espm´s brazilian multinationals observatory espm´s brazilian multinationals observatory analysis...

TRANSCRIPT

1

ESPM´s Brazilian Multinationals Observatory

Analysis and Trends Year 1 – Number 1

An overview of 100 Brazilian

multinationals: the search for global markets and consumers

Analysis & Trends Year 1 – Number 1 (October, 2014)

2

Brazilian Foreign Direct Investments have grown strongly in recent years. However,

the number of Brazilian companies operating abroad is still unknown. In 2010, a study

accomplished by Brazilian scholars stated that there were about 95 Brazilian companies

worldwide. Today, an effort made by ESPM’s Brazilian Multinationals Observatory

estimated that there are over 400 Brazilian companies present in 56 countries.

The rise of Brazilian firms abroad points to the need to promote efforts to support

the internationalisation process of these companies. It also points to the necessity of

providing incentives to the development of a global mindset among managers, generating

information for decision -makers and developing guidelines to support government

policies.

In order to contribute to the competi t iveness of Brazilian companies, we present an

overview of 100 Brazilian multinationals.

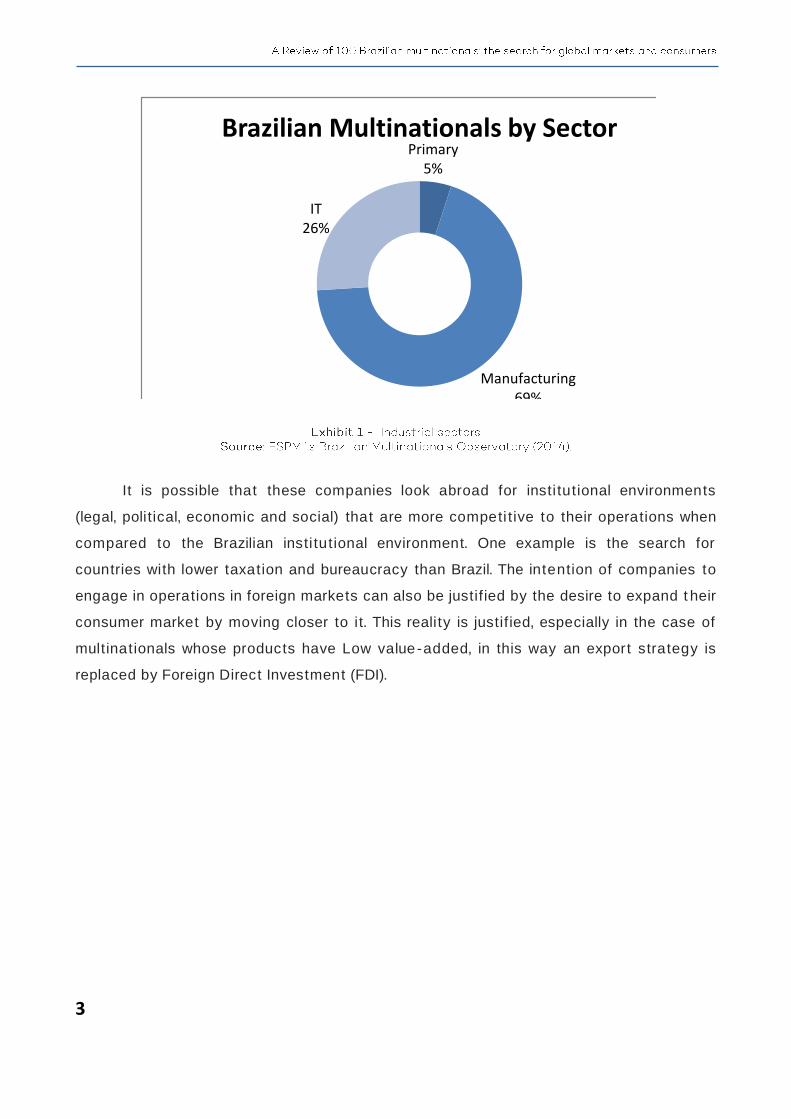

There is a prevalence of manufacturing companies (69%), followed by IT service

firms (26%). The primary/extractive sector represents only 5% of the sample (see Chart 1).

Drivers that motivate international expansion are diverse. For the manufacturing

firms, it is clear that these companies are driven by the search for strategic resources,

such as cheaper labour and natural resources. Another decisive aspect, particularly for

high - technology and medium -high - technology industries, is the search for new

knowledge overseas. This movement can represent an opportunity for improvements to be

incorporated into their products or processes.

3

Primary5%

Manufacturing69%

IT26%

Brazilian Multinationals by Sector

It is possible that these companies look abroad for insti tutional environments

(legal, political, economic and social) that are more competi t ive to their operations when

compared to the Brazilian insti tutional environment. One example is the search for

countries with lower taxation and bureaucracy than Brazil. The intention of companies to

engage in operations in foreign markets can also be justif ied by the desire to expand t heir

consumer market by moving closer to it. This reality is justif ied, especially in the case of

multinationals whose products have Low value -added, in this way an export strategy is

replaced by Foreign Direct Investment (FDI).

4

3%

3%

3%

3%

4%

6%

9%

10%

10%

13%

13%

23%

Rubber and plastic-made goods

Petroleum products

Mineral and non-metallic goods

IT

Wood and wood-made goods

Others

Metal and metal-made goods

Machinery and equipments

Chemicals

Food, beverage and tobacco

Textile, clothing and leather

Motor vehicles and transportation equipments

Secondary industry sub-sectors

Large part of manufacturing firms abroad is operating in the field of motor vehicles

and transport equipment (23%), as shown in Figure 2. For these companies, the

internationalisation driver is the demand for technological knowledge, and the need to be

closer to global competi tors.

In second position within the manufacturing group, there are the Brazilian

multinationals in the sub -sectors of "textiles, clothing and leather" (13%) and "food,

beverages and tobacco" (13%). The internationalisation of these companies is motivated

essentially by the expansion of consumer markets. Firms that produce Low value -added

products can be more competi t ive by adopt ing economies of scale (reducing production

costs and waste).

The significant rise of Brazilian manufacturing multinationals results in part from

the slowdown of industrial activi t ies within the country. Af ter the downturn of Brazilian

national industry, which includes the reduction of profi ts and labour market, the path of

internationalisation turned to be an escape for these companies.

In the tertiary sector, Brazilian multinationals operate mainly in the Information

Technology sub -sector (73%) followed by companies in the construction industry (23%),

5

as shown in Graph 3. The multinationals operating in the provision of other commercial

services account for 4% and essentially work with data trading.

A recent phenomenon in the Information Technology sector is the entry of our

companies in countries whose labour proves to be more cost effective than Brazil, or

where emerging countries’ industry are in full development, for example. By doing this firms

within the industry find new clients. Still, there is a movement to follow customers, that is,

many companies internationalise in order to meet their local customers in foreign markets.

IT73%

Construction23%

Other 4%

Sub-sectors of the tertiary sector

In addition, the entry into Latin American countries allows these firms to serve

customers that share the same language in dif ferent countries.

With regard to the multinationals of the construction industry, their process of

internationalisation is driven by political t ies and knowledge of how to operate in

countries with weak insti tutional infrastructure.

6

Extraction and mining companies (80%) lead primary sector statist ics, as shown in

Graph 4, while companies in the oil and gas extraction sub -sector account for 20% of the

sample. What drives these companies to become international? The search for natural

resources and competit iveness.

Despite this sector being the least significant in terms of the absolute number of

foreign subsidiaries abroad, it is representat ive in terms of capital exchange and size of

the operations overseas.

Extraction and mining

80%

Petroleum and natural gas extraction

20%

Primary sector sub-sectors

7

Concerning the ownership structure of Brazilian multinationals, it is observed that

most of them (63%) do not own shares in stock exchange markets. They are closed

capital companies, as illustrated in Graph 5. In Brazil, this type of company usually belongs

to a few partners. On the other hand, in the last years, a significant portion of Brazilian

firms are opening their capital through stock exchange. This movement pushes companies

to be more transparent and more efficient in terms of managerial practices. We believe, a

gap to be addressed in future studies is related to the understanding of how Brazilian

companies capitalise themselves in order to face internationalisation challenges.

Open37%

Closed63%

Type of capital of Brazilian multinationals

8