ewe ag/media/ewe_com/pdfs im inhalt/moodys_rating.pdf · moody's investors service...

TRANSCRIPT

INFRASTRUCTURE AND PROJECT FINANCE

CREDIT OPINION20 May 2016

Update

RATINGSEWE AG

Domicile Germany

Long Term Rating Baa1

Type LT Issuer Rating - FgnCurr

Outlook Stable

Please see the ratings section at the end of this reportfor more information.The ratings and outlook shownreflect information as of the publication date.

Contacts

Stefanie Voelz 44-20-7772-5555Senior Credit [email protected]

Neil Griffiths-Lambeth

44-20-7772-5543

Associate [email protected]

EWE AGUpdate following the conclusion of VNG sale

Summary Rating RationaleGerman utilities currently face a difficult operational environment with very low marketprices for conventional power generation, partly a reflection of a revised national energypolicy and partly linked to a decline in commodity and CO2 prices. EWE is less exposed tothese developments than its larger German peers, given the focus on monopoly-regulatednetwork activities, and its increased financial flexibility following the April 2016 sale of thecompany's stake in VNG.

Exhibit 1

German power prices, spreads and CO2

Source: FactSet

Consequently, EWE's Baa1 rating reflects (1) the fairly stable and predictable cash flowsgenerated by its monopoly-regulated energy distribution activities; (2) long-term contractswhich stabilise the competitive businesses in the area of power generation, gas storageand waste-to-energy; (3) the company's fairly strong market position in its core region,which somewhat reduces the risk inherent in its competitive supply activities; (4) its growingexpertise in renewable generation, particularly on- and offshore wind, and intelligent networkdevelopments, both of which are key factors in the current German energy policy; and (5) ourassumption that the company's interest in international markets, particularly in Turkey, andtheir contribution to consolidated cash flows will remain small over the medium term.

EWE's Baa1 rating is constrained by the company's financial profile, which has been affectedin recent years by (1) the negative gas/oil spread movements reflected in rising procurement

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 20 May 2016 EWE AG: Update following the conclusion of VNG sale

costs that the company was unable to fully pass on to consumers; and (2) certain volatility in the gas activities linked to one-off events,such as a negative court ruling on the company's historical gas price contracts resulting in significant pay-outs to customers, andadverse weather patterns.

Credit Strengths

» Multi-utility with focus on energy distribution and supply activities as well as telecommunication and information technologyservices

» Stable network operations and limited generation create some buffer against negative wholesale price developments affectingother generators

» Financial metrics should strengthen as investment projects are finalised and ongoing cost-savings are implemented

» Sale of VNG stake creates financial headroom in the medium term

Credit Challenges

» Relatively high exposure to gas sales, creating volatility in revenues and cash flows depending on weather patterns

» Low power prices reduce margins for conventional thermal generation but EWE's exposure largely mitigated by limitedconventional generation capacity compared with German peers and generally long-term capacity contracts to sell power orgeneration capacity benefiting from renewable subsidies

Rating OutlookThe rating outlook is stable, reflecting the company's core focus on regulated network activities and renewable generation, limitedexposure to negative power price developments compared with its larger German peers and the successful conclusion of the VNGsale in April 2016 with proceeds being largely used to repay a portion of existing debt and leading to a commensurate improvement infinancial flexibility.

Factors that Could Lead to an UpgradeMoody's expects EWE's credit metrics to improve following disposal of the VNG stake while noting that the proceeds may not allbe used for debt repayment. In particular, EWE may choose to support its shareholders in acquiring the remaining EWE shares fromEnBW by 2019. While a rating upgrade is unlikely over the short-term, upward pressure could result from a sustainable improvement infinancial metrics, with FFO/Net Debt at least in the low twenties and RCF/Net Debt comfortably in the high teens, for example due tode-leveraging of the EWE group, or the successful execution of the company's ongoing efficiency and disposal programme.

Factors that Could Lead to a DowngradeEWE's Baa1 ratings could come under downward pressure if the company were to exhibit financial metrics consistently below theminimum parameters outlined for the current rating of FFO/Net Debt in the high teens and RCF/Net Debt in the mid-teens, inpercentage terms. Furthermore, we could consider a downgrade in case of a change in EWE's business risk profile that would increaseexposure to higher risk countries, such as Turkey, and/or result in increasing volatility of cash flows.

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

3 20 May 2016 EWE AG: Update following the conclusion of VNG sale

Key Indicators

Exhibit 2

Volatility on metrics due to gas activities' exposure to adverse weather patterns and price developments

Note: All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial CorporationsSource: Moody's Financial Metrics™

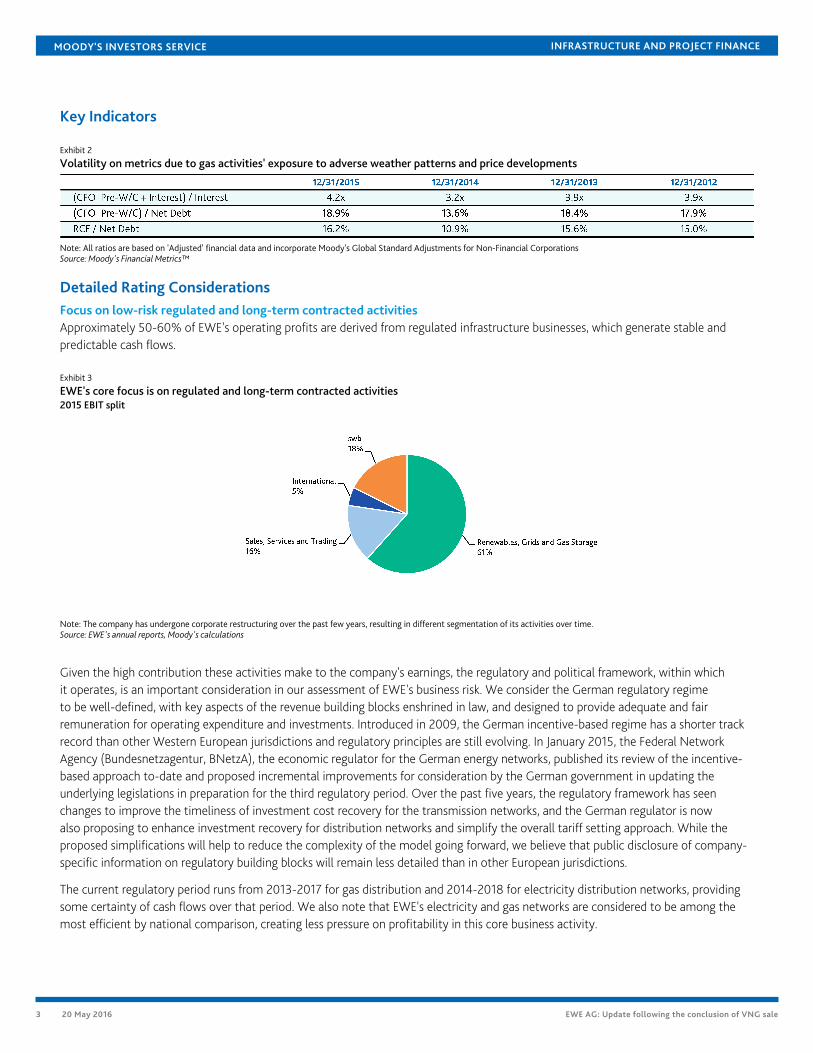

Detailed Rating ConsiderationsFocus on low-risk regulated and long-term contracted activitiesApproximately 50-60% of EWE's operating profits are derived from regulated infrastructure businesses, which generate stable andpredictable cash flows.

Exhibit 3

EWE's core focus is on regulated and long-term contracted activities2015 EBIT split

Note: The company has undergone corporate restructuring over the past few years, resulting in different segmentation of its activities over time.Source: EWE's annual reports, Moody's calculations

Given the high contribution these activities make to the company's earnings, the regulatory and political framework, within whichit operates, is an important consideration in our assessment of EWE's business risk. We consider the German regulatory regimeto be well-defined, with key aspects of the revenue building blocks enshrined in law, and designed to provide adequate and fairremuneration for operating expenditure and investments. Introduced in 2009, the German incentive-based regime has a shorter trackrecord than other Western European jurisdictions and regulatory principles are still evolving. In January 2015, the Federal NetworkAgency (Bundesnetzagentur, BNetzA), the economic regulator for the German energy networks, published its review of the incentive-based approach to-date and proposed incremental improvements for consideration by the German government in updating theunderlying legislations in preparation for the third regulatory period. Over the past five years, the regulatory framework has seenchanges to improve the timeliness of investment cost recovery for the transmission networks, and the German regulator is nowalso proposing to enhance investment recovery for distribution networks and simplify the overall tariff setting approach. While theproposed simplifications will help to reduce the complexity of the model going forward, we believe that public disclosure of company-specific information on regulatory building blocks will remain less detailed than in other European jurisdictions.

The current regulatory period runs from 2013-2017 for gas distribution and 2014-2018 for electricity distribution networks, providingsome certainty of cash flows over that period. We also note that EWE's electricity and gas networks are considered to be among themost efficient by national comparison, creating less pressure on profitability in this core business activity.

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

4 20 May 2016 EWE AG: Update following the conclusion of VNG sale

Approximately 8-10% of EWE's operating profits come from renewable generation, which we consider as lower risk than conventionalgeneration, given the feed-in tariffs guaranteed by the German government. This regime limits EWE's risks essentially to the output ofthe plants, which is subject to weather conditions and technical losses. However, existing installations are not exposed to market pricerisks.

The cash flow volatility of some of EWE's other activities is reduced due to existing long-term contracts. This is particularly the case inthe gas storage business (15-20% of group operating profits), with more than two-thirds of capacity being contracted for a remainingcontract lifetime of 7-10 years (50% is for own use). This protects divisional profits from adverse effects of low gas storage prices in thecontext of a generally oversupplied German gas market and compressed winter-summer spreads. Moreover, ca. 60% of input volumesof EWE's waste-to-energy operations are contracted on medium to long-term contracts.

EWE's domestic sales & trading activities (ca. 37TWh natural gas and 14TWh electricity supplied in 2015) are, in contrast, subject tointensifying competition and could suffer pressure on supply margins. Moreover, electricity generation activities, although small, areaffected by the adverse market environment in the German electricity wholesale market, as discussed below.

International operations are focused on Turkey and Poland and largely related to energy distribution and sales activities (approximately26TWh of natural gas supplied in 2015). While we consider these activities to be of higher risk than the core domestic business, thecontribution to operating profit remains small (accounting for less than 5% of consolidated EBITDA) and EWE's current ratings do notassume a material growth in this area.

Reduction of exposure to power generation and gas supply marketsEWE owns and operates a conventional thermal generation fleet of approximately 1.0 GW installed capacity. The profitability ofconventional plants in Germany has suffered from weak fuel prices (coal and natural gas), low carbon prices as well as compressedgeneration margins (both clean dark and spark spreads). Key reasons are the weakness of the global economy, increasing supply ofcommodities (especially natural gas), an oversupply of EU carbon certificates and the material expansion of renewable generationcapacities. In this unfavourable environment, however, EWE has managed to de-risk more than half of its generation portfolio byentering into or amending existing bilateral supply contracts with several industrial consumers. We understand that these individualcontracts transfer market risks to customers, while, at the same time, EWE will safeguard a small level of profitability for the underlyinggeneration capacities.

Overall, EWE is much less exposed than its larger German peers, E.ON SE (Baa1, negative outlook) and RWE AG (Baa3, stable outlook),to the currently low forward baseload prices in Germany, which have declined by around 20% over the last year. Current one-yearforward baseload prices of around €20-25/MWh are below Moody's estimates published in June 2015 of a €30-35/MWh range. Takinginto account the contracted capacity and generally small generation portfolio, which is primarily coal-fired, we have estimated that adecline in clean dark spreads by €3/MWh would result in around 1% reduction in operating profits.

On the gas side, EWE has a number of long-term take-or-pay arrangements. In common with the major German gas importersand integrated utilities, EWE's profitability has been affected negatively by the movement of the gas/oil spread, which meant thatthe oil-price linked contracts were more expensive than buying gas on the spot market. We understand that EWE has managed torenegotiate more than 90% of its supply portfolio to market-based pricing going forward. As a result, gas/oil spread risks have declinedconsiderably.

Focus on cost cutting and de-leveraging to counter recently weak resultsTo counteract a challenging market environment, EWE focused on increasing its efficiency and achieved cost savings over 2012-15. Thenew management team, put in place over the past year, envisages further efficiency measures in the coming years.

With the commissioning of major investment projects in 2014, the company has also passed the peak of its investment growthstrategy, reducing future capex requirements and resulting in positive operating cash flow contributions from the newly commissionedassets.

Management's ongoing focus on cost efficiencies and de-leveraging of the business should help counteract a challenging operationalenvironment. The 2014 financial results were particularly weak, primarily due to mild weather conditions. Warm weather led to a fall ingas sales, leading to reduced revenue in both the Sales and Network divisions and also a devaluation of EWE's gas reserves. A decrease

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

5 20 May 2016 EWE AG: Update following the conclusion of VNG sale

in demand for electricity also led to lower revenues across the group and an impairment loss was recognized on EWE's conventionalgeneration units.

The financial year ending December 2015 saw significantly improved results. In relation to the group's network activities, which accountfor the majority of cash flows generated, EWE benefits from a true-up mechanism for under-recovered revenues compared withregulatory allowances. Effectively, a proportion of the lower cash flows generated from adverse weather will be recoverable. However,such true-up adjustment will typically take place only at the next regulatory review (the next regulatory period for gas distributionnetworks will commence on 1 Jan 2018, or 1 Jan 2019 for electricity distribution networks), unless they account for variations in excessof 5% compared with regulatory assumptions.

VNG sale creates financial flexibility in the medium termEWE owned a 47.9% minority stake in the German natural gas company VNG from 2004, but became the majority shareholder in2014 when it increased its stake to 63.7%. In July 2015, EWE acquired a further 10.52% of the shares from Gazprom Germania GmbH,taking its stake to 74.2%.

In October 2015, EWE announced that it would sell its stake in VNG to EnBW, which itself would divest of its 26% shareholdingin EWE. EWE bought 10% of its own shares for a consideration of €504.8 million, and its then 74% owner, the Ems-Weser-ElbeVersorgungs- und Entsorgungsverband (EWE Verband), an association of municipalities and provinces in the area of EWE's coreoperations, will purchase the remaining 16% in EWE's shares in a two-stage process.

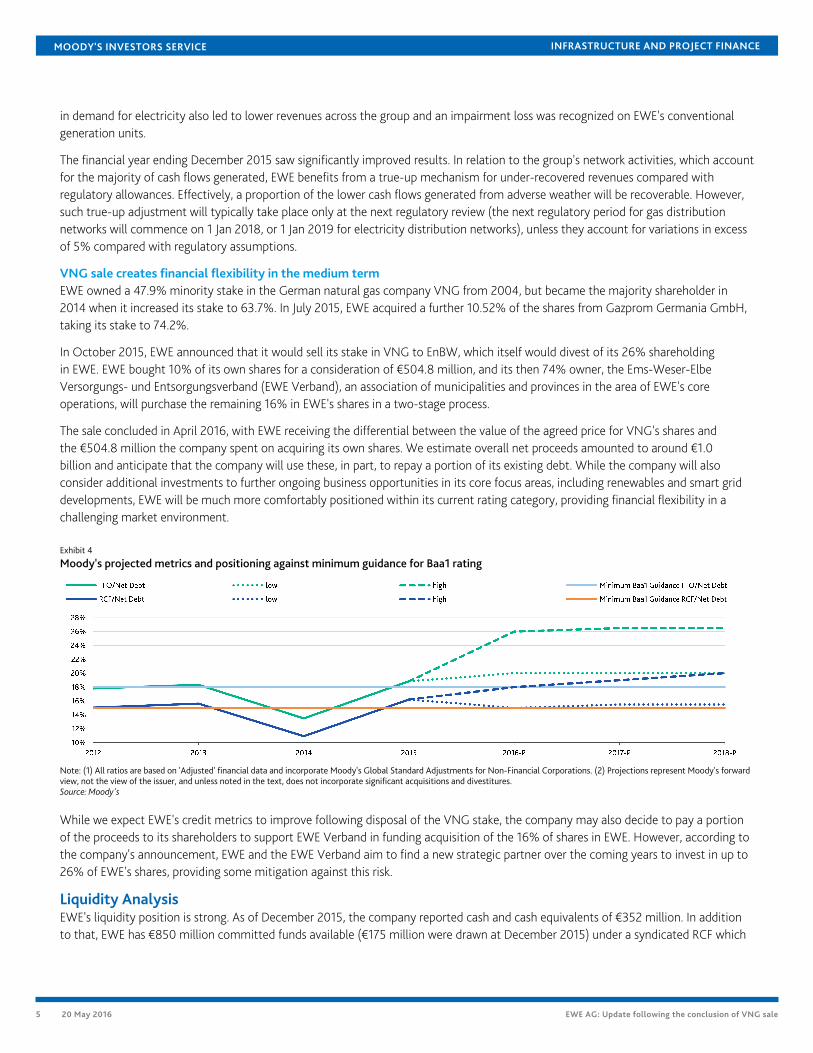

The sale concluded in April 2016, with EWE receiving the differential between the value of the agreed price for VNG's shares andthe €504.8 million the company spent on acquiring its own shares. We estimate overall net proceeds amounted to around €1.0billion and anticipate that the company will use these, in part, to repay a portion of its existing debt. While the company will alsoconsider additional investments to further ongoing business opportunities in its core focus areas, including renewables and smart griddevelopments, EWE will be much more comfortably positioned within its current rating category, providing financial flexibility in achallenging market environment.

Exhibit 4

Moody's projected metrics and positioning against minimum guidance for Baa1 rating

Note: (1) All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations. (2) Projections represent Moody's forwardview, not the view of the issuer, and unless noted in the text, does not incorporate significant acquisitions and divestitures.Source: Moody's

While we expect EWE's credit metrics to improve following disposal of the VNG stake, the company may also decide to pay a portionof the proceeds to its shareholders to support EWE Verband in funding acquisition of the 16% of shares in EWE. However, according tothe company's announcement, EWE and the EWE Verband aim to find a new strategic partner over the coming years to invest in up to26% of EWE's shares, providing some mitigation against this risk.

Liquidity AnalysisEWE's liquidity position is strong. As of December 2015, the company reported cash and cash equivalents of €352 million. In additionto that, EWE has €850 million committed funds available (€175 million were drawn at December 2015) under a syndicated RCF which

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

6 20 May 2016 EWE AG: Update following the conclusion of VNG sale

matures in July 2017. €809 million of this tranche have already been extended until July 2018. All credit facilities are reported to be freeof restrictive covenants and MAC clauses. Therefore, they represent a highly reliable source of liquidity.

EWE's main uses of cash in the next 12-18 months include capital expenditure, an annual dividend payment of typically around €90million, although expected to be higher in 2016 to reflect the book gain achieved from the VNG sale, and total debt repayments ofaround €230 million in 2016 and a similar amount in 2017.

Exhibit 5

VNG sale proceeds will at least partly be applied to cover near-term debt maturitiesEWE's bond maturities (in € millions)

Source: EWE annual report 2015

Corporate ProfileHeadquartered in Oldenburg, Germany, EWE AG is one of Germany's largest regional utilities and provides energy distribution andsupply as well as telecommunications and IT services to customers in the federal state of Lower Saxony and parts of eastern Germany.EWE is currently owned 6% by EnBW Energie Baden Württemberg AG (EnBW, A3 negative) and 84% by two holding companies whichaltogether represent 21 local cities and municipalities/counties located in the state of Lower Saxony. The remaining 10% are held byEWE itself.

Exhibit 6

EWE owned 84% by local cities and municipalities

Source: EWE AG

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

7 20 May 2016 EWE AG: Update following the conclusion of VNG sale

Rating Methodology and Scorecard FactorsEWE is rated under the rating methodology for Unregulated Utilities and Power Companies, published October 2014. Compared withmost of its German peers, EWE benefits from (1) a much lower direct exposure to merchant generation power prices in the challengingGerman power market (nevertheless, it must continue to manage its procurement strategy and margins in respect of its downstreamcustomer base); (2) an entrenched and rather stable customer base in its core markets; and (3) a materially higher proportion ofearnings from low risk monopoly-regulated network activities. These comparative strengths support an actual assigned rating of Baa1that is higher than the grid-indicated rating.

Exhibit 7

EWE AG - Rating Factors Grid

Note: (1) All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations. (2) As of 21/31/2015. (3) This representsMoody's forward view, not the view of the issuer, and unless noted in the text, does not incorporate significant acquisitions and divestitures.Source: Moody's Financial Metrics™

Given its ownership structure, EWE's final rating also takes into account the joint default analysis under our rating methodology forgovernment-related issuers, published in October 2014, inter alia reflecting (1) our assessment of low probability of extraordinarysupport by the municipalities that own EWE, due to the fragmented nature of EWE's municipal ownership; and (2) our assessment ofmoderate dependence, which takes into account that a large part of EWE's revenues are generated within the regions and cities thatalso comprise EWE's municipal owners, but part of EWE's earnings are generated outside of Lower Saxony.

Given the low support assumption under a generally fragmented municipal ownership structure, EWE's Baa1 rating is in line with thecompany's stand-alone credit quality absent any extraordinary assumed support, the so-called baseline credit assessment (BCA).While EWE's ratings may be impacted by changes in the GRI input factors, e.g. the credit quality of the supporting municipalities, or

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

8 20 May 2016 EWE AG: Update following the conclusion of VNG sale

our assessment of default dependence and support, we note that given the assumed low probability of support from EWE's ultimatemunicipal shareholders, the potential for rating uplift from the BCA remains generally limited.

Ratings

Exhibit 8Category Moody's RatingEWE AG

Outlook StableIssuer Rating Baa1Senior Unsecured -Dom Curr Baa1

Source: Moody's Investors Service

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

9 20 May 2016 EWE AG: Update following the conclusion of VNG sale

© 2016 Moody's Corporation, Moody's Investors Service, Inc., Moody's Analytics, Inc. and/or their licensors and affiliates (collectively, "MOODY'S"). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES ("MIS") ARE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY'S ("MOODY'SPUBLICATIONS") MAY INCLUDE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKESECURITIES. MOODY'S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANYESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKETVALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY'S OPINIONS INCLUDED IN MOODY'S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICALFACT. MOODY'S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHEDBY MOODY'S ANALYTICS, INC. CREDIT RATINGS AND MOODY'S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDITRATINGS AND MOODY'S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDITRATINGS NOR MOODY'S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY'S ISSUES ITS CREDIT RATINGSAND PUBLISHES MOODY'S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY ANDEVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY'S CREDIT RATINGS AND MOODY'S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY'S CREDIT RATINGS OR MOODY'S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY'S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY'S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY'S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody's Publications.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY'S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY'S.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY'S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER.

Moody's Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody's Corporation ("MCO"), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody's Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody's Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading "Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy."

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY'S affiliate, Moody's InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody's Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to "wholesale clients" within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY'S that you are, or are accessing the document as a representative of, a "wholesale client" and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to "retail clients" within the meaning of section 761G of the Corporations Act 2001. MOODY'S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY'S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. ("MJKK") is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody'sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody's SF Japan K.K. ("MSFJ") is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization ("NRSRO"). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1025695

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

10 20 May 2016 EWE AG: Update following the conclusion of VNG sale

Contacts

Tom Neugebauer 4420-7772-1451Associate [email protected]

Stefanie Voelz 44-20-7772-5555Senior Credit [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454