evaluating credit risk models using loss density forecasts: a synopsis amanda k. geck undergraduate...

TRANSCRIPT

Evaluating Credit Risk Models Using Loss Density Forecasts:

A Synopsis

Amanda K. Geck

Undergraduate Student

Department of Computational and Applied Mathematics

Rice University

November 12, 2003

Outline

Background information/motivation

Frerichs-Löffler evaluation framework, Berkowitz procedure

Two-state model, Multi-state model

Applications

Conclusions

Background information/motivationFrerichs-Löffler evaluation framework, Berkowitz procedure

Two-state model, Multi-state model

Applications

Conclusions

What is credit risk?

Credit risk is the chance that a borrower will default on a loan

Firm defaults when asset value drops below critical value determined by liabilities (Merton 1974)

Who uses credit risk models?

Banks

Bank regulators

Risk managers

What is a portfolio credit risk model?

Quantifies potential losses/gains from holding portfolio of risky debt

Produces probability distribution for value effects of credit-related events

Characteristics of portfolio credit risk models

Some restrict analysis to losses from defaults

Some include effects of credit quality changes

Many capture credit event correlations through correlated latent variables

Limitations

Scarcity of credit events

Long forecast horizons

Data limitations

Evaluation procedure concerns

Research Scarce

Only empirical paper: Nickell, Perraudin, Varotto (2001)

Only theoretical paper: Lopez, Saidenberg (2001)

Background information/motivation

Frerichs-Löffler evaluation framework, Berkowitz procedureTwo-state model, Multi-state model

Applications

Conclusions

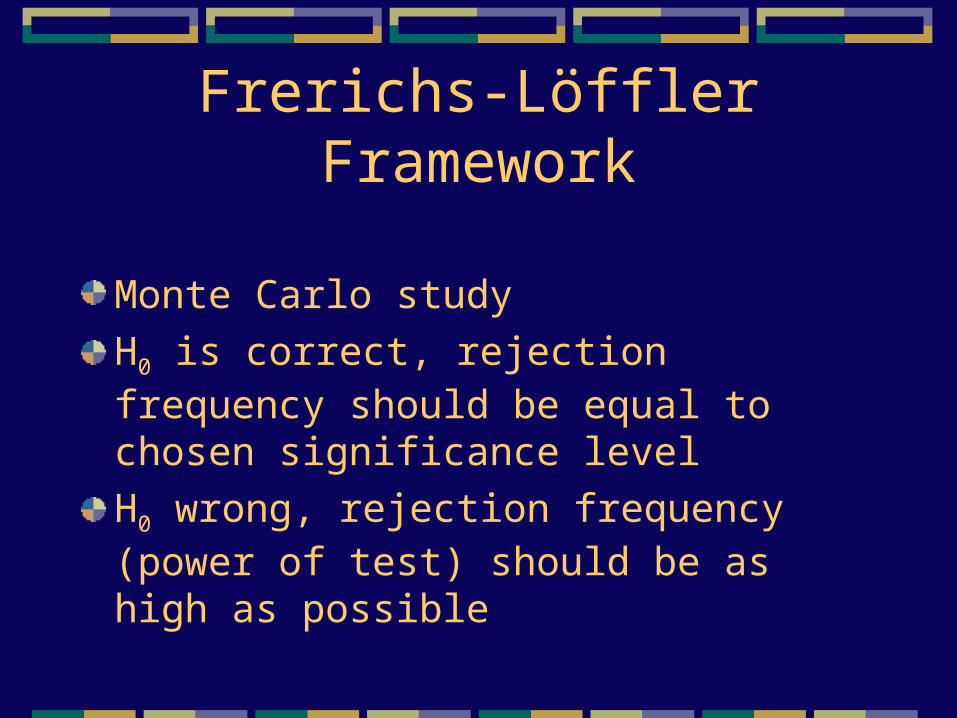

Frerichs-Löffler Framework

Monte Carlo study

H0 is correct, rejection frequency should be equal to chosen significance level

H0 wrong, rejection frequency (power of test) should be as high as possible

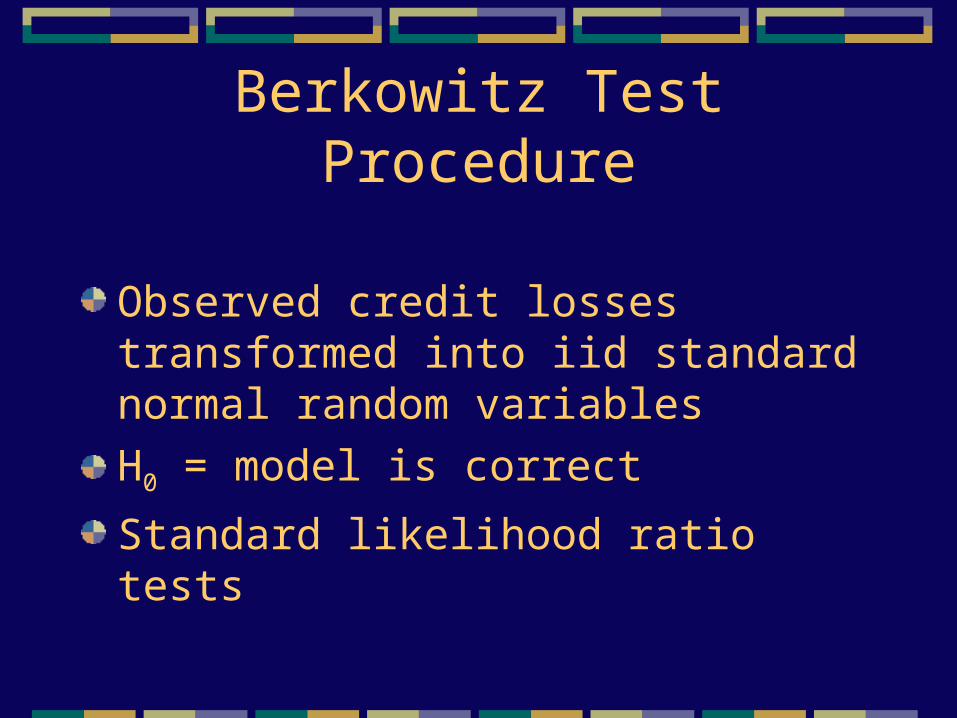

Berkowitz Test Procedure

Observed credit losses transformed into iid standard normal random variables

H0 = model is correct

Standard likelihood ratio tests

Background information/motivation

Frerichs-Löffler evaluation framework, Berkowitz procedure

Two-state model, Multi-state modelApplications

Conclusions

Two-state model

Neglects migration risk and recovery rate

Describes full loss distribution by distribution of number of defaults in portfolio

Why a two-state model?

Little data requirements

Consistent data not available for recovery rates

Data available for number of recent defaults

Base Case Setup

No recovery in case of default

10,000 borrowers in portfolio

1% unconditional default probability

Uniform asset correlation in true data-generating model = w2 = 5%

Asset value distribution N(0,1)

10 year credit loss history

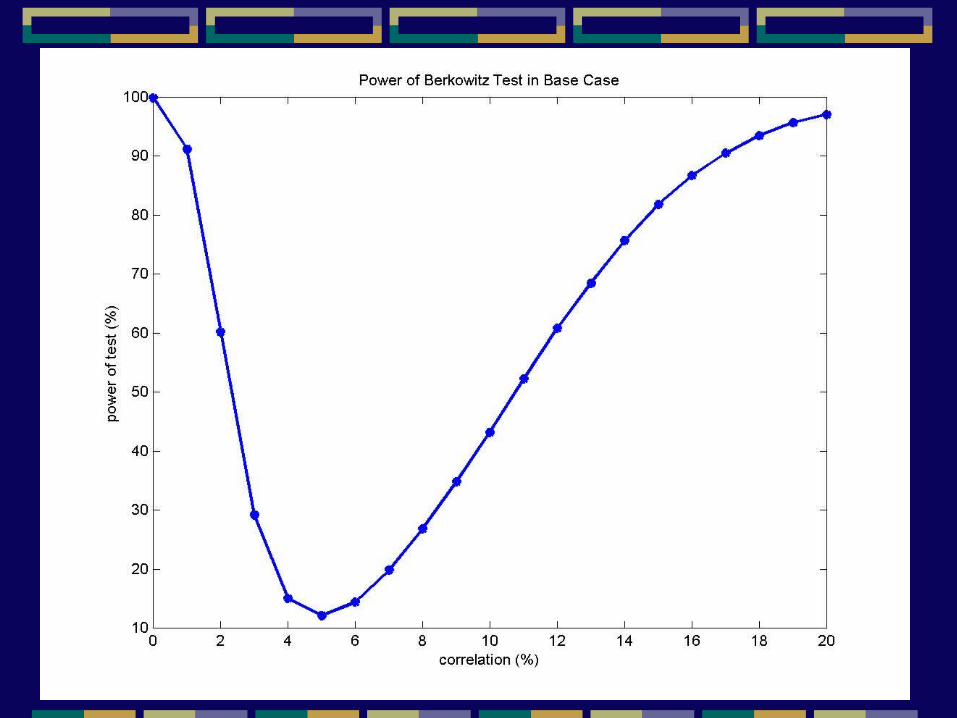

Base Case

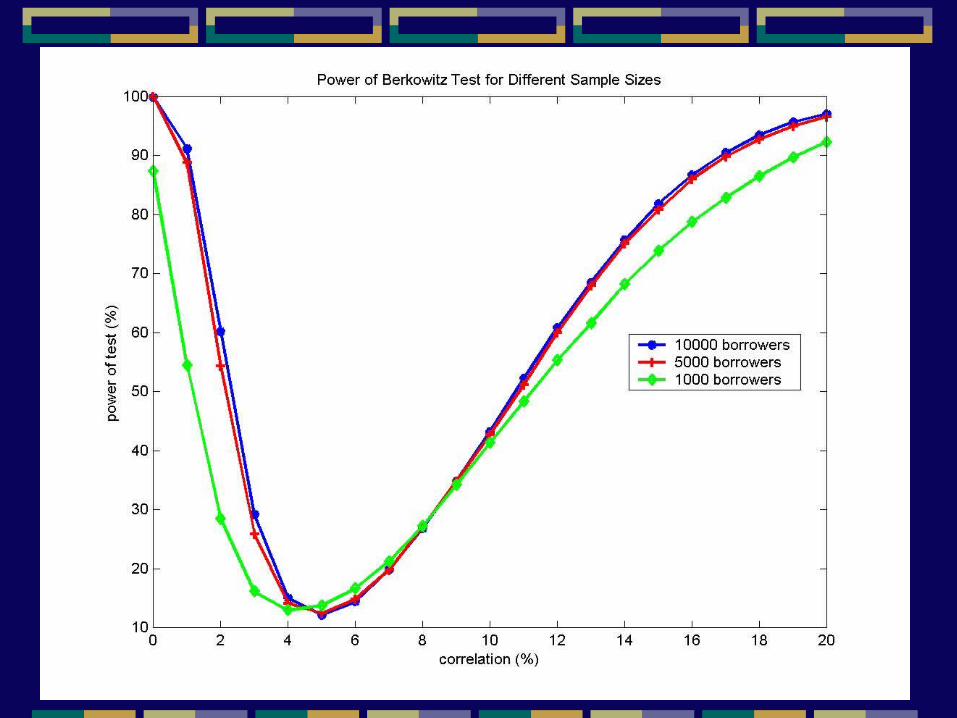

Different Sample Sizes

Different Histories

Issues with two-state model

Choosing an appropriate asset correlation value

Detecting misspecifications in asset correlation when default probability estimates noisy

Heterogeneous portfolio

Split portfolio into seven rating classes

Add noise: Overestimate by 50% default probabilities

for half of borrowers in each rating classUnderestimate by 50% for other half

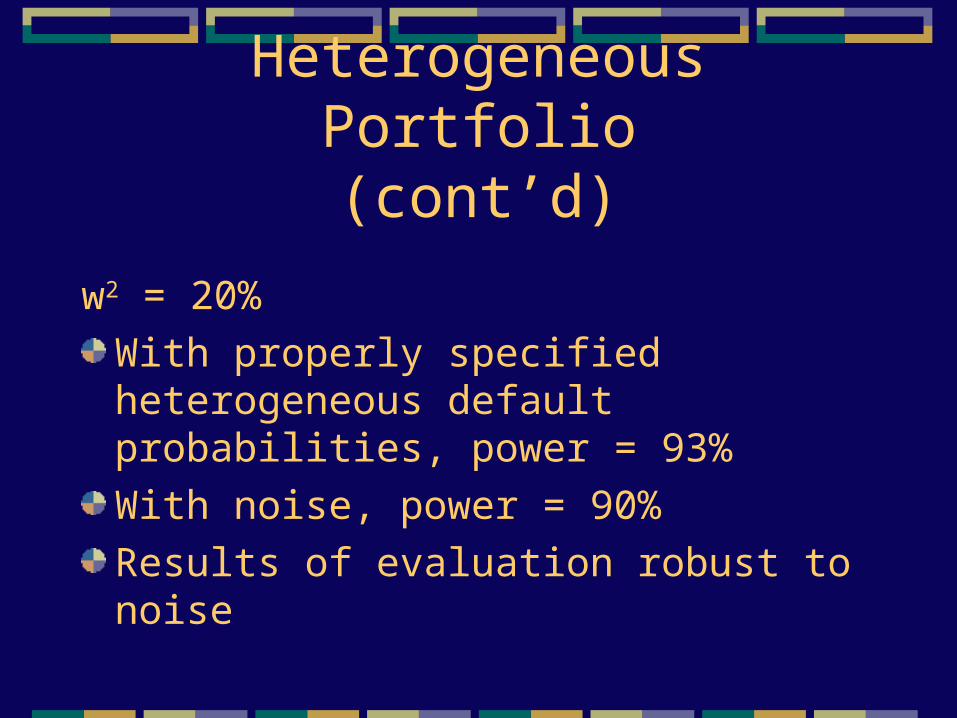

Heterogeneous Portfolio(cont’d)

w2 = 20%

With properly specified heterogeneous default probabilities, power = 93%

With noise, power = 90%

Results of evaluation robust to noise

Heterogeneous Default Probabilities

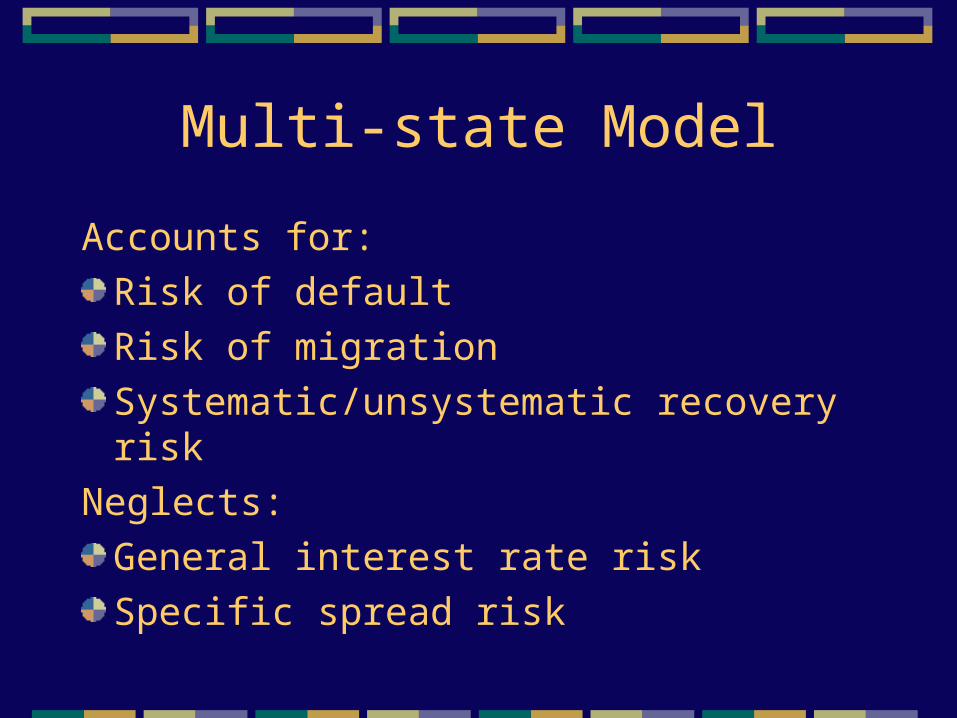

Multi-state Model

Accounts for:

Risk of default

Risk of migration

Systematic/unsystematic recovery risk

Neglects:

General interest rate risk

Specific spread risk

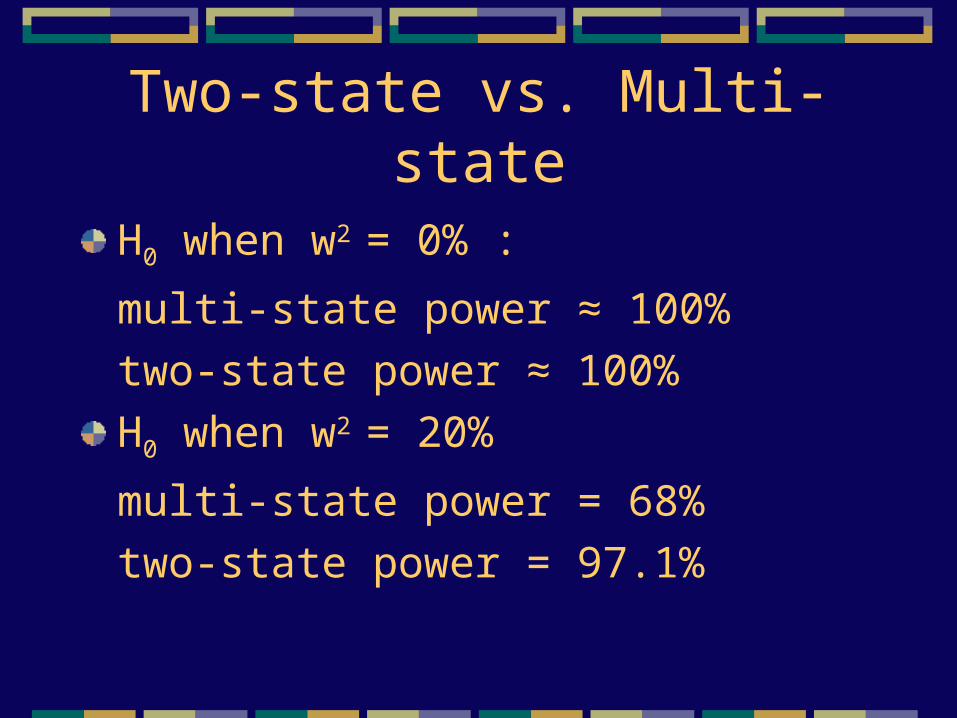

Two-state vs. Multi-state

H0 when w2 = 0% :

multi-state power ≈ 100%

two-state power ≈ 100%

H0 when w2 = 20%

multi-state power = 68%

two-state power = 97.1%

Why is two-state power higher?

Compare unexpected losses

Multi-state: w2 = 20% leads to unexpected loss 1.7 times higher than with w2 = 5%

Two-state: same ratio is 3 times higher

Background information/motivation

Frerichs-Löffler evaluation framework, Berkowitz procedure

Two-state model, Multi-state model

ApplicationsConclusions

Applications for Banks

Use evaluation method to:

Confirm or improve chosen model specifications

Assess powers of models applied to bank’s data

Decide weight given to results in specification process

Applications for Regulators

Validate underlying assumptions of new capital adequacy framework (Basel Committee, 2001)Encourage banks with enough records of past losses to check consistency with Basel assumptionsCheck if assumptions sufficient on average

Background information/motivation

Frerichs-Löffler evaluation framework, Berkowitz procedure

Two-state model, Multi-state model

Applications

Conclusions

Conclusions

Tests good for identifying misspecifications of asset value distribution

Results robust to variations in portfolio size and composition

Power significantly better for two-state model than for multi-state

Reference

Frerichs and Löffler, “Evaluating Credit Risk Models Using Loss Density Forecasts”, Journal of Risk, Summer 2003