Realtime)

k4: Change From 52 week High f6: Float Shares

j6: Percent Change From 52

week Low n: Name

k5: Percent Change From 52

week High n4: Notes

w: 52 week Range s: Symbol

s1: Shares Owned

x: Stock Exchange

j2: Shares Outstanding

Misc

w1: Day’s Value Change g1: Holdings Gain Percent

w4: Day’s Value Change

(Realtime) g3: Annualized Gain

p1: Price Paid g4: Holdings Gain

m: Day’s Range g5: Holdings Gain Percent

(Realtime)

m2: Day’s Range (Realtime) g6: Holdings Gain (Realtime)

52 Week Pricing Symbol Info

k: 52 Week High v: More Info

j: 52 week Low j1: Market Capitalization

j5: Change From 52 Week Low j3: Market Cap (Realtime)

k4: Change From 52 week High f6: Float Shares

j6: Percent Change From 52

week Low n: Name

k5: Percent Change From 52

week High n4: Notes

w: 52 week Range s: Symbol

s1: Shares Owned

x: Stock Exchange

j2: Shares Outstanding

29 | © 2015 Global Association of Risk Professionals. All rights reserved.

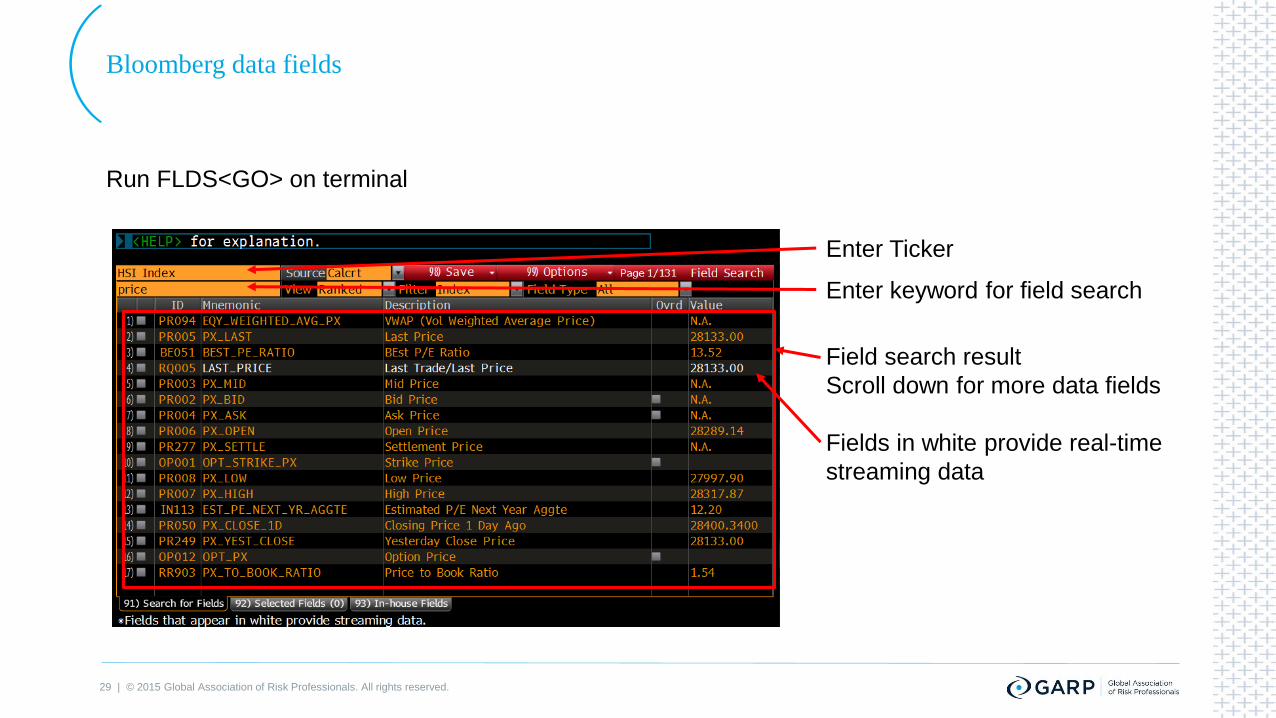

Run FLDS<GO> on terminal

Bloomberg data fields

Enter Ticker

Enter keyword for field search

Field search result

Scroll down for more data fields

Fields in white provide real-time

streaming data

Questions?

“Develop into a lifelong self-learner through voracious reading; cultivate

curiosity and strive to become a little wiser every day”

- Charlie Munger

31 | © 2015 Global Association of Risk Professionals. All rights reserved.

C r e a t i n g a c u l t u r e o f

r i s k a w a r e n e s s ®

Global Association of

Risk Professionals

111 Town Square Place

14th Floor

Jersey City, New Jersey 07310

U.S.A.

+ 1 201.719.7210

2nd Floor

Bengal Wing

9A Devonshire Square

London, EC2M 4YN

U.K.

+ 44 (0) 20 7397 9630

www.garp.org

About GARP | The Global Association of Risk Professionals (GARP) is a not-for-profit global membership organization dedicated to preparing professionals and organizations to make better informed risk decisions. Membership represents over

150,000 risk management practitioners and researchers from banks, investment management firms, government agencies, academic institutions, and corporations from more than 195 countries and territories. GARP administers the Financial Risk

Manager (FRM®) and the Energy Risk Professional (ERP®) Exams; certifications recognized by risk professionals worldwide. GARP also helps advance the role of risk management via comprehensive professional education and training for

professionals of all levels. www.garp.org.