ex-post evaluation of lebanon’s free trade agreements: the

TRANSCRIPT

19-00984

Distr.

LIMITED

E/ESCWA/EDID/2019/WP.13

13 September 2019

ORIGINAL: ENGLISH

Economic and Social Commission for Western Asia (ESCWA)

Ex-Post Evaluation of Lebanon’s

Free Trade Agreements:

The Cases of the FTA with the European Union

and PAFTA with the Arab Countries

United Nations

Beirut, 2019

© 2019 United Nations

All rights reserved worldwide

Photocopies and reproductions of excerpts are allowed with proper credits.

All queries on rights and licenses, including subsidiary rights, should be addressed to the United

Nations Economic and Social Commission for Western Asia (ESCWA), e-mail: publications-

The findings, interpretations and conclusions expressed in this publication are those of the

authors and do not necessarily reflect the views of the United Nations or its officials or Member

States.

The designations employed and the presentation of material in this publication do not imply the

expression of any opinion whatsoever on the part of the United Nations concerning the legal status

of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers

or boundaries.

Links contained in this publication are provided for the convenience of the reader and are

correct at the time of issue. The United Nations takes no responsibility for the continued accuracy of

that information or for the content of any external website.

References have, wherever possible, been verified.

Mention of commercial names and products does not imply the endorsement of the United

Nations.

References to dollars ($) are to United States dollars, unless otherwise stated.

Symbols of United Nations documents are composed of capital letters combined with figures.

Mention of such a symbol indicates a reference to a United Nations document.

United Nations publication issued by ESCWA, United Nations House,

Riad El Solh Square, P.O. Box: 11-8575, Beirut, Lebanon.

Website: www.unescwa.org.

iii

Acknowledgements

This report was prepared by the Regional Integration Section of the Economic Development and

Integration Division of the UNESCWA. The core team was led by Mohamed A. Chemingui, chief of regional

integration section, and included Badri Narayanan. G (GTAP Research Fellow) and Mehmet Eris (Economic

Affairs Officer at the regional integration section). Additional contribution was provided by Yasmine Arida

(intern at RIS/EDID/ESCWA).

v

Contents

Page

Acknowledgements ....................................................................................................................... iii Introduction ................................................................................................................................... 1

Chapter

A. The FTA with the European Union ............................................................................. 3 B. The PAFTA ................................................................................................................. 4

A. Macroeconomic and sectoral changes ......................................................................... 8 B. Trade impacts .............................................................................................................. 11 C. Foreign Direct Investments (FDIs) .............................................................................. 17

A. Implementation of the FTA with the European Union ................................................ 21 B. Implementation of GAFTA ......................................................................................... 22

A. Absence of financial integration and lack of intra-Arab investments ......................... 32 B. Declining mobility of the intra-Arab workforce .......................................................... 32 C. Weak agricultural and food security integration ......................................................... 32 D. Highly restricted trade in services ............................................................................... 33 E. Poor trade facilitation performance ............................................................................. 35 F. Poor economic diversification ..................................................................................... 38 G. Absence of a development strategy ............................................................................. 43 H. Poor competition policy............................................................................................... 44 I. Exchange rate policy ................................................................................................... 44 J. Fiscal pressure ............................................................................................................. 45

ANNEXES

I. Provisions of the Euro-Mediterranean Agreement with Lebanon ..................................... 47 II. GAFTA Provisions ............................................................................................................ 69

References...................................................................................................................................... 74

vi

Contents (continued)

Page

List of tables

1. Structure of Lebanese Government revenues ...................................................................... 10

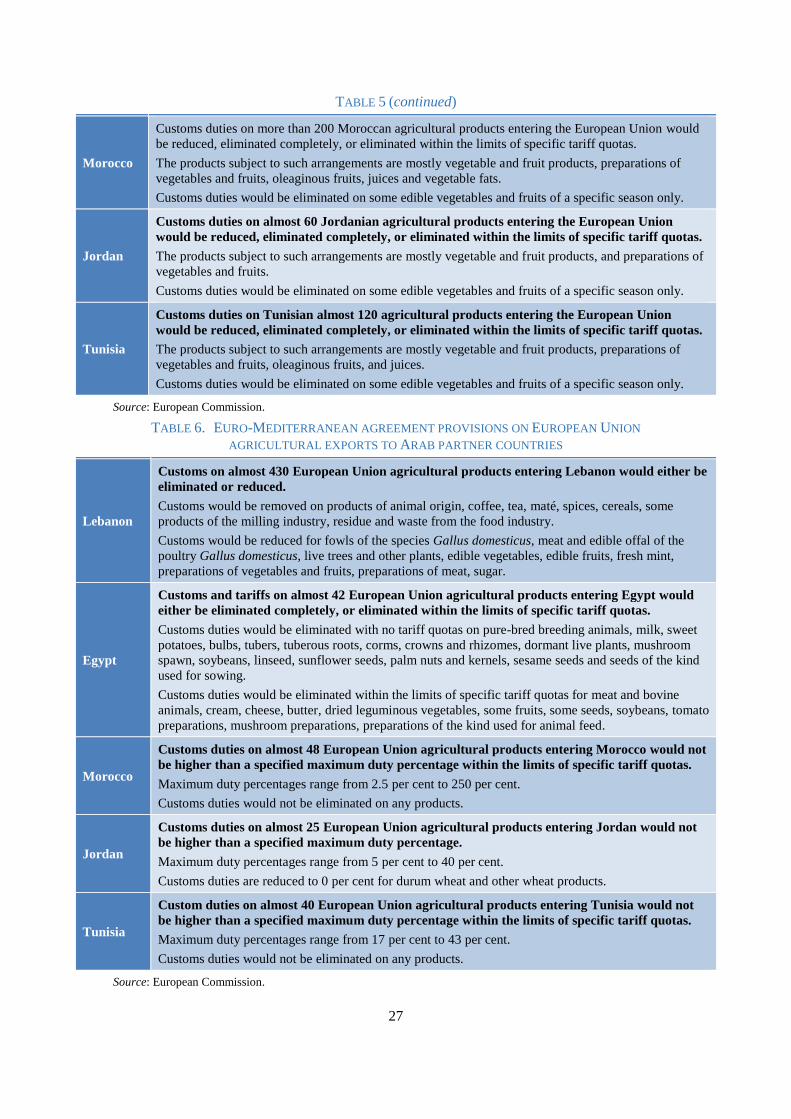

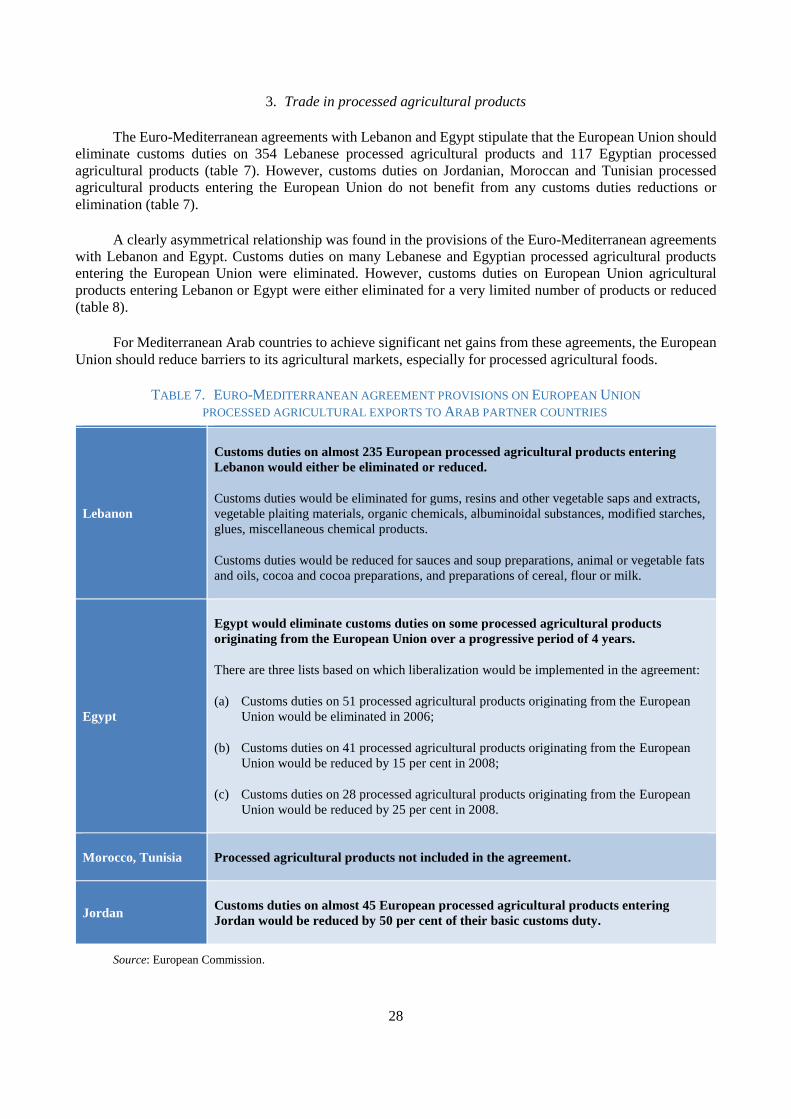

2. Product groups that have benefited from customs duty elimination ................................... 21

3. Product groups that have benefited from customs duty reductions ..................................... 21

4. Euro-Mediterranean agreement provisions on European Union industrial exports

to Arab partner countries ..................................................................................................... 25

5. Euro-Mediterranean agreement provisions on European Union agricultural imports

from Arab partner countries ................................................................................................ 26

6. Euro-Mediterranean agreement provisions on European Union agricultural exports

to Arab partner countries ..................................................................................................... 27

7. Euro-Mediterranean agreement provisions on European Union processed agricultural

exports to Arab partner countries ........................................................................................ 28

8. Euro-Mediterranean agreement provisions on European Union processed agricultural

imports from Arab partner countries ................................................................................... 29

9. Euro-Mediterranean agreement provisions on fishery products

from Arab partner countries ................................................................................................ 29

10. Euro-Mediterranean agreement provisions for trade in services ......................................... 30

11. Euro-Mediterranean agreement provision on payments and movement of capital ............. 30

12. Euro-Mediterranean agreement provisions on cooperation in social

and cultural matters ............................................................................................................. 31

13. STRI sin some sectors in Lebanon, and the overall measure compared

to those of other countries in the region .............................................................................. 33

14. Official exchange rate ......................................................................................................... 44

List of figures

1. GDP growth in Lebanon ..................................................................................................... 8

2. Share in GDP by economic sector in Lebanon .................................................................... 9

3. Household and NPISH consumption for Lebanon .............................................................. 9

4. Lebanon export shares ......................................................................................................... 14

5. Lebanon import shares ........................................................................................................ 14

6. Trade intensity index ........................................................................................................... 15

7. Trade complementarity between Lebanon and PAFTA member countries ........................ 15

8. Export diversification index ................................................................................................ 16

9. Export similarity index ........................................................................................................ 17

10. FDI flows, 1996-2017 ......................................................................................................... 17

vii

Contents (continued)

Page

11. Trends in Green Field FDI by major geographical origin:

the case of the service sector, 2003-2016 ............................................................................ 19

12. Trends in Green Field FDI by major geographical origin:

the case of the manufacturing and agricultural sectors, 2003-2016 .................................... 19

13. Service imports by Lebanon in constant dollars ................................................................. 34

14. Service exports by Lebanon in constant dollars .................................................................. 34

15. Trends in overall LPI score for Lebanon, 2010-2016 ......................................................... 35

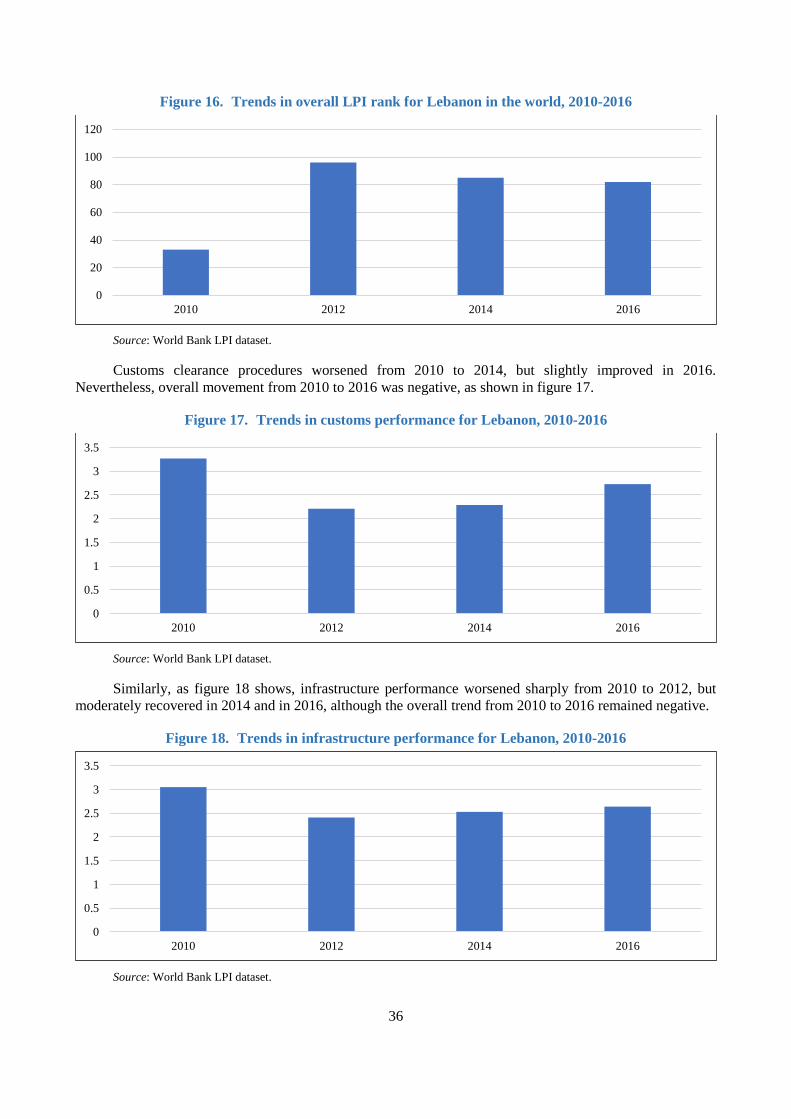

16. Trends in overall LPI rank for Lebanon in the world, 2010-2016 ...................................... 36

17. Trends in customs performance for Lebanon, 2010-2016................................................... 36

18. Trends in infrastructure performance for Lebanon, 2010-2016 .......................................... 36

19. Trends in international shipment performance for Lebanon, 2010-2016 ............................ 37

20. Trends in logistics quality and competence for Lebanon, 2010-2016 ................................. 37

21. Trends in tracking and tracing score for Lebanon, 2010-2016 ........................................... 37

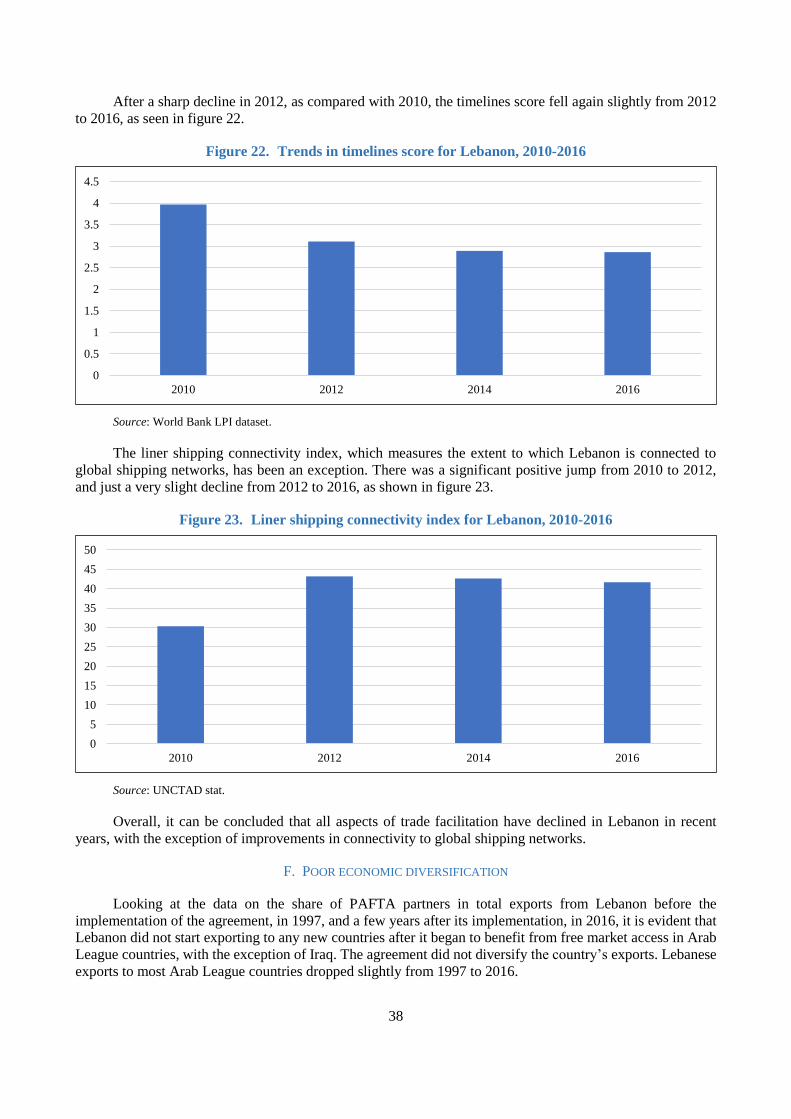

22. Trends in timelines score for Lebanon, 2010-2016 ............................................................. 38

23. Liner shipping connectivity index for Lebanon, 2010-2016 ............................................... 38

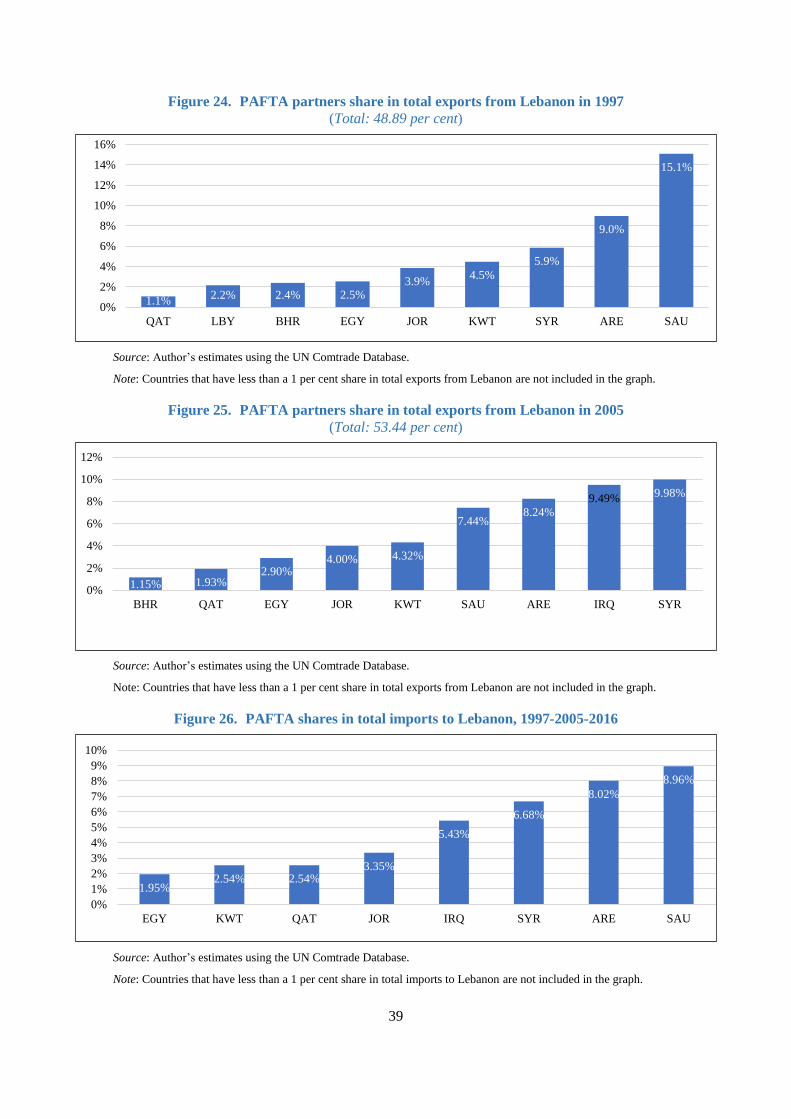

24. PAFTA partners share in total exports from Lebanon in 1997 ........................................... 39

25. PAFTA partners share in total exports from Lebanon in 2005 ........................................... 39

26. PAFTA shares in total imports to Lebanon, 1997-2005-2016 ............................................ 39

27. PAFTA partners share in total imports to Lebanon in 1997 ............................................... 40

28. PAFTA partners share in total imports to Lebanon in 2005 ............................................... 40

29. PAFTA partners share in total imports to Lebanon in 2016 ............................................... 40

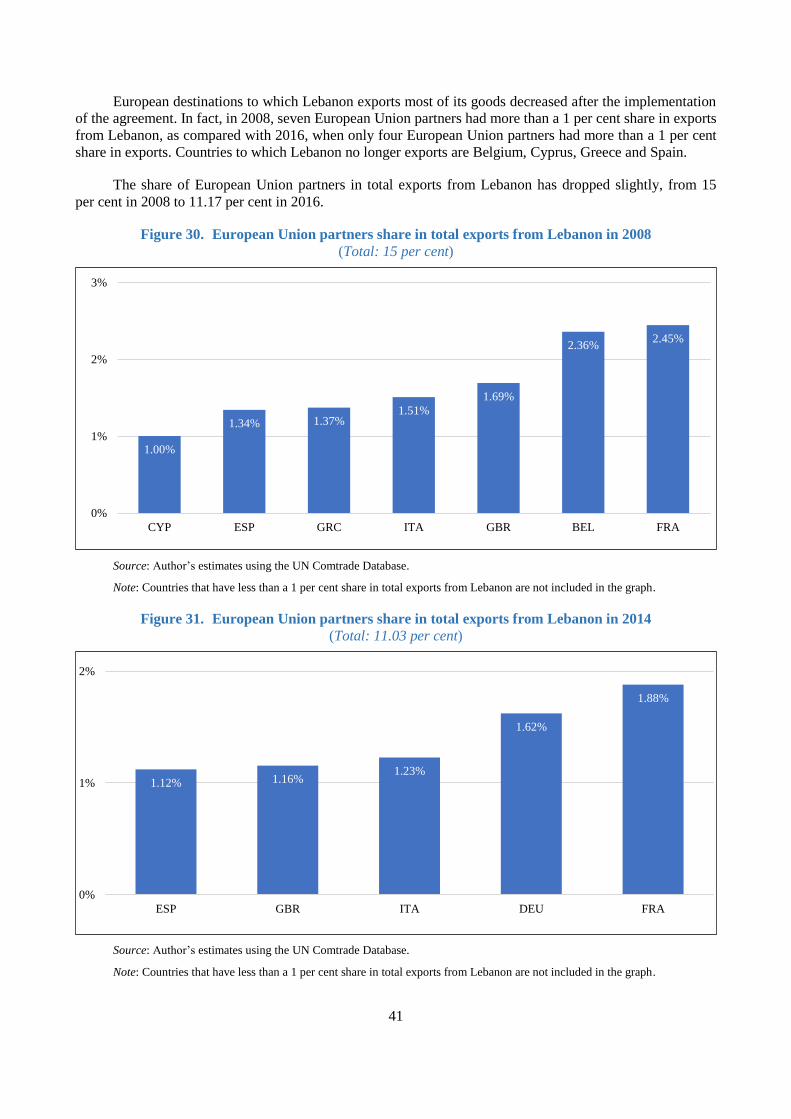

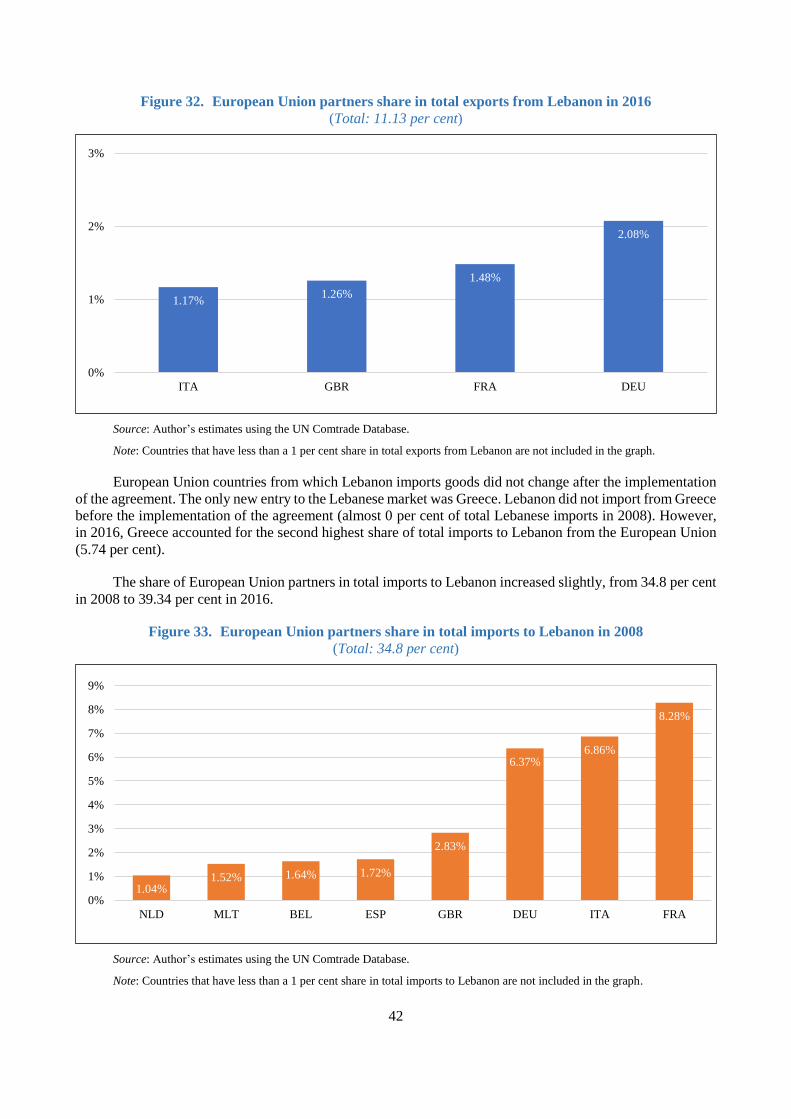

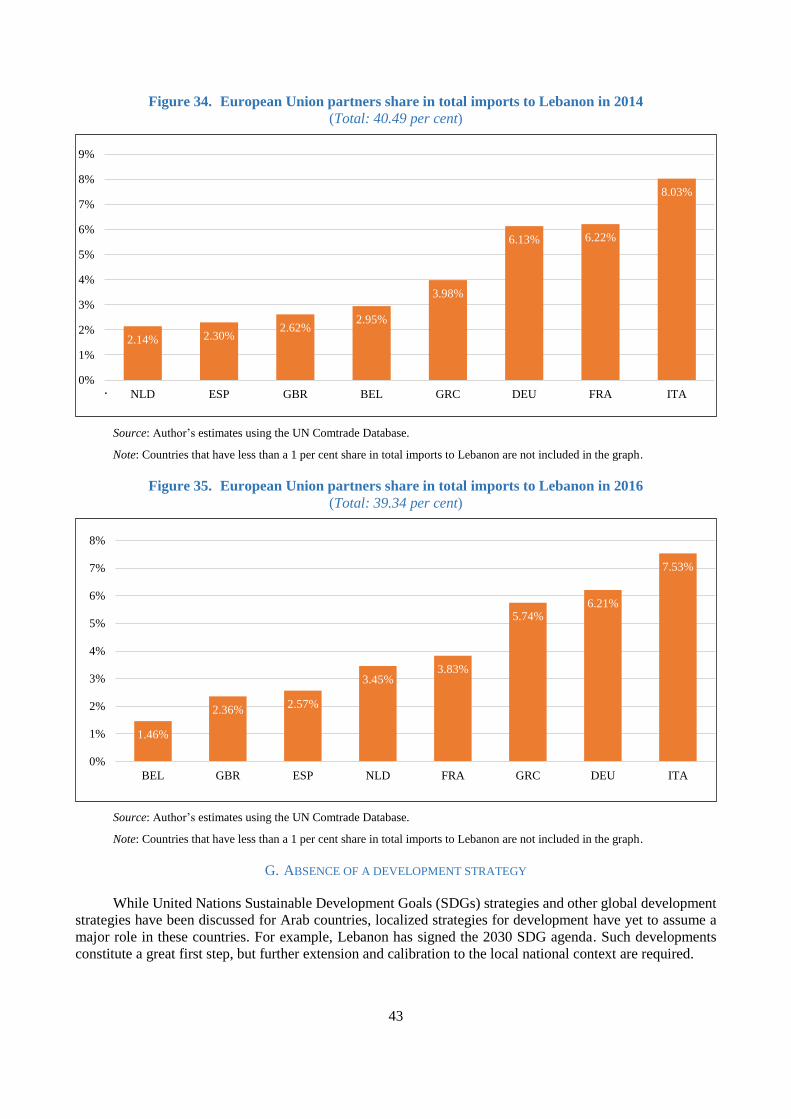

30. European Union partners share in total exports from Lebanon in 2008 .............................. 41

31. European Union partners share in total exports from Lebanon in 2014 .............................. 41

32. European Union partners share in total exports from Lebanon in 2016 .............................. 42

33. European Union partners share in total imports to Lebanon in 2008 .................................. 42

34. European Union partners share in total imports to Lebanon in 2014 .................................. 43

35. European Union partners share in total imports to Lebanon in 2016 .................................. 43

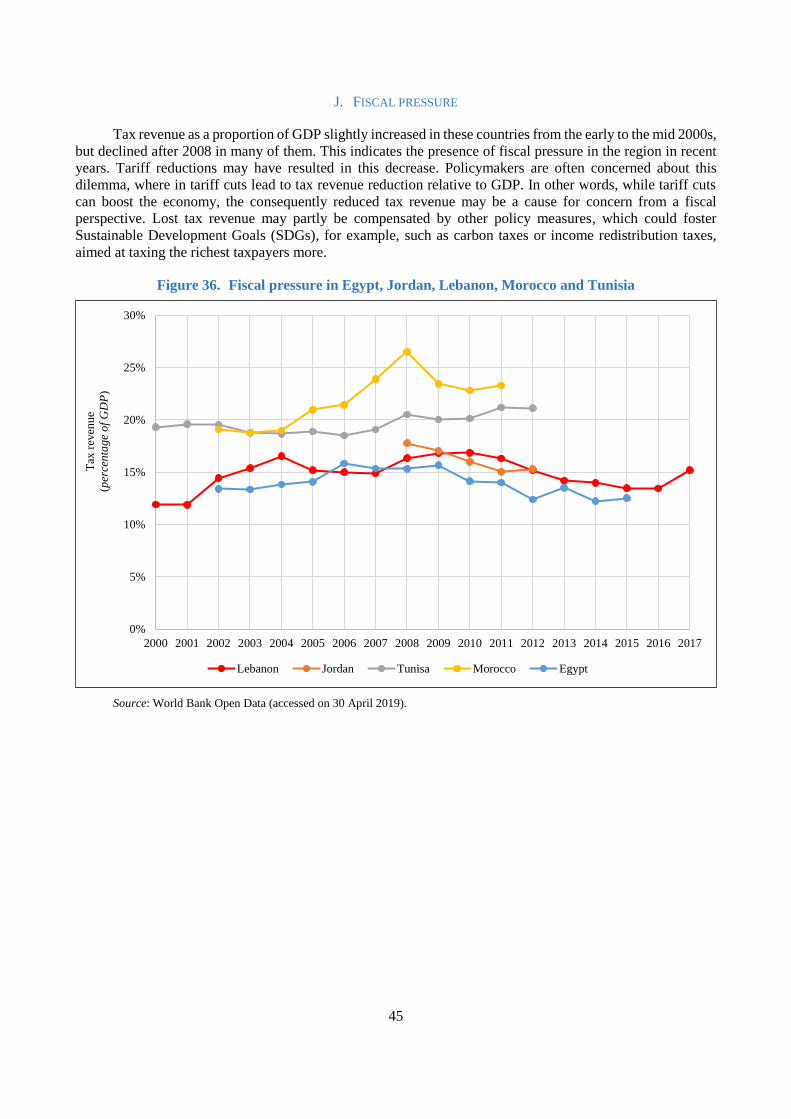

36. Fiscal pressure in Egypt, Jordan, Lebanon, Morocco and Tunisia ...................................... 45

Introduction

Compared with many Arab countries, Lebanon has traditionally had a relatively open trade regime.

Efforts towards trade liberalization have focused on the European Union (EU) and the Arab world. The free

trade agreement (FTA) with the European Union came into force in April 2006, and was gradually

implemented over the period 2008-2014. It provides for reciprocal free trade on most industrial goods, and

liberalizes trade on a wide range of raw and processed agricultural goods. In parallel with the FTA with the

European Union, Lebanon signed an FTA with the European Free Trade Association (EFTA) in 2004, and an

association agreement with Turkey in 2010, to establish a free trade area over the subsequent ten years.

The agreement has not yet been ratified. These two agreements, with the EFTA and Turkey, were meant

to be aligned with European Union trade policy, which is linked to the members of the EFTA and Turkey

through a Customs Union. Lebanon also signed the Greater Arab Free Trade Agreement (GAFTA) with

17 Arab countries.

At a time when Lebanon is being invited to take part in the second phase of deepening the Euro-Med

Partnership, national policy makers and private operators are looking at the country’s experience, with regard

to the agreement with the European Union implemented since 2006, as a learning phase before embarking on

effective negotiations to expand the FTA to a Deep and Comprehensive FTA (DCFTA). The DCFTA

represents the new wave of partnership initiated by the European Union with most of its partners in the Euro-

Med partnership. The DCFTA will be a comprehensive agreement on trade and economic relations, covering

a full range of regulatory areas, such as trade facilitation, technical barriers to trade, sanitary and phytosanitary

measures, investment protection, public procurement and competition policy. Its main objective will be the

progressive integration of the Lebanese economy into the European Union single market. This constitutes a

unique opportunity to further open up Lebanon and make it more competitive in global markets. The ultimate

objective is for Lebanon to strategically use its preferential partners to break into global markets, particularly

in a context where production increasingly takes place in global value chains. However, since its inception,

many European observers and analysts have regarded free trade with developing countries like Egypt, Jordan,

Lebanon, Morocco, and Tunisia, as a dangerous instrument that boosts the re-allocation of investments from

Europe to these countries, despite the fact that the latter already enjoyed free access to European markets for

most of their manufacturing exports. They envision European jobs being lost in a flood of goods from countries

with an average wage ranging from less than one-tenth to half that of most European countries (mainly France,

Germany, and Italy). Others see the Euro-Mediterranean Partnership (EMP) as a boon to European

employment and living standards, through greater trade and investment opportunities. For Arab countries,

these agreements provide, for the first time, reciprocal treatment of European exports to their markets, which

are considered serious competitors for their domestic manufacturing industries, and may contribute to

increased unemployment.

Today, the need to strengthen the economic performance of Arab countries has become essential,

especially in the aftermath of political upheavals and civil conflicts in the region. In essence, efforts not only

to come up with a well-structured agenda of agreements, but also to implement those agreements, could benefit

the Arab region on various economic, social, and political levels. In fact, as most national economies

progressively move away from import substitution policies to more open regimes, regional integration

arrangements have become increasingly important. Regional Integration Agreements (RIAs) not only serve

the purpose of gaining market access and ensuring a level playing field, but also constitute important vehicles

for achieving other objectives, which notably include strengthening regional cooperation and coordination and

locking in domestic reforms. Various theoretical and practical arguments have been put forward in the

literature in favor of regional economic integration. According to Baldwin and Venables,1 three categories of

economic effects are generated by RIAs: (a) static allocation of resources; (b) accumulation of productive

factors; and (c) spatial allocation of resources.

1 Baldwin and Venables, 1995.

2

Regional Arab economic integration is more than just a desirable plan for growth and development.

In fact, it has become a necessity for Arab economies to maintain a presence among other world economies.

According to a recent ESCWA report,2 statistics reveal that growth rates in the Arab region have been sluggish

over the past few decades. The report also indicates that the Arab region “remains poorly integrated into the

global economy, apart from the oil sector”. Sincere plans for regional integration could therefore help increase

the level of participation of the Arab world in the global economy by enhancing its competitive power.

Certainly, competitive power is better achieved when tasks are divided efficiently among countries, with each

holding expertise in a specific field, rather than having each country competing on an individual basis at all

marketing and production levels. In other words, specialization in production improves efficiency and

empowers Arab countries to compete with the rest of the world.

Benefits from regional economic integration would accrue to both high and low-income countries. While

rich Arab countries would benefit from lower costs of production and tariffs, poorer countries would diversify

their production base and decrease their unemployment rates. In a nutshell, strengthening intra-Arab

co-operation would help boost the region’s competitiveness and thus encourage foreign investments in local

Arab economies. This would greatly help nurture various economic sectors, especially the service sector, which

perfectly fits the requirements of the Arab region. More subtly, for many of the poorer Arab countries, the

service sector ultimately works better than the trade sector in terms of enriching the economy. Indeed, those

investments help create jobs, transfer technology and expertise, and improve equilibrium in the balance of

payments for poor countries.

In order to evaluate the ex-post implications of the FTAs with the European Union and with Arab

countries, it is important to highlight the specific nature of the two agreements and their importance for

Lebanon. These FTAs are based on the EMP and the Arab Trade Facilitation Agreement. The FTA with the

European Union is a different kind of partnership agreement, as compared with the kind that prevailed within

the European Union, and favored the free movement of workers and capital from wealthier countries to the

least-advanced nations so as to reduce economic disparities between members. As such, since its effective

implementation in 1995, the Euro-Med Partnership has been one of the most debated trade agreements.

Conflicting expectations for the Arab countries involved in the Euro-Med Partnership have widely been subject

to speculation, as a result of assessments of other trade agreements or of projections generated by simulation

models. But since the Free Trade component between the European Union and Lebanon has been fully in

operation since 2014, the question is not what this FTA is likely to deliver, but what it has delivered already.

Typically, the debate over FTAs across the world has focused on jobs. However, to really understand

the effects of FTAs on employment or living standards, it is important to first answer the most fundamental

question: what effect it has had on trade. Changes in trade patterns, caused by a lowering or complete removal

of trade barriers, are ultimately the mechanism by which jobs and living standards are affected, through

changes in production, specialization and diversification, productivity, investment, etc. This paper examines

how the FTAs with the European Union and with Arab countries have affected the Lebanese economy, based

on an assessment of what did and did not work for Lebanon. In addition, this paper contributes to the active

debate over how to approach current and upcoming negotiations on the DCFTA and the Arab Customs

Union (ACU).

This paper is organized as follows. The next section provides some basic background on the in-force

FTAs signed by Lebanon, with a special focus on the agreements with the European Union and with Arab

countries. The third section presents and discusses the major outcomes of the FTAs with both partners from

an ex-post perspective. The fourth section analyzes the shortcomings of these FTAs. The last section includes

an evaluation of the success of the two FTAs and discusses the way forward.

2 E/ESCWA/EDID/2017/6.

3

THE PROVISIONS OF THE TWO AGREEMENTS

A. THE FTA WITH THE EUROPEAN UNION

Except for Libya and the Syrian Arab Republic, all Arab countries that are involved in the Euro-

Mediterranean process have signed an FTA with the European Union (table 1). The process involved Algeria,

Egypt, Jordan, Lebanon, Morocco, the State of Palestine, and Tunisia.

On the whole, all the FTAs signed by the European Union with Arab partners display the same structure,

and include three main parts. The first concerns political and security cooperation, the second deals with trade

operations among partners, and the third with economic and cultural cooperation. The latter part of the Euro-

Med Partnership between the Arab countries involved and the European Union is dominated by general

declarations of principles, and does not include clear commitments. The trade component defines the

modalities of trade liberalization between the partners, through a mechanism of gradual tariff dismantlement

schemes associated with numerous products. Generally, under these FTAs, the European Union maintains the

existing preferences accorded to its Arab partners’ exports of manufactured products, with specific treatment

of agricultural trade for each country. At the same time, the Arab countries involved in the partnership process

commit themselves to eliminating all existing barriers to market access for most non-agricultural products

imported from European Union countries. Some Arab countries have gone beyond core product coverage, to

the partial liberalization of agricultural imports from the European Union. On a practical level, all the Arab

countries involved have chosen to implement tariff dismantlement in a gradual manner over a maximum

transition period of 12 years.

Depending on the specific level of sensitivity to European competition, the Arab countries involved

have organized their imports into various categories. In the case of Lebanon, under the previous trade and

cooperation agreements in effect since 1976, almost all Lebanese industrial exports had free access to European

Union markets. The FTA with the European Union stipulates that all Lebanese industrial products entering the

European Union should be allowed in free of customs duties and charges having equivalent effect (annex I,

table annex I.2), and that customs duties and charges having equivalent effect on imports into Lebanon of

products originating in the European Union should be progressively eliminated, in accordance with the

schedule adopted, with periods ranging from 5 to 12 years after the entry into force of the agreement (annex I,

table annex I.2). Quantitative restrictions and tariffs on numerous items, mainly equipment goods, are

eliminated immediately upon the agreement’s entry into force. However, the gradual implementation of the

agreement was later revised, and tariff dismantling was implemented during the period 2008-2014.

The provisions concerning agricultural products do not stipulate the full liberalization of trade in

agricultural, fisheries and processed agricultural products, but aim to strengthen the relationship in the future.

Under the agreement, all tariffs and quotas on Lebanese agricultural products entering the European Union

should be eliminated immediately upon its entry into force. However, several exceptions, listed in Protocol 1

of the FTA, do not fall within the scope of the agreement. Such exceptions include mostly vegetables, fruits,

nuts and wine from fresh grapes. Meanwhile, Lebanon commits to completely removing duties on some

agricultural and processed agricultural products, and to cut tariffs on others. Tariff cuts range from 20-50

per cent reductions in customs duties (annex I, table annex I.3).

Since 2012, the European Union has been ranked the top trading partner for Lebanon, covering 36.4

per cent of the country’s total trade in 2017. Trade provisions in the agreement not only confirm that free trade

in manufactured goods was already taking place, but also seek to reinforce it through dialogue in several related

areas. Notably, these include provisions for the freedom of establishment, free movement of capital, trade

facilitation and the approximation of legislation (annex I). The FTA also covers the liberalization of services,

the right of establishment, and an effective protection of commercial and intellectual property rights (annex I).

In addition, it goes well beyond the previous cooperation framework, and calls for the comprehensive

harmonization of the regulatory framework, with plans to phase out any practices that might disrupt trade

between the two parties. This includes monopolies, government subsidies, and privileges granted to public

4

enterprises. The agreement strengthens economic and financial cooperation, particularly in support of

industries that have faced difficulties in adjusting to trade liberalization, and with the aim to enhance

environmental protections. It also calls for the harmonization of standards and norms (in telecommunications,

transport, etc.), as well as rules and regulations concerning accounting and financial services, customs, and

statistics.3 Regarding trade in services, there are no specific provisions (annex I, table annex I.5). In fact,

European Union offers under the FTA usually go hand in hand with multilateral commitments made under the

General Agreement on Trade in Services (GATS). With the non-conclusion of the Doha Round, the DCFTA

initiative represents a second chance to boost bilateral cooperation between the European Union and Lebanon,

through the inclusion of all agricultural products and services.

B. THE PAFTA

On 3 June 1957, the League of Arab States4 signed the Arab Economic Unity Agreement, which sought

to achieve economic advancement and gains for its member States. The agreement included in its terms the

following items: regulations on tariff reduction; intra-Arab facilitation of capital and labor mobility; unification

of economic legislations on Arab trade, agriculture and service sectors, as well as ownership rights;

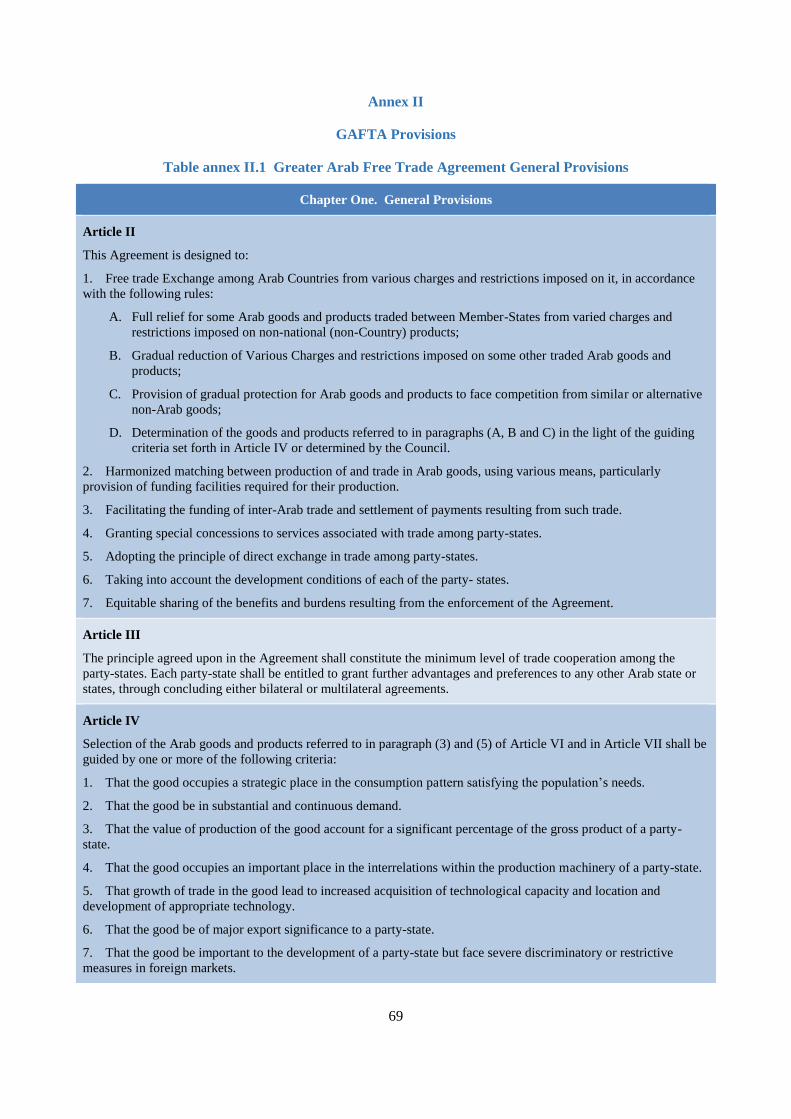

coordination of foreign trade policies; and promotion of foreign investments internally (annex II). Beginning

on 1 January 1998, tariff rates, fees, and taxes began to be reduced at an annual rate of 10 per cent. Certain

products were exempted from the execution program of GAFTA, being forbidden for religious, environmental,

security, and health reasons. As of 1 January 2005, the agreement reached full trade liberalization of

goods, through the full exemption of customs duties and charges having equivalent effect, among all GAFTA

member countries.

However, this agreement remained unimplemented to a large extent, mainly because achieving regional

economic integration would have had to be preceded by adjustments undergone on a smaller scale in the

member States.

Upon realizing that the Arab Economic Unity Agreement did not succeed in building coherent

foundations for achieving regional economic integration, Arab countries renewed their efforts at the Eleventh

Arab League Summit Conference, held in Jordan. Specifically, in 1980, they signed another economic unity

agreement known as the “Unified Agreement for the Investment of Arab Capital in the Arab States”. This

agreement, similar in nature to the Arab Economic Unity Agreement that preceded it, asserted the need to

reduce the Arab development gap not only with the rest of the world, but also between Arab countries. Its

major focus was facilitating labor transition within the Arab world, as well as creating incentives and benefits

for highly qualified Arab nationals to stay in their home countries or return to the region. Concerning

international relations, the agreement emphasized the importance of having economic investments directed

towards serving internal regional issues, such as the Palestinian cause. Uniting the Arab world against foreign

greed, achieving greater self-reliance, and eliminating colonialism, poverty and intellectual invasion, were also

at the core of its program.

Again, apart from minor efforts undertaken to ease the mobility of capital, services and labor, and to

facilitate intra-Arab investments in the region, sadly, many of this agreement’s items remained mere proposals

that were never put into effect. Subsequent attempts were made after the 1980 agreement, with the aim of

implementing the regional economic integration plan. Thus, in 1981, the League of Arab States signed the

“Agreement to Facilitate and Develop Trade among Arab States”. However, past causes of failure were left

un-addressed and thus the agreement faced obstacles with regard to trade facilitation that hindered it from

achieving any meaningful progress. Despite the establishment of the Arab Investment Court in 1985, which

3 Chemingui and Bchir, 2012.

4 The League of Arab States was founded in March 1945 and includes 22 member countries.

5

was mandated to oversee the items stipulated in the 1980 agreement, the committee formed by the court lacked

a well-structured roadmap for action and did not manage to integrate the region successfully.

It is worth noting that evidence from other integrated regions around the world – such as the European

Union, ASEAN and NAFTA – suggests that achieving effective economic integration is a gradual process that

needs to go through successive stages and is not immediately attainable.5 Such stages involve internal as well

as intra-regional changes and commitments for each of the member States. They also confirm that successful

integration does not require public declarations as much as it requires a coherent and organized set of gradual

steps towards achieving it. Taking this into consideration, a new perspective for uniting the Arab region was

adopted in 1997, mainly focused on establishing the Pan Arab Free Trade Area (PAFTA). Negotiations

conducted by the League of Arab States led to the decision that the agreement should be put into force in

gradual steps, and that each step should be thoroughly implemented before proceeding to further steps, in the

process of achieving economic integration.

The PAFTA agreement, as declared by fourteen Arab countries in 1997, was among the most important

agreements proposed for the Arab World, as it constituted the very first step towards integrating the region.

By 2006, eighteen out of twenty-two countries in the League of Arab States had signed the PAFTA agreement.6

The main concern of this agreement was to lift tariff and non-tariff barriers on intra-Arab trade, by means of a

yearly reduction of around 10 per cent of tariffs on goods, by 2007. In January 2005, earlier than the scheduled

timing, tariff removal was fully put into force, while Non-Tariff Barriers (NTBs) remained unaddressed to a

certain extent. In this context, the PAFTA agreement exempted less developed member countries, such as the

State of Palestine, the Sudan and Yemen, from bearing the burdens of customs duties. It also extended their

gradual tariff reduction on imports until 2012 rather than 2007.

PAFTA members were required to share trade data with each other for transparency purposes; and valid

documentation and records on existing transactions were to be clearly provided to the Economic and Social

Council. The latter, in turn, insured that the terms of the agreement were being fulfilled, and that member

States were honoring their commitments. In addition, the council was responsible for solving trade disputes

among Arab countries.

The liberalization of the service sector among member States was also considered, within the context of

implementation, in the PAFTA agreement. However, negotiations on trade in services between Arab countries

did not achieve any tangible results, not until late 2015. The reasons for this delay are connected to the wide

variations in service sector liberalization among PAFTA members.

Despite the fact that the implementation of the PAFTA agreement faced a range of obstacles, it is worth

noting that it did succeed in reaching several desirable goals, which will be discussed throughout the paper.

5 ASEAN refers to the Association of South-East Asian Nations. ASEAN was founded in 1967 and includes 10 South-East

Asian member countries. NAFTA refers to the North American Free Trade Agreement signed in 1994 between Canada, Mexico and

the United States.

6 The Comoros, Djibouti, Mauritania and Somalia did not sign the agreement.

6

LESSONS FROM THE EX-ANTE ASSESSMENTS OF THE IMPACT

OF THE FTAS WITH THE EUROPEAN UNION AND WITH ARAB

COUNTRIES ON THE LEBANESE ECONOMY

The study by Dessus and Ghaleb7 represents the first real attempt to model the Lebanese economy to try

to answer some of the key policy questions facing the Lebanese Government, something that had previously been

restricted to either partial equilibrium analysis or linear methods. They developed a computable general

equilibrium model to assess the full implications of a nexus of recent and upcoming fiscal and trade measures on

the domestic economy, the associated adjustment costs, and the welfare of consumers.

The model developed and used in this paper is static with imperfect substitution between domestic and

foreign goods. Prices are endogenous in each market (goods; factors), and they equalize supply (factors supply;

imports; Lebanese production intended for domestic markets) and demand (factors demand; intermediate demand

from producers; final demand from households, investors, Government, and the rest of the world), to obtain the

equilibrium. The latter is described as “general equilibrium”, in the sense that it simultaneously concerns all

markets. Imperfect competition is modeled by imposing a markup on marginal costs (for domestic products sold

on the domestic market) or on the domestic price of imports. Rents stemming from markups accrue to the

suppliers of the goods, be they domestic (the Lebanese representative household) or foreign (in the form of capital

income transfers). The rent is distributed among foreign and local suppliers, in proportion to their respective

market shares on the domestic market.

In calibrating for the imperfect structure of markets, a composite weighted competitiveness index was first

calculated, using the database of multiple HHI indicators from a 2003 study by the Lebanese Ministry of

Economy and Trade. The markets surveyed were then reclassified from the ISIC nomenclature to meet the

European national accounts nomenclature, and the composite index was subsequently calculated. A set of

simulations were performed, of which the main results can be summarized as follows.

The first scenario examines the static effects of simple tariff reduction scenarios on the economy, and

specifically on the fiscal budget of the Lebanese Government. With tariffs reduced by half, results show that

imports become cheaper on the domestic market. They are shown to grow by 3 per cent, as compared with the

benchmark scenario. But this is insufficient to maintain tariff receipts, which decrease by 47 per cent. As a result,

government revenue decreases by 17 per cent. Growth only modestly picks up: exports grow significantly (+12

per cent), but from a low base. The allocative efficiency of the economy (and the business environment) is

improved, but in the absence of productivity growth or additional investment, it is insufficient to foster greater

activity (-0.3 per cent real output, +0.1 per cent GDP). Investment drops because government savings drop, thus

crowding out private savings. The winner here (at least in the short run) is the household, which sees its

purchasing power grow by 2.6 per cent; but the public deficit increases, since the drop in tariff receipts is not

compensated by an increase in other fiscal revenues (stemming from the choice of the closure rule). From a

sectoral point of view, some sectors suffer directly from lower protection (e.g., furniture, nonmetallic products),

others benefit from cheaper imported and domestic inputs (e.g., textiles). Construction services suffer from lower

investment, and other sectors (e.g., services and utilities) benefit from greater domestic demand.

The second scenario assumes greater competition through a reduction of the markup on foreign goods,

which is the ultimate goal of any trade integration initiative. In fact, the specialized literature concedes that trade

agreements which lead only to tariff reduction result in poor static or dynamic gains from trade. The gains would

be multiplied if NTBs were removed or reduced. However, most studies, when examining NTBs, consider

variables such as red tape, transaction costs, standards and norms, but rarely characterize the lack of competition

as a typical NTB that can also act as an obstacle to free trade and economic growth. This is the case in Lebanon,

with the continued implementation of the law of exclusive agencies and the existence of imperfect market

structures, as highlighted by the authors, both of which lead to rent-seeking behavior (price markup) and thus

hinder free trade and reduce efficiency. This reduction of markup could for instance be achieved by eliminating

exclusive import agencies. As a direct result, imports become cheaper at the border (like the effect of positive

terms of trade). Imports grow by 2 per cent in real terms, which increases tariff receipts by a similar relative

7 Dessus and Ghaleb, 2006.

7

amount. Capital income outflows (the rent accruing to foreign suppliers) decrease, relaxing the balance of

payment constraints. As a result, exports decrease as well, with producers shifting their production towards the

domestic market. Output grows by 0.2 per cent (and real GDP by 0.3 per cent), as a result of a positive terms of

trade effect and improved allocative efficiency (less distortion). Unlike in scenario 1, market liberalization is

accompanied by an improved fiscal position. From a sectoral vantage point, sectors which were in competition

with protected imports suffer from increased competition. This is the case for non metallic products.

In a third scenario, markup on domestic goods is reduced by half, which could be achieved by greater

financing access for SMEs, domestic markets de-segmentation, pro-competition policies, or any other measure

the Government of Lebanon might be planning to implement. In this case, the domestic demand for Lebanese

products increases sharply. Imported products become less competitive (-2 per cent); producers also shift their

production towards domestic markets (exports decline by 8 per cent). Real private consumption grows, but as the

price of consumption drops, nominal consumption declines slightly, which explains why government revenue

(VAT receipts) declines. This effect is compounded by the decline in imports, which are taxed more than

domestic goods. One important and interesting effect is the increase in the remuneration of factors of production:

with an increased demand for domestic products (and constant productive capacities), wages and return to capital

both rise by some 5.8 per cent. In some respects, the hypothesis that rent-seeking behavior depresses productivity,

and leads to a production possibility frontier that is below international levels, is shown to be correct. At the

sectoral level, outputs in sectors that were previously shielded from competition grow, as the demand for their

products grows. Some sectors suffer indirectly from the macro impact of the reform: trade, as import and export

volumes drop, and construction, as investment drops (because final consumption becomes cheaper).

The last scenario assumes increased competition domestically and on import activity, which is a

combination of the two previous scenarios. The impact of raising domestic competition is significant on economic

activity and real per capita income (+1.8 per cent). The combination of the two policies is close to the sum of the

two policies taken independently. And, contrary to the tariff reduction scenario, it is not fiscally painful. Nominal

wages and return to capital increase by 6.1 per cent and 6.0 per cent respectively.

Contrary to all studies financed by the European Union commission to assess the impact of the Euro-Med

Partnership on the Arab economies involved, the findings of this paper make it very clear that no economic

improvements can be expected if the association agreement is limited to removing tariffs on imports from the

European Union. The existing setup of exclusive agents leaves the consumer, as well as the government, as the

main loser. However, while the consumer has no say in the pricing policy or the contract signed between the

agent and the exporter, and is therefore just paying a price higher than the marginal cost, the government does

have a say, but is nevertheless not benefiting from any of the rent it is indirectly creating by protecting exclusive

contracts. If exclusive agents and other manifestations of imperfect market structures cannot be properly

addressed by policy-makers, with the aim of promoting increased competition, economic principles and

reasoning should drive the government to tax the rent generated by the private Lebanese agents dominating

market activity.

There have been some gravity-based studies on the potential impact of PAFTA on the economy in general

and on trade in particular in Lebanon. For example, Yigezu and others8 assess the impact of PAFTA on trade in

all its members, from 1995 to 2007. While the aggregate PAFTA intra-regional trade has increased, this study

concludes that Lebanon and the Syrian Arab Republic are the only members that have seen positive effects on

both imports and exports, with Lebanon in particular tending to import more than it exports. Babili and Baghasa9

find less evidence for improvements in intraregional trade as a result of PAFTA. Asserting that tariff reduction

is not sufficient although it is necessary, these authors recommend the introduction of more profound measures,

such as on rules of origin, and reductions in non-tariff barriers. In this section, a detailed and comprehensive ex-

post assessment of the impact of PAFTA is conducted. It is based on actual outcomes, rather than forecasts or

simulated figures. The objective is to verify to what extent PAFTA has delivered on its promises, and what

reasons the deviation could be attributed to.

8 Yigezu and others, 2013.

9 Babili and Baghasa, 2008.

8

EX-POST ASSESSMENTS OF THE TWO FTAS

A. MACROECONOMIC AND SECTORAL CHANGES

1. Changes in the structure of the economy

The Lebanese economy has grown by 4.4 per cent annually on average between 1971 and 2016. In 2016,

the country’s GDP increased by 2 per cent, showing a significant decrease in growth, compared with as recently

as 2009, when GDP grew by 10.1 per cent. Tourism in Lebanon is one of the most important sectors for the

country’s economy, and due to civil wars and Israeli occupation, the tourism industry has been declining,

causing GDP growth to fall. In fact, most of the decline in growth can be attributed to the instability in the

region. The Syrian conflict has caused a ripple effect in Lebanon, with more than a million refugees in the

country today. Constant warfare has forced the government to allocate most of its resources to reconstruction

efforts, leading to higher public debt, with fiscal deficits at around 7 to 10 per cent. Currently, the debt to GDP

ratio is 150 per cent. Foreign investments have also decreased due to instability and corruption, further

hampering the economy.

The banking sector has taken a large hit as well. Lebanon has historically relied on Lebanese diaspora

deposits, at times making up 40 per cent of its GDP. Investments have recently slowed down to a halt, due to

investors being concerned about the Syrian conflict surrounding the country.

The Lebanese economy primarily relies on banking and tourism, which constitute 80.76 per cent

of the GDP. It is also structured around the role played by expatriates from abroad. Remittances account

for a significant proportion of bank deposits. The industrial sector only contributes 14 per cent to the

GDP, which indicates that the economy relies on external income. The agricultural industry is the country’s

largest internal sector, exporting 46 per cent of its production, but the country remains at a trade deficit in

the sector.

Figure 1. GDP growth in Lebanon

Source: Authors’ computations using the World Bank Open Data. Available at https://data.worldbank.org/ (accessed on

15 April 2019).

1.34%

3.84%

3.42%

3.23%

6.29%

2.75%

1.70%

9.34%9.25%

10.06%

8.04%

0.92%

2.80%

2.65%1.97%

0.24%

1.74%1.53%

0%

2%

4%

6%

8%

10%

12%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Gro

wth

rat

e

9

Figure 2. Share in GDP by economic sector in Lebanon

Source: Authors’ computations using the World Bank Open Data. Available at https://data.worldbank.org/ (accessed on

15 April 2019).

2. Shares of private consumption and exports in GDP

Private consumption in Lebanon represented 87.6 per cent of the country’s GDP in 2017. It has stayed

consistently at around 80 to 86 per cent of the GDP since 1998. Exports represented 23.6 per cent of the GDP

of Lebanon in 2017,10 down from around 37 per cent during the years 2004-2006, prior to the FTAs. Still, this

shows that Lebanon is an open economy, exporting a fourth of the value of the goods produced in the economy.

Although it is an open economy, private consumption represents a much larger portion of the GDP, as most

goods produced are bought and sold internally. This is also consistent with the country’s massive trade deficit,

of €6.4 billion with the European Union in 2016, and a total of $15.68 billion.

Figure 3. Household and NPISH consumption for Lebanon

Source: Authors’ computations using the World Bank Open Data. Available at https://data.worldbank.org/ (accessed on

15 April 2019).

10 World Bank, Open Data.

0%

10%

20%

30%

40%

50%

60%

70%

80%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sh

are

in G

DP

Agriculture Manifacturing Services

84.1%83.9%

83.0%

84.8%

83.3%

81.9%

84.7%

85.6%

87.9%

84.1%

87.6%88.4%

88.7%

85.2%

89.6%

86.5%

88.5%

87.5%

76%

78%

80%

82%

84%

86%

88%

90%

92%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Ho

use

ho

ld a

nd

NP

ISH

co

nsu

mp

tio

n

(per

cen

tag

e o

f G

DP

)

10

3. The trade agreements and public finances

Tax revenues represented around 14 per cent of GDP in Lebanon in 2016, down from 16.7 per cent in

2004. The dependence of the Lebanese Government on tax revenues is significant, but has fallen over time.

TABLE 1. STRUCTURE OF LEBANESE GOVERNMENT REVENUES

In LL Million

2000 2005 2010 2013 2014 2015 2016 2017

Total Domestic Revenue 4 188 000 6 984 000 12 018 000 13 385 000 14 742 000 13 635 721 13 989 252 16 247 075

Tax Revenue of which: 2 936 000 4 867 000 9 976 000 10 116 000 10 388 000 10 330 195 10 597 42 12 380 657

Direct Taxes of

which: 774 000 1 461 000 3 138 000 3 703 000 4 040 000 4 066 540 4 139 590 5 614 400

Taxes on Income 500 000

203 000 400 000 636 000 704 000 734 449 764 376 839 231

Taxes on Profits 841 000 1 417 000 1 865 000 2 091 000 1 897 615 2 249 580 3 361 009

Taxes on Property 274 000 414 000 1 088 000 1 201 000 1 245 000 1 179 240 1 124 490 1 413 100

Indirect Taxes of

which: 1 970 000 3 164 000 6 385 000 5 940 000 5 853 000 5 780 398 5 889 801 6 242 035

Domestic Indirect Taxes

of which: 220 000 1 896 000 3 583 000 3 782 000 3 811 000 3 716 577 3 772 856 4 079 027

VAT - 1 693 000 3 193 000 3 296 000 3 302 000 3 158 782 3 233 902 3 475 606

Excises - - - - - - - -

Other 220 000 192 000 382 000 477 000 500 000 548 703 531 401 592 220

Imports Indirect Taxes

of which: - 787 000 1 992 000 1 341 000 1 276 000 1 350 476 1 410 617 1 438 783

VAT - - - - - - - -

Excises - 787 000 1 992 000 1 341 000 1 276 000 1 350 476 1 410 617 1 438 783

Other - - - - - - - -

Customs or Import

Duties 1 750 000 481 000 810 000 817 000 766 000 713 345 706 328 724 225

Source: Authors’ calculations using the data from the Ministry of Finance of Lebanon. Available at

http://www.finance.gov.lb/en-us (accessed on 15 April 2019).

4. Weak job creation

Job creation in Lebanon continues to be weak and a persistent problem. The labor market is characterized

by low employment rates and activity. Youth employment is key to resolving this problem moving forward,

as it concerns the next generation of skilled workers. Today, with the Syrian crisis, the outlook in the labor

market has further worsened, as refugees are predicted to add 30 to 50 per cent to the labor force.

The country’s poor job creation is partly due to the lack of an economic development plan. If a plan

were put in place, it would foster economic activity, creating high-skill and high-wage jobs. In 2013, 5,000

new jobs were created, but there were 32,000 new entrants to the job market. Most of the economy in Lebanon

consists of the private sector. 90 per cent of Lebanese businesses are small to medium sized enterprises (SMEs).

The preferred form of employment in Lebanon is self-employment, with 36 per cent of the labor force being

self-employed (and 88 per cent of them preferring to remain self-employed). Additionally, 20 per cent of

workers are informal wage employees. Such employees have low productivity and lack access to insurance

programs and social security, creating a problem of regulations and economic structure.

11

Another characteristic of the Lebanese job market is its emigration rate of high-skilled laborers.

Although the number of university graduates in the country is increasing, the skills acquired by such graduates

do not match the needs of local corporations. Due to the high cost of higher education, graduates’ wage

demands are much higher than what is being offered in the domestic job market. As a result, a majority of

them emigrate to countries that offer competitive wages and benefits for their skill level. Meanwhile, a majority

of immigrants are Syrian and Palestinian refugees, and most of them are low-skilled workers with low

productivity. Around 40 per cent of the labor pool consists of workers who have no education to only primary

education. This creates a skill mismatch,with employers looking for high-skilled workers, and most of the

latter emigrating to other countries for better wages. Local youth also lack access to an adequate education

system, leading to a high number of high school dropouts. This creates a large pool of low-skilled individuals

looking for jobs, with the number of jobs created in this sector being far smaller than the pool. Although a

majority of job creation is low-skilled, the emigration of high-skilled citizens and the high rate of high school

dropouts have created a shortage of high-skilled applicants and an overabundance of low-skilled labor. This

mismatch in skills has caused 41 per cent of employees to engage in tasks above their education level. It has

also placed constraints on the growth of businesses, as 55 per cent of corporations state that the education level

of available labor is inadequate for their needs.

An increase in the productivity of firms is required to increase the job creation rate. Start-ups represent

the largest source of job creation, with 177 per cent of aggregate net job creation accounted for by start-up

firms. 66,000 jobs were created by such companies in the period 2005-2010. When such firms prosper, the job

market becomes more productive. With just a 1 per cent increase in firm productivity, there is a 3.9 per cent

increase in job creation. However, the lack of proper infrastructure limits the ability of start-ups for growth.

To obtain electricity, firms have to wait an average of 56 days and experience over 50 power outages

per month. The lack of consistent policy development and implementation causes firm managers to spend

12 per cent of their working time with government entities discussing policy creation, thus decreasing the

overall productivity level of firms.

B. TRADE IMPACTS

The only available studies on how the FTA with the European Union affects jobs, trade, and growth in

Lebanon were carried out either before the implementation of the agreement or at the beginning of the

implementation period. As a result, all of them are forward-looking. This contrasts with the backward-looking

approach of this paper. The techniques used to determine the future impact of the FTA fall into two broad

categories. The only available ex-ante study, carried out by the World Bank, clearly shows that Lebanon should

not expect any major gains if the trade agreement with the European Union is limited to tariffs.

Unlike the Dessus and Ghaleb study,11 which sought to predict how reducing or removing tariffs on

imports would affect the economy of Lebanon, this paper’s intent is to determine how the FTA has already

affected it. To assess the effects of the FTA, changes in major economic variables are empirically estimated

with pre- and post- FTA data. The analysis is based on estimating the changes that have occurred in the

economy of Lebanon since the implementation of the FTA began. However, this type of analysis has two

shortcomings. First, the analysis would attribute all changes to the implementation of the FTA with the

European Union, when Lebanon implemented many other economic reforms and trade agreements with other

partners during the same period. Second, most of the changes in Lebanese trade policy occurred during the

final years of the agreement’s implementation phase. Against these shortcomings, the present analysis has at

least two advantages. First, the analysis can estimate trade flows and changes in other major economic

variables, utilizing data gathered since the implementation of major trade commitments with the European

Union. Second, it can also capture most of the potentially important aspects of the FTA, including tariff and

non-tariff reductions, as well as changes in administrative rules, regulations, and expectations about the

11 Dessus and Ghaleb, 2006.

12

sustainability of free trade that cannot easily be quantified. Gould12 argues that changing expectations for the

sustainability of free trade are potentially among the most important aspects of an FTA. If the FTA does not

create a credible commitment to free trade, new investment will not flow into export industries to take

advantage of reduced trade barriers. Without a credible FTA, the benefits would be much lower. Expectations,

for a more stable and open trading environment, affect trade by providing the incentive for firms to make long-

term capital commitments. Those expectations cannot easily be accounted for using the methodology cited

previously, because it is difficult to translate them into price changes.

Using trade data at the six digit level of the harmonized system of product calassiciation (HS6) level, an

ex-post assessment was made over three different periods of time: prior to the implementation of the FTA with

the European Union, during the implementation period, and after its full implementation.

Prior to the implementation of the FTA with the European Union, total exports from Lebanon in 2005

amounted to $11.3 billion. Exports to European Union countries totaled $3.6 billion, representing 31 per cent

of all exports. Total imports from the European Union amounted to $3.8 billion, with Lebanon running a deficit

of $200 million. The largest European Union export partner was Italy, at $54.5 million. Lebanon imported the

most from France, with a valuation of $971.2 million, representing a quarter of imports from the European

Union. Precious stones and natural pearls were the primary exports, at $223.4 million in value, and the top

import was mineral fuels at $1.98 billion. The True Strength Indicator (TSI) measures trade momentum and

valuation trends. The TSI in 2005 was -0.122, which indicates that trade was trending down, and that the value

of goods was decreasing. The export diversification index quantifies the diversification of commodities

exported by the country. In 2005, the index stood at 0.738. The index being close to 1 indicates that Lebanese

exports are highly concentrated in a few sectors or commodities. The lack of diversification of exports is due

to the country relying heavily on automobiles, electrical machinery, technological equipment and precious

metals for its primary exports. The trade intensity index, which indicates whether the country exports more to

a given destination than the world does on average, was 0.337 in 2005 between Lebanon and the European

Union. This relatively low index means that exports to the European Union from Lebanon were not significant,

relative to exports to the European Union from the rest of the world, prior to the FTA.

During the implementation period, while exports from Lebanon increased by a billion dollars between

2005 and 2010, imports from the European Union increased by $1.19 billion over same period, to reach $4.99

billion in 2010, causing Lebanon to run a trade deficit of $390 million, from a surplus of $590 million in 2005,

prior to the implementation of the FTA. The export diversification index remained consistently the same as

before the implementation, which indicates that the country’s export portfolio did not improve. Unlike the

diversification index, the trade intensity index increased to 0.595. The increase in trade intensity from Lebanon

to the European Union is a positive indication that the FTA increased the ratio of Lebanese exports relative to

total world exports to the European Union. France was the largest European Union export partner at $349

million. Lebanon imported the most from Italy at $1.39 billion. The top export and import sectors did not

change during this period. Although the FTA was not yet fully implemented in 2010, the increase in trade

value between Lebanon and the European Union was trending positively towards policy goals. From the

perspective of the Lebanese economy, the FTA decreased the trade surplus and turned it into a

trade deficit.

Finally, after the full implementation of the FTA in 2014, Lebanon’s total exports in 2016 were at $15.3

billion. The 28 European Union countries accounted for $4.8 billion, or 30 per cent, of Lebanon’s exports.

Imports from the European Union were valued at $4.93 billion. Lebanon ran a trade deficit of $130 million

with the European Union. Compared with the period of implementation, the country’s European Union partner

exports increased by $300 million, and imports from the European Union stayed relatively constant, as they

only decreased by $30 million. When compared with the period prior to the FTA, on the other hand, exports

increased by $1.2 billion and imports increased by $1.13 billion. The trade balance decreased from prior to the

FTA, with the deficit increasing by $330 million, but decreasing from the implementation period by $260

12 Gould, 1998.

13

million. Turkey was the top European Union export partner at $71 million, and Lebanon imported the most

from Italy at $1.4 billion.

The FTA did not improve export diversification in Lebanon. Greater investments and the internal

development of new industries are necessary to improve diversification. The trade intensity index stood at

0.346, which is consistent with its value prior to the FTA, but represents a decrease of almost 40 per cent from

the implementation period. The large increase in trade intensity in 2010 could be an anomaly. If the FTA is

causing an increase in trade, the index should increase, as the greater the index, the greater the valuation of

exports from Lebanon to European Union countries. Judging from the True Strength Index, the momentum of

trade has been positive, as compared with the period prior to implementation, but has declined significantly

from the implementation period. The TSI partner index in 2016 was 0.149, compared with 0.407 during

implementation and -0.122 prior to the FTA. An increase of the index by 130 per cent from prior to the FTA

tells us that trade between the European Union and Lebanon is gaining momentum and the valuation of goods

is increasing. The implementation of the FTA increased trade between Lebanon and the European Union.

Although the policy has been positive up to this point, effectively accomplishing the policy goal, it has not

improved Lebanon’s economic trade performance. Exports did increase by 33 per cent relative to prior to

implementation, but the increase in imports outpaced the increase in exports. As a result, the trade surplus

Lebanon ran in 2005 was eliminated and became a deficit. The free trade agreement improved total trade

balance but did not benefit the Lebanese economy as much as expected.

Regarding the FTA with Arab countries, the situation is quite different. During the implementation

period of the agreement (1998-2004), the value of average exports from Lebanon to Arab countries was

$17.492 billion. Exports contributed 8.4 per cent of yearly GDP. The three categories of exports were

commercial service, service and goods exports. Commercial service and service exports both represented 45

per cent of total exports, valued at $7.88 million each. Goods exports represented the remaining 10 per cent of

exports, at $1.707 million. Average total imports was at $19.311 billion, which represents 36 per cent of GDP.

Commercial service and service imports accounted for 31 per cent of imports at $6 billion, respectively. Goods

imports were valued at $7.28 billion. During the implementation period, Lebanon ran a trade deficit of $1.8

billion with Arab countries. Looking at trade on a yearly basis, exports increased by 2.1 times in value from

2002 to 2004, from $10.19 billion up to $21.55 billion. Imports increased at a similar rate, by 1.97 times from

$12.82 billion to $25.5 billion. The trade deficit increased by $1.8 billion from 2002 to 2004. Although trade

increased due to the implementation of PAFTA, it did not help improve the trade performance of Lebanon

with Arab countries. However, after the full implementation of PAFTA, average yearly exports reached $34.05

billion and imports reached $39.95 billion. This represents a significant increase, of $16.5 billion and $20.64

billion, respectively. Exports increased from $24.07 billion in 2005 to $33.78 billion in 2016, peaking at $41.86

billion in 2011. Exports averaged 11 per cent of GDP, an increase of 3 per cent, but trends have been negative

since 2008, dropping from 15 per cent to 7.4 per cent in 2016. Imports also increased from $24.72 billion to

$44.14 billion. Imports averaged 43 per cent of GDP, an increase of 7 per cent, but have also been decreasing

since 2008, falling to 20 per cent in 2016. The decrease in the contribution of exports and imports to GDP is

due to the GDP itself having steadily increased. The average trade deficit was $5.9 billion. The free trade

agreement has created a base which has stimulated trade between Lebanon and Arab countries. The increase

in average trade deficit by $4.1 billionraises some concerns, as the post-PAFTA situation has harmed the

Lebanese economy, increasing government debt. The deficit peaked in 2016 at $10.36 billion. The trade deficit

has only increased every year since the elimination of tariffs on intra-Arab trade. The continued increase in

trade value after PAFTA indicates that the trade agreement has successfully stimulated trade. The increase in

deficit shows that reformsinLebanese economic policy are necessary.

Figure 4 below shows that, after reaching a maximum share in total exports of goods in 2004, exports

to Arab countries dropped significantly, to less than 50 per cent in 2016. However, during the period

2000-2016, Arab countries still represented the major export destination for the country.

14

Figure 4. Lebanon export shares

Source: Author’s estimates at HS6 digit level using Trade Map database (2017).

In terms of imports, the European Union still represents the major supplier for Lebanon, with its share

in total imports ranging from 55 per cent to around 65 per cent. Imports from PAFTA member countries did

not experience a significant increase since its implementation, with a share ranging between 23 per cent and

17 per cent during the period 2000-2016. This shows that the implementation of PAFTA since 2005 has not

affected the provenance and destination of Lebanon’s foreign trade (figure 5).

Figure 5. Lebanon import shares

Source: Author’s estimates at HS6 digit level using Trade Map database (2017).

15

The trade intensity index captures whether the value of trade between a country and its partners is greater

or smaller than would be expected on the basis of their importance in world trade. Lebanon has traditionally

traded more intensively with PAFTA countries than the world trade share of PAFTA as a bloc. More recently,

African countries have gained considerable ground, and today they are more important trade partners for

Lebanon than their world trade share might suggest (figure 6). The trade intensity index was at 15.284 in 2005,

which indicates a very strong trade relationship between Lebanon and Arab countries. A high index means that

Lebanon exports a greater amount to Arab countries than the rest of the world does on average. The abnormally

large values reflect geographic proximity, as all PAFTA countries are geographically close to Lebanon, and

relatively isolated from other markets.

Figure 6. Trade intensity index

Source: Author’s estimates at HS6 digit level using the UN Comtrade database.

The trade complementarity index captures how well the structures of a country’s exports and its partner’s

imports match, showing the extent of prospects for further exchange. The index takes a value of 0 when

no goods are exported by one country or imported by the other, and a value of 1 when export and import shares

match exactly. Increasingly, the index has been reaching relatively higher values with PAFTA (figure 7).

Figure 7. Trade complementarity between Lebanon and PAFTA member countries

Source: Author’s estimates at HS6 digit level using the UN Comtrade database.

0

2

4

6

8

10

12

14

16

18

ASEAN EU28 NAFTA PAFTA RestAfrica RestAmerica RestAsia

1995 2000 2005 2010 2016

16

The True Strength Indicator in 2016 was at 0.86352, and it decreased after the full implementation of

the agreement. Although trade value increased, the decrease in the TSI indicates that the increase in trade value

is partially due to the inflation of the dollars and the lower value of the Lebanese pound relative to the latter.

The trade intensity index averaged 11.78 during this period. The decrease after implementation shows that the

free trade agreement played an important part in intensifying the value of exports to Arab countries.

The true strength indicator in 2002 was at 0.94, which backs our trade values. The value being closer

to 1 means that trade is growing, and represents a positive trend in the long term. During the period of

implementation of PAFTA, intraregional trade intensity between Lebanon and PAFTA member countries

averaged 286.7. The intensity index trended upwards from 241.1 in 2001 to 328.7 in 2004. The increase in the

index, as the free trade agreement was being phased in, indicates that trade between Lebanon and PAFTA

members was increasing, and that their trade relationship was improving. The average intraregional trade share

for Lebanon stood at 0.17 during this period. There was once again a positive trend in the index, which

increased from 0.16 to 0.20. This matches the increase in intraregional trade intensity, as an uptick in imports

and exports within the region from Lebanon would increase the ratio of intraregional trade valuation to overall

world trade.

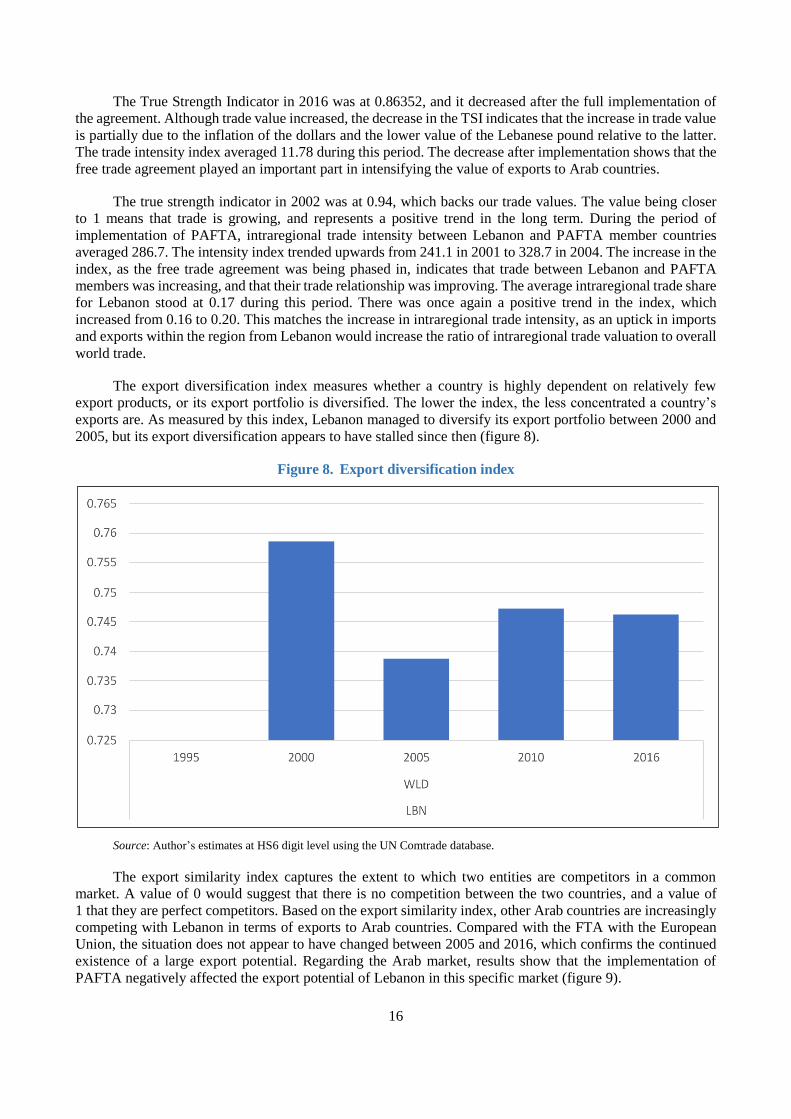

The export diversification index measures whether a country is highly dependent on relatively few

export products, or its export portfolio is diversified. The lower the index, the less concentrated a country’s

exports are. As measured by this index, Lebanon managed to diversify its export portfolio between 2000 and

2005, but its export diversification appears to have stalled since then (figure 8).

Figure 8. Export diversification index

Source: Author’s estimates at HS6 digit level using the UN Comtrade database.

The export similarity index captures the extent to which two entities are competitors in a common

market. A value of 0 would suggest that there is no competition between the two countries, and a value of

1 that they are perfect competitors. Based on the export similarity index, other Arab countries are increasingly

competing with Lebanon in terms of exports to Arab countries. Compared with the FTA with the European

Union, the situation does not appear to have changed between 2005 and 2016, which confirms the continued

existence of a large export potential. Regarding the Arab market, results show that the implementation of

PAFTA negatively affected the export potential of Lebanon in this specific market (figure 9).

17

Figure 9. Export similarity index

Source: Author’s estimates at HS6 digit level using the Comtrade database.

C. FOREIGN DIRECT INVESTMENTS (FDIS)

Since 2008, Lebanon has witnessed a rather significant decrease in FDI inflows, which reached their

lowest level in 2015. However, FDI inflows have been gathering pace, although slowly, since 2016. FDI

outflows, on the other hand, are much more muted in general, but showed a considerable increase in 2013.

It is only starting in 2015 that the tendency began to change (figure 10).

Figure 10. FDI flows, 1996-2017

Source: Author’s estimates using the UNCTAD 2018 World Investment Report.

0

0.05

0.1

0.15

0.2

0.25

2005 2016

EU28 PAFTA

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

-1

1

3

5

7

9

11

13

15

17

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

WLD

LBN

FDI outflows (right axis) FDI inflows (left axis)

18

Figure 10 clearly shows that no direct links could be observed between the implementation of PAFTA

and the flows of FDIs. Thus, a closer look at the inflows of FDIs from the Arab region is investigated using

the latest available figures.

During the implementation phase of the agreement (1998-2004), yearly foreign direct investment

averaged $1.7 billion from PAFTA member States. Capital inflows were trending positively, increasing from

$993.5 million in 2000 to $1.9 billion in 2004. As a proportion of GDP, FDIs fluctuated heavily, peaking at

14.25 per cent in 2003, and hitting their lowest point at 5.75 per cent in 2000. Out of 17 projects over a two-

year period, 4,165 jobs were created. Half of total investments came from the United Arab Emirates, with a

capital expenditure of $1.1 billion for 9 projects. The United Arab Emirates invested heavily in the real estate

and hotels and tourism sectors, with $546.3 million and $455.8 million in investments, respectively. Saudi

Arabia and Kuwait invested $557.6 million and $503.7 million, respectively. There was a large investment in

the real estate sector from Saudi Arabia, worth $546.3 million. The two largest capital expenditures were in

the real estate sector, totaling $1.093 billion. Kuwait invested $477.9 million in the hotels and tourism sector.

The latter was the second highest capital expenditure sector, totaling $933.3 million. Iran was the other country

to invest in Lebanon, with a capital expenditure of $96.1 million. However, after the full implementation of

the agreement (2005-2016), the average capital inflow was $3.2 billion a year, with an average of 1,629 jobs

created. Inflows continued to increase until 2009, when they peaked at $4.8 billion, or 13.54 per cent of the

country’s GDP. Since reaching this peak, foreign investments have fallen to $2.6 billion in 2016, representing

only 5.25 per cent of GDP. During this period, the United Arab Emirates invested the greatest amount of

capital, at $6.138 billion, or 93.3 per cent of foreign direct investments. Some of the decrease in investments

is due to the Syrian conflict, which began in March 2011. The instability in the region has shaken the

confidence of foreign investors in the viability of growth in Lebanon. This will harm the economy, as a

decrease in capital inflow will lead to lower job creation and an overall decrease in GDP. The top sectors of

investment did not change from the prior period, with the real estate and hotels and tourism sectors receiving

$3.966 billion and $1.503 billion in capital, respectively.

The decline in investments can be seen as the result of unstable conditions in the region

around Lebanon. A weak economy and multiple conflicts, including the Syrian conflict, have scared off

investors, as uncontrollable outside factors have caused warfare within Lebanon as well as in surrounding

areas. The risk of investment loss outweighs the benefits which the FTA could provide, and this continues to

hamper economic growth in the country, as foreign investments are crucial for expedited economic

development.

The two largest investment sectors by capital expenditure are the real estate and hotels and tourism

sectors. Total capital investments in 2003 in the Lebanese real estate market were of $5.6712 billion. Unlike

the Lebanese economy as a whole, the housing market has been surprisingly stable since 2008, and

housing prices doubled from 2008 to 2012. But the market has been stagnating over the past few years,