ethanol rail transportation review - surface … rail transportation reviewethanol rail...

TRANSCRIPT

Ethanol Rail Transportation ReviewEthanol Rail Transportation Review

June 12, 2008

Paul Hammes – VP & GM Agricultural Products

STB Rail Energy Transportation Advisory Council

2

Ethanol Rail Transportation Review

• Ethanol Market Overview• Ethanol and DDGS Impact on Rail Network• Ethanol Supply Chain Components• Potential Ethanol Supply Chain Constraints• Managing Ethanol Rail Transportation

3

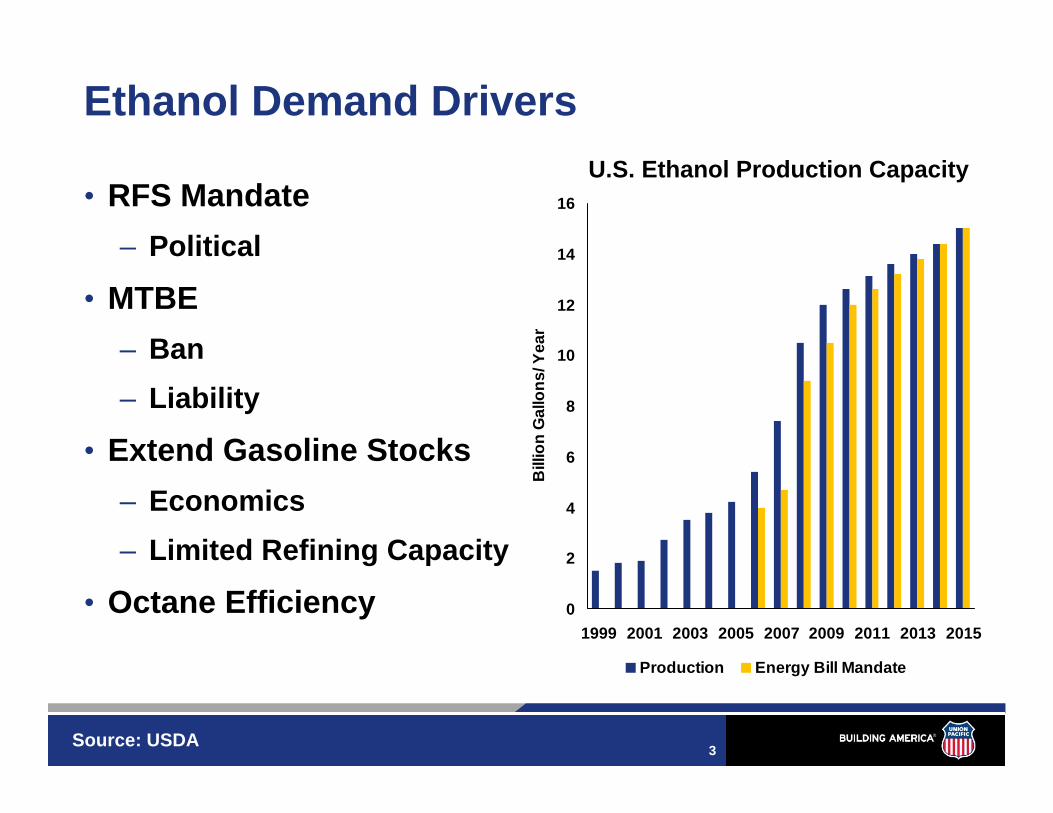

Ethanol Demand Drivers

• RFS Mandate – Political

• MTBE – Ban– Liability

• Extend Gasoline Stocks– Economics– Limited Refining Capacity

• Octane Efficiency 0

2

4

6

8

10

12

14

16

1999 2001 2003 2005 2007 2009 2011 2013 2015

Bill

ion

Gal

lons

/ Yea

r

Production Energy Bill Mandate

U.S. Ethanol Production Capacity

Source: USDA

4

Ethanol Production and Demand Markets

CA2%

IL/ IN/ OH

23%

Other19%

ND/ SD11%IA/ MN/

NE45%

CA2%

IL/ IN/ OH

23%

Other19%

ND/ SD11%IA/ MN/

NE45%

CA1%

IL/ IN/ OH

24%

ND/ SD10%

Other22%

IA/ MN/ NE

43%

CA1%

IL/ IN/ OH

24%

ND/ SD10%

Other22%

IA/ MN/ NE

43%

Other21%

CA13%

North East33%

South East24%

TX9%

Other21%

CA13%

North East33%

South East24%

TX9%

Production

Demand

2008 2015

South East17%

Other32%

North East22%

CA21%

TX8% South

East17%

Other32%

North East22%

CA21%

TX8%

Source: UPRR Estimate using various data sources

5

DDGS Production and Demand Markets

IL/ IN/ OH

14%

Other15%

CA/TX5%

ND/ SD20%

IA/ MN/ NE

46%

IL/ IN/ OH

14%

Other15%

CA/TX5%

ND/ SD20%

IA/ MN/ NE

46%

ND/ SD13%

IL/ IN/ OH

14%

CA/TX4%

Other23%

IA/ MN/ NE

46%

ND/ SD13%

IL/ IN/ OH

14%

CA/TX4%

Other23%

IA/ MN/ NE

46%

CA/ ID12%Other

26%TX/ KS/

OK25%

South West5%

Export10%

IA/ MN/ NE

22%

CA/ ID12%Other

26%TX/ KS/

OK25%

South West5%

Export10%

IA/ MN/ NE

22%

2008 2015

CA/ ID9%

South West4%

Export16%

IA/ MN/ NE

17%

TX/ KS/ OK

20%

Other34%

CA/ ID9%

South West4%

Export16%

IA/ MN/ NE

17%

TX/ KS/ OK

20%

Other34%

Source: UPRR Estimate using various data sources

Production

Demand

6

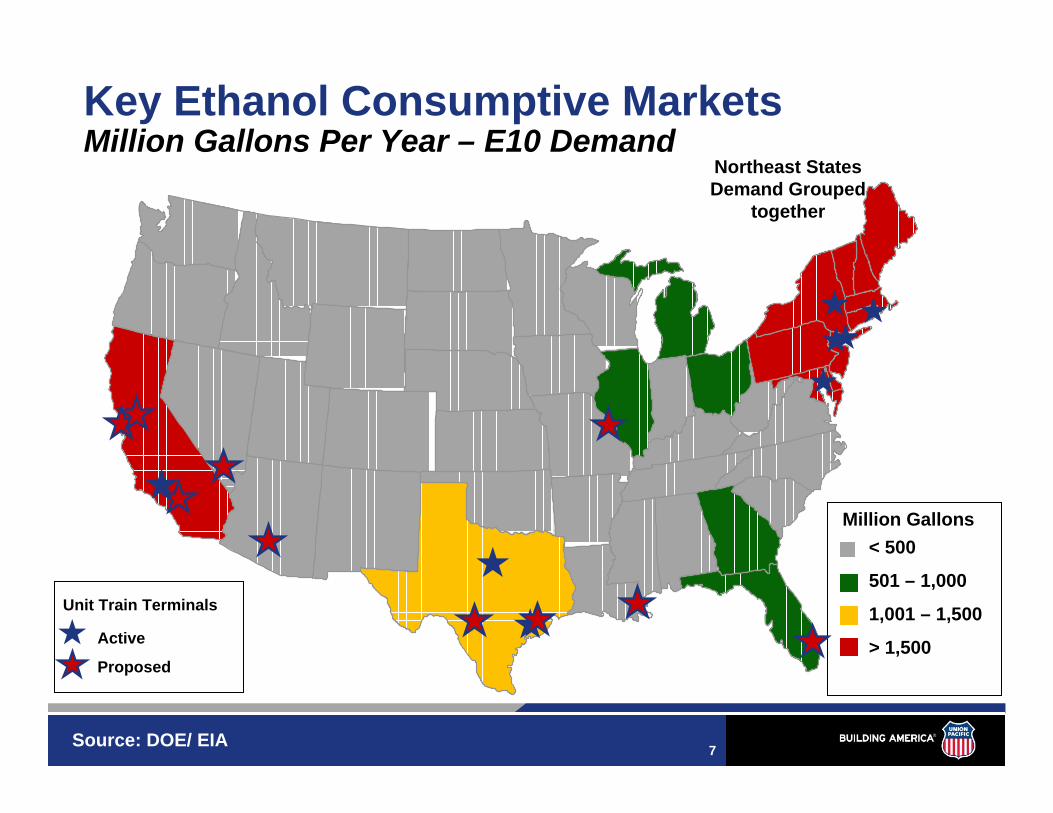

US Ethanol Biorefinery Locations

Source: Renewable Fuels Association

7Source: DOE/ EIA

Northeast States Demand Grouped

together

< 500

501 – 1,000

1,001 – 1,500

> 1,500

Million Gallons

Active

Proposed

Unit Train Terminals

Key Ethanol Consumptive MarketsMillion Gallons Per Year – E10 Demand

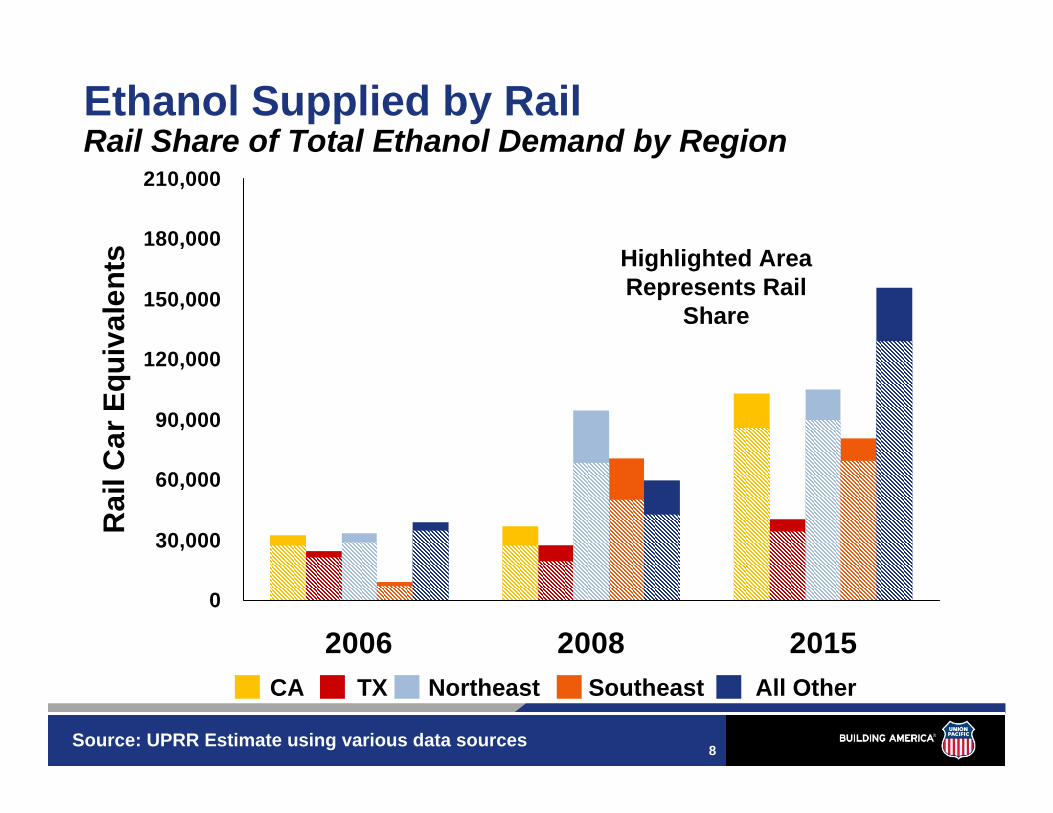

8

0

30,000

60,000

90,000

120,000

150,000

180,000

210,000

2006 2008 2015

Rai

l Car

Equ

ival

ents

Ethanol Supplied by RailRail Share of Total Ethanol Demand by Region

Highlighted Area Represents Rail

Share

Source: UPRR Estimate using various data sources

CA Northeast Southeast All OtherTX

0

30,000

60,000

90,000

120,000

150,000

180,000

210,000

2006 2008 2015

Rai

l Car

Equ

ival

ents

9

0

20,000

40,000

60,000

80,000

100,000

120,000

2006 2008 2015

Rai

l Car

Equ

ival

ents

DDGS Supplied by RailRail Share of Total DDGS Demand by Region

CA/ ID TX/ KS/ OK IA/ MN/ NE Southwest Export Other

0

20,000

40,000

60,000

80,000

100,000

120,000

2006 2008 2015

Rai

l Car

Equ

ival

ents

Source: UPRR Estimate using various data sources

Highlighted Area Represents Rail

Share

10

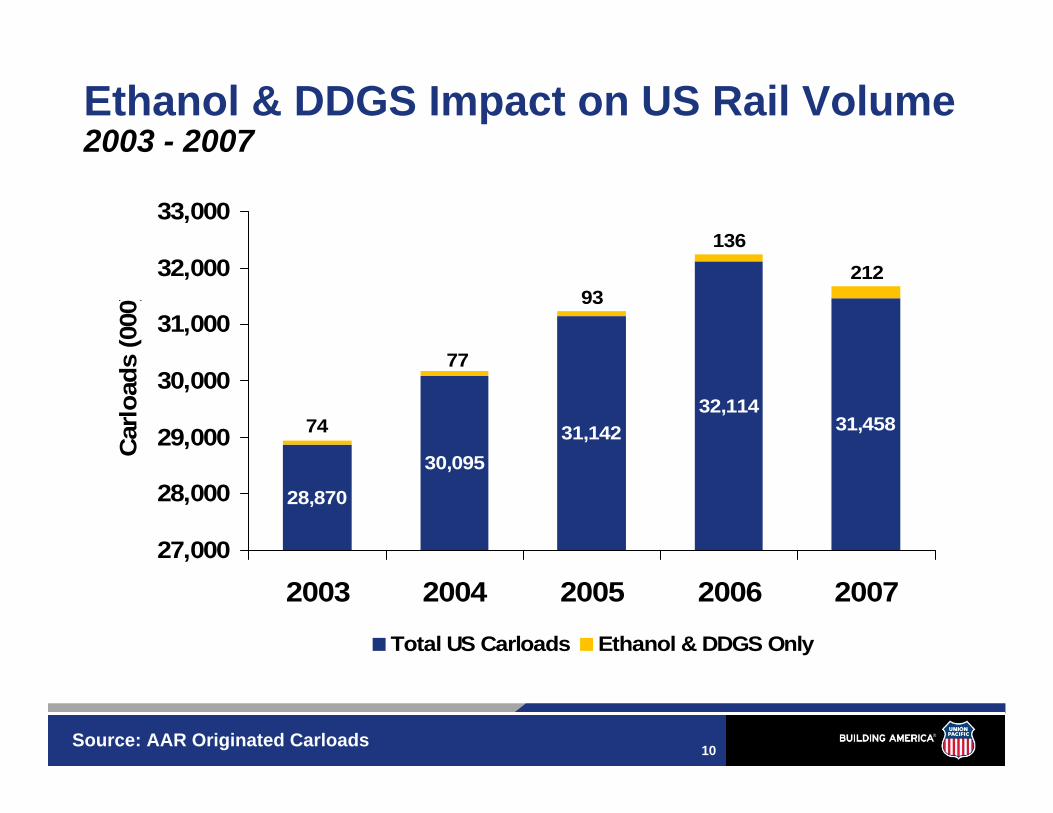

Ethanol & DDGS Impact on US Rail Volume2003 - 2007

28,870

30,09531,142

32,11431,458

212136

93

77

74

27,000

28,000

29,000

30,000

31,000

32,000

33,000

2003 2004 2005 2006 2007

Car

load

s (0

00)

Total US Carloads Ethanol & DDGS Only

Source: AAR Originated Carloads

11

Ethanol Supply Chain Components

• Production Plant– 55 MGY generates 5 cars each of ethanol and DDGS per day– Track infrastructure

• Tank Cars• Rail Network

– Manifest/Gathered-Combo/Unit– Terminal Yards/Line haul

• Unload Terminal– Unload System and Tank Storage

• Truck Rack

12

Potential Ethanol Supply Chain Constraints

• Rail Line Capacity• Rail Terminal/ Yard Capacity • Unit vs Manifest Shipments• Terminal Unload Capacity• Pipeline Management• Tank Cars• Storage Capacity

13

Future Corridor Volumes Compared to Current Corridor Capacity2035 Without Improvements

Source: National Rail Freight Infrastructure Capacity and Investment Study by Cambridge Systematics, Inc.

Note: Volumes are for the 85th percentile day

14

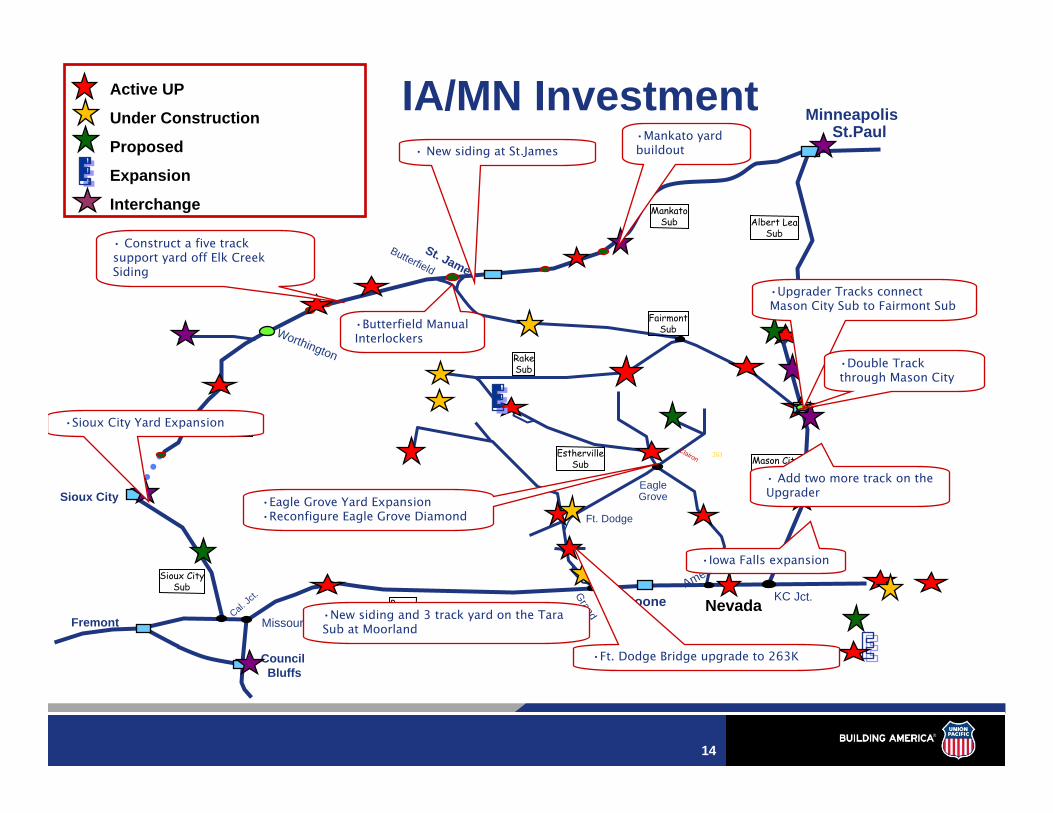

Sioux City

IA/MN Investment

Council Bluffs

Fremont

MinneapolisSt.Paul

Boone

Worthington

Butterfield

EagleGrove

Ames

Grand

Jct.

KC Jct.

Ft. Dodge

St. James

Clairon

Cal. Jc

t.

Missouri Valley

263

FairmontSub

EsthervilleSub

RakeSub

Mason City Sub

Albert LeaSub

BooneSub

WorthingtonSub

Sioux CitySub

Nevada

MankatoSub

Active UP

Under Construction

Proposed

Expansion

Interchange

• New siding at St.James•Mankato yard buildout

•Eagle Grove Yard Expansion•Reconfigure Eagle Grove Diamond

•Iowa Falls expansion

•New siding and 3 track yard on the Tara Sub at Moorland

• Construct a five track support yard off Elk Creek Siding

•Sioux City Yard Expansion

•Upgrader Tracks connect Mason City Sub to Fairmont Sub

•Ft. Dodge Bridge upgrade to 263K

• Add two more track on the Upgrader

•Butterfield Manual Interlockers

•Double Track through Mason City

15

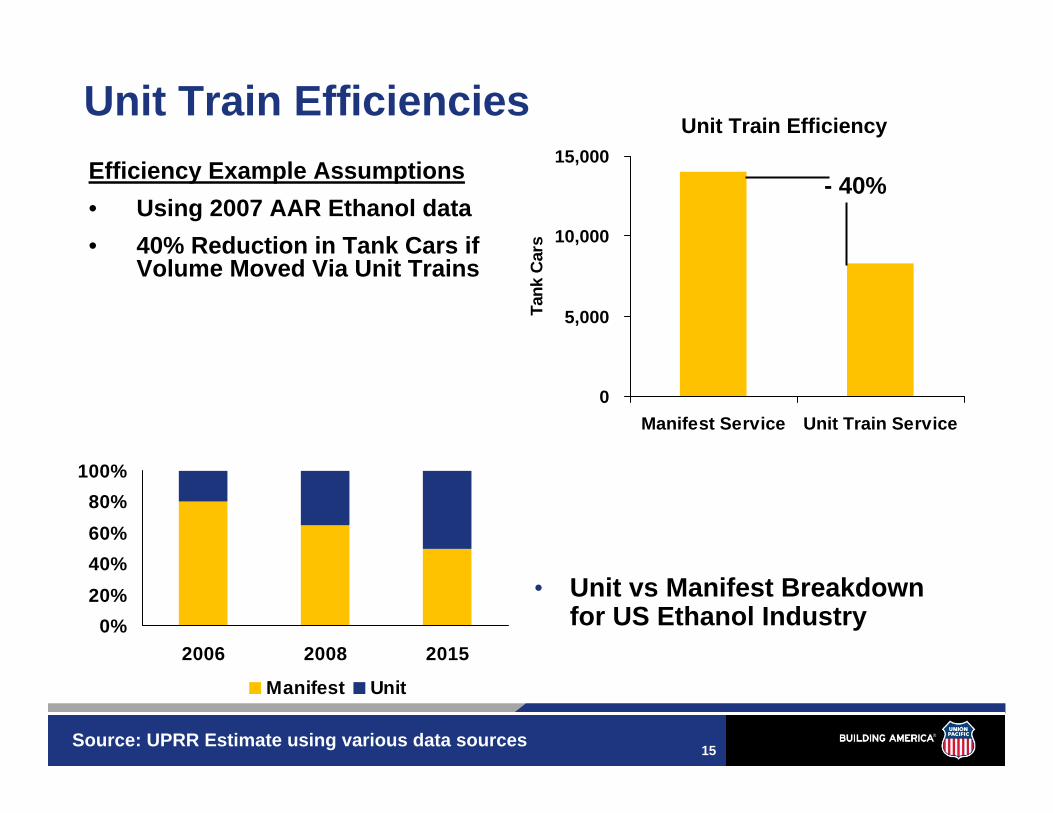

Unit Train Efficiencies

0

5,000

10,000

15,000

Manifest Service Unit Train Service

Tank

Car

s

Efficiency Example Assumptions• Using 2007 AAR Ethanol data• 40% Reduction in Tank Cars if

Volume Moved Via Unit Trains

• Unit vs Manifest Breakdown for US Ethanol Industry0%

20%40%60%80%

100%

2006 2008 2015

Manifest Unit

Unit Train Efficiency

- 40%

Source: UPRR Estimate using various data sources

16

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2006 2008 2010

Car

load

s

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2006 2008 2015

Car

load

sEstimated Unit Train Terminal CapacityMaximum vs Current or Forecasted

CA Northeast Southeast All OtherTX

Shaded Area Represents Current

and Expected Operating Capacity

Source: UPRR Estimate using various data sources

52% 60%

33%20%

50%

15%

31%

26%

60%

15%

25%

17

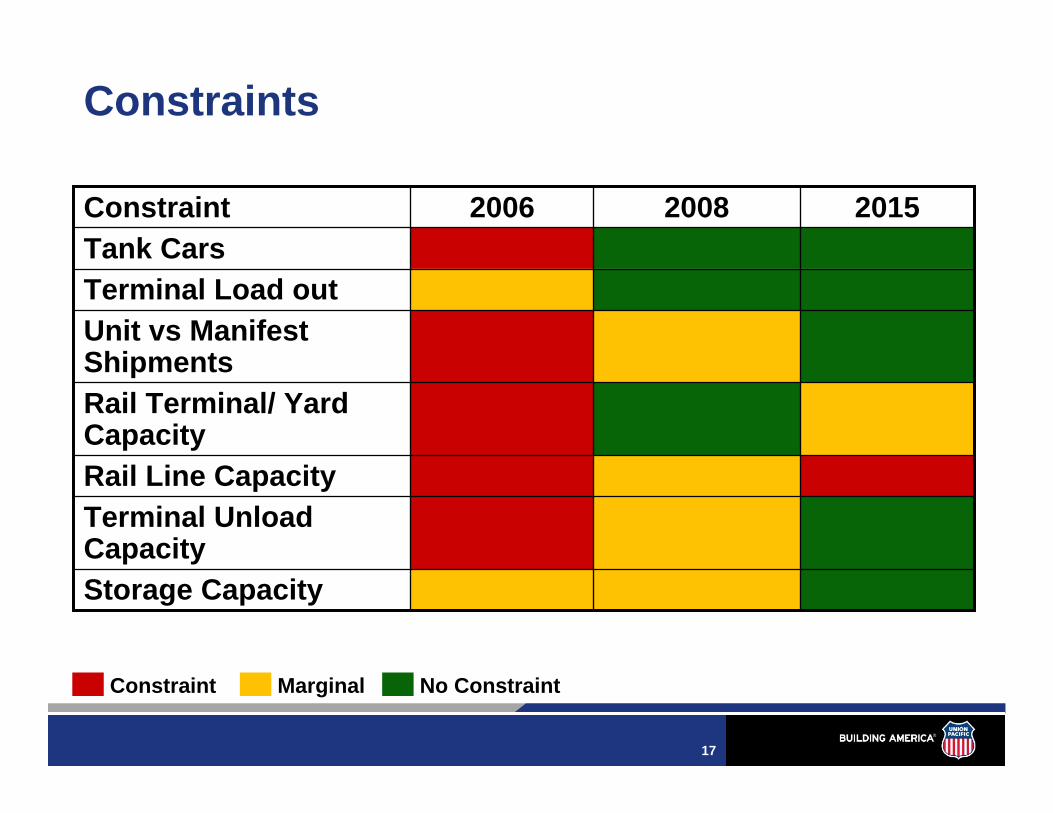

Constraints

Rail Line Capacity

Rail Terminal/ Yard Capacity

Tank CarsTerminal Load out

Storage Capacity

Terminal Unload Capacity

Unit vs Manifest Shipments

201520082006Constraint

Constraint Marginal No Constraint

18

Managing Ethanol Rail Transportation

• Resource and Capacity Planning• Pipeline Management• Tactical Management Tools

19

Resource and Capacity Planning

• Site Development Assistance• Guidelines for Rail Service to New Industry Locations• Rail Access Approval Process

– Links to Operating, Network Planning, Service Design, Engineering and Commercial Teams

• Capacity and Resource Evaluation

20

Restricted Access -- Mainline CorridorControlled Access – Mainline CorridorAllowable Access – Mainline Corridor

OregonTrunkJct

Hinkle

Ft. Worth

Oakley

San Jose

NorthPlatte

LosAngeles

Memphis

Laredo

Guidelines for Rail Service to New Industry Locations

on Union Pacific’s Mainline

San Antonio

Nampa

Poplar Bluff

Barstow

Seattle

Oakland

KansasCity

Salt Lake City

CouncilBlufffs

St.Louis

Denver

Alexandria

Pocatello

Stockton

Las Vegas

New Orleans

Lynndyl

South Morrill

Salem

Taylor

Texarkana

Livonia

Angleton

Dillon

Silver Bow

La Grande

Spokane

Eastport

Marysville

Chickasha

Bloomington

Corpus Christi

Provo

Jeff City

Robstown

N. Little Rock

Wagoner

Paola

Granger

Houston

Salina

Brownsville

Shreveport

Mason

City

MinneapolisSt.Paul

JanesvilleBelvidere

Valley Park

Clinton

K C JctBoone

Milwaukee

Sioux City

Chicago

Shawnee Jct

Adams

0

Woodland Jct

Portland

Roseville

Ogden

Santa Barbara W.Colton

Tucson

Phoenix

Dotsero

El Paso

Wichita

Pueblo

Topeka

0

Hearne

Dallas

Pine Bluff

Palestine

EaglePass

Nogales

Mojave

Bakersfield

Dexter

Yuma Picacho Lordsburg

Vaughn

Hutchinson

Fresno

Helper

GrandJct.

Lewisville

Eugene

Sierra Blanca

KlamathFalls

Flatonia

Lathrop

Martinez

JonesboroStratford

Chico

Amarillo

Tacoma

Reno

San Luis Obispo

Gibbon

Waco

Spofford

Pratt

Coffeyville

Parsons

Sanderson

Bill

Smelter

Egbert

Bond

Phippsburg

O'Fallons

Mt. Vernon

Odem

Beaumont

LakeCharles

Lafayette

Sweetwater

Arco

Niland

Portola

Elko

Marysville

Marshall

Bald Knob

Brinkley

Herington

NorthportRawlins

CheyenneFremont

Nelson

Altoona

Van Buren

San Marcos

Ontario

Chemult

Flanigan

Sacramento

Watsonville

St. James

Muskogee

Findlay Jct.

Ayer Jct

Idaho Falls

Axial

Ridgley

Round Rock

McAlester

Nogales

September 14, 2006

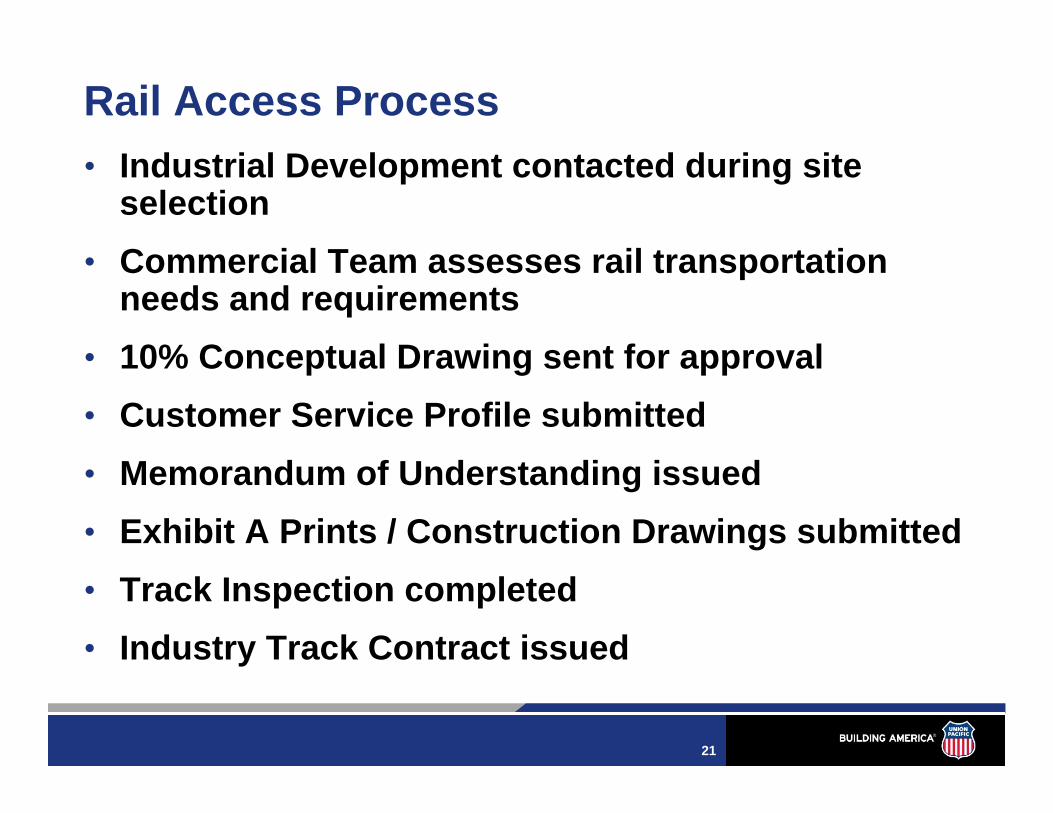

21

• Industrial Development contacted during site selection

• Commercial Team assesses rail transportation needs and requirements

• 10% Conceptual Drawing sent for approval• Customer Service Profile submitted• Memorandum of Understanding issued• Exhibit A Prints / Construction Drawings submitted• Track Inspection completed• Industry Track Contract issued

Rail Access Process

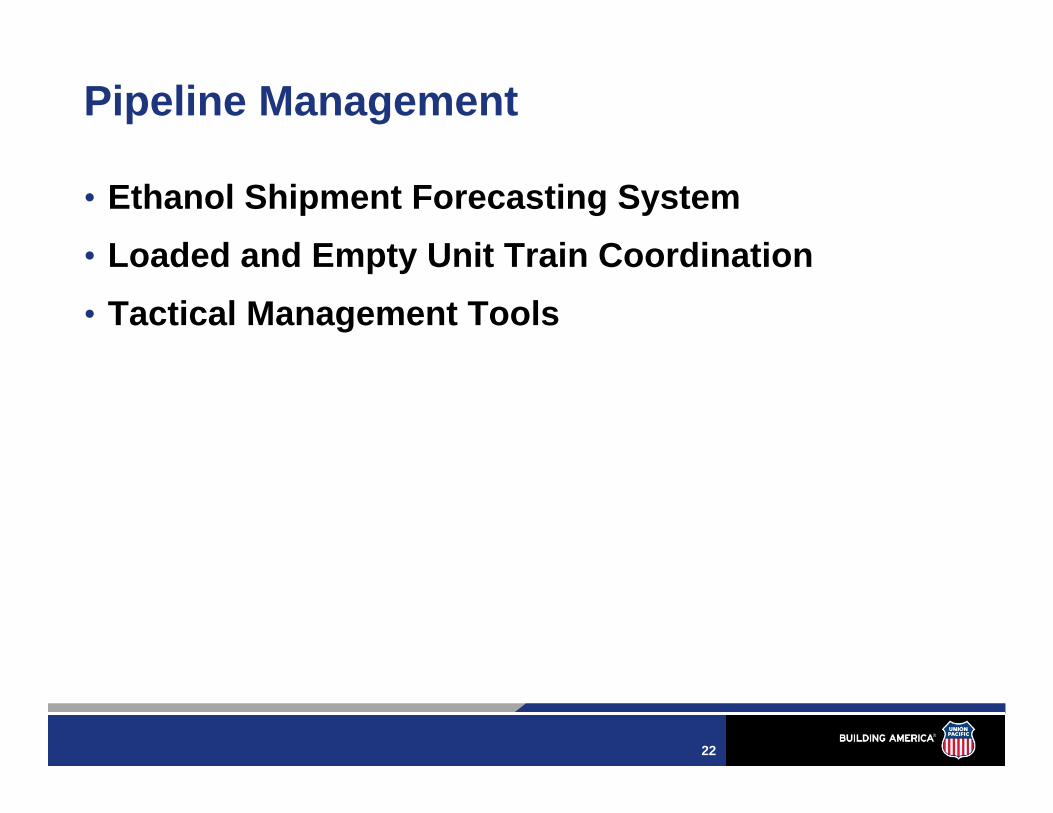

22

Pipeline Management

• Ethanol Shipment Forecasting System• Loaded and Empty Unit Train Coordination• Tactical Management Tools

23

Ethanol Shipment Forecasting System

• 30 Day Rolling Forecast

• Update System as Changes Arise

• Provide Trace and Buffer Cars in System 24 Hours Prior to Release

• Provide Billing Prior to 9A Cutoff

24

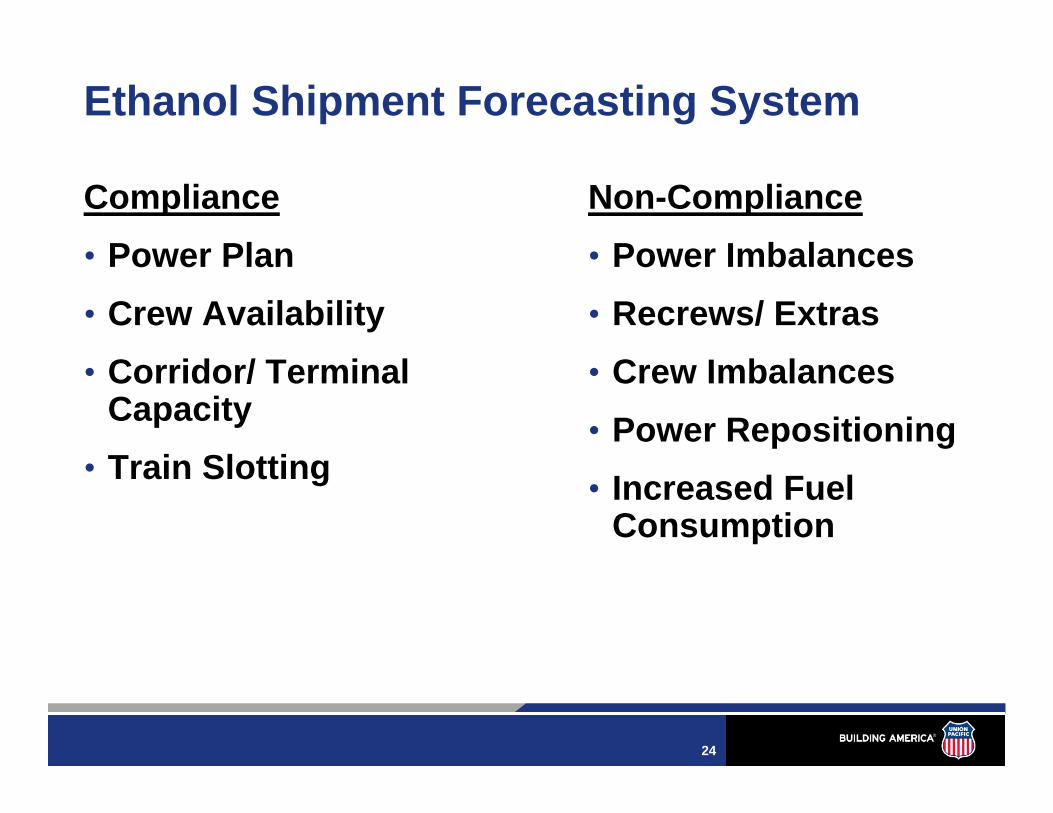

Ethanol Shipment Forecasting System

Compliance• Power Plan• Crew Availability• Corridor/ Terminal

Capacity• Train Slotting

Non-Compliance• Power Imbalances• Recrews/ Extras• Crew Imbalances• Power Repositioning• Increased Fuel

Consumption

25

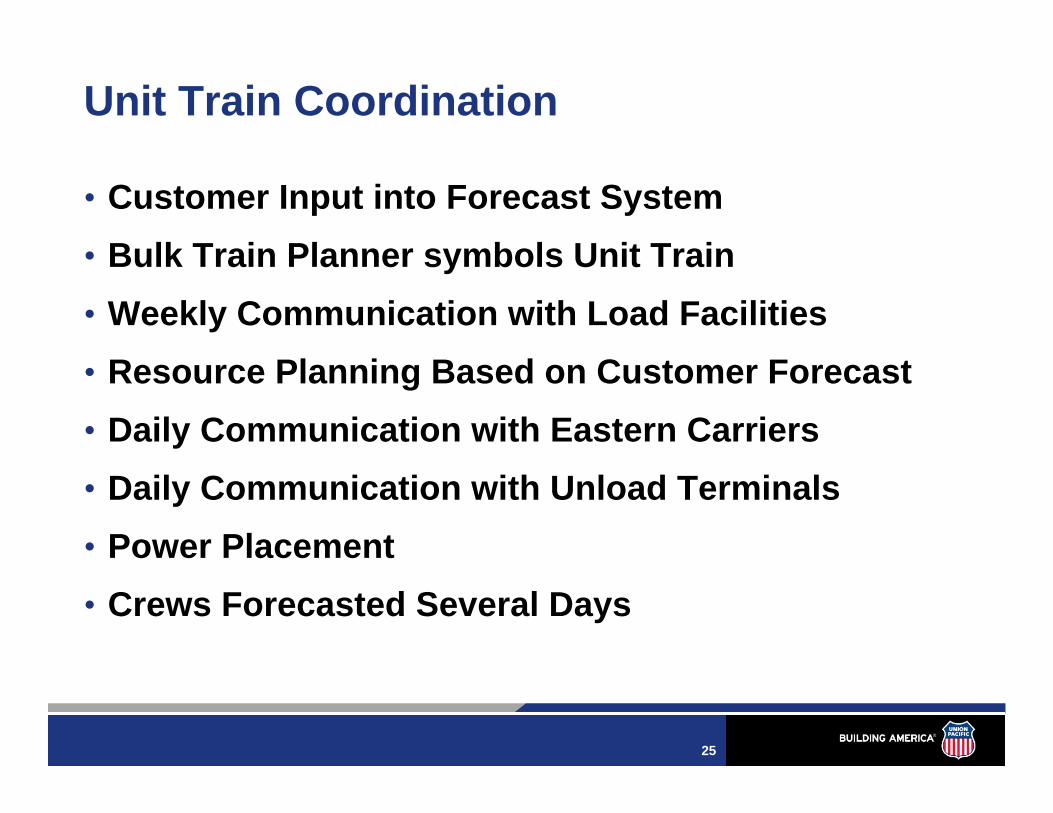

Unit Train Coordination

• Customer Input into Forecast System• Bulk Train Planner symbols Unit Train• Weekly Communication with Load Facilities• Resource Planning Based on Customer Forecast• Daily Communication with Eastern Carriers• Daily Communication with Unload Terminals• Power Placement• Crews Forecasted Several Days

26

Tactical Management Tools

• Bulk Train Planner (BTP)– Real Time Unit Train Monitoring– Efficient Coordination of Unit Train Resources

• Customer Inventory Management System (CIMS)– Proactive Management of Customer Car Flow

• Customer Operating Instructions (COI)• Permit Distribution System (PDS)

– U.S. Development Group (USD) System– Schedule and Control Traffic Flow into USD Terminals