eskom 2018/19 revenue application - nersa10).pdf · eskom sales declining due to a combination of...

TRANSCRIPT

Eskom 2018/19

Revenue Application

Nersa Public Hearings

30 October 2017

Where we are coming from

• This revenue application is being made for the year 2018/19, after the EnergyRegulator maintained its revenue decision made in 2013 for the 2017/18 year, whereit approved total allowable revenue of R205 billion.

• The allowed revenue resulted in an average increase of 2.2% due to baseadjustments made in preceding years following approved RCA balances for Eskom(12.69% for 2015/16 for MYPD2 and 9.4% for 2016/17 for first year of MYPD3).

• The 2.2% average increase resulted in consumers receiving an effective decrease inelectricity prices, in a situation where costs to produce electricity are increasing.

• Eskom, in this revenue application for the 2018/19 year has applied the NERSA MYPDmethodology of 2016, with a phasing-in of return on assets being applied

• Allowed revenue and price adjustments decisions will be applicable from 1 April 2018

• This revenue application does not include any RCA applications for the MYPD 3period. Eskom understands that NERSA will process RCAs for years 2, 3 and 4 of theMYPD 3 period at a later stage. The adjustments will be applicable from 1 April 2019onwards in a phased manner

1

Eskom’s revenue application is completed within the legislative and NERSA’s regulatory framework

2

Electricity Pricing

Policy (EPP)

Electricity Regulation

Act (ERA)

Municipal Finance

Management Act

(MFMA)

Multi-Year Price

Determination (MYPD)

Methodology

Eskom Retail Tariff &

Structural Adjustment

(ERTSA) Methodology

Provides guidelines to NERSA in approving prices and tariffs for the

electricity supply industry

• Enable an efficient licensee to recover full cost of its licensed activities,

including a reasonable margin

• Avoid undue discrimination between customer categories

• May permit cross subsidy of tariffs

• Only implement tariffs determined by NERSA

• Eskom consults with SALGA & National Treasury prior to submission to

NERSA

• Municipal tariffs tabled in Parliament by 15 Mar for 1 July

implementation

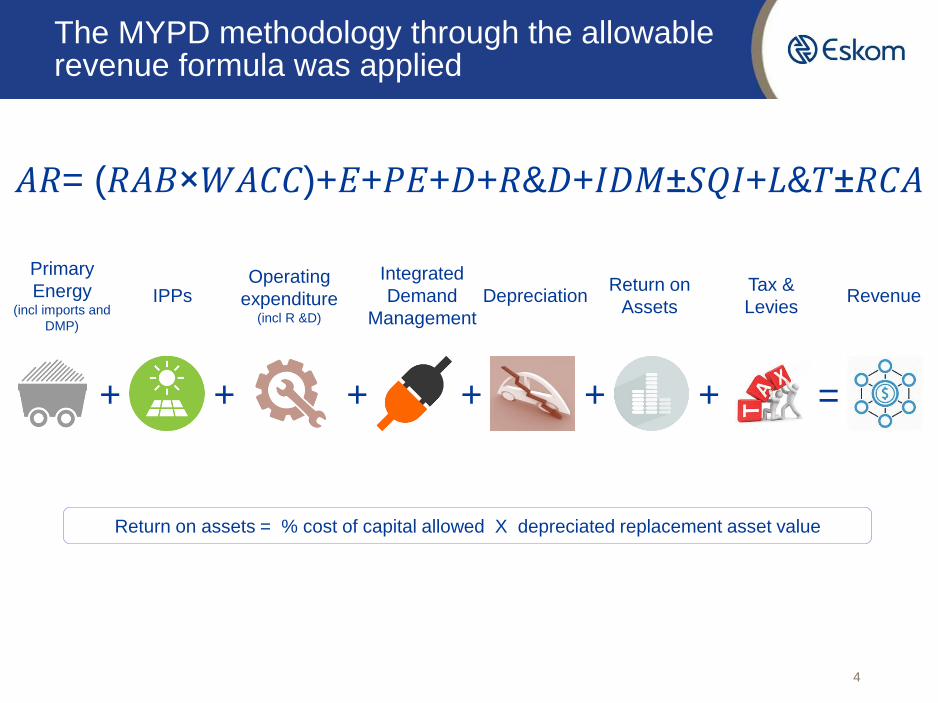

• Determines allowable revenue (AR) for efficient costs and fair return

where 𝐴𝑅 = (𝑅𝐴𝐵×𝑊𝐴𝐶𝐶)+𝐸+𝑃𝐸+𝐷+𝑅&𝐷+𝐼𝐷𝑀±𝑆𝑄𝐼+𝐿&𝑇±𝑅𝐶𝐴• RCA not included in this revenue application

• Allows for NERSA determined allowed revenue to be recovered by the

assumed volume of sales for each year of the revenue period.

• Determines rate adjustments to tariffs applicable to customer groups

and schedule of standard prices applicable to different Eskom tariffs

Notes: Regulatory asset base (RAB); Primary energy (PE); Service Quality incentives (SQI); Expenditure (E); Levies & Taxes (L&T);

Research & Development (R&D); Weighted Average Cost of Capital (WACC); Integrated Demand Management (IDM); Regulatory Clearing

Account (RCA)

Framework Requirements

Electricity Regulation Act is basis of Eskom’s revenue application

In accordance with the Electricity Regulation Act (ERA)

Nersa must:

Enable an efficient licensee to recover the full cost of its licensed activities, including a reasonable margin or return;

Eskom has applied for a revenue that corresponds to

– efficient costs related to it’s licensed activities and

– a phased return that migrates towards a reasonable return

– The phasing-in of the return is in accordance with the previous Nersa decisions

This link between the legislative requirement to Eskom’s revenue application is the Multi-Year Price Determination (MYPD) methodology

3

Depreciation

The MYPD methodology through the allowable revenue formula was applied

4

+ + + + + =

Primary

Energy(incl imports and

DMP)

IPPsOperating

expenditure(incl R &D)

Integrated

Demand

Management

Return on

AssetsRevenue

+

Tax &

Levies

Return on assets = % cost of capital allowed X depreciated replacement asset value

𝐴𝑅= (𝑅𝐴𝐵×𝑊𝐴𝐶𝐶)+𝐸+𝑃𝐸+𝐷+𝑅&𝐷+𝐼𝐷𝑀±𝑆𝑄𝐼+𝐿&𝑇±𝑅𝐶𝐴

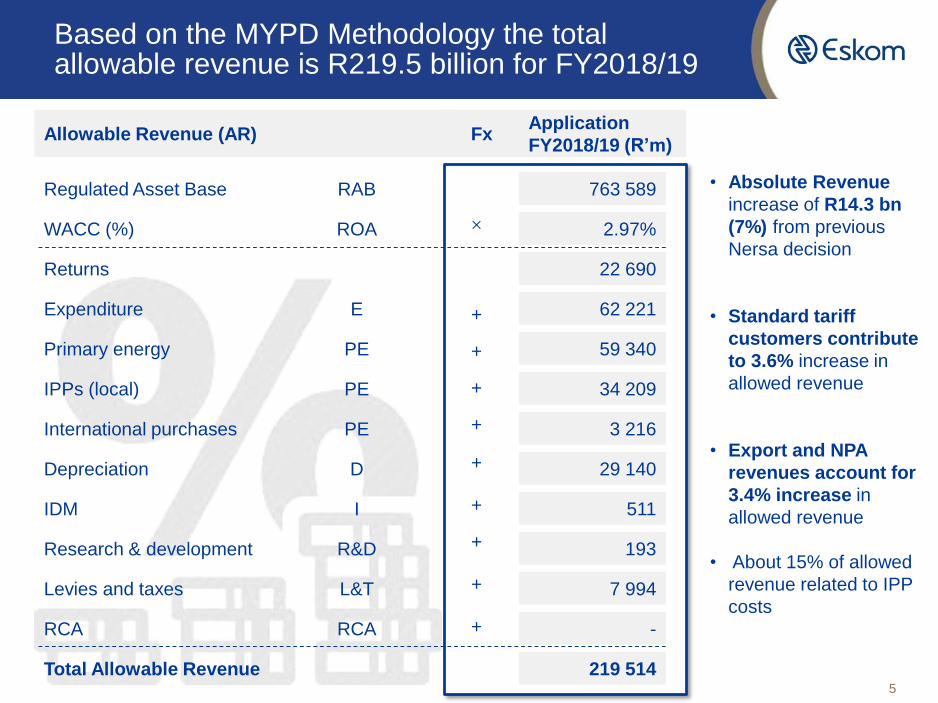

Based on the MYPD Methodology the total allowable revenue is R219.5 billion for FY2018/19

5

• Absolute Revenue

increase of R14.3 bn

(7%) from previous

Nersa decision

• Standard tariff

customers contribute

to 3.6% increase in

allowed revenue

• Export and NPA

revenues account for

3.4% increase in

allowed revenue

• About 15% of allowed

revenue related to IPP

costs

Regulated Asset Base

WACC (%)

Returns

Expenditure

Primary energy

IPPs (local)

International purchases

Depreciation

IDM

Research & development

Levies and taxes

RCA

Total Allowable Revenue

763 589

2.97%

22 690

62 221

59 340

34 209

3 216

29 140

511

193

7 994

-

219 514

×

+

+

+

+

+

+

+

+

+

RAB

ROA

E

PE

PE

PE

D

I

R&D

L&T

RCA

Allowable Revenue (AR) Application

FY2018/19 (R’m)Fx

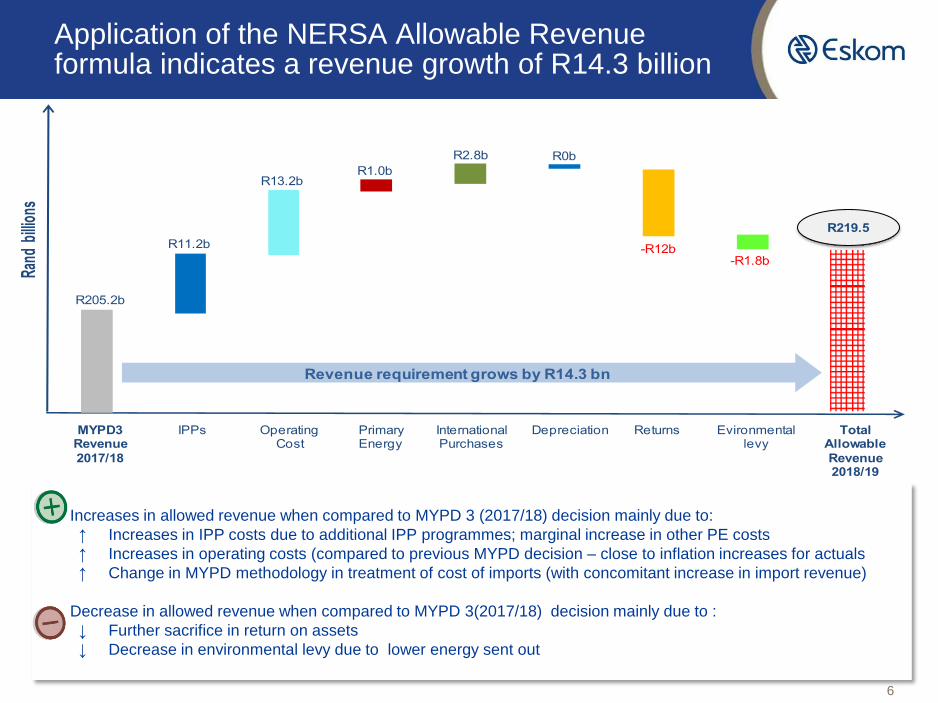

Application of the NERSA Allowable Revenue formula indicates a revenue growth of R14.3 billion

6

Increases in allowed revenue when compared to MYPD 3 (2017/18) decision mainly due to:

↑ Increases in IPP costs due to additional IPP programmes; marginal increase in other PE costs

↑ Increases in operating costs (compared to previous MYPD decision – close to inflation increases for actuals

↑ Change in MYPD methodology in treatment of cost of imports (with concomitant increase in import revenue)

Decrease in allowed revenue when compared to MYPD 3(2017/18) decision mainly due to :

↓ Further sacrifice in return on assets

↓ Decrease in environmental levy due to lower energy sent out

R219.5

MYPD3Revenue

2017/18

IPPs Operating Cost

Primary Energy

InternationalPurchases

R11.2b

Depreciation Returns Total Allowable

Revenue2018/19

Evironmentallevy

Rand

billi

ons

R205.2b

R13.2bR1.0b

R2.8b R0b

-R12b-R1.8b

Revenue requirement grows by R14.3 bn

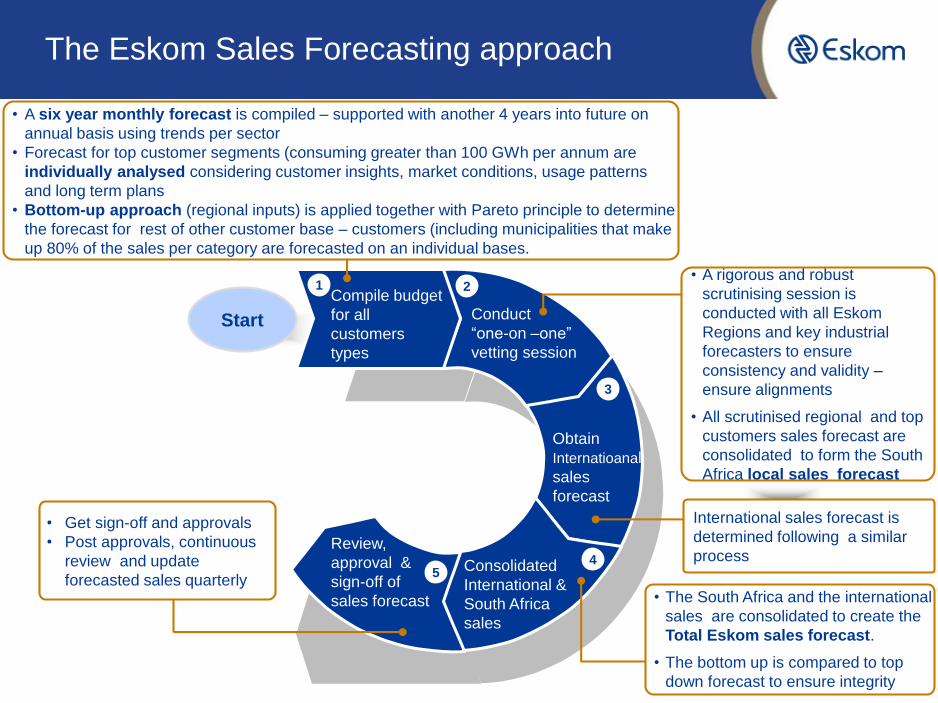

Start

• A six year monthly forecast is compiled – supported with another 4 years into future on

annual basis using trends per sector

• Forecast for top customer segments (consuming greater than 100 GWh per annum are

individually analysed considering customer insights, market conditions, usage patterns

and long term plans

• Bottom-up approach (regional inputs) is applied together with Pareto principle to determine

the forecast for rest of other customer base – customers (including municipalities that make

up 80% of the sales per category are forecasted on an individual bases.

• A rigorous and robust

scrutinising session is

conducted with all Eskom

Regions and key industrial

forecasters to ensure

consistency and validity –

ensure alignments

• All scrutinised regional and top

customers sales forecast are

consolidated to form the South

Africa local sales forecast

International sales forecast is

determined following a similar

process

• The South Africa and the international

sales are consolidated to create the

Total Eskom sales forecast.

• The bottom up is compared to top

down forecast to ensure integrity

1 2

3

45

Compile budget

for all

customers

types

Conduct

“one-on –one”

vetting session

Obtain

Internatioanal

sales

forecast

Consolidated

International &

South Africa

sales

Review,

approval &

sign-off of

sales forecast

The Eskom Sales Forecasting approach

• Get sign-off and approvals

• Post approvals, continuous

review and update

forecasted sales quarterly

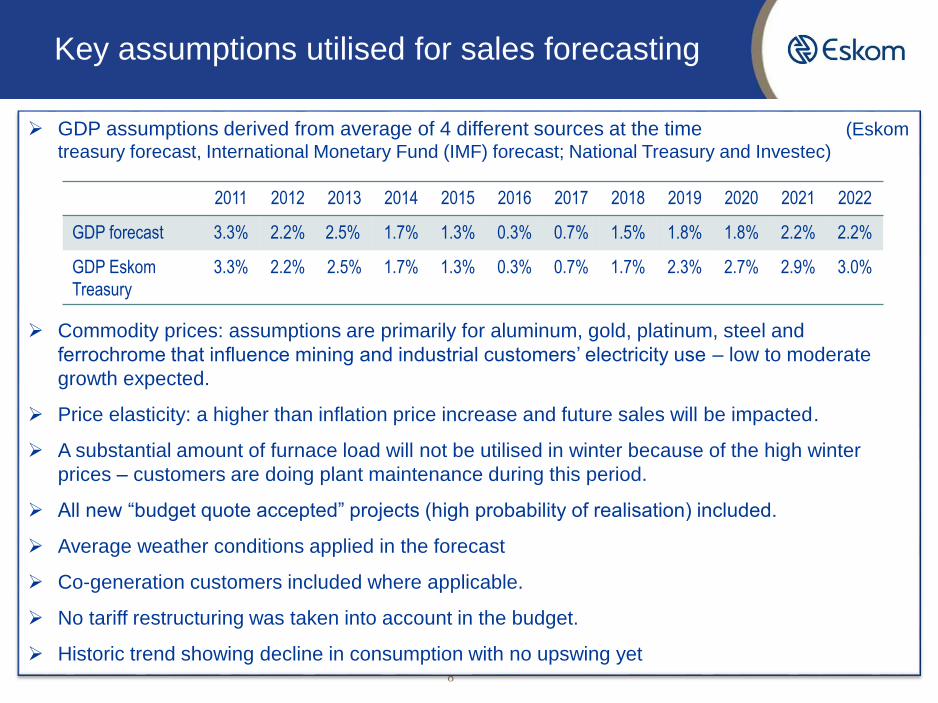

Key assumptions utilised for sales forecasting

8

GDP assumptions derived from average of 4 different sources at the time (Eskom

treasury forecast, International Monetary Fund (IMF) forecast; National Treasury and Investec)

Commodity prices: assumptions are primarily for aluminum, gold, platinum, steel and

ferrochrome that influence mining and industrial customers’ electricity use – low to moderate

growth expected.

Price elasticity: a higher than inflation price increase and future sales will be impacted.

A substantial amount of furnace load will not be utilised in winter because of the high winter

prices – customers are doing plant maintenance during this period.

All new “budget quote accepted” projects (high probability of realisation) included.

Average weather conditions applied in the forecast

Co-generation customers included where applicable.

No tariff restructuring was taken into account in the budget.

Historic trend showing decline in consumption with no upswing yet

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

GDP forecast 3.3% 2.2% 2.5% 1.7% 1.3% 0.3% 0.7% 1.5% 1.8% 1.8% 2.2% 2.2%

GDP Eskom

Treasury

3.3% 2.2% 2.5% 1.7% 1.3% 0.3% 0.7% 1.7% 2.3% 2.7% 2.9% 3.0%

Declining sales trend over MYPD 3 period indicates requirements to rebase sales (technical correction)

9

MYPD3 Sales Decision

Realistic Forecast

Eskom sales declining due to a combination of reasons

10

Although still on par with average international electricity prices, Eskom lost competitive

electricity price advantage (previously lowest cost producer) with recent high price

increases

With the Eskom load shedding there was huge pressure on customers to increase

electricity efficiency; together with load reduction programmes - leading to a decrease in

reliance on Eskom electricity and permanently lost sales (also co-generation)

World economic markets lead to a drop in commodity prices and hence markets for

products for large users - closure of industrial & manufacturing customers; or

plants/shafts

Energy intensive users are mostly global companies who decide on utilisation of plants

from a global perspective – rather using plants with the lowest production unit cost in

countries with the least uncertainty (total package and not only electricity prices)

• all plant capacities not fully utilized

• consideration given to a combination of various aspects of business value chain including skills,

labour stability and costs, transport, infrastructure, etc

• need to compete with countries where Government provides support in the form of incentives

Low investor confidence in South Africa due to political instability, policy certainty,

Government support, ease of doing business and risk management

SA as a country has internationally lost competitiveness

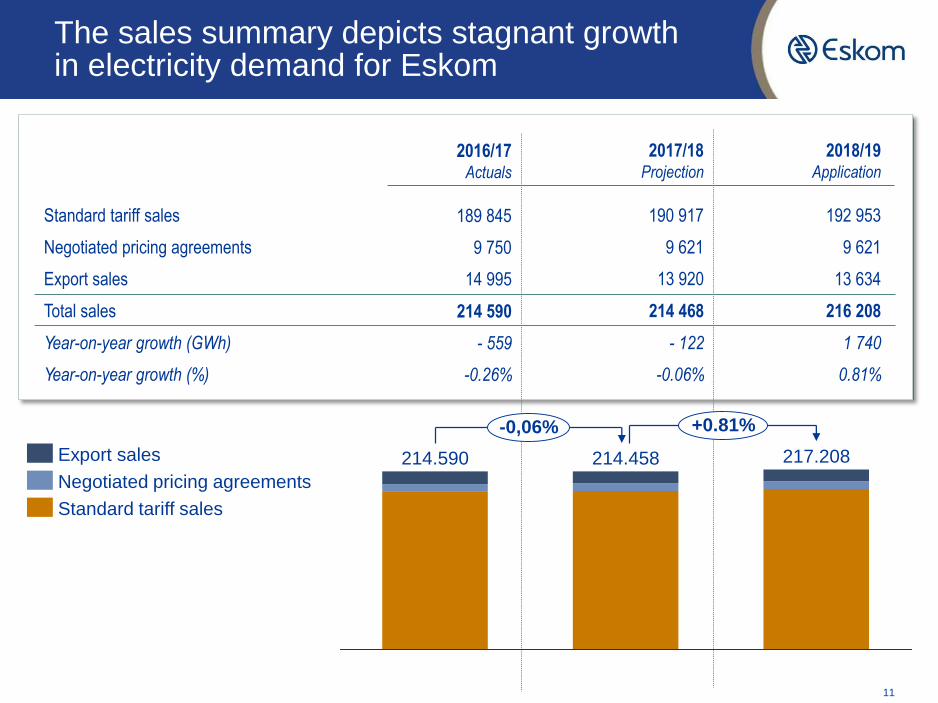

The sales summary depicts stagnant growth in electricity demand for Eskom

11

Standard tariff sales

Negotiated pricing agreements

Export sales

190 917

Total sales 214 468

192 953

9 621

13 634

216 208

2017/18Projection

2018/19Application

9 621

13 920

189 845

214 590

2016/17Actuals

9 750

14 995

Year-on-year growth (GWh) - 122 1 740- 559

Year-on-year growth (%) -0.06% 0.81%-0.26%

214.590

+0.81%-0,06%

214.458 217.208

Standard tariff sales

Negotiated pricing agreements

Export sales

In order to increase sales volumes Eskom has implemented a local demand stimulation strategy

12

Electricity price impact in 2018/19

Standard tariff revenue has increased by R7 251 million which equates to revenue increase of 3.6% from NERSA’s decision for the 2017/18 year.

As the revenue is recouped from a lower sales volume, the overall price increase required is 19.9% for 2018/19.

The 19.9% average increase translates to a 1 July 2018 local-authority tariff increase of 27.5% to municipalities.

– Municipalities continue to pay at the 2017/18 rates for the period 1 April 2018 to 30 June 2018.

– This is due to the Municipal Finance Management Act (MFMA) requiring Municipal tariff changes to be made only from 1 July each year.

13

Standard tariff revenue

Standard tariff sales volumes

Standard tariff price

198 954

Standard tariff price adjustment 2.2%

206 205

192 953

106.87

19.9%

2017/18 2018/19

223 217

89.13

R’m

%

Unit

GWh

c/kWH

Standard tariff

Factors influencing the overall price increase

14

19.9%

30

26

5

GW

hR

26

97

4m R

10

81

2m

Vo

Gro

Sales volumes

rebasing

IPPs International Purchases

9.4%

5.5%

1.4% 16.3%

Price before operating costs

changes

Generationown PE costs

7.0% 0.5% 23.8%

Opex Price after operating

costs

-6.0%

Adjustments Operating costs Depr , Returns , SPAs & Exports

Overall Price

Increase

Pri

ce Im

pact

%

SPAs &Exports

2.1%

Depr &Returns

With average 2.2% increase in 2017/18 and 19.9% proposed average increase in 2018/19

Average for two years is 11%

Even with a 0% increase in Allowable Revenue - rebasing of sales from MYPD 3 results in a 9.4% price increase

15

• The ERTSA methodology does not adjust for volume changes during a MYPD cycle

• It is only at the next cycle that adjustments can be made

• Thus the sales volume gap of about 30TWh would need to be implemented in the 2018/19 decision

• Assuming the same allowed revenue in 2018/19 as was for 2017/18; recovered over lower volume (of

30TWh) results in 9.4% price increase (after primary energy savings) – will not be extreme next time

• MYPD methodology requires recovery of allowed revenue (consisting of fixed and variable costs)

through assumed sales volume

• If sales volume drop the related fixed costs are not recovered (primary energy costs are saved)

• The converse is true if the sales volume is higher than assumed

• Sunk and fixed costs cannot be concomitantly contracted – is nature of electricity industry

22

3.2

19

19

0 9

17

20

6.4

12

20

8.4

42

2015/162013/14 2016/172014/15 2017/18

21

3.5

45

19

4.7

62

19

5.2

58

19

2.0

89

18

9.8

45

21

8.1

94

GWhAct/Proj Std

Tariff sales

MYPD 3

Sales DecisionStandard tariff revenue as at FY18

Savings on PE due to lower sales

Revised standard tariff for FY19

198 954

Standard tariff volumes (GWh) 223 217

Standard tariff ave electricity price

(revenue/sales volumes - c/kWh)

89.13

Price adj for rebasing sales volumes

198 954

-10 812

188 142

192 953

97.50

9.4%

Decision vs actual standard tariff sales Rebasing of sales volumes (R’m)

2017/18 2018/19

Primary energy costs reflects CAGR 8.5% p.a. but the position improves when local IPPs are excluded

16

• Between 2013/14 to 2018/19 , primary energy costs escalate with CAGR of 1.5% p.a.

• Primary energy costs peaked during FY2015 & FY2016 when OCGTs were utilised to

minimise load shedding

• IPPs played vital role during supply challenges – however under the current

environment the growth in IPPs are displacing Eskom power stations

• Total primary energy costs reflects CAGR of 8.7% p.a. once local IPPs are incorporated

𝐴𝑅= (𝑅𝐴𝐵×𝑊𝐴𝐶𝐶)+𝐸+𝑃𝐸+𝐷+𝑅&𝐷+𝐼𝐷𝑀±𝑆𝑄𝐼+𝐿&𝑇±𝑅𝐶𝐴

2014/152013/14

R’’m

2012/13

+8.7%

2018/192017/182015/16 2016/17

IPPs

Gx Primary Energy1.5%

Operating Costs increase by average of 7.3% over the period

17

• Employee benefits- CAGR of 4.9% p.a. from 2013/14 to 2018/19 on back of a

declining staff complement

• O&M costs escalate by CAGR of 7.3% after normalising for once off transactions

• 2019 Opex – Employee benefit of R28.3bn (46%); Maintenance of R17.7bn (29%);

Other opex of R15.8bn (25%)

𝐴𝑅= (𝑅𝐴𝐵×𝑊𝐴𝐶𝐶)+𝐸+𝑃𝐸+𝐷+𝑅&𝐷+𝐼𝐷𝑀±𝑆𝑄𝐼+𝐿&𝑇±𝑅𝐶𝐴

2014/15 2015/16 2016/17 2017/18

7.3%

2018/192012/13

R’m

2013/14

Employee benefits

Operations & Maintenance

4.9%

Conservative assumption have been used for RAB, migration of ROA towards WACC, and depreciation

18

𝐴𝑅= (𝑅𝐴𝐵×𝑊𝐴𝐶𝐶)+𝐸+𝑃𝐸+𝐷+𝑅&𝐷+𝐼𝐷𝑀±𝑆𝑄𝐼+𝐿&𝑇±𝑅𝐶𝐴

• Opening RAB balance for

FY2019 is based on the

MYPD 3 decision which is

then adjusted for the latest

capital expenditure forecasts

for the period FY2014 to

FY2018.

• Eskom will revalue the RAB

for subsequent revenue

application in accordance with

Nersa condonation decision

In accordance with the MYPD

methodology, depreciation is

computed by dividing RAB over

remaining life of respective

assets. Therefore depreciation

amounts have remained

relatively similar to 2017/18 as a

similar RAB value is used for the

FY2018/19 revenue application

• MYPD methodology allows for

ROA as proxy for interest costs,

tax and equity return to the

shareholder

• In accordance with Nersa decision

migration of ROA towards full

WACC is phased over a longer

period.

• NERSA MYPD 3 decision of 4,7%

for FY2017/18 is reduced to

2.97% for FY2018/19 revenue

application.

Assets

Working capital & WUC

Eskom RAB

592 104

171 485

763 589

Regulatory Asset Base (R’m) Return on Assets (R’m) Depreciation (R’m)

Ave RAB

Return on Assets (ROA)

Returns

763 589

8.4%

64 142

Phased in ROA 2.97%

Phased in Returns 22 690

Returns sacrificed -41 452

Generation

Transmission

Distribution

19 062

3 833

6 245

Total Depreciation 29 140Generation

Transmission

Distribution

549 527

109 371

104 691

In conclusion , Eskom will supply electricity which comes at a cost that needs be recovered

• Eskom has delivered R47billion of savings over the first 4 years of MYPD3

• We have continuously been striving to improve operations, commission new capacity assoon as possible and aim to extract cost efficiencies over the period

• Our business contains a substantial element of fixed costs that are not easily reduced in theshort term. This will require a balance of socio economic factors which must be consideredbefore making a final decision

• Eskom’s debt commitments have increased significantly over the last few years with amajor portion that has been guaranteed by Government.

• Our debt maturities reflect a step change in the near term that requires a strong balancesheet to cover these commitments

• Eskom, believes that this revenue application has taking these factors into account in aimingto keep cost escalations close to inflation and phasing in of returns to mitigate impact on thecustomer

19

Thank you