european sovereign crisis, what’s the outcome · gonzalo rengifo june 2012 mexico european...

TRANSCRIPT

Gonzalo Rengifo

June 2012

Mexico

European Sovereign Crisis, what’s the Outcome ?

Current situation

1

3Macro updatePictet Asset Management

Eurozone (im)balances: a Small World

Eurozone current accounts (% Eurozone GDP) by major EMU member

-1.6

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Austria Belgium Finland France Germany Ireland Italy Netherlands Portugal Spain Greece

%GDP

Rising imbalances since the creation of the euro

euro

Northern Europe to rest of the world Northern Europe to southern Europe

4Macro updatePictet Asset Management

Fiscal Revenue for Advanced and Emerging Countries

Fiscal revenue to GDP ratio in 2010

10.9 13

.417

.217

.417

.5 18.3 20

.720

.820

.9 22.4

22.7

23.1 24

.324

.324

.624

.725

.0 25.7 27

.231

.932

.332

.933

.133

.833

.934

.2 35.7

35.8 37

.537

.5 38.4

38.9

39.0 39.9

40.5 41.5

41.5 43

.8 44.8 46

.146

.2 48.0

48.6 49.6 52

.752

.9 54.5 56

.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Indi

aPh

ilipp

ines

Peru

Taiw

anIn

done

sia

Thai

land

Vene

zuel

aM

alay

sia

Chin

aTu

rkey

Mex

ico

Emer

ging

Sout

h Af

rica

Arge

ntin

aEg

ypt

Chile

Braz

ilKo

rea

Colo

mbi

aUn

ited

Stat

esAu

stra

liaSw

itzer

land

Japa

nRo

man

iaBu

lgar

iaIre

land

Spai

nRu

ssia

Pola

ndAd

vanc

edCa

nada

New

Zeal

and

Gree

ceUk

rain

eUn

ited

King

dom

Portu

gal

Czec

hRe

publ

icGe

rman

yHu

ngar

yIta

lyNe

ther

land

sAu

stria

Belg

ium

Fran

ceFi

nlan

dSw

eden

Denm

ark

Norw

ay

5Macro updatePictet Asset Management

Debt-to-GDP Ratio: Developed Economies

General government debt-to-GDP ratio: major advanced (21) economies

23.6 33

.9 37.8

39.8

42.6

43.4

44.7 49

.7 61.1

62.9 65.8 71

.9 82.4

83.4

85.1 92

.6

93.3

96.2

96.7 101.

1 119.

4

144.

9

200.

0

0

50

100

150

200

Aust

ralia

Emer

ging

New

Zeal

and

Swed

en

Switz

erla

nd

Denm

ark

Finl

and

Norw

ay

Spai

n

Neth

erla

nds

Unite

d Ki

ngdo

m

Aust

ria

Fran

ce

Germ

any

Cana

da

Irela

nd

Portu

gal

Belg

ium

Unite

d St

ates

Adva

nced Ita

ly

Gree

ce

Japa

n

2010 General Government Debt Maastricht Criteria (60%) Fitch criteria (80%)

%GDP

6Macro updatePictet Asset Management

Euro Countries: GDP Shares

Eurozone countries: GDP in billion of euros and in percentage of total eurozone GDP

Germany; 2481; 27%

France; 1931; 21%

Italy; 1547; 17%

Spain; 1062; 12%

Netherlands; 591; 7%

Belgium; 346; 4%

Austria; 281; 3%Greece; 230; 3%

Finland; 180; 2%Portugal; 172; 2%Ireland; 153; 2%

7Macro updatePictet Asset Management

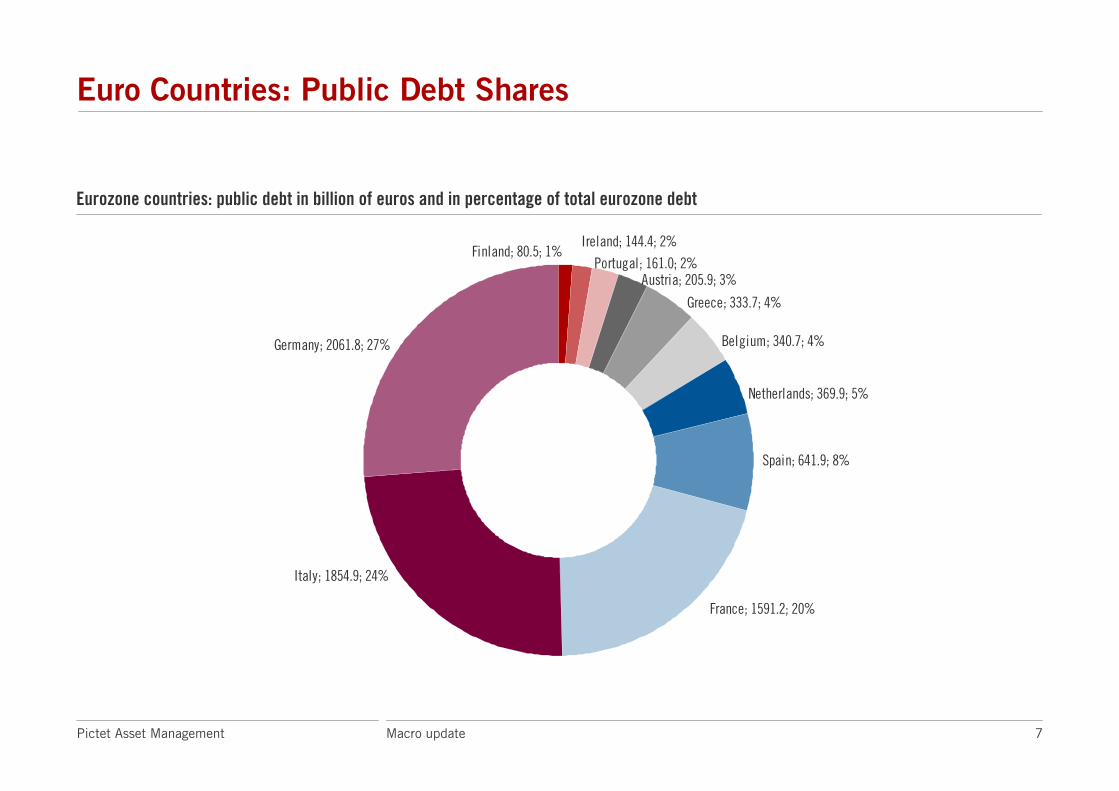

Euro Countries: Public Debt Shares

Eurozone countries: public debt in billion of euros and in percentage of total eurozone debt

Austria; 205.9; 3%

Greece; 333.7; 4%

Belgium; 340.7; 4%

Netherlands; 369.9; 5%

Spain; 641.9; 8%

Germany; 2061.8; 27%

Italy; 1854.9; 24%

France; 1591.2; 20%

Portugal; 161.0; 2%

Ireland; 144.4; 2%Finland; 80.5; 1%

8Macro updatePictet Asset Management

Who Owes Money to Whom (USD Bn)

What has been done so far ?

2

10Macro updatePictet Asset Management

Central Government Fiscal Balance

-20.0

-15.0

-10.0

-5.0

0.0

5.0

07 08 09 10 11 12

Italy Spain Portugal Greece Ireland

%GDP, 12-month moving average

Central fiscal balances have generally improved. Eurozone on average better than the UK & the US

Central fiscal balances: Italy, Spain & EFSF-3 countries Central fiscal balances: Eurozone (average), UK & US

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

07 08 09 10 11 12

Germany Eurozone France UK US

%GDP, 12-month moving average

Source: Pictet Asset Management, CEIC, Datastream, as at 25.02.2012

11Macro updatePictet Asset Management

Spanish Fiscal Policy

12Macro updatePictet Asset Management

Italy & Spain debt/GDP Evolutions under Various Interest Rates

119

132

154

80

90

100

110

120

130

140

150

160

2010 2011 2012 2013 2014 2015 2016

Interest rate at 5% Interest rate at 7% Interest rate at 10%

%GDP

98

106

120

20

40

60

80

100

120

140

2010 2011 2012 2013 2014 2015 2016

Interest rate at 5% Interest rate at 7% Interest rate at 10%

%GDP

Insert key message

Italian debt/GDP simulated for various interest rates Spanish debt/GDP simulated for various interest rates

13Macro updatePictet Asset Management

Sovereign Debt Long and Short-term Scores

Sovereign debt long and short-term scores for developed economies: a scatter diagram view

Bad long and short-term positions

Good long and short-term positions

Australia

Sweden

Austria

Belgium

Canada

Denmark

FinlandFrance

Germany

GreeceIreland

Italy

Japan

Netherlands

New ZealandNorway

Portugal

Spain

SwitzerlandUnited Kingdom

United States

-3.5

-2.5

-1.5

-0.5

0.5

1.5

-3.0 -2.0 -1.0 0.0 1.0 2.0 3.0

Sustainability (long-term) Score

Dyn

amic

(sh

ort-

term

) S

core

14Macro updatePictet Asset Management

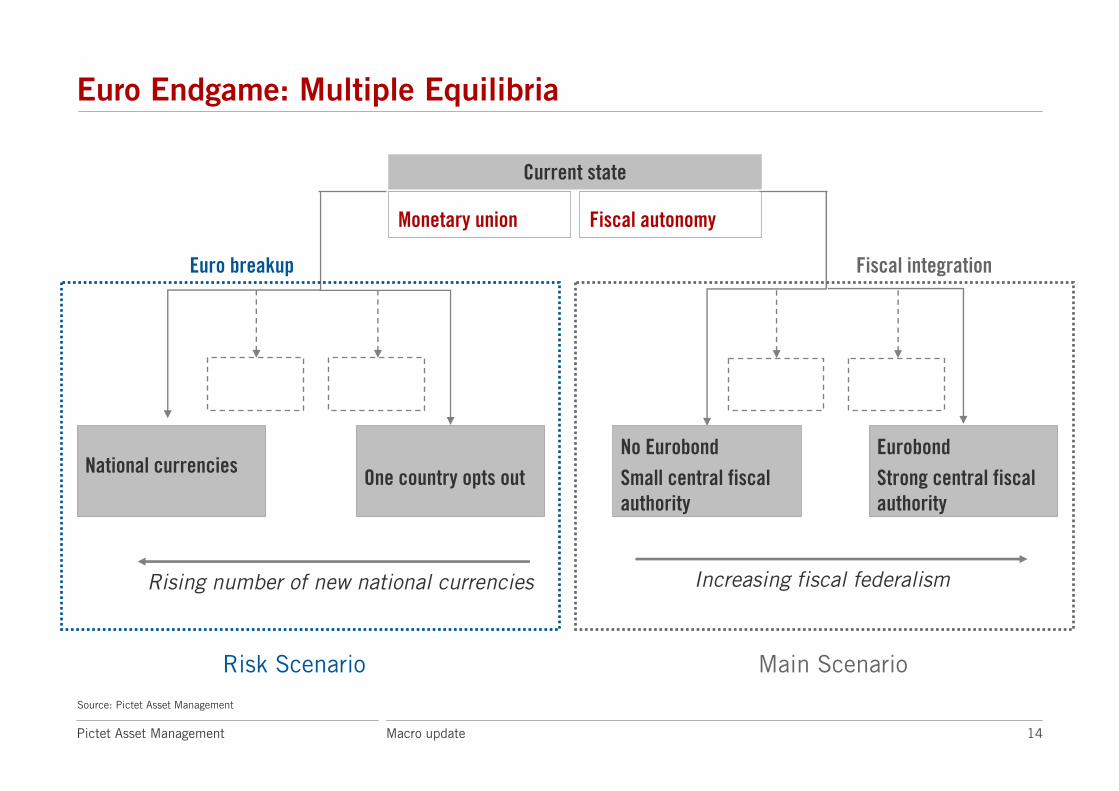

Euro Endgame: Multiple Equilibria

Monetary union Fiscal autonomy

Current state

One country opts outNational currencies

Euro breakup

Source: Pictet Asset Management

Fiscal integration

Rising number of new national currencies

No EurobondSmall central fiscal authority

EurobondStrong central fiscal authority

Increasing fiscal federalism

Risk Scenario Main Scenario

15Macro updatePictet Asset Management

Solving the Debt Problem – Four Ways Out

Official default and debt restructuration

Low short-term cost / high long-term costHigh short-term cost / low long-term cost

Solution

Debt solving mechanism

Sovereign defaultBail-out MonetizationDebt repayment

Bilateral agreements orsupranationalbail-out

Central Bank Intervention to usethe inflation channelto solve the debtproblem

Primary balancedeficit reduction

Domestic consequences

International consequences

Limited if no accessto the internationalmarket of capitalsfor an extended period

Loss of economicindependence

Loss of the Central Bank’s credibility

Currency depreciation

Lower economicnominal growth

Social imbalances andconflicts between taxpayers and publicworkers

Sovereign crisiscontagion

Banking system crisis

Bilateral agreements:higher spreads for thecountry that fundsthe bail-out

Possible socialconflicts

Competition oncurrency depreciation

Weaker externaldemand coming fromthe indebted country

16Macro updatePictet Asset Management

EU/IMF Financial Aid Package

– €80bn from EMU countries (funding according to countries’ quotas in the ECB’scapital)

– €30bn from the IMF

Fiscal policy Monetary policy

Greek packageEUR 110bn

Unconventional monetary policy tools

Additional packageEUR 720bm

– First loan tranche of €14.5bn was sent to Greece on 18th of May while second tranche of €9bn was sent on 9th of Sept.

– Total package covers Greek debt service until Dec 2012 (i.e. interest payments + principal but excluding primary deficits financial needs)

– €60bn available under the existing European Commission balance-of-payments lending facility (Funded and guaranteed by the 27 EU members)

– €440bn available through the creation of the European Financial Stabilisation Fund (EFSF) funded according to countries’ quotas in the ECB’s capital and guaranteed by the 16 Eurozone members

– €220bn from the IMF

– Irish package: EUR85bnEFSM/EFSF/IMF: EUR22.5bn eachDomestic sources: EUR17.5bn

– Portuguese package: EUR78bnEFSM/EFSF/IMF: EUR26bn each

– Remaining effective lending capacity: EUR575bn (Spanish debt service is about EUR350bn until Dec 2014)

– The EFSF pave the way towards a closer fiscal union in Europe

– Outright purchases in the Euro area public and private debt securities markets

– Reactivation of 1Y, 6-month and 3-month refinancing operations at fixed rate with full allotment

– Reactivation of liquidity swap lines with the Fed

– Outright bonds purchases of €165bn (as of Oct. 14th), absorbed with one-week fixed-term deposit

Quarterly conference call 17Fixed Income Outlook

Source: Bloomberg, Pictet Asset Management. Updated 2011-10-14

0

5'000

10'000

15'000

20'000

25'00000

.01.

1900

04.0

6.20

10

25.0

6.20

10

16.0

7.20

10

06.0

8.20

10

27.0

8.20

10

17.0

9.20

10

08.1

0.20

10

29.1

0.20

10

19.1

1.20

10

10.1

2.20

10

31.1

2.20

10

21.0

1.20

11

11.0

2.20

11

04.0

3.20

11

25.0

3.20

11

15.0

4.20

11

06.0

5.20

11

27.0

5.20

11

17.0

6.20

11

08.0

7.20

11

29.0

7.20

11

19.0

8.20

11

09.0

9.20

11

30.0

9.20

11

21.1

0.20

11

11.1

1.20

11

€ bn

0

25'000

50'000

75'000

100'000

125'000

150'000

175'000

200'000

225'000

€ bn

Weekly Amount (ls) Cumulated Amount (rs) 4 week moving average (ls)

ECB Government Bonds PurchaseAccelerating ECB interventions mainly focused on Italy, but to be continued with stronger commitment

ECB Eurosystem securities market program-weekly and cumulated amounts

18Macro updatePictet Asset Management

EU/IMF Packages & Financing Needs for Countries at Risk

Debt servicing until Dec. 2014 for EFSF-3, Spain & Italy & remaining packages

168

42

431

843

80

0

200

400

600

800

1'000

1'200

Gre

ece

Irel

and

Por

tuga

l

Spa

in

Ital

y

Fina

ncin

g ne

eds

until

Dec

. 2

01

4 (

bn o

f €

)

Greek remaining package, 37

+ Irish remaining package, 46+ Portugal remaining package, 66

+ EU/IMF remaining lending capacity, 575

Current lending capacity just enough to cover EFSF-3 & Spain until Dec. 2014

19Macro updatePictet Asset Management

Euro Sovereign Risk

Italy

Spain

Portugal

Ireland

Greece

Euro area

Greece is bankrupt and by no mean can muddle through whatever the measures taken. Significant losses have to be taken through a set of orderly haircuts ultimately amounting to circa 70%.

Disorderly default

Ireland will have to resort to a second bailout plan in the coming months. The widely nationalised banking sector is still threatening dramatically public finances. An orderly default going forward can not be ruled out.

No stabilisation of the current negative fiscal balance trend

Portugal can muddle through but will be highly dependant on the whole zone growth and the ECB monetary policy.

Lack of growth endangering the current positive trend in terms of public finances adjustment

Spain has made significant efforts on the fiscal front but a banking sector recapitalisation will be needed. The latter is manageable provided the real estate necessary adjustment is done gradually.

Lack of growth

Brutal adjustment of the real estate loans value on the banks balance sheets

Italy has already a primary balance almost at equilibrium. The stabilisation of its debt /GDP ratio is highly achievable especially with the newly decided fiscal measures. But the ECB then EFSF/ESM will have to maintain an active SMP to avoid contagion through government refinancing rates.

Lack of growth

Government rates pushed significantly and structurally above 5%

The cost of the Euro breakup option is so high that the already started transfer between the strongest and the weakest countries will continue. More fiscal discipline and a painful adjustment process will lead to low growth over a 5 to 7 years cycle.

Euro breakup. Disorderly default from Greece triggering a round of contagion to other Eurozone countries and the whole banking sector.

Our ViewMain risks

Source: Pictet Asset Management

Themes & risks to dominate the market in the short and long run

20Macro updatePictet Asset Management

Eurozone: Key Messages

• Eurozone contracted in 2011Q4. No collapse in 2012, the zone might even avoid a recession

• Germany is recovering, while Greece is entering into its 4th year of declining activity.

• Biggest risk remains a Greek downward spiral, notably in Spain: contracting activity – lower fiscal revenues – more fiscal austerity –additional contraction in activity

• Inflation to decline: no reason for the ECB not to continue loosening conventional & possibly unconventional monetary policy

• Euro debt crisis:

– no euro break-up, but more fiscal integration

– EFSF/ESM not a solution for Spanish/Italian financing needs, only the ECB can afford it (monetization… indirect QE)

– ECB further non-conventional monetary policy to depend on two conditions:

– a political commitment to fiscal federalism with credible fiscal rules (that will not be breached)

– Complete disorderly market conditions

– Greece, Portugal and Ireland to default … orderly

Recession in the Eurozone, no euro break-up but more fiscal federalism

What should be done?

3

22Macro updatePictet Asset Management

Wrong Way

23Macro updatePictet Asset Management

Right Way?

24Macro updatePictet Asset Management

What Should Be Done ?

Surgery in Greece

A wall – ECB – better than a firewall

Control supranational (European) of the budgets of the euro area countries

Lower interest rates in Europe

Second phase: policies that promote growth consistent with the reduction of public expenditure

25Macro updatePictet Asset Management

Pictet Asset Management SARoute des Acacias 60, 1211 Geneva 73

Tel: +41 58 323 3333 Fax: +41 58 323 2040

Pictet Asset Management LimitedAuthorised and regulated by the Financial Services Authority

Moor House, Level 11120 London Wall

London EC2Y 5ETTel: +44 20 7847 5000 Fax: +44 20 7847 5300

Pictet Asset Management (“PAM”) definition: In this document, Pictet Asset Management includes all the operating subsidiaries and divisions of the Pictet group that carry out institutional asset management: Pictet Asset Management SA, a Swiss corporation registered with the Swiss Financial Market Supervisory Authority FINMA, Pictet Asset Management Limited, a UK company authorised and regulated by the Financial Services Authority, and Pictet Asset Management (Japan) Limited, a Japanese company regulated by the Financial Services Agency of Japan.

This document is for distribution to professional investors only. However it is not intended for distribution to any person or entity who is a citizen or resident of any locality, state, country or other jurisdiction where such distribution, publication, or use would be contrary to law or regulation. Information used in the preparation of this document is based upon sources believed to be reliable, but no representation or warranty is given as to the accuracy or completeness of those sources. Any opinion, estimate or forecast may be changed at any time without prior warning. Investors should read the prospectus or offering memorandum before investing in any Pictet managed funds. This document has been issued in Switzerland by Pictet Asset Management SA and/or Pictet & Cie and in the rest of the world by Pictet Asset Management Limited and may not be reproduced or distributed, either in part or in full, without their prior authorisation.

For UK investors, the Pictet and Pictet Total Return umbrellas are domiciled in Luxembourg and are recognised collective investment schemes under section 264 of the Financial Services and Markets Act 2000. Swiss Pictet funds are only registered for distribution in Switzerland under the Swiss Fund Act, they are categorised in the United Kingdom as unregulated collective investment schemes. The Pictet group manages hedge funds, funds of hedge funds and funds of private equity funds which are not registered for public distribution within the European Union and are categorised in the United Kingdom as unregulated collective investment schemes.

For US investors, the Shares of the funds managed by the Pictet Group are being offered to United States tax-exempt investors Shares sold in the United States or to US Persons will only be sold in private placements to accredited investors pursuant to exemptions from SEC registration under the Section 4(2) and Regulation D private placement exemptions under the 1933 Act and qualified clients as defined under the 1940 Act. The Shares of the Pictet funds have not been registered under the 1933 Act and may not, except in transactions which do not violate United States securities laws, be directly or indirectly offered or sold in the United States or to any US Person. The Management Fund Companies of the Pictet Group will not be registered under the 1940 Act.

For more information, please contact your Pictet client relationship manager

www.pictet.com