european summer update - harris williams

TRANSCRIPT

www.harriswilliams.com

www.harriswilliams.de

European Summer

Update August 2013

63 Brook Street

London W1K 4HS

United Kingdom

Phone: +44 20 7518 8900

Red Norrie

Managing Director

Julien Darmon

Managing Director

Thierry Monjauze

Managing Director

Francois Morin

Director

Jeffery Perkins

Managing Director

An der Welle 4

60322 Frankfurt am Main

Germany

Phone: +49 69 7593 7166

Quarterly Quick Read

European

Economic

Environment1

European M&A

Deal Volume

Activity9

GDP2 Manufacturing

Confidence3 Consumer Confidence3

+25.0%

Inbound

M&A Deal Volume

to Europe9

Consumer Prices3

(0.7%)

M&A

Environment

• European M&A activity declined across nearly all sectors in Q2 2013, falling 7% compared to Q2 2012. However, the pace of

decline has slowed compared with the three previous quarters, amid early signs of improved economic conditions

• UK & Eire accounted for 37% of overall European activity by volume compared to 33% in Q1 2013. M&A activity in the

Benelux region increased by 10% in volume compared to Q1 2013

1

European Equity

Market8

TMT

• Vodafone acquired Kabel Deutschland, Germany’s biggest cable operator, in a €7.7 billion deal and plans on completing the

transaction in the next quarter

• Springer Science+Business Media, the academic and business publisher, was acquired by BC Partners for €3.3bn in the

largest private equity deal in Germany for seven years

Consumer

• EU Consumer Confidence index is on the rise increasing by 4.1 points to reach (17.5). Consumer confidence has improved

for seven consecutive months in EU

• UK retail is gaining momentum with sales volume in Q2 2013 up by 0.9% over Q1 2013 and by 1.8% over Q2 2012,

positively affected by the non-food segment and product discounts

ADG

• 50th International Paris Air Show in June resulted in $150 billion of signed contracts and demonstrated the continuing battle

between Boeing and Airbus, which booked 570 and 327 jet orders in Q2 2013, respectively

• The global airline sector continued to expand at a solid rate in Q2 2013 – the global air travel market expanded by 4.3% in

2013 May YTD compared to the same period in 2012, driven by recovering European market and growth in emerging regions

Healthcare & Life

Sciences

• Senior health officials warned the NHS is facing a potential £30 billion funding gap by 2020

• Thermo Fisher, the US laboratory equipment manufacturer, acquired Life Technologies, the producer of testing equipment

used in DNA analysis, for $13.6 billion

Energy & Power

• The trend of divestures of non-core assets by leading power utility companies such as Dong Energy, Total, Enel, Iberdrola,

E.ON, RWE, and GDF Suez continued in Q2 2013

• International major Oil & Gas companies continue to seek exposure to the European oilfield service and equipment market as

demonstrated by the acquisition of Blohm+Voss Oil Tools by Forum Energy as well as the announced acquisition of Fred

Olsen Production by Yinson

• The IMF estimated a 3.3% increase in global GDP during 2013, down 20 bps from its January 2013 outlook but modestly

above 2012 growth of 3.2%

• Invensys, the UK engineering group, received a takeover approach from Schneider Electric, the French power equipment

group, valuing the company at €3.1 billion. The deal would provide Schneider access to key electro-intensive segments as

well as energy management

Diversified

Industrials

Business Services

• In its recent report, the CBI highlighted the UK’s clear competitive advantage in Business Services and estimates there to be

£30 billion worth of export opportunities in the sector by 2020

• The Big Four accountancy groups appear primed for further expansion in the consulting market, with PwC, Deloitte and E&Y

all linked with potential bids for Roland Berger, the strategy consultant

Notes: For the purposes of this Quarterly Update, Europe is defined as: United Kingdom, Eire, France, DACH (Germany, Austria, Switzerland), Spain, Italy, Benelux

(Belgium, The Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland); Evolution calculation based on the quarter finishing 30 June, 2013

(1) For the countries based in the EU27; (2) Year-on-year GDP growth for Q1 2013; (3) PMI, CCI and CPI quarterly growth shown for March 2013- June 2013;

(4) Aerospace, Defence & Government Services; (5) Also includes Building Products and Paper & Packaging; (6) Telecom, Media & Technology; (7) Also includes Speciality

Distribution; (8) For all listed companies based in the countries mentioned above and with a market cap greater than €50m; (9) Change from Q1 2013 to Q2 2013

(6.4%) (1.1%)

TMT6 Consumer Diversified

Industrials5

Transport &

Logistics7 ADG4 Business

Services

Healthcare &

Life Sciences

Energy &

Power

Transport &

Logistics

• Talks have opened between the European Union and the US aimed at removing trade and investment barriers through creating

the world's largest free trade zone

• IATA upgraded global outlook for the airline industry in 2013, forecasting $711 billion of revenues and $12.7 billion profit,

higher than projection in March ($671 billion and $10.6 billion, respectively)

(16.7%)

(0.1%)

0.0%

Sources: Eurostat, Bloomberg, Markit Economics, S&P Capital IQ

(4.2%) (5.9%) 300.0%

(66.7%) (5.9%) 41.7%

4.9%

Last Quarter 2.2% (2.6%) (1.4%) (2.3%) (5.6%) (1.0%) (0.9%) 2.0%

Last Year 29.8% 21.1% 15.6% 15.9% (1.2%) 19.0% 15.1% 20.8%

Last 3 Years 51.4% 23.8% 24.1% 18.6% (8.0%) (1.0%) 25.6% 10.9%

(35.3%) (28.6%)

NM 0.0% (14.3%) (13.5%)

Key Countries % Y-o-Y Growth

Q1 14E Q1 13A

(20%)

(15%)

(10%)

(5%)

0%

5%

10%

(40)

(30)

(20)

(10)

0

10

20

Jun-09 Jun-10 Jun-11 Jun-12 Jun-13

Co

nsu

mer

Pri

ce I

nd

ex (

%)

Co

nsu

mer

Co

nfi

den

ce I

nd

ica

tor

CCI CPI Y-o-Y %

40

45

50

55

60

(10%)

(5%)

0%

5%

10%

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13

PM

I In

dex

Va

lue

Ch

an

ge in

PM

I (M

-o-M

)

Change (M-o-M %) Eurozone PMI

(6%)

(4%)

(2%)

0%

2%

4%

6%

Q4 08 Q2 09 Q4 09 Q2 10 Q4 10 Q2 11 Q4 11 Q2 12 Q4 12 Q2 13E Q4 13E Q2 14E Q4 14E Q2 15E Q4 15E

European Economic Climate

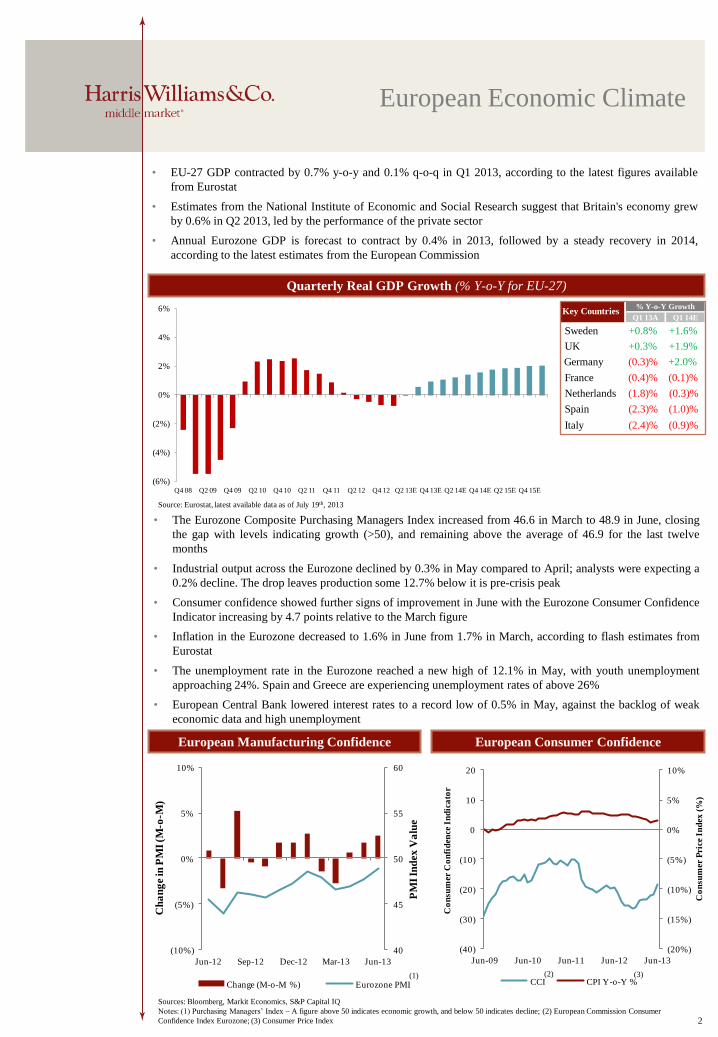

Source: Eurostat, latest available data as of July 19th, 2013

Sources: Bloomberg, Markit Economics, S&P Capital IQ

Notes: (1) Purchasing Managers’ Index – A figure above 50 indicates economic growth, and below 50 indicates decline; (2) European Commission Consumer

Confidence Index Eurozone; (3) Consumer Price Index

Quarterly Real GDP Growth (% Y-o-Y for EU-27)

European Manufacturing Confidence European Consumer Confidence

• EU-27 GDP contracted by 0.7% y-o-y and 0.1% q-o-q in Q1 2013, according to the latest figures available

from Eurostat

• Estimates from the National Institute of Economic and Social Research suggest that Britain's economy grew

by 0.6% in Q2 2013, led by the performance of the private sector

• Annual Eurozone GDP is forecast to contract by 0.4% in 2013, followed by a steady recovery in 2014,

according to the latest estimates from the European Commission

• The Eurozone Composite Purchasing Managers Index increased from 46.6 in March to 48.9 in June, closing

the gap with levels indicating growth (>50), and remaining above the average of 46.9 for the last twelve

months

• Industrial output across the Eurozone declined by 0.3% in May compared to April; analysts were expecting a

0.2% decline. The drop leaves production some 12.7% below it is pre-crisis peak

• Consumer confidence showed further signs of improvement in June with the Eurozone Consumer Confidence

Indicator increasing by 4.7 points relative to the March figure

• Inflation in the Eurozone decreased to 1.6% in June from 1.7% in March, according to flash estimates from

Eurostat

• The unemployment rate in the Eurozone reached a new high of 12.1% in May, with youth unemployment

approaching 24%. Spain and Greece are experiencing unemployment rates of above 26%

• European Central Bank lowered interest rates to a record low of 0.5% in May, against the backlog of weak

economic data and high unemployment

(1) (2) (3)

2

UK +0.3% +1.9%

Germany (0.3)% +2.0%

France (0.4)% (0.1)%

Spain (2.3)% (1.0)%

Italy (2.4)% (0.9)%

Netherlands (1.8)% (0.3)%

Sweden +0.8% +1.6%

87%

13%

Strategics Financials

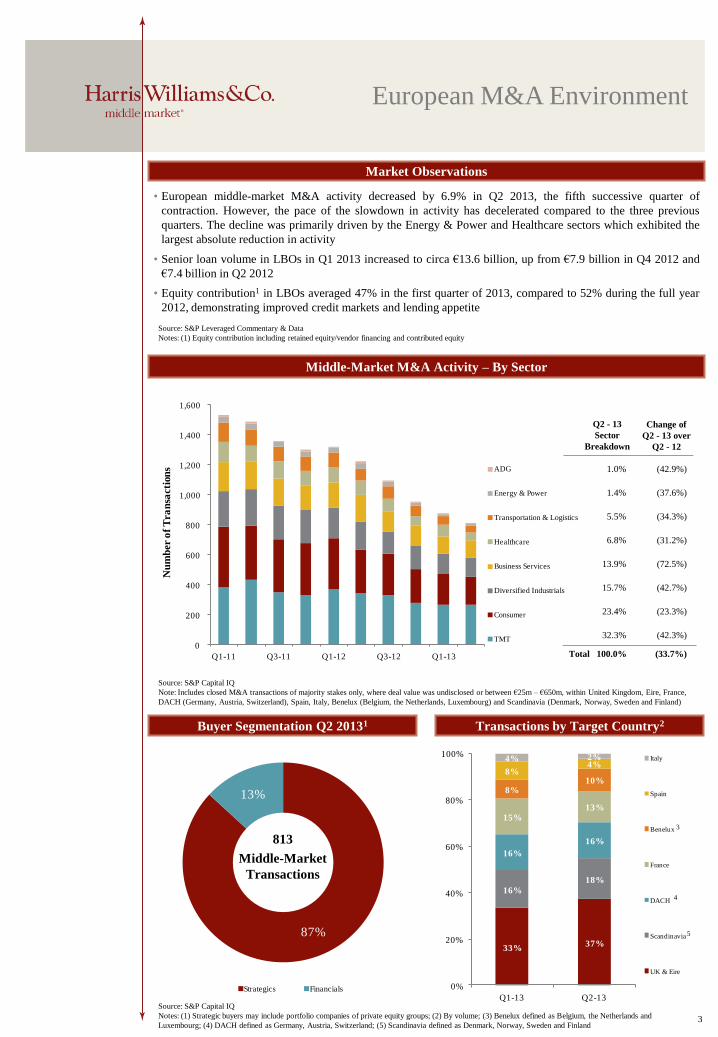

European M&A Environment

Market Observations

• European middle-market M&A activity decreased by 6.9% in Q2 2013, the fifth successive quarter of

contraction. However, the pace of the slowdown in activity has decelerated compared to the three previous

quarters. The decline was primarily driven by the Energy & Power and Healthcare sectors which exhibited the

largest absolute reduction in activity

• Senior loan volume in LBOs in Q1 2013 increased to circa €13.6 billion, up from €7.9 billion in Q4 2012 and

€7.4 billion in Q2 2012

• Equity contribution1 in LBOs averaged 47% in the first quarter of 2013, compared to 52% during the full year

2012, demonstrating improved credit markets and lending appetite

Transactions by Target Country2 Buyer Segmentation Q2 20131

813

Middle-Market

Transactions

Source: S&P Capital IQ

Notes: (1) Strategic buyers may include portfolio companies of private equity groups; (2) By volume; (3) Benelux defined as Belgium, the Netherlands and

Luxembourg; (4) DACH defined as Germany, Austria, Switzerland; (5) Scandinavia defined as Denmark, Norway, Sweden and Finland

Source: S&P Capital IQ

Note: Includes closed M&A transactions of majority stakes only, where deal value was undisclosed or between €25m – €650m, within United Kingdom, Eire, France,

DACH (Germany, Austria, Switzerland), Spain, Italy, Benelux (Belgium, the Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland)

Q2 - 13

Sector

Breakdown

1.0%

1.4%

5.5%

6.8%

13.9%

15.7%

Change of

Q2 - 13 over

Q2 - 12

23.4%

Middle-Market M&A Activity – By Sector

3

33%37%

16%

18%

16%

16%

15%

13%

8%10%

8%4%

4% 2%

0%

20%

40%

60%

80%

100%

Q1-13 Q2-13

Italy

Spain

Benelux

France

DACH

Scandinavia

UK & Eire

32.3%

100.0% Total

Source: S&P Leveraged Commentary & Data

Notes: (1) Equity contribution including retained equity/vendor financing and contributed equity

4

3

5

0

200

400

600

800

1,000

1,200

1,400

1,600

Q1-11 Q3-11 Q1-12 Q3-12 Q1-13

Nu

mb

er o

f T

ra

nsa

cti

on

s ADG

Energy & Power

Transportation & Logistics

Healthcare

Business Services

Diversified Industrials

Consumer

TMT

(42.9%)

(37.6%)

(34.3%)

(31.2%)

(42.7%)

(23.3%)

(72.5%)

(42.3%)

(33.7%)

% of Total Deal Volume Q 2-11 Q3-11 Q4-11 Q 1-12 Q2-12 Q 3-12 Q 4-12 Q 1-13 Q2-13

ADG 17% 14% 23% 0% 29% 25% 67% 50% 13%

Business Services 5% 10% 9% 10% 8% 5% 10% 10% 15%

Consumer 6% 8% 8% 9% 9% 6% 8% 8% 8%

Diversified Industrials 8% 10% 10% 8% 11% 10% 9% 11% 12%

Energy & Power 13% 18% 23% 19% 8% 7% 13% 18% 9%

Healthcare 9% 18% 9% 15% 16% 14% 6% 9% 11%

TMT 14% 20% 17% 16% 18% 21% 18% 20% 17%

Transportation & Logistics 6% 7% 7% 5% 5% 10% 3% 0% 9%

0

2,000

4,000

6,000

8,000

10,000

0

50

100

150

200

Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Q3-12 Q4-12 Q1-13 Q2-13

Dea

l V

alu

e (

€m

)

Nu

mb

er o

f T

ra

nsa

cti

on

s

International Activity by Number International Activity by Value

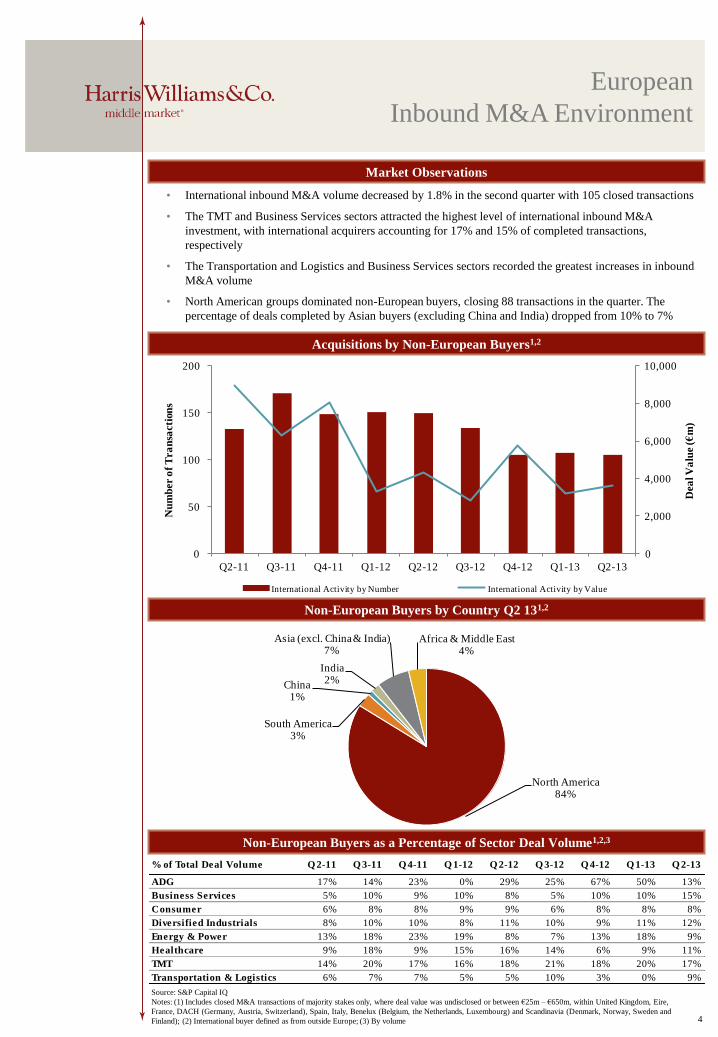

North America84%

South America3%

China1%

India2%

Asia (excl. China & India)7%

Africa & Middle East4%

European

Inbound M&A Environment

Acquisitions by Non-European Buyers1,2

Non-European Buyers by Country Q2 131,2

Non-European Buyers as a Percentage of Sector Deal Volume1,2,3

4

Market Observations

• International inbound M&A volume decreased by 1.8% in the second quarter with 105 closed transactions

• The TMT and Business Services sectors attracted the highest level of international inbound M&A

investment, with international acquirers accounting for 17% and 15% of completed transactions,

respectively

• The Transportation and Logistics and Business Services sectors recorded the greatest increases in inbound

M&A volume

• North American groups dominated non-European buyers, closing 88 transactions in the quarter. The

percentage of deals completed by Asian buyers (excluding China and India) dropped from 10% to 7%

Source: S&P Capital IQ

Notes: (1) Includes closed M&A transactions of majority stakes only, where deal value was undisclosed or between €25m – €650m, within United Kingdom, Eire,

France, DACH (Germany, Austria, Switzerland), Spain, Italy, Benelux (Belgium, the Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and

Finland); (2) International buyer defined as from outside Europe; (3) By volume

0

1

2

3

4

5

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

North America Asia (excl. China & India) China

India South America Africa & Middle East

0

2

4

6

8

10

12

14

16

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

UK & Eire Scandinavia DACH France Benelux Spain Italy

Aerospace, Defence & Government

Services

5

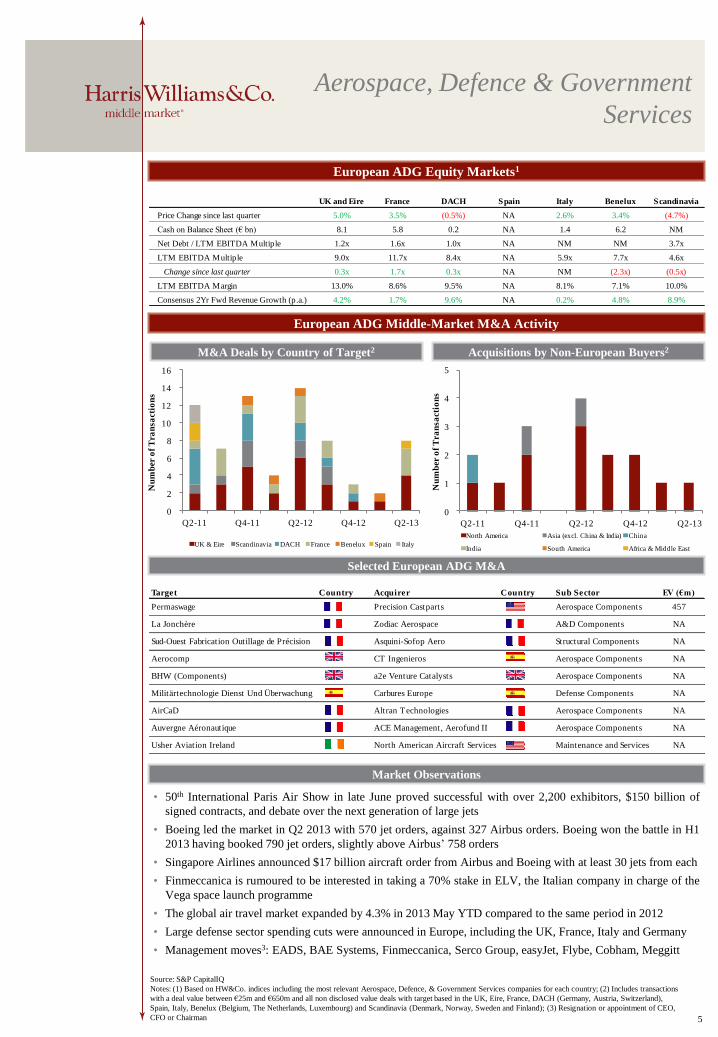

European ADG Equity Markets1

European ADG Middle-Market M&A Activity

Source: S&P CapitalIQ

Notes: (1) Based on HW&Co. indices including the most relevant Aerospace, Defence, & Government Services companies for each country; (2) Includes transactions

with a deal value between €25m and €650m and all non disclosed value deals with target based in the UK, Eire, France, DACH (Germany, Austria, Switzerland),

Spain, Italy, Benelux (Belgium, The Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland); (3) Resignation or appointment of CEO,

CFO or Chairman

M&A Deals by Country of Target2 Acquisitions by Non-European Buyers2

Selected European ADG M&A

Market Observations

• 50th International Paris Air Show in late June proved successful with over 2,200 exhibitors, $150 billion of

signed contracts, and debate over the next generation of large jets

• Boeing led the market in Q2 2013 with 570 jet orders, against 327 Airbus orders. Boeing won the battle in H1

2013 having booked 790 jet orders, slightly above Airbus’ 758 orders

• Singapore Airlines announced $17 billion aircraft order from Airbus and Boeing with at least 30 jets from each

• Finmeccanica is rumoured to be interested in taking a 70% stake in ELV, the Italian company in charge of the

Vega space launch programme

• The global air travel market expanded by 4.3% in 2013 May YTD compared to the same period in 2012

• Large defense sector spending cuts were announced in Europe, including the UK, France, Italy and Germany

• Management moves3: EADS, BAE Systems, Finmeccanica, Serco Group, easyJet, Flybe, Cobham, Meggitt

Target Country Acquirer Country Sub Sector EV (€m)

Permaswage Precision Castparts Aerospace Components 457

La Jonchère Zodiac Aerospace A&D Components NA

Sud-Ouest Fabrication Outillage de Précision Asquini-Sofop Aero Structural Components NA

Aerocomp CT Ingenieros Aerospace Components NA

BHW (Components) a2e Venture Catalysts Aerospace Components NA

Militärtechnologie Dienst Und Überwachung Carbures Europe Defense Components NA

AirCaD Altran Technologies Aerospace Components NA

Auvergne Aéronautique ACE Management, Aerofund II Aerospace Components NA

Usher Aviation Ireland North American Aircraft Services Maintenance and Services NA

UK and Eire France DACH Spain Italy Benelux Scandinavia

Price Change since last quarter 5.0% 3.5% (0.5%) NA 2.6% 3.4% (4.7%)

Cash on Balance Sheet (€ bn) 8.1 5.8 0.2 NA 1.4 6.2 NM

Net Debt / LTM EBITDA Multiple 1.2x 1.6x 1.0x NA NM NM 3.7x

LTM EBITDA Multiple 9.0x 11.7x 8.4x NA 5.9x 7.7x 4.6x

Change since last quarter 0.3x 1.7x 0.3x NA NM (2.3x) (0.5x)

LTM EBITDA Margin 13.0% 8.6% 9.5% NA 8.1% 7.1% 10.0%

Consensus 2Yr Fwd Revenue Growth (p.a.) 4.2% 1.7% 9.6% NA 0.2% 4.8% 8.9%

0

5

10

15

20

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

North America Asia (excl. China & India)China IndiaSouth America Africa & Middle East

0

50

100

150

200

250

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

UK & Eire Scandinavia DACH France Benelux Spain Italy

Business Services

6

European Business Services Equity Markets1

European Business Services Middle-Market M&A Activity

M&A Deals by Country of Target2 Acquisitions by Non-European Buyers2

Selected European Business Services M&A

Market Observations

• The CBI released a new report on the importance of the Business and Professional Services sector to the UK

economy, highlighting the UK’s clear competitive advantage and estimating £30 billion of export opportunities

by 2020. The UK has the highest trade surplus in the Business Services sector amongst the OECD countries

• The Big Four accountancy groups appear primed for further expansion in the consulting market, with PwC,

Deloitte and E&Y all linked with potential bids for Roland Berger, the strategy consultant. The Big Four are

looking for ways to increase their higher margin consulting businesses, as their core audit operations come

under regulatory pressure

• Management moves3: Capita, G4S, Serco, Hays, Caverion Corporation, Impellam Group, Harvey Nash Group

Source: S&P CapitalIQ

Notes: (1) Based on HW&Co. indices including the most relevant Business Services companies for each country; (2) Includes transactions with a deal value between

€25m and €650m and all non disclosed value deals with target based in the UK, Eire, France, DACH (Germany, Austria, Switzerland), Spain, Italy, Benelux (Belgium,

The Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland); (3) Resignation or appointment of CEO, CFO or Chairman

Target Country Acquirer Country Sub Sector EV (€m)

Gazeley UK Brookfield Property Partners Distribution 353

Portfolio of Logistics Properties Apollo Global Management Distribution 145

Nimbus Park Tritax Securities Distribution 43

KnowledgePool Group Capita Education Services 28

CMFT Groupe Climater Maintenance Services NA

Protección y Seguridad del Noroeste Segur Ibérica Security Services NA

MPB France S.A.-Matières Plastique Paprec Waste Management NA

Blue Sky Performance Improvement Capita Education Services NA

Sony Mobile Communications Lab Tech Mahindra Testing Services NA

LVQ-WP Werkstoffprufung Bureau Veritas Testing Services NA

UK and Eire France DACH Spain Italy Benelux Scandinavia

Price Change since last quarter (0.2%) (4.9%) (2.7%) (1.6%) -% (4.9%) (4.4%)

Cash on Balance Sheet (€ bn) 4.8 9.8 3.9 152.7 33.8 0.8 NM

Net Debt / LTM EBITDA Multiple 1.4x 1.5x 1.0x 8.8x 4.8x 2.7x 2.6x

LTM EBITDA Multiple 10.0x 6.7x 8.7x 12.6x 13.8x 8.9x 9.2x

Change since last quarter 1.2x (0.3x) (0.1x) 1.9x 3.9x (0.7x) (0.6x)

LTM EBITDA Margin 9.3% 10.2% 5.9% 7.4% 5.2% 4.1% 8.5%

Consensus 2Yr Fwd Revenue Growth (p.a.) 6.1% 3.8% 3.5% 0.4% 3.3% 4.4% 2.5%

Target Country Acquirer Country Sub Sector EV (€m)

Vue Entertainment OMERS; Alberta IMC Entertainment 1,085

Groupe SMCP KKR Apparel 998

Club Méditerranée AXA; Fosun International Travel 724

Pomellato Kering (previously PPR) Jewellery 366

HMV Group Hilco UK Specialty Retail 259

Burn Stewart Distillers Distell Group Beverage 215

WCL Group Nord Anglia Education Education 180

Medstop Group Holding Orion Holding Sverige Pharmacy 176

Kidsunlimited Bright Horizons Family Solutions Nursery 51

Ella's Kitchen Group The Hain Celestial Group Food Retail 34

HIB Trim Part Solutions NBHX Trim Specialty Retail 34

0

5

10

15

20

25

30

35

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

North America Asia (excl. China & India) China

India South America Africa & Middle East

0

50

100

150

200

250

300

350

400

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

UK & Eire Scandinavia DACH France Benelux Spain Italy

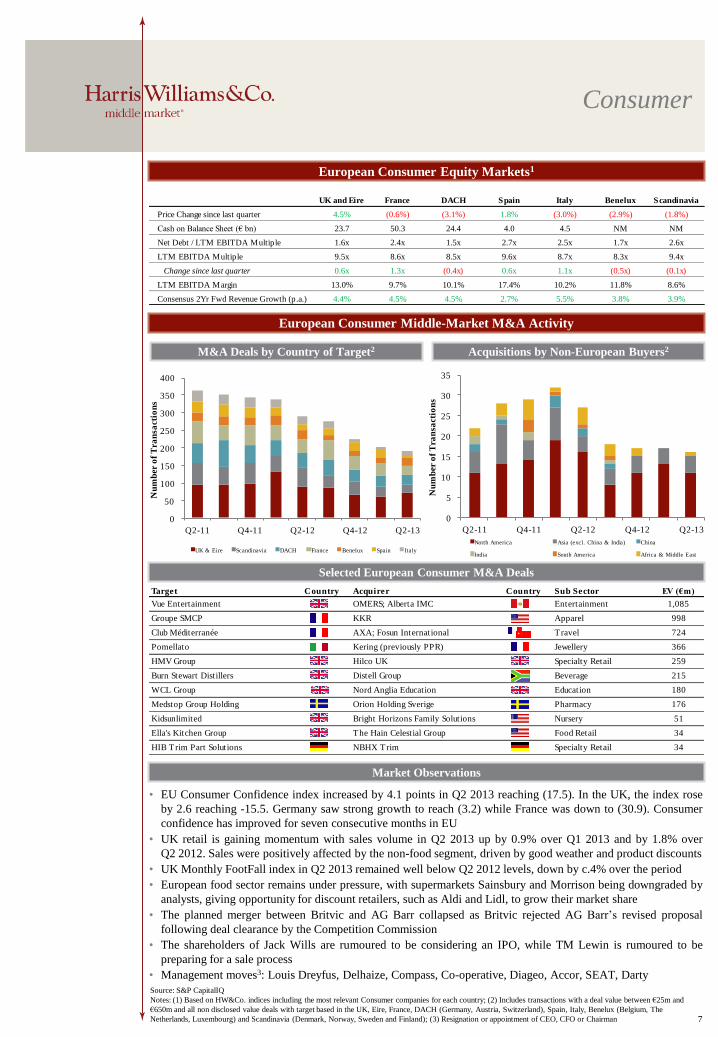

Consumer

European Consumer Equity Markets1

European Consumer Middle-Market M&A Activity

M&A Deals by Country of Target2 Acquisitions by Non-European Buyers2

Source: S&P CapitalIQ

Notes: (1) Based on HW&Co. indices including the most relevant Consumer companies for each country; (2) Includes transactions with a deal value between €25m and

€650m and all non disclosed value deals with target based in the UK, Eire, France, DACH (Germany, Austria, Switzerland), Spain, Italy, Benelux (Belgium, The

Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland); (3) Resignation or appointment of CEO, CFO or Chairman

Selected European Consumer M&A Deals

• EU Consumer Confidence index increased by 4.1 points in Q2 2013 reaching (17.5). In the UK, the index rose

by 2.6 reaching -15.5. Germany saw strong growth to reach (3.2) while France was down to (30.9). Consumer

confidence has improved for seven consecutive months in EU

• UK retail is gaining momentum with sales volume in Q2 2013 up by 0.9% over Q1 2013 and by 1.8% over

Q2 2012. Sales were positively affected by the non-food segment, driven by good weather and product discounts

• UK Monthly FootFall index in Q2 2013 remained well below Q2 2012 levels, down by c.4% over the period

• European food sector remains under pressure, with supermarkets Sainsbury and Morrison being downgraded by

analysts, giving opportunity for discount retailers, such as Aldi and Lidl, to grow their market share

• The planned merger between Britvic and AG Barr collapsed as Britvic rejected AG Barr’s revised proposal

following deal clearance by the Competition Commission

• The shareholders of Jack Wills are rumoured to be considering an IPO, while TM Lewin is rumoured to be

preparing for a sale process

• Management moves3: Louis Dreyfus, Delhaize, Compass, Co-operative, Diageo, Accor, SEAT, Darty

Market Observations

UK and Eire France DACH Spain Italy Benelux Scandinavia

Price Change since last quarter 4.5% (0.6%) (3.1%) 1.8% (3.0%) (2.9%) (1.8%)

Cash on Balance Sheet (€ bn) 23.7 50.3 24.4 4.0 4.5 NM NM

Net Debt / LTM EBITDA Multiple 1.6x 2.4x 1.5x 2.7x 2.5x 1.7x 2.6x

LTM EBITDA Multiple 9.5x 8.6x 8.5x 9.6x 8.7x 8.3x 9.4x

Change since last quarter 0.6x 1.3x (0.4x) 0.6x 1.1x (0.5x) (0.1x)

LTM EBITDA Margin 13.0% 9.7% 10.1% 17.4% 10.2% 11.8% 8.6%

Consensus 2Yr Fwd Revenue Growth (p.a.) 4.4% 4.5% 4.5% 2.7% 5.5% 3.8% 3.9%

7

Diversified Industrials

European Diversified Industrials Equity Markets1

European Diversified Industrials Middle-Market M&A Activity

M&A Deals by Country of Target2 Acquisitions by Non-European Buyers2

Selected European Diversified Industrials M&A

Market Observations

• The IMF estimated a 3.3% increase in global GDP during 2013, down 20 bps from its January 2013 outlook

but modestly above 2012 growth of 3.2%

• At 50.6 in June, unchanged from May, the global PMI index indicated an expansion of the global

manufacturing sector for the sixth month running, signaling further increase in output and new orders

• Several large European industrial manufacturers have recently announced planned divestitures, including

GEA’s announcement to divest its €1.3 billion Heat Exchanger business and Siemens’ announcement to divest

its €1 billion Water Technologies business

• An acquisition of Invensys by Schneider would provide cost synergies between the two companies and provide

Schneider access to key electro-intensive segments as well as energy management offerings and the fast-

growing software business for industrial operational efficiency

• Management moves3: ABB, WashTec, SKF, Sensata Technologies, FLSmidth & Co.

Source: S&P CapitalIQ

Notes: (1) Based on HW&Co. indices including the most relevant Diversified Industrials companies for each country; (2) Includes transactions with a deal value

between €25m and €650m and all non disclosed value deals with target based in the UK, Eire, France, DACH (Germany, Austria, Switzerland), Spain, Italy, Benelux

(Belgium, The Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland); (3) Resignation or appointment of CEO, CFO or Chairman

Target Country Acquirer Country Sub Sector EV (€m)

0

50

100

150

200

250

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ra

nsa

cti

on

s

UK & Eire Scandinavia DACH France Benelux Spain Italy

0

5

10

15

20

25

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ra

nsa

cti

on

s

North America Asia (excl. China & India) China

India South America Africa & Middle East

UK and Eire France DACH Spain Italy Benelux Scandinavia

Price Change since last quarter 1.5% (2.2%) (2.9%) (1.7%) (2.3%) (3.0%) (5.2%)

Cash on Balance Sheet (€ bn) 7.5 29.8 33.8 10.9 10.0 8.0 NM

Net Debt / LTM EBITDA Multiple 1.3x 1.8x 1.6x 5.2x 3.4x 2.0x 2.1x

LTM EBITDA Multiple 8.4x 7.0x 8.2x 7.7x 8.3x 8.4x 9.5x

Change since last quarter (0.3x) 0.0x (0.2x) (0.2x) 0.9x 0.0x 0.1x

LTM EBITDA Margin 10.7% 10.1% 9.4% 10.1% 10.9% 10.4% 9.5%

Consensus 2Yr Fwd Revenue Growth (p.a.) 4.4% 3.3% 4.6% 1.8% 3.8% 4.0% 3.1%

8

ista International CVC Capital Partners Utility Metering 4,079

Invensys Schneider Electric Capital Equipment 3,054

CeramTec Cinven Construction Materials 1,490

Schmolz + Bickenbach Renova Industries Steel 1,210

Armacell Charterhouse Capital Partners Chemicals 500

The Flexitallic Group Bridgepoint Advisers Automotive 450

Marelli Motori The Carlyle Group Heavy Electrical Equipment 212

European Energy & Power Equity Markets1

European Energy & Power Middle-Market M&A Activity

Energy & Power

M&A Deals by Country of Target2 Acquisitions by Non-European Buyers2

Selected European Energy & Power M&A3

Market Observations

• In Q2 2013, the trend of divestures of non-core assets by leading power utility companies continued. DONG

Energy exited several onshore wind power as well as hydropower assets and E.ON announced the sale of the

regional utility E.ON Westfalen Weser

• Generalist Private Equity Groups as well as specialized E&P and Infrastructure investors are increasingly

taking the opportunity to benefit from legislative changes and challenging dynamics for large utilities by e.g.

acquiring mothballed gas power plants and betting on a medium-term market turnaround

• International major Oil & Gas companies continue to seek exposure to the European oilfield service and

equipment market. Key transactions in Q2 include the acquisition of Blohm+Voss Oil Tools by Forum Energy

as well as the announced acquisition of Fred Olsen Production by Yinson

• Management moves4: Vestas, Iofina, Norwegian Energy, Faroe Petroleum, Bergen Group, Gulfsands Petroleum

9

Source: S&P CapitalIQ

Notes: (1) Based on HW&Co. indices including the most relevant Energy & Power companies for each country

(2) Includes transactions with a deal value between €25m and €650m and all non disclosed value deals with target based in the UK, Eire, France, DACH (Germany,

Austria, Switzerland), Spain, Italy, Benelux (Belgium, The Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland); (3) Includes

acquisitions of majority stakes only (4) Resignation or appointment of CEO or CFO

0

5

10

15

20

25

30

35

40

45

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er

of

Tra

nsa

ctio

ns

UK & Eire Scandinavia DACH France Benelux Spain Italy

0

1

2

3

4

5

6

7

8

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ra

nsa

cti

on

s

North America Asia (excl. China & India) China

India South America Africa & Middle East

UK and Eire France DACH Spain Italy Benelux Scandinavia

Price Change since last quarter (13.8%) (1.5%) (4.4%) 8.8% (1.1%) (2.2%) (5.7%)

Cash on Balance Sheet (€ bn) 32.6 34.0 11.5 19.0 23.0 14.8 14.4

Net Debt / LTM EBITDA Multiple 0.6x 1.9x 1.6x 3.3x 2.9x 4.4x 2.4x

LTM EBITDA Multiple 6.3x 5.3x 7.8x 7.7x 5.7x 10.3x 8.1x

Change since last quarter (0.5x) 0.4x 0.5x 0.6x (0.5x) (0.4x) 1.1x

LTM EBITDA Margin 16.4% 19.8% 15.7% 21.6% 13.7% 33.9% 34.1%

Consensus 2Yr Fwd Revenue Growth (p.a.) 18.6% 8.9% (0.3%) 0.5% (1.3%) 2.7% 6.5%

Target Country Acquirer Country Sub Sector EV (€m)

E.ON Westfalen Weser 48 German municipalities Utility 360

Fred. Olsen Production Yinson Offshore Services 235

Vestas' Gebeleisis & Hrabrovo Projects Lukerg Renew Renewables 127

DONG Energy's Onshore Wind Business PFA Renewables 101

South Staffordshire KKR Water Utility NA

Deep Sea Mooring Hitech Vision Oilfield Services NA

Blohm + Voss Oil Tools Forum Energy Technologies Oilfield Equipment NA

Marwin ABM Group AS Oilfield Equipment NA

Healthcare & Life Sciences

10

European Healthcare & Life Sciences Equity Markets1

European Healthcare & Life Sciences Mid-Market M&A Activity

M&A Deals by Country of Target2 Acquisitions by Non-European Buyers2

Selected European Healthcare & Life Sciences M&A

Market Observations

• Senior health service officials have warned that the NHS is facing serious cash shortages and a £30 billion

funding gap by 2020, which will likely lead to closure of local hospitals across the country

• Thermo Fischer acquired Life Technologies for $13.6 billion in April, creating a powerhouse in bio-pharma,

lab instrumentation and supplies with combined revenues of $16.3 billion

• Onyx Pharmaceuticals launched an auction for the company, following the board’s rejection of an offer of

$120 per share from Amgen in late June which values Onyx at nearly $10 billion

• The FTC has asked for more information on the $8.5 billion buyout of Warner Chilcott by Actavis, extending

the waiting period to completion of the deal, which was originally announced in May

• Valeant announced the acquisition of global healthcare company Bausch & Lomb in May for $8.1 billion.

Valeant raised over $7.0 billion of debt to fund the deal

• Management moves3: Mediclin, Novartis, Silence Therapeutics, Stallergenes, Vectura Group, United Drug

0

20

40

60

80

100

120

140

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

UK & Eire Scandinavia DACH France Benelux Spain Italy

0

5

10

15

20

25

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

North America Asia (excl. China & India) China

India South America Africa & Middle East

Source: S&P CapitalIQ

Notes: (1) Based on HW&Co. indices including the most relevant Healthcare & Life Sciences companies for each country; (2) Includes transactions with a deal value

between €25m and €650m and all non disclosed value deals with target based in the UK, Eire, France, DACH (Germany, Austria, Switzerland), Spain, Italy, Benelux

(Belgium, The Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland); (3) Resignation or appointment of CEO, CFO or Chairman

Target Country Acquirer Country Sub Sector EV (€m)

Xellia Pharmaceuticals Novo Pharmaceuticals 535

Heraeus Kulzer Mitsui Chemicals Healthcare Equipment 450

Tertianum Swiss Prime Site Healthcare Facilities 400

Doc Generici Charterhouse Capital Partners Pharmaceuticals 296

Okairos GlaxoSmithKline Pharmaceuticals 250

ProFibrix The Medicines Company Biotechnology 183

Bionostics Holdings Research And Diagnostic Systems Healthcare Equipment 79

Neurelec William Demant Holding Healthcare Equipment 58

Vets4Pets Pets At Home Group Healthcare Services 46

UK and Eire France DACH Spain Italy Benelux Scandinavia

Price Change since last quarter (0.8%) (2.8%) 1.1% 5.0% 7.8% (7.2%) (4.3%)

Cash on Balance Sheet (€ bn) 14.8 2.5 15.5 0.5 0.3 1.1 NM

Net Debt / LTM EBITDA Multiple 1.8x 1.6x 1.7x 1.5x 1.0x 2.3x 1.1x

LTM EBITDA Multiple 10.1x 9.2x 10.7x 13.5x 9.2x 12.7x 13.8x

Change since last quarter (0.4x) 0.6x 0.3x 0.0x 0.8x 1.3x 2.4x

LTM EBITDA Margin 16.8% 12.5% 13.9% 17.1% 12.3% 8.9% 14.7%

Consensus 2Yr Fwd Revenue Growth (p.a.) 7.7% 8.5% 5.7% 5.7% 8.4% 5.2% 7.8%

Technology, Media & Telecom

11

European Technology, Media & Telecom Equity Markets1

European Technology, Media & Telecom Mid-Market M&A Activity

M&A Deals by Country of Target2 Acquisitions by Non-European Buyers2

Selected European Technology, Media & Telecom M&A

Market Observations

• Kabel Deutschland’s Board has agreed to the €7.7bn (€87.00 a share) takeover offer from Vodafone, which

was €2.00 a share higher than Liberty Media’s, and is aiming to complete the acquisition by October

• French government has blocked Yahoo!’s acquisition of Dailymotion citing that it is not in French interests

• BMC Software was taken private by a group led by Bain Capital and Golden Gate Capital for c.$6.9 billion

• BC Partners acquired Springer Science+Business Media to for approximately €3.3bn

• Spending on mobile advertising in 2013 in Western Europe is expected to exceed $2.9 billion

• Management moves3: BT Group, Deutsche Telekom, Thomson Reuters, TeliaSonera, Sage, Virgin Media

0

50

100

150

200

250

300

350

400

450

500

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

UK & Eire Scandinavia DACH France Benelux Spain Italy

0

10

20

30

40

50

60

70

80

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

North America Asia (excl. China & India) China

India South America Africa & Middle East

Source: S&P CapitalIQ

Notes: (1) Based on HW&Co. indices including the most relevant Technology, Media & Telecom companies for each country; (2) Includes transactions with a deal value

between €25m and €650m and all non disclosed value deals with target based in the UK, Eire, France, DACH (Germany, Austria, Switzerland), Spain, Italy, Benelux

(Belgium, The Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland); (3) Resignation or appointment of CEO, CFO or Chairman

UK and Eire France DACH Spain Italy Benelux Scandinavia

Price Change since last quarter (1.1%) 0.8% (0.9%) (3.1%) (3.5%) (0.5%) (3.7%)

Cash on Balance Sheet (€ bn) 23.1 28.2 18.7 7.0 7.5 13.1 NM

Net Debt / LTM EBITDA Multiple 1.4x 1.3x 1.3x 5.5x 2.2x 1.8x 1.1x

LTM EBITDA Multiple 9.9x 6.9x 8.7x 12.8x 7.3x 9.0x 8.3x

Change since last quarter (0.3x) 0.2x 0.2x 0.3x (0.2x) 0.2x 0.7x

LTM EBITDA Margin 17.8% 11.6% 10.6% 7.2% 9.5% 18.7% 11.0%

Consensus 2Yr Fwd Revenue Growth (p.a.) 5.9% 4.9% 5.2% 3.7% 5.9% 4.7% 4.4%

Target Country Acquirer Country Sub Sector EV (€m)

Civica OMERS Private Equity Outsourcing 452

Stonesoft McAfee Software 287

Ubiquisys Cisco Systems Hardware 237

Osiatis SA (55% stake) Econocom Group IT services 155

Energy Micro Silicon Laboratories International Semiconductors 130

Hostelbookers.com Web Reservations International Online Travel 100

Axell Wireless Cobham Communications 99

Oslo Kino Nordisk Film Entertainment 80

Alfacam Group Videohouse Broadcast Studio 79

Alti Tata Consultancy Services IT services 75

CliniSys Solutions Montagu Private Equity Healthcare IT NA

Transportation & Logistics

European Transportation & Logistics Equity Markets1

European Transportation & Logistics Middle-Market M&A Activity

M&A Deals by Country of Target2 Acquisitions by Non-European Buyers2

Selected European Transportation & Logistics M&A

Market Observations

• Talks have opened between the European Union and the US aimed at removing trade and investment barriers

through creating the world's largest free trade zone

• The European Commission has unveiled plans to simplify customs formalities for ships that will contribute to

the reduction of bureaucracy and delays in ports as well as to increase the competitiveness of the sector

• Investor Dietz AG announced that the new cargo center on the site of Berlin Brandenburg Airport (BER) in

Schönefeld will begin operation on August 1st

• Turkish low-cost carrier Pegasus Airlines has floated 34.5% of its share capital on the Istanbul stock exchange,

completing its long-awaited initial public offering. The share price has risen by over 40% since the IPO in

April

• Management moves3: PostNord, Lufthansa (CO Group Airlines and Logistics), Panalpina

Source: S&P CapitalIQ

Notes: (1) Based on HW&Co. indices including the most relevant Transportation & Logistics companies for each country; (2) Includes transactions with a deal value

between €25m and €650m and all non disclosed value deals with target based in the UK, Eire, France, DACH (Germany, Austria, Switzerland), Spain, Italy, Benelux

(Belgium, The Netherlands, Luxembourg) and Scandinavia (Denmark, Norway, Sweden and Finland); (3) Resignation or appointment of CEO, CFO or Chairman 12

0

1

2

3

4

5

6

7

8

9

10

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

North America Asia (excl. China & India) China

India South America Africa & Middle East

0

20

40

60

80

100

120

Q2-11 Q4-11 Q2-12 Q4-12 Q2-13

Nu

mb

er o

f T

ran

sact

ion

s

UK & Eire Scandinavia DACH France Benelux Spain Italy

UK and Eire France DACH Spain Italy Benelux Scandinavia

Price Change since last quarter 9.1% 5.1% 2.4% (0.2%) 0.6% (1.4%) (0.1%)

Cash on Balance Sheet (€ bn) 5.0 26.8 58.8 5.8 22.9 1.6 NM

Net Debt / LTM EBITDA Multiple 2.7x 2.9x 3.1x 5.9x 3.1x 3.6x 2.9x

LTM EBITDA Multiple 8.0x 9.2x 7.9x 10.9x 9.2x 10.3x 8.6x

Change since last quarter 0.0x 0.8x 0.0x (0.7x) 0.3x 0.3x 0.1x

LTM EBITDA Margin 10.1% 6.9% 14.5% 12.1% 18.9% 7.1% 10.8%

Consensus 2Yr Fwd Revenue Growth (p.a.) 3.6% 3.8% 3.2% 7.7% 5.2% 1.6% 3.5%

Target Country Acquirer Country Sub Sector EV (€m)

Hochtief Airport Pension Investment Board Airport Management 1,500

Unifeeder Nordic Capital Logistics 400

Troms Offshore Tidewater Inc. Shipping 277

WiderøesFjord 1, Nordland

Fylkeskommune, TorghattenAirline 250

Fiege Logistik (Italy, Spain, Portugal) Norbert Dentressangle Logistics 129

GE Equipment Services Europe HNA Group Ltd. Trailor Leasing NA

ERS Railways Freightliner Group Rail Freight Operator NA

ITG LGI Logistics Freight Forwarding NA

Exeter International Airport Patriot Aerospace Group Airport Operator NA

Finnair (Engine Service Business) GA Telesis Engine Services Airline Services NA

Cemelog United Parcel Service Warehousing NA

0

50

100

150

200

Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Q3-12 Q4-12 Q1-13

Eurozone GDP Performance Germany GDP Performance

Featured Theme

Harris Williams & Co. International Expansion

German Market Observations

• The opening of the new HW&Co. German office is strategically positioned to take advantage of the strong

German economy that continues to surpass overall Eurozone economic performance

• The German economic improvement continues to outpace the Eurozone in every major indicator:

− The German Economic Sentiment Indicator (ESI) improved to 99.8, while the Eurozone ESI

reached 92.6

− The German Industrial Confidence Indicator (ICI) increased by 3.4 points, a 41% improvement,

whereas the Eurozone ICI rose by 1.8 points reflecting a 16% improvement

− The Production Expectations Index (PEI) in Germany increased from (2.6) to 2.8 points, an

improvement greater than 200%, while the Eurozone PEI increased 137% to 0.7 points

− Order Books (OB) in Germany improved by 4.7 points, a 24% improvement, whereas the Eurozone

OB rose by 2.5 points reflecting a 9% improvement

− Stocks of Finished Products (SFP) in Germany remained flat at 8.2, whereas the Eurozone SFP

decreased from 6.1 to 5.9

•

GDP at Market Prices

Indexed at 2010 Q1

Germany and Eurozone GDP Performance

Eurozone 3-year GDP Growth Rate: 5.3%

Germany 3-year GDP Growth Rate: 10.1%

Source: Eurostat as of 30 June 2013

Source: Eurostat

A new report from McKinsey predicts that between

now and 2025 German exports will rise by 80%,

pushing their share in the economy from 50% to

68% of GDP

The economic outlook for Germany is brightening, its

central bank said, as improved trade and rising industrial

output suggested Europe's biggest economy is slowly

leaving recent weakness behind it.

"The outlook for the German economy has become

brighter again following the slowdown towards the end

of 2012," the Bundesbank wrote in its June monthly

report

Germany's top 30 Blue Chip [DAX] companies has

created 36,909 new jobs so far in 2013, according to

calculations made by German financial

daily Handelsblatt, based on an analysis of their company

reports. This represents a "considerable increase"

compared with the previous year, the paper notes.

Source: McKinsey, Handelsblatt, Bundesbank

German Economic News Headlines

13

€0

€2,000

€4,000

€6,000

€8,000

€10,000

0

50

100

150

200

250

Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Q3-12 Q4-12 Q1-13 Q2-13

To

tal T

ra

nsa

cti

on

Va

lue

Nu

mb

er o

f T

ra

nsa

cti

on

s

Number of Transactions Total Transaction Value

Featured Theme

Germany as a Buyer in Global M&A

German Targets in Global Cross-Border M&A Activity

Note: Companies above represent select experience of Harris Williams & Co. professionals

70%

4%

3%

3%

3%

2%

2%2%

2%

9% Germany

France

United Kingdom

United States

Switzerland

Austria

Sweden

Italy

Australia

Other (17 Countries)

Q2 2013 Targets by Geography

Representative Experience in Germany

• The German M&A market is currently in a “lull” despite

all relevant factors pointing in the right direction

− Financing is readily available for transactions and

interest rates are low

− Corporate debt levels in relation to EBITDA have

significantly improved since the beginning of the year

− Due to a rather flat development of the overall

economy, most growth scenarios are being based on

external initiatives

• H1 2013 M&A activity in Germany was down despite a

number of large transactions being completed for German

targets

• Private equity sell-side activity remained calm during H1

2013 and is expected to pick up during Q3 and Q4. On the

buy-side, the market is flooded with liquidity and

characterized by strong investment pressure for PEGs that

should drive interest for quality assets coming up for sale

German M&A Activity and Sentiment Recent M&A Activity of German Targets

For the Period CY 2012 – 2013 YTD

Date Target Buyers/Investors TEV (€m)

06/13 Kabel Deutschland Holding Vodafone € 11,136

06/13 Springer Science+Business Media BC Capital € 3,300

05/12 Open Grid Europe BC Investment Management € 3,200

01/12 Inoxum Outokumpu Oyj € 3,122

04/13 ista International CVC Capital Partners Limited € 3,100

06/12 Elster Group Melrose Industries € 2,272

06/12 BSN Medical EQT Partners € 1,820

10/12 Douglas Holding Advent International € 1,685

05/13 HOCHTIEF AirPort Public Sector Investment Board € 1,500

06/13 CeramTec Cinven Limited € 1,490

11/12 Real's Eastern Europe Business Groupe Auchan € 1,100

02/12 Borkum Riffgrund Kirkbi; William Demant Invest € 632

05/12 Tele Columbus Kabel Deutschland Holding € 618

07/12 Nordenia International Mondi Group € 614

01/12 Air Products, Homecare Business Linde Aktiengesellschaft € 590

09/12 KraussMaffei Technologies Onex Corporation € 568

04/13 Armacell Charterhouse Capital Partners € 500

08/12 Aenova Holding BC Partners € 500

12/12 trivago Tron NewCo GmbH € 476

04/13 Heraeus Kulzer Mitsui Chemicals € 450

05/12 Schuler Andritz € 415

10/12 Coperion Hillenbrand € 408

14

Source: CapitalIQ

Note: Refers to deals across all sectors

Sources: CapitalIQ, Analyst Reports, Market Research

Source: CapitalIQ

Note: Refers to deals across all sectors

335311

351

423444

428456

376

430

344

408

446

403

345

0

50

100

150

200

250

300

350

400

450

500

Q1-10 Q3-10 Q1-11 Q3-11 Q1-12 Q3-12 Q1-13

Nu

mb

er o

f T

ran

sact

ion

s

Target Client Description

Advised AXA Private Equity on selling Phönix Armaturen to Curtiss Wright

Advised STAR Capital on selling Blohm + Voss Industries (carve out) to SKF

Advised DBAG on selling coperion to Hillenbrand, Inc. in exclusive process

Advised Stargate Capital on selling Gehring Technologies to Penta Investments

Advised Plansee, Austrian family owned business, on selling PMG to VVG, German family office

Contacts and Disclosures

Thierry Monjauze

Managing Director

63 Brook Street

London W1K 4HS

United Kingdom

Phone: +44 20 7518 8901

Julien Darmon

Managing Director

63 Brook Street

London W1K 4HS

United Kingdom

Phone: +44 20 7518 8905

Red Norrie

Managing Director

63 Brook Street

London W1K 4HS

United Kingdom

Phone: +44 20 7518 8906

Francois Morin

Director

63 Brook Street

London W1K 4HS

United Kingdom

Phone: +44 20 7518 8907

Jeffery Perkins

Managing Director

An der Welle 4

60322 Frankfurt am Main

Germany

Phone: +49 69 7593 7166

www.harriswilliams.com

www.harriswilliams.de

Harris Williams & Co. is a preeminent middle market investment bank focused on the advisory needs of clients worldwide. The firm has deep

industry knowledge, global transaction expertise, and an unwavering commitment to excellence. Harris Williams & Co. provides sell-side

and acquisition advisory, restructuring advisory, board advisory, private placements, and capital markets advisory services.

Harris Williams & Co. Ltd is a private limited company incorporated under English law having its registered office at 5th Floor, 6 St.

Andrew Street, London EC4A 3AE, UK, registered with the Registrar of Companies for England and Wales under company number

7078852. Directors: Mr. Christopher Williams, Mr. Ned Valentine, Mr. Paul Poggi and Mr. Thierry Monjauze, authorised and regulated by

the Financial Conduct Authority.

Harris Williams & Co. Ltd Niederlassung Frankfurt (German branch) is registered in the Commercial Register (Handelsregister) of the

Local Court (Amtsgericht) of Frankfurt am Main, Germany, under registration number HRB 96687, having its business address at An der

Welle 4, 60322 Frankfurt am Main, Germany. Permanent Representative (Ständiger Vertreter) of the Branch Niederlassung: Mr. Jeffery H.

Perkins.

THIS REPORT MAY CONTAIN REFERENCES TO REGISTERED TRADEMARKS, SERVICE MARKS AND COPYRIGHTS

OWNED BY THIRD-PARTY INFORMATION PROVIDERS. NONE OF THE THIRD PARTY INFORMATION PROVIDERS IS

ENDORSING THE OFFERING OF, AND SHALL NOT IN ANY WAY BE DEEMED AN ISSUER OR UNDERWRITER OF, THE

SECURITIES, FINANCIAL INSTRUMENTS OR OTHER INVESTMENTS DISCUSSED IN THIS REPORT AND SHALL NOT

HAVE ANY LIABILITY OR RESPONSIBILITY FOR ANY STATEMENTS MADE IN THE REPORT OR FOR ANY FINANCIAL

STATEMENTS, FINANCIAL PROJECTIONS OR OTHER FINANCIAL INFORMATION CONTAINED OR ATTACHED AS AN

EXHIBIT TO THE REPORT. FOR MORE INFORMATION ABOUT THE MATERIALS PROVIDED BY SUCH THIRD PARTIES,

PLEASE CONTACT US AT +44 (0) 20 7518 8900.

The information and views contained in this report were prepared by Harris Williams & Co. Ltd (“Harris Williams”). It is not a research

report, as such term is defined by applicable law and regulations, and is provided for informational purposes only. It is not to be construed

as an offer to buy or sell or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading

strategy. The information contained herein is believed by Harris Williams to be reliable but Harris Williams makes no representation as to

the accuracy or completeness of such information.

Harris Williams and/or its affiliates may be market makers or specialists in, act as advisers or lenders to, have positions in and effect

transactions in securities of companies mentioned herein and also may provide, may have provided, or may seek to provide investment

banking services for those companies. In addition, Harris Williams and/or its affiliates or their respective officers, directors and employees

may hold long or short positions in the securities, options thereon or other related financial products of companies discussed herein.

Opinions, estimates and projections in this report constitute Harris Williams’ judgment and are subject to change without notice. The

financial instruments discussed in this report may not be suitable for all investors and investors must make their own investment decisions

using their own independent advisors as they believe necessary and based upon their specific financial situations and investment objectives.

Also, past performance is not necessarily indicative of future results. No part of this material may be copied or duplicated in any form or by

any means, or redistributed, without Harris Williams’ prior written consent.

Copyright © 2013 Harris Williams & Co., all rights reserved.