eu rice economic fact s - european commission 2015 european commission directorate-general for...

TRANSCRIPT

March 2015

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR AGRICULTURE AND RURAL DEVELOPMENT Directorate C. Single CMO, economics and analysis of agricultural markets C.4. Arable crops

EU RICE ECONOMIC FACT SHEET

1. INTERNATIONAL MARKETS ................................................................................ 2

1.1 Production ............................................................................................................. 2

1.2 International Trade ................................................................................................ 3

1.3 Consumption ......................................................................................................... 5

1.4 World rice balance sheet ....................................................................................... 7

1.5 International market prices .................................................................................... 6

2. EU MARKET .............................................................................................................. 8

2.1 Production ............................................................................................................. 8

2.2 External Trade ..................................................................................................... 11

2.3 Consumption ....................................................................................................... 13

2. 4 EU Rice Balance sheet ....................................................................................... 14

2.5 EU market prices ................................................................................................. 14

2

1. INTERNATIONAL MARKETS

1.1 Production

Global rice production in 2014/15 has little changed from the previous year's record.

FAO forecast for global paddy production in 2014 stands at 745 million tonnes of paddy

(for a total area of 163 million ha), only 0.2% below the 2013 record estimate for 746

million tonnes of paddy.

These FAO estimates for paddy production are consistent with International Grain

Council (IGC) estimate of a global production of 474 mio tonnes (milled equivalent) in

2014/15 compared to 475 mio tonnes in 2013/14 – see graphic below.

Evolution and projection of world rice production

Source: International Grain Council

Rice production is very concentrated geographically: Asia produces more than 90% of

the total world rice production, with a production of approx. 675 million tonnes of paddy

in Asia (out of a global production of 745 million tonnes of paddy).

China and India are by far the two biggest rice producers with a production of 205 mio

tonnes and 155 mio tonnes of paddy respectively, i.e. almost 50% of the world rice

production.

Other major paddy rice producers in Asia are Indonesia (70 mio tonnes), Bangladesh (50

mio tonnes), Vietnam (45 mio tonnes) and Thailand (38 mio tonnes). Brazil with a

production of 12 mio tonnes of paddy is the biggest non-Asian producer, followed by the

USA with a production of 10 mio tonnes of paddy per year.

With a production of less than 3 mio tonnes of paddy per year (less than 2 mio tonnes in

milled equivalent), the EU-28 represents approx. 0.4% of global rice production.

3

Main rice producers

Source: FAO December 2014

1.2 International Trade

Historically, a small amount of rice is traded globally compared with other commodities

like wheat, maize or soyabeans. Despite a continuous growth, the international trade in

rice corresponds approx. to only 8% of the total rice production.

In 2014 international trade in rice surpassed the record 40 million tonne mark (milled

equivalent) corresponding to 8.4% of the global rice production of 475 million tonnes

(milled equivalent). A further small expansion is expected in 2015.

Rice is a strategic commodity for many rice producing countries. Most countries try to

reach self-sufficiency in rice due to its strategic importance in domestic food security. It

is also essential for local authorities and state agencies to control rice trade flows in order

to stabilise their domestic rice market.

Rice exports are very concentrated geographically. The top five rice exporters (Thailand,

India, Vietnam, USA, Pakistan) account for 80% of global rice exports. The share of EU

rice exports (approx. 200 000 tonnes milled eq) is minimal at global level (approx. 0.5%

of global rice exports).

Unlike the high concentration in export market, the rice imports are more evenly spread

between the continents: not only Asia but also Africa and the Middle East region

represent a significant part of the global rice imports. The top 5 importers (China,

Nigeria, Philippines, Iran and Iraq) account for approx. 30% of global rice imports. The

share of EU rice imports (approx. 1 mio tonnes milled eq.) is also minimal at global level

(approx. 2.5% of global rice imports).

4

Major rice exporters

Source: FAO December 2014

Major rice importers

Source: FAO December 2014

5

1.3 Consumption

In 2014/15 global rice consumption is projected at a record 500.5 million tonnes (milled

basis) and to outpace production for the first time in a decade. Global rice consumption is

projected to further increase in the coming years.

About 83% of rice utilization (415 million tonnes milled basis) would correspond to food

uses, while feed uses would represent 3% and other uses (seed, industrial, waste) would

represent 14%.

China (30 %) and India (21%) are the world biggest rice consumers, being responsible

for more than half of the total world rice consumption. Other significant consumers are

Indonesia (9 %), Bangladesh (8 %), Vietnam (4 %) and the Philippines (3 %). The EU-28

ranks 20th with a stable share of 0.6%.

Main rice consumers (million tonnes, milled basis)

Country 2013/14 est. 2012/13

China 146.30 144.00

India 99.18 94.03

Indonesia 38.50 38.13

Vietnam 22.00 21.90

Philippines 12.85 12.85

Thailand 10.88 10.60

Myanmar 10.50 10.40 Source: USDA Dec. 2014

The global rice production-consumption balance is very fragile due to the minor

difference between the annual output and demand. Since global rice consumption is

predicted to surpass production in 2014/15, global rice stocks are expected to decrease

but despite the decline, world reserves remain high, with a stock-to-use ratio estimated at

34.8% in 2014/15.

Projection of world rice consumption vs. production vs. stocks (milled basis)

Source: IGC Nov. 2014

6

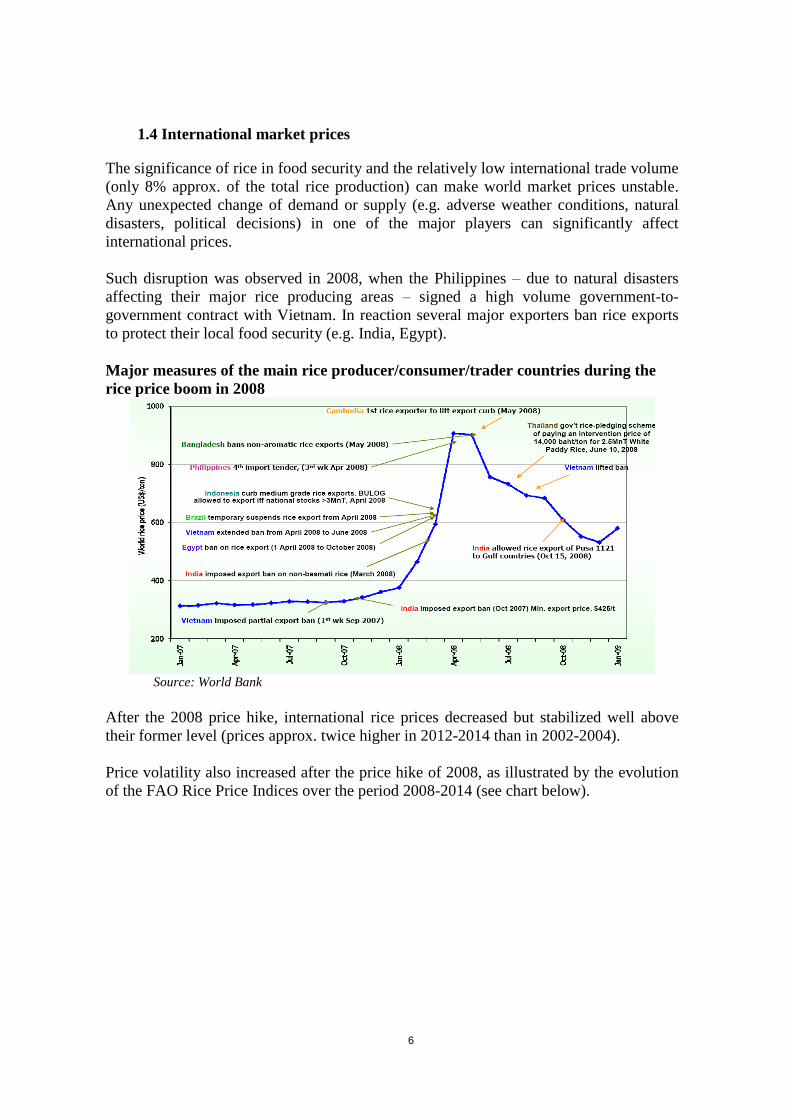

1.4 International market prices

The significance of rice in food security and the relatively low international trade volume

(only 8% approx. of the total rice production) can make world market prices unstable.

Any unexpected change of demand or supply (e.g. adverse weather conditions, natural

disasters, political decisions) in one of the major players can significantly affect

international prices.

Such disruption was observed in 2008, when the Philippines – due to natural disasters

affecting their major rice producing areas – signed a high volume government-to-

government contract with Vietnam. In reaction several major exporters ban rice exports

to protect their local food security (e.g. India, Egypt).

Major measures of the main rice producer/consumer/trader countries during the

rice price boom in 2008

Source: World Bank

After the 2008 price hike, international rice prices decreased but stabilized well above

their former level (prices approx. twice higher in 2012-2014 than in 2002-2004).

Price volatility also increased after the price hike of 2008, as illustrated by the evolution

of the FAO Rice Price Indices over the period 2008-2014 (see chart below).

7

Source: FAO Rice Market Monitor

1.5 World rice balance sheet

Years 2013/14 and 2014/15 have been characterised by:

- High level of rice production (coming close to 500 million tonnes milled basis)

- High level of rice consumption, with global rice consumption projected at a

record 500.5 million tonnes (milled basis) in 2014/15 and to outpace production

for the first time in a decade

- Record level of rice trade, above 40 million tonnes (milled basis)

Global Rice Supply and Demand Estimate

(million tonnes milled eq.)

2012/13 2013/14 2014/15

2014/15

Vs

2013/14

Production 490.5 497.5 496.6 -0.2%

Total Supply 690.7 712.5 718.6

Consumption 477.4 491.2 500.5 +1.9%

Food uses 401.9 409.6 415.4

Feed uses 13.3 14.1 14.5

Other uses 62.3 67.5 70.6

Trade 37.3 40.2 40.5

Ending Stocks 175.7 181.21 177.5 -2.1%

Source: FAO December 2014

This trend of high production, high consumption and high trade on the global rice

markets is expected to stay in the medium term, as illustrated with the five-year global

supply and demand projections issued by IGC end 2014 (see table below).

8

Source: IGC, December 2014

2. EU MARKET

2.1 Production

Over the last years the annual EU rice production has been approx. 1.8 million tonnes

(milled basis) over an area of approx. 450 000 ha (incl. approx. two-thirds of Japonica

rice and one-third of Indica rice).

More precisely in the 2013/14 marketing year the EU-28 produced 1.77 million tonnes

(milled basis) over 425 000 ha. For 2014/15, the forecast is 1.64 million tonnes (milled

basis) over 414 000 ha (due to a significant reduction of the Indica rice area and

production).

EU rice production ('000 t, milled equivalent)

Source: DG AGRI, based on communication from Member States

9

EU rice production is dominated by Japonica rice, which represents approx. 65-70% of

total EU rice production. Historically, Japonica rice has been the traditional rice in

Europe and part of the Mediterranean diet notably in Italy and Spain. Traditional foods

such as paella or risotto are made with Japonica varieties, whose characteristics (e.g.

ability to absorb the flavour of the spices or the sauce itself) make it much more suitable

for the preparation of these foods than Indica rice.

The relative scarcity of Japonica rice at global level (approx. 13% only of global rice

production is Japonica), the small volumes traded internationally and its higher price on

the world market also support predominance of EU japonica rice on the EU market, with

limited competition from imports.

EU rice production is located in 8 Member States. Italy and Spain together are

responsible for 80% of the total rice production (50% for Italy, 30% for Spain)

Share from the EU rice production (2014/15, milled basis)

10

The tables below show the recent evolution of Japonica and Indica areas in the Member

States (in ha).

Japonica area (ha) 2010/11 2011/12 2012/13 2013/14 2014/15

Italy

174 159 181 063

174 974

144 573

164 234

Spain

63 718 62 936

72 452

65 583

58 235

Portugal

22 903 22 905

24 936

25 000

16 243

Greece

10 520 10 835

8 584

9 690

15 433

France

16 000 18 481

18 805

14 500

13 743

Bulgaria

11 059 10 983

8 711

9 595

9 839

Romania

5 300 10 748

10 000

7 750

9 528

Hungary

2 500 2 500

2 463

3 000

2 191

EU

306 000 320 000

321 000

280 000

290 000

Indica area (ha)

2010/11 2011/12

2012/13

2013/14

2014/15

Italy

73 494 65 478

60 078

71 446

55 298

Spain

58 747 58 810

52 687

43 037

43 003

Portugal

5 027 6 745

6 500

6 174

12 425

Greece

23 200 21 743

21 832

17 690

10 573

France

2 800 3 000

3 175

3 500

1 207

Bulgaria

70 100

509

130

31

Romania

8 000 1 912

1 000

3 806

1 733

Hungary

0 0

0

0

0

EU

171 000 158 000

146 000

146 000

124 000

Source: DG AGRI/Member States

Rice yields are quite stable over time, with lower yields for Japonica than for Indica.

2010/11 2011/12 2012/13 2013/14 2014/15

Japonica

Area ( '000 ha) 306 320 321 280 290

Yield (t/ha) paddy 6.2 6.2 6.5 6.4 6.3

Indica

Area ( '000 ha) 171 158 146 146 124

Yield (t/ha) paddy 7.1 7.5 7.8 7.8 7.3 Source: DG AGRI/Member States

11

2.2 External Trade

The role of the external trade, in particular imports, is very significant in the EU, as

around one third of EU rice needs must be imported.

The EU imports every year approx. 1 million tonnes of rice (milled basis) and 300 000

tonnes of broken rice.

EU rice imports consist mainly of Indica rice. For Japonica, the EU is self-sufficient and

a small exportable surplus is produced (approx. 200 000 tonnes milled eq). Around 90%

of EU rice exports are made of Japonica rice. Italy is responsible for around 70% of the

total exports and Spain provides an additional 15 %.

Volumes and origin are influenced by the tariff preferences granted by the EU to various

EU rice producing countries. For instance:

- around 300 000 tonnes or 30% of total EU rice imports come as duty-free imports

from countries benefiting from the so-called EBA agreement like Cambodia and

Myanmar

- around 300 000 tonnes or 30% of total EU rice imports come as duty-free imports

of husked Basmati rice from India and Pakistan

The structure of rice imports has changed over the last years with an increase of imports

of milled rice (approx. 600 000 tonnes ie 60% of all rice imports) and a decrease of

imports of husked rice (non-Basmati).

12

EU Rice Imports

2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

paddy 988 934 337 650 1,191 1,189

husked 494,091 492,776 552,324 454,194 441,896 453,883

husked basmati 155,715 238,485 238,153 250,020 286,593 294,483

husked non-basmati 338,375 254,291 314,171 204,174 155,303 159,400

milled/semi-milled 353,312 411,072 426,904 418,141 494,068 604,171

Total (excl. broken) 848,391 904,781 979,565 872,984 937,154 1,059,243

broken 322,768 258,670 217,206 246,059 304,861 312,107

Grand Total (incl. broken) 1,171,159 1,163,451 1,196,771 1,119,042 1,242,015 1,371,350

Source: COMEXT

Imports of husked Basmati rice have been increasing thanks to the commercial

agreement with India and Pakistan which allow duty-free imports of husked Basmati rice

produced from 9 eligible varieties (see Regulation (EC) No 972/2006). Basmati imports

represent ~ 30 % of total EU rice imports (300 000 tonnes milled eq). In general, two-

thirds of Basmati imports are covered by India and one-third by Pakistan.

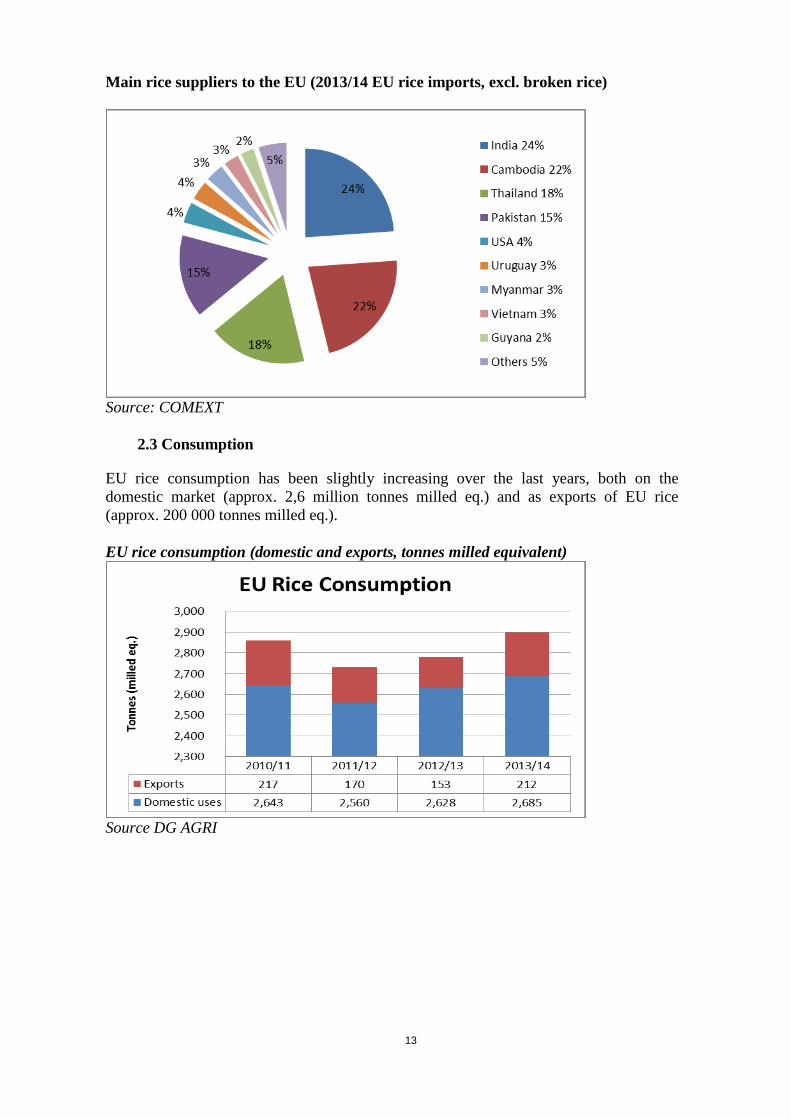

The origin of EU rice imports has also significantly changed over the last years. While

India and Thailand remain key suppliers, duty free imports originating from countries

benefiting from the Every But Arms (EBA) agreement, mainly Cambodia and Myanmar,

have been increasing, while imports originating from ACP countries such as Guyana and

Surinam have been decreasing.

Origin of EU Rice Imports (tonnes milled eq., excl. broken)

Country of Origin 2013/14

India 253 140

Cambodia 235 968

Thailand 189 560

Pakistan 159 970

United States 39 887

Uruguay 36 719

Myanmar 35 135

Vietnam 28 929

Guyana 25 847

Others 54 088

Total 1 059 243

13

Main rice suppliers to the EU (2013/14 EU rice imports, excl. broken rice)

Source: COMEXT

2.3 Consumption

EU rice consumption has been slightly increasing over the last years, both on the

domestic market (approx. 2,6 million tonnes milled eq.) and as exports of EU rice

(approx. 200 000 tonnes milled eq.).

EU rice consumption (domestic and exports, tonnes milled equivalent)

Source DG AGRI

14

2. 4 Balance sheet

The EU rice balance sheet is regularly updated and published at

http://ec.europa.eu/agriculture/cereals/balance-sheets/rice/overview_en.pdf

LAST UPDATED: 26/02/2015 '000 metric tonnes (in milled eqivalent)

Japonica IndicaTOTAL

RICEJaponica Indica

TOTAL

RICEJaponica Indica

TOTAL

RICEJaponica Indica

TOTAL

RICEJaponica Indica

TOTAL

RICE

Beginning stocks

Private 226 277 503 197 274 471 237 257 494 285 255 540 191 281 471

Intervention - - - - - - - - - - - - - - -

Total beginning stocks 226 277 503 197 274 471 237 257 494 285 255 540 191 281 471

Usable production 1,125 723 1,847 1,180 705 1,885 1,205 685 1,890 1,077 693 1,770 1,089 548 1,637

Area ('000 ha) 306 171 477 320 158 478 321 146 467 280 146 425 290 124 414

Agronomic yield (t/ha, on paddy basis) 6.2 7.1 6.5 6.2 7.5 6.6 6.5 7.8 6.9 6.4 7.8 6.9 6.3 7.3 6.6

Milling yield (%) 59% 60% 59% 59% 60% 59% 57% 61% 58% 60% 61% 61% 60% 61% 60%

Imports (from third countries) 69 911 980 76 793 869 81 856 937 92 967 1,059 90 1,050 1,140

TOTAL SUPPLY 1,420 1,910 3,330 1,452 1,772 3,224 1,523 1,798 3,321 1,454 1,915 3,369 1,370 1,878 3,249

Domestic uses

Human consumption / Industrial uses / Animal feed 1,008 1,584 2,592 1,031 1,472 2,503 1,069 1,503 2,573 1,046 1,583 2,629 973 1,579 2,553

Seed *** 32 19 51 36 21 57 36 19 55 34 22 56 37 19 56

Total domestic uses 1,039 1,604 2,643 1,067 1,493 2,560 1,106 1,522 2,628 1,079 1,605 2,685 1,010 1,598 2,609

Exports (to third countries) 183 33 217 148 22 170 133 21 153 183 29 212 220 30 250

TOTAL USE 1,223 1,637 2,860 1,215 1,515 2,730 1,238 1,542 2,781 1,263 1,635 2,897 1,230 1,628 2,859

Final stocks ****

Private 197 274 471 237 257 494 285 255 540 191 281 471 140 250 390

Intervention - - - - - - - - - - - - - - -

Total final stocks 197 274 471 237 257 494 285 255 540 191 281 471 140 250 390

Change in stocks -29 -3 -33 40 -17 23 48 -1 46 -94 25 -69 -51 -31 -81

Change in public stocks - - - - - - - - - - - - - - -

2010/11 2011/12 2012/13 2013/14** 2014/15 fc

2.5 EU market prices

EU prices for Indica paddy rice are lower (approx. 275 EUR/tonne on average since

2010) than for Japonica paddy rice (approx. 300 EUR/tonne on average since 2010). The

same applies for EU prices of milled rice which correspond approx. twice to the EU

prices of paddy rice (ie. approx. 550 - 600 EUR/tonne). Rice prices on the EU market are

higher than on the world market (approx. 550 EUR/tonne for EU milled rice (indica) vs

approx. 400 USD/tonne for Asia milled rice (indica))

Average paddy prices in key EU markets

Source: DG AGRI and Member States communications