europeaid/138-539/dh/ser/lk technical assistance to the

TRANSCRIPT

Technical Assistance to the Modernisation of

Agriculture Programme in Sri Lanka

EuropeAid/138-539/DH/SER/LK Technical Assistance to the Modernisation of Agricultural Programme in Sri Lanka (TAMAP)

TAMAP Value Chain Analysis Study On Floriculture In Sri Lanka March 2020 Submitted to: Delegation of the European Union to Sri Lanka and the Maldives 389, Bauddhaloka Mawatha, Colombo 7, Sri Lanka Ministry of National Policies & Economic Affairs Department of National Planning, The Secretariat, 1st floor Colombo 01, Sri Lanka

This project is implemented by a Consortium led by Ecorys Nederland, B.

Technical Assistance to the Modernisation of

Agriculture Programme in Sri Lanka

Technical Report: TAMAP Value Chain Analysis Study on Floriculture in Sri Lanka

Project title: Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

Project number: ACA/2017/389-911

Country: Sri Lanka

Address: Ecorys Nederland B.V Watermanweg 44 3067 GG Rotterdam The Netherlands

Tel. number: T: +31 10 453 86 76

Fax number: F : +31 10 453 87 55

Contact person: Nick Smart [email protected]

Date of report: 29 March 2020

VCD Studies Assignment period:

15 October to 1 November 2019

Disclaimer. The content of this report does not reflect the official opinion of the European Union. Responsibility for the information and views expressed lies entirely with the author(s) and the consortium led by Ecorys Nederland BV for the implementation of TAMAP

Technical Assistance to the Modernisation of

Agriculture Programme in Sri Lanka

PROJECT SYNOPSIS

Project Title: Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

Project Details: Project Ref. No:

EuropeAid/138-539/DH/SER/LK Programme Manager

Dr Olaf Heidelbach

Date of project start:

8 January 2018 Contracting Authority

Delegation of the European Union to Sri Lanka and the Maldives 389 Bauddhaloka Mawatha, Colombo 7, Sri Lanka

Contract Duration:

36 months Name of contact person (Contractor):

Project Director: Nick Smart

Contract No:

ACA/2017/389-911

Contractor’s name, address, telephone numbers and e-mail address:

Ecorys Nederland B.V Watermanweg 44 3067 GG Rotterdam The Netherlands T +31 (0)10 453 88 00 [email protected]

Total contracted amount:

EUR 4, 167, 000 Team Leader

Dr. Christof Batzlen Postal Address: Ministry of National Policies and Economic Affairs, Treasury Building, Lotus Road, Colombo 01, Sri Lanka.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page i

TAMAP Value Chain Analysis Study on Floriculture in Sri Lanka

1 EXECUTIVE SUMMARY............................................................................. 9

2 INTRODUCTION AND CONTEXT ............................................................ 16

2.1 Introduction to the project .......................................................................... 16

2.2 Challenges of the agriculture sector in Sri Lanka and its reorientation ....... 16

2.3 Value chain and VCA4D methodology....................................................... 17 2.3.1 What are value chains? ............................................................................. 17 2.3.2 VCA4D methodology ................................................................................. 18

2.4 Data collection........................................................................................... 19 2.4.1 Secondary data ......................................................................................... 19 2.4.2 Primary data .............................................................................................. 19 2.4.3 Why Floriculture was selected for the study .............................................. 19

2.5 Sector Overview in Sri Lanka .................................................................... 20 2.5.1 Live Plants and foliage .............................................................................. 20 2.5.2 Cut flower production ................................................................................ 22 2.5.3 Major species in Sri Lankan floriculture production .................................... 22 2.5.4 Exports and imports of floriculture products from and to Sri Lanka ............ 25 2.5.5 Production & exports of foliage and live plants and cut flowers ................. 26

2.6 Governance and Institutional framework ................................................... 28 2.6.1 Floriculture policies and strategies ............................................................ 28 2.6.2 Institutions responsible for and supporting the sector ................................ 29 2.6.3 Legal framework and acts ......................................................................... 30 2.6.4 Export and market requirements and licenses ........................................... 31

2.7 Problems encountered in the floriculture sector ......................................... 32 2.7.1 Live Plants and Foliage ............................................................................. 32 2.7.2 Cut flowers ................................................................................................ 34 2.7.3 Copying strategies of floriculture producers ............................................... 35

2.8 Demand related aspects on floriculture in Sri Lanka .................................. 36 2.8.1 Size of local and export market ................................................................. 36 2.8.2 Sri Lanka’s import and export of floriculture products ................................ 38 2.8.3 Cost of production of major competitors compared to Sri Lanka ................ 41 2.8.4 Growth of the floriculture sector in Sri Lanka ............................................. 43

3 FUNCTIONS ............................................................................................. 45

3.1 Function description .................................................................................. 45 3.1.1 Introduction ............................................................................................... 45 3.1.2 Organisational functions along the chain ................................................... 48 3.1.3 Marketing networks and distribution channels ........................................... 49 3.1.4 Stakeholder Strategies .............................................................................. 50 3.1.5 Horizontal and vertical coordination ........................................................... 51

3.2 Flows of Product ....................................................................................... 55 3.2.1 Value Chain network map ......................................................................... 56

3.3 Location of activities .................................................................................. 58

3.4 Quantification ............................................................................................ 59

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page ii

3.5 Contribution Analysis (distribution of margins along the value chain) ........ 59

3.6 Gross Margin Analysis .............................................................................. 66

3.7 Contribution of VC to public sector finance and balance of trade ............... 72

3.8 Viability of the VC in international economy ............................................... 72 3.8.1 Live plants and foliage ............................................................................... 72 3.8.2 Cut flowers ................................................................................................ 72

3.9 Competitiveness analysis .......................................................................... 73 3.9.1 Live plants and foliage ............................................................................... 73 3.9.2 Cut flowers ................................................................................................ 75

4 SOCIAL ANALYSIS.................................................................................. 77

4.1 Working Conditions in the VC acceptable .................................................. 77

4.2 Land and water rights in VC acceptable .................................................... 77

4.3 Gender equality in VC ............................................................................... 77

4.4 Social infrastructure and services acceptable ............................................ 78

5 ENVIRONMENTAL ANALYSIS ................................................................ 79

5.1 Impact of floriculture production on the environment ................................. 79

5.2 Impact of climate change on floriculture production ................................... 79

6 OPPORTUNITIES, OUTLOOK AND RECOMMENDATIONS ................... 81

6.1 Opportunities ............................................................................................. 81 6.1.1 Untapped potential in floriculture ............................................................... 81 6.1.2 Opportunities to develop the local market .................................................. 81 6.1.3 Opportunities to develop the out-grower schemes ..................................... 81 6.1.4 Potential to develop new products ............................................................. 81 6.1.5 Potential to develop semi-mechanisation .................................................. 81 6.1.6 Opportunity to develop foreign investment for exports ............................... 82

6.2 Outlook...................................................................................................... 82

6.3 Recommendations .................................................................................... 82 6.3.1 Improve the import regime for planting materials and agro inputs .............. 82 6.3.2 Improve export promotion to access new markets and products ............... 83 6.3.3 Establish recognised training ..................................................................... 83 6.3.4 Promote use of more efficient technologies and best management practices

.................................................................................................................. 83 6.3.5 Provide suitable public land for floriculture ................................................ 83 6.3.6 Promote the horizontal and vertical integration .......................................... 84

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page iii

List of Tables

Table 1 Utilisation of Sri Lankan floriculture sector products .................................. 25

Table 2 Major export markets for live plants from Sri Lanka in 2017 ...................... 39

Table 3 Major export markets for cut flowers from Sri Lanka in 2017 ..................... 39

Table 4 Major export markets for foliage from Sri Lanka in 2017 ............................ 40

Table 5 Distribution Channel Farmer > Collector > Florist – Gerbera flowers ......... 60

Table 6 Distribution Channel Farmer > Collector > Florist – Chrysanthemum flowers .................................................................................................................. 61

Table 7 Distribution Channel Farmer > Collector > Florist – Rose flowers .............. 62

Table 8 Distribution Channel Farmer > Collector > Florist – Lily flowers ................. 63

Table 9 Distribution Channel Farmer > Collector > Exporter – Queen palm (type of live plant) ................................................................................................... 64

Table 10 Distribution Channel Farmer > Collector > Exporter – Sandriyana stems (type of foliage) ......................................................................................... 65

Table 11 Gross margin analysis for Gerbera flowers ................................................ 66

Table 12 Gross margin analysis for Chrysanthemum flowers ................................... 67

Table 13 Gross margin analysis for Rose flowers .................................................... 68

Table 14 Gross margin analysis for Lily flowers ....................................................... 69

Table 15 Gross margin analysis for Queen Palm ..................................................... 70

Table 16 Gross margin analysis for Sandruyana stems ........................................... 71

Table 17 Difference between FOB export and CIF import in 2017 ........................... 76

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page iv

List of Figures

Figure 1 Comparison of exports of live plants and foliage ....................................... 21

Figure 2 Dynamics in Sri Lanka export prices of live plants and foliage ................... 21

Figure 3 Sri Lanka export of cut flowers .................................................................. 22

Figure 4 Imports and exports of floriculture products to and from Sri Lanka in 1000 US $ and metric tons ................................................................................. 25

Figure 5 Export value of floriculture products from Sri Lanka in US$ thousands ...... 26

Figure 6 Export from Sri Lanka and estimated production in metric tons ................. 27

Figure 7 Trend in imports of floriculture products in Sri Lanka ................................. 38

Figure 8 Prices for live plants and foliage in 2017 ................................................... 40

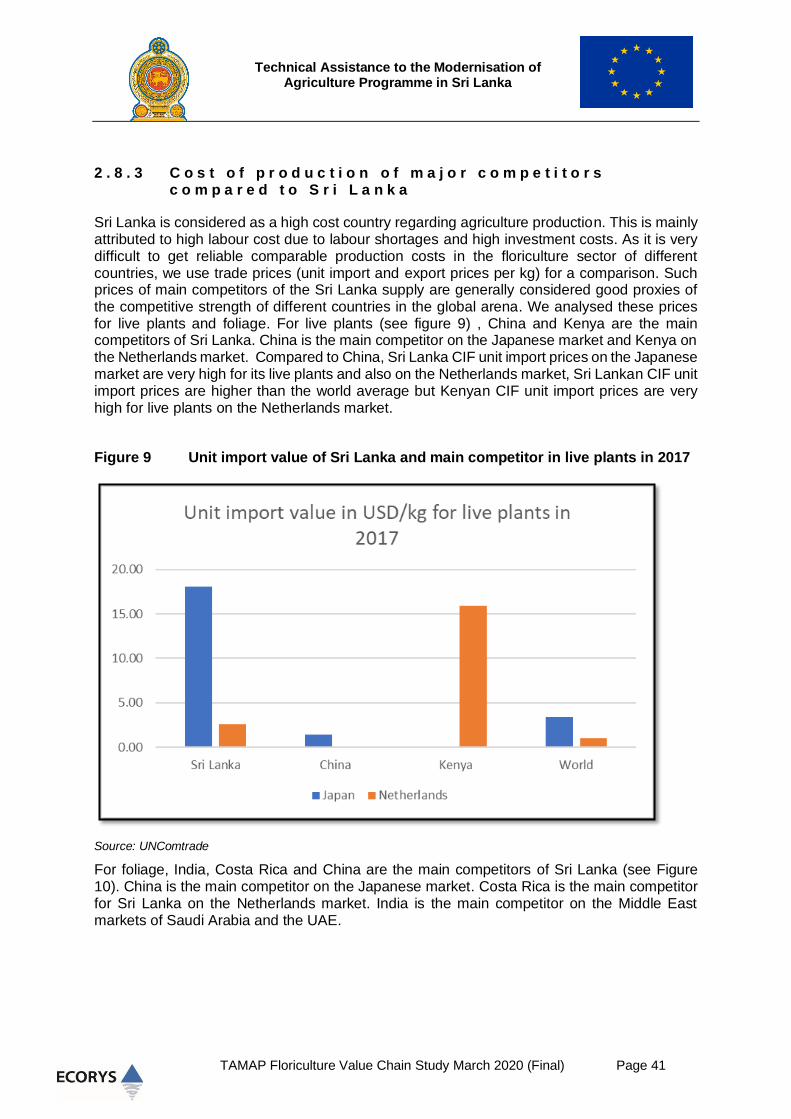

Figure 9 Unit import value of Sri Lanka and main competitor in live plants in 2017 .. 41

Figure 10 Unit import value of Sri Lanka and main competitor in foliage in 2017 ...... 42

Figure 11 Export value of live plants and foliage from Sri Lanka ............................... 43

Figure 12 Trend in exports of live plants and foliage from Sri Lanka.......................... 44

Figure 13 Floriculture sector value chain function map .............................................. 53

Figure 14 Floriculture sector value chain stakeholder map ........................................ 54

Figure 15 Value Chain map ....................................................................................... 57

Figure 16 Import share of Sri Lanka and main competitor in live plants in 2017 ........ 74

Figure 17 Import share of Sri Lanka and main competitor in foliage in 2017 .............. 75

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page v

List of Photos

Photo 1 Tropical floriculture products ..................................................................... 47

Photo 2 Tissue culture products ............................................................................. 48

Photo 3 Temperate zone floriculture products ........................................................ 55

Photo 4 Women working on flower farm ................................................................. 78

Units and measurements

Old system of measurements Modern, commonly understood measurements

1 acre 0.4048 ha = 4,048 m2

1 mile 1.6093 km

1 foot or feet 30.48 cm

1 acre feet (volume) 1,233.5 m3

1 cusec (1 cubic foot per second) 0.2832 m3

1 bushel of paddy rice 22.5 kg paddy rice

1 square mile 2.59 km2

1 US$ 181 LKR

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page vi

ACRONYMS

€ Euro

AEO Agricultural Extension Officers

ASC Agricultural Service Centre

BOI Board of Investment

CARP Council for Agricultural Research Policy

CBC Ceylon Business Council

CBO Community Based Organisation

CFA Core functional analysis

CIF Cost Insurance Freight

CRIDF Climate Resilience

CSA Climate Smart Agriculture

CSEF Civil Society Environmental Fund

CSO Civil Society Organisation

DEA Department of Export Agriculture

DoA Department of Agriculture

EC European Commission

EDB Export Development Board

EDF/BUDGET European Development Fund

EEP Economic Empowerment of Poorest

EU European Union

EUD European Delegation

FAO Food and Agriculture Organisation

FDI Foreign Direct Investment

FIRST Food and Nutrition Security Impact, Resilience, Sustainability and Transformation

FOB Free on Board

GAMP Good Agricultural Manufacturing Practices

GAP Good Agricultural Practices

GDP Gross Domestic Product

GMPs Good Manufacturing Practices

GoSL Government of Sri Lanka

GSP General System of Prefernces

Ha Hectare (100,000 m2)

HRARTI Hector Kobbekaduwa Agrarian Research and Training Institute

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page vii

HRM Human Resource Management

ICRISAT International Crops for Research in Semi Arid Tropics

ICT Information Communication Technology

IFPRI International Food Policy Research Institute

ILRAD International Livestock Research Institute

IPARD Institute for Participatory Agricultural Research Inst

ITMIS Information Technology Management Information System

JICA Japanese International Cooperation Agency

JPAs Job Performance Aids

KE Key Expert

KPI Key Performance Indicator

M&E Monitoring & Evaluation

MEDA Microenterprise Development Association

MEDC More Economically Developed Countries

MOA Ministry of Agriculture

MOF Ministry of Finance and Mass Media

MONPEA Ministry of National Policies and Economic Affairs

MoPI Ministry of Primary Industries

MTEF Medium Term Expenditure Framework

NAO National Authorising Officer

NAP National Agriculture Policy

NAP New Agriculture Policy

NCFRU National Committee on Floriculture Research & Development

NGO Non-Government Organisation

NKE Non Key Expert

NLDB National Livestock Development Board

NPF National Program for Floriculture Sector

NRM Natural Resource Management

NSS National Statistics Service

OECD Overseas Economic Council for Development

OFCs Other field crops

PAF Performance Assessment Framework

PEP Performance Enhancement Programme

PET Public Expenditure Tracking

PFM Public Finance Management

PIP Public Investment Programme

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page viii

PMU Project Management Units

PPP Public Private Partnerships

PSC Project Steering Committee

R&D Research & Development

RDD Rubber Research Department

RMS Resource Management System

RWASH Rural Water Sanitation and Hygiene

SACCOs Savings And Credit Cooperative Organisations

SRC Sector Reform Contract

SDDP Support to District Development Programme

SL Sri Lanka

SLBDC Sri Lanka Business Development Centre

SLCARP Sri Lanka Council for Agricultural Research Policy

SMART Specific, Measurable, Accurate, Realistic, Timebound

SWOT Strengths, Weaknesses, Opportunities, Threats

T&V Training and Visit

TAT Technical Assistance Team

TACIS Technical Assistance to the Commonwealth of Independent States

TAIEX Technical Assistance and Information Exchange of the EU

TAMAP Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TNA Training Needs Analysis

ToRs Terms of Reference

TOT Training of Trainers

TRI Tea Research Institute

VCA4D Value Chain Analysis for Development

WB World Bank

WTO World Trade Organisation

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 9

1 E X E C U T I V E S U M M A R Y

Introduction and context

This value chain study on floriculture in Sri Lanka is part of a series of value chain studies carried out by the Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka (TAMAP) team in order to assist the GoSL and the EUD SL in developing an overarching agriculture policy and implementation strategy aiming on increasing the productivity and efficiency of the agriculture sector among others by programming specific interventions.

Though the importance of the agriculture sector has decreased over the last years in Sri Lanka, there are still opportunities for diversified and commercially oriented farming. To fully understand the development potential of the floriculture sector TAMAP commissioned a value chain analysis study. The methodology applied in this study follows to a large extent the EU facilitated value chain analysis for development (VCA4D), apart from conducting a detailed economic effects analysis.

For this study, information of secondary sources as well as interviews with stakeholders was used. Interviews were conducted with stakeholders (exporters, traders and farmers) in Western and North Western Province and Central Province.

Floriculture sector in Sri Lanka

Sri Lanka’s floriculture sector is a small niche sector with estimated 4,450 metric tons exports, about 500 to 550 metric tons local production and 249 metric tons import in 2017. The focus is on flowering and non-flowering live plants, foliage and cut flowers from tropical and temperate zone flora. Sri Lanka is only a small participant in the floriculture world market. TAMAP estimates the production value of the Sri Lankan commercial floriculture sector in 2017 at 18 to 20 million US $ or LKR 2,800 to 3,100 million. The contribution of the commercial

floriculture sector to the country’s Agriculture GDP was about 0.5%1. The main period of growth of the Sri Lanka floriculture production was before 2010. Since 2010, the total production is rather stable with only recently some growth. The 2012 decline in floriculture sector production was mainly caused by a sharp drop in production of foliage due to decreasing export prices in 2011.

About 46% of the local production volume is flowering and non-flowering live plants, 48% is foliage and the remainder cut flowers. 80 to 90 percent of the Sri Lankan production of live plants and 99 percent of the production of foliage is for export purpose. The annual production of 4,690 metric tons on 472 hectares is 8 to 9 metric tons per hectare or nearly 1 kg per sqm. The productivity is quite high compared to international average. The production of foliage and live plants is dominated by large scale commercial growers some with foreign partners.

The production of cut flowers for exports has totally collapsed over the past decade and currently the export is about 130 to 140 tons. The production of cut flowers for the local market has increased to 150 to 200 metric tons annually presently on 350 to 450 hectares. The productivity per hectare has declined considerably and is now about 0.8 metric tons per hectare. This is about 80,000 cut flower stems per hectare which is extremely low compared to international averages.

1 Agriculture GDP according to Central Bank of Sri Lanka

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 10

Governance and entities supporting the sector

The National Policy Framework 2010 aimed at establishing 1,500 floriculture villages and 30,000 floriculture jobs in sub-urban and rural areas. The Department of National Botanic Gardens and the Ministry of Primary Industries received funds for implementing the strategy. The National Committee on Floriculture Research and Development (NCFRD) identified priorities for the floriculture sector for the period 2017 to 2021.

The Department of Agriculture is collaborating with the private sector to establish a floriculture park to increase exports of floriculture products. The regulations under the Plant Protection Act No 35 of 1999, are implemented by the Department with among others the National Plant Quarantine Service providing extension services for pest & disease control.

The Department of National Botanical Gardens in Peradeniya has been the main promoter for the development of the floriculture sector in Sri Lanka. The Department manages 16 gardens and 4 war graves as well as 2 education and training centers. The Department organized women groups for floriculture production in many districts of the country. The Ministry of Sustainable Development and Wildlife also administers the Fauna and Flora Protection Ordinance No2 of 1937 with most recent amendments in 2009. The Ordinance provides the legal framework for the plant quarantine regulations and the procedures for import and export of plant materials.

Up to the end of 2018, the Ministry of Primary Industries was quite active in promotion of the floriculture sector. The Department of Export Agriculture was the driving force behind these initiatives. The Board of Investment and the Export Development Board provide support to registered exporters. Through the One Window Portal established by the Ministry of Finance, the trading community is provided with access to online systems developed for Regulatory Agencies involved in Import & Exports.

Problems encountered in the floriculture sector and coping mechanisms

Sri Lanka is a high cost producer because of high labour, high taxation and high freight costs. The national carrier Sri Lanka Airlines is more expensive for exporters than the other available airlines. Obtaining all certificates and permits for export is mentioned by all exporters as a major challenge and raising the cost of their business. Different governmental institutions are involved in the processing of an export order and the co-operation between these institutions is problematic.

The non-enactment of the Plant Breeder’s Rights protection and the outdated quarantine regulations for import of planting material are a major constraint for the floriculture sector. The Sri Lankan quarantine and inspection laws are complicated with many restrictions. Even if import is allowed it is costly and time consuming which is destructive for a sector that is highly market oriented and competitive. The Sri Lanka quarantine and inspection service should be more demand driven. Working closely together with established exporters is considered required to develop flexible, efficient and effective quarantine and inspection.

Recently, the EDB has simplified the exporters registration procedures and now trading companies have registered as exporters. These companies don’t have a farm and can easily under-bit established exporters. The established exporters with farms confirmed the loss of business for Sri Lanka while it resulted in harm to the image of Sri Lanka as a reliable supplier. The established exporters also observed that the EDB export promotion activities could be better targeted to the needs of floriculture exporters.

The export-oriented floriculture sector is weakly organised. The Flora Association exists but seems not actively promoting the interests of the sector. At the moment, most exporters are not co-operating and collaborating to advocate for better trade strategies and cost reduction.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 11

Most of the Sri Lankan floriculture tissue labs don’t manage to get enough orders and buyers and fair prices for the materials. Tissue material takes a long time to produce (1.5 years from start to sales is quite normal) and substantial economies of scale can be achieved if larger orders can be obtained.

The level of mechanization is low in most of the Sri Lankan floriculture sector but especially in cut flower production. A majority of farms use old polytunnels as investment in new equipment is very costly. In 2016, the import tax on equipment for the floriculture sector was raised with 25% making import of required equipment even more expensive.

Especially medium-size cut flower producers showed interest to expand their business but face the problem that access to land is restricted. Farmers have requested additional land from government but failed to obtain the land. In addition, leasing additional land from private owners is difficult.

Most cut flower farms lose control over their supply during transport as produce is transported by public train or bus to major local markets. The farmer has to send his product first and expects to be paid later. Many buyers, however, don’t pay in time and many farmers have large outstanding amounts with buyers. Sometimes, buyers go bankrupt before payment is completed and the farmers have to carry major loss.

Established registered cut flower farms face fierce competition from unregistered smallholders. Smallholders purchase cuttings from importers and start multiplication. Smallholders can buy plants, produced with imported material and use those as mother plants for production of cuttings and their commercial plants. They don’t have the costs of imports and the royalties and can produce the plants at a much lower cost.

The TAMAP team observed the following strategies of businesses participating in the floriculture sector to cope with the indicated issues:

• Exporters turn to the local market to compensate for lost export market share. This switch is only possible for exporters who focus on live plants as there is virtually now local market for foliage.

• The most successful Sri Lankan exporters moved away from the Netherlands as their only or dominant buyer and developed markets in the Middle East and Asia. Importers in these countries are more loyal and accept longer delivery periods of the orders which is beneficial for relatively small producers like Sri Lanka.

• Some companies decided to switch new markets segments (which have less traditional limitations from rules and regulations) such as aquatic plants, multiplication for export purposes and tissue culture production.

• Many established exporters and larger local market producers have invested in building the relationship with a number of dedicated out-growers. This strategy also ensures flexibility in terms of costs of production.

• Most established exporters are constantly evaluating the possibilities to mechanise labour-intensive operations such as automatic dosing of the nutrients and chemicals in the drip lines, mechanising production of growing medium, transport of plants over the farm and semi-automation of the preparation of the plants for export.

• Some cut flower farms are attempting to establish reliable license agreements with foreign suppliers of planting materials. To serve the local market with better quality product but (in case scale economies can be achieved) additionally it may also open up export opportunities.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 12

Market for live plants, foliage and cut flowers

Sri Lanka live plants and foliage are produced for the export market while Sri Lanka cut flowers are produced for the local market. The export market for Sri Lankan floriculture produce is estimated at 4,450 metric tons annually and the local Sri Lankan floriculture market at 804 metric tons of which about 30% import. The demand on the local market is generated by special shops (about 30% of the demand) and road side flower and gardening shops (about 70% of the demand). The special shops are in the main cities while the road side flower and gardening shops can be found all over the country.

Sri Lanka is with its floriculture exports of about 16 million US $ in 2017 only a minor player in the world market. Of all the three floriculture market segments relevant for Sri Lanka, globally the segment of live plants is the largest market while foliage is the smallest market. Sri Lanka exports hold a tiny share of all major live plant markets but especially the share on the large Germany is one of the main markets and should provide opportunities for growth. Compared to the Sri Lankan share of the Japanese and Netherlands market, the share of the German market is very small. Sri Lanka holds a virtually neglectable share of the international cut flower market. The Netherlands is Sri Lanka’s single most important foliage export market but as a region, the Middle East countries are more important for Sri Lanka foliage exports than European countries or Japan.

Competition, competitors and outlook

Sri Lanka’s imports of floriculture products are quite stable in volume but sharply increasing in value. The imports are dominantly live plants with increasingly higher unit import values. These are mainly orchids supplied by Thailand. On the local market these imports compete with locally produced orchids but not with cut flowers.

For live plants, China and Kenya are the main competitors. China is the main Sri Lankan competitor on the Japanese market and Kenya on the Netherlands market. Compared to China, Sri Lankan CIF unit import prices for the live plants on the Japanese and Netherland market are very high. Sri Lankan CIF unit import prices are higher than the world average but Kenyan CIF unit import prices for live plants on the Netherlands market are much higher.

For foliage, India, Costa Rica and China are the main competitors for Sri Lanka. China is the main competitor on the Japanese market. Costa Rica is the main competitor on the Netherlands market. India is the main competitor on the Middle East markets of Saudi Arabia and the UAE. Compared to China, Sri Lankan CIF unit import prices for its foliage on the Japanese market are high. Also, on the Netherlands market, Sri Lankan CIF unit import price are higher than the world average and the main competitor Costa Rica. On the S. Arabia and UAE market, Sri Lanka has considerably higher CIF unit import prices than its main competitor India.

For cut flowers, the main international market is The Netherlands. Sri Lanka cut flower exports are higher priced than the Kenyan ones and also more expensive than the overall average imports.

Sri Lankan floriculture products are high priced on the international market and Sri Lanka is a high cost country in the global floriculture sector. A comparison between the average FOB export price and the average CIF import price for major markets showed that the high price of Sri Lankan products is mainly related to the high costs of insurance and freight. Pricewise, Sri Lanka is not competitive in major live plants markets and Sri Lankan products are extremely expensive on the US market. For foliage Sri Lanka is pricewise somewhat competitive on the Saudi Arabian market and the Japanese market but not in Europe and the UAE.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 13

However, it should be noted that prices are only one aspect of the floriculture trade. Kenya has the highest import prices for its live plants but also a relatively high share of The Netherlands imports of live plants. Also, Sri Lanka has high import prices for its foliage but also a high share of the imports in S Arabia and the UAE. The assortment of different products in this business is large and qualities exported vary.

Over the last decennium, the value of Sri Lankan foliage exports seems to gradually increase but the value of Sri Lankan live plants exports is basically stable. The growth trend in Sri Lankan exports for live plants is erratic and for foliage extremely erratic. Sri Lankan foliage exports seem to be a high-risk business. The outlook of exports over the coming 5 years is difficult to predict but we estimate that Sri Lanka will import about 250 metric tons of live plants annually and exports around 1,950 metric tons annually. In the coming years, the value of exports is expected to be between 6,2 and 6.5 million US $ annually. For foliage exports, we estimate exports to figure around 2,500 to 2,700 metric tons annually with a value between 10 and 12 million US $ annually. For cut flowers, the total size of the market is about 280 to 350 metric tons in 2017 of which 150 to 210 metric tons for local market, 130 to 140 metric tons for exports and some small imports. The market is expected to grow with 30 to 50 metric tons per year in the coming period.

Margin and gross margin analysis

Gerbera and Chrysanthemum cut flower production provides for a relatively high contribution margin for farmers of about 27 to 31%. The collector gets a margin of about 7 to 11% and the florist about 22%. Rose and lilies provide a lower contribution margin for farmers of about 19% while the collector gets about 14% for roses and 22% for lilies. Florist gets a relatively high margin on roses of about 60% and 42% on lilies. Cost of production and transport are much higher in live plant and foliage production. For example, in Queen Palm the farmer gets a margin of about 3%, the collector about 4% and the exporter 30% while in foliage the farmer gets a margin of about 5%, the collector not more than 2% and the exporter about 27%. It should be considered that the production of live plants and foliage is less risky for the producer than the production of cut flowers (higher risk of crop failure and higher perishability of the crop) and consequently cut flower farmers require a higher margin to maintain their business than farmers of live plants and foliage.

Gross margin for Gerbera and Chrysanthemum were calculated at about US $ 1,900 to 2,200 per year for a 1,000 ft2 polytunnel. A 1,000 ft2 polytunnel of roses will provide a gross margin of about US $ 4,300 annually and lilies about US $ 5,500. Live plants and foliage have considerably lower gross margins. The gross margin of a 1,000 ft2 area of queen palm was calculated at about US $ 1,700 annually and foliage about US $ 1,400.

Social Analysis

The floriculture sector employs an estimated amount of 20,000 people directly on the farms and a similar amount of people indirectly in logistics and sales. Almost 80 percent of the directly employed workforce in the floriculture sector are women. The workers of larger export companies are on a permanent carder. They are being paid all the employee benefits including overtime pay and holidays. On the farm and in processing areas, workers wear proper working gear. Small and medium scale farmers are using family labour for their operations. They hire labour when needed on a daily rate basis.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 14

Environmental Analysis and impact of climate change

Flowers and plants require abundance of water. The business has to rely on water from rivers or from dug wells. Dug wells are less effective and deep tube wells are needed to get water especially during the dry season. In some areas this decreased the availability of water for nearby houses and villages. This is more prominent in places where small and medium scale growers have set up their farms. Larger farms have enough land to mitigate the impact of deep tube wells on other lands. The floriculture sector consumes large amounts of chemicals for pest and disease control and weeding. The use of chemicals is especially high in the cut flower industry. The incremental utilisation of chemicals in cut flower production increases the likelihood of pollution of water and soil resources. Water pollution in the hill country areas may result in substantial pollution and depletion of resources in the downstream areas.

The impact of climate change is already evident in Sri Lanka floriculture sector. Prolonged droughts have serious consequences for the floriculture industry. Large scale floriculture exporters in the West and North West province rely mainly on rivers. Drought can dry off rivers, dug wells and agro-wells. Heavy rainfalls and changes in night and day temperatures will impact mainly the floriculture sector in the Central province of Sri Lanka. Farmers already experienced lower flower yields during the rainy seasons. Changes in the night and day temperatures in the Central province caused smaller flowers and lesser yields per plant. In addition, heavy and prolonged rainfalls resulted in higher prevalence of pests and diseases.

Opportunities, outlook and recommendations

Sri Lanka has excellent growing conditions for both tropical and temperate zone floriculture products. It has experience in growing floriculture products for local and export markets. Export markets are substantial and growing. Also, local demand for floriculture products in the major towns and cities is growing. In floriculture, the value added per sqm is high compared to other horticulture produce and the area under floriculture is still limited with huge opportunities to expand. The quality of the produce in special shops and garden markets in Sri Lanka has considerably improved over the last decade. With better connection and logistics to markets and more promotion and marketing, the sales on the local market can be further fostered. Out-grower schemes provide a good opportunity for smallholder farmers to participate in wider markets and may increase the flexibility of operations of exporters and larger farmers. The system is operational in the Sri Lanka floriculture sector, but its scale and effectivity could be substantially increased. Various companies have started investment and production of new products and are creating a new export market for Sri Lanka. The rate of return of these products (multiplication, aquatic plants and tissue culture) is high compared to traditional floriculture products provided scale economies can be achieved. The exporting companies are studying methods to mechanise logistics, handling and packaging and production. Due to the extremely low level of mechanisation in virtually the whole sector, the potential gains in efficiency from semi-mechanisation are high. With the appropriate incentives for foreign investors, improvement of the inspection and quarantine laws including the adoption of the Plant Breeder’s Rights Law by Sri Lanka, the country has the potential to be a highly attractive location for direct foreign investment in floriculture. The latter would not only benefit foreign investors but also local businesses. The floriculture sector needs the flexibility to follow trends in markets, fashion and designing. Constant adjustment of the supply in terms of colours and varieties and cultivars of flowers and plants is essential for survival. This is to the extreme applicable for the cut flower and foliage market segment and to a somewhat lesser extend for the live plants. The outlook for the Sri

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 15

Lanka floriculture sector depends on innovation in the laws and institutions governing the sector.

The study team proposes the following key recommendations for the development of the floriculture sector:

• Improve the import rules and regulations for planting materials and agro inputs and Enact the Plant Breeders Rights Act;

• Improve export promotion to access new markets and products;

• Establish recognized training;

• Promote use of more efficient technologies and best management practices;

• Make suitable underutilized public land available for floriculture production;

• Promote the further horizontal and vertical integration of the floriculture sector.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 16

2 I N T R O D U C T I O N A N D C O N T E X T

2 . 1 I n t r o d u c t i o n t o t h e p r o j e c t

The Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka (TAMAP) service contract, implemented by a consortium led by ECORYS, started with the mobilisation of the Technical Assistance Team (TAT) on 8 th January 2018. The project will have an operational phase of 36 months and will end on 7 th January 2021.

The objective of the service contract is to contribute to a more productive, sustainable, diversified, climate-resilient, market-oriented and inclusive agriculture in Sri Lanka. The following four (4) results have to be accomplished within this service contract. They are:

Result 1: An overall (overarching) Agricultural Policy in line with the Government Development Goals is developed.

Result 2: An enabling environment is created and relevant policies for the modernisation and diversification of agricultural production, as well as the promotion of agricultural exports, are implemented.

Result 3: Existing systems and practices used by central and provincial agricultural ministries for planning, budgeting and policy implementation are improved.

Result 4: The statistical and analysis systems to monitor and assess the impact of implementing the overall agricultural policy are improved.

The threads running through these five critical elements are the coordination, facilitation, training, mentoring and mainstreaming of cross-cutting issues such as climate change, gender, youth and smart nutrition.

One of the main activities of the TAMAP is to develop in close consultation with the stakeholders an Overarching Agriculture Policy (OAP) and based on that an Implementation Strategy specifying detailed action plans and costs for all relevant subsectors with the main objective to make the entire agriculture sector more productive, effective and efficient. Several assignments are being carried out to support the development of the overarching policy and its implementation strategy as well as to assist the EUD Sri Lanka in the programming of future interventions. As such 8 value chain studies on commodities with future potential for development and a cold chain pre-feasibility study are and will be carried out to assess and recommend future interventions in the agriculture sector.

2 . 2 C h a l l e n g e s o f t h e a g r i c u l t u r e s e c t o r i n S r i

L a n k a a n d i t s r e o r i e n t a t i o n

Agriculture has been an important driver of poverty reduction through income and employment

generation in Sri Lanka. Although Sri Lanka has a history of exporting agricultural products a

large part of the agricultural population remained highly traditional with archaic relations to

markets and commercial networks. Also, the share of GDP generated by agriculture sector

decreased as other sectors gained more prominence. With the departure of labour force from

the rural areas to urban areas and other economic activities it becomes increasingly urgent to

modernize the farming sector.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 17

Promoting farming as a business has the potential to uplift rural areas further and increase the

contribution of agriculture to the national economy. Improved connectivity to potential demand

and markets, investment in agriculture to increase labour productivity and diversify production,

reduction of wasteful use of resources and adding value to agricultural processes via

processing and improved handling are all components of the modernization process.

Over the last decades it has become increasingly clear that farming for a market cannot be

promoted by stimulating the supply side only. Modern commercial farming is part of a total

system which gets its information from the demand side of the economy and leads this to the

supply side where it sets the rules and regulations for participation of the farmers. This system

operates in a regulatory environment set by policies and strategies of local and international

governments and is supported by financial and non-financial services. Over the last decades

in more and more countries (and also in Sri Lanka) systems are evolving in which all

stakeholders co-operate closely together to generate the highest possible value in the chain.

Such chains are identified as value chains.

This report provides an analysis of the floriculture value chain in Sri Lanka, using to some

extent the evidence-based, largely quantitative, toolkit developed/ compiled by the Directorate-

General for International Cooperation and Development (DG DEVCO) within the project “Value

Chain Analysis for Development” (VCA4D).

This diagnosis of the floriculture value chain is intended to support the European Commission

and the Government of Sri Lanka in structuring their policy dialogue around the strategic issues

related to this sector. This to assist in developing a resilient, competitive, commercially viable

and environmentally sustainable floriculture sector in Sri Lanka. The goal is to increase the

value added in the chain and secure social inclusion of smallholders.

This study was conducted over a period of four weeks, from 1 October to 1 November 2019

by 2 agriculture economists from the TAMAP project.

2 . 3 V a l u e c h a i n a n d V C A 4 D m e t h o d o l o g y

2 . 3 . 1 W h a t a r e v a l u e c h a i n s ?

Value Chains are interactive systems with products, money and information flowing through

them, all reliant on relationships. The success of a value chain depends on effective flow and

use of information along the entire chain from the market via traders and retailers and

processors to farmers and agro-input suppliers. The flow depends on trust and commitment

between trading partners. The success of the chain depends on understanding market

opportunities and the whole chain rather than looking at its own part of the chain in isolation.

In a successful value chain, each stakeholder knows the whole chain and understands benefits

from chain-wide interdependence in the flow of products and money. Every stakeholder in the

chain cooperates and works together to supply the same market opportunity and avoid

competing only on price. The value created in the chain increases through gains in efficiency

and quality. Relations between stakeholders in a chain are stable and strong. Conducting such

a collaborative action to avoid price competition and focus on efficiency gains and produce

quality only makes commercial sense in case market information shows that reference

products in local and export markets generate considerable higher value than the standard

products of the supply chain of a sub-sector. This is exclusively the case for demand/markets

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 18

catering for the middle- and high-income groups (tourist hotels and restaurants, supermarkets

and specialty shops) and export production. These markets are the target for value chain

development approaches.

A large amount of knowledge and methodologies have been developed related to value chain

development since Michael Porter introduced the concept in his book Competitive Advantage

in 1985.

2 . 3 . 2 V C A 4 D m e t h o d o l o g y

The VCA4D project is part of the European Union’s “Inclusive and Sustainable Value Chains

and Food Fortification” Programme.

The VCA4D methodology aims to provide evidence, supported by a list of indicators measured

quantitatively or based on expert assessments that together provide an answer to four framing

questions:

1. What is the contribution of the VC to economic growth?

2. Is this economic growth inclusive?

3. Is the VC socially sustainable?

4. Is the VC environmentally sustainable?

The analytical process has four components:

Functional analysis: provides a general mapping and description of the main actors,

activities, and operations in the chain, an overview of the products and product flows, the major

production systems, a description of the main governance mechanisms in the chain, and a

short description of (known) constraints. The functional analysis forms the basis for the

analyses in the other three components. The analysis is mainly based on secondary data, and

key informant interviews with both value chain actors and key experts.

Economic analysis: Firstly, consists of a financial analysis of each actor type (financial

accounts, return on investment), as well as an assessment of the consolidated value chain

(total value of production, global operating accounts). Secondly, it assesses the economic

performance (contribution to economic growth in terms of direct and indirect value added

generated, and the sustainability/viability for the national economy (domestic cost ratio, Policy

analysis matrix Data is derived from secondary data, key informant interviews, and structured

questionnaires.2

The social analysis explores whether the value chain is socially sustainable. It also

contributes to discussion on whether potential economic growth in the value chain can be

socially inclusive. The social analysis draws on multiple information sources, including

secondary data and field data from floriculture producers at different scales, farmers, traders,

exporters etc., and other government and non-government stakeholders.

2 The economic analysis in the VCA4D methodology applies to a large extent the economic effects analysis which is a tool often used in financial and economic analysis. Given the limited time available for the floriculture value chain study, an economic effects analysis was not conducted.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 19

The environmental analysis evaluates the environmental sustainability of the value chain.

2 . 4 D a t a c o l l e c t i o n

2 . 4 . 1 S e c o n d a r y d a t a

The study team obtained relatively latest information from projects and GoSL sources (reports

and statistics) and from trade related websites such as IndexMundi or UNcomtrade.

2 . 4 . 2 P r i m a r y d a t a

Primary data was collected through key informant interviews and focus group discussions with farmers (small, medium and large), traders, exporters in the main production areas of Gampaha, Negombo as well as Colombo town and Nuwara Eliya. The study team is aware that the data collected maybe considered sensitive and given the prevailing challenges the sector is facing with limited growth and increasing competition, many of the stakeholders are reluctant to expose information which could generate competitive advantages of potential competitors.

2 . 4 . 3 W h y F l o r i c u l t u r e w a s s e l e c t e d f o r t h e s t u d y

In the course of this report more details on the justification why floriculture was selected for a detailed value chain assessment. However, in order to understand the report, a brief summary is presented on the justification.

Floriculture is the subsector of horticulture concerned with the cultivation of flowering and ornamental plants for gardens and for floristry. The development of new varieties via plant breeding is also a major occupation of floriculturists. As such it is a farming activity as plants are grown for commercial purposes by farming communities

Sri Lanka has excellent growing conditions for tropical plants in the central and western part of the country with plenty of water. Sri Lanka has an enormous botanical diversity and is home of a wide range of floricultural species. Plants and flowers have always played an important role in Sri Lanka culture and have a long tradition as being used for religious purposes.

The Global Floriculture sector is one of the major agribusiness sectors and one of the vast

growing larger markets in the world3. Floriculture provides income and rural employment to small, medium-scale and large farmers and foreign currency earnings to countries participating in the business. Given the large potential Sri Lanka has to further develop the floriculture sector, this sector has been selected for the value chain analysis.

3 Global Floriculture Market Analysis 2019, Syngene Research, January 2019

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 20

2 . 5 S e c t o r O v e r v i e w i n S r i L a n k a

Sri Lanka’s floriculture industry can be divided into two subsectors i.e. live plants and foliage and cut flower production. Sri Lanka’s floriculture sector is small with estimated 4,450 metric tons exports. The local market is about 500 to 550 metric tons local production and 249 metric tons import in 2017. The focus is on flowering and non-flowering live plants, foliage and cut flowers from tropical and temperate zone flora.

The larger scale commercial farming and exports in the subsector are of much more recent date. Sri Lanka started only in the ninety seventies with commercial growing and exports of floriculture products. Even presently, Sri Lanka has only a tiny share of the floriculture world market with the total global production value estimated at 55 billion US $ with an export value

of 19 billion US $ in 2017. Sri Lankan exports are valued at 16 million US $4. We estimate the production value of the Sri Lankan commercial floriculture sector in 2017 at 18 to 20 million US $ or LKR 2800 to 3100 million

2 . 5 . 1 L i v e P l a n t s a n d f o l i a g e

This floriculture sub-sector produces stems and cuttings as well as complete plants for indoors and outdoors use and attractive leaves and plant parts to add colour and shape to flower arrangements. Sri Lanka focus is on products such as Queen Palm, Croton, Chinese grass, Scindapsus, Syngonium, Cordyline, Dracaena, Orchids and Anthurium.

Different parts of Sri Lanka can produce specific types of live plants and foliage. In the wet and colder areas temperate zone plants can be farmed such as Cyprus, Begonia, Caladium, Roses, Caladium and Maranta. In the dry and hot areas Hibiscus, Cacti, Palms, Euphorbia, Jatropha, Jasmine, Bougainvillea, Cycads and Ixora can be produced whereas in tropical humid wet areas Dieffenbachia, Calathea, Dracaena, Anthurium, Scindapsus and Philodendron grow extremely well. So, Sri Lanka has the natural growing conditions suitable for the production of a large variety of marketable live plants and foliage.

The Sri Lanka commercial production of live plants is over 80% for exports while foliage is over 95% for the export market. The estimated area under foliage and live plants is 472 hectares

with an annual volume of about 4690 metric tons5. About 20 companies control the production and exports. These companies started as export companies. Some used foreign investment and BOI support to establish and develop the business. All are using shading net greenhouses and drip and sprinkler irrigation systems. Some of these companies produce plants in collaboration with foreign partners to increase access to planting materials, technology and markets. More recently, part of the main exporters started deliveries to local market as well but still we estimate that about 80 to 90 percent of the Sri Lankan exporting companies’ production of live plants and 99 percent of foliage is for export purpose. Consequently, the data on export volume in the two product categories provide a good estimation of the dynamics in the production of these products in Sri Lanka. It can be concluded that the major development in the total production was in the period before 2010. From 2010 the total production is rather stable with only recently improving slightly. The major recent dip in production was in 2012 which was especially caused by dynamics in the foliage sub-sector (see Figure 1).

4 C Ryswick World Floriculture Map 2016

5 Dhanasekera, Cutflower production in Sri Lanka, In Cutflower production in Asia, FAO Bangkok, 1998

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 21

Figure 1 Comparison of exports of live plants and foliage

Source: Own calculations based on UNComtrade

The 2012 drop in production of foliage came after a sharp drop in the export prices in 2011. As figure 2 shows, in the year 2011 Sri Lanka got the lowest ever average export price for its foliage. This will have discouraged the production of foliage in the subsequent year which had on its turn a positive impact on the export prices in 2012 due to reduced supply.

Figure 2 Dynamics in Sri Lanka export prices of live plants and foliage

Source: Own calculations based on UNComtrade

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 22

2 . 5 . 2 C u t f l o w e r p r o d u c t i o n

Sri Lankan cut flower production comprises of temperate zone flowers and tropical flowers. Temperate zone flowers include carnation, rose, statice, gypsophyla, alstroemeria, chrysanthemum, lilies and irises. Tropical zone flowers include anthurium, orchids, strelitzia, heliconia, lotus. Most temperate zone flowers are grown in polytunnels and open field and anthurium and orchids are grown under shade nets and mist and drip irrigation systems. More recently gerbera cut flower production has become more popular due to the availability of a wide range of good cultivars.

The export of cut flowers is about 130 to 140 tons. Large producers take care of the exports while medium and small-scale producers are focussing on the local market. All the producers are using poly tunnels or nets but most equipment is old. The small-scale producers use manual water provision, the medium scale producers use drip and sprinklers. Over the last decade, the cut flower production for export has totally collapsed (see figure 3). The FOB unit export prices for Sri Lankan cut flowers have sharply come down to a level that it is largely uneconomically to export.

Figure 3 Sri Lanka export of cut flowers

Source: Own calculations based on UNComtrade

However, this doesn’t mean that the Sri Lankan production of cut flowers has collapsed. The area that was previously used for export production of carnation and other flowers is now used for production of cut flowers for the local market. The production of cut flowers for the local

market has increased to 150 to 200 metric tons annually presently on 350 to 450 hectares6.

2 . 5 . 3 M a j o r s p e c i e s i n S r i L a n k a n f l o r i c u l t u r e p r o d u c t i o n

In the market segment of live plants and foliage, the main species produced by Sri Lanka are Cane Palm, Fishtail Palm, Queen Palm, Lady Fingers Palm, Croton, Chinese grass, Scindapsus, Syngonium, Cordyline, Dracaena and Anthurium.

6 A Jaees, An Overview of Upcountry Cut flower Industry Sri Lanka, Colombo 2018

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 23

Cane Palm (Dypsis lutescens) also known as areca palm, yellow palm or butterfly palm is a flowering plant in the family Arecaceae, native to Philippines, Madagascar and South India but now naturalized in many tropical countries for commercial production

Fishtail Palm (Caryeta) is a flowering plant in the family Arecaceae native to Asia, northern Australia and South Pacific but has become an invasive introduced species in Florida and other subtropical and tropical climates.

Queen Palm (Syagrus romanzoffiana) also known as cocos palm is native to South America and introduced throughout the world as a popular ornamental tree.

Lady Fingers Palm (Rhapis Excelsa) is also family of the Arecaceae and native to Southern China and Taiwan. Its striking appearance is popular and works well in floor standing pots

Croton is a flowering plant in the family of Euphorbiaceae. The plant is since long time naturalized in many countries but is native from Indonesia, Malaysia, Australia and Western Pacific.

Chinese Grass (Miscanthus sinensis) also known as silver grass is a flowering plant in the family of Poaceae and native to Eastern Asia

Scindapsus belongs also to the family of Araceae and is native to South East Asia. New Guinea and Australia and Western Pacific. The plants are primarily root climbing vines

Syngonium belongs also to the family of Araceae and is native of tropical rainforest of Southern Mexico, West Indies, Central and South America. The leaves change shape according to the plant’s stage of growth.

Cordyline comprises of about 15 species in the family of Asparagaceae. The plant is native to Western Pacific, New Zealand and Eastern Australia, South East Asia and Polynesia with one species found in South America

Dracaena comprises of about 120 species of trees and succulent shrubs in the family of Asparagaceae. The majority of the species are native to Africa with a few in South Asia and Northern Australia with two species in tropical Central America. The plant is one of the most popular live plants and foliage plants worldwide.

Anthurium comprises of about 1000 species of flowering plants of the family Araceae and native of Northern Mexico, Northern Agentina and the Caribbean. It is most naturalised tropical plants in the world with a long history of use for religious and ornamental purposes. The plant is very popular both for its flowers as well as its foliage.

In the market segment of cut flowers the main species produced in Sri Lankan are carnation, rose, statice, gypsophyla, alstroemeria, chrysanthemum, lilies and iris, anthurium, orchids, gerbera, strelitzia, heliconia and lotus.

Carnation (Dianthus caryophyllus) is a species of the family of Dianthus, native to the Mediterranean and used for extensive cultivation for the last 2000 years

Rose is a woody perennial flowering plant in the family of Rosacecae. There are over 300 species and thousands of cultivars. Most species are native to Asia with smaller numbers native to Europe, North America and North West Africa.

Statice (Limonium) is a genus of 120 flowering plants species belonging to the family of Plumbaginaceae. The plant is native from the Eastern Mediterranean.

Gypsophyla is a flowering plant in the family of Caryophyllaceae and native to Europe and Asia, Africa, Australia and the Pacific. Turkey has the most species i.e. 35 endemic species.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 24

Alstroemeria also known as Peruvian lily is a flowering plant in the family of Alstroemeriaceae and a native of South America and naturalized in USA, Mexico, Australia, New Zealand and other countries.

Chrysanthemum are flowering plants in the family of Asteraceae. They are native to Asia and North East Europe. Most species originate from East Asia with the center of diversity in China. Countless varieties and cultivars exist

Lilies (lilium) is a genus of flowering plants growing from bulbs. Lilies are native to the temperate northern hemisphere though their range extends into the northern subtropics.

Iris is a genus of up to 300 species of flowering plants with showy flowers

Anthurium (see under live plants and foliage)

Orchids belong to the family of Orchidaceae with flowering plants with blooms that are colourful and fragrant. There are about 28000 currently accepted species. Orchids are native to all tropical rainforest regions in the world. Commercially Phalaenopsis and Cattleya are the most cultivated Orchids both have a huge number of hybrids and cultivars

Gerbera is member of the Asteraceae family and native of the tropical regions of Africa, Asia and Latin America. Thousands of cultivars exist varying in shape, size and colours. It’s commercially the fifth most important cut flower in the world after rose, carnation, chrysanthemum and tulip.

Stelitzia is a genus of five species of perennial plants native to South Africa and belongs to the family of Strelitziaceae.

Heliconia belongs to the family of Heliconiaceae with about 194 known species. The plant is native to tropical Americas. In many tropical countries species are cultivated as ornaments and few species are also naturalized in Asia and Africa.

Lotus (Nelumbo nucifera) is a aquatic plant in the family Nelumbonaceae. The plants are native to Northern India, Northern Indochina and East Asia. The plant is widely naturalised in Southern India, Sri Lanka, South East Asia, New Guinea, Australia. It has a history of cultivation of over 3000 years.

Table 1 provides an overview of dominant types of utilisation of floriculture products from Sri Lanka.

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 25

Table 1 Utilisation of Sri Lankan floriculture sector products

Key product category Varieties

Decorative Foliage Draceana sanderiana,Draceana massengeana, Cordyline, Aglaonema, Adiantum, Calathea, Maranta, Codiaeum, Monstera, Pothos, Pandanus, Thaloide, , Philodendron, Miscanthus, Anthuriums, Diffenbachia, Scindapsus, Caryota urens, Chrysalidocarpus, Differnbachia, ,Aspidistra

Rooted/ Un rooted young Plants &

indoor pot plants

Draceana sanderina, Draceana massengeana, Codiaeum, Agloanema,Scindapsus ,Draceana marginata , Cordyline, Pleomele reflexa, Polyscias, Livistonia

Cut Flowers Roses , Carnations , Gerbera, Chrysanthemum,Lilies,

Gypsophila, Limonium, Anthurium,

Landscaping plants Plumeria, Gardenia, Codiaeum, Ixora, Hibiscus, Cassia, Bouhinia, Bougainvella, Allamanda, Jasmine,Acalypha, Neem,

Tissue cultured plants Ananas, Musa sp, Cordyline, Dracaena, Syngonium

Philodendron, Ficus

Aquarium plants Anubious, Cryptocoryne, Ceratophyllum, Echinodorus etc.

Source: http://www.srilankabusiness.com/floriculture/floriculture-products-ebrochures.html

2 . 5 . 4 E x p o r t s a n d i m p o r t s o f f l o r i c u l t u r e p r o d u c t s f r o m a n d t o S r i L a n k a

Figure 4 presents an overview of imports and exports of floriculture products to and from Sri Lanka. It is clear that the Sri Lanka trade balance in floriculture is strongly positive. Exports both in terms of quantity and value are much higher than imports. The imports are growing but very slowly and reach 1 million US $ for the first time in 2017. The exports are more or less stable in value terms over the last decade and also the export unit values remained stable at about US $ 3.2 to 3.6 per kg over the last 5 years with the exception of 2015. In 2017, the export had a value of 15.9 million US $.

Figure 4 Imports and exports of floriculture products to and from Sri Lanka in 1000 US $ and metric tons

Source:UNComtrade

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 26

Figure 5 shows the trend in exports and it is clear that in terms of value the most successful export product is foliage. The value of exports of foliage is gradually increasing with only a major dip in 2012. Exports of live plants are more or less stable in value since 2010 and the exports of cut flowers shows a steadily declining trend. In 2017 the value of cut flowers exports from Sri Lanka was merely US $150,000. The decreasing export value of cut flowers is partly caused by the issues related to the importation of planting material cut flower producers (see par 3.3.2. Also, the good local market for cut flowers played a major role with producers turning away from exports.

Figure 5 Export value of floriculture products from Sri Lanka in US$ thousands

Source: UNComtrade

2 . 5 . 5 P r o d u c t i o n & e x p o r t s o f f o l i a g e a n d l i v e p l a n t s a n d c u t f l o w e r s

2.5.5.1 Foliage and live plants

Foliage and live plants production started as an industry in the 1970s in Western, North Western and Central Provinces. The annual production of 4690 metric tons on 472 hectares is 8 to 9 metric tons per hectare or nearly 1 kg per sqm. The productivity is quite high compared

to international average7. The production of foliage and live plants is dominated by large scale commercial growers some with foreign partners. About 4 to 5 exporters have about 20 or more hectares, the others have 2 to 10 hectares. The largest companies employ 4 to 5 workers per hectare, the smaller ones 6 to 8 workers per hectare. These companies mainly produce flowering and non-flowering live plants both rooted and unrooted, foliage as well as small amounts of bulbs, corms and tubers. The sub-sector also produces aquatic plants for exports and 5 companies operate commercial tissue culture labs.

7 Y.Xia, X Deng, P Zhou a.o.. The World Floriculture Industry. Dynamics of Production and Markets, Harbin 2006

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 27

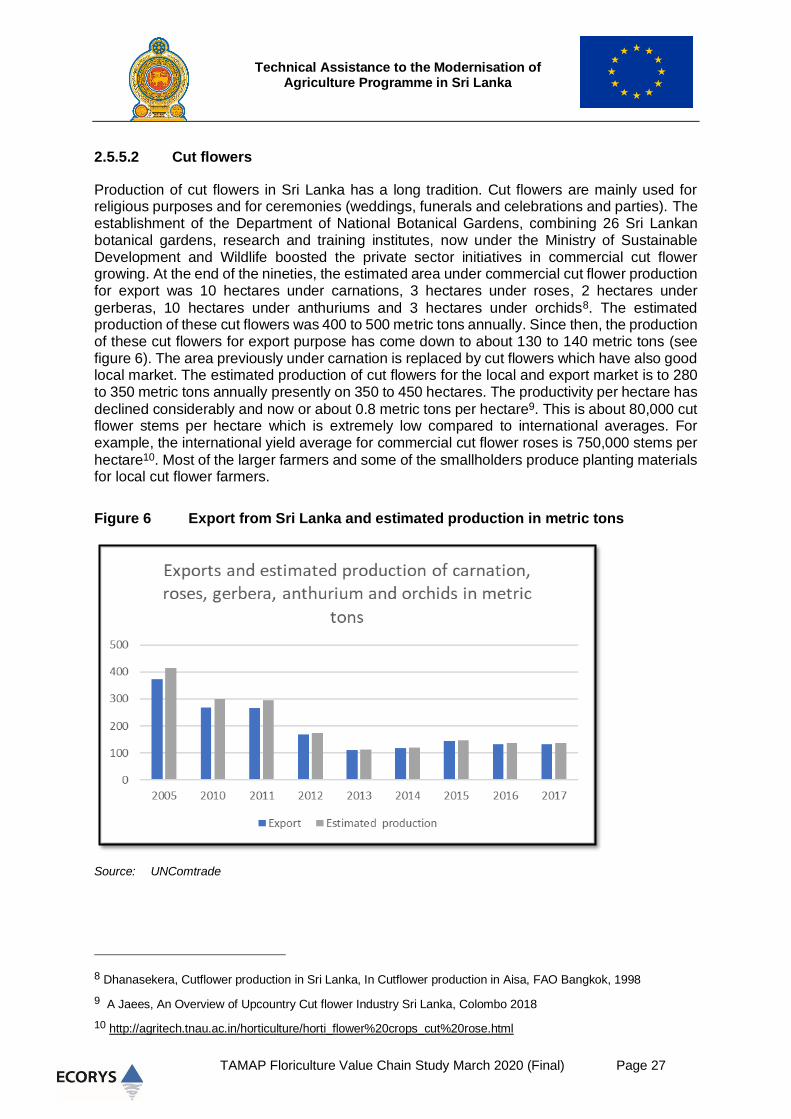

2.5.5.2 Cut flowers

Production of cut flowers in Sri Lanka has a long tradition. Cut flowers are mainly used for religious purposes and for ceremonies (weddings, funerals and celebrations and parties). The establishment of the Department of National Botanical Gardens, combining 26 Sri Lankan botanical gardens, research and training institutes, now under the Ministry of Sustainable Development and Wildlife boosted the private sector initiatives in commercial cut flower growing. At the end of the nineties, the estimated area under commercial cut flower production for export was 10 hectares under carnations, 3 hectares under roses, 2 hectares under

gerberas, 10 hectares under anthuriums and 3 hectares under orchids8. The estimated production of these cut flowers was 400 to 500 metric tons annually. Since then, the production of these cut flowers for export purpose has come down to about 130 to 140 metric tons (see figure 6). The area previously under carnation is replaced by cut flowers which have also good local market. The estimated production of cut flowers for the local and export market is to 280 to 350 metric tons annually presently on 350 to 450 hectares. The productivity per hectare has

declined considerably and now or about 0.8 metric tons per hectare9. This is about 80,000 cut flower stems per hectare which is extremely low compared to international averages. For example, the international yield average for commercial cut flower roses is 750,000 stems per

hectare10. Most of the larger farmers and some of the smallholders produce planting materials for local cut flower farmers.

Figure 6 Export from Sri Lanka and estimated production in metric tons

Source: UNComtrade

8 Dhanasekera, Cutflower production in Sri Lanka, In Cutflower production in Aisa, FAO Bangkok, 1998

9 A Jaees, An Overview of Upcountry Cut flower Industry Sri Lanka, Colombo 2018

10 http://agritech.tnau.ac.in/horticulture/horti_flower%20crops_cut%20rose.html

Technical Assistance to the Modernisation of Agriculture Programme in Sri Lanka

TAMAP Floriculture Value Chain Study March 2020 (Final) Page 28

2 . 6 G o v e r n a n c e a n d I n s t i t u t i o n a l f r a m e w o r k

2 . 6 . 1 F l o r i c u l t u r e p o l i c i e s a n d s t r a t e g i e s

The Sri Lankan government considers the floriculture sector a development priority. The National Policy Framework 2010 aimed at establishing 1,500 floriculture villages and 30,000 jobs in sub-urban and rural areas related to floriculture business. The primary institutions that received funds under the NPF for implementing the strategy were the Department of National Botanic Gardens and the Ministry of Primary Industries. The National Committee on Floriculture Research and Development (NCFRD) identified four priorities for the floriculture

sector for the period 2017 to 202111. The identified priorities for the floriculture sector are:

• Development of Marketable Novel Products;

• Mechanisation of Production Process for better Productivity;

• Marketing and Networking Research to Identify Emerging Markets;

• Smart Plant Nutrient Packages, Growing Media and Plant Protection;

For each of the priorities, NCFRD identified the current challenges, possible solutions, issues to be addressed when implanting the solutions and developed an implementation strategy to adequately introduce the prioritised innovations.

For Development of Marketable Novel Products novel varieties are needed. The advised strategy is to develop clear cut procedures for importing and exporting planting materials and to develop a national market-oriented breeding program.

For Mechanisation of Production Process for better Productivity locally manufactured machines for the floriculture industry are needed. The advised strategy is making people aware of new tools and methods and appropriate irrigation techniques and introduce new equipment and techniques and support research on poly tunnels and crop protection systems.