erratum – health insurance supp notes revised format... · the supplementary retirement scheme...

TRANSCRIPT

Copyright reserved by Singapore College of Insurance Page 1 of 32

CHFC02: RISK MANAGEMENT, INSURANCE AND RETIREMENT PLANNING (2ND EDITION, 2012)

Version 1.1 Issued On: 1 December 2014 Note: (1) This Version 1.1 of the amendments below shall apply to any candidate who sits

for the ChFC02 examination as from 2 February 2015 onwards. (2) The next set of amendments, if any, will be issued on 1 October 2015.

Amendments are made to the Risk Management, Insurance And Retirement Planning Study Text (2nd Edition, 2012) as follows:

1. Table of Contents, Page v to vi

By deleting the chapter and section titles and substituting the following:

Chapter 9 – Retirement Funding Chapter Outline 1. Introduction 2. The Central Provident Fund (CPF) 3. The Minimum Sum Scheme (MSS) 3.1 Topping Up The Minimum Sum (MS) 3.2 Deferring Withdrawal Of CPF Funds At Age Of 55 Years 3.3 Increase In Draw Down Age (DDA)

4. Medisave Minimum Sum (MMS) 5. Case Studies – Withdrawal From CPF At Age Of 55 Years 6. Central Provident Fund Investment Scheme (CPFIS) 7. The Supplementary Retirement Scheme (SRS) 8. Insurance 8.1 What Are Annuities? 8.2 How Do Annuities Work? 8.3 Benefits & Limitations Of Annuity Policy 8.4 CPF LIFE Scheme 9. Savings And Investments 9.1 Cash & Cash Equivalents 9.2 Shares 9.3 Derivatives 9.4 Bonds 9.5 Unit Trusts 9.6 Real Estate Investments 9.7 Structured Products 10.How To Help Clients To Overcome Inadequate Retirement Resources 10.1 Reverse Mortgage (RM) 10.2 Lease Buyback Scheme (LBS) 10.3 Right Sizing 10.4 Selling The Flat 10.5 Renting Out Part Of The Flat

Copyright reserved by Singapore College of Insurance Page 2 of 32

10.6 Maintenance Of Parents 10.7 Post-retirement Employment 11.Case Study – How Mr Tan Can Overcome Inadequate Retirement Resources Appendix 9A Appendix 9B

2. Chapter 5, Page 106, Section 2.1.2 Add a new sentence to the last paragraph on Page 106:

“With effect from 1 March 2013, there will be an increase in the Medisave withdrawal limits for MediShield and Integrated Shield Plans premiums from S$800 to S$1,000 (per insured person, per policy year) for those aged 76 to 80 years, and from S$1,150 to S$1,200 (per insured person, per policy year) for those above the age of 80 years.”

3. Chapter 9, Pages 211 to 232

By deleting the entire Chapter 9 and substituting witth Annex 1 of this Supplementary Notes.

Copyright reserved by Singapore College of Insurance Page 3 of 32

Annex 1

CHAPTER 9 RETIREMENT FUNDING

Chapter Outline

1. Introduction

2. The Central Provident Fund (CPF)

3. The Minimum Sum Scheme (MSS)

3.1 Topping Up The Minimum Sum (MS)

3.2 Deferring Withdrawal Of CPF Funds At Age Of 55 Years

3.3 Increase In Draw Down Age (DDA)

4. Medisave Minimum Sum (MMS)

5. Case Studies – Withdrawal From CPF At Age Of 55 Years

6. Central Provident Fund Investment Scheme (CPFIS)

7. Supplementary Retirement Scheme (SRS)

8. Insurance

8.1 What Are Annuities?

8.2 How Do Annuities Work?

8.3 Benefits & Limitations Of Annuity Policy

8.4 CPF LIFE Scheme

9. Savings And Investments

9.1 Cash & Cash Equivalents

9.2 Shares

9.3 Derivatives

9.4 Bonds

9.5 Unit Trusts

9.6 Real Estate Investments

9.7 Structured Products

10. How To Help Clients To Overcome Inadequate Retirement Resources

10.1 Reverse Mortgage (RM)

10.2 Lease Buyback Scheme (LBS)

10.3 Right Sizing

10.4 Selling The Flat

10.5 Renting Out Part Of The Flat

10.6 Maintenance Of Parents

10.7 Post-retirement Employment

11. Case Study – How Mr Tan Can Overcome Inadequate Retirement Resources

Appendix 9A

Appendix 9B

Learning Objectives

After reading this chapter, you should be able to:

Learn about the CPF and its related schemes

Know how annuities work and its importance in retirement planning

Understand the different kinds of savings and investments

Recognise the help available to clients with inadequate retirement resources

Copyright reserved by Singapore College of Insurance Page 4 of 32

1. INTRODUCTION

In this chapter, we will look at the various sources of funds that an individual may draw on

for their retirement use, as well as how you can help your clients who do not have sufficient

retirement resources, to overcome their problems. Let us begin with the Government Schemes

followed by other sources of funds.

2. THE CENTRAL PROVIDENT FUND (CPF)

The Central Provident Fund (CPF) started on 1 July 1955, as a national old age savings plan,

with the simple objective of ensuring that every working individual in Singapore would have

sufficient income to meet basic expenses during their retirement years. The CPF is

administered by the Central Provident Fund Board (CPF Board), a statutory board under the

Ministry of Manpower, in accordance with the Central Provident Fund Act (Cap. 36).

Over time, as the Singapore’s economy progressed, changes were made to the CPF system, to

enable the CPF members to have adequate savings for their retirement. In September 2009,

the CPF LIFE Scheme was introduced to realise the idea of having lifelong retirement income

for the CPF members.

The CPF has evolved into a comprehensive and unique social security savings system

providing not only for retirement needs, but also for healthcare and housing needs of

Singaporeans. Today, the CPF system in providing for the social security of Singaporeans

comprehensively encompasses the five pillars of financial security – retirement adequacy,

home ownership, healthcare, family protection and asset enhancement. We will cover these

pillars later in this chapter.

3. THE MINIMUM SUM SCHEME (MSS)1

The Minimum Sum Scheme (MSS), started on 1 January 1987, aims to help the CPF

members to set aside sufficient savings to support a modest standard of living during their

retirement.

For more information on the MSS, do refer to the CPF Website at: www.cpf.gov.sg

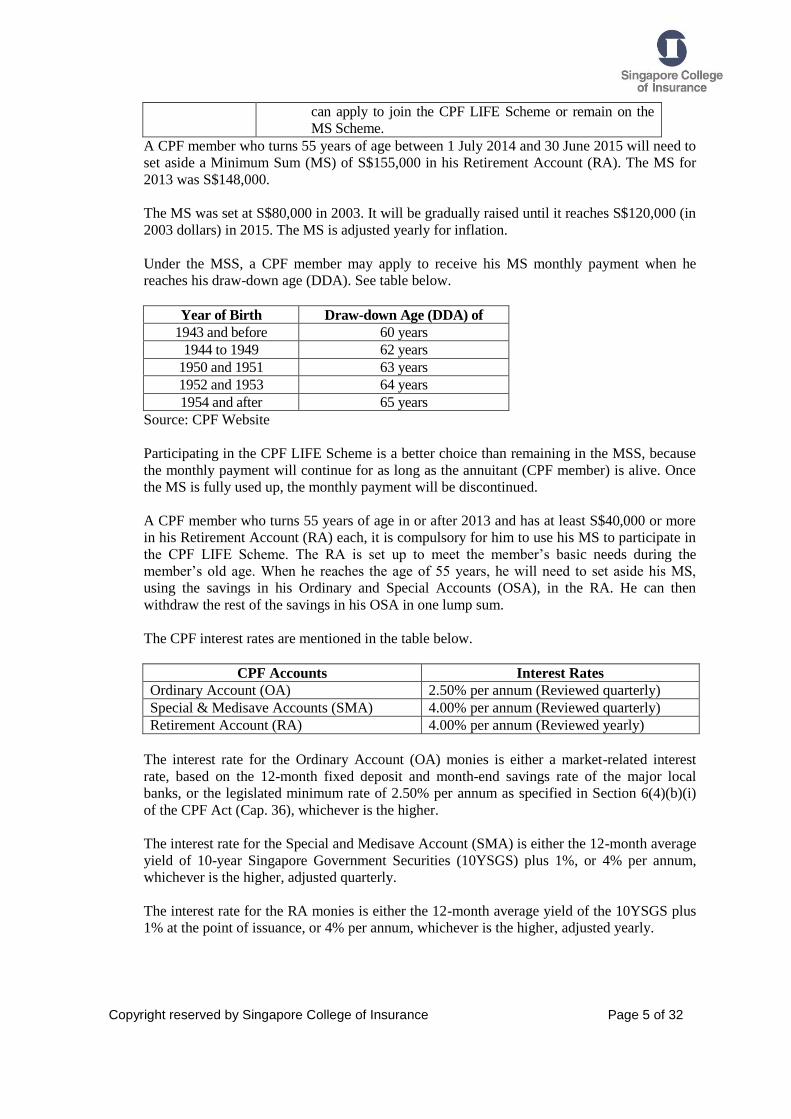

Upon reaching the age of 55 years, the CPF member can use his Minimum Sum (MS) in the

manner as described in the table below.

Birth Year What The CPF Member Can Do

1957 and earlier He can apply to join the CPF LIFE Scheme any time up till

one month before he turns 80 years of age; or

He can remain on the MS Scheme.

1958 and later If he has at least S$40,000 in his Retirement Account (RA)

at the age of 55 years or at least S$60,000 in his RA at the

age of 65 years, he will be placed on the CPF LIFE Scheme.

If he has less than S$40,000 in his RA at the age of 55 years

or less than S$60,000 in his RA at the age of 65 years, he

1 Adapted from www.cpf.gov.sg

Copyright reserved by Singapore College of Insurance Page 5 of 32

can apply to join the CPF LIFE Scheme or remain on the

MS Scheme.

A CPF member who turns 55 years of age between 1 July 2014 and 30 June 2015 will need to

set aside a Minimum Sum (MS) of S$155,000 in his Retirement Account (RA). The MS for

2013 was S$148,000.

The MS was set at S$80,000 in 2003. It will be gradually raised until it reaches S$120,000 (in

2003 dollars) in 2015. The MS is adjusted yearly for inflation.

Under the MSS, a CPF member may apply to receive his MS monthly payment when he

reaches his draw-down age (DDA). See table below.

Year of Birth Draw-down Age (DDA) of

1943 and before 60 years

1944 to 1949 62 years

1950 and 1951 63 years

1952 and 1953 64 years

1954 and after 65 years

Source: CPF Website

Participating in the CPF LIFE Scheme is a better choice than remaining in the MSS, because

the monthly payment will continue for as long as the annuitant (CPF member) is alive. Once

the MS is fully used up, the monthly payment will be discontinued.

A CPF member who turns 55 years of age in or after 2013 and has at least S$40,000 or more

in his Retirement Account (RA) each, it is compulsory for him to use his MS to participate in

the CPF LIFE Scheme. The RA is set up to meet the member’s basic needs during the

member’s old age. When he reaches the age of 55 years, he will need to set aside his MS,

using the savings in his Ordinary and Special Accounts (OSA), in the RA. He can then

withdraw the rest of the savings in his OSA in one lump sum.

The CPF interest rates are mentioned in the table below.

CPF Accounts Interest Rates

Ordinary Account (OA) 2.50% per annum (Reviewed quarterly)

Special & Medisave Accounts (SMA) 4.00% per annum (Reviewed quarterly)

Retirement Account (RA) 4.00% per annum (Reviewed yearly)

The interest rate for the Ordinary Account (OA) monies is either a market-related interest

rate, based on the 12-month fixed deposit and month-end savings rate of the major local

banks, or the legislated minimum rate of 2.50% per annum as specified in Section 6(4)(b)(i)

of the CPF Act (Cap. 36), whichever is the higher.

The interest rate for the Special and Medisave Account (SMA) is either the 12-month average

yield of 10-year Singapore Government Securities (10YSGS) plus 1%, or 4% per annum,

whichever is the higher, adjusted quarterly.

The interest rate for the RA monies is either the 12-month average yield of the 10YSGS plus

1% at the point of issuance, or 4% per annum, whichever is the higher, adjusted yearly.

Copyright reserved by Singapore College of Insurance Page 6 of 32

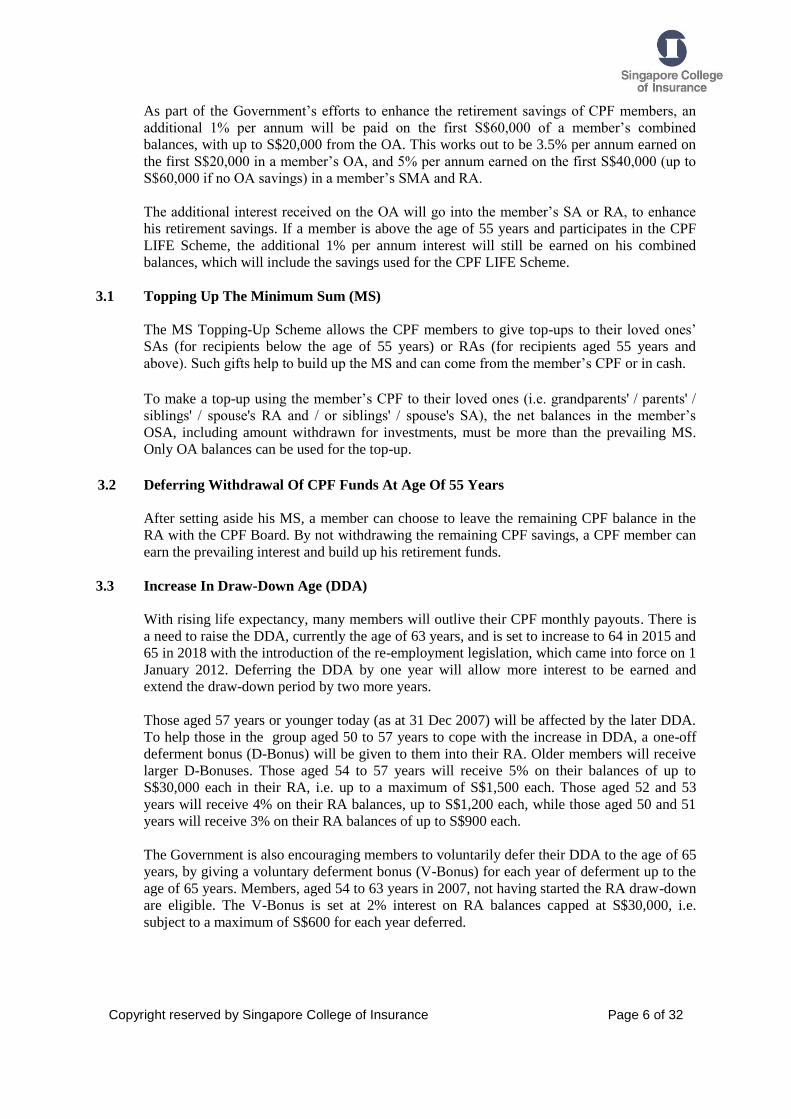

As part of the Government’s efforts to enhance the retirement savings of CPF members, an

additional 1% per annum will be paid on the first S$60,000 of a member’s combined

balances, with up to S$20,000 from the OA. This works out to be 3.5% per annum earned on

the first S$20,000 in a member’s OA, and 5% per annum earned on the first S$40,000 (up to

S$60,000 if no OA savings) in a member’s SMA and RA.

The additional interest received on the OA will go into the member’s SA or RA, to enhance

his retirement savings. If a member is above the age of 55 years and participates in the CPF

LIFE Scheme, the additional 1% per annum interest will still be earned on his combined

balances, which will include the savings used for the CPF LIFE Scheme.

3.1 Topping Up The Minimum Sum (MS)

The MS Topping-Up Scheme allows the CPF members to give top-ups to their loved ones’

SAs (for recipients below the age of 55 years) or RAs (for recipients aged 55 years and

above). Such gifts help to build up the MS and can come from the member’s CPF or in cash.

To make a top-up using the member’s CPF to their loved ones (i.e. grandparents' / parents' /

siblings' / spouse's RA and / or siblings' / spouse's SA), the net balances in the member’s

OSA, including amount withdrawn for investments, must be more than the prevailing MS.

Only OA balances can be used for the top-up.

3.2 Deferring Withdrawal Of CPF Funds At Age Of 55 Years

After setting aside his MS, a member can choose to leave the remaining CPF balance in the

RA with the CPF Board. By not withdrawing the remaining CPF savings, a CPF member can

earn the prevailing interest and build up his retirement funds.

3.3 Increase In Draw-Down Age (DDA)

With rising life expectancy, many members will outlive their CPF monthly payouts. There is

a need to raise the DDA, currently the age of 63 years, and is set to increase to 64 in 2015 and

65 in 2018 with the introduction of the re-employment legislation, which came into force on 1

January 2012. Deferring the DDA by one year will allow more interest to be earned and

extend the draw-down period by two more years.

Those aged 57 years or younger today (as at 31 Dec 2007) will be affected by the later DDA.

To help those in the group aged 50 to 57 years to cope with the increase in DDA, a one-off

deferment bonus (D-Bonus) will be given to them into their RA. Older members will receive

larger D-Bonuses. Those aged 54 to 57 years will receive 5% on their balances of up to

S$30,000 each in their RA, i.e. up to a maximum of S$1,500 each. Those aged 52 and 53

years will receive 4% on their RA balances, up to S$1,200 each, while those aged 50 and 51

years will receive 3% on their RA balances of up to S$900 each.

The Government is also encouraging members to voluntarily defer their DDA to the age of 65

years, by giving a voluntary deferment bonus (V-Bonus) for each year of deferment up to the

age of 65 years. Members, aged 54 to 63 years in 2007, not having started the RA draw-down

are eligible. The V-Bonus is set at 2% interest on RA balances capped at S$30,000, i.e.

subject to a maximum of S$600 for each year deferred.

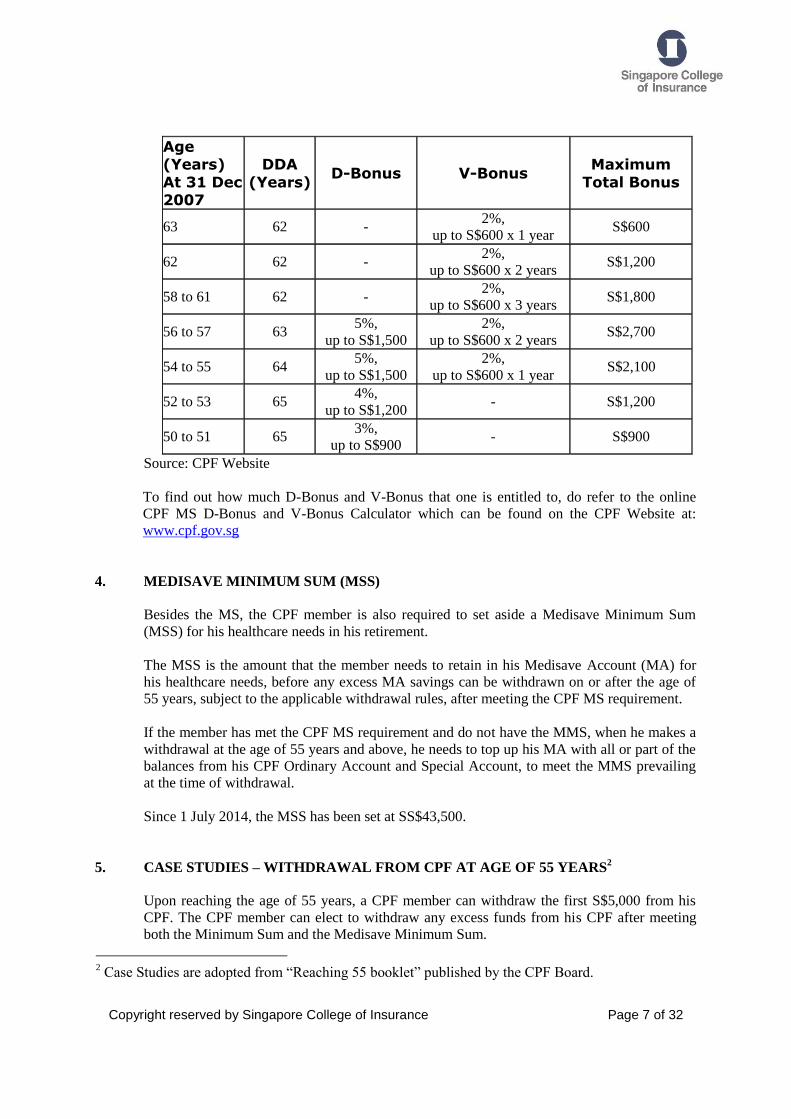

Copyright reserved by Singapore College of Insurance Page 7 of 32

Age (Years)

At 31 Dec 2007

DDA

(Years) D-Bonus V-Bonus

Maximum

Total Bonus

63 62 - 2%,

up to S$600 x 1 year S$600

62 62 - 2%,

up to S$600 x 2 years S$1,200

58 to 61 62 - 2%,

up to S$600 x 3 years S$1,800

56 to 57 63 5%,

up to S$1,500

2%,

up to S$600 x 2 years S$2,700

54 to 55 64 5%,

up to S$1,500

2%,

up to S$600 x 1 year S$2,100

52 to 53 65 4%,

up to S$1,200 - S$1,200

50 to 51 65 3%,

up to S$900 - S$900

Source: CPF Website

To find out how much D-Bonus and V-Bonus that one is entitled to, do refer to the online

CPF MS D-Bonus and V-Bonus Calculator which can be found on the CPF Website at:

www.cpf.gov.sg

4. MEDISAVE MINIMUM SUM (MSS)

Besides the MS, the CPF member is also required to set aside a Medisave Minimum Sum

(MSS) for his healthcare needs in his retirement.

The MSS is the amount that the member needs to retain in his Medisave Account (MA) for

his healthcare needs, before any excess MA savings can be withdrawn on or after the age of

55 years, subject to the applicable withdrawal rules, after meeting the CPF MS requirement.

If the member has met the CPF MS requirement and do not have the MMS, when he makes a

withdrawal at the age of 55 years and above, he needs to top up his MA with all or part of the

balances from his CPF Ordinary Account and Special Account, to meet the MMS prevailing

at the time of withdrawal.

Since 1 July 2014, the MSS has been set at SS$43,500.

5. CASE STUDIES – WITHDRAWAL FROM CPF AT AGE OF 55 YEARS2

Upon reaching the age of 55 years, a CPF member can withdraw the first S$5,000 from his

CPF. The CPF member can elect to withdraw any excess funds from his CPF after meeting

both the Minimum Sum and the Medisave Minimum Sum.

2 Case Studies are adopted from “Reaching 55 booklet” published by the CPF Board.

Copyright reserved by Singapore College of Insurance Page 8 of 32

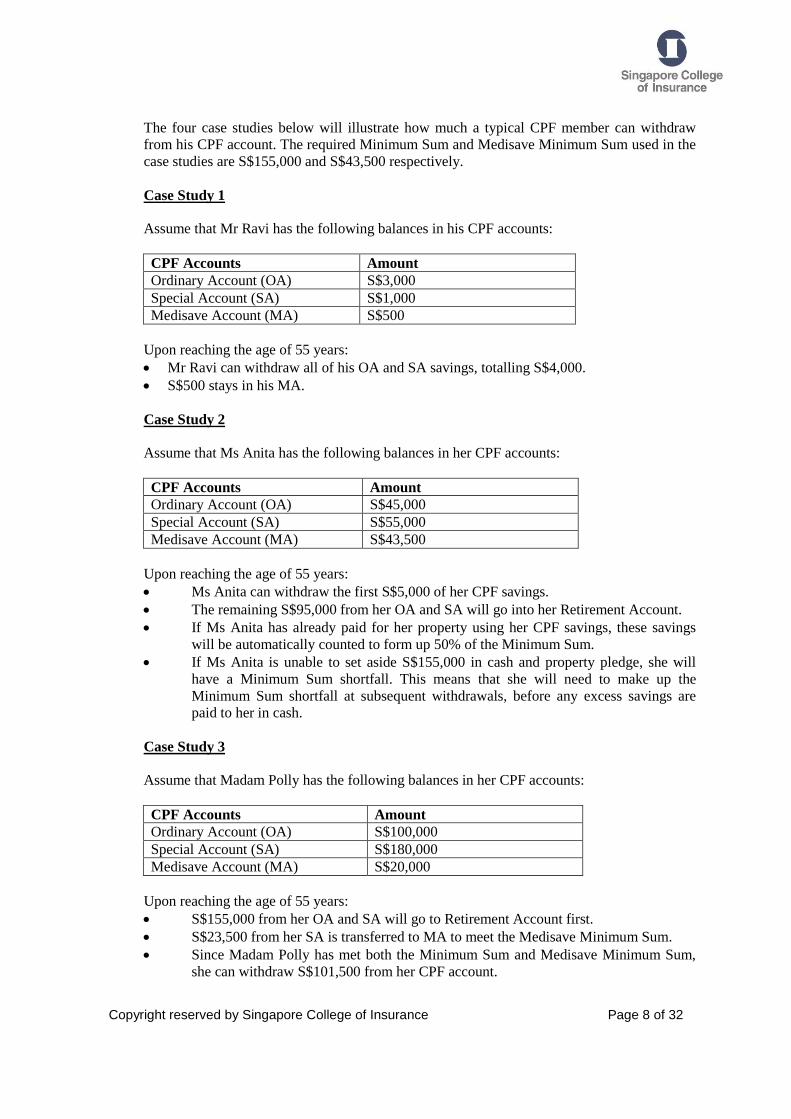

The four case studies below will illustrate how much a typical CPF member can withdraw

from his CPF account. The required Minimum Sum and Medisave Minimum Sum used in the

case studies are S$155,000 and S$43,500 respectively.

Case Study 1

Assume that Mr Ravi has the following balances in his CPF accounts:

CPF Accounts Amount

Ordinary Account (OA) S$3,000

Special Account (SA) S$1,000

Medisave Account (MA) S$500

Upon reaching the age of 55 years:

Mr Ravi can withdraw all of his OA and SA savings, totalling S$4,000.

S$500 stays in his MA.

Case Study 2

Assume that Ms Anita has the following balances in her CPF accounts:

CPF Accounts Amount

Ordinary Account (OA) S$45,000

Special Account (SA) S$55,000

Medisave Account (MA) S$43,500

Upon reaching the age of 55 years:

Ms Anita can withdraw the first S$5,000 of her CPF savings.

The remaining S$95,000 from her OA and SA will go into her Retirement Account.

If Ms Anita has already paid for her property using her CPF savings, these savings

will be automatically counted to form up 50% of the Minimum Sum.

If Ms Anita is unable to set aside S$155,000 in cash and property pledge, she will

have a Minimum Sum shortfall. This means that she will need to make up the

Minimum Sum shortfall at subsequent withdrawals, before any excess savings are

paid to her in cash.

Case Study 3

Assume that Madam Polly has the following balances in her CPF accounts:

CPF Accounts Amount

Ordinary Account (OA) S$100,000

Special Account (SA) S$180,000

Medisave Account (MA) S$20,000

Upon reaching the age of 55 years:

S$155,000 from her OA and SA will go to Retirement Account first.

S$23,500 from her SA is transferred to MA to meet the Medisave Minimum Sum.

Since Madam Polly has met both the Minimum Sum and Medisave Minimum Sum,

she can withdraw S$101,500 from her CPF account.

Copyright reserved by Singapore College of Insurance Page 9 of 32

Case Study 4

Assume Mr Ahmad has the following balances in his CPF accounts:

CPF Accounts Amount

Ordinary Account (OA) S$100,000

Special Account (SA) S$200,000

Medisave Account (MA) S$43,500

Upon reaching the age of 55 years:

S$155,000 from his OA and SA will go to Retirement Account first.

Mr Ahmad can withdraw S$145,000. He has met both the Minimum Sum fully in

cash, and does not need to make a property pledge. He does not have a Medisave

Minimum Sum shortfall as well.

6. CENTRAL PROVIDENT FUND INVESTMENT SCHEME (CPFIS)

The Central Provident Fund Investment Scheme (CPFIS) was first introduced on 1 May 1986.

It now provides CPF members with more options to enhance their retirement savings through

investments. Under this scheme, members can use their CPF savings to purchase any of the

investment instruments approved by the CPF Board. The investment returns are credited back

into the CPF member’s account, and can be taken out only when the member reaches the age

of 55 years.

From 1 July 2010, only monies in excess of S$20,000 in the CPF member’s OA and S$40,000

in the SA can be invested. However, the member can continue to service his regular premium

insurance policies (but NOT recurring single premium insurance policies or regular savings

plans for unit trusts) and agent bank fees, even if the OA balance falls below S$20,000.

7. THE SUPPLEMENTARY RETIREMENT SCHEME (SRS)

The Supplementary Retirement Scheme (SRS) was introduced by the Government on 1 April

2001 as a voluntary scheme to encourage working individuals to save for their retirement,

over and above their CPF savings. The scheme is open to all working individuals who are at

least 18 years of age. These include self-employed individuals and foreigners working in

Singapore. SRS participants will enjoy a range of investment choices in financial assets

(excluding real estate) approved by the CPF Board. They can invest as often, as much or as

little as they like through their SRS accounts, subject to a contribution cap. The contribution

cap is determined by multiplying the appropriate SRS contribution rate by an absolute income

base. The contribution rate for Singaporeans and Permanent Residents will be 15% of their

income, in recognition of the fact that they have no access to the tax benefits afforded by the

CPF schemes. The absolute income base, derived from 17 months of the CPF monthly salary

ceiling, is S$85,000 per annum from 2011 onwards. This amount is subject to change from

time to time.

SRS offers attractive tax benefits. Contributions to SRS are eligible for tax relief, investment

returns are accumulated tax-free [with the exception of Singapore dividends from which tax is

deducted or deductible by the payer company under Section 44 of the Income Tax Act (Cap.

134)], and only 50% of the withdrawals from SRS are taxable at retirement. However, if a

Copyright reserved by Singapore College of Insurance Page 10 of 32

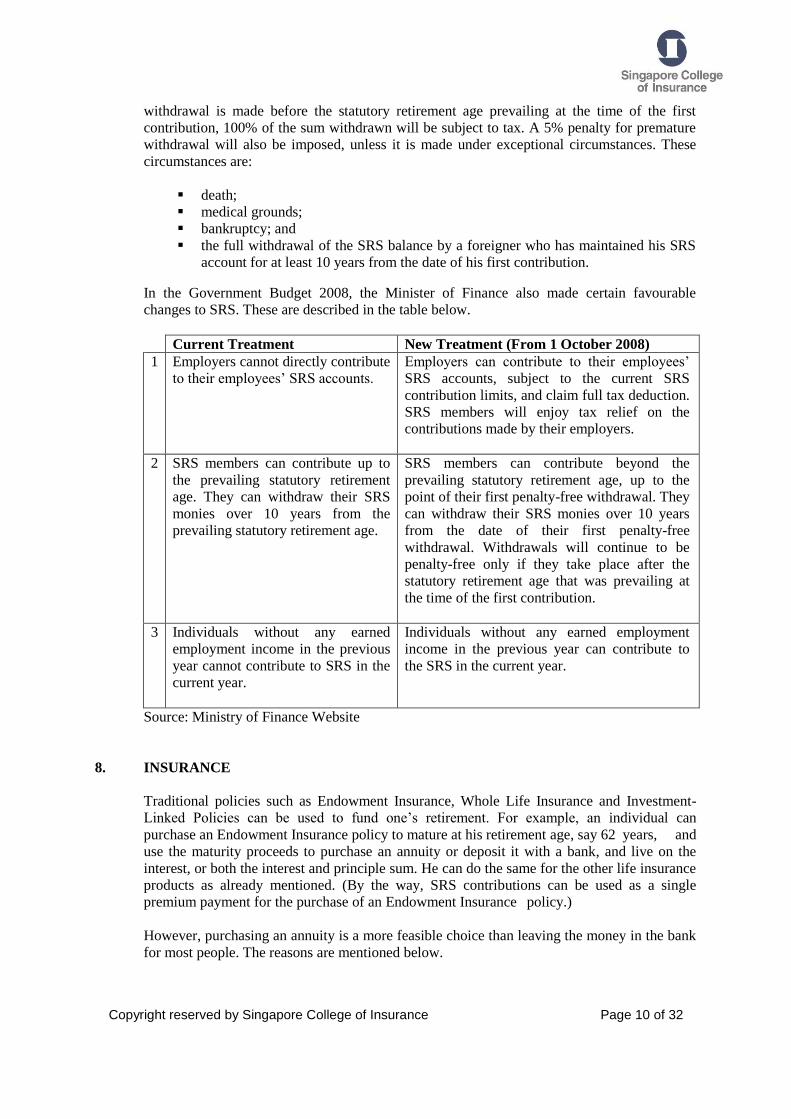

withdrawal is made before the statutory retirement age prevailing at the time of the first

contribution, 100% of the sum withdrawn will be subject to tax. A 5% penalty for premature

withdrawal will also be imposed, unless it is made under exceptional circumstances. These

circumstances are:

death;

medical grounds;

bankruptcy; and

the full withdrawal of the SRS balance by a foreigner who has maintained his SRS

account for at least 10 years from the date of his first contribution.

In the Government Budget 2008, the Minister of Finance also made certain favourable

changes to SRS. These are described in the table below.

Current Treatment New Treatment (From 1 October 2008)

1 Employers cannot directly contribute

to their employees’ SRS accounts.

Employers can contribute to their employees’

SRS accounts, subject to the current SRS

contribution limits, and claim full tax deduction.

SRS members will enjoy tax relief on the

contributions made by their employers.

2 SRS members can contribute up to

the prevailing statutory retirement

age. They can withdraw their SRS

monies over 10 years from the

prevailing statutory retirement age.

SRS members can contribute beyond the

prevailing statutory retirement age, up to the

point of their first penalty-free withdrawal. They

can withdraw their SRS monies over 10 years

from the date of their first penalty-free

withdrawal. Withdrawals will continue to be

penalty-free only if they take place after the

statutory retirement age that was prevailing at

the time of the first contribution.

3 Individuals without any earned

employment income in the previous

year cannot contribute to SRS in the

current year.

Individuals without any earned employment

income in the previous year can contribute to

the SRS in the current year.

Source: Ministry of Finance Website

8. INSURANCE

Traditional policies such as Endowment Insurance, Whole Life Insurance and Investment-

Linked Policies can be used to fund one’s retirement. For example, an individual can

purchase an Endowment Insurance policy to mature at his retirement age, say 62 years, and

use the maturity proceeds to purchase an annuity or deposit it with a bank, and live on the

interest, or both the interest and principle sum. He can do the same for the other life insurance

products as already mentioned. (By the way, SRS contributions can be used as a single

premium payment for the purchase of an Endowment Insurance policy.)

However, purchasing an annuity is a more feasible choice than leaving the money in the bank

for most people. The reasons are mentioned below.

Copyright reserved by Singapore College of Insurance Page 11 of 32

The person may not have the discipline to not over-draw from the account for reasons,

such as going for tours more often than planned. This will cause the principal sum to

deplete faster.

Annuity policies are specially designed to protect one against living too long and

outliving his resources.

Most annuity payments continue to be paid, even though the principal sum (purchased

price) has been exhausted.

Depending on the type of annuity bought, some annuity payments continue to pay out up

to a certain period, or a lump sum to beneficiaries even after the demise of the annuitant.

Let us look at what an annuity is and how it works.

8.1 What Are Annuities?

An annuity is a contract that provides a guaranteed periodic income to the annuitant for life (or a

shorter specified period), with income payments made yearly, half-yearly, quarterly or monthly.

Annuities have sometimes been described as the opposite of life insurance, because life

insurance provides protection against someone dying too soon, while annuities provide

protection against someone “living too long” – living so long as to outlive one’s financial

resources.

Although not strictly a life insurance product, annuities are sold by life insurers in Singapore.

One can either use cash or the CPF Minimum Sum to purchase annuities.

8.2 How Do Annuities Work?

How an annuity policy works is dependent on which category that it falls under. Annuities can

be classified in many different ways, depending on the point of emphasis. Figure 9.1 gives an

illustration of the various ways on how Annuities may be classified.

Copyright reserved by Singapore College of Insurance Page 12 of 32

Figure 9.1: Classification Of Annuities

8.2.1 Number Of Lives Covered

The annuity may cover a single life or more than one life. A contract that covers two or more

lives may be a Joint-life Annuity, or a Joint-and-last-survivor Annuity. The Joint-life Annuity

provides that the annuity income ceases at the first death among the lives covered. A Joint-and-

last-survivor Annuity, on the other hand, provides that the annuity income ceases only at the last

death among the lives covered. Both types of joint life annuity policies are not common here in

Singapore.

8.2.2 Time When Benefit Payments Commence

Annuities can also be classified as immediate or deferred. An immediate annuity makes the first

benefit payment on one payment interval after the date of purchase. For example, if the contract

provides for monthly payments, the first benefit payment is due one month after the date of

purchase. If, on the other hand, the annuitant opts for annual benefit payment, then the first

payment is due one year after the date of purchase. An immediate annuity is always purchased

with a single premium payment.

By parties in the contract

Single Life

Joint Lives

Survivorship

By time when

benefits begin

Immediate

Deferred

By method

of purchase

Single Premium

Instalment Premium

By plan of

distribution

Straight or Pure Life

Guarantee or refund

By amount

of annuity

payment Variable or

equity-indexed

Fixed dollar

Instalment

Period certain

Cash

ANNUITIES

Copyright reserved by Singapore College of Insurance Page 13 of 32

Under a deferred annuity, usually several years will elapse between the date of purchase and the

time when payments commence. During the deferment period, the premiums used to purchase

the annuity earn an investment return. As one ages, the annuity becomes costlier. Annuity

policies approved under the CPF MSS are deferred annuities. The CPF member purchases the

annuity at the age of 55 years using his Minimum Sum, and the annuity payment starts at his age

of 62 years.

8.2.3 Method Of Premium Payment

Immediate annuities must be purchased with a lump sum payment. As for deferred annuities, the

payment may be in a lump sum or by periodic payments. Periodic payments may be scheduled

level deposits or may be flexible deposits, with the amount and timing at the purchaser’s

discretion. Deferred annuities provide an attractive and convenient method of accumulating the

necessary funds for an adequate old age income.

8.2.4 Nature Of The Insurer’s Obligation

(a) Straight Or Pure Life Annuity

A pure annuity, often referred to as a straight life annuity, provides periodic (usually

monthly) income payments that continue as long as the annuitant lives and terminate at the

annuitant’s death. The annuity is considered fully liquidated upon the annuitant’s death,

regardless of how soon that may occur after purchase. No refund is payable to the deceased

annuitant’s estate, and there is no guarantee that any particular number of monthly payments

will be made. This non-refund feature applies to both an immediate and a deferred annuity.

So under a pure annuity, no part of the purchase price will be refunded even if the annuitant

dies during the accumulation period, before the benefit payment commences. However,

some insurers do provide for a refund of all the premiums paid, with or without interest, in

the event of the insured’s death, before commencement of the annuity payment, with no

refund feature after the annuity payment starts.

(b) Guarantee or Refund Annuity

The guarantee or refund feature can be in one of the following forms:

a promise to provide at least a certain number of annuity payments whether the

annuitant lives or dies; or

a promise to refund all or a portion of the purchase price in the event of the annuitant’s

early death.

The three common types of refund annuities are:

Life Annuity Certain; Instalment Refund Annuity; and Cash Refund Annuity.

Life Annuity Certain: This annuity pays a guaranteed number of monthly payments,

regardless of whether the annuitant lives or dies, and payments will continue for the

whole of the annuitant’s life if he lives beyond the guaranteed period.

Instalment Refund Annuity: Under this type of annuity, if the annuitant dies before

receiving the monthly payments equal to the purchase price of the annuity, the payments

Copyright reserved by Singapore College of Insurance Page 14 of 32

will continue to a designated beneficiary or beneficiaries until the full cost is recovered.

As with Life Annuity Certain, the annuity payments continue for as long as the annuitant

is alive, even when the purchase price has been recovered in full.

Cash Refund Annuity: This type of annuity promises at the annuitant’s death, to pay to

the annuitant’s estate or to a designated beneficiary in a lump sum amounting to the

difference, if any, between the purchase price and the sum of the monthly payments.

So far, only these three types of refund annuities have been approved by the CPF Board

under the MSS.

8.2.5 Fixed And Variable Annuities

A fixed annuity pays a fixed amount of annuity benefits on every payment date. A variable

annuity, on the other hand, provides benefits adjusted to changes in the market value of the assets

(typically common stocks and / or bonds) in which the annuity reserves are invested.

The main advantage of fixed annuities lies in their security and low risk. This is to say that,

regardless of the performance of their underlying investments, the annuitant is always assured of

a continuous stream of periodic income, often for a lifetime. Thus, fixed annuities can be ideal

for retirees and other risk-averse people who do not want to subject themselves to the risks of

investment. With fixed rate annuities, you get a certain amount of return on your annuity

investment, without exposing yourself to high investment risk.

Conversely, the downside to fixed annuities is the fact that they offer no room for growth, and

regardless of how well the investments made using your annuity premium performs, you still get

a fixed return from it.

For asset accumulation products that are used as annuities, their main advantage is the room for

growth that they offer, which may potentially translate into significantly higher returns in the

long run. The downside to variable annuities is the fact that they expose the annuitant to the

investment risk. If the investments made using the annuity premium perform poorly, the

annuitant may end up seeing a significantly diminished stream of periodic income from the

annuity.

8.3 Benefits & Limitations Of Annuity Policy

The benefits and limitations of an annuity policy are described below.

BENEFITS

Annuity payout is free from income tax.

It provides guaranteed income.

It provides option for annuitant to pay the purchase price over his working years.

Investment returns earned during the accumulation period are tax-free.

Capital may be guaranteed depending on the types of annuity purchased.

LIMITATIONS

It cannot be used for death protection, and should be purchased only after provision for

premature death is in place.

Copyright reserved by Singapore College of Insurance Page 15 of 32

It cannot be used to provide for major or critical illness protection.

It is not suitable for people in poor health.

It usually does not have any feature to counter the effect of inflation, although some

insurers provide for participation in profits.

8.4 CPF LIFE Scheme3

The CPF Lifelong Income For the Elderly (CPF LIFE) Scheme was first mooted in 2007 by

the Singapore Prime Minister for the need of a lifelong income system for Singaporeans. It is

a scheme that will provide a monthly payout starting from the Draw-Down Age (DDA), for as

long as the CPF member lives.

The CPF member who turns 55 years old from 1 January 2013 and is either a Singapore

Citizen or Permanent Resident will be placed on the CPF LIFE Scheme if he has at least:

1. S$40,000 in his Retirement Account (RA) when he reaches the age of 55 years; or

2. S$60,000 in his RA when he reaches his DDA.

However, if he has already attained the age of 55 years and is not placed on the CPF LIFE

Scheme, he can apply to join CPF LIFE before his 80th birthday.

8.4.1 CPF LIFE Bonus

To encourage and help Singapore citizens born before 1963 to join the CPF LIFE Scheme, the

Government will provide a bonus of up to S$4,000, called the LIFE Bonus (L-Bonus). To

receive the L-Bonus, the CPF member will need to join the CPF LIFE Scheme as shown

below.

If the CPF member was born in: When to join CPF LIFE Scheme?

1955 to 1962 Within 12 months after turning the age

of 55 years

The amount of LIFE Bonus that one receives depends on the annual assessable income (AI)

and annual value (AV) of his property.

The CPF LIFE Payout Estimator at www.cpf.gov.sg can help the CPF member to estimate the

LIFE Bonus that he will receive.

8.4.2 CPF LIFE Plans

There are two CPF LIFE plans, each with a different combination of trade-offs between the

monthly payouts that the CPF member receives and the bequest he leaves for his

beneficiaries:

Plan Type Monthly Payout Bequest

LIFE Standard Plan Higher Lower

LIFE Basic Plan Lower Higher

3 Adapted from www.cpf.gov.sg

Copyright reserved by Singapore College of Insurance Page 16 of 32

A CPF member may choose between the two types of CPF LIFE plans. If he does not choose

a plan within six months from his 55th birthday, he will be automatically placed on the LIFE

Standard Plan.

8.4.3 CPF LIFE Standard Plan

Annuity premiums will be taken from the CPF member’s RA in two instalments.

When the member is 55 years old, the CPF Board will deduct the member’s RA savings up to

the Minimum Sum Cash Component (MSCC) that applies to him as the first instalment of his

annuity premium. The rest of his RA savings will stay in his RA. The MSCC is half of the MS

that applies to him.

One to two months before the CPF member’s DDA, the CPF Board will deduct the rest of his

RA savings as the second instalment of his annuity premium. This will include any new money

that he has built up between his 55th birthday and his DDA. The new money can be from any

CPF top-ups, transferring of funds from other accounts into the CPF member’s RA, interest

earned, or refunds from selling property or investments.

When the member reaches his DDA, he will start to receive monthly payouts from the

annuity fund. The annuity fund is also known as the Lifelong Income Fund. In this context, it

consists of the annuity premium, the interest earned on the annuity premium and the 1%

extra interest earned by members on the CPF LIFE Standard Plan.

8.4.4 CPF LIFE Basic Plan

Annuity premiums will be taken from the CPF member’s Retirement Account (RA) in two

instalments.

When the CPF member is 55 years old, the CPF Board will deduct a small portion (about

10%) of his RA savings as the first instalment of his annuity premium. The rest of his RA

savings will stay in his RA.

One to two months before the CPF member’s DDA, the CPF Board will deduct a small portion

of any new money that has built up in his RA between his 55th birthday and his DDA as the

second instalment of his annuity premium.

When the CPF member reaches his DDA, he will receive monthly payouts (paid from his RA)

starting up until one month before he reaches the age of 90 years. Once he reaches the age of 90

years, he will continue to receive monthly payouts (paid from the annuity fund) for as long as he

lives.

8.4.5 What Happens Upon Death?

Under the CPF LIFE plans, all unused annuity premium and RA savings, if any, will be

refunded after the CPF member’s death. The refund will be paid into the CPF member’s

account and it will be paid, with his remaining CPF savings, to his beneficiaries.

THE CPF LIFE Payout Estimator at www.cpf.gov.sg can help the CPF member to estimate

the bequest that will be left for his nominated beneficiaries.

Copyright reserved by Singapore College of Insurance Page 17 of 32

8.4.6 Case Study4

Mr. Tan’s background

Mr Tan is a Singaporean who will be attaining the age of 55 years in December 2014. He has

S$100,000 in his RA and will be placed on the CPF LIFE Scheme. He can choose between

the two existing plans (the LIFE Standard Plan or the LIFE Basic Plan).

Option 1: If he chooses the LIFE Standard Plan

When Mr Tan reaches the age of 55 years, the CPF Board will deduct S$77,500 (the MSCC

that applies to him) from his RA as the first annuity premium for his LIFE Standard Plan. The

rest of his RA savings (S$22,500) will stay in his RA until his DDA.

About one to two months before Mr Tan reaches the age of 65 years, the CPF Board will

deduct the rest of his RA savings (S$22,500), together with any interest that has built up and

any other new money in Mr Tan’s RA, as the second annuity premium for his LIFE Standard

Plan. This is based on the assumption that Mr Tan does not use or promise to use money from

his RA to buy a property. If he does use money from his RA to buy a property, his monthly

payouts at the age of 65 years will be much lower.

When Mr Tan reaches the age of 65 years, he will receive a monthly payout of between

S$822 and S$908 for as long as he lives. The monthly payout includes the payment from the

two annuities that he bought. The amount of monthly payout that he can receive is based on

the assumption that there is no new money paid into Mr Tan’s RA between the age of 55

years and his DDA (the age of 65 years).

Depending on how old Mr Tan is on the date of his death, his nominated beneficiaries may

receive bequests as illustrated below.

Based on how old Mr Tan

is on the date of his death

Bequest (Estimated)

65 years old S$108,505 to S$109,894

75 years old S$11,909 to S$12,571

85 years old S$0

Option 2: If he chooses the LIFE Basic Plan

When Mr Tan reaches the age of 55 years, the CPF Board will deduct approximately 10% of

S$100,000 from his RA as the first annuity premium for his LIFE Basic Plan. The rest of Mr

Tan’s RA savings will stay in his RA until his DDA.

Between the age of 55 years and his DDA, Mr Tan can have new money paid into his RA.

The CPF Board will deduct approximately 10% of this new money from the RA as the second

annuity premium about one to two months before Mr Tan’s DDA.

When he reaches the age of 65 years, Mr Tan will receive an estimated monthly payout of

between S$737 and S$815 from his RA until his 90th birthday. The amount of monthly payout

4 The following case study is adopted from the “CPF LIFE: Retire With Peace of Mind” by the CPF

Board.

Copyright reserved by Singapore College of Insurance Page 18 of 32

that he can receive is based on the assumption that there is no new money paid into his RA,

other than the 1% extra interest between his 55th birthday and his DDA (65th birthday). When

he reaches the age of 90 years, he will start to receive an estimated monthly payout of

between S$737 and S$815 from his LIFE annuity. The monthly payout includes a payout of

about S$50 from the extra interest which is paid from the RA, for as long as it is being earned.

Depending on how old Mr Tan is on the date of his death, his nominated beneficiaries may

receive bequests as shown below.

Based on how old Mr Tan

is on the date of his death

Bequest (Estimated)

65 years old S$146,080 to S$153,009

75 years old S$105,914 to S$112,305

85 years old S$48,151 to S$50,886

8.4.7 Considerations

As a new scheme, many people would have queries as to whether they should join the CPF

LIFE Scheme and which plan to select. This includes your clients who are eligible to join now

and needs to make their choice. For those who turn 55 years old in year 2013, it is mandatory

for them to participate in the CPF LIFE Scheme if they have more than S$40,000 each in their

RA. As a professional financial consultant, advising your clients on the CPF LIFE Scheme

should form part of the retirement planning process, as making the wrong choice could have

serious repercussions for your clients in their retirement years. The clients should know that,

once entered into the CPF LIFE Scheme, they could not change plans or withdraw. Listed

below are some areas for consideration on whether they should join the CPF LIFE Scheme

and, if yes, which plan to choose:

a. How much bequest does the client wish to leave for his beneficiaries (if any)?

b. The amount of monthly payout desired by the client?

c. The client’s financial health.

d. The client’s balance in his RA and the amount of funds that the client is investing in the

CPF Life Scheme (if he chooses to).

e. The age at which the client is participating in the CPF LIFE Scheme.

f. Does the client have any pre-existing illnesses that may possibly shorten his life

expectancy?

g. Does the client have other needs that potentially forbid him to join the CPF LIFE

Scheme?

h. Does the client have better options available for investment?

9. SAVINGS AND INVESTMENTS

This is yet another source of income for retirement. It can provide both income streams and a

lump sum cash amount for the client’s retirement. Investment instruments available to investors

include:

cash and cash equivalents;

shares;

derivatives;

Copyright reserved by Singapore College of Insurance Page 19 of 32

bonds;

unit trust;

real estate (property) investments; and

structured products.

Let us look at each of them in turn.

9.1 Cash & Cash Equivalents

Cash and cash equivalents are assets that are highly liquid and practically risk-free. It

includes:

cash;

savings deposits;

fixed deposits; and

money market funds.

This type of investment provides the lowest returns of all financial instruments. The interest

earned is fixed and can provide an income stream to the investor, or be left with the bank.

However, as the interest is fixed, this asset is subject to inflation risks. Note that there is no

scope for capital appreciation for investments in cash equivalents.

9.2 Shares

Shares (also known as common stocks) are financial securities that represent ownership

interests in a corporation. They may be purchased from the Singapore Stock Exchange (SGX)

through a broker or online using an Internet account opened with a selected stock broking firm.

People buy shares for two main reasons as appended below.

to receive income in the form of dividend paid by the corporation. This is the income stream

that the investor receives; and

to obtain capital gain through buying at a low price and selling at a high price. Selling the

shares will provide the investor with a lump sum of cash.

Shares are appealing to investors because of the substantial return opportunities that they

offer. This is because they generally provide attractive, highly competitive returns over the

long term. However, investment in shares is a risky venture. It is subject to different types of

risks which include business and financial risk, purchasing power risk, market risk and

possibly event risk.

As a retiree, it is important to understand that not all kinds of stocks may be suitable, since the

ability to absorb losses is lower, assuming that there is no employment or passive income and

a shorter remaining life span. The list that follows describes some of the more common

categories.

Growth Stocks: This refers to stocks of companies whose sales and earnings are expanding

faster than the general economy and / or other stocks. These companies are usually

aggressive, and they plough back most of its earnings for future expansion. Therefore, they

usually pay little or no dividend. Investors buy these types of stocks for capital appreciation.

They are usually very volatile and risky, but may offer huge returns in the short run. As such,

retirees should normally steer clear of this category of stocks.

Copyright reserved by Singapore College of Insurance Page 20 of 32

Income Stocks: These are stocks of companies that consistently pay higher than average

dividend yields. When economic conditions become uncertain, investors become more

attracted to the dividends of these stocks. Most blue-chip companies usually belong to this

category. Retirees are likely to be more attracted to such stocks for their relatively lower

volatility.

Defensive Stocks: Such stocks are regarded as stable and comparatively safe, especially in

periods of recession, or decline in a particular sector. Examples are shares of utilities, food

and drug companies whose businesses remain largely unaffected in a downturn. These kinds

of shares are suitable for retirees too.

Cyclical Stocks: On the opposite end of defensive stocks are cyclical shares. Stocks of such

companies usually fluctuate sharply with the economy owing to the positive correlation

between its earnings and the business cycle. Examples of such companies are semiconductor

and automobile manufacturers. Such stocks tend to be high risks and are not suitable for

retirees.

Even though income stocks may be suitable for most retirees, it is also not advisable to purely

invest in stocks from only this category. Diversification is often the best bet, since the old

adage of, “never put all your eggs in one basket”, still holds true. The concept and benefits of

diversification will be examined in a later chapter.

9.3 Derivatives

Two common types of derivatives in the Singapore market are Options and Warrants. A lot of

investors get confused about Options and Warrants, since they are quite similar. Both offer

the investor the right, but not obligation, to buy or sell an underlying share and a fixed / strike

price. Both also come with an expiration date. However, that is where the similarities end. If a

retiree is interested in investing in Derivatives, the financial consultant will need to advise his

client of the high risk nature of such instruments and to exercise extreme caution.

In fact, Options and Warrants have certain distinct differences. These differences are

discussed below.

9.3.1 Contracting Parties

Stock options are contracts between a person or institution owning a stock and another person

who either wants to buy or sell those stocks at a specific price. In this aspect, stock options are

just like the option that you sign when you buy a house from a seller of that house. It is a

contract between a party who owns the stock, through purchase from the open market, and

another party who wishes to buy that stock from the writer of the options contract. It is

essentially a contract between two investors. Also, listed companies often issue stock options

to their senior employees as an incentive.

Warrants, on the other hand, are contracts between investors and the bank or financial

institution, issuing those warrants on behalf of the company, whose stocks in which the

warrants are based. When you buy warrants, it is these financial institutions selling it to you

and, when you sell warrants, it is these same financial institutions buying from you and not

another investor. Companies issuing warrants do so, in order to encourage the sale of their

shares, and to hedge against a reduction in company value owing to a drop in their company

share price.

Copyright reserved by Singapore College of Insurance Page 21 of 32

9.3.2 Exercise & Delivery

Stock options are either American style, allowing the investor to exercise at any time during

the life of the options, or European style, allowing the investor to exercise only on expiration.

Warrants which are only European style are automatically exercised during expiration if they

are in the money (i.e. strike price less current price for Call Warrants). Remember, the issuers

of warrants are the issuing banks directly representing the companies issuing the shares.

These companies win as long as their shares get sold and capital raised. This would be unlike

stock options, where the investors selling the options, could lose significant amounts of

money, when call options that they wrote get in the money and then subsequently exercised.

9.3.3 Pricing

As warrants are only European style, its extrinsic value is significantly lower than that of

American style stock options. American style stock options have higher extrinsic value owing

to the added benefit of allowing the holder to exercise the options at anytime during the life of

the stock options.

9.4 Bonds

A bond is a debt security issued by a government or a company to raise funds to finance the

expenditures or investment activities. The bond issuer is a borrower, while the bondholder is a

lender or investor. In issuing the bond, the bond issuer promises to pay the investor interest

(known as coupons) over a specified period of time and the principal sum at maturity. The

interest yield that an investor gets is dependent on the credit risk of the bond issuer. The

higher the credit risk, the higher the interest paid by bond issuers, in order to attract investors.

Bonds appeal to investors for a number of reasons. Firstly, bonds pay investors a regular

stream of income called coupons. These coupons are generally higher than the interest earned

on bank savings and fixed deposits. It is mandatory for the bond issuer to pay the coupons at

regular fixed intervals until the bond matures. For bonds with a high yield, reinvestment risk

may be present. This is so, as during maturity or coupon payouts, the investor may not be able

to find other investments generating equal or higher yield with the same risk profile.

Secondly, investors who are very risk averse may feel more secure investing their hard-earned

savings in bonds than in stocks. The volatility of bond investment is generally much lower

than that of stock investment. However, this does not hold true for all kinds of bonds. Retirees

who are generally risk averse should be investing their savings into high grade bonds.

Standard & Poor’s (S&P) and Moody’s are two credit rating agencies which assess the credit

worthiness of a corporation’s debt or bond issues.

Thirdly, investors may enjoy capital appreciation from bond investments. Capital gains are

obtained if bonds are bought at prices lower than what they are eventually sold. Unlike

coupons which are taxable, capital gains from bond investments are tax-exempt in Singapore.

Lastly, investing in bonds allows the investor to accumulate a target sum of money over the

medium or long term, by reinvesting or accumulating the coupons. There may be instances

where the bond appreciates in value before maturity, and the investor is able to liquidate to

enjoy capital gains. Examples of such objectives include saving for a child’s education and

building a nest egg.

Copyright reserved by Singapore College of Insurance Page 22 of 32

Do note that bonds are not as liquid as shares, and the client may have problem selling them

at the time of his retirement. If the purpose of the retiree is to generate regular income from

the bonds, the liquidity of the bond may not be a serious issue.

9.5 Unit Trusts

A Unit Trust is a tripartite arrangement made up of the fund manager, trustee and unit holders.

The fund manager pools the funds received from the unit holders who buy into the funds, and the

fund manager invests them in bonds, stocks and sometimes cash equivalents. The trustee

safeguards the rights and interests of the investors. The trustee will ensure that the fund manager

abides by the investment mandate, assumes legal ownership of all assets belonging to the unit

trust and holds them in trust for the unit holders. Although a Unit Trust has the advantage of the

expertise of the fund manager, as well as the spreading of risk by diversification, it does not mean

that there is no risk involved. In fact, the dividend payouts, as well as the risks and volatility of a

Unit Trust, are all dependent on the underlying assets. This is to say that, if the underlying asset

comprises more of shares, the fluctuation in the risk and return will be more drastic.

Note that Unit Trusts can be easily liquidated for additional income, if required.

Unit Trusts come in a myriad of investment objectives and are usually classified according to

the sector and region that it is investing in. Unit Trusts which are broadly diversified are

lower risk than those who are narrowly focused. For example, a fund that invests in the global

bond market is lower risk than a fund that invests the Asian equities market. For a risk averse

investor like a retiree, the financial consultant will need to advise clearly on the risk of the

fund, before sinking in the investment.

9.6 Real Estate Investments

Real estate investment offers income streams, capital growth and acts as a hedge against

inflation. The income stream may come from rental income or reverse mortgage (see Section

8.1 of this Chapter). However, this type of investment is illiquid and may have to be sold at a

loss if there is an urgent need for cash. Furthermore, buying a property usually involves a

large amount of funds, as well long-term commitment, which a retiree may not have.

9.6.1 Real Estate Investment Trust (REIT)

For a real estate investment that is more liquid and requires less outlay, a Real Estate

Investment Trust (REIT) may be the solution. A REIT is a specialised form of investment

trust. It is an investment vehicle, where the funds of individual investors are pooled together,

to invest in real estate or real estate mortgages.

In many respects, a REIT is similar to any unit trust in providing the benefits of

diversification, professional management, affordability and liquidity. Yet, a REIT can be

different from a typical Unit Trust in the ways as described below.

It requires a wider range of specialists to manage. A REIT manager has to be more hands-

on, as he is involved in the actual running and operation of the properties that he buys into.

The market value of REIT is determined by the demand and supply of its shares on the stock

exchange. Unit Trust, on the other hand, trades at its net asset value and is not listed on a

stock exchange. However, the underlying listed shares of the Unit Trust are determined by

the demand and supply of its shares on the stock exchange.

Copyright reserved by Singapore College of Insurance Page 23 of 32

A REIT is regulated to distribute a substantial portion of the surplus to the investors. This

surplus is determined after deducting the income generated from its underlying properties,

with all relevant expenses necessary to maintain the properties.

There are different types of REITs. It can be sector-specific, e.g. it is only invested in office

properties or industrial buildings. Alternatively, it can be a hybrid with investments in

different sectors of property, such as offices, retail and industrial warehouses. REITs are long-

term investments, subject to the ups and downs of the property cycle. For a retiree looking for

a steady stream of income, REIT is a necessary consideration for his investment portfolio.

9.7 Structured Products

Much has been talked about Structured Products in recent years. We had all heard about the

client who went to the bank to renew his fixed deposit, but instead invested in a Structured

Deposit at the behest of a financial consultant, without fully understanding the risks involved.

In September 2008, with the filing of Chapter 11 bankruptcy protection by Lehman Brothers,

many investors were also left with worthless investments of mortgage-backed Structured

Notes. Some Structured Notes were even sold on the premise of “Capital Protected”, but the

investors still lost a substantial amount of their capital outlay. Let us now examine what

Structured Deposits and Structured Notes are.

9.7.1 Structured Deposits5

A Structured Deposit is essentially a combination of a deposit and an investment product,

where the return is dependent on the performance of some underlying financial instruments.

Typical financial instruments linked to such deposits include market indices, equities, interest

rates, fixed-income instruments, foreign exchange, mortgage-backed securities, collateral-

debt obligations, or a combination of these.

Structured Deposits have some important characteristics that distinguish them from traditional

deposits. In the case of fixed deposits, the returns and maturity periods are fixed. Structured

Deposits, on the other hand, have variable returns, and in some cases, variable maturities as

well.

Variable returns: Structured Deposits generally provide the possibility of higher returns

compared to fixed deposits. However, the investor should balance this possibility of higher

returns against the risk of variable returns. In some scenarios, the investor may get lower or

no returns at all.

Variable maturities: Structured Deposits have maturity periods that vary from as short as

two weeks to as long as 10 years. This means that the investor may not be able to use his

money for other purposes before maturity. Some Structured Deposits include an agreement

that enables the bank to redeem or "call" the deposit, before the maturity date for reasons as

specified in the terms and conditions of the contract. Where a Structured Deposit is callable,

an investor can expect to receive, at a minimum, the full value of the principal sum.

When conducting retirement planning for your client, it is important for you to advise your

client of a Structured Deposit’s difference from a Fixed Deposit, and its limitations. No doubt,

5 Adapted from www.moneysense.gov.sg

Copyright reserved by Singapore College of Insurance Page 24 of 32

a Structured Deposit potentially offers a much higher return than a Fixed Deposit, if your

client ranks liquidity as a priority, then a Structured Deposit will not be suitable, since early

withdrawal always involves a penalty.

9.7.2 Structured Notes

According to the Securities and Futures (Offers of Investments) (Shares and Debentures)

Regulations 2005, “Structured Notes”6 means any type of debentures which are issued under a

synthetic securitisation transaction, and the investment is payable in accordance with a formula

based on one or more of the following:

(a) the performance of any type of securities, equity interest, commodity or index, or of a

basket of more than one types of securities, equity interests, commodities or indices;

(b) the credit risk or performance of any entity or a basket of entities; and / or

(c) the movement of interest rates or currency exchange rates.

“Synthetic securitisation transaction” means an arrangement involving the use of derivatives

to create exposure to assets that are not transferred to, or are otherwise a part of an asset pool

held by a single purpose vehicle.

Investopedia® has perhaps a simpler definition

7. Structured Notes refer to “debt obligation

that also contains an embedded derivative component with characteristics that adjust the

security's risk / return profile. The return performance of a structured note will track that of

the underlying debt obligation and the derivative embedded within it.” As you can see,

Structured Notes belongs to a category of investments which are extremely complex and not

easily understood. Examples of Structured Notes include Lehman Brothers packaged

Minibonds and Morgan Stanley backed Pinnacle Notes. These products have since failed

spectacularly one way or another, since Lehman filed for bankruptcy in September 2008.

As a rule of thumb, investors undergoing retirement planning should steer clear of risky and

complicated products, since they have a lower threshold of risk. Furthermore, if their

investments failed, they have lesser time to recoup their investments as compared to an

investor in his 20s or 30s. If the soon-to-retire investor wishes to invest in a Structured Note,

then it should ideally make up only 20% or less of his investment portfolio.

10. HOW TO HELP CLIENTS TO OVERCOME INADEQUATE RETIREMENT

RESOURCES

Sometimes you may encounter clients who will not be able to meet their retirement needs. In

such cases, you can help them by suggesting one of the options mentioned below, to enable

them to have a higher source of income, such that they can have a more comfortable

retirement:

reverse mortgage;

lease buyback;

right sizing;

6 For full definition, please refer to Section 2(1) of the Securities and Futures (Offers of Investments)

(Shares and Debentures) Regulations 2005. 7 http://www.investopedia.com/terms/s/structurednote.asp

Copyright reserved by Singapore College of Insurance Page 25 of 32

selling the house;

renting out of part of the house;

maintenance of parents; and

post-retirement employment.

10.1 Reverse Mortgage (RM)

Reserve Mortgage (RM) is a special type of loan that allows a property owner to use his

home, to exchange for a lump sum of cash, monthly income just like the payments of an

annuity, a line of credit or a combination of the three, without selling his home.

As the name implies, a RM operates the opposite of a mortgage. In a regular mortgage, the

homeowner borrows a large sum from a financial institution to purchase a home, and then he

pays the financial institution an amount each month as repayment of the loan. In a RM, it is

the financial institution that pays the borrower (i.e. mortgagor). The financial institution

charges an interest on the amount paid to the mortgagor. Thus, a RM is a rising-debt loan.

This is because the interest added to the principal loan balance increases significantly with

time owing to the effect of compounding.

To qualify for a RM, one must attain a certain age (at least 60 years old) and own a property.

Reverse Mortgages (RMs) have been available in Singapore since 1994, when NTUC Income

first introduced the scheme for private property owners. Shortly after, the Housing &

Development Board (HDB) relaxed its regulations in March 2006, to allow elderly HDB

home owners to take up reverse mortgages on commercial terms offered by banks and

financial institutions in Singapore. NTUC Income also launched reverse mortgages on HDB

flats.

The amount of money that one can get depends on a number of factors, namely:

the borrower’s expected life expectancy; the financial institution’s desired return of his investment; the type of property and property appreciation rates; the remaining lease on the property; expenses to be incurred by the financial institution in the transaction; and term of the payment period.

Example 9.1 gives an illustration of how a Reverse Mortgage works.

Example 9.1: How Does A Reverse Mortgage Work?

Mr Ang, a 60-year-old retiree decides to reverse mortgage his S$1 million family home.

Based on the following assumptions made:

the property appreciates by 3% a year; the loan interest rate is 5.9% per annum on a monthly rest basis; and the mortgage is set at 70% of the valuation of the home.

Copyright reserved by Singapore College of Insurance Page 26 of 32

In this case, the financial institution offers to pay Mr Ang S$1,500 per month for the next

37 years. If he wants a higher amount of payment per month, the period of payment will be

shortened.

Source: The Straits Times, 12 January 1997

Most RMs do not require any repayment of principal or interest, for as long as the mortgagor

stays in the house used in the reverse mortgage transaction. In other words, as long as the

mortgagor owns and occupies the home, he is not obliged to repay the loan. Usually, the

mortgagor repays the loan from the proceeds of selling the house. In the event of death, the

financial institution will sell the house for the estate. Any money remaining after deducting

the loan plus interests is paid to the deceased’s beneficiaries. The financial institution may

also allow the children to keep the house if they can repay the loan.

As the mortgagor retains title to his home with a RM, he is responsible for property taxes,

insurance, as well as conservancy charges and utilities charges.

10.1.1 Types of Reverse Mortgage (RM)

There are generally three types of RM arrangements, namely:

Term RM;

Split-term RM; and

Tenure RM.

In a Term RM, the mortgagor will receive monthly payments until the end of the term as

specified in the contract. At the end of the term, the mortgagor must repay the loan with

accrued interest.

In a Split-term RM, the mortgagor will also receive monthly payment until the end of the

term, but the mortgagor need not repay the loan until he sells the property or until he dies.

As for Tenure RM, the mortgagor will receive payments monthly until he sells the property or

until he dies, and the loan with interest accrued will be repaid only at that point of time.

10.1.2 Advantages Of Reverse Mortgage (RM)

There are two advantages offered by RMs as follows:

the mortgagor is able to tap into his equity with no immediate cost; and

the mortgagor is able to live a better lifestyle with the additional income.

10.2 Lease Buyback Scheme (LBS)8

The Enhanced Lease Buyback Scheme (LBS) is an additional monetisation option to help

low-income elderly households in 3-room and smaller flats, to unlock part of their

housing equity while they continue to live in their homes, and receive a lifelong income

stream to supplement their retirement income.

Under the Enhanced LBS, the elderly flat owners sell part of their flat lease to HDB and

retain a 30-year lease. Their proceeds from selling part of the flat lease will be used to top

8 Adapted from www.hdb.gov.sg/lbs

Copyright reserved by Singapore College of Insurance Page 27 of 32

up their CPF Retirement Accounts (RAs). Flat owners will use their full CPF RA savings to

purchase a CPF LIFE plan to give them a monthly income for life.

10.2.1 Restrictions of LBS

During the 30-year lease

The Enhanced LBS is intended for those who wish to age-in-place. Hence, the 30-year lease

term is non-transferable in the open market. The flat owner cannot sell his flat in the open

market or sublet the whole flat.

Premature Termination of Lease

To terminate the lease prematurely, the flat owner can:

Return the flat to HDB, and

Receive a refund for the residual lease pro-rated on a straight-line basis

The CPF LIFE plan will not be terminated and will continue to provide a lifelong

monthly income.

If the flat owner outlives the 30-year Lease

There may be cases where the flat owner outlives the 30-year lease. Such cases will be dealt

with on an individual basis, and appropriate housing arrangements will be provided to those

flat owners who are not in a position to pay for the lease extension.

No elderly flat owner will be left homeless if he / she outlives the 30-year lease of the LBS

flat.

What happens if the flat owner passes away within the 30-year lease?

The flat owner’s spouse or child who is staying in the flat will be given the option of

either staying in the flat for the balance of the 30-year lease, or returning the flat to HDB.

If the flat owner’s lease is terminated prematurely, HDB will reimburse the residual value

of the lease based on straight-line depreciation to his beneficiaries.

The unused portion of his premium9, if any, will be refunded to his CPF accounts when

he passes away. The monies will then be distributed to his nominees. If he has not made a

nomination, the monies will be distributed to his family members according to the

intestacy law, namely the Intestate Succession Act (Cap. 146).

More information about the Enhanced LBS can be found at the HDB Website at:

www.hdb.gov.sg

10.3 Right Sizing

Right Sizing is an option available to all elderly Singaporeans, whether rich or poor, as long

as they own a housing unit. Under this option, the homeowner sells the housing unit that he

owns and buys one that is smaller. For example, an elderly couple living on their own in a

9 The unused portion of the premium is the annuity premium less annuity payouts that he has received

thus far. For example, if the annuity premium is S$50,000 and he has received S$250 monthly for a

total of 10 months, the unused portion of the premium is S$47,500.

Copyright reserved by Singapore College of Insurance Page 28 of 32

HDB 5-room flat may sell it and buy a HDB 3-room flat. The sales proceeds can be used as a

supplement income for their retirement. They can use the sales proceeds to invest in

investment instruments, such as trust fund, buy an annuity policy, or simply leave it with a

bank.

10.3.1 Silver Housing Bonus

The Silver Housing Bonus (SHB) is introduced to help lower-income elderly household

supplement their retirement income when they right-size their flat.

If the home owner buys a smaller flat type (up to 3-room flat) or Studio Apartment (SA), he

can apply for the SHB and receive up to S$20,000 cash bonus per household by using some

of his net sale proceeds to top up his CPF Retirement Account (RA) and join the CPF LIFE

Scheme.

More information about the SHB can be found at the HDB Website at: www.hdb.gov.sg

10.4 Selling The Flat

If the flat owner has children living on their own, he has the choice of selling his flat

outright to live with his children. However, this may not be a prudent decision because the

flat owner does not have the capacity to manage a large sum of cash, or he cannot get

along with his children living in the same flat. In the worst case scenario, the flat owner will

be homeless if his children do not accept him.

10.5 Renting Out Part Of The Flat

Renting out part of the flat is not only a good way to supplement one’s retirement income, but

also to let the homeowner keep the title to the flat. Under this option, the homeowner lets out

the spare rooms in the flat in return for a monthly rental income. However, this option has

drawbacks, such as finding a good tenant. Besides, the tenant may delay the rental payment

giving rise to credit risk.

10.6 Maintenance Of Parents

This option is available only to elderly Singaporeans who have children. The Maintenance of

Parents Act (Cap. 167B) was passed by the House of Parliament on 2 November 1995, to help

elderly parents to settle their maintenance claims from their children. Under this Act, parents

who cannot support themselves are entitled to claim maintenance from their children, but it

does not entitle them to a share of their children’s wealth.

10.7 Post-retirement Employment

Working after retirement will provide the retiree with extra cash. You can advise your client

to work on a part-time or full-time basis. He can also work as a consultant or even start a

business. However, the latter may pose some risk because, if his business is not making

money, it may even “eat into” what he has managed to set aside for his retirement. To

encourage the elderly to continue working in their retirement years, the Government came up

with a Workfare programme to reward these low-wage, productive elderly citizens.

Copyright reserved by Singapore College of Insurance Page 29 of 32

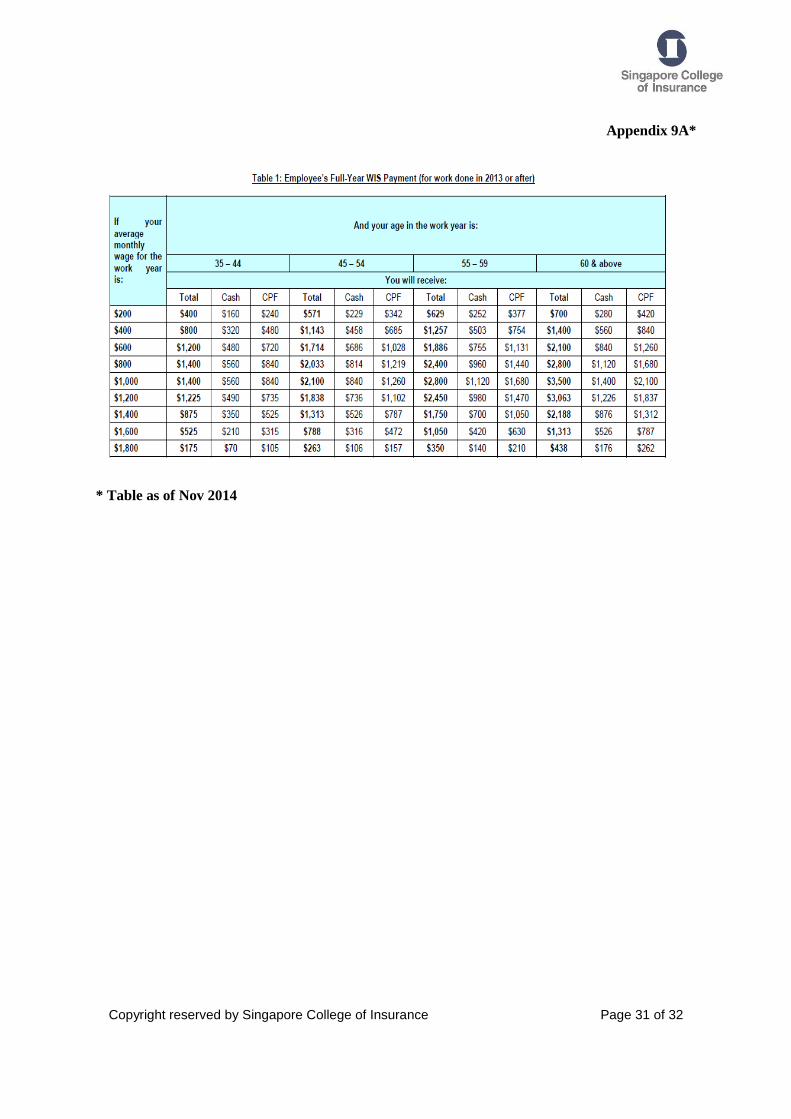

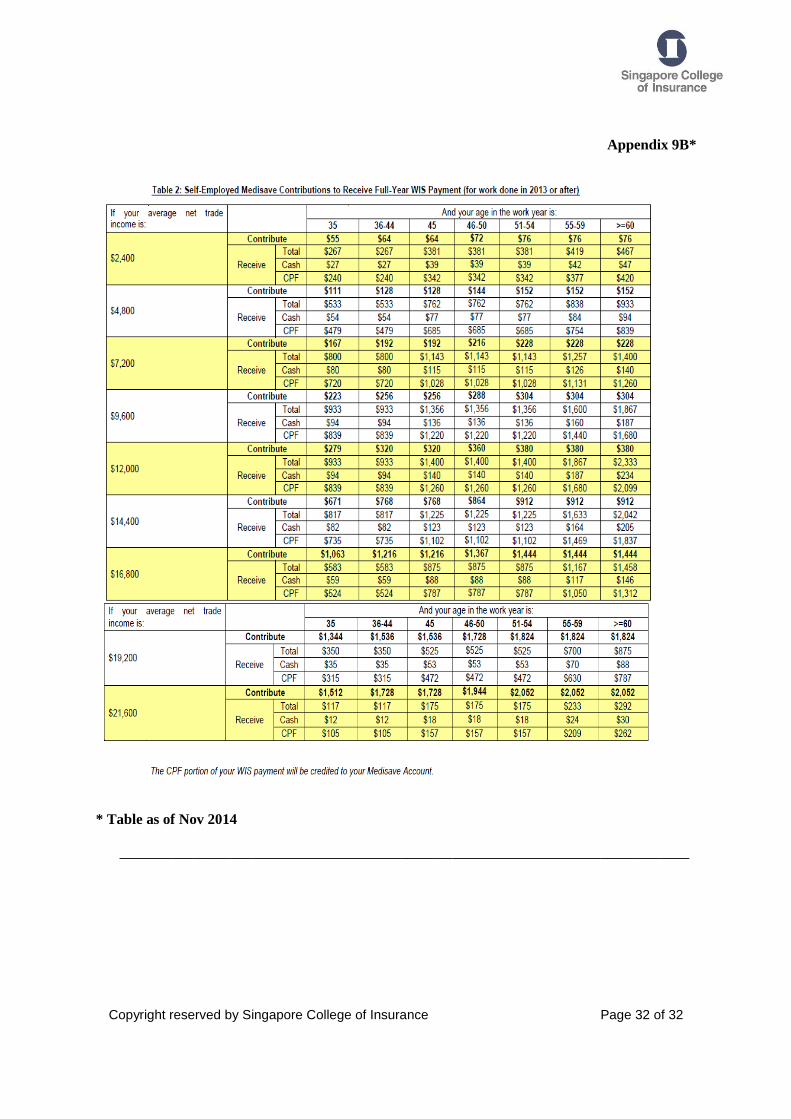

10.7.1 Earnings & Workfare

The Workfare Income Supplement (WIS) Scheme was announced during the 2007 Budget

Speech as a permanent scheme following the one-off Workfare Bonus Scheme. The

objectives of WIS are to supplement the wages and retirement savings of older low-wage

workers, as well as to encourage them to stay employed.

Most retirees who may be working on an informal or casual basis will reap the benefits of

Workfare if they meet the qualifying criteria. For more information on Workfare, do refer to:

www.workfare.sg

If your client is self-employed or informally employed, he will need to declare his income to

the CPF Board or Inland Revenue Authority of Singapore (IRAS) and contribute to his

Medisave Account, in order to qualify for Workfare. All qualifying members will need to

fully pay up their Medisave liability, before Workfare can be allotted.

The schedule of contribution rates for both employees and self-employed can be found in

Appendices 9A and 9B respectively.

11. CASE STUDY – HOW MR TAN CAN OVERCOME INADEQUATE

RETIREMENT RESOURCES

During the 2014 National Day Rally Speech, Prime Minister Lee Hsien Loong took on the

role of a “financial planner” to a hypothetical Tan family, advising on how the family can

overcome inadequate retirement resources.

Profile of Mr. Tan

Mr. Tan is 54-plus years who is a senior technician and earns S$4,500 per month. His

wife, Mrs Tan, is a house wife and is about the same age. They have two kids, the son has

finished NS (National Service) and is going to university, while the daughter is still in

school. The family is currently living in a four-room flat in Ang Mo Kio. The flat is fully

paid-up and is worth the value of S$450,000.

For Mr. Tan to retire with S$2,000 per month from the age of 65 years for the rest of his life,

he needs at least S$250,000 now (inclusive of CPF) when he is 55 years old. For Mr. Tan to

meet his retirement shortfall, the proposed solutions as discussed are appended below.

No. Proposed Solution to Overcome

Inadequate Retirement Resources

Remarks

1. He continues working for an income. The government plans to raise the re-

employment age beyond 65 years.

2. He asks the children to support the

parents when they start working.

3. He draws on his personal savings.

Copyright reserved by Singapore College of Insurance Page 30 of 32

4. He monetises his flat by renting the

flat out.

S$700 per month for renting one

room

S$2,500 per month for renting

the whole flat

5. He monetises his flat by right-sizing

to a studio apartment.

With the Silver Housing Bonus of

S$20,000 from the government, he

gets a total of S$210,000 plus S$800

per month.

6. He monetises his flat by selling his

flat.

He may end up homeless if he stays

with his children and cannot get

along with them.

7. He monetises his flat by taking up

the Lease Buyback Scheme.

It will be applicable to 4-room flats

from 1 April 2015 onwards.

Copyright reserved by Singapore College of Insurance Page 31 of 32

Appendix 9A*

* Table as of Nov 2014

Copyright reserved by Singapore College of Insurance Page 32 of 32

Appendix 9B*

* Table as of Nov 2014

_____________________________________________________________________________