evaluating thailand's alcohol excise tax system

TRANSCRIPT

MEMO

To: Korn Chatikavanij, Minister for Finance

From: Jonathon Flegg, Policy Unit, Ministry of Finance

Date: 02/06/11

Subject: Liquor Tax Reform Recommendation

The consumption of alcohol in Thailand has become an increasing public health concern. While only 31% of Thais

consume alcohol1, annual per person consumption exceeds that of France, where the vast majority of the population

consume alcohol2. The economic cost to Thailand has been estimated at 156,105.4 million baht, or 1.99% of GDP

3.

It is for this reason the Thai Government has sought the advice of the Policy Unit within the Ministry of Finance in

reviewing the current policy on liquor taxation.

1. What perspectives should the government take into consideration in making the decision?

The Ministry of Finance is confronted with the need to balance three competing primary policy objectives

of alcohol policy: “to reduce alcohol consumption, protect the local liquor industry and minimize the

impact on government revenue from excise collection4.” However there are also a number of other

perspectives that should also be considered when deciding on liquor policy. As the burden of the liquor

tax inescapably falls on the poor, and given that it constitutes a considerable component (7%) of total

government revenue, it is also important to ensure that any reform does not create a more socially

regressive taxation system.

The issue of alcohol consumption can be considered as an activity that generates social costs unpaid for in

the market price of alcoholic beverages. These negative externalities might be direct, such as increased

health care costs, costs of law enforcement, and costs of property damage due to road-traffic accidents; or

indirect, such as costs of productivity loss due to premature mortality, and reduced productivity. To

achieve the socially efficient level of alcohol consumption, traditional economic approaches would

therefore consider the need to apply an excise tax equal to the social externalities that alcohol

consumption generates. Optimal commodity taxation would also demand that to achieve efficiency,

effective excise tax rates are set in proportion to the inverse of the price elasticity of demand of individual

alcoholic beverages.

Finally, a precondition for a reform proposal is that it must be both politically and administratively

feasible. While there is considerable public support for acting on the issue of alcohol consumption5, the

Government is also concerned about the effect that increasing taxation might have domestic producers.

1 Thavorncharoensap, M. et al. 2010. “The economic costs of alcohol consumption in Thailand, 2006”. BMC Public Health 10:

323 – 335. 2 Techajareonvikul, A. 2006. “Liquor Tax Reform in Thailand: Competing Interests and Objectives”. HKS Case Study CR14-

06-1857.0. 3 Thavorncharoensap, M. et al. 2010.

4 Techajareonvikul, A. 2006, pg 2.

5 On the 18

th March 2007 a marathon of runners delivered a total of 13 million signatures to Parliament calling for action to

curb alcohol consumption. This was the largest petition ever collected in Thai history.

2. How should the government balance different objectives?

The primary consideration for any reform proposal is whether it can achieve a significant reduction in

overall alcohol consumption while retaining the current level of excise revenue. These goals are not

incompatible with each other, if tax rates can be increased in such a way that excise revenue is not

adversely affected. The goal of protecting domestic alcohol producers can most effectively be achieved

by using import duties rather than excise tax. This approach means that local producers within the

domestic spirits and wine industries are not adversely affected by an excise tax regime that attempts to

target foreign imports6.

There is strong evidence to suggest that the current liquor tax system is inefficient. Beer, a popular

segment of the market accounting for 43% of its total value, is taxed quite heavily (see Table 1) despite

its high elasticity of demand. When compared with its closest substitute at the cheaper end of the market,

domestically-distilled white liquors, there is a nine-fold difference in effective tax rates7. These two

segments form a majority of the Thai alcohol market and closing the gap between their effective tax rates

is a precondition for efficient liquor tax reform. Under the current excise system traditional producers of

white spirits have enjoyed preferential treatment that is now no longer sustainable if alcoholic

consumption is to be reduced.

Any feasible form of alcohol excise is likely to be socially regressive, because poor Thais tend to spend a

greater proportion of their income on alcohol compared with wealthier Thais. For equity reasons the

Government should not attempt to collect excessive revenue from liquor tax, particularly from beverages

preferred by poorer Thais. Revenue should remain broadly neutral. This goal comes into conflict with an

attempt to incorporate the increased social costs of alcohol consumption into the price of alcohol. The

current estimate of social costs to the Thai economy are 156 billion baht compared with only 6.9 billion

baht collected in liquor tax. To fully incorporate the social costs of alcohol consumption would be both

inequitable and infeasible. A more appropriate policy goal is to reduce the social costs by focusing on

reducing consumption. Reducing social regressivity can be achieved my retaining higher effective tax

rates on beverages consumed by wealthier Thais, such as wine and imported liquors.

3. What option should the government choose?

Of the plans provided by the Excise Department, only Plan C will succeed in both reducing the overall level of

alcohol consumption and maintaining revenue derived taxing alcohol8. The projections produced by the Policy Unit

of the effect on average prices (P), consumption (C) and excise revenue (R) can be seen in Table 2 and 39.

6 The domestic Thai wine industry, while still developing by international standards, has experienced considerable growth of

over 6% annually. 7 This is despite having similarly high price elasticities of demand.

8 Consumption is based on per litre of pure alcohol to facilitate comparison across beverage categories.

9 In this analysis we assume municipal and health tax as constant, which are calculated as a small percentage of the levied

excise tax amount.

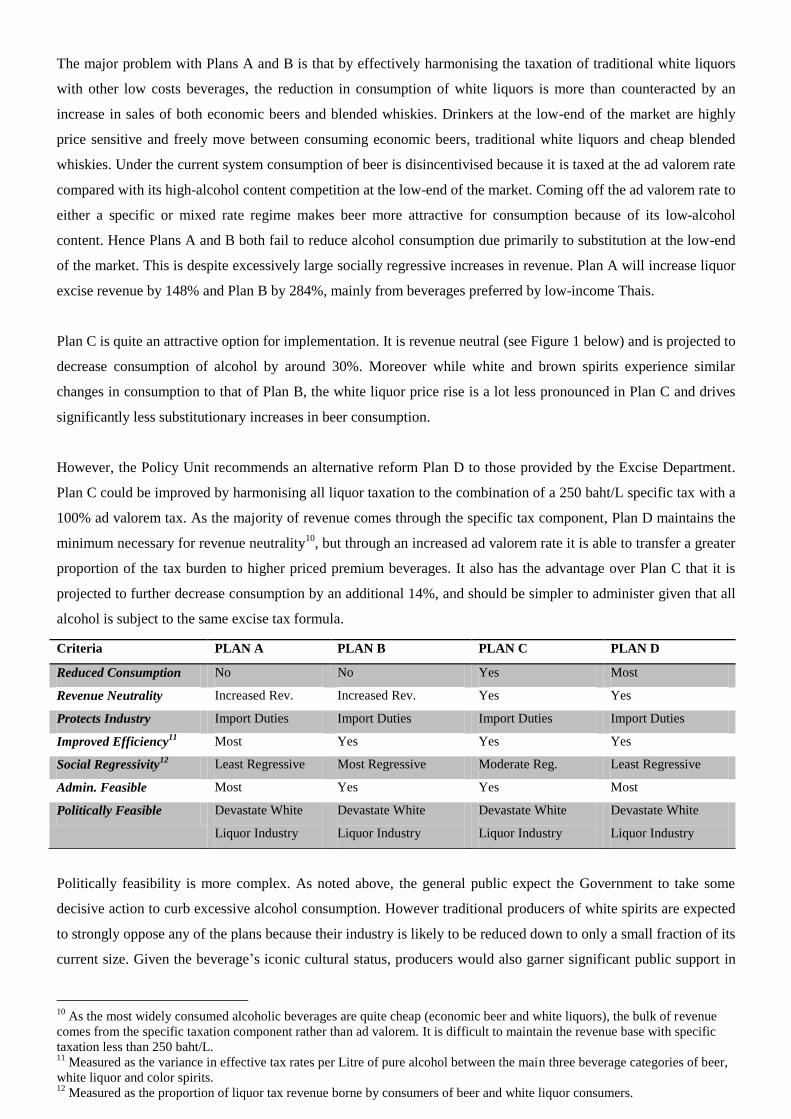

The major problem with Plans A and B is that by effectively harmonising the taxation of traditional white liquors

with other low costs beverages, the reduction in consumption of white liquors is more than counteracted by an

increase in sales of both economic beers and blended whiskies. Drinkers at the low-end of the market are highly

price sensitive and freely move between consuming economic beers, traditional white liquors and cheap blended

whiskies. Under the current system consumption of beer is disincentivised because it is taxed at the ad valorem rate

compared with its high-alcohol content competition at the low-end of the market. Coming off the ad valorem rate to

either a specific or mixed rate regime makes beer more attractive for consumption because of its low-alcohol

content. Hence Plans A and B both fail to reduce alcohol consumption due primarily to substitution at the low-end

of the market. This is despite excessively large socially regressive increases in revenue. Plan A will increase liquor

excise revenue by 148% and Plan B by 284%, mainly from beverages preferred by low-income Thais.

Plan C is quite an attractive option for implementation. It is revenue neutral (see Figure 1 below) and is projected to

decrease consumption of alcohol by around 30%. Moreover while white and brown spirits experience similar

changes in consumption to that of Plan B, the white liquor price rise is a lot less pronounced in Plan C and drives

significantly less substitutionary increases in beer consumption.

However, the Policy Unit recommends an alternative reform Plan D to those provided by the Excise Department.

Plan C could be improved by harmonising all liquor taxation to the combination of a 250 baht/L specific tax with a

100% ad valorem tax. As the majority of revenue comes through the specific tax component, Plan D maintains the

minimum necessary for revenue neutrality10

, but through an increased ad valorem rate it is able to transfer a greater

proportion of the tax burden to higher priced premium beverages. It also has the advantage over Plan C that it is

projected to further decrease consumption by an additional 14%, and should be simpler to administer given that all

alcohol is subject to the same excise tax formula.

Politically feasibility is more complex. As noted above, the general public expect the Government to take some

decisive action to curb excessive alcohol consumption. However traditional producers of white spirits are expected

to strongly oppose any of the plans because their industry is likely to be reduced down to only a small fraction of its

current size. Given the beverage’s iconic cultural status, producers would also garner significant public support in

10

As the most widely consumed alcoholic beverages are quite cheap (economic beer and white liquors), the bulk of revenue

comes from the specific taxation component rather than ad valorem. It is difficult to maintain the revenue base with specific

taxation less than 250 baht/L. 11

Measured as the variance in effective tax rates per Litre of pure alcohol between the main three beverage categories of beer,

white liquor and color spirits. 12

Measured as the proportion of liquor tax revenue borne by consumers of beer and white liquor consumers.

Criteria PLAN A PLAN B PLAN C PLAN D

Reduced Consumption No No Yes Most

Revenue Neutrality Increased Rev. Increased Rev. Yes Yes

Protects Industry Import Duties Import Duties Import Duties Import Duties

Improved Efficiency11

Most Yes Yes Yes

Social Regressivity12

Least Regressive Most Regressive Moderate Reg. Least Regressive

Admin. Feasible Most Yes Yes Most

Politically Feasible Devastate White

Liquor Industry

Devastate White

Liquor Industry

Devastate White

Liquor Industry

Devastate White

Liquor Industry

opposing the reforms. It is unknown whether this industry, without realising economies of scale, could recover

from the implementation of Plan A were prices to rise over six-fold. Plan C would do the least damage to this

traditional industry but would still decrease it to 25% of its former size. Currently to devastate this iconic

traditional industry with such a rapid policy reform will be politically costly, if not completely infeasible.

In contrast domestic beer and blended whiskey producers are likely to support any reform over the status quo as

consumers switch across to their products in large numbers. Large beer and whisky producers have diversified

interests across both types of products and could adapt to the new market possibilities provided by the reforms.

Plans A and B would offer the large beer and whiskey producers the greatest opportunities for increased sales.

In summary the Policy Unit of the Ministry of Finance is of the position that the Government should implement a

new alcohol excise tax policy that combines a 250 baht/L specific tax together with a 100% ad valorem component.

This policy is superior to the plans proposed by the Excise Department because compared with Plan C it further

reduces alcohol consumption, is less socially regressive without increasing overall taxation and more simple in

implementation. While the Government can expect opposition from traditional white liquor producers, this is

inevitable with any reform as currently these producers are enjoying an unsustainable level of preference. This

treatment is one of the major factors facilitating the availability of cheap, hard liquor across Thailand. If the

Government proceeds with any of the reforms it should be aware of this inevitable community opposition and seek

policy measures to soften its impact on small-scale white liquor producers.

TABLE AND FIGURES

Table 1: Effective Tax Rates and Price Elasticity of Demand for Major Alcoholic Beverage Categories

PLAN A

PLAN B

PLAN C

PLAN D

∆P/P ∆C/C ∆R/R ∆P/P ∆C/C ∆R/R ∆P/P ∆C/C ∆R/R ∆P/P ∆C/C ∆R/R

Beer -18% 235% 174% 123% 221% 431% 109% -11% 12% 144% -57% -4%

Wine -83% 50% -75% 107% -64% -57% 100% -60% -60% 128% -77% -60%

White Liquors 614% -87% -9% 389% -79% 186% 202% -75% 34% 237% -83% 18%

Color Spirits 35% 249% 370% 202% 77% 316% 89% 57% 34% 100% 71% 70%

Imported Liquors -29% 18% -17% 144% -88% -72% 115% -70% -57% 145% -89% -100%

Table 2: Projected Percentage Change in Price, Consumption and Revenue for Major Alcoholic

Beverage Categories

Tax Per Litre of

Beverage Tax Per Litre of

Alcohol Elasticity

(baht/L) (baht/L) of Demand

Color Spirits 145 371 -1.56

Blended 160 400 Compounded 84 240 White Liquors 28 70 -2.73

Beers 39 613 -2.68

Imported Liquors 283 708 -0.61

Wine 409 3030 -0.6

Revenue from Alcohol Excise

Overall Alcohol Consumed

(bns of baht) (mns of litres)

STATUS QUO 6.9

19.43

PLAN A 17.1

34.28

PLAN B 26.6

26.94

PLAN C 7.2

13.62

PLAN D 7.1 10.78

Table 3: Comparison of Projected Liquor Tax Revenue and Overall Alcohol Consumed

Figure 1: Liquor Tax Revenue, By Source

0

5

10

15

20

25

30

Status Quo Plan A Plan B Plan C Plan D

Liquor Excise Revenue By Source (bns of baht)

Color Spirits White Liquors Beers Imported Liquors Wine