european cranes - research-doc.credit-suisse.com

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

9 October 2017 Europe

Equity Research

Capital Goods

European Cranes Research Analysts

Leo Carrington

44 20 7883 4532

Andre Kukhnin, CFA

44 20 7888 0350

Max Yates

44 20 7883 8501

Artem Tokarenko

44 20 7888 2676

Iris Zheng

44 20 7883 5298

Specialist Sales: Andrew Bell

44 20 7888 0479

INITIATION

Konecranes and Cargotec Initiation We extend our Pan-European Capital Goods coverage, initiating with an

Outperform rating on Konecranes (TP €43) and a Neutral rating on

Cargotec (TP €52). We take a deep dive into evolving trends in port terminal

CapEx following structural changes in shipping and advances in automation,

as well as industry concentration following Konecranes' acquisition of Terex's

MHPS division. We find these trends somewhat supportive for Cargotec, but

believe Konecranes is set to benefit across all areas of its business.

■ Customer CapEx growth following a pause: Formation of shipping

alliances enabled use of ever-larger ships calling at fewer terminals,

straining ports' handling peaks. This resulted in uncertainty amongst port

operators planning capacity and a hiatus in CapEx growth in 2016 and

2017; we expect a catch-up in growth in 2018 and 2019 with 8% and 15%

growth respectively, settling to its c.5% historic growth rate mid-term, in line

with our container trade forecasts.

■ Port Automation - machines to outclass manual in 2018. In our view, in

terms of Lifts per Hour and safety, automated will outclass manual ports

and drive an equipment replacement cycle limited only by negotiation with

unions. Konecranes and Cargotec are the two leading suppliers of manual

and automated port products.

■ Industry concentration across Port and Industrial Cranes. Following

c.20 acquisitions since 2004, there are now three scale players in Port

Equipment and Industrial Cranes globally. We see Konecranes' acquisition

of Terex MHPS as concluding the trend; in Port Equipment, the three

largest players now control >50% of the market ex-China, and in Industrial

Cranes, the three largest players now control >50% the market. We see

industry concentration enabling pricing power across all of Konecranes'

products, and c50% of Cargotec's.

■ Stock calls: We favour Konecranes as it benefits from Port Equipment

growth and industry concentration. This provides it with a clear roadmap to

close the gap to the Mechanical peer group's margins, with upside to

synergy targets that we view as conservative. The investment case in

Cargotec is balanced as its positive exposure to growing end-markets in

Port Equipment and Marine cranes is balanced against valuation, which we

see as fair. Our target prices are DCF based.

Figure 1: Relative valuation – the crane companies trade at a c.20%

discount to their mechanical peers on 2018E EV/EBITA

Source: Credit Suisse estimates. Peers detailed in Figure 61

Div Yield

2017E 2018E 2017E 2018E 2017E 2017E 2018E 2019E

Cargotec N € 52.00 18.4 16.2 14.7 12.7 2.1% 8.2% 9.3% 9.5%

Konecranes OP € 43.00 22.8 14.8 16.1 11.6 2.7% 6.8% 9.0% 11.0%

Average 20.6 15.5 15.4 12.2 2.4% 7.5% 9.2% 10.2%

Pan Euro ME Avg. 23.0 20.8 17.4 15.8 2.4% 14.9% 15.4% 14.6%

PE EV/EBITA (Adj) EBITA % (Adj)Rating Target Price

9 October 2017

European Cranes 2

Key Charts Figure 2: c.55% of the Port Equipment market ex-

China is now controlled by two players...

Figure 3: …while in Industrial Cranes, >50% of the

market is controlled by the three largest players

Source: Credit Suisse market share estimates, Global ex-China. Market share based on 2016 reported sales.

Source: Credit Suisse market share estimates, Global ex-China. Market share based on 2016 reported sales.

Figure 4: Port Capex drives Port Equipment sales.

We forecast a rebound in CapEx growth of 8%/14%

in 2018E/2019E benefiting both companies…

Figure 5: …while growing ship size mean ports

upgrade cranes to handle higher peak loads,

providing growth opportunities in Port Equipment

Source: Company data, Credit Suisse estimates, Credit Suisse Proprietary Port Operator CapEx model

Source: Clarkson's

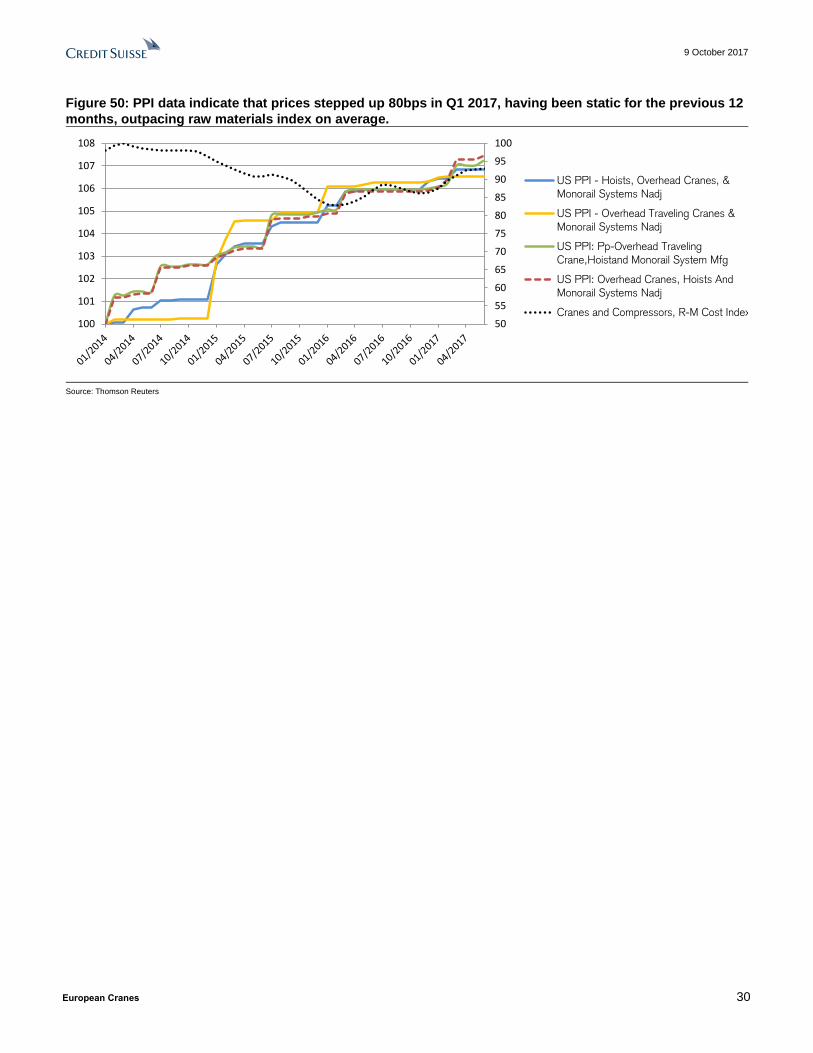

Figure 6: PPI data indicates Industrial Crane prices increased 80bps in 2017, having been static for the

previous 12 months, and on average outpacing the raw materials index on average

Source: Thomson Reuters

Cargotec Equipment,

30%

Konecranes Equipment,

22%

ZPMC Container

Equipment, 10%

Liebherr Maritime

Equipment, 12%

Others, 26%Konecranes

18%

Terex11%

Stahl 3%

Columbus McKinnon

16%Kito7%

Others45%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

CS Port Operator CapEx Model growth %yoyCargotec (Kalmar) Org. GrowthKonecranes (Port Solutions) Org. GrowthZPMC (Container Cranes) growth

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

100-2,999 TEU 3,000-5,999 TEU 6,000-7,999 TEU 8,000-11,999 TEU 12,000-14,999 TEU 15,000+ TEU

50

55

60

65

70

75

80

85

90

95

100

100

101

102

103

104

105

106

107

108

US PPI - Hoists, Overhead Cranes, &

Monorail Systems Nadj

US PPI - Overhead Traveling Cranes &

Monorail Systems Nadj

US PPI: Pp-Overhead Traveling

Crane,Hoistand Monorail System Mfg

US PPI: Overhead Cranes, Hoists And

Monorail Systems Nadj

Cranes and Compressors, R-M Cost Index

9 October 2017

European Cranes 3

Figure 7: Konecranes looks relatively undervalued

on 2018E multiples…

Figure 8: ..while Cargotec's valuation looks more in

line with the mechanicals sector.

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 9: Konecranes - revenue, organic growth and

margin history and forecast

Figure 10: Cargotec - revenue, organic growth and

margin history

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 11: Konecranes is currently credited with 9%

mid-cycle margins, while we see synergies and

pricing power push margins to 10.5% by 2020

Figure 12: Cargotec sees limited margin expansion,

which we see as fair due to undefined self-help

strategy & mixed record on service growth.

Source: Credit Suisse estimates Source: Credit Suisse estimates

8

9

10

11

12

13

14

15

16

17

18

19

Konecranes EV/EBITA Average EV/EBITA

Trough: 5.1 8

9

10

11

12

13

14

15

16

17

18

19

Cargotec EV/EBITA Average EV/EBITA

11.8%

7%7.4%

6.2%6.4%5.5%5.9%5.5%6.6%

6.9%9.3%

11.1%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0

900

1,800

2,700

3,600

4,500

Revenue (operating margins in label) Organic Growth % (RHS)

5.7%

2.4% 5.5%

6.6%4.8%

4%4.5%

6.2%7.1%

8.3% 9.3%9.4%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Revenue (operating margins in label) Organic growth % (RHS)

9 October 2017

European Cranes 4

Table of contents

Executive summary 6

Sector overview ......................................................................................................... 6

Konecranes: Initiate with an Outperform rating and target price of €43 ................... 8

Cargotec: Initiate with a Neutral rating and a €52 target price. ................................ 9

Medium-term Driver #1: structural changes in container shipping and port

automation to drive a rebound in customer CapEx in 2018E 10

Shipping line consolidation has been the principal factor slowing CapEx .............. 11

Benefits of port terminal automation ....................................................................... 12

End-market sizing ................................................................................................... 15

Medium-term Driver #2: Industrial Crane and Port Equipment industry

concentration should lead to better margins 21

Market shares by product type................................................................................ 22

Key Conclusions from the European Commission competition case ..................... 25

Effect on Pricing ...................................................................................................... 29

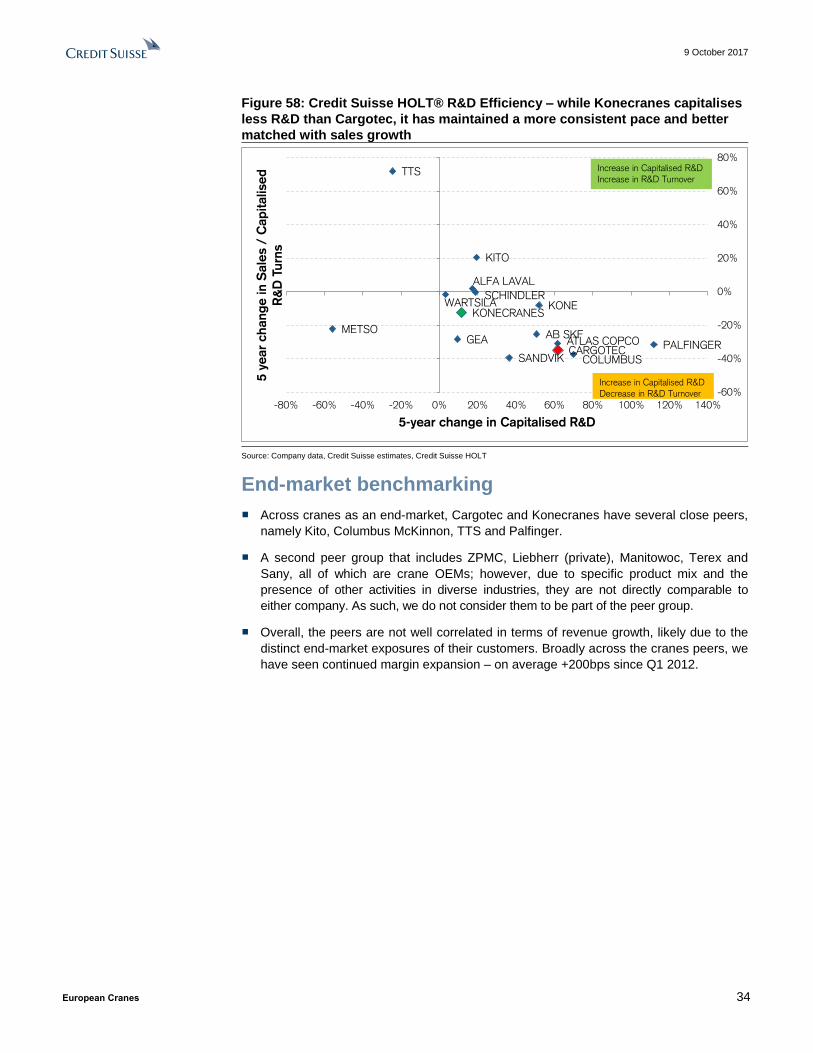

Company and end-market benchmarking 31

Company benchmarking ......................................................................................... 31

End-market benchmarking ...................................................................................... 34

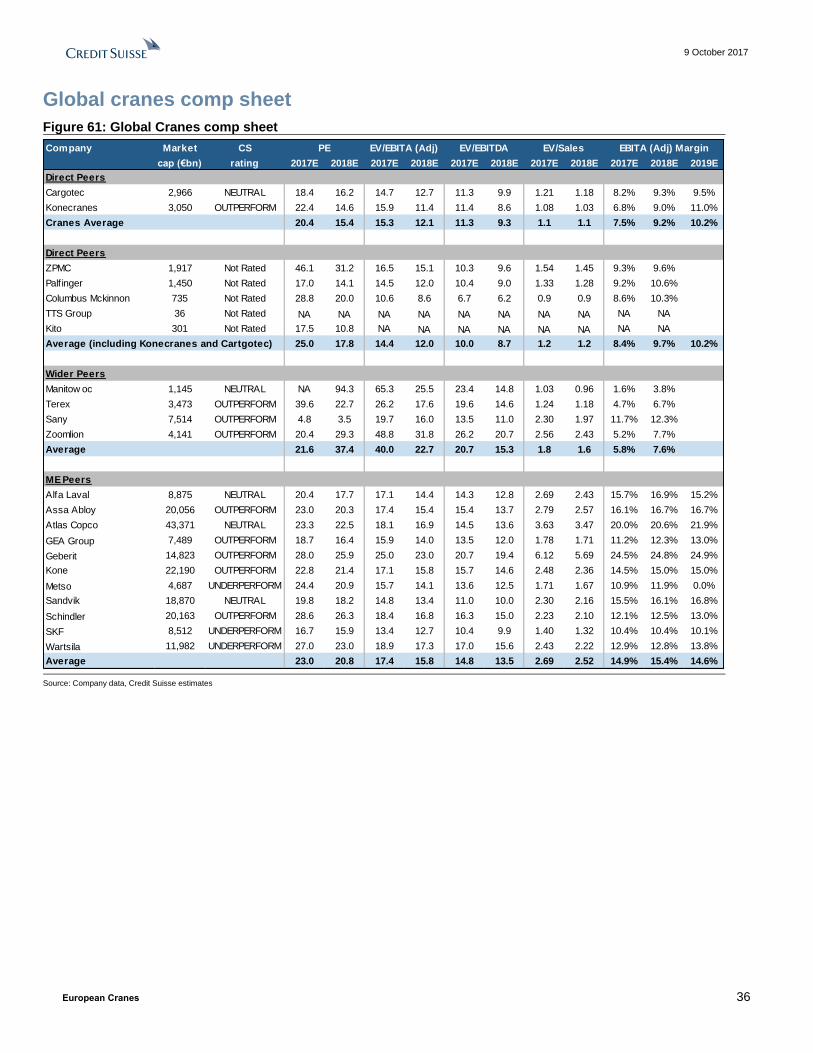

Global cranes comp sheet ...................................................................................... 36

Konecranes (KCRA.HE) 40

Prime beneficiary of heavy lifting in market consolidation 40

Konecranes: Key charts .......................................................................................... 42

Konecranes: Valuation ............................................................................................ 46

Konecranes: Overview ............................................................................................ 49

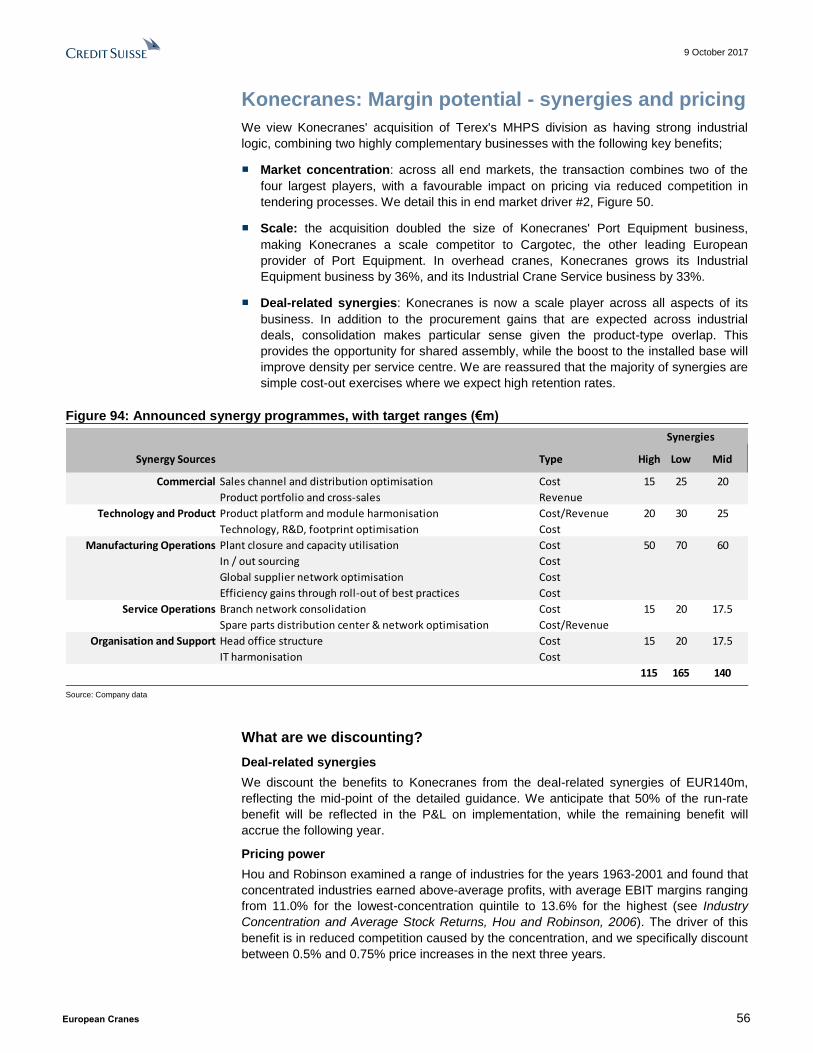

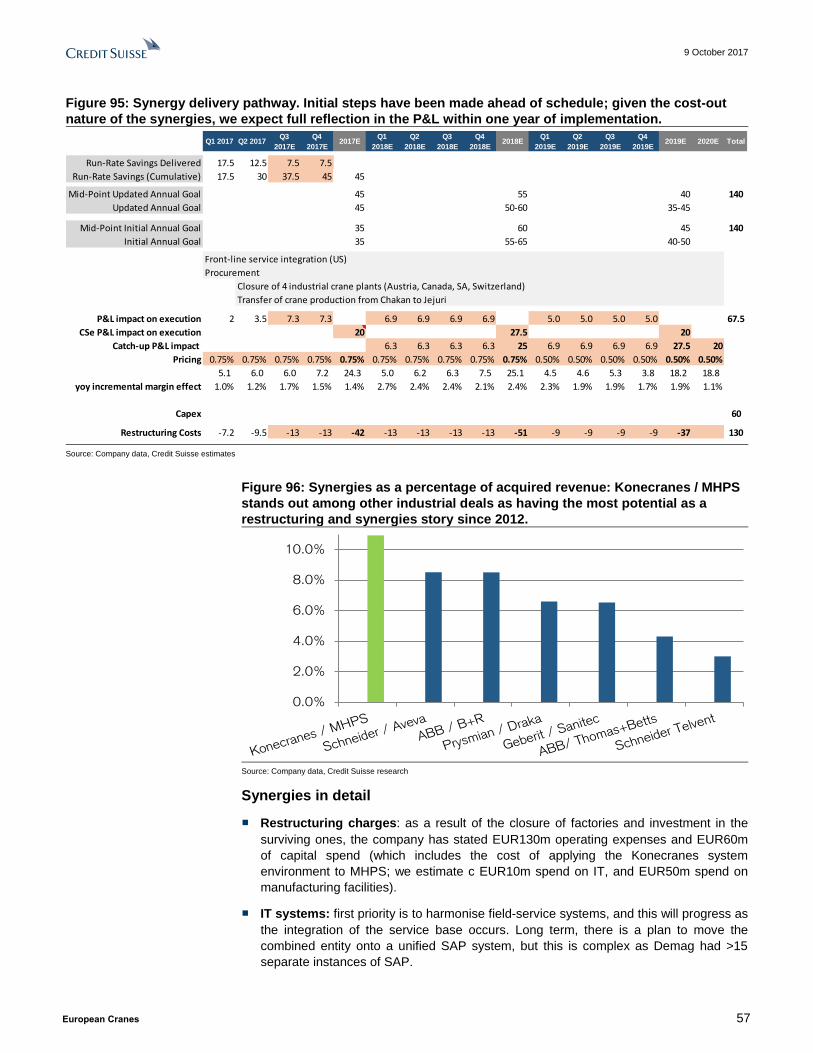

Konecranes: Margin potential - synergies and pricing............................................ 56

Konecranes: Financials ........................................................................................... 68

Cargotec (CGCBV.HE) 73

Cargotec: Key charts .............................................................................................. 75

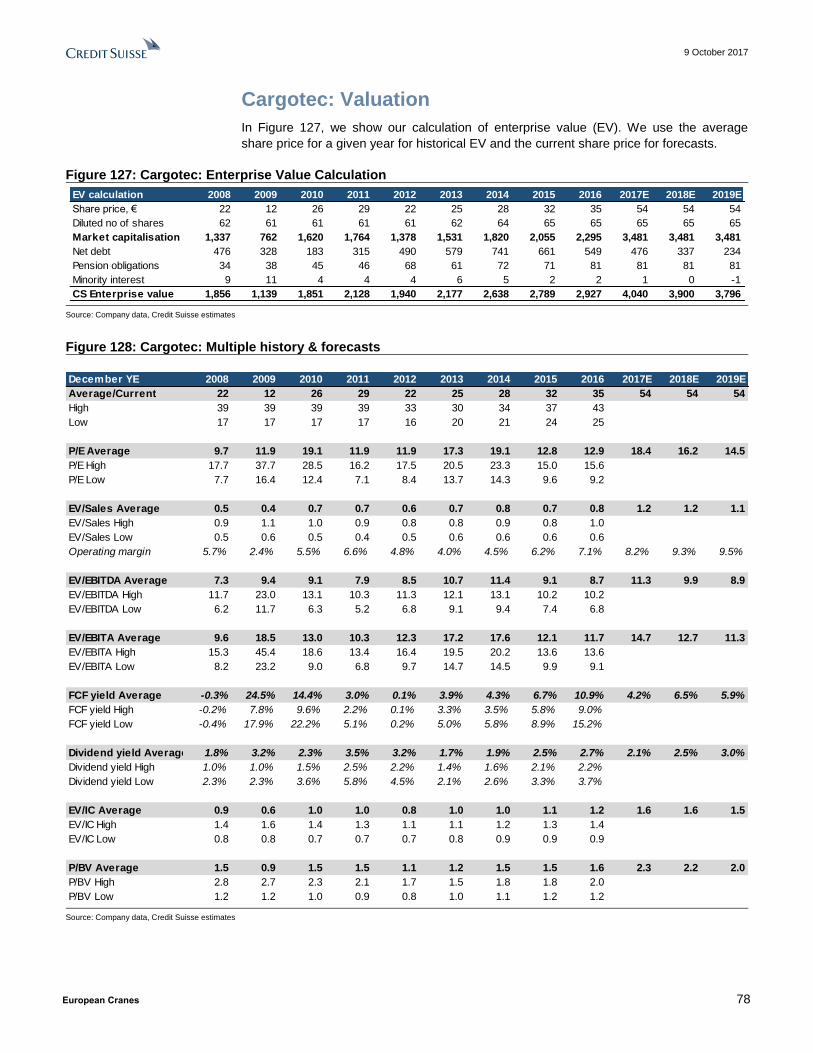

Cargotec: Valuation ................................................................................................ 78

Cargotec: Kalmar .................................................................................................... 81

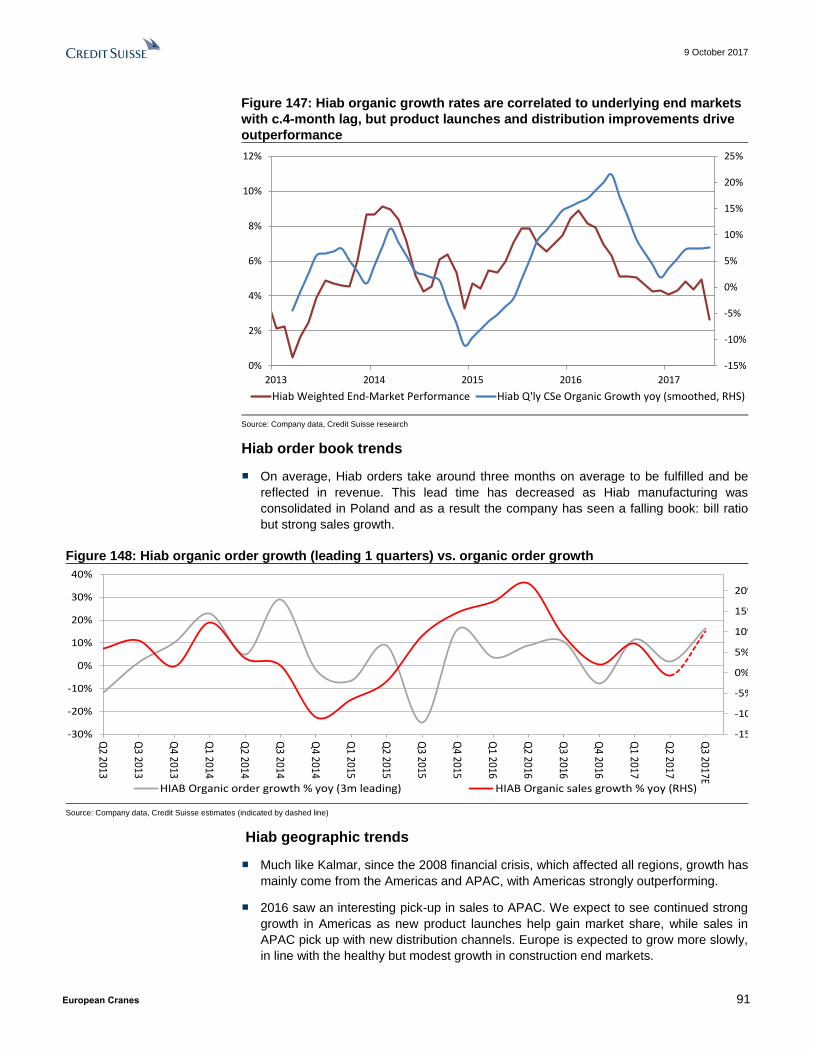

Cargotec: Hiab ........................................................................................................ 87

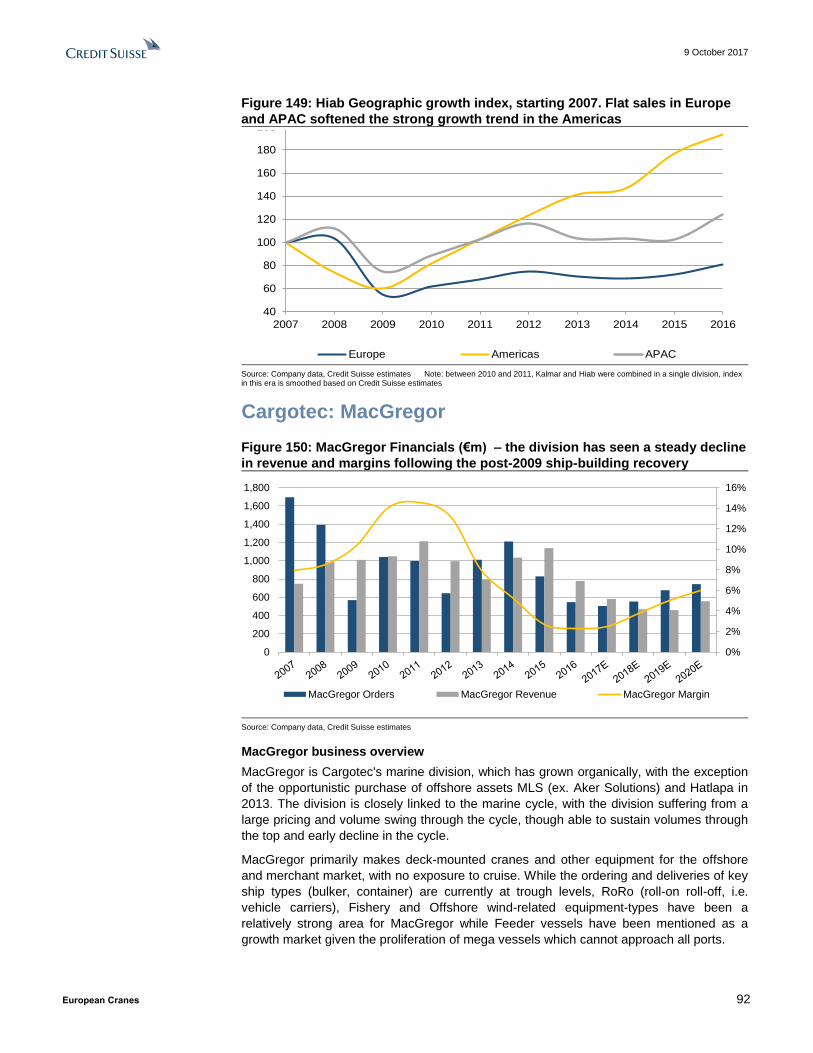

Cargotec: MacGregor ............................................................................................. 92

Cargotec: Financials ............................................................................................. 107

Appendices: 112

9 October 2017

European Cranes 5

End-market Primers Series

This report contains detailed analysis on the Cranes end market, including sections on

Port Equipment and Industrial Cranes. Other end-market primers published by the team:

Marine, Industrial Automation, Offshore Wind, Elevators, Warehouse Automation,

Aerospace, Dairy, Healthcare, Locks, Low Voltage, Construction

Equipment, Metal 3D, Oil & Gas Capex, Mining, Cables, Power Generation

The authors of this report wish to acknowledge to contribution made by Sweta

Mishra, Manisha Boyina and Shruti Garg, employees of CRISIL Global Research and

Analytics, a business division of CRISIL limited, a third party provider of offshore

research services to Credit Suisse.

9 October 2017

European Cranes 6

Executive summary

Sector overview

We identify two key mid-term drivers that we view as beneficial for the European crane

companies;

■ Driver #1: a catch-up in port operator CapEx in 2018 and 2019 following a period of

end-market uncertainty, with additional growth opportunities from automation.

■ Driver #2: Industry concentration largely concluded by Konecranes' acquisition of

Terex's MHPS division is set to drive margin improvement in the Industrial Equipment

end market, and leave two strong Port Equipment players with scale to defend against

ZPMC, a major Chinese competitor.

We see Konecranes as the major beneficiary of these two factors, given 100% of its

revenues are derived from Port Equipment and Industrial Cranes, while only c.50% of

Cargotec's revenues (the Kalmar division)is set to benefit. As such, we prefer to play these

themes through Konecranes.

Driver #1: structural changes in container shipping, and port automation to drive a rebound in customer CapEx in 2018

■ Overcapacity, alliance formation and low freight rates between 2014-2016 led to

uncertainty in the container shipping industry and paused Container Port CapEx growth

in 2016 and 2017.

■ Alliance formation encouraged ordering of mega-vessels >20,000TEU, which require

significant upgrades to port equipment in order to handle the peak loads and physical

size of ships.

■ We expect port CapEx growth to bounce back in 2018, and see additional growth in

outer years from port automation as a solution to handle peak loads of larger ships,

which offer significant OpEx savings and safety improvements.

■ Cargotec and Konecranes are leaders in manual and automated container handing

equipment and are ideally placed to benefit from resumed CapEx growth in 2018. We

see opportunities for automation to accelerate the replacement cycle; however, very

strong union pressure will result in slow adoption rather than a "tipping point".

Where are we vs. consensus;

On 2019 revenues, we are 5% ahead of consensus for Konecranes Port Solutions and in

line for Cargotec Kalmar. For two relatively analogous businesses, we find this

discontinuity surprising, and therefore see good relative value in Konecranes.

Figure 13: We estimate 8% and 14% growth in port operator capex in 2018 and 2019, which drops through

to Konecranes Port Solutions and Cargotec Kalmar with a c.6m delay.

Source: Company data, Credit Suisse estimates

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E

World Container Exports growth 4% -9% 14% 8% 3% 5% 5% 2% 4% 4% 4% 4% 4%

CS Proprietary Port Capex Growth Model 19% -29% 4% 22% 8% 9% -13% 29% 1% -8% 8% 14% 8%

Cargotec Kalmar org. growth 16% -33% -14% 21% 24% 5% -3% 4% 2% -1% 3% 12% 7%

Konecranes P.S. org. growth -3% 5% 12% 7%

9 October 2017

European Cranes 7

Driver #2: Industrial Crane and Port Equipment industry concentration will lead to better margins

■ Industry concentration in Industrial and Container cranes appears to be coming to an

end following c20 separate acquisitions, and culminating with Konecranes' acquisition

of Terex MHPS.

■ According to our estimates, in Container cranes, Cargotec, Konecranes and ZPMC

control c70% of the market, while globally ex. China, Cargotec and Konecranes control

>60% of the market.

■ In the European Industrial crane market, the top 2 OEMs, Konecranes and Columbus

McKinnon control c50% of the market, with no scale players in the residual portion.

■ We find the remedy enforced by the European Commission following the MHPS

acquisition more in favour of Konecranes, requiring only divestment of a specialist

product-group with €135m revenue while gaining €436m of NI sales, further

concentrating the mid-range market in particular.

■ As a result of industry concentration, we identify pricing tailwinds worth 75bps in 2018E

and 50bps in 2019E for Konecranes, mainly in the Industrial crane segment, while

deal-related synergies provide €140m of run-rate EBIT benefit by 2021.

Where are we vs. consensus;

For the Port Equipment businesses of Konecranes and Cargotec, we see industry

concentration as protective of pricing rather than providing meaningful margin upside as a

result of the presence of a strong Chinese competitor.

In Industrial Cranes, we see significant benefits for Konecranes' Industrial Equipment and

Service businesses. We are slightly ahead of consensus in terms of revenues for these

divisions, (+0.3% and +1.1% in 2018 and 2019 respectively). We are significantly ahead in

terms of operating profit; +3.6% and +9.7% in 2018 and 2019 respectively, in part due to

the positive pricing impact that is not discounted by consensus.

Figure 14: Two decades of industry concentration led by Konecranes have concluded following the Terex

MHPS Acquisition, in our view.

Source: Company data, We have only included acquisitions from the Industrial Crane and Port Equipment markets.

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

PWB Anchor

ARMSEL MHE

Kito Kito

Yale International

Columbus McKinnon Columbus McKinnon

CVS Ferrari CVS Ferrari

Belotti * Cargotec's bid for CVS Ferrari was blocked CVS Service

by the German Competition Commission

Demag Cranes

Noell

Fantuzzi

Terex (MHPS)

WMI Cranes Ltd

Asio Sistemas de Elevacion

Eydimen 2000

Meiden Host Systems

Consens Transport Sys.

MMH

Stahl Cranesystems

SMV Lifttrucks AB

MAN SWF

Konecranes Konecranes

Kone

Cargotec Cargotec

Navis

Asciano Automation

ZPMC ZPMC

Liebherr Liebherr

9 October 2017

European Cranes 8

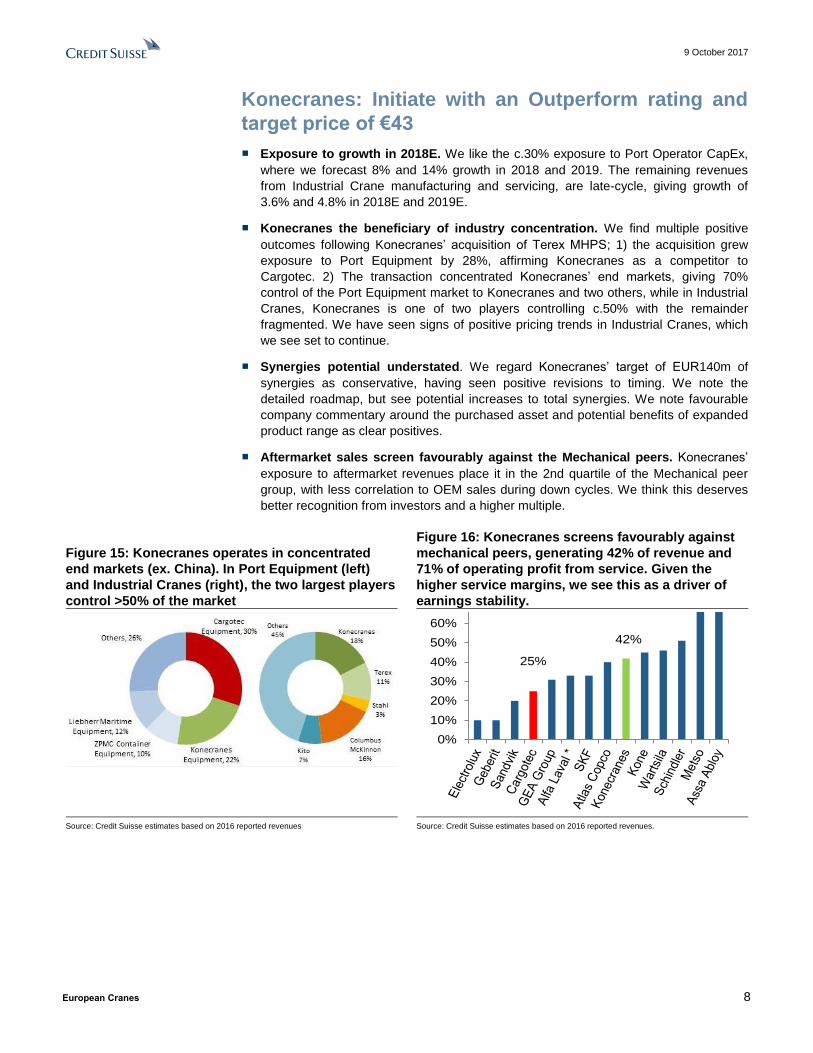

Konecranes: Initiate with an Outperform rating and

target price of €43

■ Exposure to growth in 2018E. We like the c.30% exposure to Port Operator CapEx,

where we forecast 8% and 14% growth in 2018 and 2019. The remaining revenues

from Industrial Crane manufacturing and servicing, are late-cycle, giving growth of

3.6% and 4.8% in 2018E and 2019E.

■ Konecranes the beneficiary of industry concentration. We find multiple positive

outcomes following Konecranes’ acquisition of Terex MHPS; 1) the acquisition grew

exposure to Port Equipment by 28%, affirming Konecranes as a competitor to

Cargotec. 2) The transaction concentrated Konecranes’ end markets, giving 70%

control of the Port Equipment market to Konecranes and two others, while in Industrial

Cranes, Konecranes is one of two players controlling c.50% with the remainder

fragmented. We have seen signs of positive pricing trends in Industrial Cranes, which

we see set to continue.

■ Synergies potential understated. We regard Konecranes’ target of EUR140m of

synergies as conservative, having seen positive revisions to timing. We note the

detailed roadmap, but see potential increases to total synergies. We note favourable

company commentary around the purchased asset and potential benefits of expanded

product range as clear positives.

■ Aftermarket sales screen favourably against the Mechanical peers. Konecranes’

exposure to aftermarket revenues place it in the 2nd quartile of the Mechanical peer

group, with less correlation to OEM sales during down cycles. We think this deserves

better recognition from investors and a higher multiple.

Figure 15: Konecranes operates in concentrated

end markets (ex. China). In Port Equipment (left)

and Industrial Cranes (right), the two largest players

control >50% of the market

Figure 16: Konecranes screens favourably against

mechanical peers, generating 42% of revenue and

71% of operating profit from service. Given the

higher service margins, we see this as a driver of

earnings stability.

Source: Credit Suisse estimates based on 2016 reported revenues Source: Credit Suisse estimates based on 2016 reported revenues.

25%

42%

0%

10%

20%

30%

40%

50%

60%

70%

9 October 2017

European Cranes 9

Cargotec: Initiate with a Neutral rating and a €52

target price.

■ Port equipment opportunity. We forecast port operator capex growth of 8% and 14%

in 2018E and 2019E respectively, while recent industry consolidation and imminent

adoption of automation will be protective for pricing. Cargotec derives c.50% of its

revenue from sales of Port Equipment.

■ Positive mid-term outlook, consensus optimistic near term. Overall we see strong

mid-term growth prospects for Cargotec from the MacGregor (marine) and Kalmar

(Port Equipment) divisions, however we near-term downside risk from earnings

revisions due to consensus forecasts which are, in our view, anticipating growth c.12

months early.

■ Long-term cyclicality risks weigh on valuation. We note that Cargotec’s relatively

low proportion of sales from aftermarket places it in the bottom quartile of the

Mechanical Capital Goods peer-group. In addition, we note a surprisingly high degree

of cyclicality in aftermarket organic growth and strong correlation to OE sales during

downturns. As such, we see the 19% discount to the sector on 2018E EV/EBITA

implied at current share price levels as appropriate.

Figure 17: Cargotec EBIT (€m) guidance evolution

vs. reported outcomes (and 2017 consensus).

Cargotec's low proportion of service places it in the

bottom quartile of the mechanical peer group, while

driving earnings volatility

Figure 18: MacGregor growth index – there is

clearly significant through-cycle upside; however,

with a marine upcycle only beginning, and long

revenue conversion, we see little near-term

catalysts

Source: Company data, Credit Suisse estimates. Vara consensus Source: Company data, Credit Suisse estimates

80

100

120

140

160

180

200

220

240

260

280

2009A 2010A 2011A 2012A 2013A 2014A 2015A 2016A 2017E

Bottom end of guidance Top end of guidance

Mid-point of EBIT guidance Actual/ C'sus forecast

50

70

90

110

130

150

170

190

2007 2009 2011 2013 2015 2017E 2019E

MacGregor Equipment MacGregor Services

9 October 2017

European Cranes 10

Medium-term Driver #1: structural changes in container shipping and port automation to drive a rebound in customer CapEx in 2018E

Summary:

1. Overcapacity, alliance formation and low freight rates between 2014 and 2016 caused

uncertainty in the container shipping industry and paused Container Port CapEx growth in

2016 and 2017.

2. Alliance formation increased orders for >20,000TEU mega vessels. Significant

upgrades to port equipment are required to handle the peak loads and the physical size of

these ships.

3. We expect port CapEx growth to bounce back in 2018, and see port automation as a

solution to handle the peak loads of larger ships, in addition to offering significant OpEx

savings and safety improvements.

4. Cargotec and Konecranes are leaders in manual and automated container handing

equipment and should be ideally placed to benefit from resumed CapEx growth in 2018.

We see opportunities for automation to accelerate the replacement cycle; however, strong

union pressure will likely result in gradual adoption rather than a "tipping point".

Figure 19: Cyclical port CapEx drives Cargotec

Kalmar's sales

Figure 20: Lows in the CapEx cycle follow declining

container rates; with recovering rates, we forecast

CapEx growth in 2018 and 2019

Source: Company data, Credit Suisse Proprietary Port Operator CapEx model. Data source: custom built index of 19 Port terminal Operators. China Merchant Port Holdings, Shanghai International Port Group and Ningbo Port have been deliberately excluded, as while they have shown strong accelerations in their Capex, the prime beneficiary of this is ZPMC, a local supplier. The strong acceleration in Capex in 2015 is largely due to investments by Hutchison, International Container Services and Adani Ports. Growth ex these names was 4%.

Source: Company data, Thompson Reuters, Credit Suisse Proprietary Port Operator CapEx model

-40%

-30%

-20%

-10%

0%

10%

20%

30%

CS Port Operator CapEx Model growth %yoy

Cargotec (Kalmar) Org. Growth

Konecranes (Port Solutions) Org. Growth

ZPMC (Container Cranes) growth

40

50

60

70

80

90

100

110

120

40

60

80

100

120

140

160

180

Port capex index (LHS) Freight rate index (leading, 18MMA)

9 October 2017

European Cranes 11

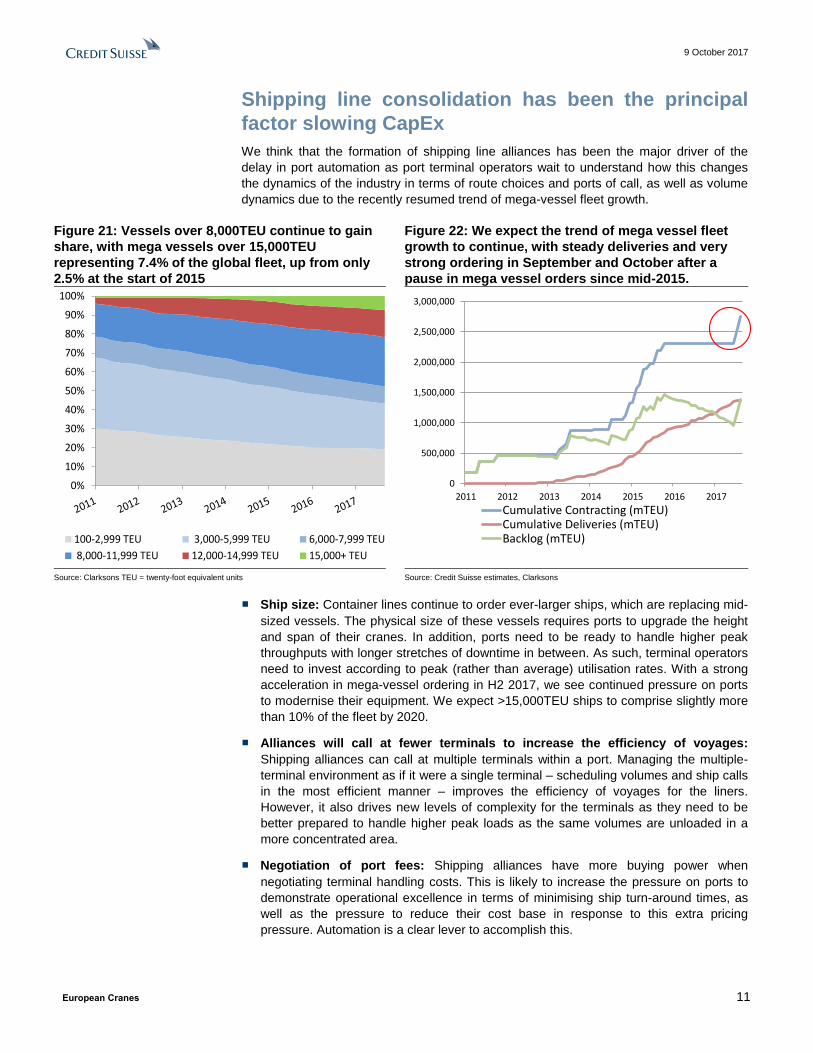

Shipping line consolidation has been the principal

factor slowing CapEx

We think that the formation of shipping line alliances has been the major driver of the

delay in port automation as port terminal operators wait to understand how this changes

the dynamics of the industry in terms of route choices and ports of call, as well as volume

dynamics due to the recently resumed trend of mega-vessel fleet growth.

Figure 21: Vessels over 8,000TEU continue to gain

share, with mega vessels over 15,000TEU

representing 7.4% of the global fleet, up from only

2.5% at the start of 2015

Figure 22: We expect the trend of mega vessel fleet

growth to continue, with steady deliveries and very

strong ordering in September and October after a

pause in mega vessel orders since mid-2015.

Source: Clarksons TEU = twenty-foot equivalent units Source: Credit Suisse estimates, Clarksons

■ Ship size: Container lines continue to order ever-larger ships, which are replacing mid-

sized vessels. The physical size of these vessels requires ports to upgrade the height

and span of their cranes. In addition, ports need to be ready to handle higher peak

throughputs with longer stretches of downtime in between. As such, terminal operators

need to invest according to peak (rather than average) utilisation rates. With a strong

acceleration in mega-vessel ordering in H2 2017, we see continued pressure on ports

to modernise their equipment. We expect >15,000TEU ships to comprise slightly more

than 10% of the fleet by 2020.

■ Alliances will call at fewer terminals to increase the efficiency of voyages:

Shipping alliances can call at multiple terminals within a port. Managing the multiple-

terminal environment as if it were a single terminal – scheduling volumes and ship calls

in the most efficient manner – improves the efficiency of voyages for the liners.

However, it also drives new levels of complexity for the terminals as they need to be

better prepared to handle higher peak loads as the same volumes are unloaded in a

more concentrated area.

■ Negotiation of port fees: Shipping alliances have more buying power when

negotiating terminal handling costs. This is likely to increase the pressure on ports to

demonstrate operational excellence in terms of minimising ship turn-around times, as

well as the pressure to reduce their cost base in response to this extra pricing

pressure. Automation is a clear lever to accomplish this.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

100-2,999 TEU 3,000-5,999 TEU 6,000-7,999 TEU

8,000-11,999 TEU 12,000-14,999 TEU 15,000+ TEU

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

2011 2012 2013 2014 2015 2016 2017

Cumulative Contracting (mTEU)Cumulative Deliveries (mTEU)Backlog (mTEU)

9 October 2017

European Cranes 12

Why has port automation implementation lagged?

The port industry is at least 10 years behind other industries in terms of technical

development according to a Cargotec-funded McKinsey study. Despite the clear

operational and financial benefits of automation and the longstanding existence of the

technology, adoption has been very low.

We note that port operators are at a low point in their CapEx cycle, with no growth in 2016

and a c-5% decrease in CapEx spending in 2017, on our estimates, which has had an

effect on sales of all types of Port Terminal handling equipment. We see low port operator

CapEx as a result of the low rates environment and uncertainty surrounding the calling

patterns of the new shipping alliances. With the alliances now looking settled and the rates

environment improving as overcapacity is reduced, we anticipate a return to growth for

Port Operators in 2018, accompanied by an acceleration in automation projects.

We have identified four key phases of terminal automation:

2000-10 Early movers (e.g. ECT Delta) took time to achieve operational goals.

2010-15 Broader acceptance of automation, DPW and APM launched several projects.

2016-17 Pause in CapEx growth while productivity / technology advance imminent.

2018-30 30+ LPH achieved, Alliances settled and mega-vessel ordering confirmed,

resulting a resumption of growth in automation projects.

Figure 23: Port operator CapEx growth moves in line with underlying trade

growth. We forecast a catch-up with underlying demand by 2019, while see

scope for an additional spend as the benefits of port automation are realised

Source: Credit Suisse estimates, Credit Suisse Proprietary Port Operator CapEx model

Benefits of port terminal automation

The benefits of terminal automation can broadly be split into operational improvements

and cost reductions. Cargotec sees automation offerings as providing port operators with

an opportunity to reduce labour costs by 60% and other variable OpEx by 21%, before

taking into account the human and operational benefits of improved safety.

We identify five key benefits of automation:

1. Employee cost reductions: Following years of unionisation and general

underlying wage inflation, employee cost reduction is the primary potential benefit

of automation, in our view. According to Cargotec, the total annual cost of hiring a

straddle carrier driver on the US West Coast is $300k. (and ports require 10s of

80

100

120

140

160

180

200

Port capex index (LHS) Container trade index

9 October 2017

European Cranes 13

carriers working three shifts per day.) At Qingdao Qianwan Container Terminal

(QQCTN), the number of workers required to unload a cargo ship has been

reduced from 60 to 9 following the implementation of automation, representing an

85% reduction in employee costs.

2. Effective capacity increases: By accurately predicting throughput rates and

reducing non-revenue generating lifts, the productive capacity of existing

equipment is accelerated. This results in effective capacity increases without

expanding a port's footprint.

− Fewer unnecessary lifts: automated (or automation-ready) terminals scan

a container's data (typically printed letters) to track its location. Previously

this had all been done manually, which led to frequent errors.

− Consistent throughput rates: automated terminals are more consistent

and can operate in all weather conditions. This benefits planning of port

logistics and ship and truck turnaround times, improving service quality.

− Reduced downtime: automation means that machines are being built with

a much higher technology content, and the sensor load in new cranes

provides an opportunity to eliminate downtime via preventative servicing.

3. Safety: Port accidents can be fatal given the scale of machinery. Automation

allows segregation of humans and machines – the only task for truck drivers in an

automated terminal is loading containers onto lorries, where the driver has to get

out the cab, partly for safety reasons but also to manually confirm that the

interface is lined up properly on the truck.

4. Reduced energy consumption and wear and tear: Automated machinery can

be run more efficiently.

− Power consumption is reduced as automated movements avoid sharp

accelerations and boxes do not need to be lifted as high when

automatically controlled as the machine operates with tighter tolerances

than a human operator.

− These same factors reduce the effective utilisation rate and therefore cut

down on wear and tear over a given period. In addition, excessive speed

or fatigue are often factors in port accidents.

5. Lower pollution and emissions:

− Lithium batteries in straddle carriers and AVGs are highly efficient and

can be recharged quickly, making pure-electric and hybrid-electric

handling gear feasible.

− A fully automated unloading system needs no overhead lighting, which

further reduces energy consumption and light pollution.

What are the final hurdles to automation?

■ Unionisation: The key cost-saving opportunity for port terminal operators is in

reducing the number of employees manning equipment; however, this is also the

strongest resistance point.

− Port workforces are generally part of strong unions. Australia is the leader in port

automation, having started the process of union negotiations the earliest.

− Elsewhere, however (especially in the US), we anticipate negotiations with unions

to be extended and difficult – and slower than hoped for by the equipment OEMs.

We note that the proposed California cap-and-trade spending bill contains $140m

for spending on zero-emission port equipment, but with the proviso that the funds

cannot be spent on automated equipment.

9 October 2017

European Cranes 14

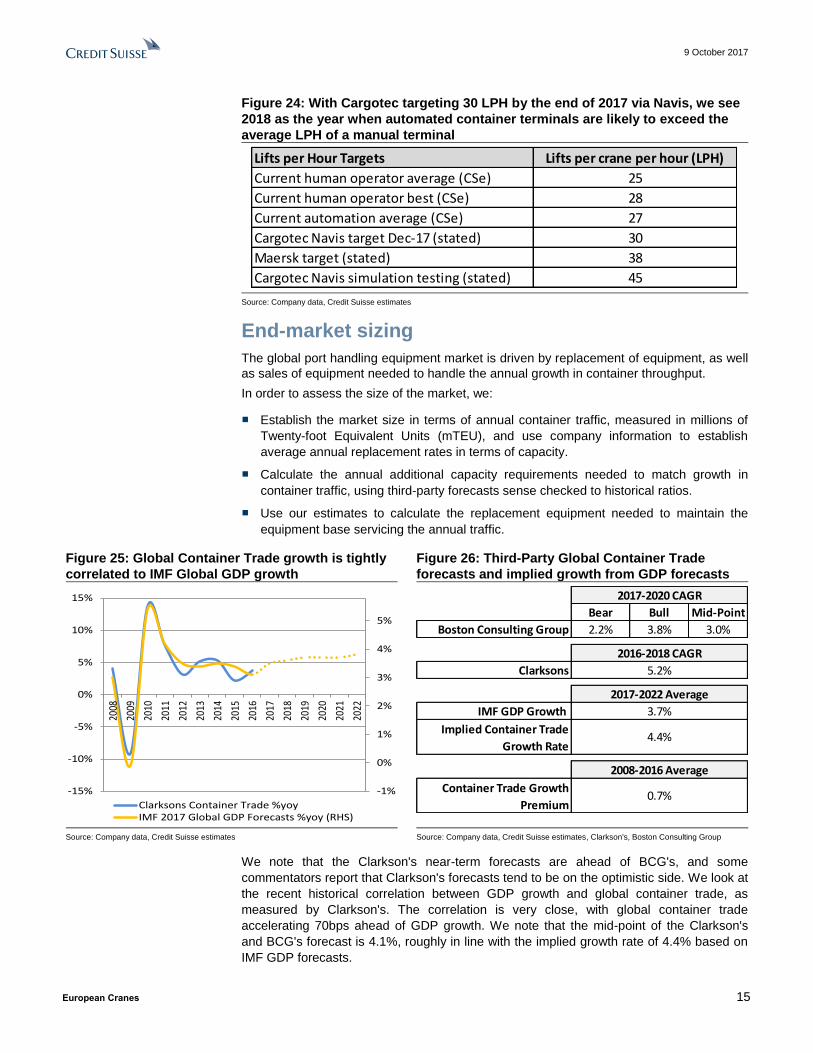

■ Lifts per Hour (LPH): automated terminals do not currently have the same throughput

as manual terminals, most likely due to the following:

− Integration of equipment and software is key, but improves with each project. At

QQCTN, Navis took one year to go live at 30 LPH, but at other sites it has taken

two years to get to 25 LPH. Cargotec notes that port operators tend to split up

contracts among the OEMs, which introduces significant integration challenges for

relatively new technology.

− The ship-to-ship (STS) transfer process is usually a bottleneck and remains manual

given that large cranes with long ropes have swaying containers, which makes the

process challenging to automate.

− Automated terminals are currently at mid-20s LPH (25-27) under the crane, while in

response to the threat of automation, non-automated terminals have stepped up to

30 LPH. Cargotec wants to get to 30 LPH by the end of 2017, while software

simulations at Cargotec can reach 45 LPH in perfect conditions using current

solutions.

− Machine vision: one of the factors that reduces the overall speed of automated

offerings is that current iterations of sensors cannot distinguish between different

obstacles. For instance, cranes will stop when birds fly past.

− Technology has been slow to develop in terms of applying well-established

automation, software and machine vision systems to the port terminal environment,

while port operators themselves have lacked the domain knowledge to implement

the systems.

■ Risk aversion:

− Customers are reluctant to outsource their terminal operating systems (TOS) to a

third party, and as such often rely on in-house systems that are unable to integrate

automated machinery.

− Ports have not been prepared to purchase machinery with no cabins, and

simultaneously are reluctant to invest in 'automation-ready' equipment that can be

slowly transitioned.

− We note too that port terminal operators have not needed to make risky

investments thus far in the 2010s, as they have been in better financial shape

relative to many of the liners. As such, we think the port operators may not have felt

pressure to invest.

In terms of efficiency, we think automated systems only need to reach parity with humans

to make automation worthwhile given its other benefits. We therefore see 2018 as a key

milestone in port automation, as automated port terminals will match manual equipment in

terms of lifts per hour, leaving only unionisation and risk aversion as the remaining

hurdles. We see efficiency/throughput as the main barrier to implementation, and expect to

see resumed announcements of large automated equipment orders in 2018, although the

pace will primarily depend on the progress of union negotiations.

9 October 2017

European Cranes 15

Figure 24: With Cargotec targeting 30 LPH by the end of 2017 via Navis, we see

2018 as the year when automated container terminals are likely to exceed the

average LPH of a manual terminal

Source: Company data, Credit Suisse estimates

End-market sizing

The global port handling equipment market is driven by replacement of equipment, as well

as sales of equipment needed to handle the annual growth in container throughput.

In order to assess the size of the market, we:

■ Establish the market size in terms of annual container traffic, measured in millions of

Twenty-foot Equivalent Units (mTEU), and use company information to establish

average annual replacement rates in terms of capacity.

■ Calculate the annual additional capacity requirements needed to match growth in

container traffic, using third-party forecasts sense checked to historical ratios.

■ Use our estimates to calculate the replacement equipment needed to maintain the

equipment base servicing the annual traffic.

Figure 25: Global Container Trade growth is tightly

correlated to IMF Global GDP growth

Figure 26: Third-Party Global Container Trade

forecasts and implied growth from GDP forecasts

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates, Clarkson's, Boston Consulting Group

We note that the Clarkson's near-term forecasts are ahead of BCG's, and some

commentators report that Clarkson's forecasts tend to be on the optimistic side. We look at

the recent historical correlation between GDP growth and global container trade, as

measured by Clarkson's. The correlation is very close, with global container trade

accelerating 70bps ahead of GDP growth. We note that the mid-point of the Clarkson's

and BCG's forecast is 4.1%, roughly in line with the implied growth rate of 4.4% based on

IMF GDP forecasts.

Lifts per Hour Targets Lifts per crane per hour (LPH)

Current human operator average (CSe) 25

Current human operator best (CSe) 28

Current automation average (CSe) 27

Cargotec Navis target Dec-17 (stated) 30

Maersk target (stated) 38

Cargotec Navis simulation testing (stated) 45

-1%

0%

1%

2%

3%

4%

5%

-15%

-10%

-5%

0%

5%

10%

15%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Clarksons Container Trade %yoyIMF 2017 Global GDP Forecasts %yoy (RHS)

Bear Bull Mid-Point

Boston Consulting Group 2.2% 3.8% 3.0%

Clarksons 5.2%

IMF GDP Growth 3.7%

Implied Container Trade

Growth Rate4.4%

Container Trade Growth

Premium0.7%

2017-2020 CAGR

2016-2018 CAGR

2017-2022 Average

2008-2016 Average

9 October 2017

European Cranes 16

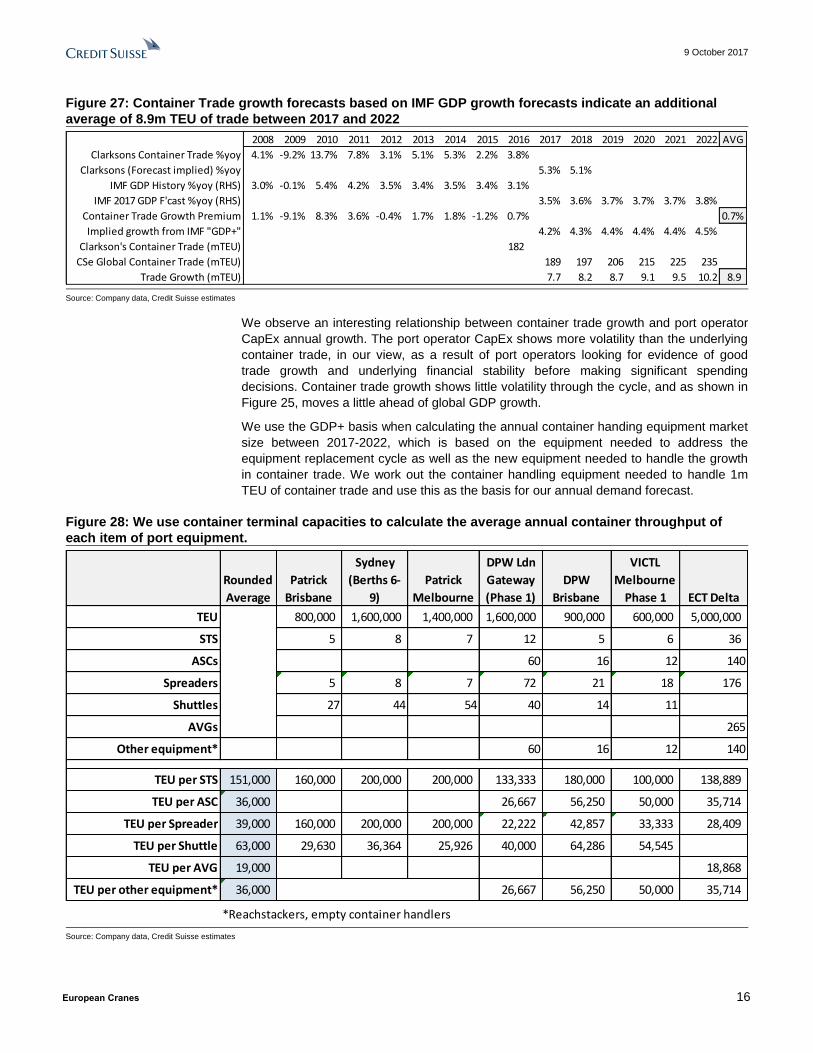

Figure 27: Container Trade growth forecasts based on IMF GDP growth forecasts indicate an additional

average of 8.9m TEU of trade between 2017 and 2022

Source: Company data, Credit Suisse estimates

We observe an interesting relationship between container trade growth and port operator

CapEx annual growth. The port operator CapEx shows more volatility than the underlying

container trade, in our view, as a result of port operators looking for evidence of good

trade growth and underlying financial stability before making significant spending

decisions. Container trade growth shows little volatility through the cycle, and as shown in

Figure 25, moves a little ahead of global GDP growth.

We use the GDP+ basis when calculating the annual container handing equipment market

size between 2017-2022, which is based on the equipment needed to address the

equipment replacement cycle as well as the new equipment needed to handle the growth

in container trade. We work out the container handling equipment needed to handle 1m

TEU of container trade and use this as the basis for our annual demand forecast.

Figure 28: We use container terminal capacities to calculate the average annual container throughput of

each item of port equipment.

Source: Company data, Credit Suisse estimates

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 AVG

Clarksons Container Trade %yoy 4.1% -9.2% 13.7% 7.8% 3.1% 5.1% 5.3% 2.2% 3.8%

Clarksons (Forecast implied) %yoy 5.3% 5.1%

IMF GDP History %yoy (RHS) 3.0% -0.1% 5.4% 4.2% 3.5% 3.4% 3.5% 3.4% 3.1%

IMF 2017 GDP F'cast %yoy (RHS) 3.5% 3.6% 3.7% 3.7% 3.7% 3.8%

Container Trade Growth Premium 1.1% -9.1% 8.3% 3.6% -0.4% 1.7% 1.8% -1.2% 0.7% 0.7%

Implied growth from IMF "GDP+" 4.2% 4.3% 4.4% 4.4% 4.4% 4.5%

Clarkson's Container Trade (mTEU) 182

CSe Global Container Trade (mTEU) 189 197 206 215 225 235

Trade Growth (mTEU) 7.7 8.2 8.7 9.1 9.5 10.2 8.9

Rounded

Average

Patrick

Brisbane

Patrick

Sydney

(Berths 6-

9)

Patrick

Melbourne

DPW Ldn

Gateway

(Phase 1)

DPW

Brisbane

VICTL

Melbourne

Phase 1 ECT Delta

TEU 800,000 1,600,000 1,400,000 1,600,000 900,000 600,000 5,000,000

STS 5 8 7 12 5 6 36

ASCs 60 16 12 140

Spreaders 5 8 7 72 21 18 176

Shuttles 27 44 54 40 14 11

AVGs 265

Other equipment* 60 16 12 140

TEU per STS 151,000 160,000 200,000 200,000 133,333 180,000 100,000 138,889

TEU per ASC 36,000 26,667 56,250 50,000 35,714

TEU per Spreader 39,000 160,000 200,000 200,000 22,222 42,857 33,333 28,409

TEU per Shuttle 63,000 29,630 36,364 25,926 40,000 64,286 54,545

TEU per AVG 19,000 18,868

TEU per other equipment* 36,000 26,667 56,250 50,000 35,714

*Reachstackers, empty container handlers

9 October 2017

European Cranes 17

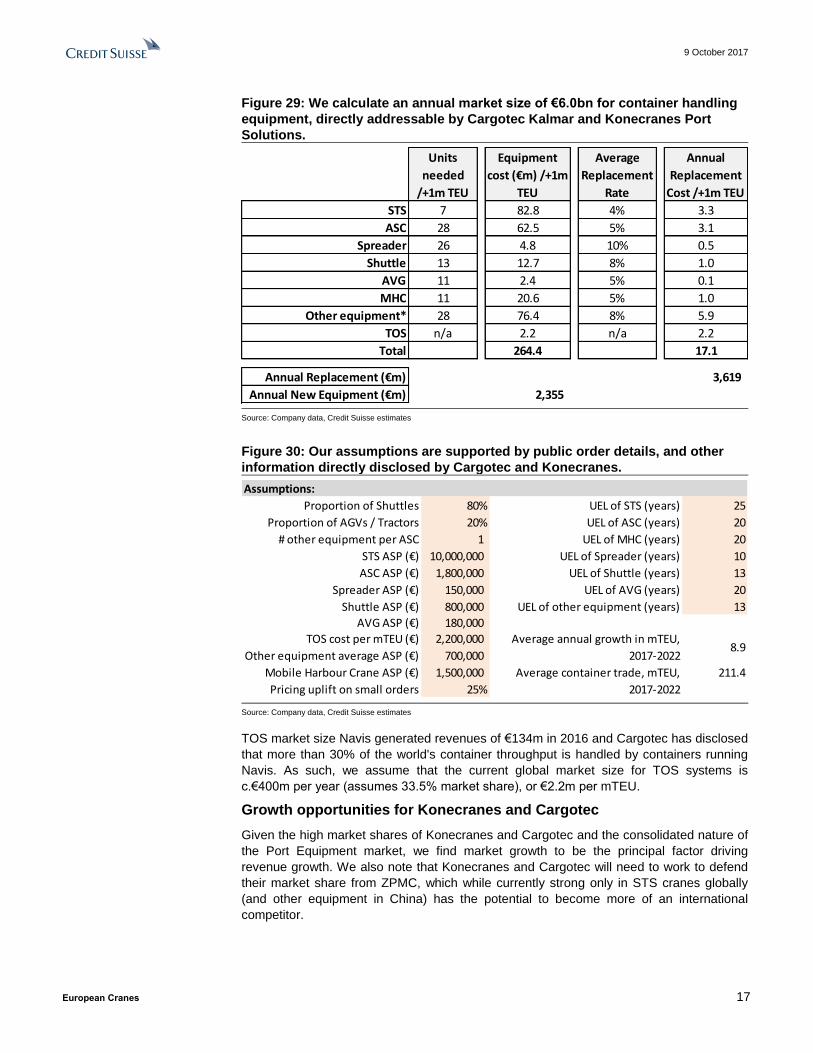

Figure 29: We calculate an annual market size of €6.0bn for container handling

equipment, directly addressable by Cargotec Kalmar and Konecranes Port

Solutions.

Source: Company data, Credit Suisse estimates

Figure 30: Our assumptions are supported by public order details, and other

information directly disclosed by Cargotec and Konecranes.

Source: Company data, Credit Suisse estimates

TOS market size Navis generated revenues of €134m in 2016 and Cargotec has disclosed

that more than 30% of the world's container throughput is handled by containers running

Navis. As such, we assume that the current global market size for TOS systems is

c.€400m per year (assumes 33.5% market share), or €2.2m per mTEU.

Growth opportunities for Konecranes and Cargotec

Given the high market shares of Konecranes and Cargotec and the consolidated nature of

the Port Equipment market, we find market growth to be the principal factor driving

revenue growth. We also note that Konecranes and Cargotec will need to work to defend

their market share from ZPMC, which while currently strong only in STS cranes globally

(and other equipment in China) has the potential to become more of an international

competitor.

Units

needed

/+1m TEU

New

Equipment

cost (€m) /+1m

TEU

Average

Replacement

Rate

Annual

Replacement

Cost /+1m TEU

STS 7 82.8 4% 3.3

ASC 28 62.5 5% 3.1

Spreader 26 4.8 10% 0.5

Shuttle 13 12.7 8% 1.0

AVG 11 2.4 5% 0.1

MHC 11 20.6 5% 1.0

Other equipment* 28 76.4 8% 5.9

TOS n/a 2.2 n/a 2.2

Total 264.4 17.1

Annual Replacement (€m) 3,619

Annual New Equipment (€m) 2,355

Proportion of Shuttles 80% UEL of STS (years) 25

Proportion of AGVs / Tractors 20% UEL of ASC (years) 20

# other equipment per ASC 1 UEL of MHC (years) 20

STS ASP (€) 10,000,000 UEL of Spreader (years) 10

ASC ASP (€) 1,800,000 UEL of Shuttle (years) 13

Spreader ASP (€) 150,000 UEL of AVG (years) 20

Shuttle ASP (€) 800,000 UEL of other equipment (years) 13

AVG ASP (€) 180,000

TOS cost per mTEU (€) 2,200,000

Other equipment average ASP (€) 700,000

Mobile Harbour Crane ASP (€) 1,500,000 211.4

Pricing uplift on small orders 25%

Average annual growth in mTEU,

2017-20228.9

Average container trade, mTEU,

2017-2022

Assumptions:

9 October 2017

European Cranes 18

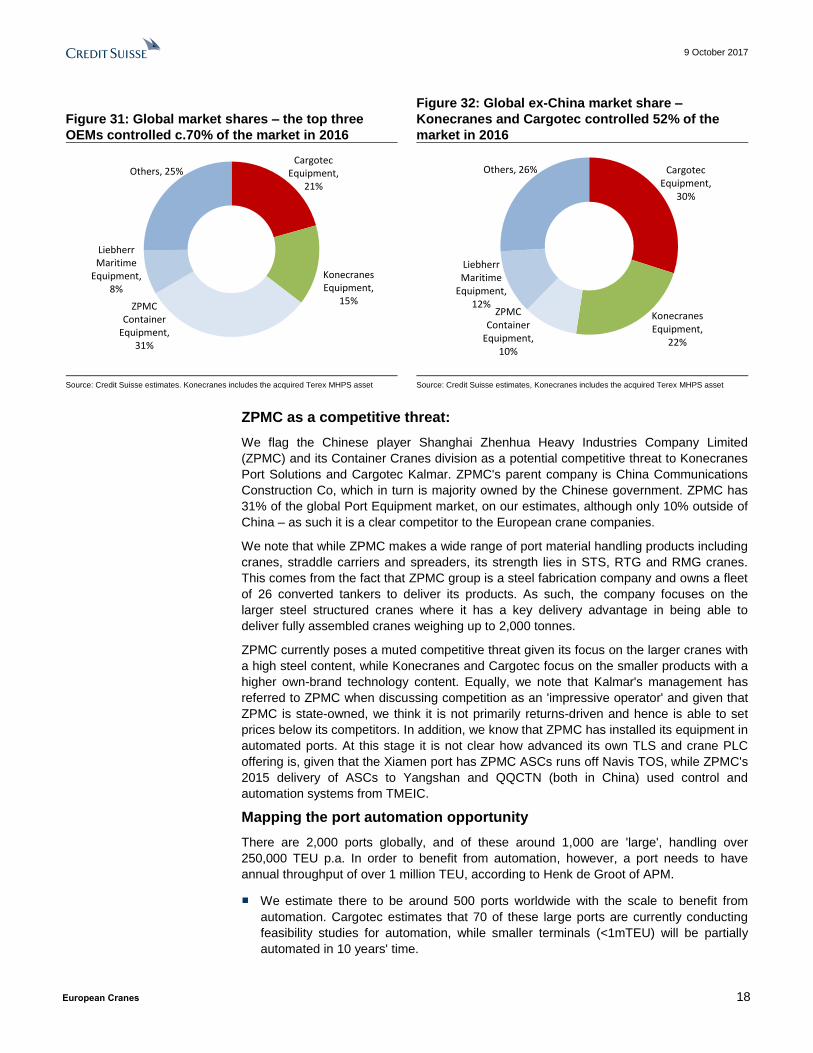

Figure 31: Global market shares – the top three

OEMs controlled c.70% of the market in 2016

Figure 32: Global ex-China market share –

Konecranes and Cargotec controlled 52% of the

market in 2016

Source: Credit Suisse estimates. Konecranes includes the acquired Terex MHPS asset Source: Credit Suisse estimates, Konecranes includes the acquired Terex MHPS asset

ZPMC as a competitive threat:

We flag the Chinese player Shanghai Zhenhua Heavy Industries Company Limited

(ZPMC) and its Container Cranes division as a potential competitive threat to Konecranes

Port Solutions and Cargotec Kalmar. ZPMC's parent company is China Communications

Construction Co, which in turn is majority owned by the Chinese government. ZPMC has

31% of the global Port Equipment market, on our estimates, although only 10% outside of

China – as such it is a clear competitor to the European crane companies.

We note that while ZPMC makes a wide range of port material handling products including

cranes, straddle carriers and spreaders, its strength lies in STS, RTG and RMG cranes.

This comes from the fact that ZPMC group is a steel fabrication company and owns a fleet

of 26 converted tankers to deliver its products. As such, the company focuses on the

larger steel structured cranes where it has a key delivery advantage in being able to

deliver fully assembled cranes weighing up to 2,000 tonnes.

ZPMC currently poses a muted competitive threat given its focus on the larger cranes with

a high steel content, while Konecranes and Cargotec focus on the smaller products with a

higher own-brand technology content. Equally, we note that Kalmar's management has

referred to ZPMC when discussing competition as an 'impressive operator' and given that

ZPMC is state-owned, we think it is not primarily returns-driven and hence is able to set

prices below its competitors. In addition, we know that ZPMC has installed its equipment in

automated ports. At this stage it is not clear how advanced its own TLS and crane PLC

offering is, given that the Xiamen port has ZPMC ASCs runs off Navis TOS, while ZPMC's

2015 delivery of ASCs to Yangshan and QQCTN (both in China) used control and

automation systems from TMEIC.

Mapping the port automation opportunity

There are 2,000 ports globally, and of these around 1,000 are 'large', handling over

250,000 TEU p.a. In order to benefit from automation, however, a port needs to have

annual throughput of over 1 million TEU, according to Henk de Groot of APM.

■ We estimate there to be around 500 ports worldwide with the scale to benefit from

automation. Cargotec estimates that 70 of these large ports are currently conducting

feasibility studies for automation, while smaller terminals (<1mTEU) will be partially

automated in 10 years' time.

Cargotec Equipment,

21%

Konecranes Equipment,

15%ZPMC Container

Equipment, 31%

Liebherr Maritime

Equipment, 8%

Others, 25% Cargotec Equipment,

30%

Konecranes Equipment,

22%

ZPMC Container

Equipment, 10%

Liebherr Maritime

Equipment, 12%

Others, 26%

9 October 2017

European Cranes 19

■ Currently, 40 are significantly automated, typically in the ASC stacking area only.

■ We identify seven ports that can be classified as semi-automated, where at least two

aspects of the terminal are automated:

− HHLA CTB Germany

− DPW London Gateway, UK

− Antwerp, Belgium

− DPW Brisbane, Australia

− Patrick Brisbane, Australia

− Patrick Sydney, Australia

− Jebel Ali T3 / T4, Dubai

■ We identify five ports that can be classified as fully or nearly fully automated:

− APM MV2 & ECT Delta, Rotterdam, Netherlands

− Los Angeles TraPac, US

− Long Beach Container Terminal, US

− VICT Melbourne, Australia

− Qingdao QQCTN, China

■ The bulk of the terminal automation market lies in the conversion of brownfield sites, as

opposed to the creation of new 'greenfield' ports. As such, inter-operability of

automated equipment with all brands, as well as the interface with legacy manual

equipment, is key for the container terminal operators.

■ Maersk wants to automate 20 terminals on the Rotterdam MV2 blueprint, and has

stated it aims for its cranes to "beat the manually-operated cranes' average

performance by 50%". The MV2 terminal cost $535m, according to Maersk.

■ DPW London Gateway is built with seven potential berths. Berths 1-3 are all in full use

(capacity: 1.6m TEU), while 4-7 are undeveloped and a decision on whether or not to

expand will be made in H2 2017 Implementation of automation will be more

straightforward in the future, drawing on lessons from the current offering. DP World

noted that the installation of Berth 3 was very simple and a direct copy of the system

already in place – Cargotec cites the 'copy with pride' principle as a pathway to

improve implementation.

■ The payback period of investing in an automated system is thought to be up to 6 years,

according to Cargotec Equally, though, developing and building the concept will take 4-

5 years.

Equipment choice

■ Port terminals typically involve several integrated systems. For example, London

Gateway uses Kalmar shuttle carriers and ASCs, ZPMC STS cranes partly automated

by ABB and OCR camera systems by CamCo. Most of the case studies cited by

Cargotec highlight the importance of being a systems integrator as well as

manufacturer.

■ Cargotec is aware of the risk of overlap with the big industrial automation names, and

approaches this by trying to create the right interface that works for the customer to

improve profitability, rather than focusing on selling a competing cloud product or a

9 October 2017

European Cranes 20

connectivity box. There are currently 17 terminals using Navis automated TOS,

including QQCTN, and they are integrated with products from a variety of other OEMs,

including Konecranes.

■ STS cranes are not typically automated due to software issues – according to DP

World, there is not a sufficiently stable system available yet. In readiness for the

required developments in software, one-third of the cranes at London Gateway are

automation-ready and can already be remotely controlled. We anticipate that ports that

have purchased 'automation-ready' equipment will switch over as soon as the Lifts per

Hour exceed those of manual operations, assuming labour negotiations are resolved.

■ In terms of servicing the largest ships, increasing the height and reach of cranes is

essential and a profitable business for Kalmar and Port Solutions (though Kalmar has a

mixed record in execution). We expect this business to continue growing steadily as

the average vessel size of the global fleet continues to increase.

■ We see automation as an interesting driver to accelerate the replacement cycle; DP

World tends to replace equipment before the expected end-of-life as new technology is

introduced. Across the board, DP World builds everything automation-ready as an

operational hedge against rising labour costs.

Conclusion:

We think 2018 will prove to be a key milestone in terminal automation: LPH rates at

automated terminals will exceed those at manual terminals, while safety and

environmental benefits should increase the appeal of automated terminals across both

cost and operational criteria.

We forecast the Port Operator CapEx cycle turning in 2018: This should provide a

supportive base for automation offerings as port operators' investment decisions catch up.

Chinese competition in certain equipment types, but not automation – yet: We flag

ZPMC as a credible competitor in certain product types, but currently this only extends to

STS and ASCs, where the proportion of steel relative to technology is much higher. We

also note that ZPMC currently outsources the procurement of automated systems that are

built into its cranes. However, we continue to watch for signs of improvement in ZPMC's

in-house technology.

Union strength will likely be a hurdle: We anticipate that Port Operators' negotiations

with employee unions will be complex and could dampen the speed of automation uptake.

As a result, we do not explicitly build benefits in volume and pricing from automation into

our forecasts.

Figure 33: What are we discounting?

Source: Company data, Credit Suisse estimates

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E

World Container Exports growth 4% -9% 14% 8% 3% 5% 5% 2% 4% 4% 4% 4% 4%

CS Proprietary Port Capex Growth Model 19% -29% 4% 22% 8% 9% -13% 29% 1% -8% 8% 14% 8%

Cargotec Kalmar org. growth 16% -33% -12% 19% 24% 5% -3% 4% 2% -1% 4% 12% 7%

Konecranes P.S. org. growth -4% 3% 13% 8%

9 October 2017

European Cranes 21

Medium-term Driver #2: Industrial Crane and Port Equipment industry concentration should lead to better margins

Summary:

1. Industry concentration in Industrial and Container cranes has now reached its likely

conclusion, in our view, following c.20 separate acquisitions in the space, culminating with

Konecranes' acquisition of Terex MHPS.

2. According to our estimates, in Container cranes, Cargotec, Konecranes and ZPMC

control 70% of the market, while globally ex. China, Cargotec and Konecranes control

c.60% of the market.

3. In the Global Industrial crane market, the top two OEMs, Konecranes and Columbus

McKinnon, control c.50% of the market, with no other players of similar scale.

4. We find the remedy enforced by the European Commission following the MHPS

acquisition relatively favourable for Konecranes, requiring only divestment of a specialist

product group with €135m in annual revenues while the company gains €436m of NI

sales, further concentrating the mid-range market in particular.

5. As a result of industry concentration, we identify pricing tailwinds worth 75bps in 2018E

and 50bps in 2019E for Konecranes, mainly in the Industrial crane segment, while deal-

related synergies provide €140m of run-rate EBIT benefit by 2021E.

Figure 34: Kito, Columbus McKinnon and Konecranes the scale players in Industrial cranes, while

Cargotec, Konecranes, ZPMC and Liebherr are the only OEMs with diversified Port Equipment offerings

Source: Company data, Credit Suisse estimates. We have only included acquisitions from the Industrial Crane and Port Equipment markets.

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

PWB Anchor

ARMSEL MHE

Kito Kito

Yale International

Columbus McKinnon Columbus McKinnon

CVS Ferrari CVS Ferrari

Belotti * Cargotec's bid for CVS Ferrari was blocked CVS Service

by the German Competition Commission

Demag Cranes

Noell

Fantuzzi

Terex (MHPS)

WMI Cranes Ltd

Asio Sistemas de Elevacion

Eydimen 2000

Meiden Host Systems

Consens Transport Sys.

MMH

Stahl Cranesystems

SMV Lifttrucks AB

MAN SWF

Konecranes Konecranes

Kone

Cargotec Cargotec

Navis

Asciano Automation

ZPMC ZPMC

Liebherr Liebherr

9 October 2017

European Cranes 22

Market shares by product type

Port Equipment:

Ship to Shore (STS) cranes: ZPMC is the clear leader globally and in Europe. As a steel

structures fabricator with its own transport fleet, ZPMC looks ideally placed to dominate

this product type. We anticipate that Cargotec may erode a small portion of ZPMC's

market share, having announced that it will produce STS cranes at its Taicang, China

production site. The Konecranes / Terex MHPS transaction has had a small impact in

concentrating this market, bringing the number of competitors to ZPMC down from four to

three; however due to the market domination by ZPMC; we do not expect the market

dynamics to change significantly.

Figure 35: Global STS Crane Market Share was

dominated by ZPMC in 2016

Figure 36: EMEA + Americas STS Crane Market

Share in 2016

Source: WorldCargoNews 2016 Source: WorldCargoNews, Credit Suisse estimates

Automatic Stacking Cranes (ASC): the Konecranes / Terex MHPS transaction has

significantly increased supplier concentration. Globally, the three largest players control

85% of the market, and within Europe this rises to c.97% of the market. The effect of the

consolidation is most visible in Europe, where Konecranes now controls 40% of the

market, having previously had only a 25% market share, behind Cargotec.

Figure 37: Global ASC Crane Market Share Figure 38: Europe ASC Crane Market Share

Source: European Commission (2016) Source: European Commission (2016)

ZPMC82%

Konecranes1.5%

Terex Demag1.5%

Liebherr7.0%

Sany0.7%

Kocks Krane3.0%

Others4%

ZPMC69.8%

Konecranes3.2%

Terex Demag3.2%

Liebherr14.3%

Sany1.6%

Kocks Krane4.8%

ZPMC35%

Konecranes25%

Terex Demag

8%

Cargotec25%

Hans Kunz8%

ZPMC3%

Konecranes15%

Terex Demag

25%Cargotec35%

Hans Kunz23%

9 October 2017

European Cranes 23

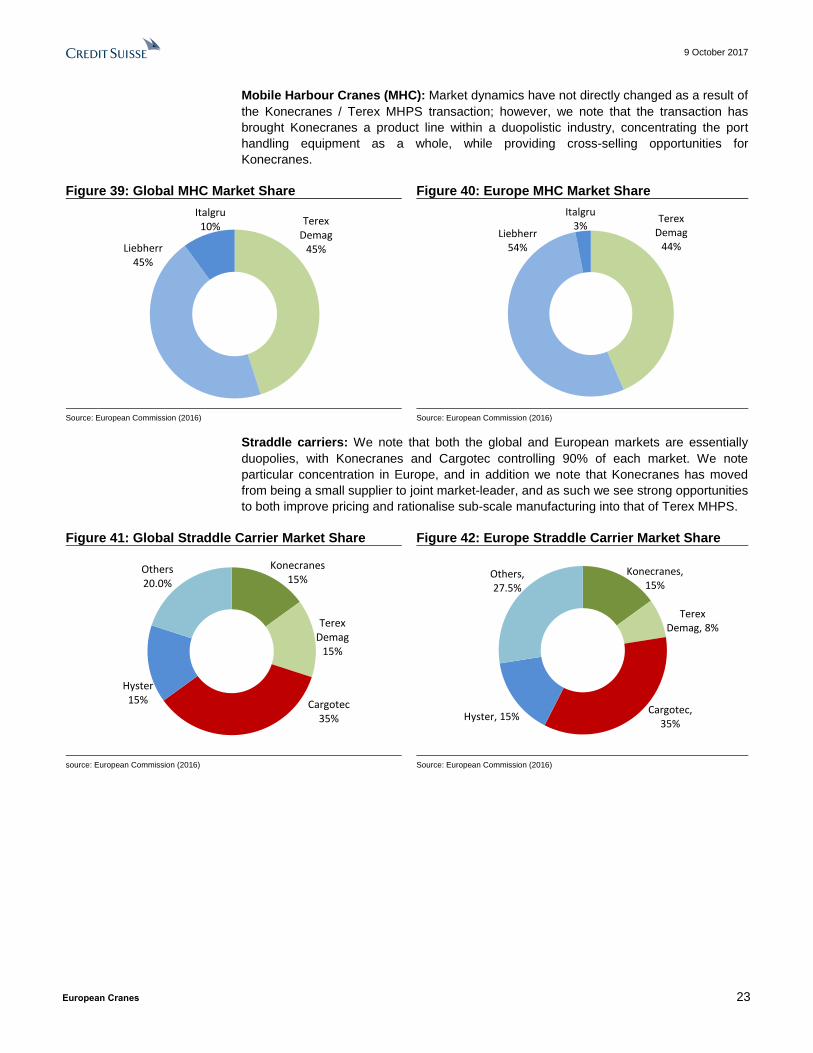

Mobile Harbour Cranes (MHC): Market dynamics have not directly changed as a result of

the Konecranes / Terex MHPS transaction; however, we note that the transaction has

brought Konecranes a product line within a duopolistic industry, concentrating the port

handling equipment as a whole, while providing cross-selling opportunities for

Konecranes.

Figure 39: Global MHC Market Share Figure 40: Europe MHC Market Share

Source: European Commission (2016) Source: European Commission (2016)

Straddle carriers: We note that both the global and European markets are essentially

duopolies, with Konecranes and Cargotec controlling 90% of each market. We note

particular concentration in Europe, and in addition we note that Konecranes has moved

from being a small supplier to joint market-leader, and as such we see strong opportunities

to both improve pricing and rationalise sub-scale manufacturing into that of Terex MHPS.

Figure 41: Global Straddle Carrier Market Share Figure 42: Europe Straddle Carrier Market Share

source: European Commission (2016) Source: European Commission (2016)

Terex Demag

45%Liebherr45%

Italgru10%

Terex Demag

44%Liebherr

54%

Italgru3%

Konecranes15%

Terex Demag

15%

Cargotec35%

Hyster15%

Others20.0%

Konecranes, 15%

Terex Demag, 8%

Cargotec, 35%

Hyster, 15%

Others, 27.5%

9 October 2017

European Cranes 24

Reach stackers: The market has been significantly concentrated following the

Konecranes / Terex MHPS consolidation, bringing 80% of the global market, and c.73% of

the European market under the control of three rather than four players. We see the reach

stacker market as being a potential area for continued consolidation given the fragmented

players (CVS Ferrari, Liebherr, Hoist, Unicarriers) operating in the residual part of the

market. That being said, we also note that reach stackers are not the highest-value items

in the port terminal handling portfolio given that they are not an automation target and use

hydraulic systems rather than motors and drives.

Figure 43: Global Reach Stacker Market Share Figure 44: Europe Reach Stacker Market Share

Source: European Commission (2016) Source: European Commission (2016)

Terminal Operating Software (TOS): Navis is the undisputed leader with a 25% market

share in a highly fragmented market (when excluding the small terminals, Navis has 39%

market share). TOS is a key part of Cargotec's acquisition strategy as the company aims

to invest in software assets, and as such we see this part of the market consolidating as

Cargotec acquires smaller vendors or takes large in-house generated software systems

under the Navis name. Konecranes has only a sub-scale offering in TOS that was

acquired from Terex. Both Konecranes and ZPMC sell Navis in their automation projects.

Figure 45: Global TOS Market Share (All Port Terminals)

Source: Cargotec Software Analyst day 2017

Konecranes7%

Terex Demag

38%Cargotec

45%

Liebherr5%

Others5% Konecranes

7%

Terex Demag45%

Cargotec45%

Liebherr3%

25%

4%

5%

3%5%

3%3%16%

36%

Cargotec Navis

TSB

Tideworks

Huadong

Jade

China Merchants

PSA

Others

Small Terminals

9 October 2017

European Cranes 25

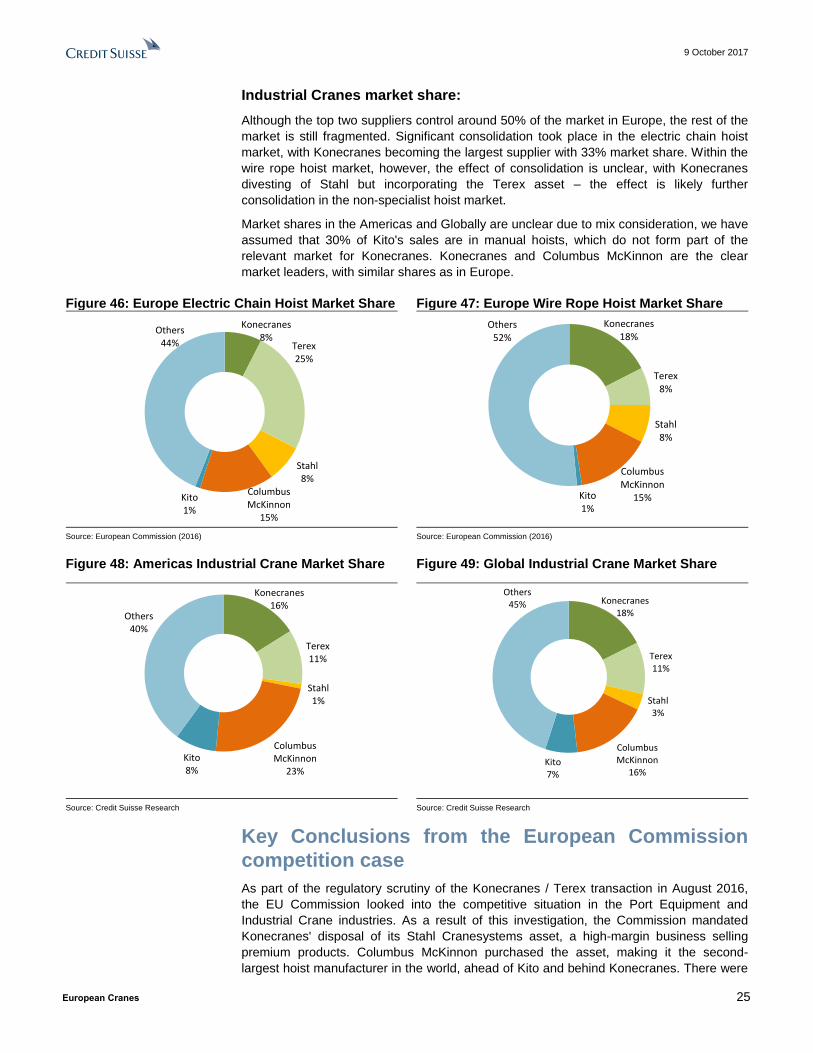

Industrial Cranes market share:

Although the top two suppliers control around 50% of the market in Europe, the rest of the

market is still fragmented. Significant consolidation took place in the electric chain hoist

market, with Konecranes becoming the largest supplier with 33% market share. Within the

wire rope hoist market, however, the effect of consolidation is unclear, with Konecranes

divesting of Stahl but incorporating the Terex asset – the effect is likely further

consolidation in the non-specialist hoist market.

Market shares in the Americas and Globally are unclear due to mix consideration, we have

assumed that 30% of Kito's sales are in manual hoists, which do not form part of the

relevant market for Konecranes. Konecranes and Columbus McKinnon are the clear

market leaders, with similar shares as in Europe.

Figure 46: Europe Electric Chain Hoist Market Share Figure 47: Europe Wire Rope Hoist Market Share

Source: European Commission (2016) Source: European Commission (2016)

Figure 48: Americas Industrial Crane Market Share Figure 49: Global Industrial Crane Market Share

Source: Credit Suisse Research Source: Credit Suisse Research

Key Conclusions from the European Commission

competition case

As part of the regulatory scrutiny of the Konecranes / Terex transaction in August 2016,

the EU Commission looked into the competitive situation in the Port Equipment and

Industrial Crane industries. As a result of this investigation, the Commission mandated

Konecranes' disposal of its Stahl Cranesystems asset, a high-margin business selling

premium products. Columbus McKinnon purchased the asset, making it the second-

largest hoist manufacturer in the world, ahead of Kito and behind Konecranes. There were

Konecranes8%

Terex25%

Stahl 8%

Columbus McKinnon

15%

Kito1%

Others44%

Konecranes18%

Terex8%

Stahl 8%

Columbus McKinnon

15%Kito1%

Others52%

Konecranes16%

Terex11%

Stahl 1%

Columbus McKinnon

23%

Kito8%

Others40%

Konecranes18%

Terex11%

Stahl 3%

Columbus McKinnon

16%Kito7%

Others45%

9 October 2017

European Cranes 26

no remedies required in the port machinery markets. Interestingly, the European

Commission considered the industrial crane market (i.e. the fully constructed crane

including steel structure) to be distinct from the industrial hoist market.

In our view, and as confirmed by Konecranes in past earnings calls, the motors, gears and

drives contain the technology content and drive service revenues. In addition, Konecranes

supplies these components to independent crane builders which carry different branding

(the 'power' brands) but are essentially the same product. As such, in some competitive

tenders, a Konecranes branded crane is tendering alongside one built by a local crane

builder but using a Konecranes power brand hoist. With both businesses equally profitable

to Konecranes, we see this route to market as advantageous, particularly in the context of

industry concentration.

As such, arguably Konecranes may have sidestepped some competitive concerns in only

being required to dispose of Stahl Cranesystems (€135m in annual revenues), while

growing its Industrial Equipment business by 36% and its Industrial Crane Service

business by 33%.

Link to EU Commission Findings

Industrial cranes (standard cranes and process cranes):

EU Commission Findings:

Industrial cranes allow handling loads, between 100 kilos and 100 tons.

Konecranes and Terex were well-established players in industrial cranes, and

Terex's KBK also has a strong product offering in modular cranes.

Standard industrial cranes are mainly used for lifting heavy loads, whereas

modular cranes are used in the assembly areas of production sites for light

loads (up to 2 tons), short span (below 8 metres), more precise than

standard cranes, as well as more expensive (up to 5 times the price of a

standard crane).

In the course of the European Commission market investigation, the majority

of customers indicated that they normally buy cranes prevalently in their own

country of operation and have limited information about pricing and

competitive offers made abroad.

Standard cranes is a mature market where barriers to entry are low and

expansion is easy. According to the Parties, there are no switching costs for

customers, who usually make their purchasing decision purely on the basis of

cost considerations. Finally, the Parties argue that there is excess capacity in

the market and that certain categories of customers of standard cranes, such

as OEMs and automotive players, can exert a significant degree of

bargaining power on standard crane suppliers.

Konecranes' brands have a price advantage (i.e. low prices) whereas Terex'

advantage is linked to the high quality, good reputation and the resulting high

brand loyalty associated to its products. In modular cranes, Terex KBK is

perceived as the best.

The majority of crane suppliers are not vertically integrated, but depend on

external suppliers for key components such as hoists. This implies that the

presence of alternative suppliers would likely eliminate all risks of anti-

competitive effect of the Transaction in relation to the crane markets.

CS view: Consolidation in a mature market is key to improving profitability. Konecranes is

a component supplier as well as industrial crane builder under its Verlinde, SWF, R&M

and now Demag brands. As such, we see Konecranes as particularly well positioned to

benefit from the consolidation.

9 October 2017

European Cranes 27

Hoists for industrial cranes:

EU Commission Findings:

The hoist is the lifting device of a crane, with either chain or wire rope.

Serially produced wire rope hoists are available with capacity up to 100T.

Largest volumes of chain hoists sold are with capacity up to 5T. Hoists can

be segmented in relation to their ability to change lifting and travelling speed.

Variable speed hoists, are particularly valuable in applications where care or

precision is needed. Most hoists only allow fixed speeds. The ability of

varying the speed is obtained by fitting a hoist with a frequency inverter.

The notifying party submits that the relevant geographic market for hoists is

global. This conclusion is based on the consideration that hoists are small

and relatively light, which makes long-distance transportation cost-efficient

Konecranes’ and Terex's price lists are brand-specific and global. Volume is

the main factor when considering discounts. Brands are consistently included

among the most relevant criteria for selecting a hoist supplier

The mix of distribution channels used by hoists' suppliers also varies by

country. One qualified hoists' competitor noted that "In Germany, France,

Netherlands and Austria, GI distribution plays a bigger role. In other countries

the crane builders and buyers of crane components/ component distributors

are more important. There is a high portion of direct sales from producers.

Demag is the leader in Germany/Austria while Konecranes' Verlinde is

strongest in France. Germany is the largest market in Europe for hoists,

accounting for c.35% of EEA sales for electric chain hoists and for c.25% of

total EEA sales for wire rope hoists.

The Commission understands that Konecranes (Stahl, SWF, Verlinde) and

Terex brands (Demag and Donati) are highly recognised amongst hoist users

as high quality and expensive products which constitute the main alternative.

One crane builder noted "Their products are becoming increasingly

expensive and in line and it is becoming very hard to find competitive prices

which was very easy before Kone bought out all the other companies"

As a consequence of these (and other) views, the Commission understands

that a majority of crane builders see the Transaction as having a negative

effect for hoists. The balance of views is stronger for variable speed wire rope

hoists and electric chain hoists. The Commission understands that similar

concerns have been echoed by distributors of hoists and to a lesser extent by

competitors for hoists. On these bases, the Commission considers that, even

if barriers to entry do not appear to be particularly high in technical terms, the

current saturation of the hoist markets by the major manufacturers would

make it particularly challenging to enter such markets, especially in Germany.

CS view: This strong response from customers drove the Commission to request the

disposal of Stahl, which reduced the market dominance of Konecranes, particularly in

France and Germany. The Commission considered the disposal of the whole overlap for

wire rope hoists and about half the overlap for electric chain hoists in the EEA and

Germany, while removing around half the overlap for wire rope hoists and electric chain

hoists in France. We find it interesting to note that hoist competitors (Kito, Columbus

McKinnon) were less opposed to the transaction than customers and distributors. We see

this as a sign that consolidation will improve pricing discipline among OEMs and reduce

competitive pressure in tenders.

9 October 2017

European Cranes 28

Provision of industrial crane services:

EU Commission Findings:

Konecranes offers services for its own and 3rd

party industrial cranes. Terex

has more limited services, which are focused on its own installed base.

The proposed Transaction gives rise to horizontally affected markets for the

supply of services in 8 European countries, where the Parties' combined

market share would range between [20-30]% (Austria, Estonia, Hungary) and

[50-60]% (Finland).

During the investigation, market participants (especially independent service

providers) raised concerns also in relation to the availability and prices of

spare parts post-merger, as well as on the availability and accessibility of the

certificates to be issued by the merged entity in order to allow third party

suppliers to perform inspections/maintenance/repairs on cranes and cranes

components. The Commission considers that those concerns are not

specifically linked to the proposed Transaction as access to spare parts was

already under the exclusive control of OEMs prior to the merger.

CS view: We note that Stahl Cranesystems was not sold with any service business, so the

transaction has further consolidated the fragmented market for industrial crane services.

We do not see any resulting sales synergies from the consolidation, though clearly there

may be cost synergies from joining service centres and growing the density of installed

base per service centre.

Supply of port equipment:

EU Commission Findings:

In straddle carriers, while Terex has been very strong, Konecranes is a small

player; its straddle carrier business has been unprofitable for a number of

years. Konecranes shut down its plant in Germany that was dedicated to

straddle carriers and shifted to using subcontractors. Consistent with this

phasing-out strategy, Konecranes has adopted an extremely selective

bidding strategy

The Commission considers that the Transaction entails a reduction of the

number of sizable players in the straddle carrier market from three to two.

The Parties submit that ZPMC is believed to be bidding to supply straddle

carriers in both U.S. and European opportunities

In ASCs, the Commission understands that neither Terex nor Konecranes

are considered as important suppliers for ASCs. In this relatively new market,

competition for all contracts is intense, particularly for the larger international

contracts that serve to attract even further business. Besides, the Parties

submit they will face aggressive price competition from ZPMC (although its

presence in Europe remains fairly limited).

The Commission did not identify any issues in the Reach Stackers market.

CS view: The competitive pressure from ZPMC was generally flagged as a factor

preventing a duopoly in port equipment, though we note that ZPMC is less of a competitive

threat in Europe and the US than in its home market of China. We also find it interesting

that the Commission left the exact definition of an ASC imprecise, and did not consider the

RTG or RMG markets in its analysis. We see the consolidation as a positive for

Konecranes and Cargotec, both in bringing down the number of global players from four

to three and creating opportunities to bring together sub-scale equipment manufacturing

facilities at Konecranes – for instance via closure of the lossmaking Lentigione site for

container handlers and terminal tractors.

9 October 2017

European Cranes 29

Effect on Pricing

In the port equipment market, we do not expect consolidation to lead to immediate

improvements in pricing dynamics, as the industry is currently in a hiatus period while the

port terminal operators' capex cycle turns. In the mid-term, however, we expect the

consolidation to be protective for Cargotec Kalmar's and Konecranes Port Solutions'

pricing, and should offset the pricing pressure generated by the port operators who are

careful to spread tenders across multiple vendors where possible. The transaction has

also provided Konecranes with the scale to catch up with Cargotec.

Hou and Robinson examined a range of industries for the years 1963-2001 and found that