essential 6-monthly finance directors' update - nov/dec 2014

TRANSCRIPT

Finance Directors’

Seminar

December 2014

www.francisclark.co.uk

Chairman’s Welcome

Charles Evans

Partner

www.francisclark.co.uk

Housekeeping

www.francisclark.co.uk

What’s new at Francis Clark ?

British Accountancy

Awards 2014

Corporate Finance

Team of the Year

www.francisclark.co.uk

Francis Clark Export Club

The Francis Clark Export Club is designed

to provide a resource for people who want

to successfully grow their business

overseas

www.francisclark.co.uk

Business Recovery team

Debt recovery services

• Are you concerned about a customer?

• Worst case scenario – is the customer insolvent?

Our Business Recovery team can help

www.francisclark.co.uk

Finance in the South West 2015

Wednesday 25th

February 2015

Exeter Racecourse

Declan CurryBusiness and Economics Journalist

Photo credit: Gill Shaw

www.francisclark.co.uk

Programme

Stephanie Henshaw, Technical Partner

• Current issues in Financial Reporting

Gordon Fox, Tax Partner

• Corporation Tax Update

Liam Dushynsky, VAT Consultant

• Topical VAT Issues

www.francisclark.co.uk

Programme

COFFEE BREAK

www.francisclark.co.uk

Programme

Gordon McCaw, Tax Consultant

• Capital allowances - Use it or lose it!

Richard Wright, Consultant

• Pensions, Pensions, Pensions!

Nick Woodmansey, Corporate Finance Associate

Director

• Current trends in Funding and Transactions

www.francisclark.co.uk

Programme

LUNCH

Current issues in

financial reporting

Stephanie Henshaw

www.francisclark.co.uk

In this session….

Practical

implementation

issues for FRS

102

Coming soon:

other financial

reporting

changes

Intra group issues

Financial

instruments

Deferred tax

Commercial impact

Thresholds for

company size

Small company

reporting

IFRS update

www.francisclark.co.uk

FRS 102 Application recap

First

year end

Transition

Date

Comparative

balance sheet

First Time

Adoption

1/1/151/1/1431/12/15

Today

www.francisclark.co.uk

Case study: Ramsey Group Limited

Overview of conversion process

Potential

areas of

change

Additional

data

required

Commercial

impact

www.francisclark.co.uk

Case study: Ramsey Group Limited

Group Structure

Ramsey

Group

Limited

Moore

Defence

Limited

H&P

Solutions

Limited

Defence

sector

Distribution

operation

Main

trading

companyWholly-

owned

subsidiaries

www.francisclark.co.uk

Ramsey Group Limited:

Financing arrangements

• Intra group balances – trading and financing

• In parent - 10 year bank loan with interest rate swap, covenants on

profit and tangible net worth

• Forward contract for purchases in foreign currency

Note: two key suppliers insure their trade debts

www.francisclark.co.uk

Case study: Ramsey Group Limited

Intra group funding

RGL MDL

H&P

Trading

Trading

Financing

www.francisclark.co.uk

Accounting under FRS 102:

Financing balances

Is the loan

repayable on

demand?

Yes

Record at

amount due

on demand

No Is a market

rate of interest

charged?

Record at

amount due

Yes

No Record at

PV of future

cash flows

Initial discount

affects retained

profit

Is the

company

dormant?

No

Yes

Record at

amount

due

Discount and “unwinding” changes profile of profit

and perception of balance sheet?

www.francisclark.co.uk

Case study: Ramsey Group Limited

Financial instruments

Must identify

types of

instrument

• If hedge transactions to manage

risk, consider whether accounts

should apply hedge accounting

• Separate into “basic” and “non-

basic”

• Consider specific terms - may also

impact on valuation within “basic”

• Classification determines whether

amortised cost (basic) or fair value

(non-basic)

www.francisclark.co.uk

Accounting under FRS 102:

Classifying bank loans – basic or non-basic

• Previously – lots of potential problems

• Now – requirements amended to restrict likelihood of non-basic

• Key elements to classify loan as basic

• No leveraging e.g. x times standard variable rate

• Any index link must be to general measure of price inflation e.g. RPI

• If fixed and variable rates are combined, variable rate must be positive

• Review loan arrangements and terms, including early payment

options

www.francisclark.co.uk

Case study: Ramsey Group Limited

Ramsey Group Limited has a 10 year

loan, taken out in 2007. Interest is

payable at the bank’s standard variable

rate plus 2.5% over the life of the loan.

The bank insisted on an interest rate swap

(to fix interest payments) as part of the

lending. There is a considerable financial

penalty for terminating the swap early.

www.francisclark.co.uk

Case study: Ramsey Group Limited

Analysis of financial instruments

Instrument Classification Ongoing

reporting

Bank loan Basic instrument Carry at amortised

cost

Interest rate swap Non-basic Recognise at fair

value on transition

with

corresponding

(debit?) entry

against reserves.

Adjust fair value

annually via P&L

www.francisclark.co.uk

Accounting under FRS 102:

Hedges and hedge accounting

• Potential solution for profit impact of fair value adjustments on

interest rate swap

• Conditions apply:

• Identify hedged item, risk (bank loan, cash flow or fair value)

• Identify hedging instrument (e.g. interest rate swap, forward contract)

• Document why expected to be effective in managing risk

• Allows offset/ matching of fair value movements via balance sheet until

settlement

• Can apply retrospectively to hedges at Transition Date

www.francisclark.co.uk

Case study: Ramsey Group Limited

Ramsey Limited buys raw materials in sterling,

dollars and euros.

Forward rate agreements are used to manage

foreign currency exposure from purchase to

settlement.

www.francisclark.co.uk

Case study: Ramsey Group Limited

Analysis of financial instruments

Current UK

GAAP

FRS 102

Foreign exchange

forward contract

Use contract value

to translate asset/

liability under

contract

Treat contract and

related transaction

as separate items

Creates potential

mismatch on

“open” contracts at

the year end

www.francisclark.co.uk

Accounting under FRS 102:

Forward contracts

Sell goods Year end Settlement

Sale at

transaction

rate

Debtor at year

end rateGain/loss on

settlement

Loss/gain on fair

valueLoss/gain on fair

value

Gain/loss in

period

Forward contract

Nil

value

Fair

value

Fair

value

www.francisclark.co.uk

Case study: Ramsey Group Limited

RGL holds property for use by group

companies. Rental of property covered in

management charges to subsidiaries

www.francisclark.co.uk

Case study: Ramsey Group Limited

Treatment of

group property

rental

Intra group property rental no

longer excluded from

investment property

Carry investment property at

fair value, adjusting via P&L

in RGL’s own accounts

Not investment property in

group accounts. No fair value

on consolidation. Depreciate

as group asset.

www.francisclark.co.uk

Accounting under FRS 102:

Investment property and distributable profit

Depreciation in

group accounts

No impact as no

distributions

from group

Fair value via

P&L in entity

accounts

Not realised

profit

Good practice:

Memo note to

accounts

www.francisclark.co.uk

Case study: Ramsey Group Limited

Additional

provisions for

deferred tax

Provide deferred tax on all

revaluations and fair value

adjustments, incl acquisitions

and overseas subs.

Provide deferred tax on all

rolled over gains

On transition, recognise

additional provision and adjust

against retained profit/

revaluation reserve as

appropriate

www.francisclark.co.uk

Deferred tax: illustrative impact

£ Comments

At Transition 140,000

Deferred tax on investment

property adjustment

50,000 Parent only,

annual adj.

Deferred tax on rolled over

gains

95,000 Parent and

group

As restated 285,000

At Transition Date accounts disclose:

Deferred tax provided £140,00

Tax on investment property valuation adjustment £50,000

Tax on rolled over gains of £95,000

Impact on balance sheet perception and covenant test?

www.francisclark.co.uk

Determining relevant profit for dividends

31/12/13 31/12/1430/9/14

Dividend

£250k

Relevant

accounts

Retained

profit

£450k

www.francisclark.co.uk

Determining relevant profit for dividends

on adoption of FRS 102

31/12/14 31/12/1530/9/15

Dividend

£250k

Relevant

accounts

Retained profit

under UK GAAP

£450k

Less: FRS 102

adjustments

£275k

www.francisclark.co.uk

Case study: Ramsey Group Limited

FRS 102 and distributable profit

Adjustment Distributable profit impact Non-distributable item

Discount on interest free

intra group finance

Yes – impact +/- depending

on whether parent or

subsidiary

Interest rate swap valuation

adjustment

Yes – if swap is

“underwater”, unless hedge

accounting applied

Fair value adjustments on

forward contracts

Yes – open contracts only.

+/- impact depending on fair

value adjustments v forex

gain/loss

Intra-group investment

property at fair value

Yes – consider memo note

to the accounts to identify

Deferred tax on investment

property valuation

adjustment

Yes – follows fair value

adjustment

Deferred tax on rolled over

gain

Yes – reduces distributable

profit

www.francisclark.co.uk

Coming soon: changes to small company

accounting requirements

• New EU Directive replaces current UK rules

• Implement by 1 January 2016

• Key features include:

• Increase size thresholds for small and medium

companies and groups

• Mandatory restriction on notes to small company

accounts

www.francisclark.co.uk

Key issues: adjusted thresholds for

small companies

Thresholds Currently EU

Minimum

EU

maximum

Potential

UK impact

£m €m €m £m

Turnover 6.5 8 12 10.2

Total assets

(balance

sheet total)

3.26 4 6 5.1

Employees 50 50 50 50

www.francisclark.co.uk

Impact of regulatory change on accounting

regime for small companies

Significant

increases to

thresholds

More small companies

• Less disclosure imposed

• Mandatory restriction on

“local” disclosures

• But still need “true & fair”

• Current FRSSE contains

“excess” disclosure

• FRC proposes to abolish

FRSSE

• FRS 102 measurement &

recognition rules for small

companies

www.francisclark.co.uk

FRS 102 and small companies

First

year end

Transition

dateComparative

balance sheet

First Time

Adoption

1/1/151/1/16 31/12/16

www.francisclark.co.uk

Q: What about the

audit threshold?

A: Not yet…..

www.francisclark.co.uk

Update on IFRS

• No significant changes relevant for 2014/15 accounts

• New rules for revenue recognition – IFRS 15

• APB 1 January 2017

• May affect point at which sales recognised where no contractual right to

payment by customer until completion

• Consider whether current contractual arrangements could affect

recognition point

• Changes to lease accounting still not finalised – will bring all

leases on balance sheet, but when?

Note: none of the above reflected in FRS 102

Corporation Tax

Update

Gordon Fox

www.francisclark.co.uk

Corporation Tax – It’s all about simplification

• One single rate of Corporation Tax with effect from 1

April 2015

• 2015 Election?

• No more Close Investment Companies

• No more “marginal rates”

• Associated Companies - from 1 April 2015 only where a

member of a 51% group.

• Standalone companies no longer ‘associated’.

www.francisclark.co.uk

Corporation Tax Rates

15%

17%

19%

21%

23%

25%

27%

29%

31%

33%

35%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Tax R

ate

Historical Corporate Tax Rates

Main Rate

Marginal Rate

Small Co Rate

www.francisclark.co.uk

Associated Companies – a simplification?

Exemptions from entitlement to claiming the NIC Employment Allowance of

£2,000 for connected companies

If, at the start of the tax year, 2 or more companies are connected with each other

and those companies would otherwise each be entitled to the Employment

Allowance, only one of those companies can qualify for the Employment

Allowance for that tax year.

Where 2 companies are only connected with each other through the attribution of

rights between certain associated persons (e.g. relatives), the connected persons

rule will only apply if the companies in question are substantially commercially

interdependent. For example, when one company gives financial support to

another, they have the same economic or commercial objectives and have

common management, employees and premises.

www.francisclark.co.uk

Associated Companies

Corporation Tax Employers National Insurance

Pre 1 April 2015 Based on Attribution of Rights Based on Attribution of Rights

Post 1 April 2015 New 51% Group Test Based on Attribution of Rights

www.francisclark.co.uk

Profit Extraction – Double Tax Hit

Profit in Company

Tax at 20%

A Limited

Salary

Dividends

Pensions

www.francisclark.co.uk

Profit Extraction – Salary vs Dividends

Salary Dividends

£ £

Available

Profit Pool 100,000 100,000

Bonus 87,873 Corporation Tax 20,000

Ers NIC (13.8%) 12,127 Profits available 80,000

for distribution

Gross Salary 87,873

Income Tax (40%) 35,149 Higher Rate Tax 20,000

National Insurance (2%) 1,757 on Dividend Income

Net Received 50,967 Net Received 60,000

Effective Tax Rate 49.03% Effective Tax Rate 40.00%

www.francisclark.co.uk

Profit Extraction – A new approach?

Pension Dividends

£ £

Available

Profit Pool 100,000 100,000

Pension Contribution 100,000 Corporation Tax 20,000

Profits available 80,000

Tax Free Lump Sum 25,000 for distribution

Balance of Fund 75,000

Income Tax (40%) 30,000 Higher Rate Tax 20,000

Pension "Income" 45,000 on Dividend Income

Net 70,000 Net Received 60,000

Effective Tax Rate 30.00% Effective Tax Rate 40.00%

www.francisclark.co.uk

Points to Note

• Cash flow – dividends vs pensions?

• Corporation Tax relief – wholly and exclusively?

• Funding?

• Spreading?

www.francisclark.co.uk

Spreading…..

Barry, Maurice and Robin are three brothers operating a successful

business. They are all aged in their 50s and have decided to

contribute to the pension fund…..

Each wants the company to contribute £190,000, a total of £570,000.

As the company contribution is more than £500,000 spreading

applies.

½ in first year and balance in year after.

www.francisclark.co.uk

One Step Further………

Einstein Limited is wholly owned by Mr Albert. Einstein Limited

carries out a certain amount of research and development activity.

Mr Albert is involved in the R&D activities and spent 11.1% of his time

in those activities.

Mr A is reaching retirement age and is thinking about how he might

extract sums from his company…..

www.francisclark.co.uk

Profit Extraction – R and D

Pension Tax Comp - Einstein Limited

£

Available

Profit Pool 100,000 Pension Contribution 100,000

Pension Contribution 100,000 Qual. for R&D (11.1%) 11,100

Enhanced R and D 13,875

Tax Free Lump Sum 25,000 deduction (125%)

(Total 225%)

Balance of Fund 75,000

Income Tax (40%) 30,000 Corp Tax Saved on 2,775

Pension "Income" 45,000 Enhanced Credit

Net Received (A) 70,000 Cost to Company (B) 97,225

Effective Tax Rate 28.00%

www.francisclark.co.uk

Autumn Statement

• Direct Recovery of Debts from taxpayer

• Unclear position on IHT and Trusts – Single NRB

• Stamp Duty Land Tax

• UK Resident Non Doms - RBC

• Transfer of goodwill on incorporation – ER

• CGT on disposal of UK residential property by non UK residents

• Diverted Profits Tax – “Google Tax”

www.francisclark.co.uk

Autumn Statement

Proposed changes to Patent Box

Topical VAT

Issues

Liam Dushynsky

www.francisclark.co.uk

Agenda

• Latest VAT changes and cases

• VAT visits - changing behaviour and current trends

• Property transaction pitfalls

www.francisclark.co.uk

Latest VAT changes and cases

Reverse charge

• Relates to certain wholesale supplies of fuel and power

• Many exclusions

• Likely to apply to ROC, CFD and BTG plants

• From 1 July 2014

• Supplier does not charge VAT

• Customer accounts for VAT

• HMRC operating a ‘light touch’ for 6 months

www.francisclark.co.uk

Latest VAT changes and cases

Mini One Stop Shop

• From 1 January 2015 charge VAT of country where customer

belongs

• Applies where

• B2C customers

• In other member states

• Electronically supplied services

• VAT registration in other EU countries

• MOSS means that VAT can be accounted for on a VAT return in

the UK

www.francisclark.co.uk

Latest VAT changes and cases

Recovering VAT on professional services

• BAA Ltd

• Relates to VAT incurred by company set up to take over BAA

• Must be direct and immediate link to taxable supplies in order to

recover input tax

• If holding company will not make taxable supplies no VAT recovery

• Document intentions

• Management agreement

• Minutes of meetings

www.francisclark.co.uk

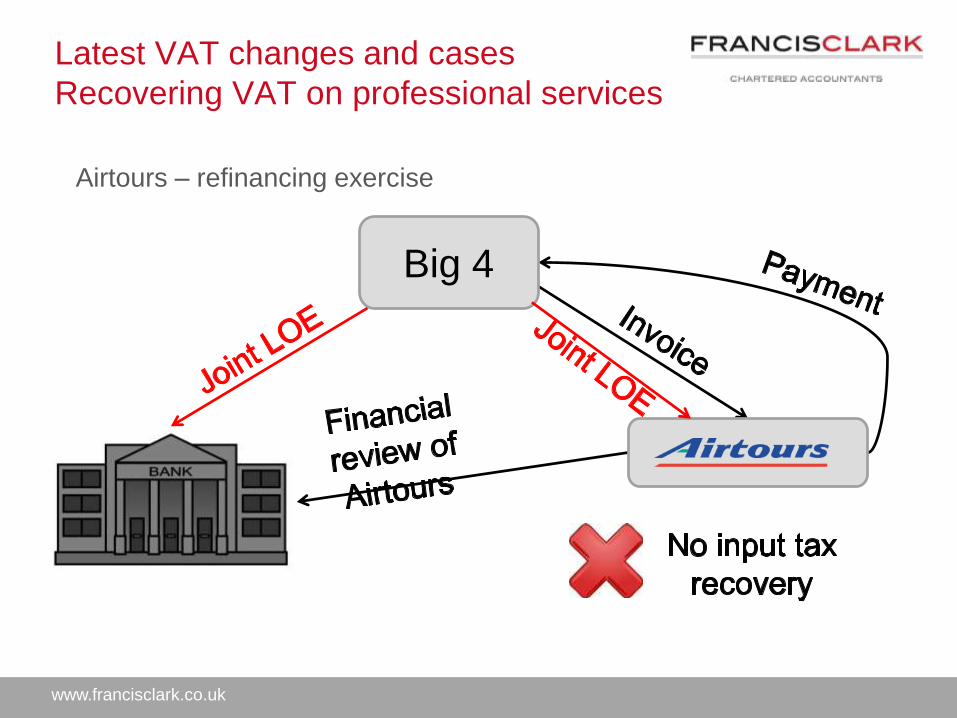

Latest VAT changes and cases

Recovering VAT on professional services

Airtours – refinancing exercise

Big 4

www.francisclark.co.uk

Latest VAT changes and cases

Which party should bear VAT?

• CLP Holding v Singh and Kaur (2014)

• Court of Appeal found that the vendor of an opted property should

bear the VAT

• At the time the property was sold it was not clear that there was an

option to tax and that VAT should be charged

• Contract stated all sums exclusive of VAT

• Special conditions specified purchase price and did not mention

VAT

• Important to ensure that any contract for sale should stipulate

whether the vendor should be indemnified by the purchaser in the

event that VAT is payable

www.francisclark.co.uk

VAT visits

Current trends

• Income with no VAT

• Indirect exports/EC Sales of goods

• Construction industry – correct certificates

• Turnover reconciliations

• Motor dealers

• Interrogation of accounting software

• Disallowance of input VAT where supplier disappeared or insolvent

www.francisclark.co.uk

VAT visits

Changing behaviour

• Unannounced visits

• Options where you disagree with a decision of HMRC

• Review by the same officer

• Review by a different officer

• Appeal to Tribunal

• Recent trend for HMRC to pull out of Tribunals prior to hearings

www.francisclark.co.uk

VAT visits

Changing behaviour - penalties

Reasonable care – 0% Careless - 30%

Deliberate but not

concealed – 70%Deliberate and

concealed – 100%

www.francisclark.co.uk

VAT visits

Changing behaviour - penalties

• Mitigation available where ‘telling, helping and giving’

• Suspension – HMRC will set conditions that must be met

• Professional fee protection cover

www.francisclark.co.uk

Property transaction pitfalls

Surplus property

• Renting surplus commercial property?

• Has an option to tax been made on the property?

• If yes charge VAT n.b. if option to tax made more than 20 years ago it

could be revoked

• If no will the property be used for storage of goods? Rental income will

be standard rated

• If no option to tax and the use is not storage, consider whether an

option to tax should be made

• Without an option to tax the income will be exempt, business becomes

partially exempt

www.francisclark.co.uk

Property transaction pitfalls

Surplus property

• Selling surplus commercial property

• Same considerations as for renting but the figures will be bigger

• If the property is less than 3 years old and the sale will be of the

freehold interest, this is automatically standard rated

• Purchaser could disapply your option to tax if they intend to convert the

property into residential accommodation

www.francisclark.co.uk

Property transaction pitfalls

Buying/renting property

• Establish at an early stage whether VAT will be charged by the

vendor/landlord

• If yes ask for evidence of their option to tax

• If you will not be able to recover VAT charged, could the vendor

revoke his option to tax?

• Unless you are purchasing the property as part of a transfer of a

going concern, SDLT will be payable on the VAT

www.francisclark.co.uk

Property transaction pitfalls

Transferring properties

• No supply between members of VAT group

• Consider VAT position if transferor and transferee are not members

of a VAT group

• If property is gifted for no consideration a VAT charge may still

arise

www.francisclark.co.uk

And finally

VAT and snowballs

www.francisclark.co.uk

COFFEE BREAK

Capital AllowancesUse it or lose it!

Gordon McCaw

www.francisclark.co.uk

What we will consider

• Capital allowances – what are they?

• New rules re fixtures

• 2012 & 2014 changes

• Properties currently owned

• Buying & selling commercial property

www.francisclark.co.uk

What are capital allowances?

• Depreciation in accounts = not tax deductible

• Capital allowances = tax allowable write-off

• Annual Investment Allowance = 100% tax relief

• Writing Down Allowance = 8% or 18%

• If not a fixture or plant then no tax relief until building sold

www.francisclark.co.uk

Annual Investment Allowance

Budget 2014

Period from AIA

1/6 April 2008 £50,000

1/6 April 2010 £100,000

1/6 April 2012 £25,000

1 January 2013 £250,000

1/6 April 2014 £500,000

1 January 2016 £25,000

www.francisclark.co.uk

Annual Investment Allowance

- Commentary

Substantial AIA

• Good news re tax relief on purchase

• Tax volatility re balancing charges

If AIA decreases

• Short life asset elections more important

• Plan timing of spend

www.francisclark.co.uk

AIA: Example

A company has a 31 August year end

What are its AIA limits?

31 August 2015 £500,000

31 August 2016

4/12ths x £500,000 = £166,667

8/12ths x £25,000 = £16,667 NB: Watch timing re spend

Total = £183,333

www.francisclark.co.uk

Fixtures - what properties?

Commercial properties

• Owner-occupied

• Landlords

• Furnished holiday lets

Not applicable to:

• Residential property

• Property developers (but their customers may be interested)

www.francisclark.co.uk

Properties most likely to gain….

Fixture-rich properties include:

• Hotels

• Restaurants/pubs

• Residential homes

• GP or dental surgeries

• Offices

• Furnished holiday lets

www.francisclark.co.uk

Fixtures

• New rules from 2012 & 2014 only relate to fixtures

• Fixtures = plant & machinery installed/fixed to building or land

www.francisclark.co.uk

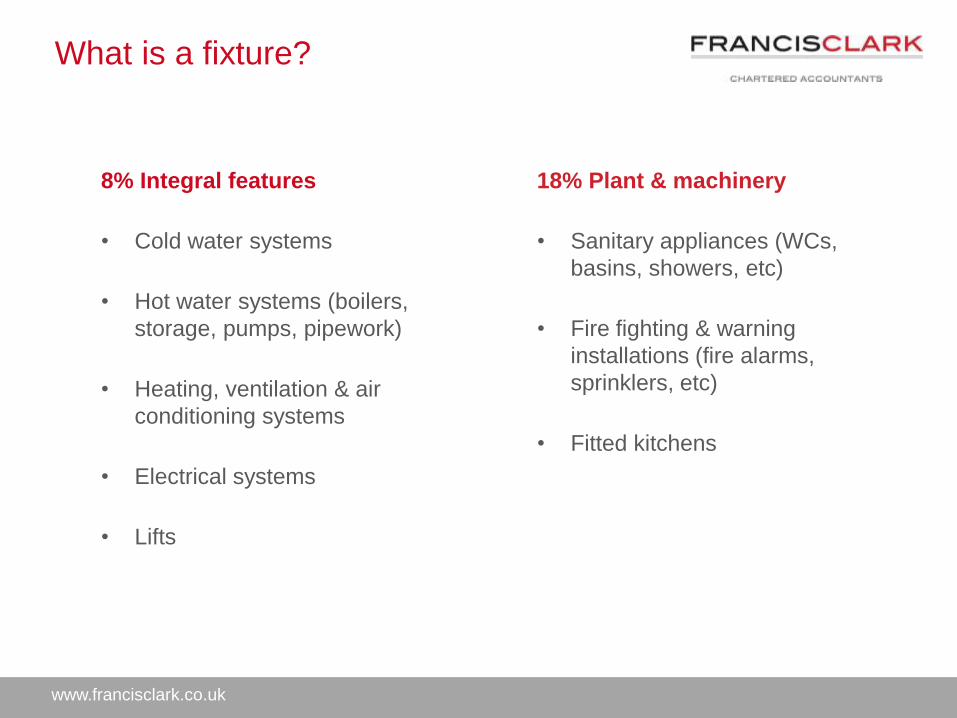

What is a fixture?

8% Integral features

• Cold water systems

• Hot water systems (boilers,

storage, pumps, pipework)

• Heating, ventilation & air

conditioning systems

• Electrical systems

• Lifts

18% Plant & machinery

• Sanitary appliances (WCs,

basins, showers, etc)

• Fire fighting & warning

installations (fire alarms,

sprinklers, etc)

• Fitted kitchens

www.francisclark.co.uk

Example – care home

Company buys a care home for £2m

35% of price paid qualifies as fixtures

Allowances due on £700k

At 20%, allowances worth £140k

For an individual paying 40% tax, could be worth £280k

www.francisclark.co.uk

In the beginning….

Before 2012 – a different landscape

• No time limit to claim capital allowances

• No requirement to “pool” expenditure

• No requirement for an election on sale

• Result

= potential for double claims

= vendor & purchaser may use different figures

www.francisclark.co.uk

Fixtures – first change

From April 2012

• Where vendor has claimed capital allowance

• New “fixed value requirement”

Within 2 years of completion date either:

• Vendor & purchaser agree an election for value of fixtures, or

• First-tier tax tribunal

www.francisclark.co.uk

Fixtures – second change

From April 2014

• Rules have been extended to transactions where vendor could

have claimed capital allowances (even if they have not)

• Vendor will have to ‘pool’ expenditure if any future owner wants

to access tax relief

• Excludes assets not qualifying in vendor’s hands

• Pre-commencement integral features

• E.g. General lighting, general electrics, cold water systems

www.francisclark.co.uk

Fixtures – pooling requirement

If 2012 “fixed value” and 2014 “pooling” requirements are not met:

• Vendor will have to include value of fixtures as a disposal in tax

computation

• Purchaser and any future owner will never be able to claim on

those fixtures

• Irrevocable loss – impact on purchase price?

www.francisclark.co.uk

Properties already owned

• No immediate impact

• Review position

• Bite the bullet sooner or later?

• If tax paid on profits, strong case for claiming allowances now

• Will probably be forced to claim on sale

• Charities & pension funds – importance of obtaining information

www.francisclark.co.uk

Negotiating transactions & due diligence

• Think about capital allowances early

• Commercial issue when negotiating deal

• Use CPSE to flush out relevant information

• CPSE = Commercial Property Standard Enquiries (Q32)

• Onus on purchaser to prove capital allowance history

• Questions often answered incompletely or incorrectly

• Different tactics for vendors than for purchasers

www.francisclark.co.uk

Election – tactics for vendors

• Plan to minimise claw-back of capital allowances

• Objective = keep fixtures value as low as possible

• £1/£2, or

• TWDV – looks ‘neutral’

www.francisclark.co.uk

Election – tactics for purchaser

• TWDV probably too low!

• Late negotiations likely to result in lost relief

• Commercial matter – jeopardise transaction or fight for relief?

• Fixtures valuation exercise

www.francisclark.co.uk

Conclusions

• Consider fixtures in currently owned property

• Property transactions – early planning is key

• Fixtures can be substantial part of property price

• CPSE responses now very important

• Ensure vendor has ‘pooled’ all relevant expenditure

• s198 elections = default position

• Impact if get it wrong now = substantial & irreversible

• From April 2014 – affects everyone buying/selling commercial

property

Pensions, Pensions,

Pensions!

Richard Wright

www.fcfp.co.uk Twitter.com/francisclarkifa

Agenda

• The new Pension Landscape from April 2015

• Case Study – a pension scheme for business

o Purchasing the business premises

o Loan-back to the business

• Auto Enrolment Update

• Summary

• Questions

The New Pension Landscape

from April 2015

www.fcfp.co.uk Twitter.com/francisclarkifa

Pensions in the media – pre-budget

Not always highly thought of…..

www.fcfp.co.uk Twitter.com/francisclarkifa

Pensions in the Media – post budget

• ……. Until now!!!

www.fcfp.co.uk Twitter.com/francisclarkifa

Pension reforms – Flexible Income

From April 2015 - Flexi-access Drawdown (FAD)

available

• Full access to pension funds from age 55

• No compulsion to purchase an annuity

• 25% of the fund still tax free

• Remainder of fund taxed at marginal rate when

drawn

• Existing drawdown pensions can be converted to

FAD

www.fcfp.co.uk Twitter.com/francisclarkifa

Pension reforms – Death Benefits

Beginning April 2015 - New Lump Sum Death Benefit

Tax Charges

• 55% tax rate scrapped

• If pension owner under 75 years old on death there

will be no tax charge on the fund – whether income

has previously been drawn or not.

• If death occurs when over 75 the remaining fund will

be payable to any chosen beneficiary at the

recipient’s marginal rate of income tax (from April 16)

• Reforms make pensions a far more attractive

savings vehicle

www.fcfp.co.uk Twitter.com/francisclarkifa

Pension reforms – Death Benefits

The current tax rules

www.fcfp.co.uk Twitter.com/francisclarkifa

Pension reforms – Death Benefits

Moving forward…

Case Study –

Love Beer Ltd

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study – Love Beer Ltd

• Founded 20 years ago by a husband and wife team

• Successful business that was bought out by senior

employees 2 years ago

• Started as a micro brewery but now expanding and

have won a contract with a major supermarket to

supply bottled beer to 500 of their stores

• Currently lease their production premises from the

original owners of the business. Lease expires

shortly.

• Owns outright a second storage premises/yard

The Company

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study – Love Beer Ltd

Issues to be considered

• New owners wish to sever final ties with previous

owners by moving to new premises

• Larger premises are required in order to fulfil the

new contract and have capacity for further growth

• Capital is needed to invest in a new bottling plant

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study – Love Beer Ltd

• The business owners consulted their Accountants

and Financial Planners to help find a solution to their

needs

• A grouped pension scheme in the form of a Small

Self Administered Scheme (SSAS) proved to be the

answer (SIPP cannot lend)

• They consolidated their individual pension assets

into one scheme with wide ranging benefits

• The business made a contribution of £20,000 to

each of their pension funds (£60,000 total)

What to do?

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study – Love Beer Ltd

One group

pension

scheme

£750,000

Existing

benefits

£250,000

Andrew

Sarah

Robert

£225,000

£275,000

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study – Love Beer Ltd

• The current premises are leased from the original

business owners

• Larger premises needed to fulfil the new contract

• The new pension fund is used to purchase a larger

premises for £500,000 and Love Beer Ltd were

installed as Tenants with a rent of £40,000 per annum

• Business owners now have control over their premises

and the pension fund has a solid return from the rent

Idea 1 Property Purchase

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study – Love Beer Ltd

• £150,000 required to purchase a new bottling plant

• Rather than approach their bank the business owners

took a loan from the pension fund:-

• First Charge on a suitable asset

• 5 year capital repayment basis at 1% above the average base rate

of leading UK banks.

• The pension has;

• funded growth

• gained a good investment (interest on the loan)

Capital to Fuel GrowthIdea 2

Auto Enrolment

Update

www.fcfp.co.uk Twitter.com/francisclarkifa

AE – The story so far

• April 2014 – DWP halves expected opt out rate to

15% - experience to date with large employers

shows 9-10% opt out rate

• August 2014 – Pensions Regulator announces 4

million workers now Auto Enrolled

• Some pension providers showing signs of strain

• Payroll software packages struggling to produce

data compatible with pension scheme providers

systems

www.fcfp.co.uk Twitter.com/francisclarkifa

Looking ahead

Pension

providers

struggled here

What will

happen

here?

Take action

now!

www.fcfp.co.uk Twitter.com/francisclarkifa

AE – The Future

• Plan early – start conversations with your advisers at

least 12 months ahead of staging

• There is a gap between payroll and the pension

scheme

• Data needs to be passed between your payroll

system/provider and the pension scheme

• Records need to be kept, employees need to receive

the right communications at the right time

www.fcfp.co.uk Twitter.com/francisclarkifa

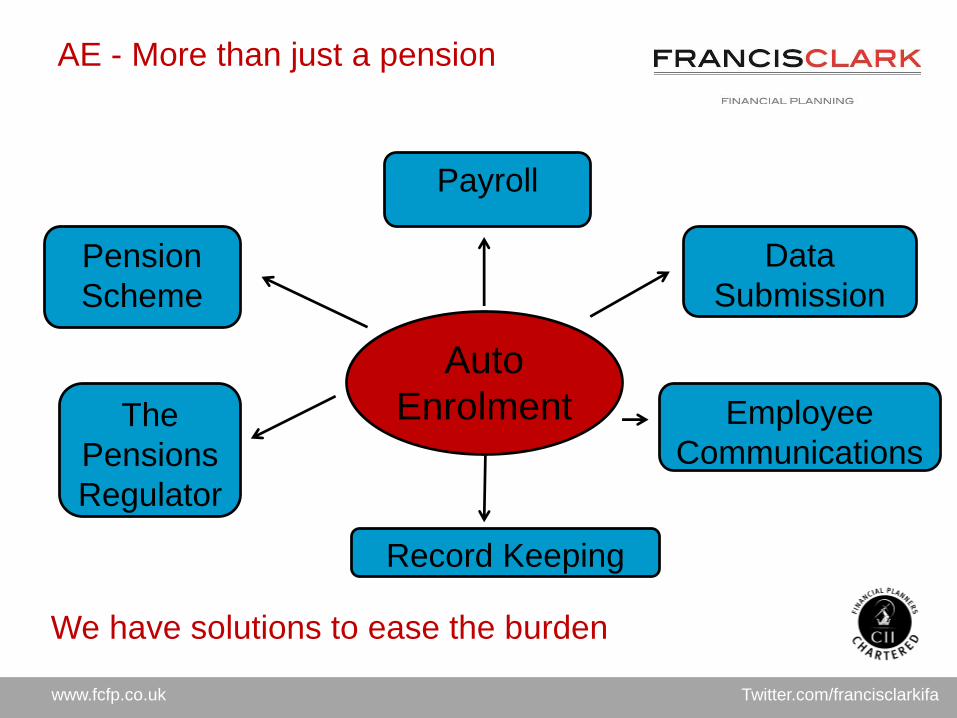

AE - More than just a pension

Auto

Enrolment

Pension

Scheme

Payroll

The

Pensions

Regulator

Employee

Communications

Record Keeping

Data

Submission

We have solutions to ease the burden

Summary

www.fcfp.co.uk Twitter.com/francisclarkifa

Summary

• The new rules for pensions make them much more

attractive to all

• They can form a critical role in the success of a

business

• Company contributions made to the pension attract

corporation tax relief

• The pension fund can be an efficient method of

funding growth

• Plan early for Auto Enrolment

Time to review your own and your business

pension planning?

www.fcfp.co.uk

No responsibility can be accepted for any action taken as a result of information contained in

this presentation. We therefore strongly recommend that no action should be taken before

obtaining detailed professional advice.

Past performance is not a guide to future returns and the value of investments and income from

them may go down as well as up and an investor may not get back the amount invested.

Francis Clark Financial Planning is a trading style for Francis Clark Financial Planning Limited,

which is authorised and regulated by the Financial Conduct Authority.

Registered Office: Sigma House, Oak View Close, Edginswell Park, Torquay, TQ2 7FF.

Registered in England No. 05413603

Exeter Plymouth Salisbury Taunton Tavistock Torquay Truro

This PowerPoint presentation is for general information only and is not intended to constitute professional advice.

Though Francis Clark Financial Planning Ltd is confident on its accuracy, no duty of care is assumed to any direct Recipient of this presentation and no liability is accepted for any

omission or inaccuracy.

Important Statement

Twitter.com/francisclarkifa

Current trends in

Funding and

Transactions

Nick Woodmansey

www.francisclark.co.uk

Overview

• Current Bank/Lending behaviour

• Credit Scoring

• Deal activity and Valuations

www.francisclark.co.uk

Current Bank/Lending behaviour

• Appetite and Leverage

• Rates

• Terms

• Approach/being prepared

• Alternatives

www.francisclark.co.uk

Current Bank/Net lending behaviour

Source: Bank of England

www.francisclark.co.uk

Current Bank/Net lending behaviour

Net lending…

www.francisclark.co.uk

Appetite and Leverage

• All are now “open for Business” – but the definition of

‘Business’ varies!

• Frontline enthusiasm, often not matched by Credit

• Non-financials/reputational risk

• Significant variation in approach/process

www.francisclark.co.uk

Appetite – Bank Process

www.francisclark.co.uk

Appetite – Bank Process

www.francisclark.co.uk

Appetite and Leverage

• Depends on the nature and structure of a transaction

– expansion/acquisition/MBO

• Generally 2.5 - 3X EBITDA

• But competition will drive higher

www.francisclark.co.uk

Rates and Terms

Source: Bank of England

3.00

3.50

4.00

4.50

5.00

5.50Jan…

May

…

Sep…

Jan…

May

…

Sep…

Jan…

May

…

Sep…

Jan…

May

…

Sep…

Jan…

May

…

Sep…

Jan…

May

…Len

din

g ra

te (

%)

SME Lending Rates (margin over base)

All SMEs

www.francisclark.co.uk

Rates and Terms

• Likely to go up –

but not by much for a

while

• Lending documentation

continuing to grow

• Harsh terms for

Borrowers?

• SME negotiating position

generally weak

• Personal guarantees - easy to give, hard to get

back

Source: www.thisismoney.co.uk

Predicted UK interest rate changes:

www.francisclark.co.uk

Current Lending - Alternatives

• P2P continues to grow, as Bank frustration remains

• Bonds

• Mezzanine

www.francisclark.co.uk

Current Lending:

Be properly prepared

A proper proposal will give you a range of benefits:

• Proper consideration by Board/Company

• Strengthens business case

• Easier to market test with other Lenders

• Reduces the overall time and cost

• Can eliminate the need for Due Diligence

• Normally results in reduced interest rates and fees

www.francisclark.co.uk

Credit Scoring

• Affects trading, but also funding and personal rating

• Needs to be proactively managed and considered

• Corporate and personal

• Some changes on the way

www.francisclark.co.uk

Credit Scoring – various impacts

• Transactions

• Changes – debt, preference shares, Director Loans,

shares

• Treatment of items - deferred income

• Timing

www.francisclark.co.uk

Credit Scoring – various impacts

£000's

5,000

700

(300)

(500)

(3,300)

(100)

(3,500)

-

-

1,500

1,500

£000's

Fixed assets 5,000

Current assets 700

Current liabilities

Trade (300)

Directors Loan (500)

Bank Debt (300)

Provisions / Deferred Income (100)

Net current (liabilities)/assets (500)

Long term liabilities

Bank Loan (3,000)

Provisions / Deferred Income -

Net assets 1,500

Share capital and reserves 1,500

£000's

5,000

700

(300)

-

(300)

-

100

(3,000)

(100)

2,000

2,000

www.francisclark.co.uk

Credit Scoring - changes

• Rating ‘lite’ Mid-Market credit product

• FICO changes for Experian, TransUnion and Equifax

www.francisclark.co.uk

Deal activity and Valuations

• YTD UK deal volumes are 3% down on 2013, but

the value of transactions was up 8.5%

www.francisclark.co.uk

Deal activity - SW

• YTD SW deal volumes

are 18.5% down on 2013,

but the value of

transactions was up

163%!

• The number of small

deals (£500K - £10m)

decreased by 18% and

deal value rose by 25%

• Most active Advisors : Legal –

CF –

Foot Anstey

Francis Clark

www.francisclark.co.uk

Deal activity - SW

• BIMBO’s still rarely seen in the SW

• Year of the MBO and FAMBO

• Year of the yoyo?

• Looking ahead – Election, tax changes?, EU

Referendum , Interest rate and quantitative easing

changes….valuations?

www.francisclark.co.uk

Valuations

Note: The above private company PER trend is for UK deals only and differs from the European data shown at www.perda.org

• Average enterprise value £15.1m and EBIT £2.6m

www.francisclark.co.uk

Summary

• Banks are keen – but make them keen for your

business by being properly prepared

• Consider your Credit Rating and what influences it

so that you can improve it

• Don’t stand still – few others are!

www.francisclark.co.uk

Key action

points!

www.francisclark.co.uk

Key action points

Financial Reporting:• Valuation of financial instruments and properties

• Understand the impact on your accounts and

distributable reserves

• Explain impact to stakeholders

Corporation Tax:• Consider the impact of simplification on remuneration

strategies

• Plan for capital allowances and understand pooling

position

• New rules for fixtures

www.francisclark.co.uk

Key action points

VAT:• Do the changes impact your business?

• Be prepared for a VAT visit!

• Identify surplus commercial property

Financial Planning:• Plan to use the new pensions rules effectively

• Plan for early auto enrolment

Funding and Transactions:• Prepare a proper proposal but first understand the

requirements

• Consider the credit score

• Do not stand still!

www.francisclark.co.uk

(c) copyright Francis Clark LLP, 2014

You shall not copy, make available, retransmit, reproduce, sell, disseminate, separate, licence, distribute, store electronically, publish, broadcast or otherwise circulate either within

your business or for public or commercial purposes any of (or any part of) these materials and / or any services provided by Francis Clark LLP in any format whatsoever unless you

have obtained prior written consent from Francis Clark LLP to do so and entered into a licence.

To the maximum extent permitted by applicable law Francis Clark LLP excludes all representations, warranties and conditions (including, without limitation, the conditions implied

by law) in respect of these materials and /or any services provided by Francis Clark LLP.

These materials and /or any services provided by Francis Clark LLP are designed solely for the benefit of delegates of Francis Clark LLP. The content of these materials and / or

any services provided by Francis Clark LLP does not constitute advice and whilst Francis Clark LLP endeavours to ensure that the materials and / or any services provided by

Francis Clark LLP are correct, we do not warrant the completeness or accuracy of the materials and /or any services provided by Francis Clark LLP; nor do we commit to ensuring

that these materials and / or any services provided by Francis Clark LLP are up-to-date or error or omission-free.

Where indicated, these materials are subject to Crown copyright protection. Re-use of any such Crown copyright-protected material is subject to current law and related

regulations on the re-use of Crown copyright extracts in England and Wales.

These materials and / or any services provided by Francis Clark LLP are subject to our terms and conditions of business as amended from time to time, a copy of which is available

on request.

Our liability is limited and to the maximum extent permitted under applicable law Francis Clark LLP will not be liable for any direct, indirect or consequential loss or damage arising

in connection with these materials and / or any services provided by Francis Clark LLP, whether arising in tort, contract, or otherwise, including, without limitation, any loss of profit,

contracts, business, goodwill, data, income or revenue. Please note however, that our liability for fraud, for death or personal injury caused by our negligence, or for any other

liability is not excluded or limited.

Disclaimer & copyright