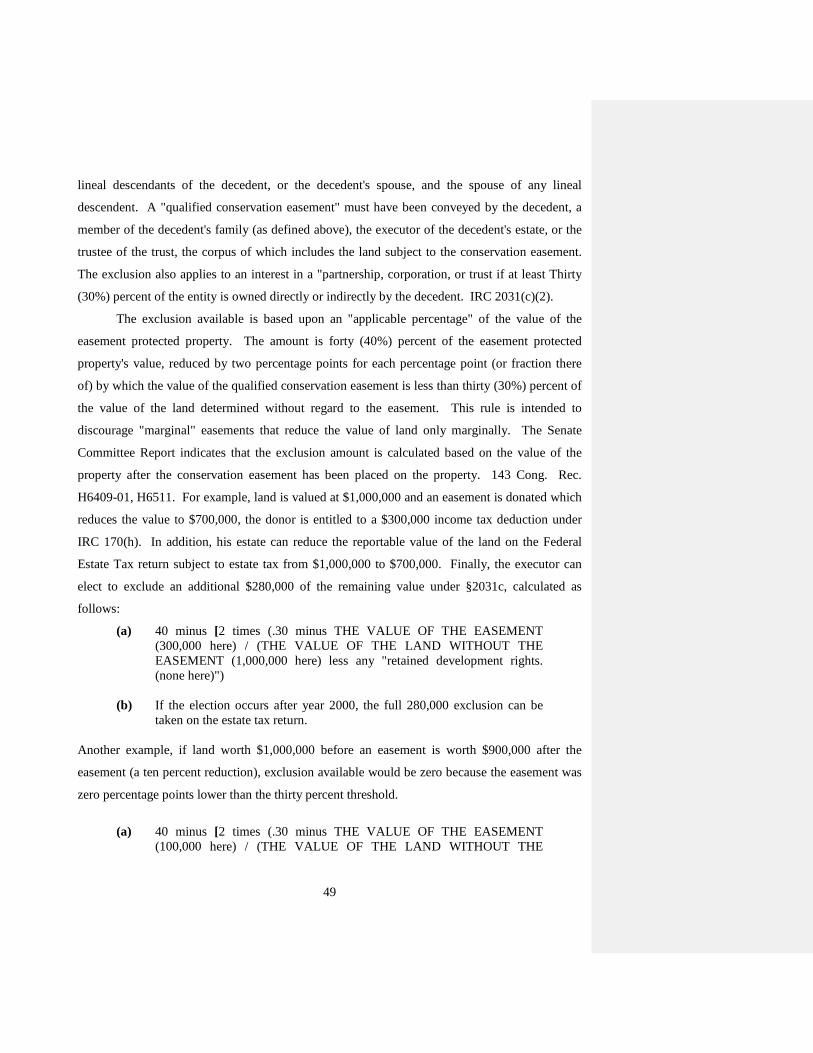

estate planning with agricultural assets: … · estate planning with agricultural assets:...

TRANSCRIPT

ESTATE PLANNING WITH AGRICULTURAL ASSETS: ACHIEVING

LIQUIDITY, LEGACY AND FLEXIBILITY

David J. Dietrich

Dietrich & Associates, P.C.

404 N. 31st Street, Suite 213

Billings, Montana 59103

E-mail: [email protected]

2

David J. Dietrich Dietrich & Associates, P.C. 404 N. 31st Street, Suite 213

Billings, Montana 59103-7054 (406) 255-7150

Email: [email protected]

David J. Dietrich graduated Whitman College, BA degree with honors (1979) and served in the United States Peace Corp in Abidjan, Ivory Coast (1979-1980). He attended the University Of Montana College Of Law and graduated with a Juris Doctor (JD) in 1984. David is the incoming Vice Chair of the 26,000 member Real Property, Trust and Estate (RPTE) Section of the American Bar Association and has served as its Secretary of since 2010.. He is a past Co-Chair of the RPTE’s Property Preservation Task Force (2003-2011), which resulted in the Uniform Law Commission’s adoption Uniform Partition of Heirs Property Act. He is active on the Planning Committee for the RPTE Section, sits on the University of Montana Tax Institute Advisory Board, and on the Board of Directors of Saint Vincent’s Hospital and Health Care Center in Billings. He served for six years on the Board of Directors of the Montana Land Reliance, a private land trust in Montana, having in excess of 1,000,000 acres under protection. David is a fourth generation Montanan, with a ranching, real estate and estate planning background in South Central Montana, Billings, a regional service center for the Northern Great Plains. His firm, Dietrich & Associates, PC, has provided real estate, tax and estate planning service to the region for over 22 years involving conservation easements, business organization, formation, and dissolution; and tax and estate planning. David’s publications include the 2011 ABA Book Conservation Easements: Tax and Real Estate Planning for Landowners and Advisors; “Selected Post-Mortem Estate Tax Elections for the Small Business Owner”(2002), “Pleasing Mother Earth and the IRS: Using Conservation Easements to Save Open Space, Income and Estate Taxes” for the Heckerling Institute for Estate Planning for the University of Miami, (January 2003); and other tax and real estate related topics for the State Bar of Montana David and his family enjoy living in the Big Sky Country; he is a Canon SLR camera fan, an avid Kindle user, engages in outdoor activities in all seasons, and is his daughter’s horse barn worker.

3

AGRICULTURAL ESTATE PLANNING IN 2013

I. INTRODUCTION

Agricultural estate planning often involves a combination of asset protection

planning, gift and estate tax minimization, and variable non-tax engagements, such as

consolidation of management through limited partnerships and limited liability companies for

land entities and Sub Chapter S corporations for operation entities. In addition, because of the

unique nature of many ranching properties, conservation easements may ensure continuity of

conservation purposes by preventing land fractionalization. As always, the agricultural real

estate lawyer must be not only familiar with valuation reduction and estate tax deferral methods

set forth in IRC § 2032A and 6166, but must also be aware of many incidents unique to

agricultural property such as mineral rights, water rights, access issues and, increasingly,

preserving the land for conservation values. The agricultural estate planner cannot be a casual

real estate lawyer.

It is particularly important in any agricultural operation to identify the clients’ “team of

advisers”. But first, identifying those members of the family who have been chosen or have

demonstrated through their own skills their abilities to continue the agricultural operation is

critical; it is equally important to determine what the senior generation desires to do for those

children who have not been favored with, or able to, remain on the operation and to provide

advice on wealth distribution to those children inasmuch as life insurance products and other

financial products can be used to provide for their well-being. In connection with all of this, it is

critical to establish the nature and extent of the engagement, and to confirm that information

given by the client to other advisors such as certified financial planners, certified public

accountants, life insurance agents and other “estate planning advisors” be also made available to

the attorney. Consideration should be given to providing for a continuing release of such

information as exhibits to the engagement letter. In addition, the engagement letter should

contain an express limitation on the scope of the engagement for information shared only with

other “estate planning advisors” which is not also shared with the attorney. Although it is a

worthy goal that a “team approach” can work with estate planning, it is necessary to have

4

waivers and disclosures of information delivered to other advisors so that the estate planning

attorney can have the entire picture before him or her. Furthermore, the recommendation that the

client return on an annual or every other year basis to the estate planner should be made a part of

the engagement letter. Finally, limited waivers of conflicts of interest consistent with the rules of

professional conduct should be obtained in the event that the attorney would be representing both

husband and wife and an agricultural business organization consisting of members of the second

generation.

II. BEGINNING THE PROCESS: EXAMINING THE FAMILY’S OBJECTIVES: LIQUIDITY, FLEXIBILITY AND LEGACY It is critical at the outset of the estate planning process to examine the estate planning

objects, family dynamics, and personal and tax related financial information, in addition to

performing due diligence on the business organizations and real estate involved in the

agricultural estate. Probing the client for their estate planning objectives is often a challenging

engagement inasmuch as the most trusted advisors may not be present during the meeting. It is

important to identify the long term goals of the client individually and the family generally,

which likely includes a determination of whether a limited partnership, limited liability company,

or Sub Chapter S corporation is a feasible business entity, involving non-family members, and

whether existing business organizations have been properly formed and are capable of

transmitting wealth by gifting or post mortem transfers to family members with appropriate

discounts. Estates rarely come in neat packages. Often in a going concern operation, clients will

deliver a 25 year old corporate minute book of a C Corporation holding highly appreciated real

estate where the minutes have not been maintained, the bylaws are outdated, no stock restriction

agreement exists, and family members negotiated a “detente” with a defacto business division

that they have made of the operation (farming and ranching). This may be a treasure trove of

legal work.

It may be necessary to identify what the client’s goals are on the “liquidity” or “legacy”

spectrum. “Liquidity” is often a luxury in many agricultural estates because many successful

agricultural operations consider their most valuable liquid assets to be livestock, unencumbered

machinery, and land which may not be necessary for the operation. Many such clients do not

have an established 401k program or portfolio of non-qualified assets. The value of cattle and

land remain volatile while the value of machinery and equipment depreciates rapidly. On the

5

other end of the spectrum, the client may be equally concerned with preserving the “legacy” of

the family ranch. Using conservation easements to restrain the development and

fractionalization of real estate is a valid but potentially radical solution to a concern about

piecemeal sales of the family ranch. A compromise position may be a limited liability company

with centralized management which can avoid partition but provide for limited distributions in

kind (at the expense of deep discounts for gifting or estate tax). Beware of tenancies in common

where the income is reported on a partnership tax return. RUPA may fold it into a partnership.

In addition, the planner must be aware of the asset protection and preservation motives of

the client. Does the client have multi-state assets? Can the client segregate his personal use

assets from the business assets, often a difficult task if the traditional family ranch has been

owned “all in” by a C corporation but likely necessary to avoid 2036 inclusion? (See discussions

of Turner, p. 18 below). Is state income tax planning an overriding consideration, as may be the

case in a no-tax state such as Wyoming; is the client also in a high risk profession such as

medicine, law or other professions; does the client have a large amount of high risk assets

engaged in trucking, shipping, cattle feeding, oil and gas or other high risk operations; are the

assets to be protected primarily real estate; to what extent may insurance be used to achieve asset

protection and to what extent should “firewalls” of other limited liability entities be created; are

the assets to be created primarily real estate and if so, are the real estate assets held in a limited

liability company, limited partnership or corporation which business interests themselves could

be successfully protected in a domestic asset protection trust under the laws of the local

jurisdiction or another jurisdiction?

Finally, serious consideration needs to be given to whether the family organization will

have non-family members. Make sure that appropriate waivers of conflict and independent

counsel relationships exist. Pay special attention to the drafting of the triggering event/buyout

provisions in stock purchase operating agreements or limited partnership agreements. What is

the net worth of the non-family members and can they dilute with capital all of the family’s

ownership? Is a private placement memorandum possible for a high net worth investor; are

securities being sold over state lines and is an exemption from the state security commissioner

necessary or advisable. Consider obtaining specialty counsel for securities compliance.

III. FUTURE CARE AND FEEDING OF THE PLAN

6

An often overlooked aspect of estate planning is maintaining and defending the plan.

Traditionally, estate planners have considered the estate planning engagement, on a legal basis,

to be finite, although in the clients’s mind the engagement is continuing. The initial engagement

is the due diligence and formulation of the will or trust including a business entity, with

healthcare or financial powers of attorney. It is at this juncture that estate planners are

particularly vulnerable to changes in technology which are rapidly changing our profession in the

form of do-it-yourself (“DIY”) wills or DIY corporations and LLC’s. Enter a query on Google

for “do-it-yourself wills and trusts” and the first ten entries generate websites including

legalzoom.com, totallegal.com, uslegalforms.com, ca-trusts.com, Quicken Willmaker Plus and

Suzie Orman’s Will and Trust Kit. The Texas legislature amended its unauthorized practice of

law statutes in response to a court decision finding that Quicken Family Lawyer violated the

unauthorized practice of law requiring it to specify that such products are not a substitute for the

advice of an attorney. Legal scholars who have studied the subject recommend that any such

programs affirmatively disclose that the organization selling the product is not a law firm, that

the ethical duties lawyers have to clients may not apply to the transaction between the buyer and

the seller of the product, and that the organization selling such software should be required to file

with an appropriate agency wherever it authorizes its services or products the location of its

principal business and the names and addresses of its senior officers with the fact and the

location of this filing revealed on this organization’s website. Furthermore, if any lawyers have

participated in the creation of the program or its content, their names, business addresses and bar

number status must be posted on the website; or, if no lawyers participated in the content or

creation of the program, then that fact must also be stated. See Generally Stephen Gillers, A

Profession If You Can Keep It, How Information, Technology And The Fading Borders Are

Reshaping the Legal Marketplace and What We Should Do About It, p. 155 found at

http://ssrn.com/abstract=2026052.

Make no mistake about it, the planner must justify to the client, agricultural or otherwise,

that the value of their services are significantly better than anything they can obtain from DIY

internet websites. An initial meeting with the client identifying the clients’ objectives,

explaining the risks of DIY programs cited above, comparing the use of a will or a trust, with or

without entity planning, with or without more advanced estate planning topics such as

irrevocable life insurance trusts or advanced planning techniques, certainly will impress the

7

client and possibly dissuade them from Quicken Willmaker Plus or Susie Orman’s Will and

Trust Kit.

In addition, the attorney must not only justify the nature and extent of his or her initial

engagement, but also provide a clear basis for the clients’ continuing use of the estate planning

attorney. In this connection, the client should be advised of when and under what circumstances

the estate plan should be reviewed, including death, divorce, inheritance of additional assets,

change in the family structure, or change in tax laws.

It is advisable that the attorney send annual letters advising the client to meet with the

attorney to update the estate plan, on an automatic basis. This can usually be done on the basis

that there is considerable continuing uncertainty with respect to the federal gift and estate tax and

clients need to know that they need to continually reassess their plan.

IV. PROBATE VERSUS REVOCABLE TRUSTS

Each state has different laws for probating wills, although many are “non-intervention”

Uniform Probate Code states. Probate can be extremely rapid and inexpensive (no court

involvement except upon opening an informal probate or the conversion of the proceeding to

formal or supervised administration). Heir contests, creditors’ claims, or disputes about the

distribution of assets by an unsupervised but irresponsible personal representative may also delay

administration. Inadvertent probates may be required where property has not been funded into a

revocable trust, mineral rights are discovered after probate, or property is not held in joint

tenancy with right of survivorship under a payable or transfer on death designation in the case of

a bank account or stock account.

In a non-intervention state such as Montana, the petitioner need only provide a petition

with an original will showing his or her statutory priority to serve as personal representative, a

proposed order to be appointed as personal representative, letters undertaking the duties to serve

as a personal representative and a notice to the heirs and devisees that such an administration has

begun. Thereafter, the personal representative is largely free to accumulate assets and pay debts

without necessity of further court involvement. Closing can be achieved by filing a sworn

statement that all assets have been administered and all debts paid after which the personal

representative’s authority expires within six months.

Notwithstanding the simplicity and low cost of probate, the prevalence of revocable trusts

since the early 1990’s has continued. The most basic reason for this is that the revocable trust

8

allows and in fact requires the trustor to accumulate and inventory assets which may be

otherwise missed in the accumulation and inventory of assets when a simple or more tax

sensitive will is drafted and signed. As a consequence, it is critical in any estate plan to confirm

that all transfer on death and beneficiary designation assets have been properly accounted for and

that the beneficiary designation’s coordinate with either the will or the revocable trust. This is

particularly the case with complex assets involving an agricultural estate plan which may include

certificate of title vehicles, non-titled equipment, livestock bearing brands, real estate assets held

under joint tenancy with right of survivorship, and business organizations including Sub Chapter

C corporations, LLC’s and limited partnerships, the interests of which may, in fact, be held in

joint tenancy rather than outright by the decedents. The process of inventory and appraising all

assets of the decedent in the context of planning for a revocable trust often results in better asset

management than achieved with drafting the simple will. Moreover, a revocable trust may save

considerable filing fees.

V. AN OVERVIEW OF FUNDING CLAUSES

Since 2001, the Applicable Exclusion Amount or exemption amount (often the amount

funded into a bypass trust and otherwise known as an exemption trust or credit shelter trust) has

been a moving target. Exemption amounts have ranged from $1 million to $5 million dollars..

Since the current tax revision in early 2013, the Applicable Exclusion Amount is the sum of the

basic exclusion amount of $5.25 million dollars and, in the case of a surviving spouse, the

Deceased Spousal Unused Exclusion Amount. See IRC § 2010(c)(2). This statutory language

implements the term “portability” such that the unused amount of the deceased spouse

exemption is carried forward to the surviving spouse as limited by the term “the last deceased

spouse of such surviving spouse”. See IRC § 2010(c)(4). The executor of the estate of the

deceased spouse must file an estate tax return to make the election. IRC § 2010(c)(5)(A). See

also Notice 2011-82.

Consequently, it is not necessary to use a bypass trust to “capture” the entire applicable

exclusion amount available to both spouses. Nevertheless, due to the need for asset protection or

trust management, traditional planning techniques, split the estate on a first death into a (1) credit

shelter trust (the non-marital share) and (2) a marital trust (a QTIP general power of appointment

or QDOT trust) remain an extremely attractive estate planning strategy, particularly where the

9

agricultural operation has been placed into a business organization such as a sub chapter S

corporation, limited liability company or limited partnership.

Tax funding clauses are the heart of what divides and allocates these trusts and the most

commonly used are the fractional tax funding clauses and the pecuniary tax funding clauses. See

Kelly, Donald, Estate Planning For Farmers and Ranchers, Chapters 4:21, 4:22.

Fractional Clause - A fractional formula expresses the amount which can pass free of

estate tax calculated on the basis of the value of the assets in the estate at the applicable valuation

date and entitles the surviving spouse or marital trust to that fraction of the reside. The simplest

form of the fractional formula is an in-kind distribution of the fractional interests in all assets. If

the executor has the power to “pick and choose assets” to be used in funding the marital legacy, a

fractional formula is considered by some to avoid disadvantages of both fractional and pecuniary

legacies. An example of such a clause is set forth as follows:

Devisees of real and personal property/spouse survives

If my spouse survives me, as such survival is herein defined, I hereby give and devise my property as follows: (1) all personal effects, household goods, and automobiles, of which I may die the owner, together with all policies of insurance relating thereto, to my spouse. (2) to my Trustee that fraction of my residuary estate of which the numerator shall be a sum equal to the largest amount, after taking into account all allowable credits and all property passing in a manner resulting in a reduction of the Federal Estate Tax Unified Credit available to my estate, that can pass free of Federal Estate Tax and the numerator of which shall be the total value of my residuary estate. (3) for the purpose of establishing such fraction, the value finally fixed in the Federal Estate Tax proceeding and my estate shall control. (4) the balance of the residue of my estate after the satisfaction of the above devise, I devise to my spouse provided that any property otherwise passing under this paragraph which shall be effectively disclaimed or renounced by my spouse under the provisions of the governing state law or the Internal Revenue Code shall pass under the provisions of paragraph ___ below. (The paragraph cross-referenced in paragraph 4 is a reference to

10

the Credit Shelter Trust which would normally follow this paragraph.)

Using entities for the ownership of agricultural land automatically apportions chattels,

elected real property and unelected real property between the marital and credit legacies, which

confirms the need to form entities for both the agricultural operational entity and land holding

entity. Kelly, Donald H., Estate Planning for Farmers and Ranchers, Chapters 4:61, 4:64,

Supplement at p. 181, See also Cason, The “Just Enough” Funding Technique: An Innovative

New Strategy, 35 Estate Planning 27 (June 2008); See also Soled, Wolf and Arnell, Funding

Marital Trusts: Mistakes and Their Consequences, 31 Real Property Probate and Trust J. 89

(Spring 1996).

Pecuniary Clause - On the other hand, a pecuniary formula arrives at a specific dollar

amount generally tied to the complete use of the federal estate tax unified credit in order to

reduce the estate taxes on the first estate of the spouses and assure full use of the unified credit of

each spouse. Such formulas which result in a pecuniary amount passing to the surviving spouse

are based on a calculation which subtracts from an amount equal to the taxable estate the amount

of unified credit value equivalent and makes other adjustments. A pecuniary formula can first

fund the marital share and leave the residue as the credit shelter trust. See Kelly, Donald H.,

Estate Planning for Farmers and Ranchers, Chapters 4:21, 4:22

The pecuniary to the surviving spouse form of marital deduction formula may be

addressed either (1) by minimal reduced to zero (least tax language); or (2) by carving out

prescribed amounts from the maximum marital deduction that will reduce the spousal legacy.

An example of such a pecuniary clause is as follows:

An amount equal to the maximum marital deduction allowable to my estate is finally determined for federal estate tax purposes, less the value so determined of all other property interests passing to my surviving spouse, other than by this instrument, which are includable in my gross estate for Federal Estate Tax purposes and which qualify for such marital deduction; unless such further amount, if any, required to increase my taxable estate to the largest amount that will result in the least amount of Federal Estate Tax [and state death taxes computed by the credit allowable under § 2011 of the Code] payable in my estate; [provided that the state death tax credit shall be taken into account only to the extent that it does not result in an increase in state or federal death taxes otherwise payable.] after taking into account all allowable credits and all property passing in a manner resulting in a reduction of the Federal Estate Tax Unified Credit

11

available to my estate. Kelly, Donald H., Estate Planning for Farmers and Ranchers Chapter 4:92.50. In the event of an estate consisting primarily of farmland for which a 2032 election may

be made, optimum sheltering of property from taxation in the second estate occurs if the will

contains a pecuniary formula legacy to the surviving spouse and the special value election is

made across the board as to all eligible land of the decedent, regardless of whether the specially

valued property is passed to the credit shelter or to the surviving spouse. See Kelly, Donald H.,

Estate Planning for Farmers and Ranchers, Chapter 4:61, Supplement, See also Rev. Proc. 64-

19. There are several other observations regarding the mathematics of the marital deduction

involving farm land, stated as follows:

(a) The reduction in gross estate value resulting from a farm special value election leaves the Unified Credit unchanged, but lowers the amount required to obtain the marital deduction which will reduce the taxable estate to zero. As a consequence, the result obtained by funding only the necessary amount of marital deduction legacy with property at fair market value, or funding the credit shelter with § 2032(a) property at § 2032(a) value, is to add the amount of the § 2032(a) value reduction to the property covered by the credit shelter. Kelly, Donald H., Estate Planning for Farmers and Ranchers Chapter 4:6, Supplement p. 179

VI. CLAYTON QTIP WILLS

Under the Clayton QTIP regulations, Treas. Reg. 20.2056(b)(7)(D) an executor may

control the marital deduction amount rather than relying on a disclaimer by the spouse. Such a

provision generally provides that the interests of the surviving spouse is contingent upon an

executor’s QTIP election in order to constitute a qualified terminable interest property under

Section 2056(b)(7) and that the non-elective portion will pass in the form that would not qualify

for the marital deduction, i.e. a credit shelter trust. An example of a Clayton QTIP funding

clause is as follows:

If I am survived by my wife, my personal representative shall, as directed, divide my estate assets into One (1) or Two (2) shares, hereinafter designated as the “QTIP Trust" and/or the “Family Credit Shelter Trust". The QTIP Trust shall be that fraction of my estate assets (undiminished by any estate, inheritance, succession, death, or similar taxes) determined as follows: the numerator of the fraction shall be the amount elected as Qualified Terminable Interest Property

12

(“QTIP”) for federal estate tax purposes by my personal representative. The denominator of the fraction shall be the value of my estate assets as finally determined in my estate tax proceedings. The personal representative shall have the sole discretion to select the assets which shall constitute the QTIP Trust. In no event, however, shall there be included in the QTIP Trust any asset or the proceeds of any asset which will not qualify for the federal estate tax marital deduction, and the QTIP Trust shall be reduced to the extent that it cannot be created with such qualifying assets. The QTIP Trust shall be administered as hereinafter set forth. The Family Credit Shelter Trust shall be the balance of my estate assets (or the entire estate assets, if my personal representative does not make the election) after the assets have been selected for the QTIP Trust to fulfill the QTIP election.

An added benefit to a Clayton QTIP trust is that it allows the executor rather than the

surviving spouse to make the election and may do so up to fifteen (15) months after date of

death, assuming the 706 return is validly extended, rather than relying on the compliance with

state and federal disclaimer law deadlines which require a valid disclaimer to be made at the

earlier of prior to acceptance of benefits or nine (9) months. Treas. Reg. 20.2056b(7)(d)(3). It

may be advisable to have a special personal representative specifically named for making the

Clayton election. See Mulligan, Updated Planning for Marital Dispositions, Lifetime QTIPS

and QDOTS, 26 Estate Planning 395 (November 1999).

VII. DISCLAIMER TRUST WILLS.

Because of the complexity of the use of tax funding clause, as described above, clients

may desire a more simplistic approach: namely the use of a disclaimer trust will. This allows

the surviving spouse to make the election at the earlier of a time prior to the acceptance of

benefits or nine months after date of death. See Generally IRC § 2518 which defines a qualified

disclaimer:

A. To qualify the disclaimer must be an “irrevocable and unqualified refusal:

1. in writing, 2. such writing is received by the transferor or his legal representative or holder of legal title within nine months of the later of (A) the date the transfer created the interest is made; or (B) the date upon which the person disclaiming reaches age 21, 3. such person has not accepted any benefit; and 4. the interest passes without any direction on behalf of the disclaimer.

13

See IRC § 2518(b). A disclaimer can be made with respect to an undivided portion of an interest

which otherwise qualifies under § 2518(b). See IRC § 2518(c). The regulations further make

clear that joint tenancy with rights of survivorship do meet the requirements of qualified

disclaimers. Treas. Reg. § 25.2518-2(c)(4)(i). Furthermore, the regulations set forth a number of

examples wherein the disclaimant may have in his will an appropriate designation of a fiduciary

limited by an ascertainable standard where the surviving spouse can be the trustee. See Treas.

Reg. § 25-2518-2(e)(5) examples 1-12. The following is an example of a disclaimer trust

residuary clause and the related Family Trust:

Residuary Gift to Surviving Spouse; Contingent Gift to Trustee of The FAMILY TRUST. I give all the rest, residue and remainder of my property of every kind and description (including lapsed legacies and devises) wherever situate and whether acquired before or after the execution of this Will, to my wife, , if she shall survive me. If she shall not survive me or if she shall survive me but disclaims all or a portion of this residuary gift, then I give all the property or the portion thereof which is disclaimed to the Trustee of The FAMILY TRUST, to be administered as hereinafter set forth in Item X.

ITEM X

The FAMILY TRUST Introductory Provision. The

FAMILY TRUST shall be held, administered and distributed as follows:

Payment to Wife of Net Income. If my wife shall survive me, then commencing with the date of my death, my Trustee shall pay to or apply for the benefit of my wife during her lifetime such sums of the net income from The FAMILY TRUST as my Trustee deems advisable, giving preference to the needs and desires of my wife, in convenient installments but no less frequently than once every four months for any calendar year. Any undistributed income shall be added to principal of The FAMILY TRUST. Discretionary Payments of Principal for Wife. If my wife shall survive me, my Trustee may pay to or apply for the benefit of my wife during her lifetime, such sums from the principal of The FAMILY TRUST as in its sole discretion shall be necessary or advisable from time to time for the medical care, education, support and maintenance of my wife, taking into consideration to the extent my Trustee deems advisable, any other income or resources of my wife known to my Trustee.

Division Into Shares for Children. Upon or after the death of the

survivor of my wife and me, my Trustee shall divide and distribute this

14

Trust as then constituted into equal separate shares to CHILD ONE, CHILD TWO, CHILD THREE, and CHILD FOUR, by representation.

VIII. RISKS OF DISCLAIMER TRUST WILLS

Often the disclaimer trust will involves a choice between trusting the surviving spouse to

make the election or having a QTIP trust wherein there is a mandatory funding, a pecuniary

fractional or otherwise, creating control in either a spouse or third party fiduciary of the marital

share. Consideration should be given as to whether the surviving spouse will actually execute

the disclaimer. Further, consideration should be given to the risks that the surviving spouse will

accept benefits prior to the execution of a qualified disclaimer and its delivery to the trustee or

filing in probate court. Consideration should also be given to the fact that the surviving spouse

must not have the power to effect the ultimate disposition of the trust property through a limited

power of appointment. See Estate of Engelman v C.I.R., 121 T.C. Memo 54 (2003).

IX. ANNUAL EXCLUSION GIFTING

Provided that the estate planner has formed and funded a limited partnership or limited

liability company or other entity suitable for the clients’ needs, serious consideration needs to be

given to the gifting of business assets. Under the Tax Relief Unemployment Insurance

Reauthorization and Job Creation Act of 2010, the applicable credit for gift taxes increases from

$1 million dollars to $5 million dollars for 2011 and 2012 before returning to $1 million dollars

in 2013. Serious consideration needs to be given during the remainder of 2012 as to whether

sizeable gifts should be completed, utilizing discounts likely available for business interests in

limited liability company or limited partnership form. Under IRC 2035, with certain exceptions,

gifts from a donor to any donee aggregating less than $13,000.00 as adjusted for inflation in a

calendar year, are removed from the donor’s estate at the moment of the gift. The number of

permissible donees is without limit. The amount in excess of any $13,000.00 gift will be brought

into the estate tax calculation as adjusted taxable gifts.

A fundamental requirement of the gift is it must be a gift of a present interest, not a future

interest. A case of major importance in this regard is Hackel v Commissioner, 118 T.C. Memo

279, which held that gifts of entity units in a limited liability company were gifts of future

interests and not entitled to an annual exclusion. The court based its holding on a finding that the

operating agreement did not allow the donees to presently access any economic or financial

benefit from the gifted interests; had there been in Hackel current income distributed or available

Comment [JV1]: frag

15

for distribution, the ability to sell the gifted interest or the right to put the gifted interest, the

result may have been different. See Kelly, Donald H., Estate Planning for Farmers and

Ranchers, Chapter 6:35 at 6-87; See also Price v CRR, T.C. Memo 2010-2. In Price, there was

no immediate enjoyment of the donated property itself because the donees had no ability to

withdraw their capital accounts and could not sell their interests without the written consent of

all other partners and there was no immediate enjoyment of income from the donated property in

the absence of a steady flow of income since distribution of profits was in the discretion of the

general partner and the partnership agreement provided that distributions would be secondary to

the partnership’s primary purpose of generating a long term reasonable rate of return. Kelly,

Donald, H., Estate Planning for Farmers and Ranchers, Chapter 6:25, Supplement Page 463.

From a compliance standpoint, it is necessary to start the statute of limitations running

under the “adequate disclosure” regulations. See Proposed Regulations Sections 20.2001-1,

25.2504-2, and 301.6501(c)-2(f). Thus, as a practical matter, upon the filing of a federal gift tax

return, Form 709, the grantor is required to (1) describe the gifted property and any consideration

received by the donor; (2) the identity of in relationship between the donor and the donee; (3) a

detailed description of the method used to determine the fair market value of the gifted property

including relevant financial data and a description of any valuation discounts taken such as

blockage, minority, fractional interests and lack of marketability. In the case of an entity such as

an FLP or LLC, a description of the discount taken and a statement of the fair market value of

100% of the entity value without discounts must be included; and a statement of the relative facts

affecting the gift tax treatment of the transfer sufficient to apprise the service of the nature of any

potential controversy concerning gift taxes, describing any legal issue presented by the facts and

disclose any position taken contrary to any temporary or final regulations.

X. ENTITY FORMATION: INITIAL DUE DILIGENCE

An identifiable category of any estate planning engagement is the formation of business

entities for the purpose of transmitting wealth. However, many estate plans come laden with

historic business organizations which may not meet the financial and estate planning goals of the

client. While fifty years ago the estate planner was limited to C Corporations, S Corporations,

and business trusts, as well as general partnerships and sole proprietorships, today the planner

has at his or her disposal domestic asset protection trusts, limited liability limited partnerships,

limited liability companies, and more traditional C Corporations, S Corporations and general

16

partnerships. Since 1986 and the repeal of the General Utilities Doctrine, many C Corporations

remain high capital gains tax zombies with operational risks because of highly appreciated real

estate assets with a lurking 50% to 60% tax liability in the event of liquidation or sale. Often the

most valuable task that can be performed by the estate planner is a tax free division under IRC

§355, discussed below. In addition, the planner should review whether any buy sell agreements

exist, whether they are outdated, the integrity of the “financial health of existing life insurance

policies (i.e. get in force illustrations from the life insurance company or an independent analysis

by a non-commission based insurance analyst). In addition, the planner should review the stock

transfer legends of the corporation to confirm that such legends are up to date. The planner

should also review whether the corporation has a capital structure extending beyond a single

class of stock or the differentiation between voting and non-voting shares, i.e., are there

preferential voting rights or distribution rights upon liquidation. In this connection, the most

valuable work that a planner might possibly perform is encouraging all shareholders to elect

subchapter S treatment to enjoy greater net sales proceeds upon sale or liquidation date the

expiration of a ten (10) year period or of the ten year period required under rules governing

Subchapter S election.

XI. DIVISION OF CORPORATIONS

While the matriarch or patriarch of an agricultural operation is still alive, (although it is

not required under IRC §355 and related regulations), it is most feasible to achieve a tax free

division of a C Corporation or S Corporation, and avoid the prospect of a taxable liquidation or

shareholder oppression claims.

Examining the scope of the requirements under IRC §355 is beyond the scope of this

outline. The issue should be recognized, however, by the estate planner because often siblings

inheriting stock by gift or devise have different business objectives and latent or overt hostility;

some owners may be active and others may be passive. Although electing Subchapter S and

waiting the ten year period may soften the tax on liquidation, often business owners do not want

to liquidate the entire entity, or cannot afford the tax issue. As a consequence, a tax free division

under IRC §355 may provide a solution. One or more subsidiary corporations are formed by the

existing corporation transferring some or all of the assets to them. The subsidiary stock is then

transferred to the owners in exchange for the stock in the original corporation. To qualify for tax

free division, both the distributing and controlled corporation (original parent and new

Comment [JV2]: rework sentence

17

subsidiary) must be engaged in the active conduct of a trade or business immediately after the

division. In a farming situation, a problem may arise if the operation has changed to a passive

rental, which may occur of the next generation has left the farm and the older generation has

retired using the farm property as a source of retirement income from the rents. See Kelly,

Donald H., Estate Planning for Farmers and Ranchers, Chapter 8:52, see also Brunell E.

Steinmayer, Jr., Burnell E., and Turner, Todd D., Second Generation Planning – The Corporate

Division Alternative, 20 Probate and Property 49, Volume 20, Number 6, (Nov/Dec 2006). The

active conduct of a trade or business requires the corporation itself (through its officers and

employees) to perform active and substantial management and operational functions. If the

corporation engages in substantial management and operational functions, an IRC § 355 division

may be available so that the next generation of owners can then work toward their independent

goals without incurring a substantial tax cost. See Generally Rev. Ruling 73-234, Rev. Ruling

86-126 and Rev. Ruling 2003-52. Importantly, in Rev. Ruling 2003-52, the National Office of

the Internal Revenue Service ruled that a disagreement between a brother and sister operating a

corporation with respect to future operations was significantly serious such that it would prevent

each of them from developing a business in which they would have a majority interest; a division

would eliminate the disagreement and allow each of them to operate separate businesses to

which they could devote their full time and energy. The senior generation, i.e., mother and

father, would each own 25% in both of the two surviving corporations and would continue to

participate in major management decisions related to the businesses of each corporation;

however, in other situations the senior generation could no longer be active as to their vote

concerning the stock. Kelly, Donald H., Estate Planning for Farmers and Ranchers, Chapter

8:54, Supplement at page 707.

XII. FAMILY LIMITED PARTNERSHIP AND LIMITED LIABIITY COMPANIES: CAPITAL STRUCTURE AND OPERATION TO AVOID 2036 INCLUSION The limited liability company and limited liability limited partnership are the entities of

choice to hold real estate using agricultural operations. With respect to limited liability

companies, the choice of the capital structure often ranges between a member managed

organization with straight up pro rata voting depending on ownership percentages and a manager

managed structure where notwithstanding the percentage of ownership of the managers, the

18

managers control the operation, not unlike a corporation or limited partnership. A critical

determination here is the interplay between the capital structure of the limited liability company,

and the possible inclusion of the capital interests in the limited liability company under IRC §

2036(a)(2). See Generally Estate of Turner, TC Memo 2011-2009. See also Breed, Richard P.

and Hilario, Lessons From Turner to Protect Against IRS Challenge FLP, Estate Planning July

2012, Volume 39, Number 7, Page 13. The Turner case provides excellent instruction to the

estate planner forming a family limited partnership or LLC about its original capital structure and

eventual operation and how to avoid estate tax inclusion under IRC§ 2036(a)(2). Specifically,

the planner must achievethe threshold requirement that the formation and operation of the entity

meet the requirements of a “bona fide sale for adequate and full consideration” exception to IRC

§ 2036 inclusion in the estate. Specifically, to fit under the Turner requirements, and its bona

fide sale exception, the FLP or LLC must pass a two part test:

1. The facts and circumstances of the FLP or LLC transaction must present, as actual motivation for planning, a “legitimate and significant” non-tax reason to create the FLP or LLC; and 2. The Transferor must receive a proportionate partnership interest equal to the property transferred to the FLP or LLC. In the Turner case, the court considered the following factors: 1. Whether the assets by their nature required active management or special protection; 2. Whether in fact the business entity required active management and whether a special investment strategy was implemented; 3. Whether the use of the FLP structure provided greater efficiency of management; 4. Whether there was litigation or a threat of litigation among family members creating a real risk to the family estate so as to justify the creation or formation of an FLP; and 5. Whether there was an actual need to protect family assets.

19

In reviewing the factors, the Turner court held that the estate’s purported non-tax business

reasons for forming the LLC were unsubstantiated. The court also found additional factors

evidenced in the lack of a bona fide sale, as follows:

1. There was no meaningful or real negotiation with the parties involved in the transaction; 2. There was a co-mingling of personal assets and partnership funds; 3. There was a short time between the formation of the business organization and the ultimate transfer (here 8 months); and 4. There was evidence of transfer tax motives for the formation of FLP because of an attorney’s letter discussing the need to have an appraisal for gift tax purposes.

In forming an LLC or FLP it is very critical to document the non-estate tax reasons, (i.e.

legitimate business reasons) for the formation of the LLC or FLP. In addition, with respect to

the capital structure of the LLC, or the FLP, care should be given to avoid the following:

1. The ability of the senior generation to unilaterally amend the partnership agreement without the consent of the limited partners or other limited liability company owners; 2. The decedent or majority owner’s sole and absolute discretion to make distributions of partnership and income and distributions in kind; and finally 3. Because the decedent owned in excess of a majority interest of the limited partnership, he could make any decision concerning the FLP or LLC that effectively allowed him to control the limited partnership (in other words there was no super majority voting carve outs in the agreement).

In consequence of the foregoing, the tax court held that § 2036(a)(2) applied because Mr. Turner,

in conjunction with his wife, could designate who could possess or enjoy the property transferred

to the FLP.

As difficult as it may be for the estate planner, it is critical that the patriarch and

matriarch, acting in conjunction, cannot simply control all aspects of the limited liability

company or family limited partnership; to do otherwise risks inclusion under IRC § 2036(a)(2),

20

particularly if the bona fide sale exception cannot be made because of legitimate non-tax reason

that the formation of the entity cannot be demonstrated.

XIII. LIMITED LIABILITY COMPANY AND LIMITED PARTNERSHIPS: CAPITAL ACCOUNTS AND STATE LAW CONSIDERATIONS Limited partnerships and limited liability companies are often formed under the mistaken

impression that they are low maintenance. However, from the outset, it is critical that

appropriate records be maintained for the LLC particularly for book/tax purposes. It is important

to use deficit capital account restoration language, qualified income offset, and minimum gain

chargeback provisions. See Generally Baker, Jr., Donald H., What Does That Operating

Agreement Mean, a Primer on LLC Capital Accounting for the Non-Specialist,

http://www.michbar.org/business/BLJ/Summer/%202010/DBaker.pdf.

In addition, LLCs are vitally important for their flexibility because of the ability, from a

tax standpoint, to allocate depreciation to the initial investor of cash, provide preferred returns to

initial investors, and allocate tax credits. LLCs can also be used to provide for eventual

distribution in kind of certain assets but such provisions, if exercised, may violate disguised sale

or mixing bowl regulations and severely limit the discountability of LLC or FLP interests.

It is important to consider which state the LLC or FLP should be formed in, because not

all states have adopted the Limited Liability Limited Partnership Act and states have varying

rules regarding, for LLC’s, what the operating agreement must contain, how internal affairs are

handled among partners, the duties and liabilities of managers, rules governing charging orders,

rules governing recovery for improper distributions, and remedies for oppressive conduct. See

Generally 2006 Revised Uniform Limited Liability Company Act (re/ullca on the Uniform Law

Commission Website at www.ulc.org . With respect to limited partnerships also see the Uniform

Limited Partnership Act revised by NCCUSL (now ULI) in 2001 which enhances limited

partnerships for the following reasons:

1. A limited partnership can be perpetual rather than terminate after a given period of time; 2. A limited partnership can be clearly an entity; 3. A limited partnership no longer depends on general partnership rules not contained in the Uniform Limited Partnership Act;

21

4. The new Uniform Limited Partnership Act provides a full status based shield against limited partner liability for entity obligations; and 5. Under the new Uniform Limited Partnership Act, limited partnerships may opt to become limited liability limited partnerships simply by so stating in the limited partnership agreement and in the publicly filed certificate. (The effect of this election is to limit the historic unlimited liability of the general partner of the limited partnership.)

XIV. LIMITED LIABILITY COMPANY AND LIMITED PARTNERSHIP MAINTENANCE Stephanie Loomis Price of Houston, Texas, an experienced practitioner in FLP/IRS

litigation gives very insightful tips regarding FLP maintenance and transfers as follows:

1. File required annual filings and memorialize all significant partnership decisions; 2. Comply with the terms of the partnership agreement; 3. Comply with any loan terms, if loans are made; 4. Make any distributions pro rata and pursuant to the terms of the partnership agreement; 5. Refrain from the personal use of partnership assets (at least unless fair rental is paid) or using assets for the partner’s personal obligation; 6. Refrain from having the partners individually pay partnership obligations; 7. Encourage partners to maintain current and accurate books and records; 8. Avoid the following as recurring transactions between the partners and the partnership: loans, redemptions, non-regular distributions and non-pro rata distributions; 9. Review the non-tax reasons for forming the partnership and follow them; and 10. Establish a protocol for administering the partnership in accordance with the requirements of the agreement.

22

With respect to the transfers of FLP or LLC interests, Stephanie Loomis Price recommends as

follows:

1. Review books and records of the partnership prior to transfer; 2. Amend the Certificate of Limited Partnership (or LLC Articles of Organization) if necessary; 3. Execute appropriate transfer documents concurrent with transfers to the FLP or LLC; 4. Consider the effect of transfers if an IRC § 754 election is in effect; 5. Wait until after the partnership is fully funded and operational to begin gift planning; 6. Abide by transfer restrictions in the partnership agreement; 7. Carefully consider tax consequences of transfers; 8. Retain the services of an independent and qualified appraiser; 9. Encourage open communication with appraisers; 10. Do not conceal information from the appraiser; 11. Be specific about what interests need to be valued; 12. Be aware of IRS settlement guidelines; and 13. Carefully review the appraisal report and request revisions if it is not easy to understand.

XV. GIFT ON FORMATION PROBLEM

A problem encountered upon the formation of an FLP or LLC involves contribution of

property to a partnership creating an inadvertent gift upon entity formation. See Senda v C.I.R.,

T.C. Memo 2004-160, Judgment Aff’d 433(f)(3)(d) 1044 (8th Cir. 2006). See also, Gross v

C.I.R., T.C. Memo. 2008-221 (2008). Senda and Gross stand for the proposition that the step

transaction doctrine is alive and well for use by the IRS to attack initial contributions to a FLP or

LLC followed by an immediate transfer of a heavily discounted membership interest, if there is

no exposure to market risk. In Gross, a lapse of eleven days between the last contributions of

23

securities and the date of the gift was deemed sufficient. Senda strongly suggests that structuring

the creation of a limited partnership so that any gifts made are clearly disconnected with the

formation of the partnership and the contribution of property to it. The IRS has issued appeals

settlement guidelines for family limited partnership and family limited corporations available on

the IRS website at http://www.irs.gov/pub/irs-utl/asg_penalties_fa

XVI. SELECTED POST- MORTEM ESTATE TAX ELECTIONS FOR THE AGRICULTURAL BUSINESS OWNER

The post-mortem elections discussed include the alternate use valuation under IRC §

2032, special use valuation under IRC § 2032A, a qualified family business interest deduction

under IRC § 2057, the election to pay federal estate taxes in installments under IRC § 6166, and

the qualified conservation easement under § 2031(c).

XVII. IRC § 2032: Alternate Valuation

Section 2032 provides an exception to the general rule that property comprising the

decedent’s gross estate is valued at its fair market value as of the date of death. IRC § 2031(a).

As an exception, Section 2032 allows the personal representative of the decedent’s estate to elect

valuation of the gross estate at a selected later date, rather than the date of death.

Basic Requirements. If the property comprising the gross estate is distributed, sold,

exchanged, or otherwise disposed of within six months after the decedent’s death, this property

can alternately be valued as of the date of distribution, sale, exchange, or other disposition. IRC

§ 2032(a)(1).

If the property comprising the decedent’s gross estate has not been distributed, sold,

exchanged or otherwise disposed of within six months after the decedent’s death, the personal

representative may elect to have the property valued on the date which is six months after the

decedent’s death. IRC § 2032(a)(2).

If the alternate valuation date is elected, special rules apply for the valuation of interests

that are affected merely by the lapse of time. Specifically, these interests are includable in the

gross estate at the value as of the decedent’s date of death, with an adjustment in value for any

decrease in value that is not attributable to the mere lapse of time. IRC § 2032(a)(3). Such

interests generally include patents, annuities, life estates por otra vie, or other interests that are

24

dependent upon a specific time period or an individual’s life expectancy. Treas. Reg. § 20.2032-

1(f). Further, if the § 2032 election is made, the income tax basis under § 1014(a)(2) is the value

of the property on the applicable alternate valuation date.

Reduction in Value; “All or Nothing”. The alternate valuation date election may not be

made for decedents dying after July 18, 1984, unless it results in the deceased value of the

decedent’s gross estate and the reduction of any estate tax owing. IRC § 2032(c).

Additionally, the alternate valuation date election is essentially an “all or nothing”

proposition, inasmuch as the personal representative is not allowed to pick and choose as to

which properties will be valued as of the date of death and which will be valued as of the

alternate valuation date. The election must be made with respect to all properties comprising the

gross estate, or none at all.

In making such an election, the personal representative must consider the estate as a

whole and not focus on the drastic change in valuation of a single asset. Even though such a

change in value of a single asset may be substantial, the election may not be made unless the

overall value of the entire gross estate has decreased. As such, the personal representative may

elect alternate valuation even though some assets have increased in value, as long as the overall

value of the total gross estate has decreased between the date of death and the alternate valuation

date.

Property Distributed, Sold, Exchanged, or Otherwise Disposed of Within Six

Months After the Date of Death. As stated above, property that is distributed, sold,

exchanged, or otherwise disposed of within six months after the decedent’s date of death is

valued on the date of the distribution, sale, exchange, or other disposition. IRC § 2032(a)(1). As

such, the question then becomes what is the date of the actual distribution, sale, exchange, or

disposition.

The alternate valuation date to be used is generally the date when title passes as a result

of a sale, exchange, or other disposition, so that the property has ceased to form a part of the

gross estate, inasmuch as the economic benefit of the property has been transferred. Treas. Reg.

§ 20.2032-1(c)(1).

Distributed. Property is considered to have been “distributed” upon the occurrence of

the following events:

25

(a) entry of order or decree directing the property’s distribution (if the order or decree subsequently becomes final); (b) the segregation or separation of the property from the estate or trust so that it becomes unqualifiedly subject to the demand or disposition of the distributee; or (c) the actual paying or delivery of the property to the distributee. Treas. Reg. § 20.2032-1(c)(2). Additionally, a trustee’s distribution of trust property, which is includable in the decedent’s

gross estate to a beneficiary of the trust, constitutes a “distribution” under IRC § 20.2032(a)(1).

Treas. Reg. § 20.2032-1(c )(2); Rev. Rul. 73-97, 1973-1 C.B. 404. On the other hand, when a

trustee divides the corpus of a revocable trust (which was includable in the decedent’s gross estate)

into two equal parts to facilitate payment of trust income to life beneficiaries, there is no

distribution, because the original trust still exists, regardless of this division.

Sale, Exchange, Other Disposition. Property may be sold, exchanged, or otherwise

disposed of by the following parties:

(a) the executor/personal representative; (b) trustee or donee to whom the decedent made a lifetime transfer of property, which is included in the gross estate under §§ 2035 – 2038 or § 2041; (c) an heir or devisee to whom title passed by operation of law; (d) a surviving joint tenant or tenant by the entirety; or (e) any other person. Treas. Reg. § 20.2032-1(c)(3).

Further, if property is sold, exchanged or otherwise disposed of under a contract, the

alternate valuation date is the effective date of the contract, which is generally the date the contract

is executed, unless the contract specifies a different effective date. The exception to this rule is

when a contract is not subsequently carried out in accordance with its terms and provisions. Id.

The service has found that even though a decedent’s will directs the personal

representative to sell specific property to a specific party at a set price, if the personal

representative elects the 2032 valuation date, the value to be included in the decedent’s gross

26

estate is the value as of the alternate valuation date, not the price set forth in the decedent’s will.

Rev. Rul. 77-180, 1977-1 C.B. 270.

Property Not Distributed, Sold, Exchanged, or Disposed of. If the property has not been

sold, distributed, exchanged, or otherwise disposed of, then the alternate valuation date for purposes

of § 2032 election is the date six months after the decedent’s date of death. IRC § 2032(a)(2).

It is important to note that if there is no date in the sixth month following the decedent’s date

of death, which numerically corresponds to the date of death, the valuation date is the last day of the

month of the sixth month following the decedent’s death. For example, if the decedent died on

October 31st, the last day for alternate valuation would be April 30th, not May 1st. Handling Federal

Estate and Gift Taxes, 6th ed., § 4.1, p. 4-4 (2000) citing Rev. Rul. 74-260.

Change in Value Due to Lapse of Time. If the value of an interest or estate is affected

merely by the lapse of time, such interest or estate is included at its value as of the date of death,

with an adjustment for any difference in value that is attributable to factors other than the lapse

of time. (See Treas. Reg. § 20.2032-1(f) for examples of such interests or estates, and

calculations of this valuation.)

As such, the personal representative should attempt to link any decrease in property value

to other existing economic forces, and not the passage of time.

Included / Excluded Property. A decedent’s estate is comprised of his or her interest in

all property, real or personal, tangible or intangible, wherever situated, as of his date of death.

IRC § 2031. It is important to note that even if the personal representative elects the alternate

valuation date, the extent of the gross estate is still determined as of the date of death, regardless

of whether there is a subsequent § 2032 election for valuation purposes.

Generally, any interest the decedent held at his date of death, which is includable in the

gross estate under § 2033 or §§ 2035-2042 is valued at the alternate valuation date if the § 2032

election is made.

Property that comprises the decedent’s gross estate as of the date of death will remain

part of the gross estate if the § 2032 election is to be made, even if this property changes in form

during the alternate valuation period. Maass v. Higgins, 312 U.S. 443 (1941); Peoples-Pittsburg

Trust Company v. United States, 54 F.Supp. 742 (W.D.Pa. 1944).

A separate issue exists as to whether property, which was not part of the gross estate as of

the date of death, but was earned, received or accrued during the alternate valuation period is

27

includable in the gross estate. This property often takes the form of accrued interest, rent,

dividends, or stock and is said to be excluded from the gross estate, because it could not have

been identified as property owned by the decedent as of his date of death. Treas. Reg. §

20.2032-1(d).

For example, an interest-bearing obligation, such as a bond or note, may be broken down

into two categories of property that are includable in the decedent’s gross estate at the time of

death. These two categories are:

(a) the principal of the obligation itself, and (b) the interest accrued up to and including the date of death.

Treas. Reg. § 20.2032-1(d)(1). One of these elements of includable property may be separately

valued if the alternate valuation date is elected. However, any interest accruing on this property

after the date of death and before the alternate valuation date is excluded from the decedent’s

gross estate and thus not subject to the alternate valuation method.

Further, if an advanced payment of principal or interest is made between the date of death

and the subsequent alternate valuation period, which has the effect of reducing the overall value

of the principal obligation at the alternate valuation date, such payment will be included in the

gross estate and valued as of the date of such payment. Treas. Reg. § 20.2032-1(d)(1). The

following examples illustrate the inclusion or exclusion of specific property under § 2032

valuation:

(a) Lease Property. Rents for real or personal property, which have accrued to the date of death, are includable in the decedent’s gross estate and may be separately valued on the alternate valuation date. Treas. Reg. § 20.2032-1(d)(2). Conversely, rents accruing after the date of death and during the subsequent valuation period are excluded from the decedent’s gross estate. Id. (b) Prepaid Rents. Prepaid rents in which the decedent had an interest are treated in a similar fashion as advance interest payments, and are deemed to be included in the decedent’s gross estate and may be valued under the alternate valuation method. Id. (c) Non-Interest Bearing Obligations. Non-interest bearing obligations sold at a discount, such as savings bonds, are includable in the decedent’s gross estate to the extent of the principal obligation and the discount amortized to the date of death. Treas. Reg. § 20.2032-1(d)(3). The obligation itself is valued at the

28

subsequent alternate valuation date, without regard to any future increase in value due the amortized discount. Id. (d) Dividends / Stock. Stock held in a corporation, and dividends declared to stockholders of record on or before the decedent’s date of death, but not collected as of the date of death, are includable in the gross estate and may be valued under the alternate valuation method. Treas. Reg. § 20.2032-1(d)(4).

Conversely, dividends from earnings and profits declared to stockholders after the date of death

are excludable, and not to be valued under the alternate valuation method. Additionally,

dividends are excludable and not subject to the alternate valuation method, to the extent that they

are payable from post-date of death earnings of the corporation.

The following examples illustrate the inclusion or exclusion of stock and dividends with

respect to the alternate valuation date:

(a) If a corporation makes a distribution to stockholders of record during the alternate valuation period in partial liquidation, which is not accompanied by surrender of a stock certificate for cancellation, the amount of the distribution received on stock included in the gross estate is itself “included property”, except to the extent that such a distribution was made out of earnings and profits since the decedent’s date of death. (b) If a corporation, in which the decedent owned a substantial interest, and possessed, at the date of the decedent’s death, accumulated earnings and profits equal to its paid-in capital subsequently makes a distribution of all of its accumulated earnings and profits as cash dividends to stockholders of record during the alternate valuation period, the amount of the dividends received on stock includable in the gross estate will be included property under the alternate valuation method. Likewise, a stock dividend distributed under these circumstances is also “included property.” Treas. Reg. § 20.2032-1(d)(4).

Effect on Other Deductions. With respect to other deductions, such as the charitable

deduction under § 2055 or the marital deduction under § 2056, when references are made to the

value of the property at the time of the decedent’s death, this reference is deemed to refer to the

value of the property used in determining the value of the gross estate. Specifically, if the

alternate valuation date is elected, the value “at the time of death” is either six months after the

decedent’s date of death or the date of the property’s distribution, sale, exchange or other

disposition. Treas. Reg. § 20.2032-1(g).

29

Again, this adjustment in valuation may not take into account any difference in value that

is attributable to the mere lapse of time or the occurrence or non-occurrence of a contingency.

Id.

The following example illustrates the effect the § 2032 election has on other estate tax

deductions:

A decedent dies leaving to a qualified charitable organization, property worth $250,000 on the decedent’s date of death, but which increases in value to $300,000 as of six months later. The personal representative may elect the alternate valuation date, and may deduct $300,000 as a charitable deduction under § 2055, at which value he must also include the property in the decedent’s gross estate. Handling Federal Estate and Gift Taxes, 6th ed., § 4.4, p. 4-10 (2000).

Again, the above example illustrates the potential under § 2032 to achieve a higher

charitable deduction by using the increased value as of the alternate valuation date. However, the

overall value of the entire gross estate and any tax owing thereon must be decreased if the § 2032

election is to be effective.

The personal representative’s election of the § 2032 alternate valuation date, does not

affect a deduction for administration expenses under § 2053 (b) or the deduction for casualty

losses under § 2054, to the extent that the § 2032 election does not effectuate a “double dip” in

determining the taxable estate. The following example illustrates this prohibition on “double

dipping”:

M owned a farm. Approximately four (4) weeks after M’s death, a house and a barn on the farm were destroyed by fire. M’s estate incurred a $95,000 uninsured loss as a result of this fire. The executor of M’s estate elects to use the 2032 alternate valuation date. IRC § 2054 normally allows an estate tax deduction for uninsured losses incurred during the settlement of the estate. However, this provision does not apply if the loss is already reflected in the property’s value as reported on the alternate valuation date. Because the farm’s value on the alternate valuation date will reflect the $95,000 decrease in value caused by the fire, M’s estate is not entitled to a separate casualty loss under § 2054. PPC’s Guide To Practical Estate Planning, 8th ed., § 806. p. 806.15 (2001).

Method of Electing Alternate Valuation Date. The alternate valuation method is not

automatically implemented, but must be affirmatively elected by the decedent’s personal

representative. Further, once made, the alternate valuation election is irrevocable. IRC §

2032(d)(1).

30

If the alternate valuation method is to be used, the election may be made only on the

Form 706 estate tax return, and only if this return is filed no later than one year after its due date

(including extensions). IRC § 2032(d)(2).

If the personal representative makes the alternate valuation date election, the Form 706

must set forth the following information:

(a) itemized description of all property comprising the estate as of the date of death;

(b) the value of each item as of the date of death;

(c) an itemized disclosure of any distribution, sale, exchange, or other

disposition of property, and the date of each, which occurred during the six month period after the date of death;

(d) supporting statements as to any distribution, sale, exchange or

other disposition; and (e) the value of each item of property as of the alternate valuation date

elected. Any interest accrued or rents accrued on the date of death and any dividends declared, but not collected, before the date of death must be separately stated. Treas. Reg. § 20.6018-3(3), (6); Treas. Reg. § 20.6018-4(3).

Time for Making Election. Essentially, a personal representative may delay electing

the alternate valuation date until twenty-seven (27) months after the decedent’s date of death.

This result can be accomplished by obtaining a six-month extension of time to file the 706 form,

pursuant to IRC § 6081. This extends the 706-filing deadline until fifteen (15) months after the

decedent’s date of death. Accordingly, the one-year deadline for making the 2032 election,

which is established under IRC § 2032(d)(2), does not begin to run until fifteen (15) months after

the date of death. As a result, the deadline for making a § 2032 election is twenty-seven months

after the decedent’s date of death (i.e., the fifteen (15) months for filing plus twelve (12) months

thereafter.) However, regardless of any extension of time in which to make the § 2032 election,

the date of the election still reverts back to the earlier of six months after the date of death, or the

date of the property’s distribution, sale, exchange, or distribution.

The service has recently granted extensions of time for making the § 2032 alternate

valuation date election when the personal representative of the decedent’s estate acted reasonably

31

in reliance on a professional’s advice and the government’s interest was not prejudiced by the

granting of an extension. Rev. Rul. 2002-5; PLR 200227029; PLR 200203031.

The IRS has ruled that an estate may elect to value the decedent’s assets on the alternate

valuation date and also to elect to value the decedent’s qualified farm property under the rule set

forth in § 2032A. Rev. Rul. 83-31 (see also Rev. Rul 88-89).

XVIII. 2032A Special Use Valuation.

Special use valuation should be considered where the decedent or the decedent’s family

has been actively involved in a farming operation or other trade or business involving real estate,

and it is anticipated that this use will continue for a period of at least ten years after the

decedent’s death through qualified heirs of the decedent.1 In 2012, a qualified 2032A election

may reduce the value of the decedent’s estate by $1,040,000. The successors in interest to the

decedent must realize the risk of recapture during the ten-year recapture period and the practical

limitations on the sale of the property imposed by the risk of recapture. If multiple heirs will

inherit the property, the estate planner should take special caution due the complexities relating

to tax allocation and consent agreements required under IRC § 2032A.

Pre-mortem Qualified Use: Nature and Duration. The decedent must be a citizen or

resident of the United States. IRC § 2032A(a)(1)(A). The real property must be located in the

United States. Id.

The real property must have been used on the date of the decedent’s death for a “qualified

use.” IRC § 2032A(b)(1). A “qualified use” of real property is use as a farm for farming

purposes, or in a trade or business other than farming. IRC § 2032A(b)(2). The term “farm” is

broadly defined to include stock, dairy, poultry, fruit, fur bearing animal and truck farms,

plantations, ranches, nurseries, ranges, greenhouses or other similar structures used primarily for

the raising of agriculture or horticulture commodities, and orchards and woodlands. IRC §

2032A(e)(4).

1 The principal treatise to consult in referencing special use valuation is Estate Planning for Farmers and Ranchers, A Guide to Family Businesses With Agricultural Holdings, 3rd Ed., Donald A. Kelley, David A. Ludtke & B. Steinmeyer, Jr., West Publishing Co., 1999; a concise explanation of the election is also set out in Belcher, Dennis I, “Planning for The Rancher/Farmer”, Estate & Personal Financial Planning, Koren, West Publishing Group, 2001, § 4:13 through 4:31).

32

Qualified use refers to whether the owner’s income from the property depends on the

success of the operation and a cash lease does not qualify. Reg. § 20.2032A-3(a). This

provision, however, has been modified by statute in 1997 to provide that a surviving spouse or

lineal descendant of the decedent shall not be treated as failing to use the qualified real property

in a qualified use solely because such spouse or descendent rents such property to a member of

the family of such spouse or descendent on a net cash basis. A legally adopted child of an

individual is treated as a child of such individual by blood. IRC § 2032A(c)(7)(E).

There must be active farming or some other active business. T.A.M. 9428002. A

qualified use can be established by cash leasing or share crop leasing by the decedent or by the

specified members of the decedent’s family, but not by outsiders who pay a cash lease to the

decedent. See Heffley v. Comm., 884 F2d 279 (CA7 1989); see also Estate of Donahoe v. Comm.,

T.C. Memo 1988-453].

During the eight-year period ending on the decedent’s death, the property must have been

both owned and used for qualified use by the decedent or by a member of the decedent’s family

for periods aggregating at least five (5) years or more. IRC § 2032A(b)(1)(C).

A member of the decedent’s family means an ancestor or a lineal descendant, the spouse

or the spouse of any lineal descendant of the decedent; a legally adopted child of the decedent is

also treated as a child of the decedent. IRC § 2032A(e)(2).

Material Participation – Postdeath Requirements. During the decedent’s life, the

decedent or a member of the decedent’s family must have materially participated in the business