evolving structure of agriculture and collective action steve sonka assistant dean for research...

TRANSCRIPT

EVOLVING STRUCTURE OF AGRICULTURE AND

COLLECTIVE ACTION

Steve Sonka

Assistant Dean for Research Strategy

Emeritus Chair for Soybean Industry Strategy

University of Illinois at Urbana-Champaign

• A business entity is successful when:– Its services and products provide sufficient

net value to customers and – Its profits provide a rate of return that exceeds

the owner’s hurdle rate.

• In ag, our attention has tended to focus on Commodity Volume– Collective efforts

• transform stuff from large numbers of farmers with similar interests

• into output for mass markets

Two Clashing Perspectives

• A business entity is successful when:– Its services and products provide sufficient

net value to customers and – Its profits provide a rate of return that exceeds

the owner’s hurdle rate.

• In ag, our attention has tended to focus on Commodity Volume– Collective efforts

• transform stuff from large numbers of farmers with similar interests

• into output for mass markets

Two Clashing Perspectives

Agenda

Emphasize opportunity in segmentation

• Ag structure – Heterogeneity– Perspective

• An example of segmentation’s benefits– Ownership– Customer

Yesterday – Not That Long Ago

Today: Early in the 21st Century

Yesterday – Not That Long Ago

• Similar interests to neighbors• Competitor sell inputs or buys output• Non-farmers much better off• Small economic units• Unconnected to non-farm economy• Success comes from working hard

Some Dimensions of Being a Farmer

Farmers:Aren’t They All the Same?

0

200000

400000

600000

800000

1000000

1200000

1400000

U.S. Farms by ARMS Typology; 1998

Limited Resource,Retirement, &

Residential

FarmingOccupation

Large &Very Large

Family Farms

Non-Family Farms

61.8%

28.8%

7.5%

2.0%

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

400,000,000

Acreage Operated; 1998

Limited Resource,Retirement, &

Residential

FarmingOccupation

Large &Very Large

Family Farms

Non-Family Farms

20.6%

41.8%

30.1%

7.5%

Rented

Owned

Acreage Owned Versus Rented

Limited Resource,Retirement, &

Residential

FarmingOccupation

Large &Very Large

Family Farms

Non-Family Farms

76.2%

57.0%

40.7%

80.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Debt Mgt

Budgeting

Credit Line

Forward Price Inputs

Use Mktg Contracts

Limited Resource,Retirement, &

Residential

Low Sales High SalesFarming Occupation

Large &Very Large

Family Farms

% Employing SelectedManagement Practices

0%

10%

20%

30%

40%

50%

60%

Marketing

Supply

Cooperative Membership

Limited Resource,Retirement, &

Residential

Low Sales High SalesFarming Occupation

Large &Very Large

Family Farms

Linkages

• Interests of majority of farmers differ from interests of farmers who produce majority of farm output

Where Does the Farm Household’s Income

Come From?

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Off-Farm

Farm

Total Household Income: Where Farming Subtracts

Limited Resource

Low SalesFarming Occupation

Retirement ResidentialLifestyle

0

50,000

100,000

150,000

200,000

250,000

Off-Farm

Farm

Total Household Income:Where Farming Adds

High SalesFarming Occupation

Large Family Farms

Very LargeFamily Farms

0

1,000

2,000

3,000

4,000

5,000

6,000

On-Farm

Off-Farm

Hours Worked On & Off the Farm:Family Farm Households

Low Sales High SalesFarming Occupation

Large Family Farms

Very LargeFamily Farms

29.8% 24.1%18.3% 18.9%

Linkages

• Interests of majority of farmers differ from interests of farmers who produce majority of farm output

• Off-farm work consumes time/attention & is important economically across all farm categories

Who’s Well Off?

JoeAverage

Linkages

• Interests of majority of farmers differ from interests of farmers who produce majority of farm output

• Off-farm work consumes time/attention & is important economically across all farm categories

• Farmers economically advantaged

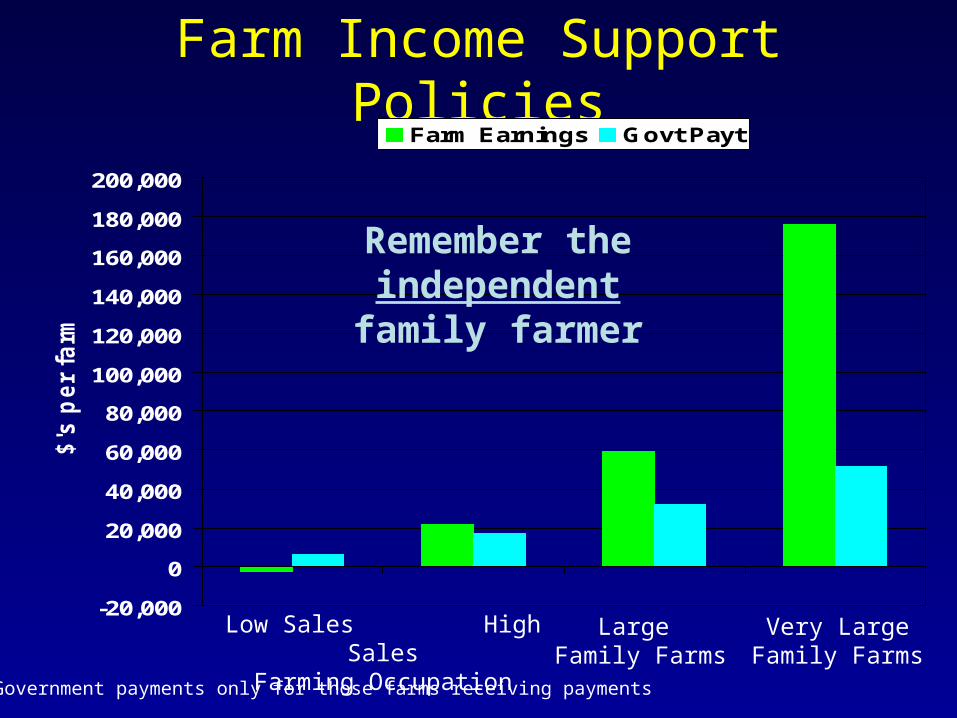

Farm Income Support Policies

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

$'s

per

farm

*

Farm Earnings Govt Payt

Low Sales High SalesFarming Occupation

Large Family Farms

Very LargeFamily Farms

* Government payments only for those farms receiving payments

Remember the independentfamily farmer

Linkages

• Interests of majority of farmers differ from interests of farmers who produce majority of farm output

• Off-farm work consumes time/attention & is important economically across all farm categories

• Farmers economically advantaged

• Farm the government, not the market

The Farmer’s Neighbor:Friend or Foe?

Tenure Dynamics in the Midwest

Full ownerPart ownerFull tenant

Linkages

• Interests of majority of farmers differ from interests of farmers who produce majority of farm output

• Off-farm work consumes time/attention & is important economically across all farm categories

• Farmers economically advantaged• Farm the government, not the market

• Competition for access to land changes relationship dynamics

Assume a Commodity Market

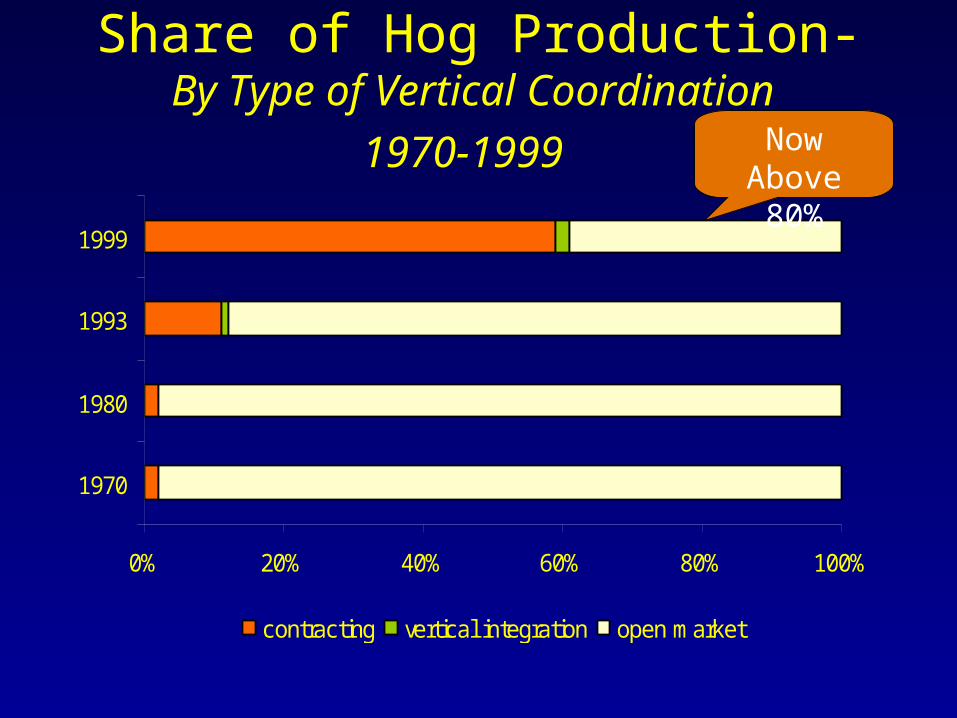

Share of Hog Production-By Type of Vertical Coordination

1970-1999

0% 20% 40% 60% 80% 100%

1970

1980

1993

1999

contracting vertical integration open market

NowAbove 80%

Linkages

• Interests of majority of farmers differ from interests of farmers who produce majority of farm output

• Off-farm work consumes time/attention & is important economically across all farm categories

• Farmers economically advantaged• Farm the government, not the market• Competition for access to land changes dynamics

• Open market sales of commodity output declining as a share of total ag output

Segmentation

New Zealand MerinoCreating a Silk Purse

From a Sow’s Ear

0

500

1000

1500

2000

2500

69/70

71/72

73/74

75/76

77/78

79/80

81/82

83/84

85/86

87/88

89/90

91/92

93/94

95/96

97/98

99/00

Season

(100

0 M

T)

0

100

200

300

400

500

600

700

800

Cen

ts/K

g

World Production Average Price

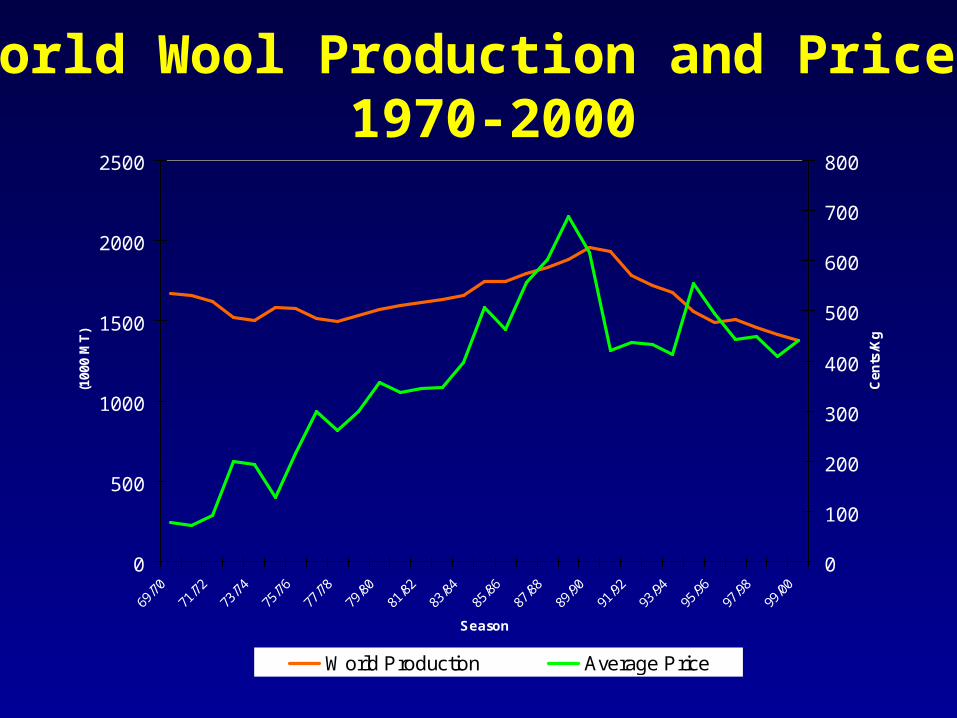

World Wool Production and Price: 1970-2000

0

5000

10000

15000

20000

25000

30000

3500010

00 M

T

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

Year

Wool Natural fibers Synthetic fibers

Old and New Substitutes Growing

New Zealand Wool Board Responded

• Generic promotion

• Trademarks with no discipline

Just not effectively,Especially for Merino !!!

* Merino has superior quality

* Typically used to raise NZ’s average quality for low value markets

A Silk Purse From a Sow’s Ear

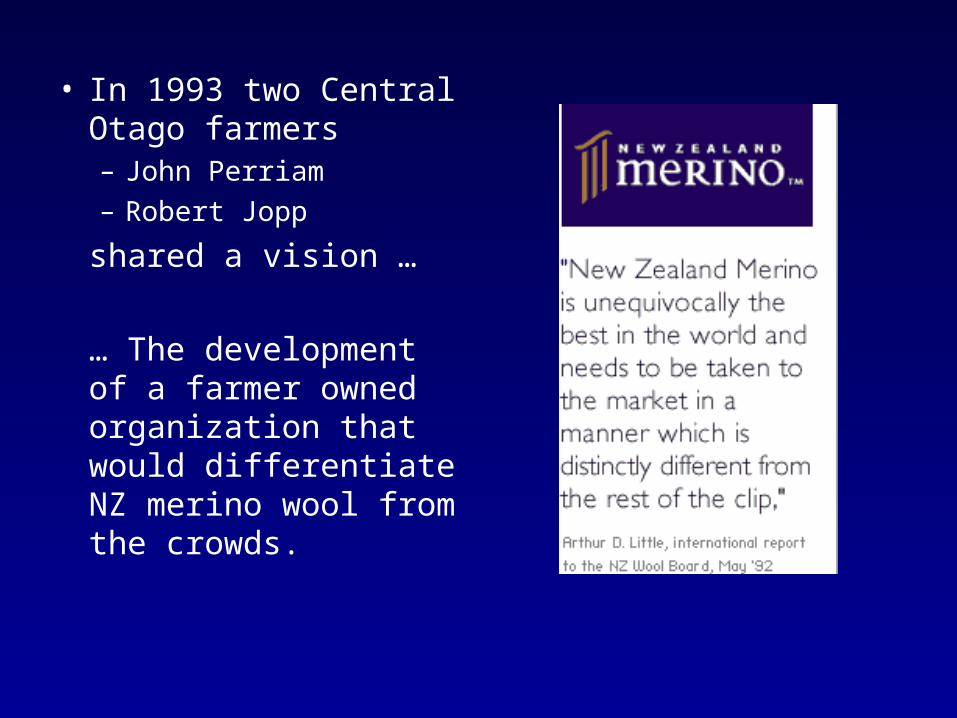

• In 1993 two Central Otago farmers – John Perriam– Robert Jopp

shared a vision …

… The development of a farmer owned organization that would differentiate NZ merino wool from the crowds.

From Vision …to Reality.

Unique Marketing Propositions.

Offers Brand Partners…

These may include Intel inside co-Branding Relationship with some Partners

And less obvious exclusive arrangements with others.

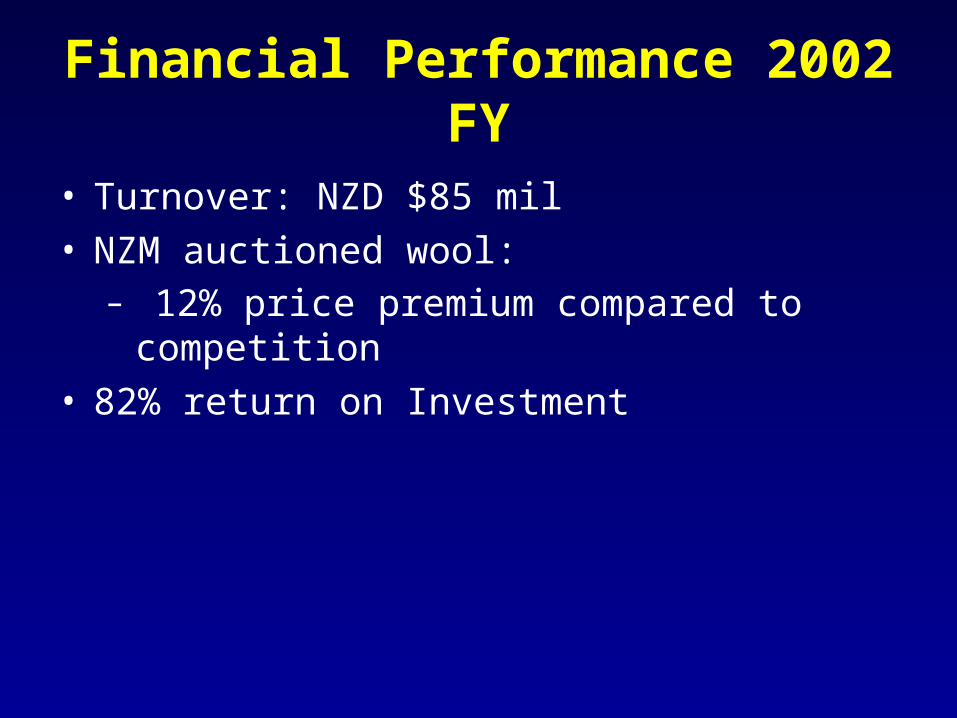

Financial Performance 2002 FY

• Turnover: NZD $85 mil• NZM auctioned wool:

– 12% price premium compared to competition

• 82% return on Investment

Summary Points

• Collective action efforts – strive to enhance farm income but underlying context has

changed and is changing– Key structural changes have eroded the commonality of the

“farm identity”

• Future success of collective action efforts requires:– Mentality shift from commodity volume to value and required

rates of return– Creative use of segmentation:

• To link needs of customer groups and interests of producer groups

• That employs innovative organizational arrangements