erin bartholomy lynda given todd krzyskowski sean mccarthy partner partner managing director first...

TRANSCRIPT

Erin Bartholomy Lynda Given Todd Krzyskowski Sean McCarthy Partner Partner Managing Director First Vice PresidentChapman and Cutler LLP Chapman and Cutler LLP Mesirow Financial Stifel, Nicolaus & Company, Inc.

May 20, 2010

Maximizing the Benefits of the Evolving American Reinvestment and Recovery Act of 2009

2

The Obama Administration’s $787 Billion Economic Stimulus Package, known as the American Recovery and Reinvestment Act, was signed into

Law on February 17, 2009 – Municipal Highlights

Eliminates AMT on Bonds Issued in 2009 and 2010

Introduces Taxable Bond Financing

Options for Tax-Exempt Issuers

Energy Infrastructure Bonds (QECBs)

(Capped Issuance)

Liberalizes Investment Rules for Financial Institutions

Qualified Zone Academy Bonds

(QZABs)(Capped Issuance)

Increases Annual “Bank Qualified” Bond Limit to $30 Million for 2009-10

The primary purpose of the Recovery Act is to Prompt Immediate Capital Formation Efforts by State & Local Governments using expanded TAXABLE borrowing alternatives to stimulate the economy and put people back to work……

Build America Bonds (BABs)

(Uncapped Issuance)

Qualified School Construction Bonds

(QSCBs)(Capped Issuance)

Recovery Zone Facility Bonds

(RZFBs)

33

The Stimulus Plan Provides State & Local Governments Including School Districts the Opportunity to Capture All of the Federal Subsidy that Was

Traditionally Shared with Tax Exempt Investors

Note: While State & Local Governments can benefit, the financing alternatives were geared to be REVENUE NEUTRAL to the U.S. Treasury, but actual impact has been more costly

Tax-Exempt Investors

State, School District, and Other Local Governments

State, School District, and Other Local

Governments

Includes:

Build America Bonds Energy Conservation Bonds Qualified School Construction Bonds Qualified Zone Academy Bonds Expanded “Bank Qualified” Bonds

Allocation of Federal Subsidies - Traditional Tax-Exempt

Allocation of Federal Subsidies - New Taxable Alternatives

4

The Borrowing Alternatives Provided by the Stimulus Plan are All TAXABLE and Must be Compared to Traditional Tax-Exempt

Alternatives – At the Margin Taxable Bonds are the base level of borrowing cost for issuers

Various borrowing options provide an approximate subsidy in the current market defined as a percentage of taxable bonds

* Treasury guidance and allocation still to be published on Recovery Zone BABs

100%

80%

65%75%

55% 55%60%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

TaxableBonds

Tax-ExemptBonds

BABsInvestor

Tax CreditSubsidy

BABs IssuerSubsidy

QECBs70%Tax

CreditSubsidy

QSCB 100%Tax Credit

Subsidy

RecoveryZone BABs

IssuerSubsidy*

Per

cent

age

of T

axab

le B

onds Subsidy Above Traditional Tax-Exempt Bonds

55

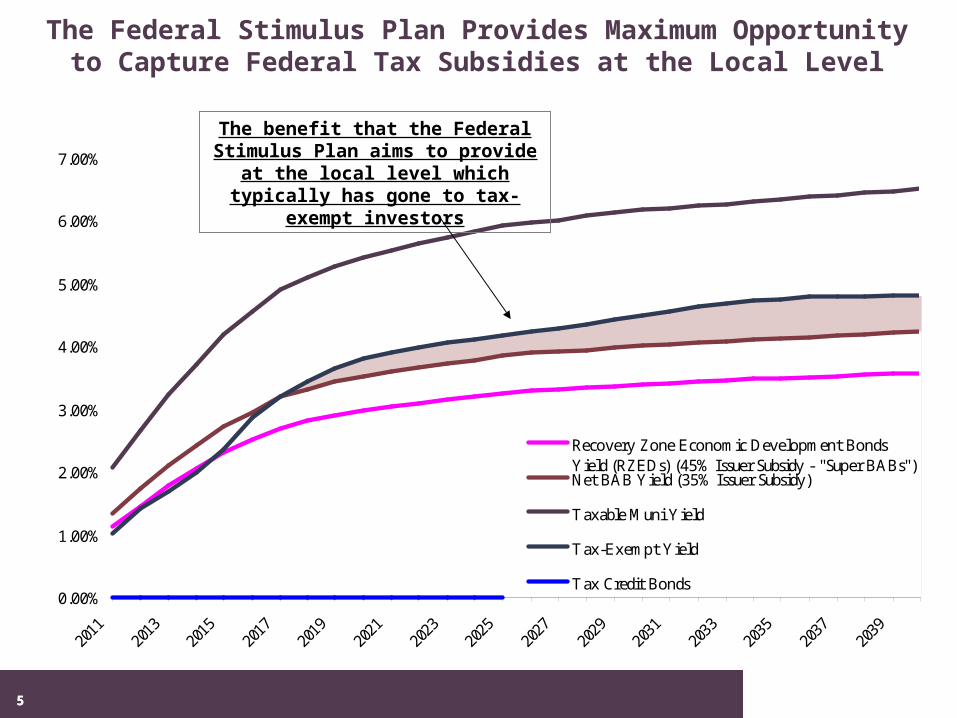

The Federal Stimulus Plan Provides Maximum Opportunity to Capture Federal Tax Subsidies at the Local Level

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

Recovery Zone Economic Development BondsYield (RZEDs) (45% Issuer Subsidy - "Super BABs")Net BAB Yield (35% Issuer Subsidy)

Taxable Muni Yield

Tax-Exempt Yield

Tax Credit Bonds

The benefit that the Federal Stimulus Plan aims to provide at the local level

which typically has gone to tax-exempt investors

66

The Illinois State Toll Highway Authority is Estimated to Have Saved Over $60,000,000 in Interest Costs Through the Use of BABs

Issuers with solid credit ratings should expect the same percentage level of savings versus traditional tax-exempt bonds subject to market conditions at the time of financing

BAB 65% Net Tax-Exempt Yield Est. BAB Est. BABMaturity Amortization Yields BAB Yield Yield* Benefit Savings % Savings $

01/01/19 21,940,000 5.293% 3.440% 3.550% 0.110% 0.89% 190,000$

01/01/20 18,460,000 5.293% 3.440% 3.750% 0.310% 2.69% 500,000$

01/01/21 15,105,000 5.293% 3.440% 3.890% 0.450% 4.17% 630,000$

01/01/22 16,975,000 5.293% 3.440% 4.020% 0.580% 5.69% 970,000$

01/01/23 13,830,000 5.293% 3.440% 4.150% 0.710% 7.32% 1,010,000$

01/01/24 13,690,000 5.293% 3.440% 4.280% 0.840% 9.05% 1,240,000$

01/01/32 67,230,000 6.184% 4.020% 4.990% 0.970% 13.07% 8,780,000$

01/01/33 70,105,000 6.184% 4.020% 5.020% 1.000% 13.75% 9,640,000$

01/01/34 262,665,000 6.184% 4.020% 5.050% 1.030% 14.42% 37,880,000$

500,000,000$ 12.17% 60,840,000$ * - Estimated Trading Spread of 65 Basis Points Over AAA MMD . Subject to change based upon market conditions.

Interest Rate Comparison BAB Benefit

The Illinois State Toll Highway Authority, Taxable Build America Bonds (BABs)Sold on May 12, 2009 - Interest Rate Comparison

7

The Stimulus Plan Sunsets on December 31, 2010 So Planning Must Begin Now – Especially if You Need to Pass a Referendum!

2/17/2009

American Recovery and Reinvestment Act is signed into law

12/31/2010

Current expiration of BAB financing opportunities

Increase to $30 million Bank-Qualified Capacity for

2009

Increase to $30 million Bank-Qualified

Capacity for 2010

12/31/2009

February 2, 2010 Primary Election for Referendum Ballot Question November 2, 2010

General Election for Referendum Ballot Question

March 18, 2010 - HIRE Act signed into law, extending BABs for 3 years

12/01/2013?

Proposed extension of ARRA including BABs subsidy (at a

reduced level)

88

What are my capital financing needs/plans? Timeframe?

What is my current debt capacity?

What type of governmental unit am I?

-Home Rule vs. Non-Home Rule

-Tax-Capped vs. Non-Capped

Do I need to pass a referendum? Can the Stimulus Plan Help that Appeal?

Am I in touch with my State Representative on Tax Credit Bond Sponsorship?

-Will State Statute Change to Assist local issuers (e.g. longer maturities)?

What is my current debt structure?

-Upward Sloping, Downward Sloping, or Level

What tax rate impact can be achieved?

-Intergovernmental cooperation

Develop Your Thoughts and Engage Your Governing Body and Community; Next Steps & Key Questions to Think About

9

Forward Starting Swap Mechanics

Cash Flows for Taxable Build America Bonds and Their Accompanying Subsidy

Federal Treasury

Issuer Subsidy BABs

Bondholders

Direct Payment of 35% of Interest Paid

Federal Treasury

Investor Subsidy BABs

Bondholders

&

Tax Credit Holders

Tax Credit Equal to 35% of Interest Received

Taxable Fixed Interest Rate

Taxable Fixed Interest Rate

Traditional Fixed Rate Bonds

Bondholders

Tax-Exempt Fixed Interest Rate

Local Issuer

Local Issuer

Local Issuer

1010

Tax-Exempt Interest Rates Have Historically Carried Yields Lower than Their Taxable Counterparts

– The 30-Year US Treasury is a taxable interest rate and the 30-Year MMD is a tax-exempt interest rate for AAA rated issuers

Taxable and Tax-Exempt Interest Rates Over the Past 20 Years

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

30-Year Treasury 30-Year MMD

The Federal Stimulus was enacted when taxable interest rates were significantly below tax-exempt interest rates to eliminate the great benefit experienced by tax-exempt bond investors at the expense of issuers

11

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.020

09

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

Mill

ions

Outstanding City of Peoria GO Debt Service Theoretical BABs Debt Service Theoretical Additional Debt Issuance Capacity

Intergovernmental Communication and Good Debt Management Are Keys to Managing Overall Taxpayer Tax Rate Impact

Theoretical $10 million BAB Debt Service for a Sample Issuer and Additional Debt Issuance Capacity

A downward sloping debt profile coupled with minimal debt allows

an issuer to issue long-term debt and maximize the benefit from the

temporary Federal Stimulus with minimal tax rate impact

Note – Additional Debt Issuance Capacity includes principal and interest; assumes maximum annual debt service of $17.5 million, based upon largest annual outstanding Sample Issuer GO Debt Service plus theoretical $10 million BAB debt service

12

Debt issuance authority must be established

The importance of Capital projects

Borrowing Options

• School Building Bonds

• Alternate Bonds

• Life Safety Bonds

• Working Cash Fund Bonds

• Debt Certificates

• Funding Bonds

ARRA and Illinois Law

122808242

13

Who is Using BABs

1,066 BABs transactions worth over $90 billion were priced from April 2009 to March 31, 2010

It is estimated that state and local governments will save approx. $12 billion in present value borrowing costs by using BABs compared to issuing solely traditional tax-exempt bonds

Proceeds must be issued to finance new money capital expenditures for which tax-exempt governmental bonds could be issued

14

When to Use BABs

Decision to issue BABs should be a “game day” decision at the time of bond sale. If it is cost effective for the district to use this program at the time of sale, it should be used.

Must analyze traditional tax-exempt and taxable Build America Bond scales to advise issuer-client and determine which financing option is the most economical.

Often, a blended transaction, which incorporates both BABs and tax-exempt bonds provides for the most economical financing solution.

15

Tax-Exempt vs. Taxable BABs Yields

Traditional Tax-exempt Bonds vs. Taxable BABs

Tax-Exempt vs. Taxable BABs Yield Curves

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028

Maturity

Yie

ld

Tax-exempt Yields Taxable Yields Taxable Yields Post 35% Subsidy

Crossover - BABs become more cost-effective

Taxable and tax-exempt yield curves are analyzed to determine to appropriate blend

16

Case Study: Jefferson County, Colorado

Jefferson County, Colorado

Certificates of Participation, Series 2009

Marketing Date: 10/20/2009

Credit ratings: Aa2/AA

Sold as 1 transaction with 2 separate series: Series A: $67,715,000 taxable COPs (Direct Pay

Build America Bonds) Series B: $8,765,000 tax-exempt COPs

Issuer saved nearly $4.5 million by issuing a combination of tax-exempt COPs and taxable direct pay Build America Bond COPs, rather than a tax-exempt only transaction

17

Maturity Schedule: Jefferson County COPs, Series 2010

Tax-Exempt

Taxable

Bond ComponentMaturity

DateAmount Rate Yield Price

Premium (-Discount)

12/1/2010 2,745,000 2.000% 0.900% 101.170 32,116.5012/1/2011 2,980,000 2.000% 1.250% 101.529 45,564.2012/1/2012 3,040,000 2.500% 1.650% 102.535 77,064.00

8,765,000 154,744.70

12/1/2013 3,115,000 3.100% 3.100% 100.00012/1/2014 3,180,000 3.300% 3.300% 100.00012/1/2015 3,250,000 3.750% 3.750% 100.00012/1/2016 3,325,000 4.200% 4.200% 100.00012/1/2017 3,420,000 4.350% 4.350% 100.00012/1/2018 3,515,000 4.900% 4.900% 100.00012/1/2019 3,625,000 5.000% 5.000% 100.00012/1/2020 3,745,000 5.150% 5.150% 100.00012/1/2021 3,870,000 5.350% 5.350% 100.00012/1/2022 4,005,000 5.500% 5.500%

35,050,000

12/1/2025 12,925,000 5.900% 5.900% 100.000

12/1/2029 19,740,000 6.250% 6.250% 100.000

76,480,000 154,744.70

Serial Bonds:

Term Bond Due 2025:

Term Bond Due 2029:

BAB Serial Bonds:

18

Net Debt Service: Jefferson County

Period Ending Principal Interest

Total Debt Service

35% Interest Subsidy

Net Debt Service

12/1/2010 2,745,000.00 4,044,741.21 6,789,741.21 -1,344,169.00 5,445,572.2112/1/2011 2,980,000.00 3,717,397.50 6,697,397.50 -1,253,629.12 5,443,768.3812/1/2012 3,040,000.00 3,657,797.50 6,697,797.50 -1,253,629.12 5,444,168.3812/1/2013 3,115,000.00 3,581,797.50 6,696,797.50 -1,253,629.12 5,443,168.3812/1/2014 3,180,000.00 3,485,232.50 6,665,232.50 -1,219,831.38 5,445,401.1212/1/2015 3,250,000.00 3,380,292.50 6,630,292.50 -1,183,102.38 5,447,190.1212/1/2016 3,325,000.00 3,258,417.50 6,583,417.50 -1,140,446.12 5,442,971.3812/1/2017 3,420,000.00 3,118,767.50 6,538,767.50 -1,091,568.62 5,447,198.8812/1/2018 3,515,000.00 2,969,997.50 6,484,997.50 -1,039,499.12 5,445,498.3812/1/2019 3,625,000.00 2,797,762.50 6,422,762.50 -979,216.88 5,443,545.6212/1/2020 3,745,000.00 2,616,512.50 6,361,512.50 -915,779.38 5,445,733.1212/1/2021 3,870,000.00 2,423,645.00 6,293,645.00 -848,275.76 5,445,369.2412/1/2022 4,005,000.00 2,216,600.00 6,221,600.00 -775,810.00 5,445,790.0012/1/2023 4,150,000.00 1,996,325.00 6,146,325.00 -698,713.76 5,447,611.2412/1/2024 4,305,000.00 1,751,475.00 6,056,475.00 -613,016.26 5,443,458.7412/1/2025 4,470,000.00 1,497,480.00 5,967,480.00 -524,118.00 5,443,362.0012/1/2026 4,645,000.00 1,233,750.00 5,878,750.00 -431,812.50 5,446,937.5012/1/2027 4,830,000.00 943,437.50 5,773,437.50 -330,203.12 5,443,234.3812/1/2028 5,030,000.00 641,562.50 5,671,562.50 -224,546.88 5,447,015.6212/1/2029 5,235,000.00 327,187.50 5,562,187.50 -114,515.62 5,447,671.88

76,480,000.00 49,660,178.71 126,140,178.71 -17,235,512.14 108,904,666.57

19

Is it Worth It?Often, BABs have provided larger savings for larger issuers.

20

BABs ChallengesExtraordinary/make-whole calls are relatively expensive and

render the debt economically non-callable

Deals are managed off the taxable desk, yet subject to MSRB rules

After-market premium inherent in the taxable market

Deal features are currently evolving

Long-term risks due to potential changes in governmental policy, etc.

21

Need Qualified Zone Academy

100 Percent Test/Qualified Purpose/2 Percent COI

Expenditure Rules

Private Business Contribution

Certain Wage and Labor Standards Applicable

Bonds may either be traditional “tax credit” QZABs or “direct pay” QZABs

Qualified Zone Academy Bonds

21

22

Supervision of an Eligible Local Education Agency (ISBE)

Application made to ISBE, ISBE grants allocation to individual Districts

Illinois allocation in 2009 $52,401,000, in 2010 $52,218,000

Designate a building or buildings as a qualified zone academy

Each academy must have 35% of students qualify for free or reduced priced lunch

10% Private Business Contribution Requirement

Qualified Zone Academy

22

23

Rehab/Repair Public School Facility(Regulations Define Rehab) – Not New

Construction

Equipment

Development of Course Materials

Training Teachers/School Personnel

Qualified Purpose of Bond Proceeds

23

24

100 Percent of Available Project Proceeds (“APP”) used for Qualified Purpose

APP=Par amount of Bonds less 2% permissible to pay costs of issuance

In General, Proceeds Must Be Spent Within Three Years

Binding Commitment to Spend At Least Ten Percent of Proceeds Within Six Months

Spend Proceeds With Due Diligence

Redeem Bonds with unspent proceeds after 3 years

Expenditure Rules

24

25

Public/Private Partnership

Written Commitment from Private Entities

Contribution Must Have PV of at Least Ten Percent of Proceeds of Issue

Must Be a “Qualified Contribution”

Private Business Contribution

25

26

Equipment

Technical Assistance to Develop Curriculum or Train Teachers to Promote “Market Driven” Technology in Classroom

Employee Services as Mentors

Internships/Field Trips, Etc.

Any Other Property or Service …

Qualified Contribution

26

27

Wage rate requirements and labor standards requirements under Subchapter IV of Chapter 31 of Title 40 of the United States Code apply to projects financed with proceeds of QZABs (Federal “Prevailing Wage”)

Certain Wage and Labor Standards Applicable

27

28

Owners receive a federal tax credit instead of interest

Tax credit received on quarterly credit allowance dates

May be supplemental coupon also

Tax credit rate and maximum term published at www.treasurydirect.gov

Can carry forward unused portion of Tax Credit

May create a sinking fund invested at the published permitted sinking fund yield

Tax Credit QZABs

28

29

Issuer receives direct payment from federal government

Payment is lower of actual interest or tax credit rate

De Minimus Premium Rules Apply

Must File Form 8038-CP

Maximum term published by Treasury

Current terms 17 year maturity 5.51% interest/tax credit rate

Direct Pay QZAB

29

30

All of the rules applicable to tax-exempt bonds must be complied with Spending requirements

Arbitrage rebate

Private use and payment tests

Rules Applicable to Build America Bonds

30

31

Irrevocable election to treat the debt as BABs

2% Cost of issuance limitation

Includes bond insurance premium

Issue some bonds as taxable non-BABs

No more than a de minimis original issue premium allowed

Based on the definition of “issue price” based on reasonable expectations

First interest payment must be within one year of the date of issuance

Rules Applicable to Build America Bonds (cont’d.)

31

32

Capitalized interest

Up to placed-in-service date of the financed project(s)

Complications with multiple projects and multiple placed-in-service dates

No CABs

Count against “small issuer” exception for rebate but NOT against the $30,000,000 annual BQ limit

Can be used for reimbursement

Can be used to refinance temporary short-term financings

Rules Applicable to Build America Bonds (cont’d.)

32

33

Form 8038-B

Bond counsel files on the closing date

Includes a debt service schedule

Form 8038-CPMust be filed not less than 45 and not more than 90 days before

each interest payment date

The first 8038-CP should be filed no earlier than 30 days after the 8038-B is filed

IRS Forms; Filings

33

34

Expect to receive an IRS Questionnaire

Respond promptly!

Post-Issuance Compliance

34

35

A Build America Bond that the issuer designates as a Recovery Zone Economic Development Bond

National limit of $10,000,000,000

Allocation formula to each Illinois county

Issuer receives payment equal to 45% of interest paid on bonds paid directly by the U.S. Treasury (rather than 35%)

Proceeds must be used for one or more qualified economic development purposes in a recovery zone

Taxable Recovery Zone EconomicDevelopment Bonds

35

36

“Qualified economic development purpose” means expenditures for purposes of promoting development or other economic activity in a recovery zone, including: Capital expenditures with respect to property located in the zone

Expenditures for public infrastructure and construction of public facilities

Expenditures for job training and educational programs

Wage rate requirements and labor standards requirements under Subchapter IV of Chapter 31 of Title 40 of the United States Code apply

Taxable Recovery Zone EconomicDevelopment Bonds (cont’d)

36

37

Effects of the Proposed “Hiring Incentives to Restore Employment Act (HIRE)”

Proposed HIRE extends BAB program and direct-pay subsidy for three years Most likely that the Issuer subsidy will be reduced (25%-30%)

BABs program becoming model for other Federal programs

QSCB program restructured to provide direct-pay subsidy

Old QSCB program resulted in only $2.6 billion in issuance last year (out of $11 billion authorized)

Expectation of increased issuance due to new direct-pay subsidy feature

Issuers receive payments equal to the lesser of the actual interest rate of the bonds or the tax-credit rate for municipal tax-credit bonds 5.86% rate for a 17 year maturity (as of April 8th) Mesirow Financial estimates the State would price at 5.41% for a 17 year maturity

Important to consider timing: Tax credit yield is determined at closing rather than pricing

37

38

Questions?

39

Thank You!